Weekly Brief: China's economic history, the early August panic, and are Indian markets overvalued?

On weekends, we usually compile the best stories of the week and release a recap for those who didn't have time to listen during the week.

However, many of you shared feedback that you listen to the Daily Brief daily and would prefer not to hear the same stories repeated over the weekend. So we are trying something different.

In today’s edition:

- Oil demand & China's economic history

- Why are the markets falling?

- Are the Indian markets overvalued?

You can also listen to this as a podcast on Spotify, Apple Podcasts or wherever you get your podcasts and video on YouTube.

What's happening in China?

The catalyst for this discussion was an edition we published on Thursday, focusing on the recent developments in the oil markets. China, a key player in global economics, has been causing a significant decline in oil demand. In short, oil demand is falling globally because the Chinese economy is in bad shape.

Even if you've only been following the news from a distance, you might already know that China’s economy has been struggling for a while. But what’s less understood is why it’s in such a state, how China became the powerhouse we know, and what’s causing its current domestic problems.

A historical context

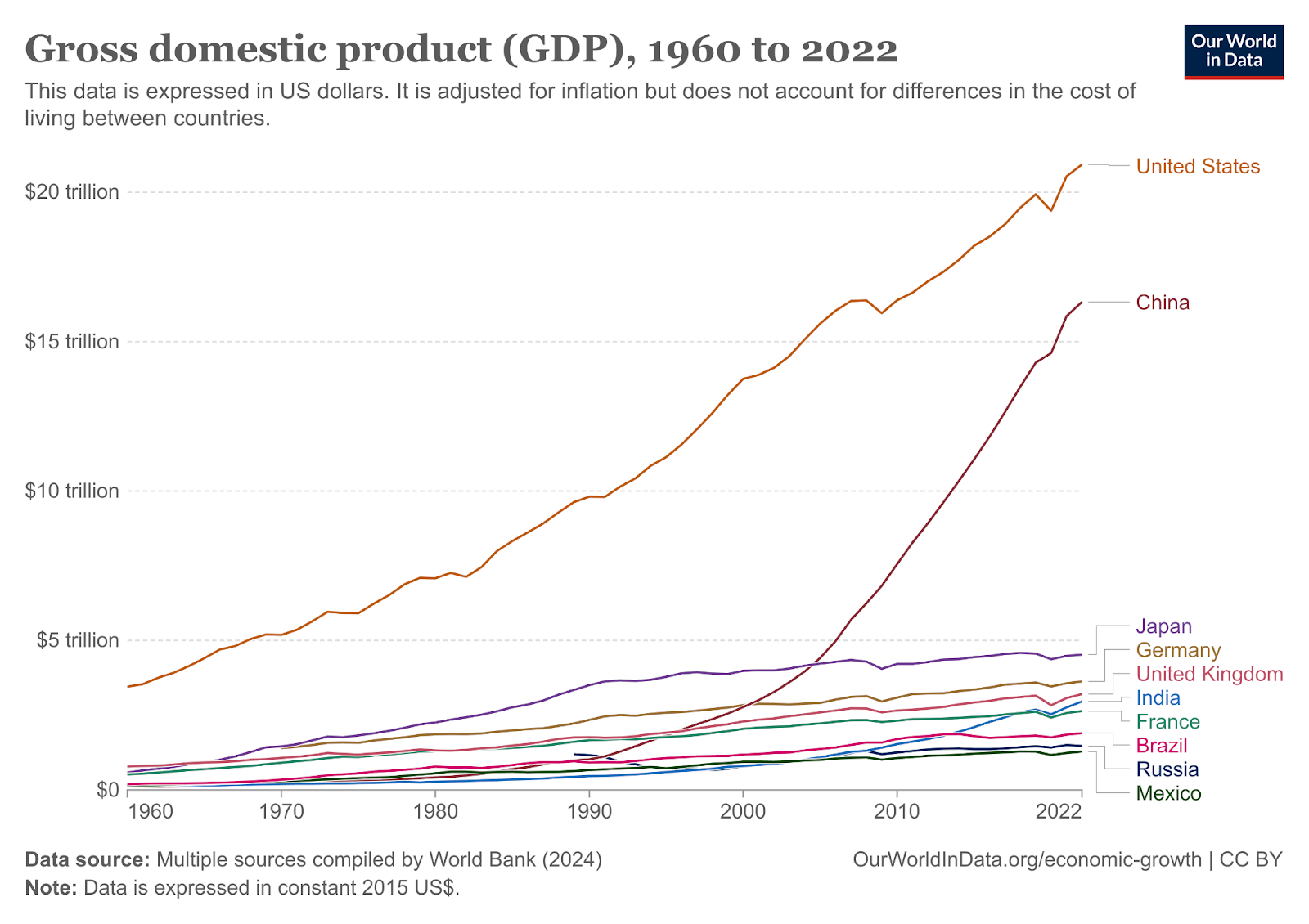

To grasp what’s happening in China today, we need to step back in time to the 1980s, when China’s economic reform journey began. Back then, China and India were roughly at the same economic level. For context, India's per capita GDP was about $380, and China’s was around $430—a negligible difference. However, what followed in China was nothing short of spectacular.

From the 1980s onwards, China’s economy grew at an average rate of 10%. This unprecedented growth, often termed the “Chinese Miracle,” has no close comparison in modern economic history. Sustaining a 10% growth rate for 20 to 30 years transformed China into the world’s second-largest economy by GDP, all within a brief period from the 1980s to around 2010.

The investment-led growth model

China’s economic rise was driven by what is known as an investment-led growth model. This model isn’t unique to China; it has roots in the Soviet Union, pre-World War I Germany, and was later adopted by countries like South Korea, Japan, and the Asian Tigers. The model involves two key components: massive investment and the suppression of household consumption.

