The price of a Wavin’ Flag

Hosting the FIFA World Cup has its costs and curses.

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The price of a Wavin' Flag

India's state budgets are a mixed bag

The price of a Wavin’ Flag

It’s that time of the year where we’re playing iconic songs like Waka Waka or Wavin’ Flag.

The 2026 FIFA World Cup is currently underway across the United States, Mexico and Canada. It’s the largest tournament in the competition’s history. The FIFA World Cup is the most watched sporting event on the planet. The 2022 final between Argentina and France drew a whopping 1.5 billion viewers, a fifth of the world’s population.

That scale also enables the World Cup to become an extraordinary money machine. Nearly a billion dollars in ticket and hospitality revenue alone flowed into FIFA’s coffers that cycle. Corporate sponsors paid $1.8 billion to slap their logos across the tournament.

Yet, it rarely makes any economic sense for any country to take the burden of hosting the World Cup.

The 2026 World Cup is also the most expensive to attend. Face-value ticket prices are several times higher than in Qatar. The attorneys general of New York and New Jersey are investigating FIFA over its ticketing practices.

And yet, the host cities will likely lose money.

This is not a new problem. The economics of hosting the World Cup have almost never made sense for the host. For them, it is structurally a money-losing venture. The promise of being a host is that the World Cup will entail a massive infrastructure boom that brings in revenue over the long-term. But the actuals often fall highly short of the estimates.

Sport researcher Adam Beissel put it quite succinctly about the rosy projections made about potential tourism revenue from mega-sporting events:

“The general rule of thumb by sport economists is to move the decimal point one place to the left for all economic impact studies.”

So, why do countries keep lining up to host? The answer lies in a peculiar collision of monopoly economics, geopolitical ambition, and a bidding process so broken that it caused the worst existential crisis in FIFA’s history.

The house always wins

To understand why hosts lose money, you have to dive into FIFA’s business model. It’s as ruthlessly asymmetric as it is simple.

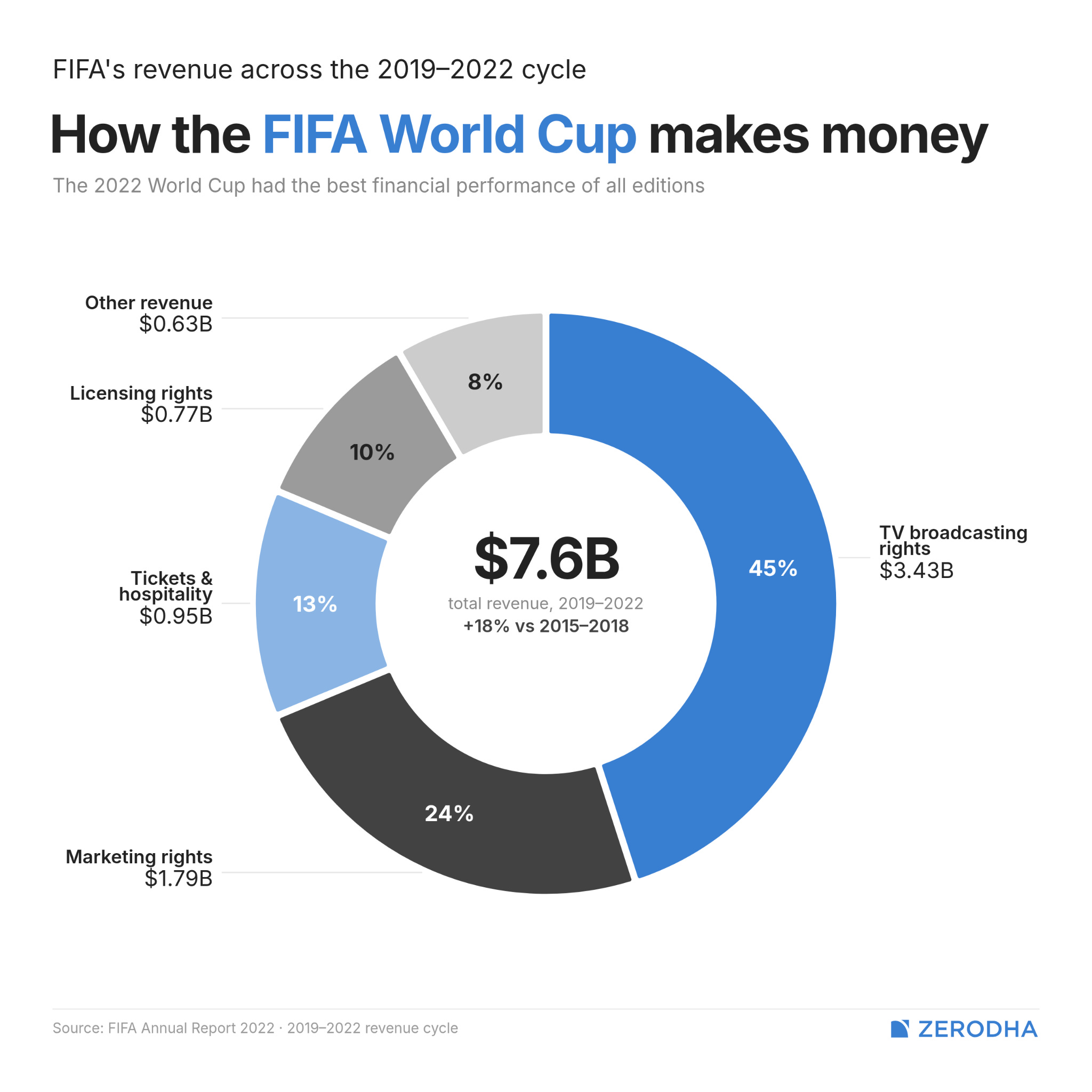

Essentially a not-for-profit organization, FIFA owns all the commercial rights to the World Cup. That means broadcasting, sponsorship, licensing, and ticketing — the four most lucrative, most scalable revenue streams the tournament generates.

