What caused the inflation to drop?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

Investors’ outlook often depends on their past experiences. Those who’ve seen bull markets are typically more optimistic and willing to take risks with equities, while those who’ve faced bear markets tend to be more cautious, favoring fixed-income assets. Striking the right balance between the two is key, especially in today’s volatile market conditions.

In this Z-connect post, we dive into past market downturns to see how tough they’ve been and why staying resilient during a bear market is more important than ever.

In today’s edition of The Daily Brief:

Breaking down the headline inflation of 5.22%

It's the dollar's world, we just live in it

Breaking down the headline inflation of 5.22%

Recently, India’s latest inflation data was released, and it’s something we, as market watchers, should pay attention to. After months of worrying about rising prices, retail inflation, measured by the Consumer Price Index (CPI), cooled down in December 2024, hitting a four-month low of 5.22%.

This is important because inflation directly impacts the cost of living. For families, businesses, and policymakers, lower inflation brings some relief, but it also comes with its own set of challenges.

Over the past few months, inflation has been steadily dropping. It peaked at 6.2% in October 2024, eased to 5.5% in November, and now, December’s 5.22% marks the lowest level in four months. The main reason behind this decline is the drop in food prices, which has been one of the biggest factors driving inflation in the country.

Food prices, however, can be unpredictable since they’re influenced by things like weather, crop production, and global markets. In December, food inflation eased to 7.69%, down from 8.2% in November—a noticeable improvement.

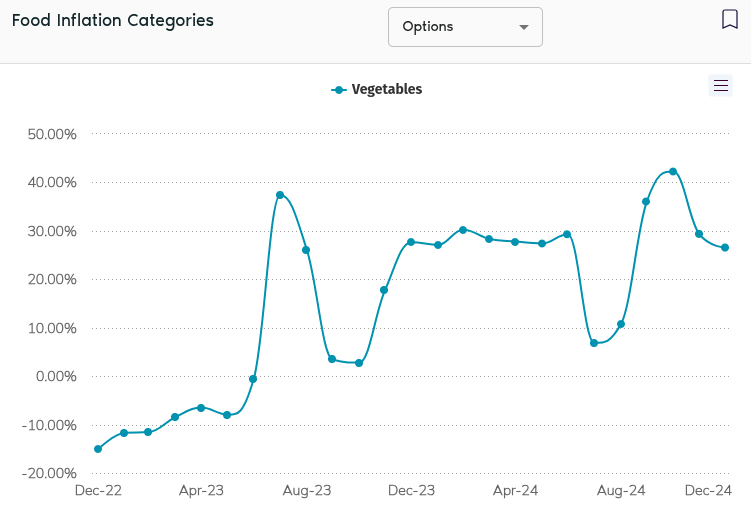

The drop in inflation was largely driven by a big reduction in vegetable prices, especially for staples like onions, tomatoes, and potatoes.

These items are a big part of the average Indian household’s diet, so when their prices go down, it brings immediate relief. For example, vegetable inflation fell to 26.6% in December, the lowest it’s been in four months.

However, not all food prices came down. Edible oils, for instance, saw their prices jump by 14.6%—the highest in 32 months—due to factors like import taxes and global supply issues. Similarly, essentials like milk and meat also became more expensive.

While food prices usually grab the most attention, there’s another part of inflation we should keep an eye on—Core Inflation. This excludes food and fuel since their prices can be very unpredictable and might not give a clear picture of overall inflation. In December, core inflation stayed steady at 3.6%.

This is good news because it shows that the prices of other goods and services—like education, healthcare, and transport—aren’t rising as quickly. In fact, core inflation has stayed below 4% for over a year, which is a sign of stability in the economy.

According to CareEdge Ratings, the outlook for agriculture looks positive. Strong Kharif production and good conditions for Rabi sowing, supported by healthy reservoir levels, are key factors. As of the end of December, Rabi sowing is up 0.5% compared to last year, showing solid progress. This should help bring food inflation down even further.

