The OPEC’s worst ever defection

How quotas, technology and politics drove the UAE away

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The UAE leaves OPEC

No money, more problems for the music business

The UAE leaves OPEC

On April 28th, leaders of the Gulf Cooperation Council met in Jeddah. They were there for an emergency session on how they would handle the Iran war. There was one empty chair, however. A prominent Gulf country was missing from the proceedings. Sheikh Mohammed bin Zayed Al Nahyan, the president of the United Arab Emirates, was not in the room. In fact, UAE officials were decrying the GCC as being weak.

This was odd.

The UAE had been cooperative until just a few weeks ago. As recently as April 5th, the UAE was still sitting in OPEC meetings, adjusting its production for the sake of “market stability”. Two days later, the OPEC publicly listed the UAE among countries that submitted updated compensation plans for past overproduction.

That cooperation, however, began crumbling over the month. It culminated on the evening of the 28th, when the UAE released its official statement: starting from May 1, it was leaving OPEC.

The world’s largest cartel

OPEC was founded in Baghdad, in 1960, by five governments — Iran, Iraq, Kuwait, Saudi Arabia, and Venezuela. Its original purpose was less about prices than about sovereignty. Most of the oil from these countries was being pumped, priced, and sold by Western international oil companies — the so-called “Seven Sisters”. OPEC was the producer states’ attempt to take that control back.

Seven years later, well before there was a country called the United Arab Emirates, one of its seven emirates — Abu Dhabi — joined the grouping.

For its first half-century, OPEC was largely a political institution. Its members coordinated on oil production and tried to shore up their bargaining power, but the machinery of their coordination was loose. National governments retained control over their output. The body set production quotas for each country, but they were difficult to enforce, and compliance was often uneven.

That changed in 2016, however. Faced with the explosive growth of US shale, OPEC signed the ‘Declaration of Cooperation’ with ten non-member producers — most importantly Russia. This expanded group, OPEC+, set up a formal structure to manage much of the world’s oil supply.

That’s when it became technocratic.

The 2016 declaration created a “Ministerial Monitoring Committee”, that would police its member states. Each OPEC+ member was assigned a baseline — a reference “production level” that the country operated at. They were then asked to cut their production, for amounts calculated as percentages off this baseline. Smaller subgroups could then layer additional cuts on top. Each country’s production would be monitored, and members who overproduce would have to submit compensation plans to make up for the excess. Deviations from the cartel’s mandate, in short, were now punished.

All of this depended on where your baseline was set. If that baseline was too low, the body’s requirements — production quotas, cutting requirements, and more — could quickly become a straightjacket.

Why the OPEC stopped working for UAE

The UAE had historically been one of the stalwarts of the OPEC, throwing its weight behind Saudi leadership, and pulling its weight in production cuts. But the new structure was beginning to pinch.

The quota trap

Ever since Russia had joined in, UAE had been growing uncomfortable with the new Saudi-Russia leadership axis that had taken over the grouping. The arrangement reeked of favouritism. Russia’s baseline production level was artificially inflated to bring it nearly in parity with Saudi Arabia, even though its historical output had been much less. Russia also played loose with the grouping’s limits, overproducing frequently with little consequence.

On the other hand, when the UAE exceeded its production limits in 2020, it was publicly rebuked. The asymmetry rankled.

The country felt short-changed. It claimed that it had been assigned an artificially low baseline of less than 3.2 million barrels a day, based on what it had produced in October 2018. That number, it said, was outdated. It had since invested heavily in upstream capacity, and the limits on it now felt too restrictive. By April 2020, it was pushing out well more than 3.8 million barrels, and that, it felt, was the right benchmark.

The quarrel broke out in public, with UAE blocking a proposal to extend pandemic-era production cuts until its grievances were heard — bringing the body to a halt. The stand-off was only resolved once they negotiated their way to a higher quota of 3.5 barrels a day.

This would slowly turn into a repeated pattern of conflict and compromise. But compromises alone couldn’t solve the core problem.

The fact was that the UAE was investing heavily in oil infrastructure, and OPEC+ limits simply didn’t keep up. The country had poured roughly $150 billion in new capacity in the post-COVID years. By May 2024, the Abu Dhabi National Oil Company had built an installed oil production capacity of 4.85 million barrels a day, with targets for 5 million barrels by 2027. Meanwhile, its OPEC+-sanctioned production limit still sat at around 3.5 million barrels. The country was forced to sit on almost 1.4 million barrels a day of unused capacity — close to forty percent of what it had built.

Of all OPEC+ members, no other country was forced to keep such a high shar of its capacity shuttered as UAE.

That cost the country serious money. By one Baker Institute estimate, UAE was letting go off roughly $3 billion in revenue every month. If it left OPEC+, by 2028, it could earn somewhere between $50 billion and $70 billion in extra revenues a year — about a fifth of Abu Dhabi’s 2022 GDP.

There was little the OPEC+ could really do, though. It was caught in a political logjam.

