There’s nothing straight about Hormuz

And a promise of liquidity for small businesses

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

To turn the Strait of Hormuz boring again

India steps in with a credit guarantee for MSMEs

To turn the Strait of Hormuz boring again

As recently as late February, the Strait of Hormuz was boring enough that you could afford to know nothing about it. It was a peculiarity; something that shipping nerds made up “what if?” scenarios around, but you could safely afford to ignore. It was, ultimately, just a routine fact of international trade.

Then, the war broke out, and briefly, it became the most important 33 kilometer stretch in the world.

It was better off as an afterthought. Back then, hundreds of ships could pass it every single day, carrying a massive share of the world’s energy, and it wouldn’t make a single headline. Ports planned their schedules weeks in advance. Insurers — private entities whose very job was to study risk — barely saw any. Just months ago, war-risk insurance for a Gulf voyage cost a quarter of a percent of your vessel’s insured value — a rounding error. It all ran like clockwork.

That boring normalcy was earnt over decades. It took a week to break. As soon as the conflict between the United States and Iran escalated, transits collapsed — from 141 a day to as few as three to six — a 97% drop. Major insurers stopped underwriting war risk in the Gulf. Hundreds of ships found themselves stranded inside. Oil wells shut down.

It took till last week for the nightmare to end, when the warring parties reached a memorandum of understanding to wind down hostilities. The world breathed a collective sigh of relief. The price of Brent crude fell to roughly $79 a barrel, from highs of over $110.

Sadly, however, the Strait won’t return to normal merely because of a political agreement. Of course, ships will resume moving through it once again. For the chokepoint to return to being a boring detail, however, we will have to rebuild a long chain — running from oil infrastructure, to terminals, to financial institutions, to markets — that was shattered link-by-link in the war.

Normalcy is still many months away.

Two lanes through a mined strait

Before the breakdown, shipping lanes used to run through the centre of the Strait of Hormuz. There used to be two separate traffic corridors that ran through it, governed by international maritime convention.

Over the war, however, Iran laid sea mines across both lanes, rendering them un-navigable. They’ve become too dangerous, now, for commercial traffic to pass through.

At the moment, ships are improvising around them. Two new lanes have spontaneously emerged. There’s one along the northern edge, close to Iranian waters. Here, ships pass through with their tracking signals on, implicitly vetted by Iran. There’s another lane at the other end, hugging Oman’s southern coast. Here, ships try to sneak through with lights and transponders off, guided by American naval forces.

Neither is “normal”. They are compromises, forced by necessity.

Many ships decided not to attempt crossing the Strait at all, given the dangers involved. Over the war, roughly 500 ships stayed stranded inside. Over those idle months in the warm waters of the Gulf, many of them were probably encrusted with barnacles and other marine life, damaging their systems, and compromising their speed and safety. Before they can exit the Strait, they’ll have to be repaired and re-provisioned. That alone will take time.

Even so, the first stranded ships have reportedly begun to exit the Strait. Reporting from the days around the deal described four supertankers emerging outside the strait, which together carry roughly eight million barrels of oil. Clearly, it’s possible to transit the Strait.

The real test of whether people trust the truce enough to resume trade, however, is whether ships start going back in to pick up fresh cargoes. We’re yet to see that happen at scale.

Even if the peace holds, and ships return to the Gulf, normalcy won’t return until the mines are cleared. That won’t be easy; removing mines is far harder than placing them. To make things worse, Iran claims to have lost track of the mines it placed in the Strait. Over the next few months, special naval vessels will slowly sweep the entire region, examining every inch of seabed with sonar detectors. Divers and undersea drones will examine every single abnormality it pings — whether it’s a mine, or something else, like a rock, or debris. This entire process will repeat again and again until shipowners and insurers will trust that the corridor is safe. According to the commodities data firm Kpler, this will take at least six months.

There are more problems still that we can’t go into here, such as mass confusion caused by signal spoofing all across the Strait. Trust, simply put, will take a while to rebuild.

That lack of trust comes with commercial implications.

