This Man Holds America’s Economic Future

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Scott Bessent vs. the World

The Return of (Potentially) Higher Inflation and Its Impact on Banks

Scott Bessent vs. the World

If you care about the world of money, Scott Bessent is one name you should know. He might be one of the most important figures in all of global finance — at least for the next four years.

See, Scott Bessent is America’s new Treasury Secretary.

The Treasury is the financial nerve center of America’s federal government. It’s responsible for managing America’s debt, overseeing tax collection, and ensuring the stability of its financial system. It’s how the American government managed its money, its debts, and its overall economic policy. The Treasury Secretary, as the head of the Treasury, is one of the most powerful economic policymakers in the world.

Scott Bessent is an interesting pick for the role — and is quite unlike many of Trump’s other appointees. He’s a veteran Wall Street investor who used to teach economic history at Yale. He’s a protégé of George Soros. Before getting behind Trump, he had donated money to the campaigns of Barack Obama and Hillary Clinton. Simply put, he’s an unexpected but well-qualified choice for a very crucial role.

This is why we’re deeply interested in how Bessent thinks. Not only will he be one of the world’s most important economic figures over the next few years, he’s also likely to give you some of the most cogent, well-considered statements of economic policy of anyone in the American federal government.

After taking office, Bessent gave two interviews to Bloomberg. We’re looking at them closely. We aren’t particularly interested in the overtly political parts of what he says — there’s plenty of that on the internet already. We’re just curious about how he’s looking at the economy, now that he’s in office. Here are the bits that leaped out to us the most.

One: The debt duration dilemma

One of Bessent’s biggest gripes, before he stepped into office, was against the Treasury’s approach to debt issuance. He believed that his predecessor, Janet Yellen, had “shortened” the duration of U.S. government debt.

See, when you lend money to the government, you’re particularly interested in the tenure for which you’re doing so. The longer the duration, the more likely it is that things will go wrong. So people generally want a higher interest rate when they’re buying long-term bonds.

Before taking office, Bessent argued that the Treasury was purposefully issuing more short-term bonds (which matured in a few weeks, or at most, a couple of years) than long-term ones (which matured in ten years or more). This allowed the American government to take on cheaper debt. But there’s a flip side: long-term bonds have stable interest, while the cost of short-term bonds depends on what’s happening immediately. In essence, Bessent complained, the American government was compromising the stability of its financing to make it cheaper.

Once in office, though, changing track seems to have become harder. Bloomberg pressed him on this, and his reply was non-committal:

“The previous administration shortened some of the duration, and we have not shortened it further, we have just kept the policy in place,” he said.

Here’s the thing: Bessent knows that increasing the maturity of U.S. debt — locking in longer-term rates — only makes sense if borrowing costs aren’t excessively high. That isn’t the case today. He’s waiting for inflation to come down, and for the Federal Reserve to sell off the long-term bonds they’re holding. (Why they’re holding bonds in the first place is a separate, long discussion, but this link should give you a primer.) And that will only happen if other policies — DOGE in particular — work out.

Why should you care? See, such decisions matter far beyond Washington. The price at which the United States borrows money, in a sense, sets the price of borrowing for the rest of the world. If Bessent were to suddenly flood the market with lots of expensive long-term debt, that would suck in money from investors everywhere, and raise borrowing costs worldwide. Not only would it make borrowing expensive for India, it would also put further pressure on the Rupee.

Two: Can America cut costs while giving tax breaks?

The American government is running a huge fiscal deficit. Last year, that touched 8% — the third highest on record.

So, what should it do? Bessent seems to have his hopes pinned on DOGE — Elon Musk’s (in)famous ‘Department of Government Efficiency.’

DOGE is, at least to its supporters, an attempt to cut waste and unnecessary spending across America’s federal government. The idea is simple: if the government can cut down what it spends, it can reduce the deficit. The way Bessent puts it, every $300 billion saved through DOGE can be put back into the economy. Cutting these costs is particularly important for anything to work — because Trump also wants to announce major tax cuts, which could put even more strain on the government’s finances. In his words:

“One way to think about this is, 25% of the U.S. economy flows through Washington, D.C.. So, if we can cut the friction on that, you know, that is a lot of savings.”

Interestingly, he pointed to there being more fraud in the US government than people realized, and flagged it as something to watch out for in the coming weeks. If we’re hearing this right, we should soon expect some corruption allegations coming out of the American government.