China poured immense amounts of money into building an industrial base, a real estate sector, and infrastructure that didn’t previously exist. It created entire cities, schools, healthcare facilities, and commercial complexes from scratch. But where did the money come from? The answer lies in a deliberate policy to suppress household consumption, which kept wages low and interest rates artificially depressed, effectively transferring wealth from households to industry.

Rise and fall of China’s economic miracle

As China’s economy began to take off in the 1980s, it had almost no industrial base to speak of. But by the early 2000s, particularly after joining the World Trade Organization in 2001, China became the world’s factory, leveraging its surplus of cheap labor. The 2008 global financial crisis marked another turning point. While the rest of the world was reeling, China embarked on a historic spending boom, investing heavily in infrastructure and manufacturing, helping to stave off a global depression.

However, by 2010, the limits of China’s investment-led model began to show. The more China built, the less economic return it generated from each dollar spent. This diminishing return was a clear sign that China couldn’t rely on this model forever. By 2015, the first cracks began to appear, with a minor economic crash that many believed would burst the Chinese bubble. Yet, Chinese policymakers managed to keep the economy afloat, though the underlying issues remained unresolved.

Fast forward to 2020, and the COVID-19 pandemic delivered another shock to China’s economy. The government started cracking down on the real estate sector, which had become a massive 30% of China’s GDP. With property prices plummeting and new construction projects hitting all-time lows, the real estate sector is in deep trouble. This is significant because about 65% of Chinese household wealth is tied up in property, making the collapse a potential disaster for the broader economy.

By 2023-2024, China is facing a new economic reality. The old model of heavy investment is no longer sustainable, and the government is reluctant to shift towards boosting household consumption. Instead, China is trying to replace the lost growth from the real estate sector with new industries like solar, wind, electric vehicles, and battery manufacturing. However, this shift is creating new tensions globally.

Global impact: The export problem

China's current strategy involves ramping up exports to offset its domestic economic problems. For instance, China can produce around 40 million vehicles a year, but domestic demand is only about half of that. The same overcapacity exists in other industries like solar cells, steel, and chemicals. This has led to a surge in Chinese exports at prices other countries can’t compete with, triggering trade tensions worldwide.

