Hi folks, welcome to another episode of Who Said What? I’m your host, Krishna. For those of you who are new here, let me quickly set the context for what this show is about.

The idea is that we will pick the most interesting and juiciest comments from business leaders, fund managers, and the like, and contextualize things around them. Now, some of these names might not be familiar, but trust me, they’re influential people, and what they say matters a lot because of their experience and background.

So I’ll make sure to bring a mix—some names you’ll know, some you’ll discover—and hopefully, it’ll give you a wide and useful perspective.

For all the sources mentioned in this video, don’t forget to check out our newsletter; the link is in the description.

With that out of the way, let me get started.

What’s going on with private credit?

In the past few days, apart from the ongoing war coverage, there’s one — actually, two — words that keep quietly popping up in financial news: private credit. Wild things are happening in the US because of it. Some people are already calling it the next financial crisis. Funds are freezing withdrawals, assets are being marked down, and companies are going bust.

What really got us curious was a specific warning from Steffen Meister, the chair of Partners Group — a Swiss private markets firm managing more than $180 billion in assets. He told the Financial Times this week that default rates in private credit could double in the next few years. When someone managing that much money says something like that publicly, it’s worth paying attention.

But since private credit is still a relatively new concept in India, let’s take a step back first — understand what it actually is and how it works — before getting into what’s going wrong.

Where private credit came from

To understand private credit, you first need a rough picture of how traditional banking works. A bank takes deposits from ordinary people like you and me — money that can be withdrawn at any time — and lends it out to businesses for years at a stretch. This is an inherently unstable arrangement, because the bank’s liabilities are short-term but its assets are long-term. If too many depositors ask for their money back at once, the bank cannot pay. That’s what a bank run looks like.

Because of this fragility, banks are heavily regulated. After the 2008 global financial crisis, that regulation got significantly tighter. In the US, new rules forced banks to hold much more capital against risky loans, which made lending to mid-sized businesses far less attractive. They pulled back, and a large portion of the market was left without a reliable source of funding.

Now, here’s where private credit stepped in.

Instead of going to a bank, a mid-sized company could now borrow directly from a private credit fund — a large pool of capital raised from institutional investors like pension funds and insurance companies, who agreed to lock their money away for several years. Because these investors weren’t demanding their money back at short notice, the fund could lend longer, lend more flexibly, and lend to borrowers that banks were no longer willing to touch. Over the decade and a half since 2008, this market has grown into a $2 trillion global industry.

How it actually works

When a private credit fund lends to a company, it isn’t going through any public market. There are no bond ratings, no standardised terms, no thousands of anonymous creditors. It’s a direct deal negotiated privately between the borrower and usually just one lender, which means every element — the repayment schedule, the interest rate, the conditions attached — can be customised. If a company needs to fund an acquisition quickly, or has a complex business model that a bank’s standard process wouldn’t know what to do with, a private credit fund can structure something that works. The trade-off is price: private credit is significantly more expensive than a traditional bank loan. In India, where bank loans might cost 8–9% a year, private credit deals routinely target lender returns of roughly 18%.

These loans also sit at the top of what’s called the capital structure.

If a company goes bankrupt and its assets are liquidated, the private credit lender gets paid back before anyone else — before other bondholders, before shareholders, before almost everyone. That combination of high returns and first-in-line repayment priority is why large institutional investors found private credit so attractive. There is one more feature worth understanding, though, because it becomes central to what’s happening right now. Unlike a fixed-rate bond, most private credit loans carry a floating interest rate, meaning the interest the borrower pays rises and falls with prevailing market rates. When rates are low, this is manageable. When rates rise sharply, the burden on the borrower can increase dramatically.

When the tide turned

For most of the decade after 2008, private credit was a success story. But two things have happened recently that are beginning to unwind it simultaneously.