To update national baselines, it would require a unanimous vote among OPEC members. But several of its members — like Algeria, or Nigeria — had actually lost production capacity over those years. If baselines were to be reset to reflect reality, they would actually lose their share. It made more sense, for them, to simply veto any change. OPEC simply couldn’t accommodate a member whose capacity was growing while everyone else’s was shrinking. The UAE was effectively trapped in its outdated quota.

Flattening energy

Meanwhile, there was a deeper structural problem at play, which threatened the very logic of a body like OPEC+. The energy world, in the words of authors Daniel Lacalle and Diego Parrilla, was “flattening”.

OPEC was built to create a sense of perceived scarcity, for a world that thought it would run out of oil. It was this sense of scarcity that gave its members their power. But that world was dying.

America’s “shale revolution” had, in one swoop, multiplied how much oil we thought we could access. It had moved North America from net oil importer to a producer that could go toe-to-toe with Saudi Arabia. OPEC+, by restricting supply and holding prices high, was simply creating the conditions for American shale producers to capture market share. Every barrel OPEC withheld from the market was a barrel American shale would sell instead.

The initial promise of the OPEC was that when individual countries restrained themselves from producing oil, they would all earn more profits per barrel. But after the shale revolution, they were now simply subsidising their replacement.

At the same time, the energy transition had well-and-truly taken off. One could quibble about when it would happen, and how much residual demand there would be. But no matter how conservative you were, it was increasingly clear that a country’s oil reserves wouldn’t always find buyers.

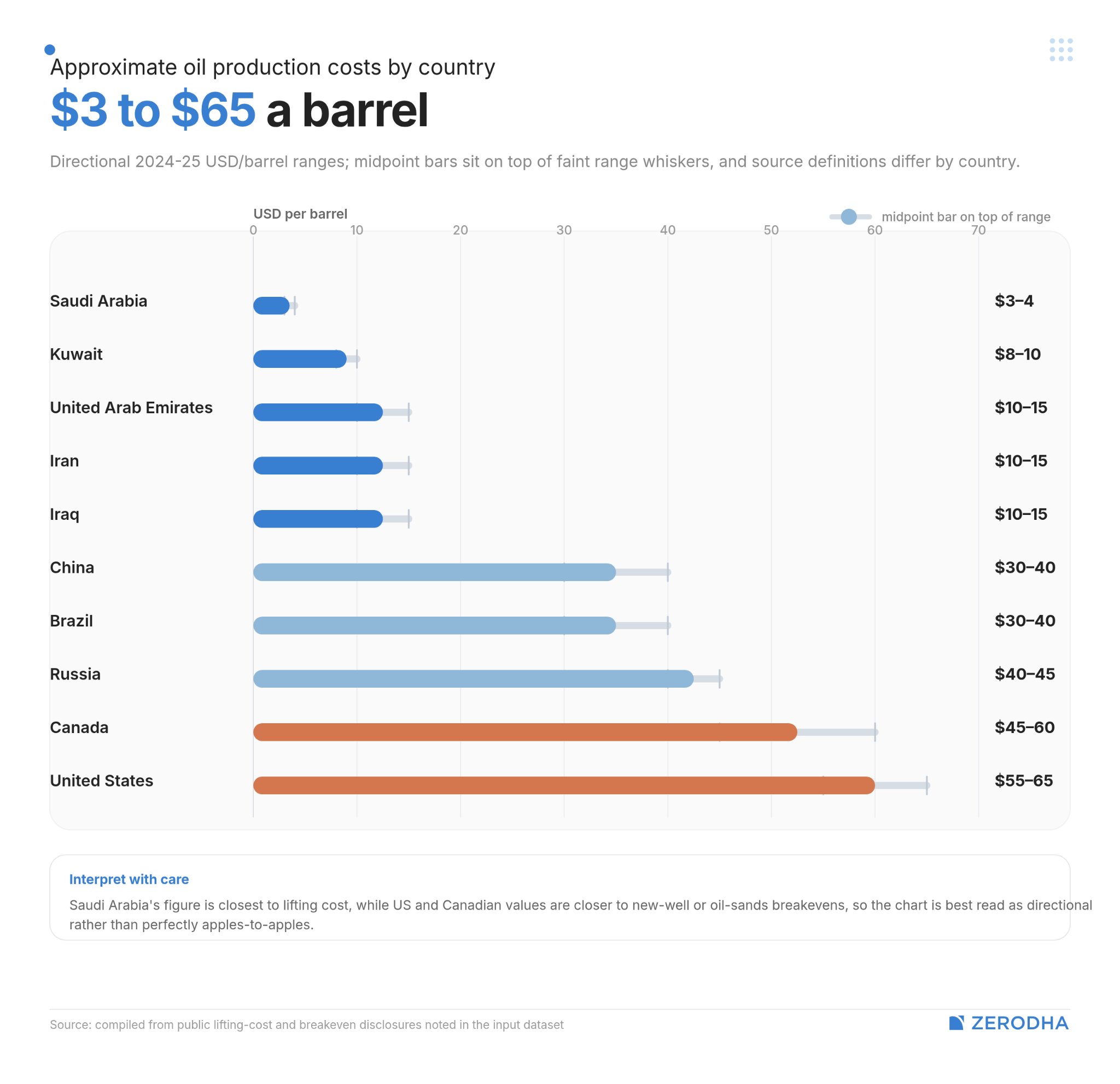

The UAE has some of the lowest oil production costs in the world — well below those of American producers. By letting this oil sit in the earth, it was simply letting others catch up. The twin “flatteners” — extraction technology and the energy transition — had effectively ensured that their oil likely wouldn’t appreciate in price even if it waited. All that waiting simply wasted the potential of its multi-billion dollar investments.