Many people have voiced doubts about how effective DOGE can be. Previous governments have tried to cut costs too, and often, they’ve failed to deliver. Some people have also pointed to the chaotic way that Elon Musk is going about the task of cutting spending — he’s getting into the Treasury’s pipelines and looking at how payments flow. This can potentially break people’s trust in the government, causing serious issues.

But that’s where Bessent makes a very interesting comment. He says that the Treasury’s approach is to “move deliberately and fix things.” This is a pointed contrast to the ethos of “move fast and break things,” the famous Silicon Valley mantra — which might be a reference to Musk’s approach.

Either way, this is a big bet, and things need not pan out as he hopes. We’ll keep watching the deficit question closely.

Three: The “strong Dollar” policy

As we’ve often mentioned here, Trump wants to bring down American imports and boost exports.

A big obstacle in this project is the exchange rate. When your currency is expensive, everything your economy makes is expensive to anyone outside your country. Now, the Dollar is the world’s reserve currency — and there’s always a very high demand for Dollars. This keeps its price up. While this means people are always looking to invest in America, it also means that America is at a natural disadvantage when it comes to exports.

So, the big question is: should America adopt policies that weaken the Dollar?

Bessent answers the question firmly: “Make no mistake, the U.S. still has a strong dollar policy.”

So, how does he manage that, even while American manufacturing increases? Bessent thinks there’s room for him to pursue both. His argument is that Trump can remove all the other barriers to American growth — by cutting regulation, cutting taxes, and running the economy well. This, along with leaps in technology, will help Americans manufacture more. At the same time, it will also give America more credibility. That will also boost investors’ confidence in America, keeping its currency strong.

That said, there’s a geopolitical edge to his statements. He distinguishes between the Dollar being strong, and other countries artificially weakening their own currencies, as he accuses China of doing. This isn’t new — Donald Trump would routinely call China a “currency manipulator” in his first term. In Bessent’s words:

“China is the most unbalanced economy in the history of the world. They are in a deep recession right now. They are experiencing deflation, and they are trying to export their way out of that. We cannot allow that. We want fair trade.”

Here’s the upshot: in Bessent’s telling, America will not move too far from its current policies around the Dollar. At the same time, it will put pressure on other countries, which it views as playing unfair. We’ll be looking out for how this plays out in practice.

Four: The inflation question

How should America look at its sticky inflation problem? After all, the latest readings indicate that inflation is higher than expected.

Bessent, however, does not seem too worried. He terms the current inflation trend “residual Biden-flation” and offers a theory: because Biden’s government spent a lot of money, it created high demand in the economy—causing a “demand shock.” At the same time, he imposed an unacceptably high degree of regulation, preventing businesses from stepping in to meet this demand. It was this mismatch between demand and supply that sent prices up.

Bessent is betting that Trump’s policies — deregulation, cheaper energy, and government efficiency — will let businesses supply things much more easily. Therefore, even if he cuts taxes — which will put more money in people’s pockets — that will not lead to inflation.

There’s one major reason that most people think otherwise: tariffs. Tariffs are basically a tax on anything imported from abroad. And because taxes are usually passed on to people — the way you and I pay GST when we buy food, for instance — that should make things expensive. When Bloomberg pressed this point, however, Bessent dismissed it.

He was careful in what he said. When you read between the lines, he does admit that tariffs could lead to price rises in the short term. In his words, “We could have a small one-time price adjustment, as we saw in Trump 1.0.” He simply believes that, with everything else that Trump does, prices will fall to a level where things will work themselves out.

Reading between the lines: What’s Bessent really thinking

Bessent clearly has a sharp sense of what he’s doing. Early on in one of his interviews, he calls himself “the nation's top bond salesman”. It’s his job to sell a rosy picture of how good America’s economy is. And he does that competently.

But this stance is based on many big bets — which may or may not play out as he hopes. His biggest bet is that DOGE will work out as intended, and will lead to a series of benefits: lower expenditures for the government, a better business environment, and cheaper things for the average citizen. More generally, he’s betting that Trump’s leadership will improve America’s economy to a degree where he’ll have a lot more breathing room to make moves. A lot of his predictions are based on these things playing out exactly as intended.