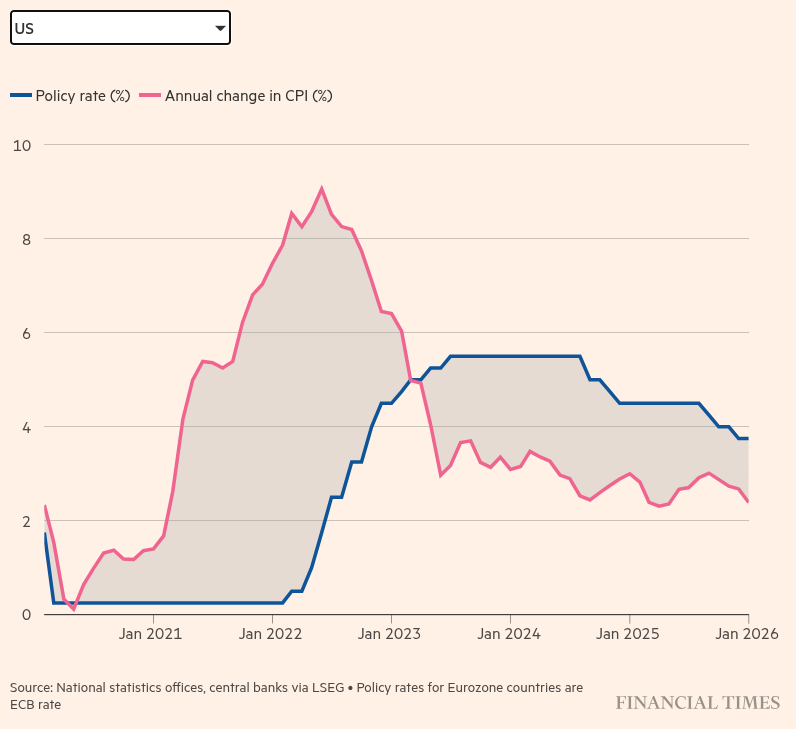

The first is interest rates. After central banks raised rates aggressively from 2022 onwards to fight inflation, the floating-rate structure that defines most private credit suddenly became far more burdensome for borrowers.

Companies that had borrowed at manageable rates found their interest payments climbing faster than their revenues. The consequences are clear in the data: according to Fitch Ratings, the US private credit default rate hit 9.2% in 2025, a record high, up from 8.1% the year before. Among the smallest borrowers, those with annual earnings under $25 million, the default rate was closer to 13%.

The second issue is AI. Over the last decade, a significant share of private credit lending went to mid-sized software and technology companies, often because private equity firms were using borrowed money to buy and consolidate these businesses. The model worked well when software companies had stable, recurring revenues. But AI tools have introduced a risk nobody priced in — the very services many of these companies sold can now be replaced or undercut. What makes this particularly painful for private credit, as opposed to private equity, is the asymmetry of the investment.

A private equity firm that owns a software company can still benefit if AI ends up helping that specific company thrive — the equity goes up, and the firm wins. A private credit fund doesn’t have that option. It lent money and needs it back with interest. It doesn’t share in the upside if a company flourishes, but it bears the full loss if the company fails. In a world where AI is bifurcating outcomes — some companies surging, many others getting wiped out — private credit is structurally exposed to the losing side. This is exactly what the fund manager I mentioned in the beginning described to the FT, and it’s why JPMorgan has already begun marking down its private credit exposure in software — a notable signal from a bank that lends heavily to these funds.

The structural cracks

Beyond the macro picture, two features of how private credit has been operating are amplifying the stress. The first is what the industry calls “covenant-lite” loans. A covenant is a rule a borrower must follow as a condition of the loan — say, a minimum cash balance they must maintain. These rules give lenders early warning if a borrower starts deteriorating, so they can intervene before things spiral. But as private credit became increasingly competitive, funds started dropping these protections to win deals. More than 30% of private credit deals today are covenant-lite, meaning a lender may not find out a borrower is in serious trouble until the company has already run out of money.

The second is opacity, and this one is directly causing the withdrawal freezes you’ve been reading about. Because private credit loans aren’t traded on any exchange, there’s no daily market price for them. Funds value their loan portfolios internally, typically at or near original value even as conditions change. This was a theoretical concern for years — until private credit firms began launching a specific type of fund called a Business Development Company, or BDC, to let wealthy retail investors into the market. Unlike traditional funds that lock capital away for a decade, BDCs offered semi-liquidity: investors could typically withdraw up to 5% of the fund’s value each quarter.

The trouble is that partial liquidity creates a classic bank-run dynamic the moment investors lose confidence. If people suspect the actual value of the loans inside a fund has fallen, but the fund is still allowing withdrawals at the original stated value, rational investors will rush to take their money out before everyone else does. Once requests hit the 5% cap, the fund freezes further redemptions — and that announcement tends to confirm exactly the fears that triggered the rush. Last week, BlackRock limited redemptions from a flagship debt fund after a surge in requests. Blackstone disclosed that its private credit fund BCRED saw a significant jump in withdrawal requests in the first quarter of this year. These are not obscure players — they are among the largest asset managers in the world.

So what’s actually happening on the ground?