And for what? Just so that laggard OPEC+ members bleeding capacity could keep afloat?

The Iran spark

Maybe the OPEC+ could survive the poor economics. But layered on top of this was a political problem. The UAE and Saudi Arabia no longer saw eye-to-eye.

Just a decade ago, their two heads-of-state, Mohammed bin Salman and Mohammed bin Zayed were close partners. They moved together on most regional questions. In 2015, they had entered the Yemen war together, fighting against the Houthis. In 2017, they co-led a blockade of Qatar.

But that alignment has been breaking down. From Sudan to Yemen, the two sides had started clashing, by proxy, all across the area. The economic frictions between the two, too, were growing. Where Dubai had enjoyed a long run as the Gulf’s undisputed commercial hub, Saudi Arabia’s “Project HQ” mandate — which forces multinationals to base regional headquarters in Riyadh in order to win government contracts — seemed to eat into its turf.

Late last year, the conflict began to escalate. The two countries had backed different sides in Yemen: the UAE backed the Southern Transitional Council, a separatist bloc, while Saudi backed its government-in-exile. Late last year, Saudi forces struck UAE-linked weapons shipments at the Port of Mukalla. It also began striking STC military bases. Relations between the two countries seemed increasingly strained.

Then came the Iran war.

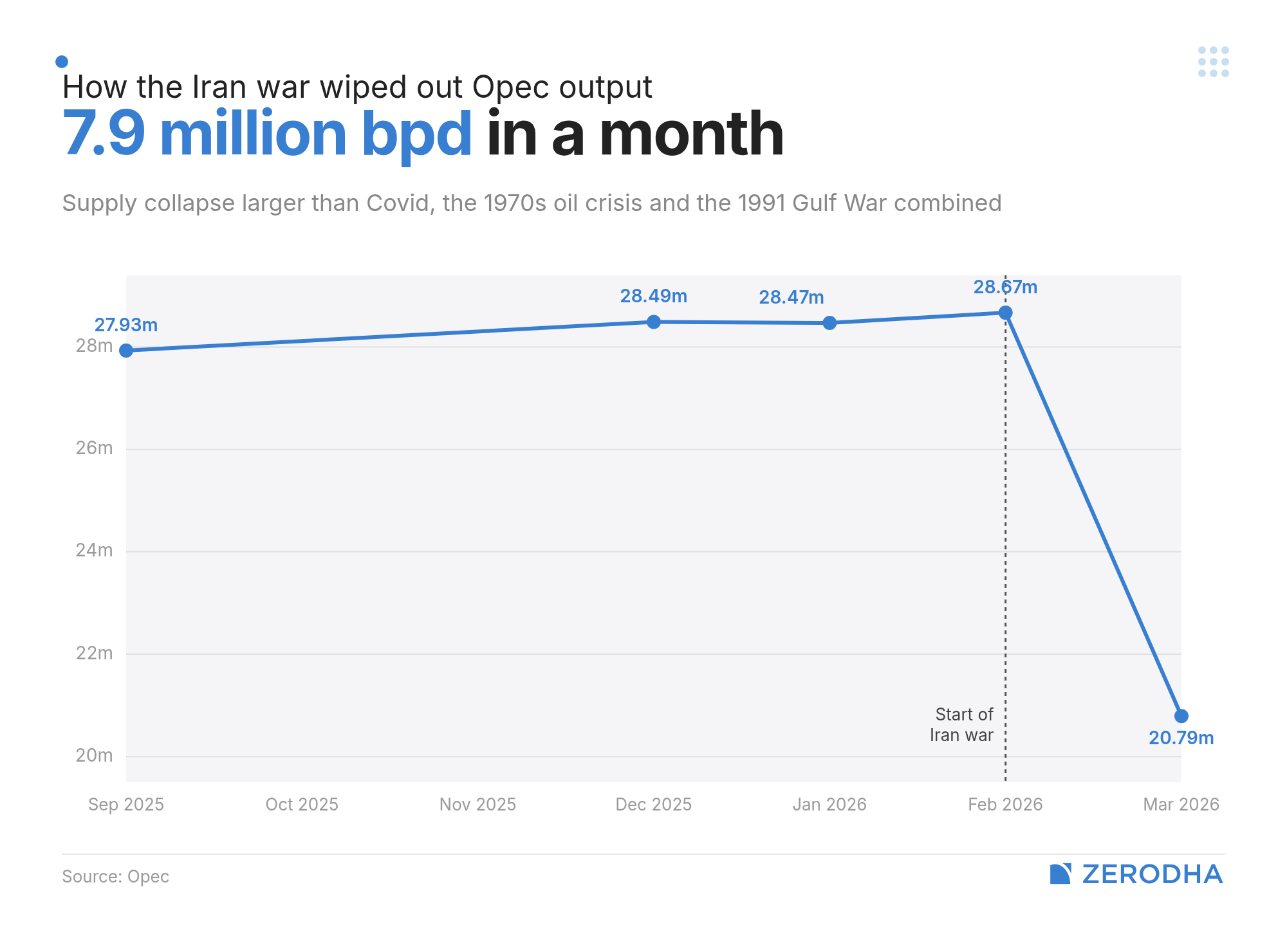

The conflict knocked out roughly 7.9 million barrels a day of OPEC output — a supply shock larger than COVID, the 1970s crisis, and the 1991 Gulf War combined. The UAE’s own production crashed by about 45%, to roughly 1.89 million barrels a day. The UAE, hit by almost 2,000 attacks from Iran, pushed Saudi Arabia and Qatar for a joint Gulf military response. They declined. Anwar Gargash, the Emirati president’s diplomatic adviser, called the GCC’s response the weakest in its history.

But amidst the chaos, the crisis also created a window.

In any other time, the UAE’s exit from OPEC+ would have bearish repercussions across global markets, bringing with it serious international pressure. But in a time like this, with the Strait of Hormuz half-paralysed and regional supply already shut in, there was nowhere for prices to go. Brent was stuck above $110 a barrel on a war premium. An announcement that would have crashed prices in normal times barely moved them.

UAE had a clean way out of the OPEC+.

What just changed

This is, by all accounts, a disaster for the OPEC+.