Specifically, it blocks access to insurance. In early March, five of the world’s biggest ship insurers — Gard, Skuld, NorthStandard, the London P&I Club and the American Club — stopped covering war risks in the Gulf. Those insurers might have returned to the market since, but as long as the risks of transit are high, they’ll charge far higher premiums than they did. After all, this coverage isn’t meant for all-out war alone, but for stray incidents — like a ship colliding with a stray mine, or a bad actor attacking it with a single improvised drone. Even if full-scale hostilities have come down, these risks remain.

This is why, since hostilities broke out, war-risk premiums for the Strait went up from 0.25% of a ship’s cargo to as much as 8%. A single ship, for a single voyage, might have to pay as much as $8 million to insurers alone.

If you’re planning a voyage to the Gulf, you either pay through your nose for insurance, or put your ship — something that can cost hundreds of millions of dollars — at risk. Even with these costs, some voyages may well make sense. But it’ll be a long time before going to the Gulf is a matter of routine.

Resuming oilfields

Even if shipping could return to the Gulf, there’s another issue: the flow of oil, having stopped, may be difficult to resume again.

When the Strait closed, and terminals were filled to capacity (or damaged in strikes), many countries were forced to shut their oil wells. This wasn’t uniform across countries — the oilwells of Saudi Arabia, for instance, never fully shut down, because they could keep pushing oil out of its ports to the West, in the Red Sea. But other countries, like Iraq, didn’t have that option. Without a way to bypass the Strait, they had to cut production and shut their wells.

Sadly, it’s easier to shut production than to restart it.

Oil wells work best when they’re running constantly. Pause production, and they quickly deteriorate. Idle equipment can erode quickly. Water can enter zones that once contained oil. Heavy components in the oil — like waxes or asphaltenes — can congeal inside the well or in the rock around it, creating blockages. Some Iraqi oilfields, for instance, are reportedly clogged with paraffin.

Moreover, many wells only keep gushing oil because we inject water into them, creating pressure that pushes the oil out. Shut that injection, and the pressure drops. Sometimes, that pressure is the only reason those underground reservoirs of oil are intact. Once it drops, they can collapse physically.

And so, before you can restart an oil well, you must test each well’s integrity, clearing blockages, re-establishing pressure. You need to do so well-by-well, separately assessing the state each is in. The longer a field sits idle, the harder this gets. By some estimates, it could be over a year before production resumes at full capacity.

The tollbooth

All of this assumes that things will return to some version of normal. There’s no guarantee that things will go as planned.

We wrote this piece on Friday. Even as we wrote, new pieces of news started to trickle in: Israel’s attacks on Lebanon had put the US-Iran deal under strain once again. While the ceasefire hasn’t collapsed yet, it may well have by the time you see this.

Even if the worst doesn’t come to pass, however, it isn’t clear what arrangement the two countries shall come to once the ceasefire kicks in.

Reports suggest, for instance, that Iran has demanded the right to collect fees from transiting ships. In fact, it already exacted payment from some vessels during the crisis. It’s unclear how long such an arrangement can last, or what its legal sanctity shall be. Under the United Nations Convention on the Law of the Sea, no country can suspend transit passage through an international strait. What sanctity, then, does such an arrangement have? Does the United States even have the authority to grant Iran such an accommodation unilaterally?

There are even trickier legal questions in the way. For instance, both the United States and the European Union have previously designated Iran’s Islamic Revolutionary Guard Corps, or IRGC, a terrorist organisation. That is the entity that, Iran proposes, will collect such a toll. Legally, however, paying a toll to the IRGC can open a shipping company, and its banks, to sanctions. Even if the Strait is physically open, unless there is legal clarity, many companies might avoid the route.

And most importantly, there’s a dark implication to such an arrangement: if the IRGC is permitted to charge tolls on the Strait, does it come with an implicit threat of violence? If payments don’t go through, or if there is some disagreement between a shipper and the IRGC, is there a risk that Iran might physically attack that ship?

At the moment, there is no clarity on any of these questions.