In the 2019–2022 cycle, FIFA reported total revenue of ~$7.6 billion, of which $6.3 billion came from rights tied to the Qatar 2022 edition alone. Their expenses amounted to $6.3 billion, leaving them with $1.3 billion surplus.

The host country — in this case, Qatar — gets nothing from these rights directly.

What the host gets instead is the bill of building and operating new stadiums, transport upgrades, security, and events outside FIFA’s commercial perimeter. And then, the country is solely responsible for the debt raised to fund all this, and the risk of stadiums sitting empty after the event. There’s no revenue sharing based on these commercial rights.

FIFA also demands that the host surrender the ability to earn tax revenue on the World Cup. Host cities must grant a full 10-year tax exemption to FIFA, its subsidiaries, and its corporate sponsors. The areas in and around stadiums become “tax-free bubbles“ where only official FIFA partners — like Coca-Cola, Visa, and Adidas — are allowed to sell goods. Local vendors are shut out.

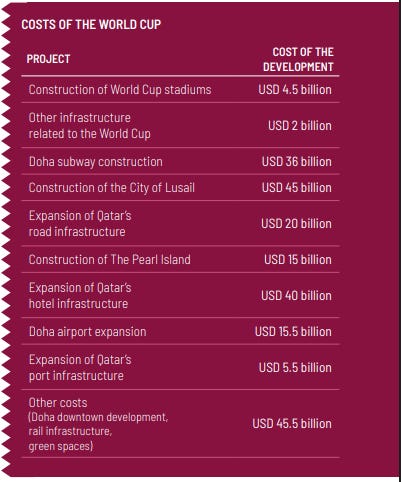

Take Qatar, which spent over $220 billion preparing for the 2022 World Cup. Most of it was on national long-term infrastructure (like airports, ports and metros) that was undertaken by using this event as justification. The IMF estimated the direct short-term economic returns from visitor spending at somewhere between $2-4 billion — less than 2% of the total investment.

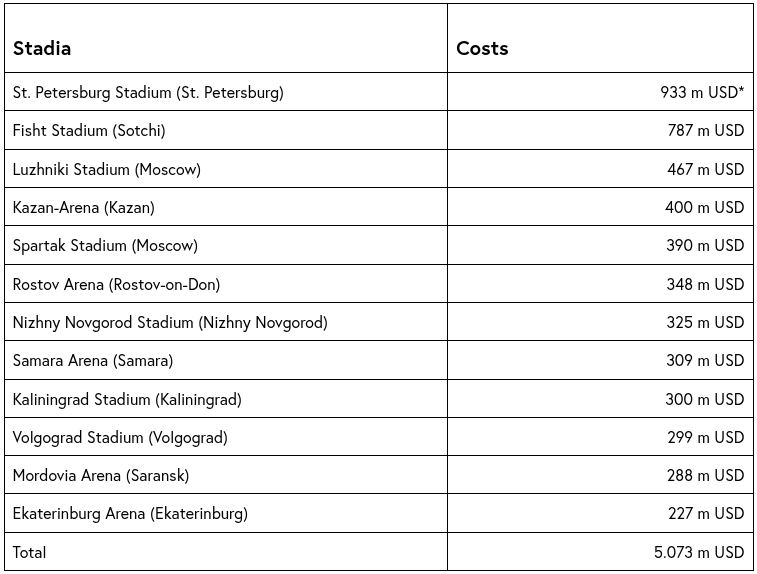

The 2018 World Cup in Russia, meanwhile, ran a smaller bill of $14-15 billion. The World Bank found a temporary lift during the tournament itself, but that eventually wore off, leading to 0% growth in the third quarter of the year.

The only promise of these massive investments are indirect spillovers from tourism, food and beverage spending, local transport use, and some temporary employment. But that often doesn’t materialize. For instance, for both South Africa and Brazil, which hosted the World Cup in 2010 and 2014 respectively, tourism spending made up only 10% or less of the total World Cup spend.

In fact, this isn’t just true for the FIFA World Cup. There’s a long documented history of mega-sporting events like the Olympics also being money burners. The actual budget for an event always overshoots the estimate. As per researchers from the University of Lausanne, four out of every five World Cup or Summer Olympics events ran budget deficits. Their average return on investment was -38%.

The geography of ambition

If the economics are so bad, why do countries keep bidding?

Because for most hosts, the World Cup is less an economic project and more a geopolitical one. The World Cup offers a month-long, wall-to-wall broadcast into every living room on the planet, with your country’s name attached. That alone is considered priceless.

As per economist Matthias Fett, history shows a pattern in where the World Cups were hosted. Between 1958-1990, FIFA alternated hosting duties between Europe and Latin America. Chile hosted in 1962, Mexico in 1970 and 1986, Argentina in 1978. The motivations varied: Mexico used the 1970 tournament to showcase colour television and satellite broadcasting. Argentina’s military dictatorship, meanwhile, treated 1978 as a “national duty“ — a tool to legitimize its rule regardless of the cost.

Then, from 1990 to 2006, the World Cup went exclusively to wealthy nations that could absorb the financial burden more easily: Italy, the US, France, Japan, Germany.

But after 2006, the geography shifted dramatically to emerging markets: South Africa hosted in 2010, Brazil in 2014, Russia in 2018, Qatar in 2022. They were nations trying to make a deliberate statement about their place in the world, using the tournament to project soft power. Outside of the World Cup, the Beijing Olympics of 2008 are heralded as the moment that China arrived on the world stage.

For regimes seeking international legitimacy, that visibility is invaluable. Russia, for instance, used 2018 to present an image of being open and competent. It worked during the tournament, even boosting the image of President Vladimir Putin.