For one, it simply creates precedent. The OPEC+ has seen other exits before — like that of Qatar in 2019, or Angola in 2024. But UAE, unlike those others, is a heavy-hitter, making up 12% of OPEC’s oil output. Never has a country with this much heft and production capacity headed for the exit. Unless the OPEC+ can comprehensively punish UAE for its defection, the next a country wants out — perhaps Iraq, or Kazakhstan, both of whom have already expressed their unhappiness — they’ll find enough political cover to do so.

But its problem is more insidious.

OPEC’s power was never really about its total production. It was about spare capacity. Whether to stabilize world markets or to punish an errant member, the OPEC’s strength lay in how it could flood the markets with excess oil on command. A lot of that capacity, however, came from the UAE. It was the only country, other than Saudi Arabia, that could push a lot of oil online. With this exit, Saudi Arabia must reprise that role all alone.

This makes UAE’s exit an existential concern for the grouping.

A lot depends on the grouping’s response, going ahead. It could try raising the costs of UAE’s exit, It could launch a price war. It could try other tools — economic blockades, airspace restrictions, and the like. It may yet make an example out of the UAE, buying a few years of time.

But it can’t outrun a simple fact: the body was made for a world where oil was scarce, and future demand was guaranteed. Neither is guaranteed any more.

No money, more problems for the music business

With the exception of the US, India produces more music streams than any other country on Earth. There are ~18 crore people who use a music streaming app in any given month, more than the entire population of most countries.

And yet, the entire revenue pool that all of this volume generates is smaller than the recorded music industries of South Korea, the Netherlands, or Mexico. We rank 15th globally.

That gap between what we listen to and what we pay for is not a measurement quirk. It is the entire shape of the Indian music business. And it explains an even stranger fact: in the last 18 months, three major streaming platforms in India have shut down. ByteDance’s Resso left in early 2024 under government pressure on Chinese apps. Bharti Airtel pulled the plug on Wynk Music in November 2024. Hungama wound down its consumer streaming service in April 2025.

Yet through this carnage, the labels whose music those platforms were carrying — Saregama, Tips Music, T-Series, and Sony Music India — kept growing revenue. Listeners are up and labels are getting richer, but platforms are just barely able to survive. How does that work?

To answer that, you have to look at how money actually moves through this industry. Once you can see the value chain, almost everything else falls into place. We also spoke to Roochay Shukla, who spent more than a decade in the industry. This is a distillation of all that we found ourselves, and learned from him.

