Whither India’s pilots?

Easy to learn, hard to master, harder yet to be captain

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

A scramble for pilots?

Coal India’s Brain Goes Public

A scramble for pilots?

Does India have enough pilots for its commercial airlines?

Headlines from the sector make things seem dire. In recent years, airlines have announced salary hikes of as much as 40% for their pilots. Just a few days ago, in fact, Akasa announced a generous incentive program to retain its pilots, amid poaching fears. The sector has been fending off pressure from Gulf and Southeast Asian carriers — a trend Indigo’s former CEO called “disturbing”. India even formally submitted a working paper to the International Civil Aviation Organisation last year, asking for the world’s help in stopping international airlines from getting their hands on our pilots.

Meanwhile, India’s own airlines have been luring from abroad. Last year, for instance, a Rajya Sabha reply noted that in the course of a single year, the number of foreign pilots with temporary authorisations to fly in India tripled.

It almost seems as though we’re desperately short of pilots.

In 2024, the Directorate General for Civil Aviation (DGCA), India’s aviation regulator, issued a record 1,628 commercial pilot licences. It was the most they had ever issued, to that point, by a comfortable margin. This was, in part, because more pilots were entering the workforce than ever before. India now has forty flight training organisations, spread across sixty-two bases, a leap from thirty-four schools just three years ago. Many of those pilots don’t have a clear path to joining India’s commercial aviation sector.

In this telling, the government seems to make sense when it says: there is no shortage of pilots in India.

Somehow, both these things are true. India is not short of pilots. Yet, India is short of very specific kinds of pilots.

The squeeze

Two years ago, the DGCA published revised flight duty time limitations — or ‘FDTL’. These are the rules that govern how much a pilot can fly, how long they can be kept on duty, and how much rest they must get between flights. With this, there was a visible drop in the amount of work any airline could ask their pilots to do.

To this point, India’s rules had been looser than global norms. That was dangerous; if there was one profession where you could not afford for someone to be fatigued and sleepy because of too many night shifts, it is pilots. The revision brought them closer to international standards.

With these new norms, the load on India’s pilots would have to decrease. They would have to be given much more weekly rest — 48 hours, instead of 36. That was, effectively, one less flying day in a week. They could only be asked to land at night twice a week, instead of the previous six, and the definition of “night” was tightened. And some loopholes were tightened: for instance, the ‘standby’ time as pilots waited for their next flight would be cut into their flyable hours.

This was a big transition for any airline: they would need a complete overhaul in how they managed their personnel. And so, airlines were given roughly twenty months to fall in line.

We don’t have to tell you how that turned out.

For now, though, we aren’t interested in a single failure, but for what these rules meant to the wider market for pilots.

This marked a big change to the baseline of what any pilot could be expected to do. If each pilot now has fewer hours to fly, you would need more to fly the same schedule. According to the Federation of Indian Airlines, the new framework meant that the same pilot would fly between 10 and 20% fewer flights. Many airlines felt the need to increase their pilot strength by as much as a quarter.

Since this was happening across the industry, the demand for pilots leapt up all at once.

Now, did the new norms put the market under pressure?

It isn’t clear why, on the surface. India’s six major domestic airlines together employ around 11,400 pilots. These new norms would add, at most, a few thousand additional pilots to the mix. Meanwhile, there are over 26,000 licensed commercial pilots in India. More than 1,600 new ones pass through the trailing pipeline every year. On paper, this looks manageable.

The trouble, however, is that a “pilot” isn’t one thing. There’s a massive difference between someone being a licensed pilot, and someone who would actually pilot your next flight.

The funnel

To become a “commercial pilot”, you need a commercial pilot licence, or a ‘CPL’.

You get this somewhere after one-and-a-half to two years of training, once you’ve flown for about two hundred hours, and spent more than half a crore in fees. India hands out roughly 1,600 of these licenses a year.

But this is only the first gate in the system. A CPL holder is not an airline pilot, much like you wouldn’t give your car to just anyone with a driving license.

To actually fly passengers on, say, an Airbus A320 — the aircraft that makes up the bulk of India’s fleet — you need a “type rating”, which effectively means you’re certified to fly that specific plane. This takes another couple of months of training for that aircraft. This costs the pilot anywhere up to twenty-five lakh rupees, over and above what they’ve already spent.

Naturally, nobody gives you a full-blown aircraft to fly this early. Instead, you practice on ‘Level D’ simulators — devices that actually make you feel the motion of that aircraft. Sadly, India only has a few of these, concentrated at a handful of facilities in Bangalore, Gurgaon, and Hyderabad. Finding a slot can be hard.

Even now, you aren’t ready to fly. First, you need to finish your airline induction. Step by step, you’re made to understand the airline’s processes, and are then slowly eased into flying, until the airline trusts your ability to fly passengers on your own. This takes the better part of a year. Once you’re done, you can become a first officer — that is, you earn a seat in the cockpit.