There is considerable repair work involved in turning the Strait of Hormuz into something boring yet again. Everything we’ve discussed here — resurrecting oil wells, fixing insurance, removing mines — needs serious amounts of time and capital. If the business case is strong enough, that time and capital can be found. But for that, one needs clarity.

Without clarity, nothing else falls in place. It makes no sense to repair an oil well if there’s a risk it will shut down again in a few months. No insurer shall offer war insurance if there’s a threat that Iran will attack any ship that doesn’t offer it a toll. You cannot have a months-long mine removal operation if the parties involved don’t see eye-to-eye.

There’s nothing straight about Hormuz

Chances are, sooner or later, a reasonable number of ships will start transiting in and out of the Strait of Hormuz. Some of the worst effects of the war — such as India’s LPG procurement crisis — could well be behind us.

That is different from things returning to normal, however. Before March, the Strait of Hormuz used to be a boring passageway. Lately, however, that boredom feels like a luxury. If everything goes to plan, from here, it shall be many months before it returns. If it doesn’t, we may live in a permanently altered world.

A working artery is a boring detail. A choked one is a catastrophe. That is true of our own bodies. It is equally true of the world economy.

India steps in with a credit guarantee for MSMEs

Picture yourself running a business. Your order book is healthy, your machines are running, and your customers still want what you make. And yet you’re suddenly in trouble because of something happening 2000 kilometres away, in a part of the world you have no control over.

A conflict has broken out in West Asia. Almost overnight, the cost of shipping your goods has jumped. The insurance premium on your cargo has spiked. The crude-linked raw material you import has gotten dearer. Your overseas buyers, spooked by the uncertainty, are paying you later than they used to. None of this is your fault, and none of it touches the long-term health of your business.

But it has opened up a hole in one specific place: your working capital. You just need some cash immediately to get across the gap — making payroll, paying suppliers, keeping the lights on — until the storm passes.

Unfortunately, the moment you need money the most is also when it becomes hardest to find. When everyone is nervous, banks get nervous too. They look at a stressed sector, see a borrower who suddenly looks risky, and they pull their hands back into their pockets.

So who steps in? The government does, with what’s called a credit guarantee scheme. And in May this year, India pulled out its favourite version of one and switched it back on.

That’s what we want to talk about today.

The government as your cosigner

Let’s start with what a credit guarantee actually is, because it often gets confused with “government-backed loans“, which it most definitely is not.

The government does not give you the money. Your bank does, out of its own pocket. What the government does is stand behind that loan as co-signer. It tells the bank: go ahead and lend; if this borrower defaults, we’ll cover the loss up to an agreed share. The bank feels better because now the downside of lending to a shaky borrower is shared with someone else, and so it lends where it otherwise wouldn’t. It’s worth noting that this guarantee makes the lender safer, but not the borrower — the small business, which can still fail.