How money moves through a song

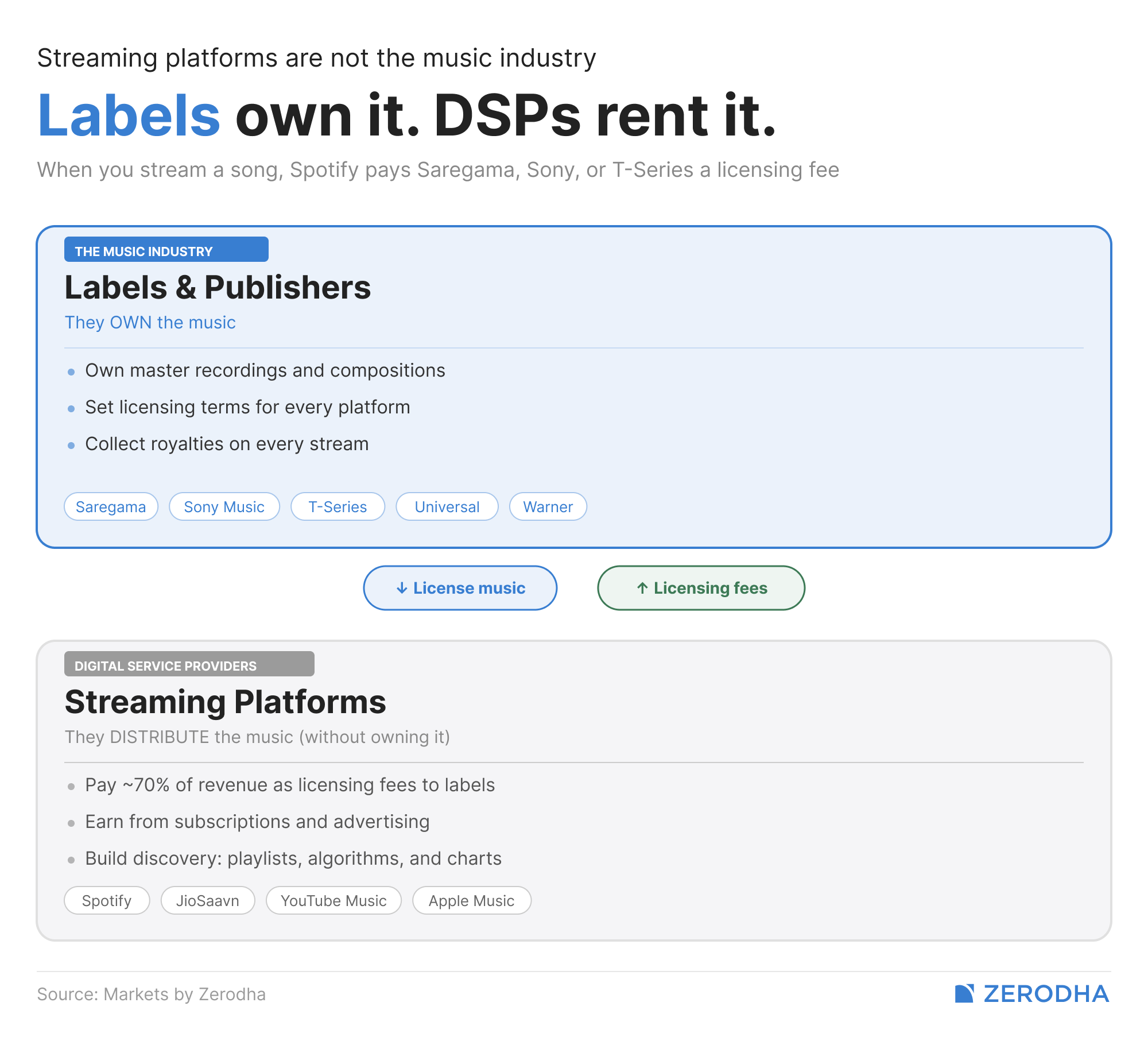

A common confusion is to treat Spotify, JioSaavn and YouTube Music as the music industry, but they aren’t. The actual music industry sits one layer above them — the labels and publishers who own the songs and license them out. When you stream a song on Spotify, Spotify isn’t selling you something it owns. It’s renting access to something Saregama, Sony Music or T-Series owns, and paying them a cut.