But you still cannot command a flight.

To become a captain — to be the pilot-in-command that actually gets to head a commercial flight — you legally need at least 1,500 hours of flight time. In practice, airlines require 2,500 to 3,500 hours before they’re willing to bump you up. Then, you need to pass a ‘command upgrade’ process, which includes a viva examination administered by the DGCA.

There is, unfortunately, a shortage of examiners, at the DGCA. According to some reports from last year, in fact, half the technical posts at the body are vacant.

This is part of a wider problem. The number of pilots you can put through, any year, depends on the number of older, more experienced pilots you have. These are important cogs in the machine. These pilots become training captains, and designated examiners. They have to be around for a young pilot to advance. It’s only when you have these that you can bring other pilots up the ladder.

These are the sorts of pilots Gulf carriers most aggressively recruit.

To run a plane, you don’t just need a pilot, you need a captain. India has thousands of certified pilots that are at the beginning of a long journey. From here, they have many thousands of hours of training and flying ahead of them. And at each step, they will have to deal with scarcity — money, simulators, training pilots, examiners, and more. There aren’t enough people who have completed this entire journey.

This is a funnel with a wide mouth, and a narrow neck. The width of the neck, however, depends on the number of in-demand experienced pilots you have.

What a plane actually needs

Here’s one way of thinking about how many pilots any airline needs.

A single narrowbody aircraft, like an A320 — the kind that makes up 90% of India’s fleet — flies roughly 10-12 hours every day. Each flight requires two pilots. And any one pilot can fly about 65-80 hours a month.

So, you need somewhere between ten and fourteen pilots for every aircraft. Ideally, you might want more, so that you can buffer for those that are sick or on leave. In the US, airlines typically run twelve to sixteen.

Compare that to India’s numbers. IndiGo has 7.6 pilots per aircraft. The others cluster around 9. Nobody even crosses ten.

Indigo is clearly an outlier, however. It has a massive fleet of aircraft of a single type, and as a facet of its cost discipline, constantly optimises its pilots’ schedules to fly as many flights as possible. This has made IndiGo the most profitable airline in India. But with just 7.6 pilots a plane, there is absolutely no room for error.

Consider this: between 2022 and 2024, Indigo hired 14 pilots for every plane they acquired. Air India, in contrast, hired 23. And so, when the new FDTL norms kicked into place, late in 2025, Indigo found itself almost 700 pilots short. What once looked like efficiency became the very reason they were hurt worse than the rest of the industry.

The shortage

India needs more captains. Every commercial flight legally needs a captain, so the size of our aviation industry directly depends on how many captains we have. Unfortunately, it takes years for a pilot to become a captain, which creates a fundamental speed-limit for India’s aviation industry.

Meanwhile, at least until recently, airlines from across the Gulf — like Emirates, Riyadh Air or Etihad — were looking at India for new pilots as well. With every pilot, you lose many years of experience, in an industry where experience requirements are literally coded into the law. This is why India formally petitioned ICAO for a global code of conduct, to regulate cross-border pilot recruitment. The proposal was rejected.

Of course, with the Gulf now on fire, this could change quickly. But if and when it recovers, the pull will begin again

Alongside captains, we also need more people to clear the other bottlenecks in the system, like pilots who are type rated and can be inducted into the system. And we need more of the sort of people that can staff the pipeline in between.

The arithmetic ahead

India’s airlines have currently ordered roughly 1,700 new aircraft — with IndiGo and Air India, alone, seeking around a thousand between them. The industry needs roughly 2,000 to 2,100 new pilots a year to service those planes.

Currently, India issues about 1,600 pilot licenses a year. The gap is notable, but not impossible. But the mouth of the funnel was never the problem. The problem is the narrow neck. When a system is built over decades, it can’t just scale in a few years.

India doesn’t have a pilot shortage. But it has a captain shortage, a simulator shortage, a training pilot shortage, and an examiner shortage. Unfortunately, those are what really matter.