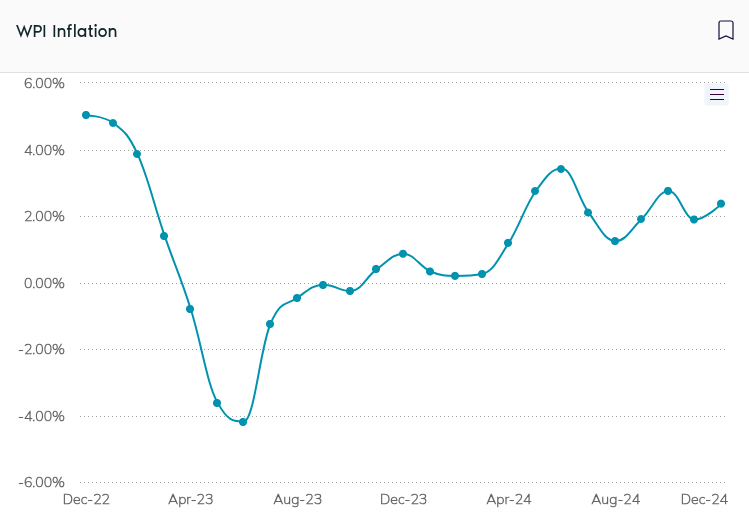

On the wholesale side, India’s Wholesale Price Index (WPI), which tracks inflation at the producer level, rose slightly to 2.37% in December from 1.89% in November.

This increase was mainly due to higher costs for food items and textiles. However, on a month-to-month basis, the WPI actually dropped by 0.38%, which shows some easing in manufacturing costs and primary articles like crude oil.

The Reserve Bank of India (RBI) is likely keeping a close eye on these numbers. In the recent Monetary Policy Committee (MPC) meeting, the policy repo rate was left unchanged at 6.50%. Most members, including former Governor Shaktikanta Das, supported this decision, emphasizing the need to balance inflation control with supporting economic growth. However, Dr. Nagesh Kumar and Professor Ram Singh voted for a 25-basis-point rate cut, arguing that it could help boost economic activity without significantly affecting inflation.

In December, the RBI projected headline inflation to average 4.8% for the quarter, and the actual numbers have aligned with this forecast. This has sparked fresh discussions about whether the central bank will cut interest rates in February 2025 to support growth. Lower interest rates make borrowing cheaper, which can encourage businesses to invest and consumers to spend, giving the economy a much-needed boost. However, global uncertainties, such as fluctuating oil prices and a weakening rupee, make the situation more complicated.

Imported inflation is another factor adding to the challenge. In December, imported inflation rose to 5.4%, the highest in 22 months. The rupee has weakened by about 4% against the dollar since the financial year began, making imported goods more expensive. This could limit the RBI’s ability to lower interest rates in the near future.

Adding to the mix, the RBI now has a new governor at the helm. It will be interesting to see how he manages the tricky balance between cutting rates to support growth and keeping inflation under control.

In summary, the drop in inflation is a welcome relief, especially for households struggling with high food prices. But the overall picture remains mixed. While vegetables are cheaper, essential items like milk, oils, and proteins are still expensive. Core inflation is steady, signaling stability, but the rise in imported inflation presents a longer-term risk.

According to India Data Hub, inflation continues to pose a challenge for rate cuts. While headline CPI has eased, the pace of decline hasn’t been sharp enough. The rupee’s persistent depreciation only adds to the complexity. Globally, monetary easing is also on hold, with Fed fund futures showing less than a 50% chance of a US Fed rate cut by March. Given all this, it seems likely that the RBI will maintain its current stance in the February policy meeting.

It's the dollar's world, we just live in it

Let’s paint a picture: Since September 2024, the Fed has cut interest rates by 1%. But here’s the twist – even with these cuts, the 10-year Treasury yield has jumped by more than 1.15%.

And that’s not all. The dollar keeps getting stronger. We’re now at the highest trade-weighted dollar levels since 1985, adjusted for inflation.

What makes this so interesting is that, historically, this is the opposite of what usually happens. Typically, when the Fed starts cutting rates, long-term yields drop too. But 2025 seems to be rewriting the playbook, and Wall Street is buzzing.

So, what’s behind all this? Experts are pointing to something called the “term premium.” In simple terms, it’s the extra reward investors want for holding longer-term bonds instead of just rolling over short-term ones. This premium has shifted from negative territory to nearly 50 basis points. But here’s the catch – no two people seem to agree on what “term premium” really means.

Jim Bianco of Bianco Research highlighted on Twitter that our only historical comparison is from 1981. Back then, when the Fed started cutting rates from 20% in May, the 10-year yield actually jumped from 12% to almost 16%. That’s when the term “bond market vigilantes” came into play – bond traders forcing the Fed’s hand through aggressive selling.

There’s an interesting debate on Wall Street about what level of the 10-year yield would be especially problematic for stocks. The consensus seems to be settling around 5%. We’ve already gotten a preview of that – the less closely watched 20-year Treasury recently hit that mark. If we reach 5% and stay there, maybe the markets can adjust. But if we blow past it? That’s a whole different story.