The rights

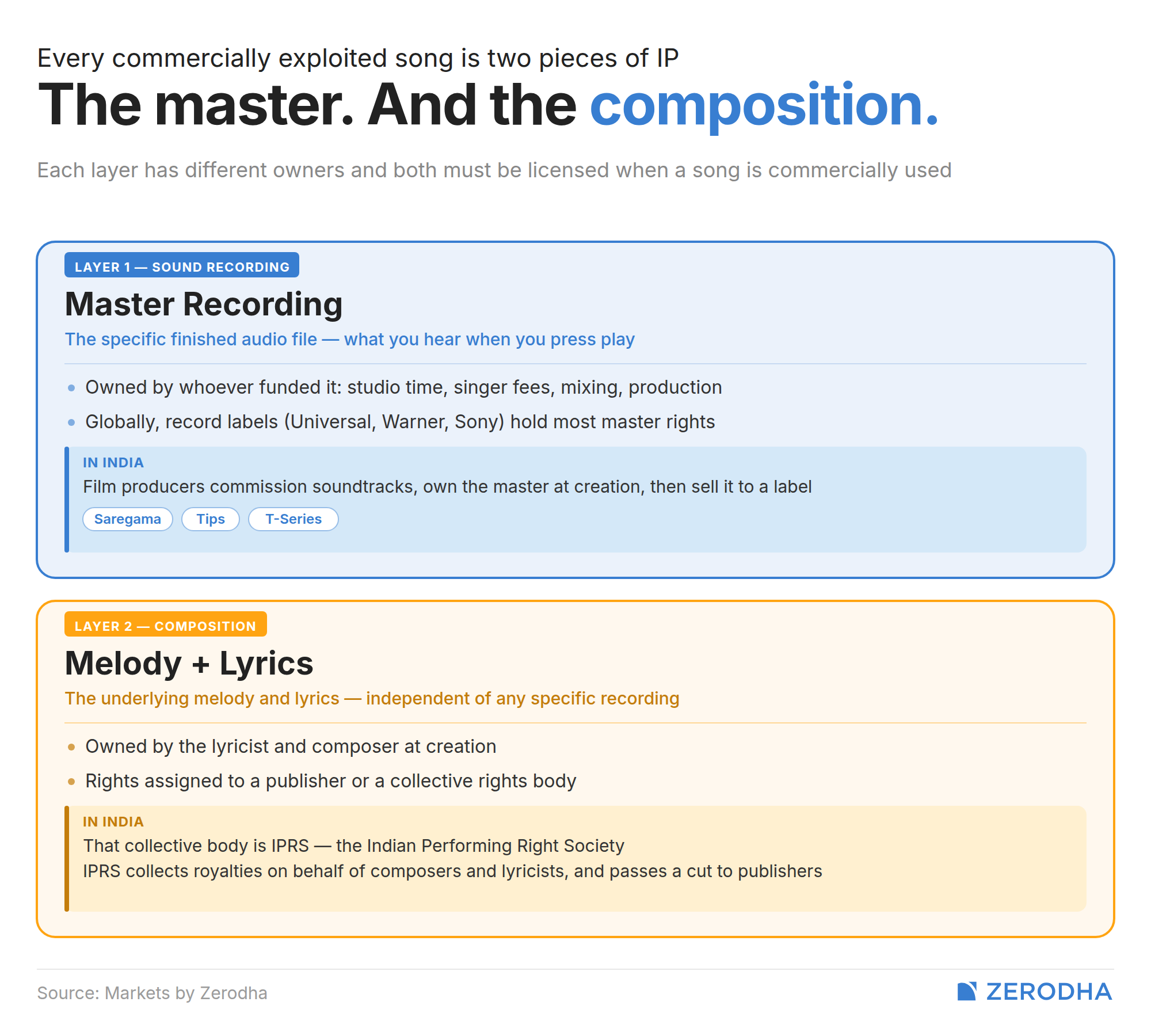

Now, every commercially exploited song is actually two pieces of intellectual property stacked on top of each other.

The first is the sound recording itself, also called the master. This is the specific finished audio file you hear when you press play. Whoever paid for the recording session, the singer’s fee, the studio time, and the mixing typically owns the master. Globally, that’s a record label like Universal or Warner.

But in India, where film music dominates everything, the picture is different. Film producers commission soundtracks as part of their movie budget, which means they own the master at the moment of creation, and they then sell it to a music label like Saregama or T-Series.

The second piece of IP is the composition itself: the underlying melody and lyrics, which are separate from any specific recording of them. If someone covers an old song or remixes it for a new film, they need permission from the composition owner even if they don’t touch the original recording. The composition is owned by the lyricist and the composer. Typically, they assign their rights either to a publisher or to a collective body of their respective country, and that body makes sure the publishers get a cut of their music. In India, that body is the Indian Performing Right Society, IPRS.

Globally, the master rights and the publishing rights are typically split into two separate businesses run by different companies, but in India, the label owns everything. That single quirk gives Indian listed labels economic ownership over their songs that even Universal and Warner don’t have over their globally-signed artists. A comparison between Saregama and Universal isn’t apples-to-apples since Saregama owns more of each song.

Royalties

Now to the part that explains how the actual rupees flow.