Coal India’s Brain Goes Public

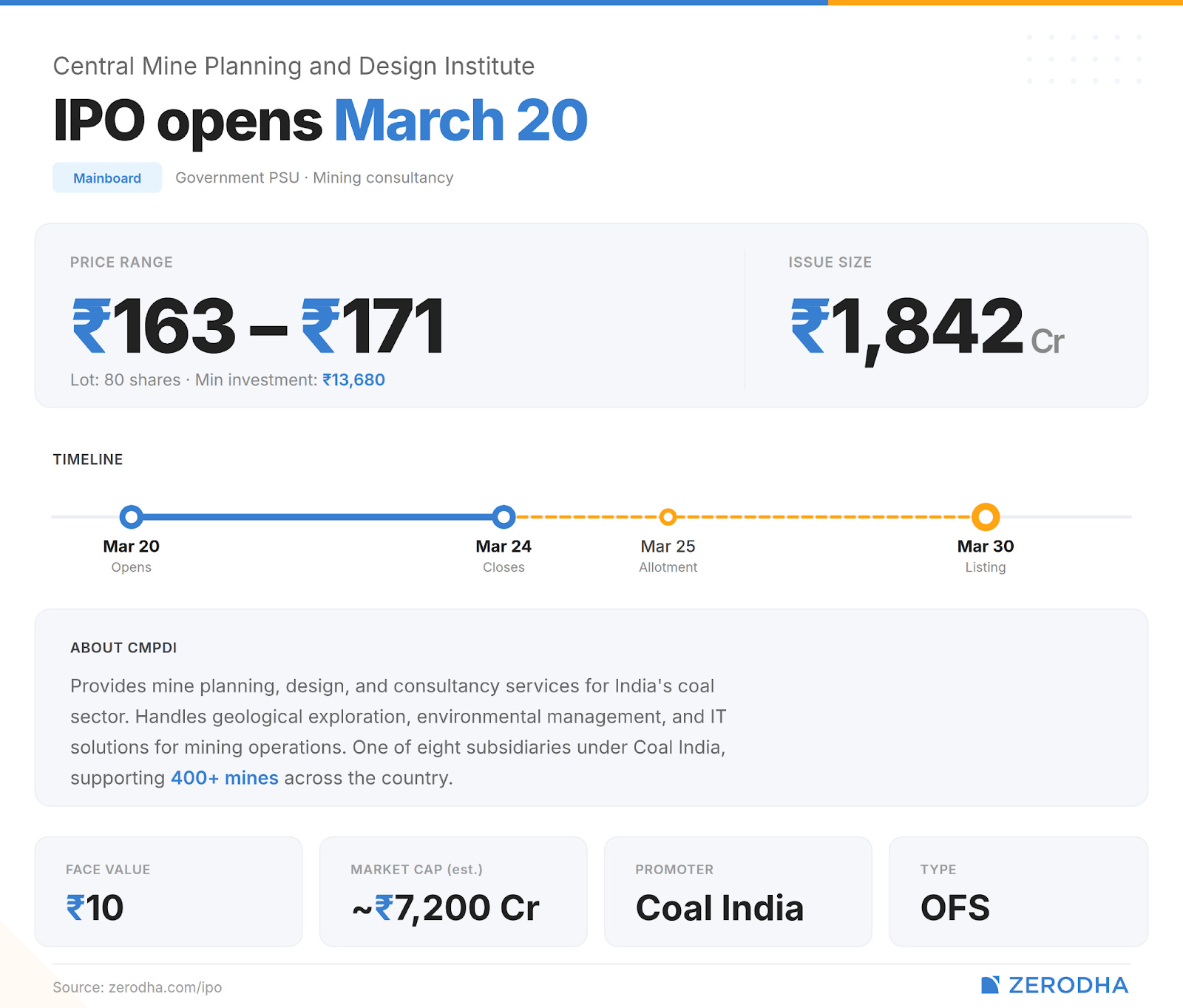

Before a coal mine opens, someone has to find the coal, map the geology, design the mine, get past regulators, and then keep measuring everything while the mine runs. In most of India’s history, that someone has been one company: Central Mine Planning & Design Institute (CMPDI).

CMPDI is Coal India’s in-house advisor or consultant. But it’s not like other advisory firms. This is a company with drill rigs in the field, eight laboratories, seven regional institutes stationed near India’s major coalfields, and the largest fleet of exploratory drills for coal in the country. It wouldn’t be a stretch to call it Coal India’s entire technical nervous system. We’ll unpack what that means as we go.

CMPDI is now going public. The IPO is an offer for sale worth ₹1,842 crore, with Coal India selling its stake. The company itself receives nothing from the issue. So the natural question is: what exactly is being put on the stock market here?

Let’s start from the ground up.

A sticky business

The best way to understand CMPDI’s business is to follow the lifecycle of a coal mine, from start to finish.

In stage one, you find the coal. The Ministry of Coal identifies a potential coal block. At this point, nobody knows how much coal is down there, what grade it is, or whether the economics work. So somebody has to go find out. CMPDI sends rigs into the ground, pulls out core samples, maps the rock formations underneath, and runs tests to figure out what’s down there and how much of it is worth extracting.