Qatar, a small Gulf kingdom, spent over $220 billion partly because the World Cup fit a long-standing soft-power strategy — one that also directly deepened political and military cooperation with France, including billions in fighter jet purchases. Their relations with other developing nations also improved after this event.

Of course, Qatar’s strategy can’t be viewed in isolation. Oil-rich Gulf nations like Saudi Arabia and the UAE have a similar strategy of hosting various sports events and purchasing European football clubs to exercise geopolitical power. Saudi Arabia are also the hosts of the 2034 FIFA World Cup.

But the reputational upside comes bundled with serious downside risk that all of these nations have faced. And sometimes, they created those risks themselves.

For instance, Qatar faced significant flak for poor labor practices used in building out World Cup infrastructure, and the accommodation built for the fans was in poor shape. Meanwhile, right before the start of the World Cup, Russia announced a cutback of pensions. Protests against this reform were suppressed because Russia instated no-protest laws in host cities. Moreover, any positive image that the World Cup helped Russia maintain was wiped out after their invasion of Ukraine.

The 2014 Brazil World Cup was supposed to be a branding triumph for a country that has been a powerhouse in the sport. Instead, it raised more questions on the host’s governance capacity, with people attributing their rising living costs to excessive expenditure on the World Cup, as well as the Olympics of 2016 in Rio de Janeiro. In fact, the city of Rio required a $900 million bailout from the government just to cover the costs of policing the Olympics.

Winner’s curse

The combination of FIFA’s monopoly and the use of the World Cup for soft power purposes has made the bidding process for the event extremely difficult.

You see, to host a World Cup, a country must submit a detailed bid covering infrastructure, venues, security, and event operations. A FIFA-appointed task force evaluates each proposal across 20 categories, scoring bids out of 500 points and assigning risk levels. Bids that fail minimum thresholds can be disqualified before the final vote by FIFA’s member nations.

That sounds orderly. But in practice, it has hardly been that.

The first problem is structural. FIFA keeps its historical financial data and cost benchmarks opaque. That means bidding nations cannot benchmark their cost estimates against what previous tournaments actually ended up costing. Every bid is, in a sense, flying blind, allowing overly optimistic forecasts to go unchecked. It also means that countries cannot learn from the mistakes of previous cycles. And since FIFA doesn’t bear those costs, it has little incentive to restrain the bidding.

Additionally, the task force’s recommendations are not binding and can be overridden.

The second problem is political. On one hand, an event like the World Cup has no economic benefit. However, it has positive political benefits. Politicians pursue hosting rights because they reap immediate rewards, while the long-term burdens get passed on to taxpayers and future administrations.

So, it’s hardly a surprise that FIFA is laden with corruption.

In 2015, a scandal blew the lid off a system inside FIFA that had been rotten for decades. Over $150 million in bribes had been exchanged to secure hosting rights and sponsorships. All but two of the 35 voting members of the FIFA Council were criminally indicted.

And a good chunk of this corruption is driven by the host country’s need to secure the bid. For instance, Qatar’s bid score was actually too low, and it was deemed “high-risk” by the task force. Yet, somehow, they secured the 2022 World Cup bid. Some of it may have to do with some under-the-counter dealings. Here’s three examples:

Mohamed bin Hammam, a Qatari member of FIFA’s Executive Committee, orchestrated a campaign that transferred $5 million directly into the bank accounts of FIFA officials to buy their votes.

Then, 3 weeks before the host selection vote, Qatari news outlet Al Jazeera offered FIFA $400 million for broadcasting rights — a deal that secretly included an extra $100 million to be deposited into a special FIFA account only if Qatar won

Qatar also financed a $387 million intelligence operation to spy on critics of FIFA

Where do we go from here?

FIFA has since made some changes. Hosting decisions now go to a public vote by the full Congress rather than a closed committee. Joint bids are permitted, allowing countries to pool existing infrastructure. But the underlying incentive structure remains intact.

The 2026 World Cup was supposed to be the proof of concept for a better model. It was a joint bid across three nations led by the US, the largest consumer market in the world. FIFA projects an unprecedented $11-13 billion of revenue in the 2023-2026 cycle.

And yet, the familiar warning signs are here.

Host cities are covering operations and security while FIFA keeps the commercial haul. Ticket prices have soared to the point of formal investigations. To make things worse, Trump’s immigration politics (and the general instability of his policies) are raising questions about who can actually attend a supposedly global event.

The World Cup works beautifully primarily for FIFA. For everyone else, it remains a gamble where the odds are stacked by design.

India’s state budgets are a mixed bag

Every February, the country pulls apart the Union Budget in obsessive detail. Almost nobody does the same for the state budgets. This is an odd blind spot, because several Indian states run economies bigger than entire nations.

Now, we can’t do 28 deep dives. The next best thing we can offer is a consolidated look at all the states together.