He’s more cautious in his actions, though. Despite loud critiques last year, he’s currently following in the footsteps of his predecessor. He’s careful when commenting on interest rates, and seems to be pushing for prudent debt policies. This is quite unlike many of his new colleagues.

We aren’t sure if things will play out as he hopes, or if they’ll collide with economic reality. Either way, we’ll be watching closely.

The Return of (Potentially) Higher Inflation and Its Impact on Banks

Just a couple of years back—around 2022 and 2023—many economies faced some of the highest inflation levels they had seen in decades. Central banks worldwide scrambled to hike interest rates in response, trying to counter these price pressures. Thankfully, inflation in many countries has inched down from those peaks.

But here’s the catch: Some respected economists, including Louis-Vincent Gave (who often discusses macro trends), are suggesting that the era of low, near-zero interest rates that many of us took for granted before COVID struck might now be gone for good. Instead, we may be poised for a longer period of elevated inflation.

Why might that be? Well, there are several structural factors at play: globalisation is going out of fashion, commodities are getting expensive as different countries fight, the green transition is changing the entire infrastructure powering our economy, and the so-called “peace dividend,” the economic benefits of world peace, is dying down.

In other words, there are big-picture forces that are pushing inflation (and, by extension, interest rates) up for longer. Of course, predicting the future of inflation is notoriously difficult, but we should be prepared if these predictions of recurring bouts of high inflation prove accurate.

Here’s one thing to be worried about: as the IMF recently noted, high interest rates could be bad news for banks.

High Inflation Usually Means Higher Interest Rates

When inflation rises, central banks usually respond by raising their policy rates. Why? The straightforward textbook logic is that borrowing costs are higher, and people are more careful with their money. If loans become more expensive, people and businesses tend to cut back on spending, and that in turn can help bring prices under control. In a high-inflation scenario:

Central banks increase policy rates to contain price growth.

Commercial banks follow suit, raising their lending rates for mortgages, business loans, etc.

Overall interest rates in the economy drift higher—from government bond yields to corporate lending rates.

But while higher rates might be a useful tool to battle inflation, it’s rarely that simple. As we’ll see, moving from extremely low rates to suddenly higher ones can shake up the banking system in ways policy-makers don’t always intend.

The Unintended Consequences for Banks

Here’s a quick refresher on how banks make money:

Banks typically take deposits (i.e., money you and I keep in checking or savings) and lend them out at higher interest rates (think mortgages, corporate loans, etc.). Their profit is essentially the difference between the two: i.e. interest income, or the money they earn from loans and investments, and interest expense, i.e. the money they pay depositors.

In the IMF’s Staff Discussion Notes, researchers explored how rising inflation and interest rates affect these dynamics. The gist is that, while banks’ gross exposures to inflation can be large — because all the money they’re dealing with gets re-priced because of inflation — their net exposure often remains relatively balanced. For most banks:

Income goes up as loans, government bond yields, and other assets adjust to higher interest rates.

Expenses also go up when deposit rates and other costs (like wages or technology investments) eventually catch up.

The end result? The average bank does not see a dramatic net profit boost or bust just because of inflation. Indeed, the IMF found that, in a wide sample of banks, most manage to match their assets and liabilities pretty effectively against inflation.

But — and this is a big ‘but’ — there are outliers.