Let’s talk about valuations. Analysts at Charles Schwab point out that, over the past 50 years, the average gap between 10-year Treasury yields and the Fed Funds rate has been around 120 basis points. Since 2010, it’s typically been in the 125 to 150 basis point range. With the Fed Funds rate at 4.5%, that puts a "fair" 10-year yield somewhere around 4.5-4.75%. Right now, we’re in that zone.

Here’s where it gets really interesting: inflation expectations. Research by Jim Bianco shows that when the Fed was hiking rates in 2022 and 2023, inflation expectations dropped and stayed low. When they paused, expectations held steady. But now that they’re cutting? Those expectations are climbing again. Think back to June 2008, when inflation expectations peaked. Back then, it was driven by oil prices hitting $145 a barrel. Today, oil is at $80, yet inflation expectations are still rising.

The global implications of all this are significant. ING’s latest research, titled "Trump’s currency, your problem" – a clever nod to John Connally’s famous quote, “The dollar is our currency, but it’s your problem” – warns that the combination of a stronger dollar and higher Treasury yields is causing serious issues worldwide. Brazil has already had to hike rates and spend $30 billion of its FX reserves to defend its currency. But the real battleground? It’s USD/CNY, where the People’s Bank of China is fighting to hold the line around 7.32-7.34.

Looking at Asia more broadly, the pressure is intense. The Korean won’s movements have raised concerns about potential intervention. India’s rupee, which remained remarkably stable through 2023 and 2024, has finally started weakening, climbing 2% just last month. ING research pointed out that the Reserve Bank of India intervened extensively in the FX market last year. However, the appointment of a new central bank governor last month has led to expectations of a less active approach to managing the rupee’s volatility. This comes as the recent GDP growth numbers for Q3 2024 came in much lower than expected. Meanwhile, the Indonesian rupiah remains especially vulnerable due to its sensitivity to U.S. interest rate changes.

Looking ahead, Schwab suggests that the upper limit for 10-year Treasury yields could reach 5% this year. That prediction assumes another 50 basis points of Fed rate cuts and gradually easing inflation. But – and this is important – that scenario assumes no major policy surprises. Given the Trump administration’s stance on tariffs, immigration, and fiscal policy, that’s a pretty big assumption.

At the December Fed meeting, policymakers signaled only two 25-basis-point cuts for 2025, which could bring the rate down to around 4%. However, here’s where things get uncertain. The market was initially expecting much steeper cuts, but December’s strong jobs report changed the narrative. Now, the likelihood of a January rate cut has dropped significantly.

So, what does all this mean for global markets? Well, the combination of higher yields and a stronger dollar is creating a massive pull of capital back to the U.S. Think about it – when you can get a nearly 5% guaranteed return in U.S. Treasuries, plus potential gains from a stronger dollar, why take risks elsewhere? This is hitting emerging markets hard. It’s not just Brazil, as we discussed earlier – we’re seeing this pressure across the board.

Tidbits

HCLTech reported a net profit of ₹4,591 crore for the third quarter of the 2025 financial year. This marks a 5.5% increase compared to the same period last year and an 8.4% rise from the previous quarter. The company’s total revenue for the quarter stood at ₹29,890 crore, up 5% year-on-year and 3.5% quarter-on-quarter. HCLTech also raised its revenue growth forecast for the 2025 financial year to a range of 4.5–5%, an improvement from the earlier estimate of 3.5–5%. This updated guidance includes the impact of its acquisition of Hewlett Packard Enterprise’s Communication Technology Group assets.

China reported a record trade surplus of $992 billion in 2024, a 21% increase compared to the previous year. This growth was fueled by strong exports, including $525 billion worth of goods shipped to the United States. In December alone, exports to the US reached $49 billion, the highest monthly figure in over two years. While global demand for Chinese goods remains strong, imports into China have been held back by weaker domestic spending and lower commodity prices.

Urban Company, valued at $2.1 billion as of June 2021, is planning to file for an IPO worth about ₹3,000 crore by March 2025. The IPO will be managed by Kotak Mahindra Capital, Goldman Sachs, and Morgan Stanley. Urban Company operates in over 50 Indian cities, as well as in the UAE and Singapore, offering services like beauty treatments and appliance repairs.

-This edition of the newsletter was written by Bhuvan and Anurag

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉 Join the discussion on today’s edition here.

Nicely written with data 👍.. can you pls do a much more simpler version where it can provide basics to talk about inflation vs interest rates.. how these parameters impact country's currency with respect to US dollar and their market and how US markets or US dollar can impact global markets.. How global markets and policies will react to US dollar strengthening.. all these are taken care in this article but still want a more simpler version with examples..🙏