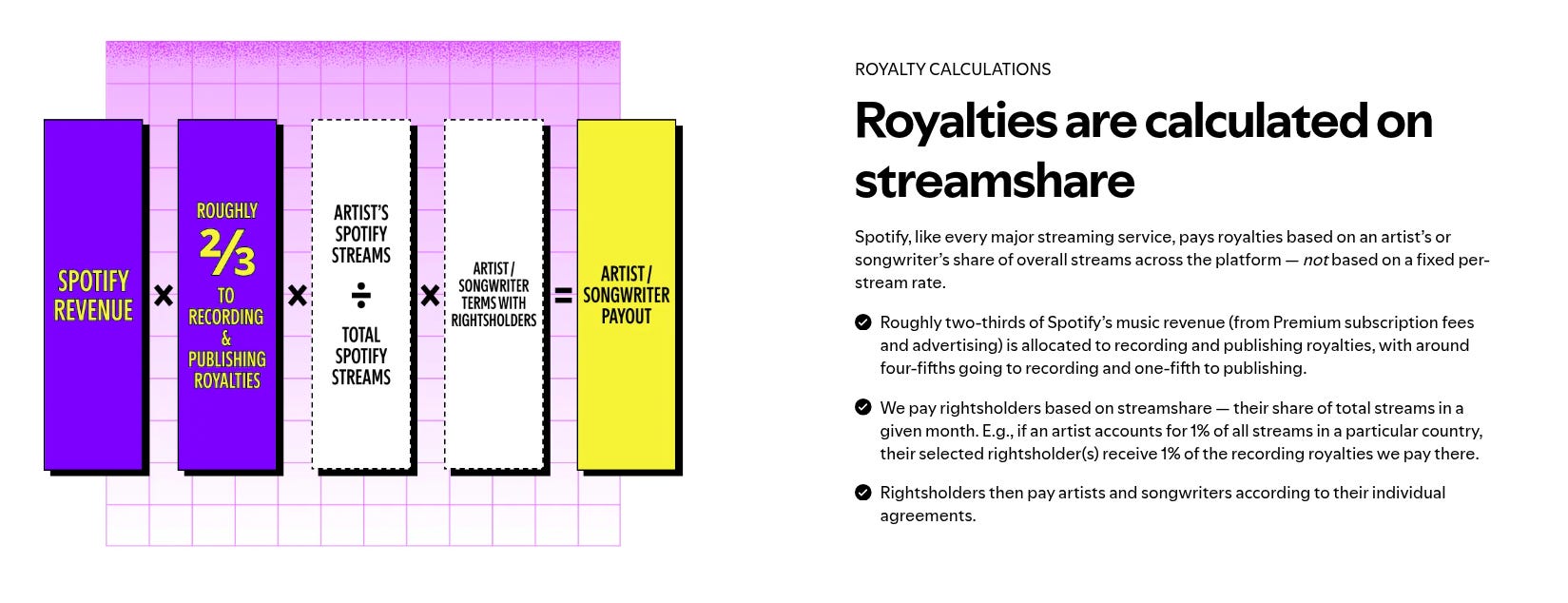

Most of the world, including India, runs on what’s called the pro-rata model — sometimes also called the market-share payment system. When you stream a song on Spotify, the platform pools all the money it earned in your country in that month, through subscriptions and ads. It keeps a cut for itself, roughly 30%, which goes towards server costs, app development, marketing, and (hopefully) profit. The remaining 70% goes into a pot that gets divided up among rights holders.

The division isn’t based on a fixed per-stream rate, but on streamshare. For instance, if Saregama’s songs accounted for 5% of all Spotify streams in India that month, Saregama gets 5 percent of the distributable Indian pool. If the pool grows because more people pay subscriptions, every label’s per-stream realisation goes up automatically. If the pool stays flat but stream volume keeps rising, per-stream realisation falls.

In India, the deals between labels and platforms also come in two other shapes that are worth understanding.

The first is the minimum guarantee (MG). Here, labels charge platforms a fixed annual fee upfront, regardless of how many streams the platform’s users actually generate. This shifts demand risk from the label to the platform. It’s how Indian labels survived the first years of streaming when paid penetration was tiny. The second is plain revenue share, where the label simply takes a cut of whatever the platform actually earns. Most Indian streaming deals are some hybrid of an MG floor and a revenue-share upside.

However, in 2023 and 2024, several platforms — Gaana, Resso, Hungama — found themselves struggling financially. They tried to renegotiate their MGs down or eliminate them entirely as they shifted to subscription-only models. On its earnings calls, Saregama attributed soft FY24 licensing growth specifically to this shift. The platforms wanted to share their pain with the labels, but the labels refused. Some platforms then died.

That is the structural skeleton of the industry.

The strangest split in Indian media

Globally, the recorded music business is doing better than it has in a generation. Recorded music revenue reached $31.7 billion in 2025, up over 6 percent. That’s eleven straight years of growth.

But India breaks the pattern. We have 18 crore streamers, but only ~1.4 crore paid subscribers. Paid penetration is around 8%, while globally it’s closer to 40%. Apple Music charges ₹119 a month here, and Spotify Premium starts at ₹139 a month for its lite plan. These are mass-friendly prices that only exist because Indian users would walk away otherwise.

It’s also why platforms keep dying in India. Someone who generates a few rupees a year in advertising revenue but consumes hundreds of streams that the label still has to be paid for, is a big drag on platforms.

That’s why the industry consolidated to 4-5 real players. You have Spotify, the only standalone audio streaming business of scale, still loss-making in India after seven years. Then there’s JioSaavn, cross-subsidised by Reliance Jio’s telecom business. YouTube Music, meanwhile, benefits from Google’s video ads business. And then there are bundled telecom plays around Apple Music and Amazon Music, which exist as adjuncts to other subscriptions.

But on the other side, Indian labels enjoy a far more privileged position.

T-Series is the dominant force in Indian recorded music. It’s a vertically-integrated behemoth, producing films and also owning the soundtracks at the moment they’re created, with no separate acquisition cost. It distributes those soundtracks on its own YouTube channel. Other labels have to win bidding wars for new film music, but T-Series doesn’t have to.

That structural advantage is what every other label is now trying to replicate in some form, and the most interesting move came from Saregama. In December 2025, Saregama announced a ₹325 crore investment in film director Sanjay Leela Bhansali’s production company. In return, Bhansali Productions agreed to exclusively sell its future Hindi film music supply to Saregama at a pre-agreed formula price. For Saregama, that was a relief — no more bidding wars for the next Padmaavat or Devdas-style soundtrack.

Saregama has been busy elsewhere too. In 2022, it terminated its global music licensing deal with Meta — Facebook, Instagram, Reels — because Meta wouldn’t accept Saregama’s new pricing. This meant that you could not use any of the Saregama songs while making your Reels. The deal was eventually restructured, and Saregama signed a parallel YouTube Shorts agreement in the meantime.