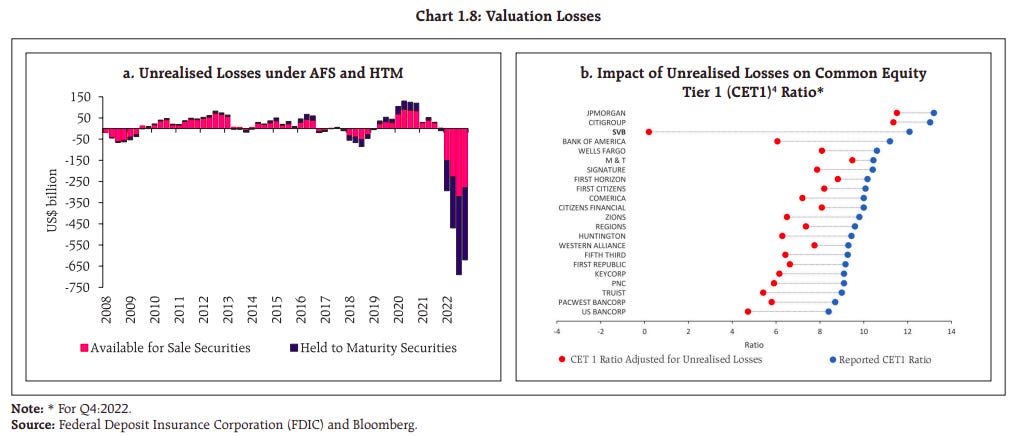

According to the same IMF study, about 5 percent of advanced economy banks and roughly 8 percent of emerging market banks are significantly more vulnerable to a shift in inflation and interest rates. Even more strikingly, 3 percent of banks in advanced economies and 6 percent in emerging markets were found to be at least as exposed as Silicon Valley Bank (SVB) was in early 2023.

This basically means that if interest rates and deposit flight converge in the wrong way, all these banks could see the sort of trouble that Silicon Valley Bank did.

When It All Goes Wrong: The SVB Case

In case you’re wondering, here’s what happened with Silicon Valley Bank (SVB) during the 2023 banking crisis.

Back then, inflation in the U.S. had climbed quickly. In response, the U.S. Federal Reserve aggressively raised interest rates in a short span. Now, many banks hold government bonds or long-dated securities in “Held to Maturity” (HTM) portfolios. Normally, HTM investments aren’t ‘marked to market’ — i.e., banks don’t have to reflect the paper losses in their daily profit calculations if they don’t plan to sell the bonds early.

But even if they don’t account for losses, as interest rates rise, the market value of older, low-interest bonds falls — since there are now more lucrative versions of the same bond out there. This is where SVB’s problems came in.

SVB had large amounts of long-dated assets locked in at lower yields. Unfortunately for them, as the private funding to their tech-company clients dried up, their deposits started flowing out. To pay for these outflows, the bank had to sell some of these long-dated securities. Only, for that, they had to stomach a steep loss. That wiped out a big chunk of its equity.

This suddenly triggered a classic run on the bank. Data shows these hits to SVB’s Common Equity Tier 1 (CET1) ratio shrinking from 12% to 0%, showing large notional losses that became real once the bank had to sell at depressed prices.

So, while many banks weathered 2023’s rate hikes just fine, outliers like SVB ended up with crippling losses. And it wasn’t alone: The events of 2023 have been dubbed the most significant banking turmoil since 2008. All of this goes to show: that risk management failures can suddenly blow up entire banks in an environment of fast-rising rates.

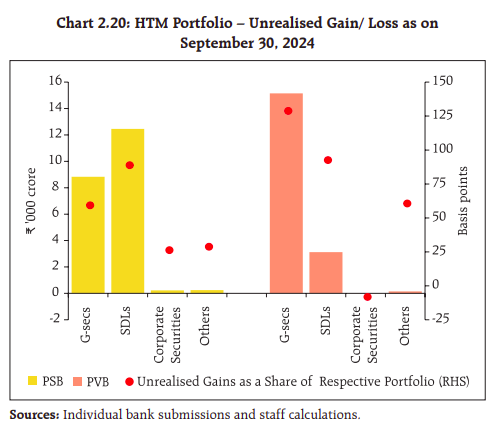

Could This Happen in India?

People naturally wonder if the Indian banking system is vulnerable to a similar meltdown. Let’s look at a few highlights:

Current HTM Portfolio Status: Based on the RBI data, Indian banks as a whole were sitting on unrealized gains in HTM portfolios as of September 2024. That’s a big plus because it means that the fair value of many Indian banks’ bond holdings is above their cost, not below.

Source: RBI Investment Fluctuation Reserve (IFR): The Reserve Bank of India (RBI) mandates that banks set aside money into an ‘IFR’ to cushion against unexpected yield movements. According to reports, Indian banks collectively have a decent IFR, which helps absorb mark-to-market losses when rates shift quickly. But that data is from December 2022, and we couldn’t get our hands on the latest data.

Sticky, Retail-Focused Deposits: India’s banking sector relies heavily on retail deposits, and not so much on a concentrated set of commercial or tech-driven customers. Reports highlight that around 60% of deposits come from smaller retail accounts, meaning deposit flight risk is historically lower since retail depositors often keep money parked for the long term.

Regulatory Scrutiny: The RBI is known to keep a relatively close watch on all banks, regardless of their size. The RBI does regular stress testing and imposes uniform liquidity and capital standards. That uniform approach can reduce the chance of an SVB-like blind spot.