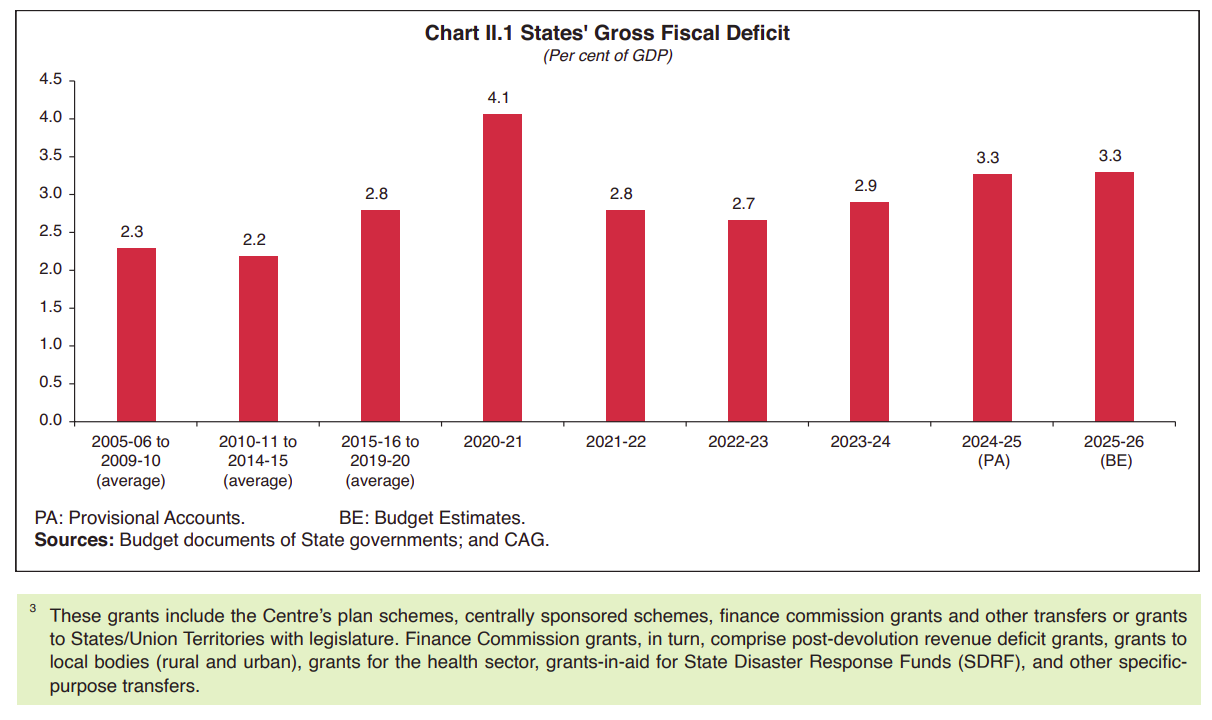

On the face of it, the story is reassuring. States’ deficits — the gap between what states spend and what they earn — has crept back above 3% of GDP, but it’s still comfortably inside the 3.5% limit the Centre sets.

State revenues grew, though the mix shifted — for better or worse, we’ll see. And the spending mix improved: a bigger share went into building things and less into day-to-day running costs, with capital spending at its highest in years. We’ll take each of these apart below.

The deficit accounting

Let’s start with that deficit.

The reason it even crosses 3% comes from one thing: a federal scheme called the Scheme for Special Assistance to States for Capital Investment. Under this, the Centre hands states 50-year, interest-free loans — on the strict condition that they spend the money on building things. It began in 2020-21 as a Covid-era stimulus, to keep money moving while the private sector sat frozen. Back then, it was pitched as a one-off. It wasn’t. It ballooned from around ₹12,000 crore in that first year to ₹1.5 lakh crore by 2024-25, and is now a permanent pillar of how states fund their capital spending.

For the states, this isn’t normal borrowing. A half-century loan at zero interest costs almost nothing to service. Moreover, it sits on top of their usual borrowing limits, letting them run a slightly bigger deficit without breaking the rules. This is why, despite a growing pile of debt, the interest states actually pay has barely budged in over a decade.

For the Centre, meanwhile, the same loans count toward its own capital-spending tally. Every rupee given here shows up in the Centre’s investment numbers, while bankrolling the states’ deficit at the same time.

This marks a quieter shift in policy. The Centre used to support states mainly through grants — money it never expected back. Now, it increasingly leans on loans the states must eventually repay, even if that shall happen decades later, and won’t yield interest. The old grants are shrinking, while this is a new channel stepping into their place.

In other words, the deficit is actually tighter than the headline suggests.

The support from Delhi is narrowing

Before we go any further, we’ll need to catch you up on a quick bit of plumbing.