That episode was a showcase of the bargaining position of a music IP owner with a deep, highly-beloved catalogue. The platform has more substitutable songs than the label has substitutable platforms. But the songs that people actually want to use in their reels are not infinitely substitutable.

The other listed Indian label is Tips Music, which is the inverse of Saregama in almost every way. Tips runs a pure-play music IP business, with about 34,000 songs in the catalogue that are predominantly 1990s and 2000s Hindi film music. It has no hardware, no live events, and no film production drag. Its EBITDA margin sits around 70%, against Saregama’s 30% at the consolidated level. In 2024, Tips signed a global distribution deal with Warner Music and a publishing tie-up with Sony Music for global markets. The strategy was to outsource everything that isn’t owning songs, and milk the catalogue.

In essence, the Indian music business is a rights business rather than a platform business. The rights owners capture roughly the same money per stream regardless of which platform the stream happens on. They don’t particularly care if Wynk dies and its users move to Apple Music.

The platforms, meanwhile, are fighting for users who barely pay, and competing on prices that barely cover their costs. Same industry; opposite economics.

What could change this

The single biggest opportunity in Indian music — one that the whole industry is hoping for — is paid conversion.

Right now, 8% of Indian streamers pay for a subscription. If it moves toward the global average of 40%, the size of the Indian recorded-music industry could roughly quadruple over a decade. But, to be fair, that’s a fanciful projection.

Another tailwind is the catalogue-revival flywheel. You’ve probably seen this unfold many times — an old film song from the 1960s just resurfaces on Instagram reels today. That, of course, earns royalties again. Very interestingly, over 40% of India’s top 50 most-streamed songs in 2025 were released before 2020.

The risks are glaring and large. For one, India is likely to remain free-first for longer than anyone expects. Free YouTube, telecom bundles, and the residual culture of piracy all act as anchors on subscription growth. The optimistic story for Indian music labels requires Indian consumers to start paying for music in a way they have not done so for a quarter of a century. That’s a huge ask.

The second risk is the cost of content acquisition. Saregama’s management has disclosed that the price range of a typical five-song Hindi film soundtrack rose from ₹15–25 crore in 2024 to ₹20–35 crore in 2025. If the labels are paying more for content than they can earn from it over its lifetime, the headline revenue growth turns out to be unprofitable. This is exactly the risk that Saregama’s deal with Bhansali Productions is meant to manage.

The third risk is, well, AI. Universal, Warner and Sony Music have already sued generative-music platforms Suno and Udio for training their models on copyrighted catalogues without licences. Universal recently settled with Udio and announced a partnership to build a licensed AI music product instead — this might be the template the rest of the industry could follow.

India hasn’t yet had its equivalent legal moment, but the questions are already showing up in viral form.

One AI cover doing the rounds takes the title track of 2025’s Saiyaara and regenerates it in Kishore Kumar’s voice. Arguably, three things are being used here without permission — the composition, which belongs to whoever owns Saiyaara’s publishing; the master, which the AI manufactured rather than copied, leaving its status unsettled; and Kishore Kumar’s vocal identity itself, which has no clear legal home in India since he died in 1987. None of these have clean answers in current Indian law.

There’s music, there’s business, and there’s music business. Those three things only sound like they should overlap — and of course they do. As activities, they couldn’t be more different.

Tidbits

[1] MUFG enters Indian real estate

Japan’s Mitsubishi UFJ Financial Group (MUFG) is expanding its Indian operations by stepping into the real estate sector and offering forex derivatives. It is a strategic, albeit quiet, move by the Japanese banking giant to capture a slice of India’s property boom and meet growing corporate demand for financial hedging.

Source: Bloomberg

[2] Exporters ditch legacy banks for fintechs

Indian MSME exporters are abandoning legacy banks and the SWIFT network in favour of high-speed fintech payment rails. By securing direct access to core payment networks, fintechs are offering exporters faster cash realization, transparent FX conversions, and fewer hidden fees, marking a quiet shift in B2B banking power.

Source: Livemint

[3] Prada’s $881 “Made in India” bet

European luxury brands usually guard their “Made in Italy” tags fiercely, but Prada is breaking the mould by explicitly marketing a new line of $881 woven leather sandals as “Made in India.” It is a subtle but massive signal that global luxury giants are beginning to view Indian craftsmanship as a premium label rather than just a backend cost-saver.

Source: Economic Times

- This edition of the newsletter was written by Pranav and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Dr. Aradhna Aggarwal on SEZs, their role in economic development, and India’s growth ambitions

What role do SEZs play in the economic development of a country? When do they succeed and when do they fail, and how did different countries achieve success with how they attracted FDI? How have SEZs worked out for India, and how are they connected to our manufacturing ambitions?

To address these questions, we had a chat with Professor Aradhna Aggarwal. She is one of India’s foremost experts on SEZs, and her work spans industrial policy, international trade, and technology transfer. What follows a really illuminating conversation on international economic development and the Indian economy that might even trump some myths.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

While reading your second piece, it got me thinking, it’d be great to see more content on the business side of sports. Maybe a deep dive into the revenues, P&L, and overall financials of Indian leagues like the IPL, ISL, and others?

Excellent macro picture in both articles.