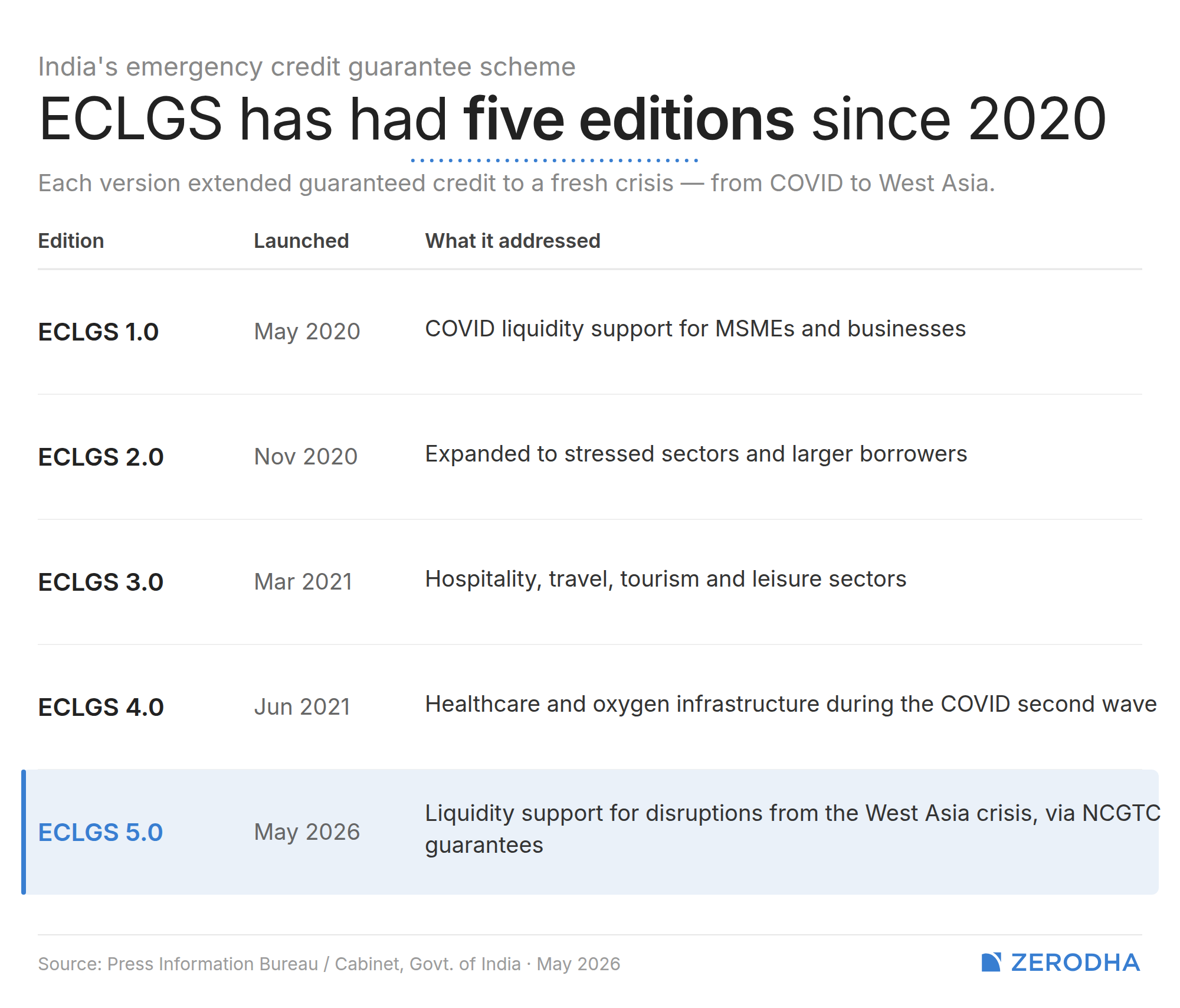

The scheme doing this right now is the Emergency Credit Line Guarantee Scheme (ECLGS), and the version the Cabinet cleared in May is its fifth version. It carries a headline figure of ₹2.55 lakh crore of additional credit open till March 2027. The guarantee is issued by a government-owned trustee company called the National Credit Guarantee Trustee Company (NCGTC).

NCGTC, the body issuing the guarantee, runs a whole shelf of such interventions for exporters, for startups, for microfinance lenders, for skilling loans, and so on. Sitting alongside it is an older, more permanent institution: the Credit Guarantee Fund Trust for Micro and Small Enterprises, or CGTMSE, set up back in 2000 to coax banks into lending to small firms without collateral.

Now, ECLGS wasn’t tailor-made for this crisis, but for the last one.

It was launched in May 2020, in the worst weeks of the COVID lockdowns, as the centrepiece of the Aatmanirbhar Bharat package. Millions of small businesses were subject to an unpredictable, brutal liquidity shock, and banks didn’t want to lend another rupee in this uncertainty. So the government stepped in.

That made ECLGS a countercyclical credit tool. It tried to prevent a liquidity crisis from becoming an insolvency crisis. And it kept mutating to chase the pandemic around the economy.