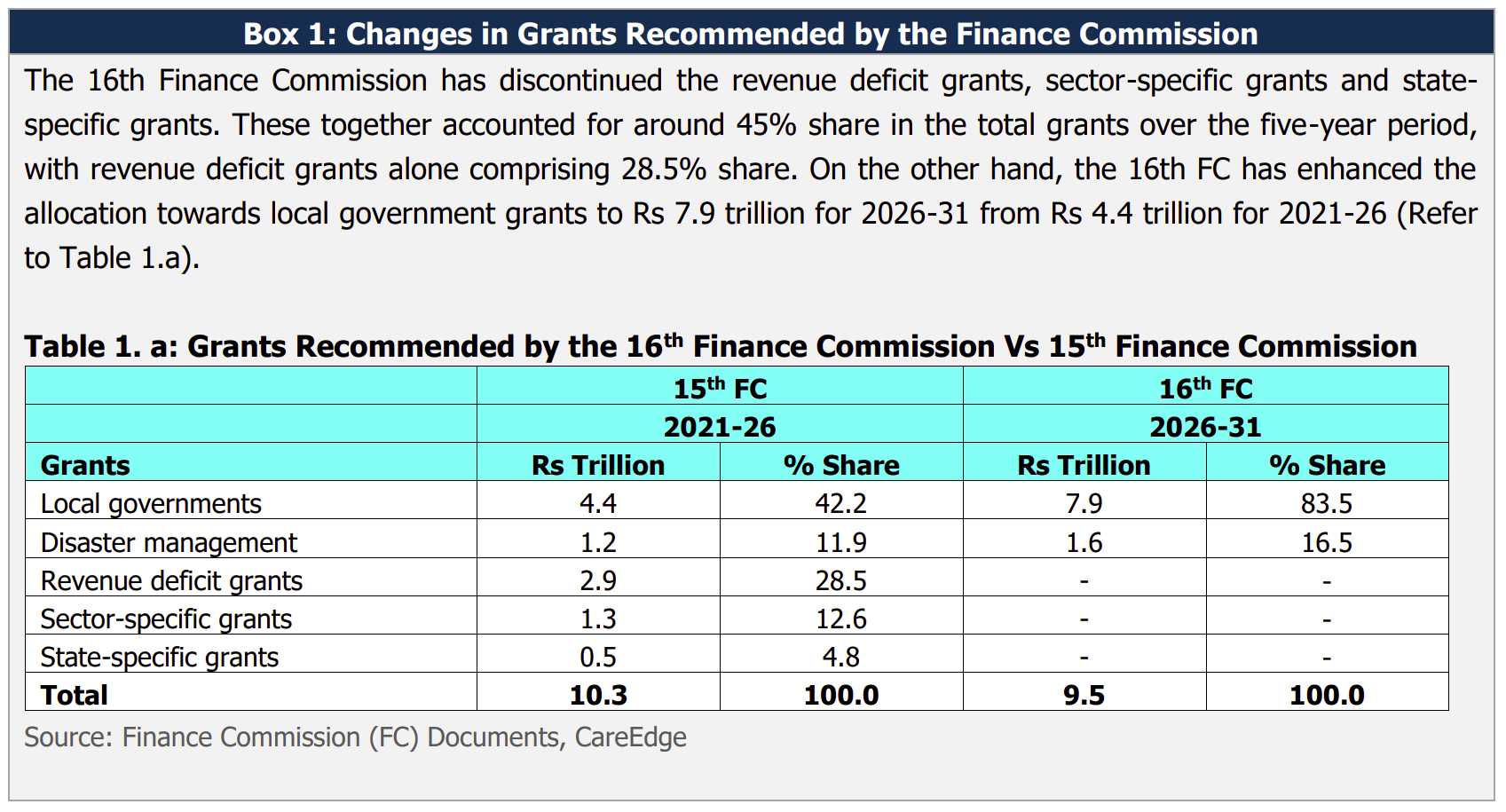

States have three sources of money: the taxes they raise themselves, and two separate pipes from Delhi. The first of these pipes, and the biggest, is devolution — the states’ fixed share of central taxes. That share is set by the Finance Commission, which redraws the formulas every five years, deciding both how big the states’ collective slice is and how it’s split between them. We dove into the mechanics of this a while back. The new 16th Finance Commission kept the states’ share steady at 41% of the tax pool. And because tax collections are broadly rising, in rupee terms, the amount the get keeps inching up.

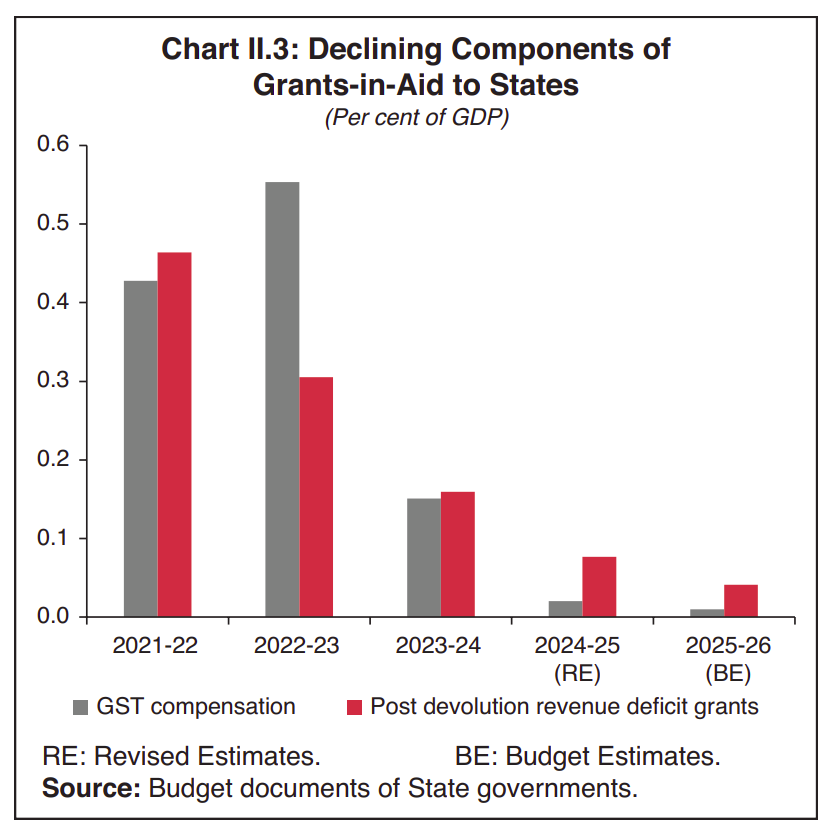

The second pipe is grants, and this is where you see the squeeze. In fact, the Finance Commission takes calls on some grants, and recently, it scrapped a whole category of them, worth roughly 45% of the old grant pool. Instead, it has funnelled more money to local bodies instead.

That’s a major swap. Suddenly, money that once went to a state goes to the tier below — local councils and municipalities — where it is earmarked for specific jobs like water and sanitation. This money is no longer the state’s to spend. What was once flexible cash, that states used to balance their own books, must go straight to local bodies.

This is arguably good policy. But states that leaned on those grants to stay afloat — such as Kerala, Himachal, Punjab, the North-East — take a bad hit.

States are effectively being asked to make do with taxes. The trouble is that their tax base is narrow: the GST they collect themselves, tax on fuel, excise on liquor, and the stamp duties on legal agreements together make up about 90% of it.

To many, the last of these is a real lever. The gap between the most and least efficient collectors of stamp duty is enormous. Many states have no real sense of the transactions happening within their boundaries. They could raise serious money through simply administrative action — digitising land records, updating outdated property values — without touching a single rate.

Beyond this, however, there’s little scope to increase revenue quickly.

States are borrowing more

If states need money, their grants are shrinking, and taxes can’t fill the gap, what do they do? Easy, borrow. States now fund about three-quarters of their combined deficit by selling bonds in the market. Their borrowing is up sharply from half a decade ago.