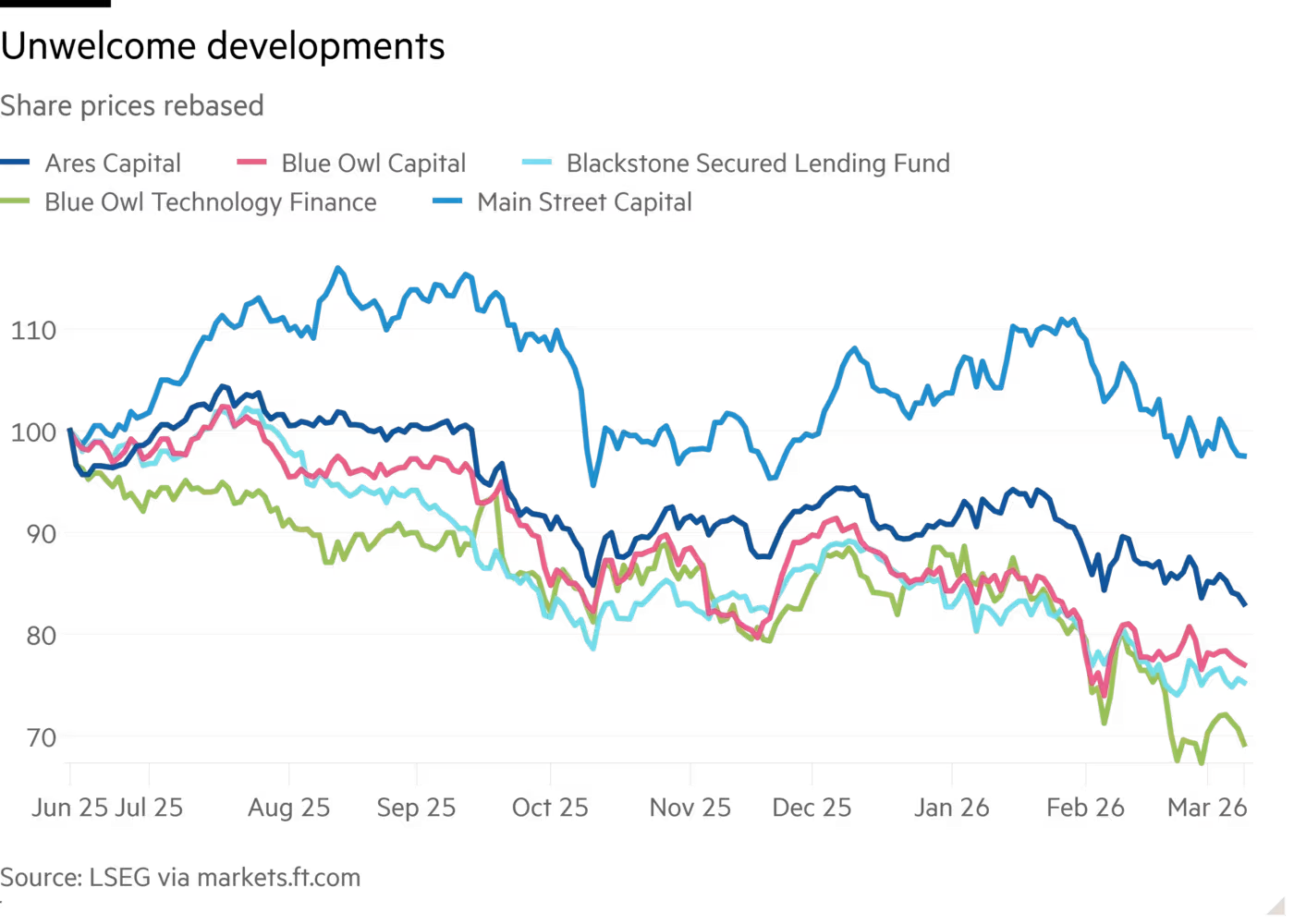

The most vivid example of all this coming together is Blue Owl Capital, one of the biggest names in private credit with over $300 billion under management. Blue Owl had built a large portion of its lending business around software companies — exactly the sector most exposed to AI disruption. When retail investors in one of its BDC funds started asking for their money back in large numbers, Blue Owl did two things. First, it sold $1.4 billion worth of loans from its portfolio to institutional investors to raise cash. Then it permanently shut the gates on quarterly redemptions for that fund — meaning investors who expected to be able to take their money out every three months no longer can. Blue Owl’s stock has since fallen sharply, entering an 11-day losing streak after the announcement, its worst run since going public. Dan Rasmussen of Verdad Capital called it “a canary in the coal mine.” Others have drawn comparisons to the early warning signs of 2007.

To be clear, none of this means a collapse is imminent. But there are warning signs.There are many more layers to this story — how these funds are structured, how fraud has crept in through some of the bankruptcies, what continuation vehicles and CLOs are, and what all of this means for India’s own private credit market, which is growing fast. We’ll get into all of it, either through future episodes of Who Said What or on The Daily Brief. For now, though, you have enough to understand why two words are suddenly everywhere.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Really interesting breakdown. Private credit sounds like a high-reward but tricky game, especially with rising rates and AI shaking up businesses. Definitely something to watch closely.

Excellent read. Simply articulated

in layman terms. Great