The first version was a blunt, broad instrument, under which any eligible MSME could borrow an extra 20% of its outstanding credit. By late 2020, version 2.0 widened the net to 26 stressed sectors, and to bigger borrowers. Version 3.0, in early 2021, went after the businesses that just wouldn’t recover — hospitality, travel, tourism, aviation — and let them borrow far more. By the time the scheme formally closed in March 2023, the government had issued guarantees backing roughly ₹3.6 lakh crore of loans across nearly 1.2 crore borrowers.

Then, three years later, amid a war rattling oil prices and trade routes, the government reached for the same tool again.

Why your bank loves this

But there’s more to why a bank loves this arrangement.

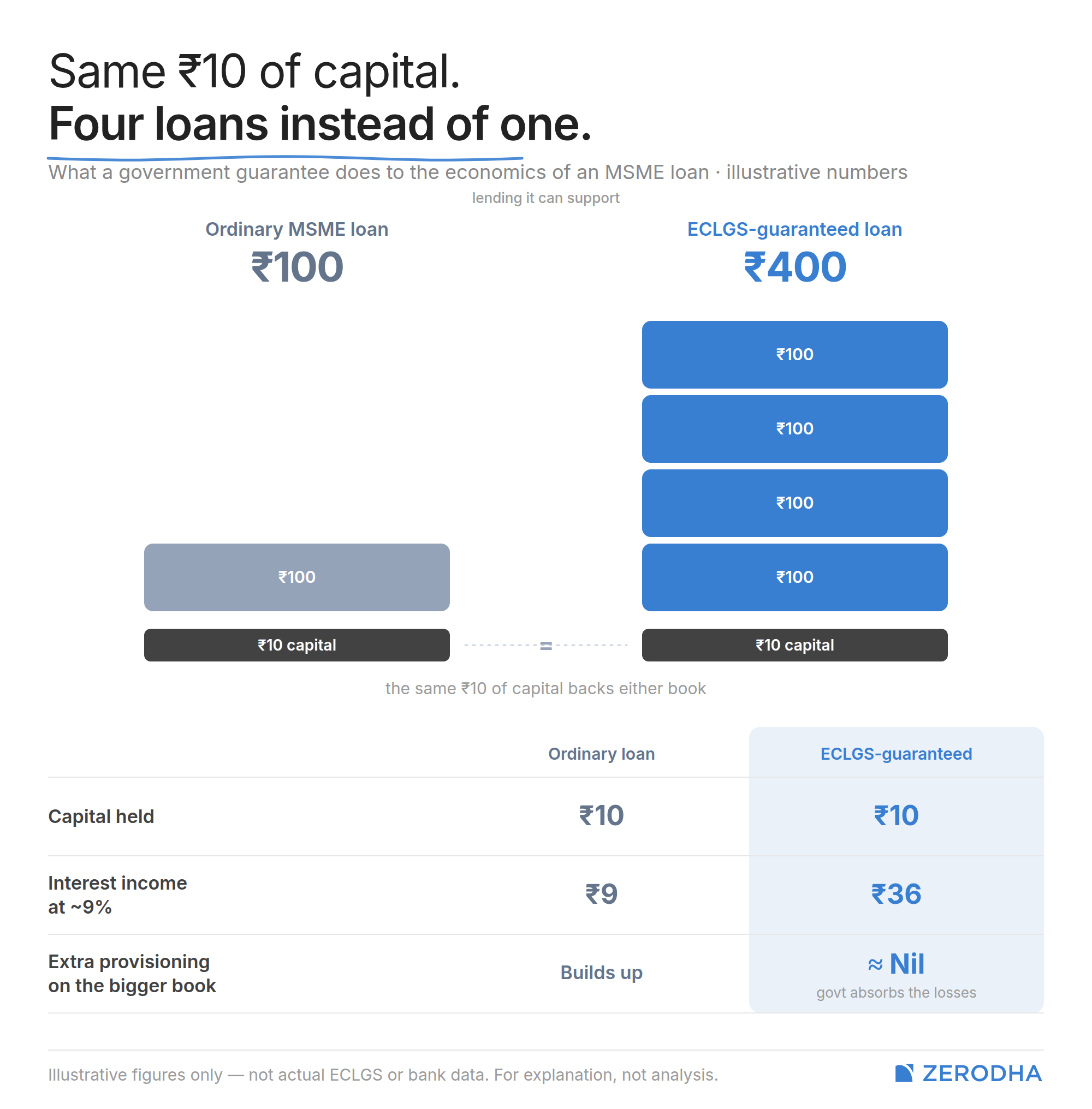

See, banks don’t lend freely even when they want to. For every loan they make, regulators force them to park a cushion of their own capital against the chance it goes bad — the riskier the loan, the bigger the buffer the regulator requires be set aside. That means, for the same capital that the bank holds, it can give out a lower number of risky loans, but a higher volume of safe loans. This risk cushion is a large constraint on how much a bank can lend.

But a government-guaranteed loan breaks that constraint.

If the state is covering your losses, the loan is barely risky from the bank’s point of view, so it needs almost no capital cushion. The RBI made this explicit for ECLGS 5.0: banks can treat 75% of the guaranteed portion as effectively risk-free, holding zero capital against it. So the guarantee does two things at once. It removes the default risk, and it frees up the capital the bank would otherwise have to lock away. The bank earns its interest, takes almost no risk, and ties up almost no capital. From a lender’s chair, that’s about as good as lending gets.

Let’s put some round numbers on it. Say a bank lends ₹100 to a small business the ordinary way. Regulators make it set aside about ₹10 of its own capital against that loan, in case it sours. So ₹100 of lending locks up ₹10 of precious capital.

Now, run that same ₹100 through ECLGS. Three-quarters of it is government-guaranteed and treated as risk-free, so the bank only holds capital against the leftover sliver — call it ₹2.50 instead of ₹10. Which means the same ₹10 of buffer that once backed a single ₹100 loan can now back four guaranteed loans. That’s ₹400 of lending, off the same ₹10 buffer.