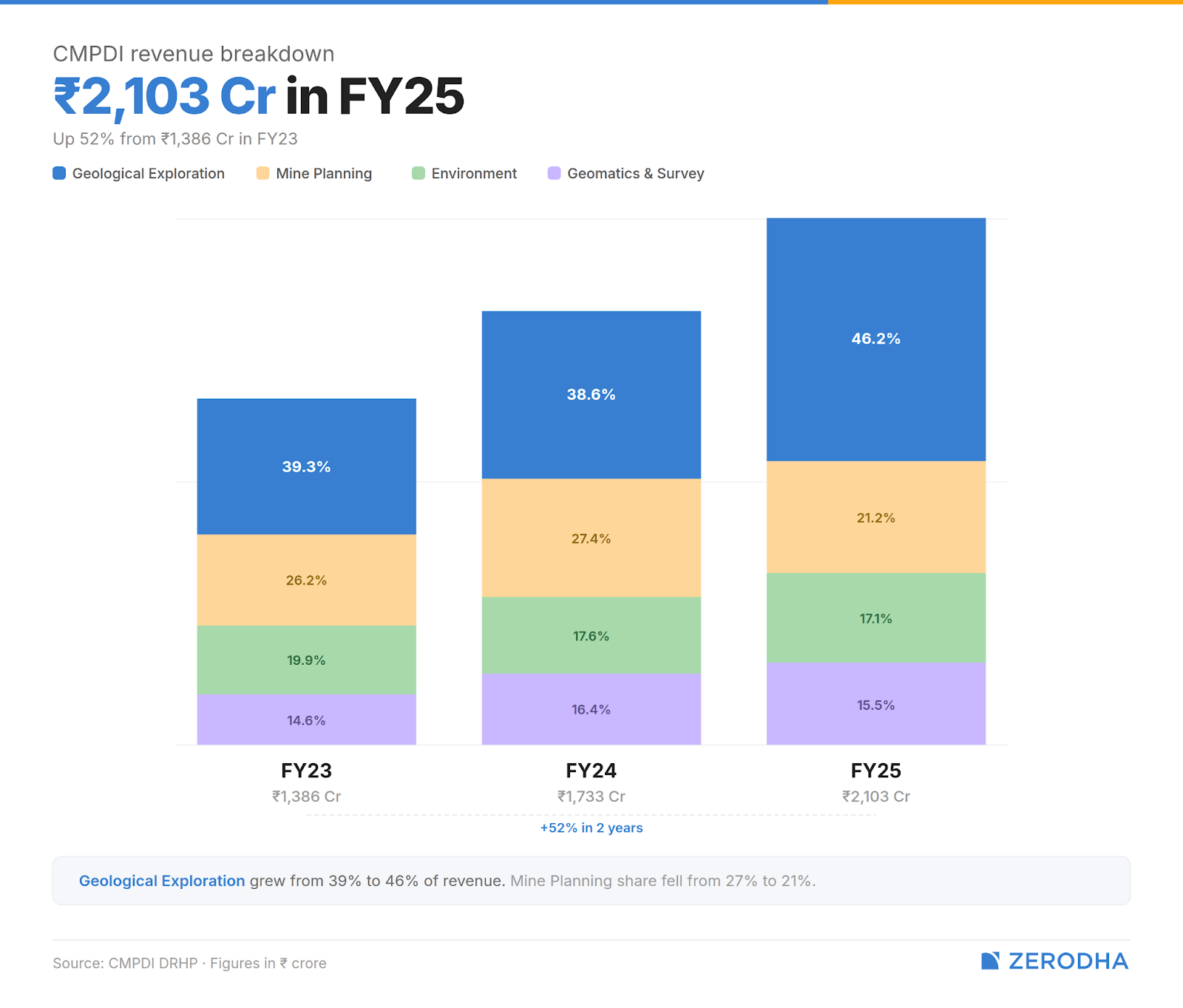

In the end, it puts together a formal ‘resource estimate’ report that says: this block contains X million tonnes of coal, of Y grade, at Z depth. Nothing moves forward without this document. No mine gets designed and no investment decision gets made — but, this is CMPDI’s biggest business. Geological exploration and resource evaluation accounts for ~46% of its revenue.

Stage two is designing the mine. Once the resource estimate confirms there’s coal worth extracting, someone has to figure out how to get it out, and that involves asking a lot of questions. Will it be an open-cast or underground mine? What will be the sequence of extraction? What equipment should be used? Anyway, CMPDI produces a feasibility study and detailed project report containing the possible answers, which goes to Coal India’s board for approval. This mine planning and design vertical make up ~20% of revenue.

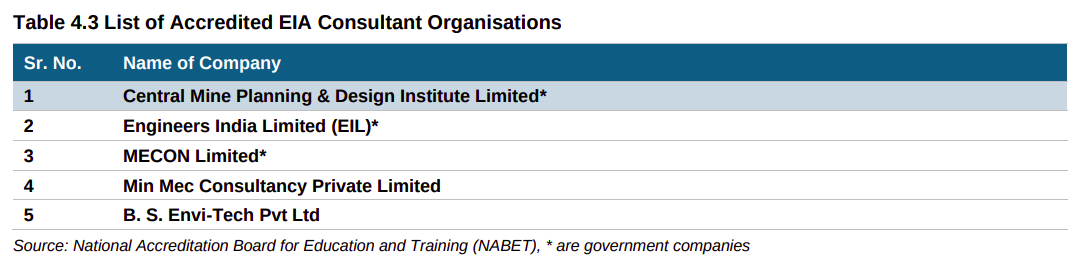

Stage three: getting past regulators. India has extremely heavy environmental regulation around mining. Before a single tonne of earth moves, the project needs an Environmental Impact Assessment (EIA), an Environmental Management Plan, forest clearance if the block sits on forest land, and consent from state pollution boards. With these many approvals, it’s probably no surprise that at this stage, projects routinely get delayed by years.