Countries around the globe are responding with tariffs and duties on Chinese imports, from electric vehicles to steel and aluminium. This protectionist wave spans not only the U.S. and Europe but also countries like Canada, Brazil, Turkey, and India. The root cause is China’s massive subsidies to its industries, which far exceed those of other advanced economies.

The world’s dilemma: Dependence on China

Despite the growing animosity towards China, the world remains heavily dependent on Chinese technology, especially for the green transition. China’s dominance in solar, wind, and electric vehicle technologies makes it an essential player in the fight against climate change. However, China’s current approach of exporting its problems through overcapacity is causing global friction that could lead to broader economic conflicts.

The world is at a critical juncture. Climate change demands global cooperation, yet rising trade tensions, largely fueled by China’s economic strategies, are creating a more divided and hostile environment. How this story unfolds will shape the global economy for years to come.

The early August drama

Remember the first week of August? It was one of those weeks where you might have been bracing for a repeat of 2008, or even the 1930s—a full-blown financial crash. The atmosphere was thick with anxiety, and for a brief moment, it felt like the sky was falling. But, as quickly as the panic set in, it evaporated. We moved on, almost as if nothing had happened.

To give you a quick recap, during the first week of August, the Nikkei, Japan’s stock index, plummeted by about 20%. Global markets dropped around 4-5% and VIX had one of the biggest single-day spikes.

Interestingly, Indian markets showed resilience and didn’t move much. A 20% fall in a major index like Japan's is terrifying, and it led many to fear that this was just the beginning of something much bigger—a sign of deep-seated issues within the global financial system, unresolved since the 2008 crisis.

With more than a decade and a half of low interest rates behind us, people were suddenly concerned that the long-awaited reckoning was here. The fear was that with inflation soaring and interest rates rising, the financial system was finally about to unravel, with this crash making 2008 look like a mild event. But, in the end, it didn’t happen. The markets rebounded, and now, they’re back at or near all-time highs, as if that week’s drama was just a bad dream.

The carry trade

What was particularly fascinating during that first week of August were the narratives that emerged to explain what was happening. The dominant one was the “carry trade.” You might remember how, almost overnight, everyone on Twitter transformed from meme enthusiasts into carry trade experts. It was a bit of a spectacle in itself.

To break it down simply, a carry trade involves borrowing money in a currency with low interest rates, like the Japanese yen, and investing it in a currency with higher interest rates, such as the U.S. dollar. Japan had maintained near-zero interest rates for over 30 years, while U.S. rates were around 5%. So, theoretically, you could borrow in yen and invest in U.S. government bonds, earning a 5% return with seemingly no risk.

But, of course, it’s not that simple. The carry trade only works as long as the gap between the currencies remains stable. If the yen appreciates or the dollar depreciates, that gap narrows, reducing profits or even turning them into losses. And that’s exactly what triggered the panic. The Bank of Japan hiked interest rates for the first time in a long while, which sent shockwaves through the market.

How one event unleashes chaos

When there’s a sudden move in one asset class, it often ripples through others. Large institutional investors, who manage portfolios based on risk rather than just money, were suddenly forced to adjust their strategies. They had to sell or buy in response, creating a chain reaction across global markets.

For example, trend-following funds, which increase positions as assets rise or fall, were caught in the turmoil. The VIX, a measure of market volatility, spiked to levels seen only a few times in history, forcing more selling and buying as portfolios were rebalanced. This virtuous cycle fed on itself, leading to a sudden crash in the Nikkei and other markets.

Our desire for simple explanations

As humans, we crave simple explanations for complex events. But in the financial markets, those simple explanations often fall short. The truth is, nine times out of ten, we just don’t know why the market moves the way it does. We have to accept the volatility and understand that it’s part of the ride. That’s what we get paid for in the stock market—navigating uncertainty and staying calm when everyone else is losing their heads.

Are the Indian markets overvalued?