That can become a problem, however, because their borrowing has a “crowding out” effect. As states rush into the bond market, they eat into the room left for the Centre and private companies to borrow. In fact, big, long-term buyers like banks, insurers, pension funds are starting to rethink their allocation strategy and their appetite for such bonds have muted.

Here’s one reason: you’d expect a shaky state to pay noticeably more to borrow than a strong one. In reality, there’s barely a difference. The gap between the safest and riskiest states is just a few basis points. The market treats every state as if Delhi will always quietly stand behind it, rather than pricing in who’s actually running their finances well.

For now, that’s a comforting assumption. If it’s ever tested, however, all bets are off. If the centre lets a state default, the repercussions could flow far and wide.

Building roads with one hand, writing cheques with the other

But why do states need more money? Well, they’re trying to do two expensive things at once.

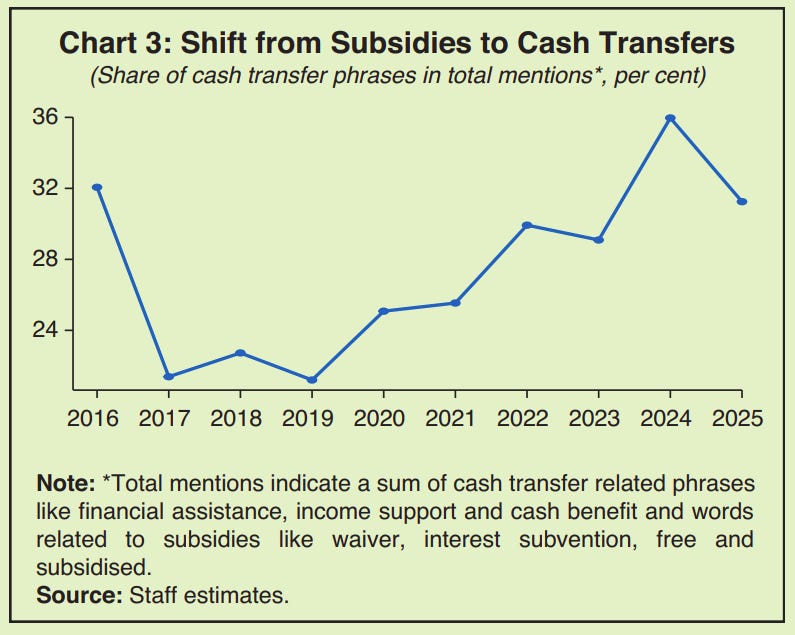

On one side, they’re making a capex push — good, and improving. At the same time, though, they’re funding a fast-growing pile of welfare promises: free electricity, loan waivers, and above all, direct cash transfers straight into people’s bank accounts. In fact, when the RBI studied the language of state budget speeches, there was a clear tell: the vocabulary has shifted from “subsidy” toward “income support.”

Welfare itself isn’t a bad thing. In a country as unequal as ours, much of it is necessary. The worry is that a cash transfer, once it starts, is almost impossible to stop. It quietly hardens into a permanent line in the budget with a very vocal constituency attached. Such promises may be easy to make, but they’re impossible to roll back.