CMPDI prepares all of this paperwork. This vertical makes up ~18% of their revenue.

The last stage is monitoring the already-running mine. Somebody needs to verify how much coal has been extracted, whether boundaries are being respected, or whether underground fires are developing — a real problem in Indian coalfields. CMPDI does GPS surveys, LiDAR scans, drone-based mapping and fire mapping. This is the geomatics and survey vertical, making up ~17% of revenue.

Once CMPDI does the exploration, it naturally does the mine plan (since it knows the geology), then the environment impact assessment (since it knows the site), and hence the ongoing surveys also. Switching consultants mid-lifecycle is costly and risky. This stickiness is the actual moat — not technology, not AI, not any other buzzword.

And none of this work can be done by just anyone. Geological exploration, environmental impact assessments, mine planning — these all require formal accreditation from government bodies. You can’t prepare an EIA without being accredited by the Quality Council of India. That limits how many firms can even participate in this market.

But who’s actually hiring them?

CMPDI’s top ten clients account for over 93% of revenue. Coal India and its subsidiaries alone contribute roughly two-thirds. Government entities overall make up 96–99% — instead of hosting competitive tenders that would invite private players too, the government simply nominates CMPDI to do their work.

So, the question of whether CMPDI is genuinely the best at what it does, or simply the beneficiary of a captive relationship, is hard to untangle. The honest answer might be both.

CMPDI is the custodian of India’s entire coal and lignite geological database. Imagine having 50 years of drilling data, over 700 geological reports, all from executing the coal lifecycle countless times. It’s also the nodal agency for the government on coal R&D and an implementing agency for exploration programs under the National Mineral Exploration Trust. They do have the technical depth and regulatory embeddedness. But they also exist inside a structure where the biggest client is also the sole shareholder AND the entity that appoints the board.

In the broader mining advisory market, though, the consultant side is fragmented. There exist a few smaller players, but nobody that rivals CMPDI’s scale or data advantage in coal. Competition does exist at the margins, especially as coal block auctions bring private miners who might hire other firms. But inside Coal India’s own ecosystem, CMPDI is effectively a monopoly.

However, in non-coal work, the competitive picture flips entirely.

CMPDI has started picking up work in critical minerals — like lithium, rare earths, and copper — under government programs. India wants to reduce its dependence on mineral imports. But the geological expertise in coal doesn’t transfer cleanly for CMPDI.

See, coal is sedimentary rock, but critical minerals typically sit in hard-rock formations, requiring different drilling techniques and different domain expertise. In that space, the Geological Survey of India and Mineral Exploration and Consultancy Limited already have institutional advantages. International firms like SRK Consulting have decades of hard-rock experience, while CMPDI has just three international assignments in total.