Lately, there's been a lot of chatter about whether the Indian markets are overvalued and if a crash is on the horizon. This concern isn’t unfounded—after all, we’ve seen an incredible bull run since the COVID lows in April 2020. The Nifty has surged around 200%, the mid-cap index has jumped by about 350%, and the small-cap index has soared over 400%. It’s been a period where almost anything you bought turned a profit. But, as with any extended bull run, anxiety is building. People are starting to worry that the market may be overheated, overvalued, or even in a bubble.

Kenneth Andrade, a well-known fund manager at Old Bridge Mutual Fund, recently did an interview with the Economic Times that caught our attention. He remarked:

"I would not really go out looking for value in a market that has none. We have been in this state for some time now."

Andrade’s comment highlights a broader concern: the market’s relentless rise since COVID, which has led some to believe that valuations have become detached from reality.

The numbers behind the concern

Nifty’s performance: The Nifty has posted positive returns for eight consecutive years, one of the longest streaks in Indian market history. This kind of sustained growth naturally leads to worries about whether the market is due for a correction.

Domestic vs. Foreign Investment: There’s been a notable shift in market dynamics. Historically, foreign institutional investors (FIIs) dominated the Indian markets. However, post-2008, domestic institutional investors (DIIs)—including mutual funds, pension funds, and insurance companies—have become the dominant players. In 2023, FIIs invested ₹1.7 lakh crores, while DIIs invested ₹1.8 lakh crores, and individual investors contributed ₹5,000 crores. In 2024, so far, FIIs have invested ₹28,000 crores, DIIs ₹3 lakh crores, and individual investors over ₹1 lakh crores. This massive influx of domestic money has led some to believe that the market’s rise is being artificially inflated by domestic liquidity.

SIP inflows: Another point of concern is the Systematic Investment Plan (SIP) inflows. The gross monthly SIP number is often quoted at ₹20,000 crores, but the net figure is closer to ₹8,500 crores. Even so, the consistent inflow of money into the market has led to fears that it’s pushing up valuations and distorting prices.

Buffett Indicator: The market cap to GDP ratio, often called the Buffett Indicator, is another metric people are watching. Historically, the average ratio for Indian markets has been around 85%, but it’s currently at about 135-136%. Similarly, the price-to-earnings (PE) ratios for large caps, mid-caps, and small caps are 23, 25, and 40, respectively. These elevated numbers have led many to scream that the market is overvalued.

Are we in a bubble?

So, is the Indian market in a bubble? Are things overvalued? The answer isn’t straightforward. While the large-cap PE ratio of 22 is only slightly above the long-term average, suggesting that it’s not wildly overvalued, mid-caps and small-caps do seem to be on the higher side. However, we’ve seen far crazier phases in the past.

One crucial thing to remember is that you can’t time markets based on valuations alone. Markets can remain overvalued for extended periods—sometimes even decades. A classic example is the U.S. market, where people have been calling for a crash since 2010 due to perceived overvaluation. Yet, the market has continued to climb, defying those predictions.

How to think about valuations

Valuations shouldn’t be used as a timing tool but rather as a way to gauge future expectations. If you’re investing when valuations are low, your future returns are likely to be higher. Conversely, investing when valuations are high might lead to lower returns. However, unless your day job is being a full-time investor, overvaluations shouldn’t keep you up at night.

The best strategy is to maintain a balanced asset allocation across equities, debt, and gold—one that allows you to sleep well at night. If you’re investing with a long-term horizon of 20-30 years, whether the markets are overvalued today shouldn’t matter much. Over multiple market cycles, things tend to balance out. But if you’re chasing after new fund offers (NFOs), small-cap stocks, or speculative investments, you’re likely to get burned when the market corrects.

So, while the talk of overvaluation is legitimate, it’s not a reason to panic. Stick to a sensible investment strategy, diversify your portfolio, and don’t get caught up in trying to time the market. Markets will go through cycles, and it’s important to stay focused on your long-term goals rather than getting swayed by short-term noise.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

If you have any feedback do let us know in the comments.

That’s something I’ve been looking for a while, an everyday brief

Good article