There are three Indias

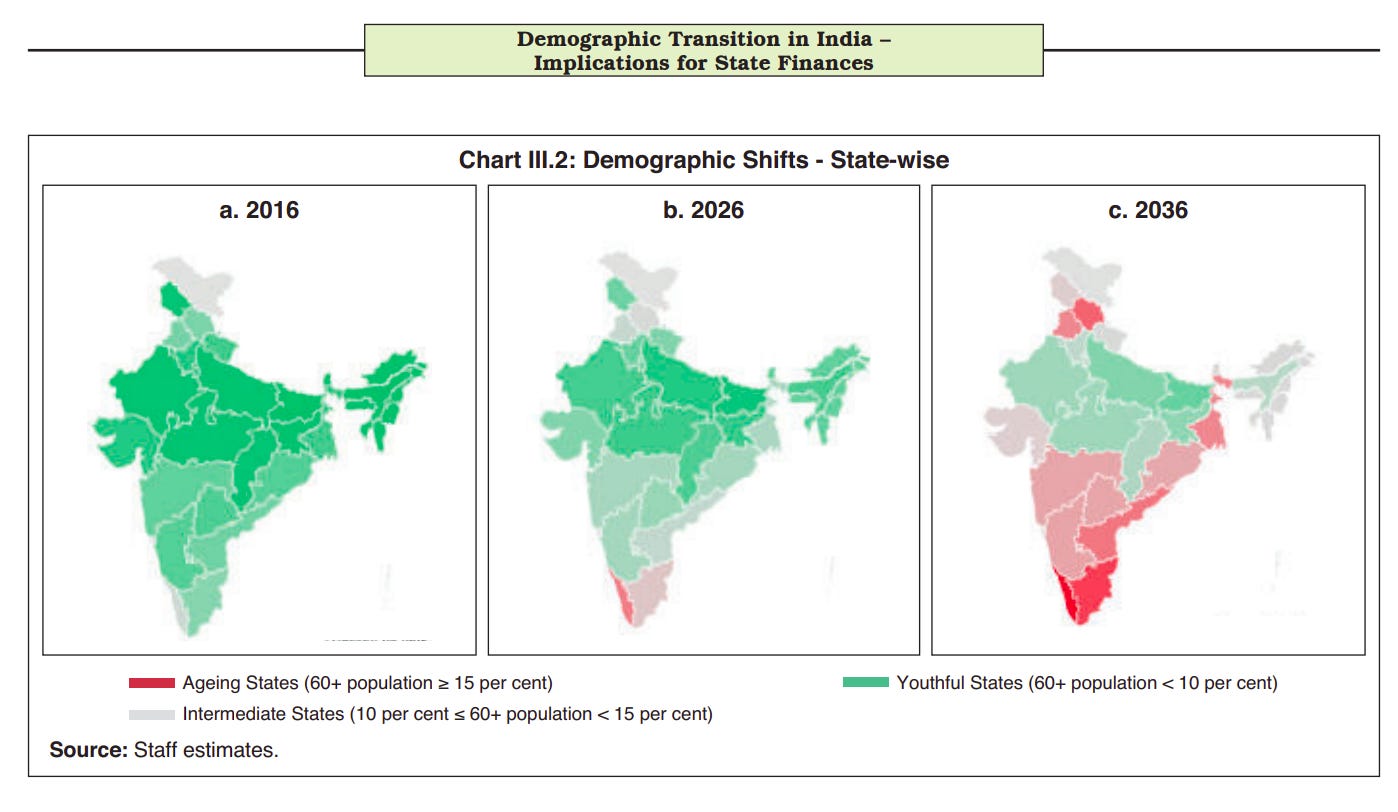

There’s a sweet spot in some country’s lives: they suddenly have a massive influx of working-age people, while there are relatively few children or elderly for them to support. Economists call this a “demographic dividend” India is famously in that window.

But that is only if you look at the national picture. Averages make it seem that way, but averages lie. In reality, different states are at completely different points on the curve.

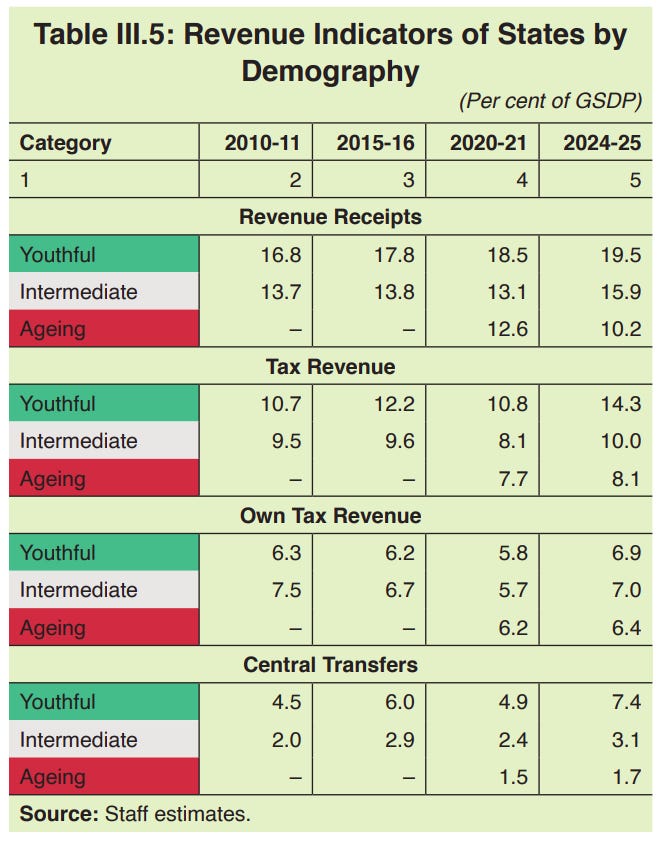

The RBI sorts Indian states into groups. Youthful states — Bihar, Uttar Pradesh, Madhya Pradesh — still have a young, growing workforce. Intermediate ones — Maharashtra, Gujarat, Karnataka — are maturing. But there are aging states, where more than 15% of people are now over 60: today, that’s just Kerala and Tamil Nadu, but Punjab and Himachal are close behind.

What does that imply for these states? Follow the money.

If you were to measure a state government’s revenue against the size of its economy, you would find that for every ₹100 an economy generates, a youthful state’s government collects around ₹19 to ₹20. An aging state, on the other hand, collects barely ₹10. Young states look far better resourced relative to the economy underneath.

It isn’t that young states tax their own people harder. If you look at just the taxes a state raises and keeps for itself, the two groups look almost identical: they draw somewhere around ₹6.50 to ₹7 out of every ₹100, whether the state is young or old.

The gap comes from Delhi. Youthful states get a big top-up from the Centre — roughly ₹7 of that ₹100. Meanwhile, aging states get under ₹2.

This imbalance is baked into the very formula that splits central money. It’s deliberately redistributive, sending more to poorer states. India’s most youthful states — Bihar, UP, Madhya Pradesh — happen to be the poorest, so they get a larger cushion. Richer but older states get a much thinner one.

When an aging state like Kerala looks fiscally stretched, it isn’t solely because it taxes badly, or spends recklessly. It faces a slow squeeze from two sides. Its shrinking workforce drags down growth, which means its tax base stays stagnant — with fewer working people, and less economic activity to tax. Meanwhile, because it’s well-off relative to everyone else, the help it gets from Delhi is thin. This is simply a feature of the system.

There’s one big caveat to this framing, though.

It’s easy to assume that people stay put. They don’t. As we discussed with authors of the State of Working India Report, young workers from poorer states like Bihar and UP migrate in huge numbers to richer, ageing states for work. That’s where they transact, and where they create economic gain. So a state that theoretically has a dividend might not reap it, while those gains go to aging states that can draw young workers from elsewhere.