Now follow that through. The loans earn interest either way — say that’s 9%. From the perspective of capital efficiency, the same ₹10 of buffer now supports ₹400 of loans instead of ₹100. At a 9% lending rate, that means four times as much interest income (₹36 in this case) can be generated from the same buffer.

Normally, lending four times as much to small, shaky borrowers would mean bracing for four times the bad loans, which forces a bank to keep setting aside money as a buffer. But with the government absorbing the losses, the bank can expand lending without a proportionate increase in capital requirements or expected losses, and earn more interest income as well.

But there’s a subtlety here that trips up a lot of people. A guarantee does not stop a loan from being recognised as bad. If you stop paying for 90 days, your loan gets marked a non-performing asset, guaranteed or not. It only changes the size of the loss the bank ultimately bears.

That distinction created a strange optical effect during COVID. Because ECLGS pumped a huge volume of fresh loans onto bank books, the ratio of bad loans to total loans looked better than it really was, as the denominator became inflated. Banks looked healthier than their underlying borrowers actually were, which is why careful analysts learned to strip ECLGS out entirely before judging a bank’s books.

The flaw baked into the kindness

A guarantee does create an awkward incentive problem, though. If you tell a bank that the government will cover a majority of any loss, why would the bank bother to check whether the borrower is any good?

This is the oldest worry about credit guarantees, and economists have a name for it — moral hazard. When a lender has no skin in the game, it has little reason to screen borrowers carefully or chase them afterwards. In the worst case, a 100% guarantee becomes a machine for quietly shovelling bad loans off bank books and onto the state balance sheet.

ECLGS tries to fence this in. It’s only open to existing borrowers, whom the bank already knows. It’s only for accounts still classified as standard and not visibly sick. And the amount you can borrow is capped against your past working capital, so nobody can balloon their debt overnight.

But guardrails only narrow the problem; they don’t dissolve it. Which brings us to the harder truth underneath all of this. Credit guarantees solve one problem — lender reluctance — but they do not automatically solve weak borrower viability, poor underwriting, low productivity or delayed recoveries.