All that said, it doesn’t mean the risk is zero. Previously, the RBI set a limit on how large banks’ HTM holdings could be, as a percentage of total investments. According to a Business Standard article, that 23% upper cap has now been removed. With no explicit limit, banks could load up on more long-duration securities.

In a high-rate scenario, that might make them more vulnerable to the same phenomenon that afflicted SVB, especially if (for instance) depositors decide to move their money quickly.

Mind the Maturity: The Role of ALM

Ultimately, the main lesson—and one that has been stressed in a speech by our Deputy Governor of RBI Mr. Rajeshwar Rao —is the importance of a solid asset-liability management (ALM) framework. That is, banks should structure their operations in a way where the profile of what they’ve lent broadly matches what they owe.

If banks hold mostly short-term deposits but invest in very long-term, fixed-rate bonds, they are exposed to a mismatch. When rates rise, the costs of their deposit can climb faster than the income from old bond investments, or the bank might be forced to sell those bonds at a loss.

Of course, it’s not that holding bonds is bad, nor is it that high inflation automatically dooms banks. But prudent ALM ensures that a bank doesn’t get caught paying higher deposit rates (or suffering deposit withdrawals) while stuck with massive losses in long-dated assets.

Wrapping Up

Summing it all up:

We might be back in a world of higher inflation where central banks won’t snap back to ultra-low rates anytime soon.

Higher inflation typically means higher rates, and banks need strong risk management to handle that.

Most banks match income and expenses well, so net profit swings shouldn’t be dramatic.

But outliers exist, as the 2023 banking crisis (especially SVB) exemplified. The speed of rate hikes and deposit runs can cause a major mishap if banks aren’t paying close attention to how they structure their investments.

In India, several factors reduce the chance of an SVB replay—like IFR buffers, robust regulation, and a large retail deposit base. However, removing a rigid ceiling on HTM holdings could introduce new risks if banks load up on long maturities without good ALM practices.

As always, it boils down to whether or not banks strike the right balance between seizing profitable opportunities (e.g., investing in higher-yielding government securities) and keeping enough liquidity on hand to serve their depositors—even when conditions suddenly change. If SVB’s troubles taught us anything, it’s that focusing on short-term profitability at the expense of prudent, long-term risk management can land you in a world of trouble when inflation—and interest rates—go in directions you hadn’t bargained for.

Tidbits

In Q3FY25, listed private nonfinancial companies posted an 8% increase in sales, up from 5.5% in the corresponding quarter a year ago and 5.4% in Q2FY25. Operating profit margins rose by 50 basis points to 16.2%, reflecting improved efficiency across the sector. Among 1,675 listed private manufacturing companies, sales grew by 7.7%, driven by higher performance in automobiles, chemicals, food products, and electrical machinery. IT companies recorded a 6.8% year-on-year increase in sales, while non-IT services companies achieved an 11.5% growth. Manufacturing firms saw a 6.3% rise in raw material expenses accompanied by a 9.5% increase in staff costs, with IT and non-IT services reporting staff cost increases of 5.0% and 12.4% respectively.

The Reserve Bank of India has revised norms for urban co-operative banks by allowing them to classify loans up to 25 Lakh rupees or 0.4% of Tier I capital, whichever is higher, as small-value loans. The ceiling per borrower has been raised from 1 crore rupees to 3 crore rupees. The new measures also increase the aggregate exposure limit for residential mortgages to 25% of total loans and advances. Exposure to non-housing real estate remains capped at 5% of total loans. Revised individual housing loan limits now range between 60 Lakh and 3 crore rupees depending on the bank tier.

Tata Communications issued commercial papers aggregating to ₹465 crore on February 21, with each security carrying a face value of ₹5 lakh. The securities are set for redemption on May 23, 2025, and they were listed on the National Stock Exchange of India on February 24, 2025. The commercial papers come with an annual discount of 7.47 percent, as detailed in the regulatory filing. This structured issuance underscores the company’s precise approach to short-term funding and liquidity management.

- This edition of the newsletter was written by Pranav and Kashish

🌱Have you checked out One Thing We Learned?

It's a new side-project by our writing team, and even if we say so ourselves, it's fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That's all. It's chaotic, it's unpolished - but it's honest.

So far, we've written about everything from India's state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you're looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