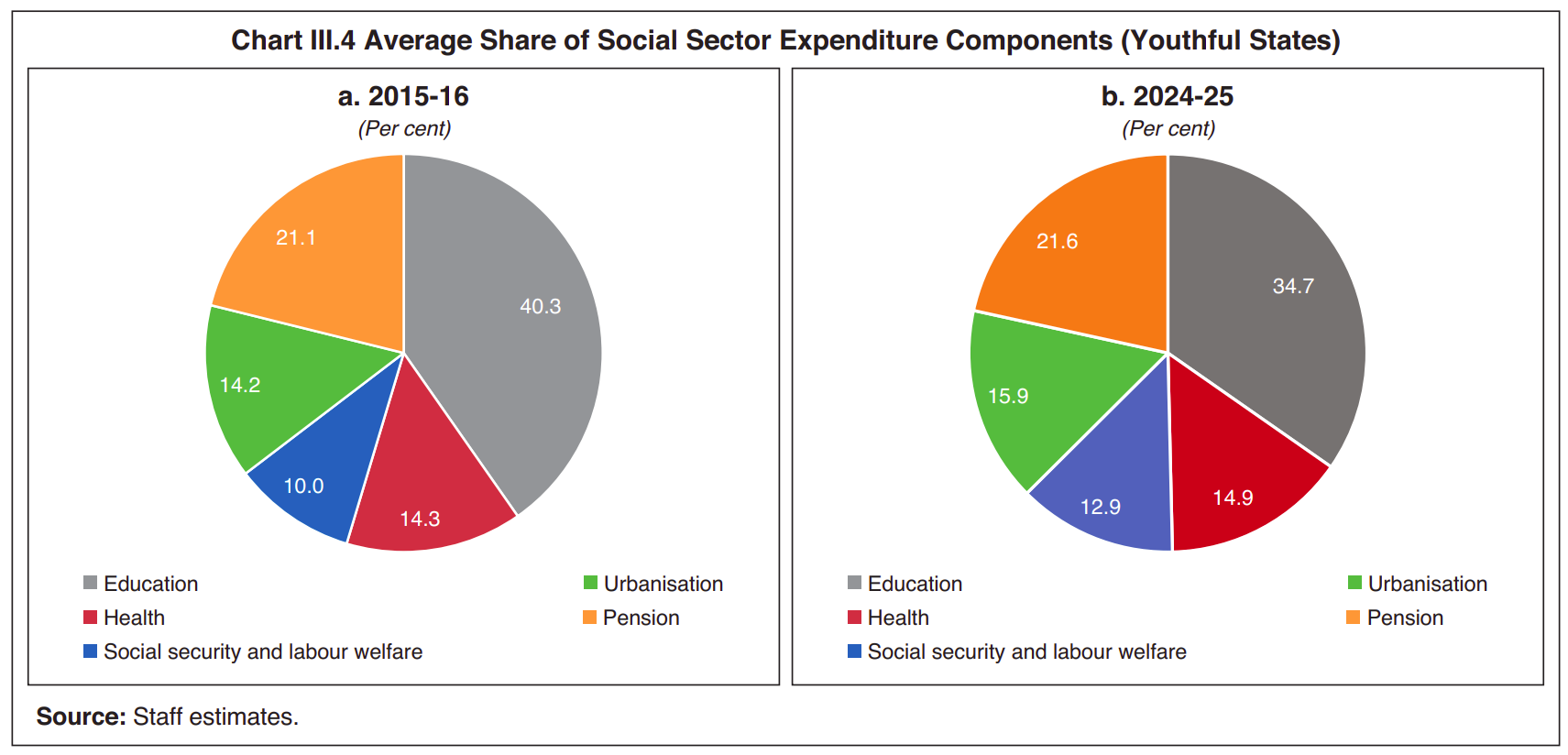

There’s a cruel irony in the data. A young state can only harvest its youth bulge if it educates those workers, turning them into skilled, employable workers. Only, even as cash transfers expand, the share of youthful states’ budgets going to education has been falling.

The bills are all coming due at once

Demographics, however, more slowly. In the meanwhile, there are bills that are more immediate, and many shall land at once.

The first is the 8th Pay Commission — the latest edition of a periodic exercise that raises government salaries and pensions, which states inevitably follow. This is expected to hit state budgets around 2027-28.

Two, climate is now becoming a budget line. India is among the world’s worst-hit countries by extreme weather, with nine states in the most-vulnerable tier, and dealing with everything that follows will be expensive

Three, there’s a time bomb hiding within state balance sheets. States have given massive guarantees, much of it to prop up loss-making power utilities. If something goes wrong, that bad debt will show up in the deficit at once, which is why the Finance Commission is forcing states to own up to them.

On top of all that, there’s the immediate shock of the Iran war. Even though the hostilities appear to have paused, the repercussions won’t cease. CareEdge expects it to slow growth, soften tax collections, and push next year’s deficit 0.2 to 0.4 percentage points wider than budgeted.

For now, everything holds — but only because Delhi keeps lending to the states for cheap, while the economy is growing fast enough to outrun the debt. Neither is guaranteed forever. As all these bills come due, right as grants dry up and the rules tighten, a state that doesn’t have a handle on its finances could be in for a rude shock.

Tidbits

RBI has barred banks and NBFCs from forcing customers to buy bundled products, and will require full refunds where mis-selling is proven. The rules kick in from January 1, 2027.

Source: LivemintChina’s retail sales fell for the first time since COVID reopening, dropping 0.6% in May, while investment also shrank 4.1% in the first five months of 2026.

Source: BloombergHCLTech is buying a 10.5% stake in Indian AI startup Sarvam AI for ₹1,427 crore, leading its Series B round. The deal values the company at $1.5 billion, making it India’s newest unicorn.

Source: Reuters

- This edition of the newsletter was written by Manie and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Amit Kumar Gupta on the copper cycle

For months, almost every major story we’ve covered—from the energy transition and the AI data-center boom to EVs and power grids—has had copper quietly sitting at the center of it. To make sense of why this metal keeps showing up everywhere, we sat down with Amit Kumar Gupta, who runs Fintrekk Capital and has over two decades of experience in the markets. Our conversation dives deep into the nuances of the copper cycle, the sheer scale of demand from new technologies, the things most people get wrong about the metal, and what it all means for the global economy. Read the key takeaways on Subtext.

Watch the full podcast episode below, where Amit walks us through the mechanics of the copper cycle and its impact on the future of energy and tech

Over 2 crore Indians invest with Zerodha. Open a free demat account in minutes and invest in stocks, mutual funds, ETFs, and bonds at 0 brokerage. No hidden charges, no gimmicks. Plus, get free access to research tools like Tijori, Sensibull and more.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