So… does any of this work?

Yet, the scheme has shown signs of success.

As per SBI Research, the COVID scheme saved around 13.5 lakh MSME accounts from going bad, protected roughly 1.5 crore jobs, and kept around ₹1.8 lakh crore of loans off the non-performing pile — about 14% of all MSME credit at the time.

However, these numbers should be treated with a little care. These are estimates resting on a counterfactual guess about what would have happened in the absence of this scheme. And the businesses that took the loans aren’t a random sample; with the guardrails we mentioned above, it’s likely that firms confident enough to borrow more were in better shape to begin with. The fall in MSME bad loans also owes a lot to the broader credit cycle and the bankruptcy code, not ECLGS alone.

On the other side of these optimistic estimates, the official record is blunter.

The RBI’s own Financial Stability Report found that by September 2022, roughly one in six ECLGS accounts had already turned bad, and noted dryly that distress was continuing in the MSME sector. The pain was wildly concentrated: micro enterprises took about a quarter of the loans but accounted for the overwhelming majority of the defaulting accounts. The defaults clustered in the very smallest borrowers, the exact segment the scheme was meant to rescue.

ECLGS appears to have succeeded in pushing credit quickly into the system and reducing immediate defaults. But its long-term success depends on how many borrowers ultimately repay, how much the government pays in claims, and whether the credit created real economic activity rather than merely postponing stress.

And that’s largely the story of it. The COVID book is still being settled, with the back quarter of every claim lagging by design, years after the crisis it was meant to fix. ECLGS 5.0 is, at bottom, a bet that this storm will pass before too many of these guarantees get called. Credit guarantees allow governments to mobilise vast amounts of lending without spending vast amounts of money upfront. But sooner or later, the bill comes due.

Tidbits

Xiaomi is entering India’s large home appliances market as smartphone volumes slide. The company is scouting local EMS partners to manufacture ACs, refrigerators, and washing machines in India, with newly appointed South Asia head Alex Tang — picked for his experience launching large appliances in Southeast Asia — leading the push. COO Sudhin Mathur framed it as Xiaomi’s next growth phase as Indian smartphone penetration hits the 100% mark.

Source: Economic TimesReliance New Energy has secured ARAI certification for four battery variants and three two-wheeler platforms, and will start trials within its own fleet before piloting in select cities — with a broader commercial rollout targeted by end of FY27. The programme centres on a removable lithium-ion battery pack that can power scooters, three-wheelers, and light commercial vehicles, initially targeting e-commerce and last-mile delivery fleets.

Source: Economic TimesIndia and the UK have resolved the steel quota dispute that was holding up their trade pact. The UK agreed to grant India enhanced duty-free access through country-specific quotas, residual quotas, and its Authorised Use Scheme, shielding about 85% of India’s ~$1 billion annual steel exports from Britain’s new safeguard regime kicking in July 1. The remaining 15% faces the tighter rules.

Source: The Hindu BusinessLine

- This edition of the newsletter was written by Pranav and Kashish.

Over 2 crore Indians invest with Zerodha. Open a free demat account in minutes and invest in stocks, mutual funds, ETFs, and bonds at 0 brokerage. No hidden charges, no gimmicks. Plus, get free access to research tools like Tijori, Sensibull and more.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Zohra Khan on the business of Indian EV infra

India’s EV adoption is now less dependent on the vehicles, and more everything it plugs into — the charger, the connector, the software, the protocols that charging networks use to talk to one another, and, most importantly, the ageing Indian electricity grid beneath all of it.

To make sense of all this, we spoke to Zohra Khan, founder & CEO of IPEC, which designs and manufactures EV chargers for India’s leading two- and three-wheeler OEMs, to understand what it actually takes to build charging infrastructure at scale in India. Read the key takeaways on Subtext.

Watch the full podcast episode below, where Zohra walks us through the mechanics of the EV charging industry and its impact on India’s energy transition

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Excellent review and perspective on Strait of Hormuz….the last two paragraphs are wonderful and sum it all 👍