What the numbers say

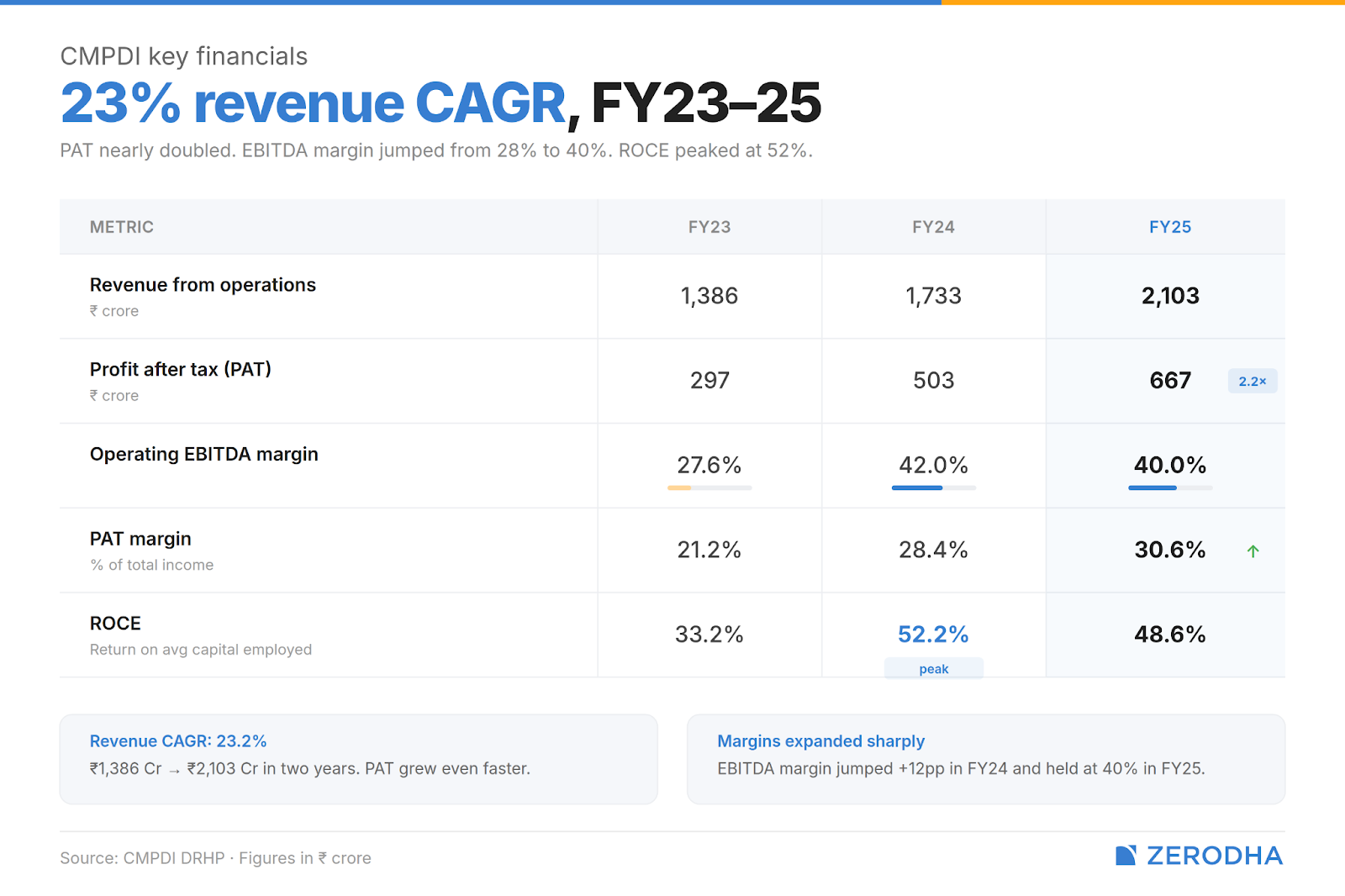

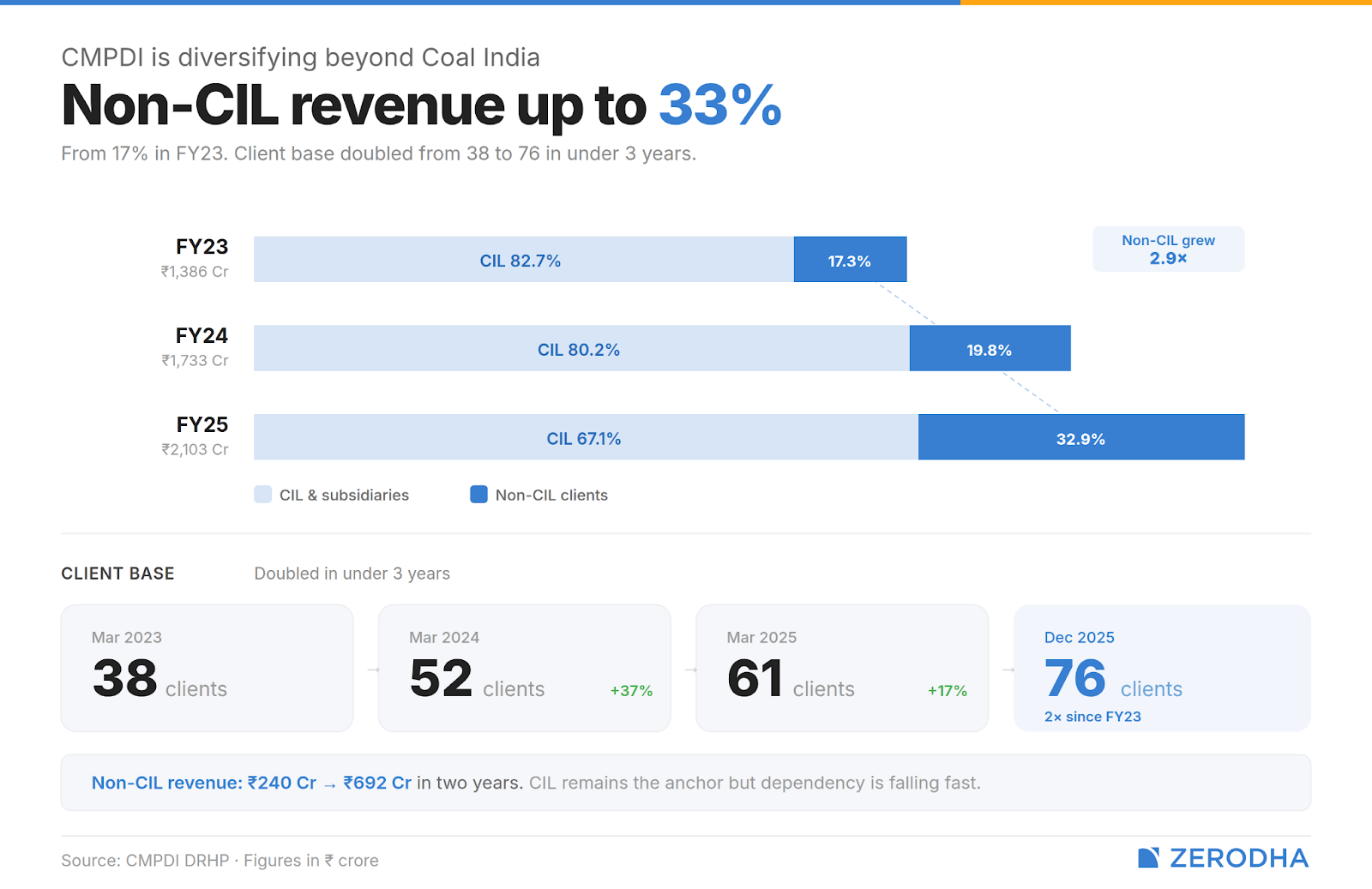

On the surface, CMPDI’s financials look remarkably strong. Revenue grew from ₹1,386 crore in FY23 to ₹2,103 crore in FY25 — a 23% CAGR. Profit after tax more than doubled, from ₹297 crore to ₹667 crore. EBITDA margins sit above 40%. Return on capital employed hit 48.6% in FY25. The company has zero debt. For an advisory business, these are really good numbers.

But where is the growth coming from? Interestingly, between FY24 and FY25, revenue from Coal India barely moved, but revenue from outside Coal India nearly doubled to ₹842 crore. The share of non-CIL in the total also doubled from 17% in FY23 to 34% in FY25. Client count went from 38 to 76 over the same period.

Clearly, CMPDI is finding work elsewhere — like government coal block auctions creating demand from private miners, Ministry of Coal scheme work, and some early critical mineral mandates.

Those are good signs, but the quality of growth needs interrogation.

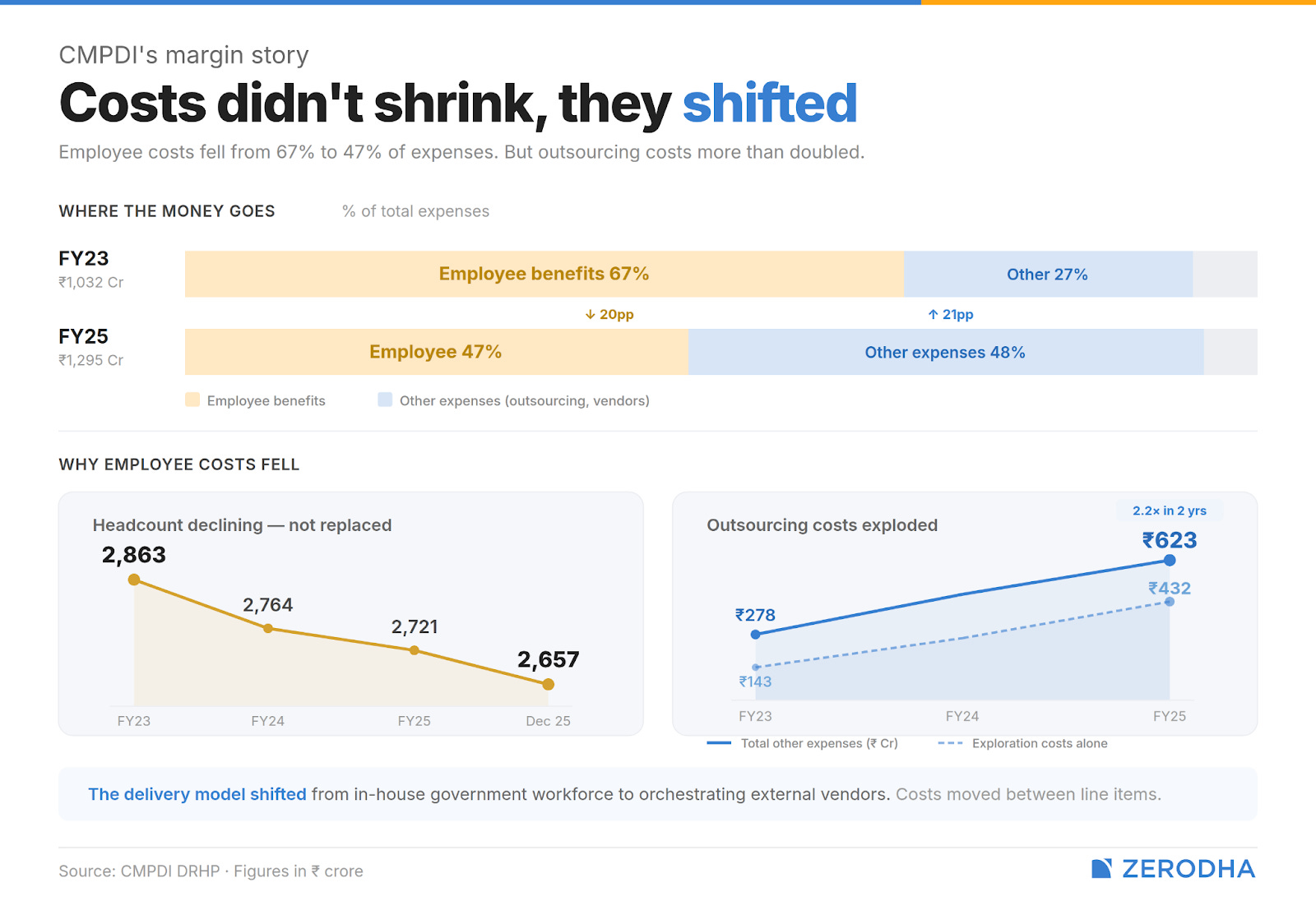

On the cost front, the margin story is more nuanced than it first appears. Employee benefits collapsed from 67% of total expenses in FY23 to 47% in FY25, driven by retirement attrition in a government workforce that isn’t being fully replaced. But the cost didn’t just vanish. Other expenses — primarily outsourced exploration and vendor costs — more than doubled over the same period. In FY25, more than half of CMPDI’s drilling was done by outside contractors, not its own rigs.

The delivery model is slowly shifting from an in-house government workforce to one that orchestrates external vendors. Margins expanded, but partly because cost moved from one line item to another, not because the underlying economics became dramatically more efficient.

Then there’s cash conversion, probably the biggest problem for them. CMPDI carries almost eight months of revenue uncollected — over ₹2,800 crore is past due beyond six months. Coal India’s own subsidiaries owe nearly ₹1,000 crore in old outstandings, and that number keeps growing. A company that can’t collect from its own parent is an odd thing to take public.

The interesting question

All of that makes the coal business clear enough. But that’s not what makes this company genuinely interesting, at least for us. It’s their activity outside of coal — in critical minerals.

India is waking up to the fact that it needs to find and secure its own supplies of lithium and rare earths. The government is pouring money into exploration through programs like NMET and Mission Critical Minerals. CMPDI, as the country’s largest mining consultancy with exploration infrastructure already in the ground, sits right at the centre of that push. And unlike coal, where demand has a visible plateau sometime in the 2030s, critical minerals have much longer demand visibility. If CMPDI could build a genuine franchise here, the business transforms from a coal-cycle story into something with a fundamentally longer runway.

But the right to win is hard to find. The mining consultancy market itself grows at just 4.8% a year — below nominal GDP. The operational texture still reads like a PSU department, not a capital-markets-grade company. And the next Pay Commission revision could push employee costs up 20–25% overnight, compressing the very margins that make the stock look attractive.

CMPDI has a genuine monopoly in a business that works — but has a ceiling. The most exciting, high-growth part of its future is precisely where the evidence is thinnest. And right now, their aspiration to achieve that growth is ahead of the proof.

Tidbits

HDFC Bank’s part-time chairman Atanu Chakraborty resigned abruptly, saying certain “happenings and practices” at the bank over the past two years weren’t in line with his personal values and ethics. He didn’t specify what those practices were. The stock crashed ~5% to a 52-week low, erasing over ₹65,000 crore in market cap. The RBI issued a public statement saying the bank remains “well-capitalised” with “no material concerns on record.”

Source: BloombergNovo Nordisk’s Indian patent on semaglutide — the molecule behind Ozempic and Wegovy — expires today (March 20). Sun Pharma, Dr Reddy’s, Zydus, Lupin, and Mankind Pharma are all planning Day 1 launches, with around 50 branded generics expected to hit the market. Monthly therapy costs are expected to drop from ₹10,000–12,000 to around ₹3,500–4,000. Jefferies has called it a “magic-pill moment,” estimating the domestic semaglutide market could eventually hit $1 billion.

Source: Business TodayThe Union Cabinet approved the Small Hydro Power Development Scheme for FY27–31, targeting 1,500 MW of new capacity through projects in the 1–25 MW range, with a focus on hilly and northeastern states. The ₹2,584.60 crore outlay is expected to crowd in roughly ₹15,000 crore in private investment, with all plant and machinery sourced domestically.

Source: PSU Watch

- This edition of the newsletter was written by Pranav and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

The rising frequency of air accidents definitely isn't helping the case, with pilots facing increased scrutiny