The fake Zerodha SMS scam | Why India's smallest businesses still struggle for credit

Inside SEBI's pump-and-dump investigation, and what new research says about the credit gap facing India's unincorporated enterprises.

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Why a gas cylinder stock exploded

A fake "Zerodha" SMS was never the scam, but, just the last piece of it. We break down how operators spent months rigging stock prices, used spoofed broker messages to lure retail investors, and eventually cashed out in what SEBI calls a large-scale market manipulation scheme.

Are India's smallest businesses getting loans?

India has spent years expanding formal lending to small businesses. But has that actually solved the problem? We look at new research that argues the real issue isn't whether businesses get a loan, but whether they get enough credit to grow—and why millions of India's smallest enterprises remain financially constrained.

Why a gas cylinder stock exploded

On paper, Mauria Udyog Limited makes steel gas cylinders. Back in 2017, its shares traded at roughly ten rupees apiece. There was little reason for it to go any higher. This was a small listed company, with no obvious growth story behind it.

But slowly, it started climbing — not dramatically, but steadily, and without any obvious explanation. The company hadn’t announced any new factories, it saw no sudden earnings jump, and there were no corporate announcements that would justify a re-rating. Nothing in the underlying business seemed to explain what the share price was doing. Yet, it kept rising — past fifty, past a hundred, past two hundred — until it touched ₹255.

Note: Account for a 1:10 stock split while reading the prices here

At that point, the stock got a lot of attention from major brokers. Or at least so it seemed, because traders began getting messages recommending that they buy the stock — from what, on the surface, looked like ICICI Securities, or even your own friendly neighbourhood brokerage, Zerodha. At the same time, websites with names like ‘midcapgains.in’ and ‘mbstocks.in’ pushed the same stock.

The public rushed in. In just a few days, trading volumes for the stock on BSE jumped more than sixteen-fold.

This was the story of many different stocks, in fact: Vishal Fabrics, 7NR Retail, GBL Industries, Darjeeling Ropeway Company — all of them saw the same pattern. Something smelled off. It seemed suspicious enough that SEBI began looking in. When the regulator finally came out with its order, on June 30, it described having uncovered as a scheme on “almost industrial scale.”

The messages

The most obviously suspicious link in this chain were the messages. It was clear that these were spoofed; brokers didn’t actually send them. But who did?

There are companies that help you carry out bulk messaging campaigns, called SMS resellers. These companies buy wholesale SMS credits, and give these out to anyone that wants to run a messaging campaign. Whoever was sending these messages had used the services of these companies.

The resellers had never met the person that had placed these orders. Everything had come to them online. But the orders had a digital trail: WhatsApp messages, emails, online payments. All of them pointed back to one person: Hanif Sheikh.

Only, Hanif denied everything. Those numbers didn’t belong to him, he claimed. At one point, he attributed everything to an entity called Darshan Orna. Later, his explanation shifted to a staff member named Inayat Deriya.

But the more SEBI looked, the more suspicious he seemed. They saw KYC filings, Yahoo account recovery emails, IMEI device identifiers, and cell tower data. Everything came back to him. He made flight bookings from that phone. He had a Swiggy account linked to the phone. The same device was used to book a Zomato order, to a hotel where he was staying at the time.

There was simply too much linking Hanif to those messages.

But bulk SMSs were only the tip of the iceberg. By itself, a bulk SMS recommending some obscure micro-cap would perhaps have done very little. Those messages had built themselves atop a base. These weren’t dead stocks — they were stocks that had seen a meteoric rise over the better part of a year. Those messages worked because they seemed to confirm a story: of a stock that — in the case of Mauria Udyog — had shot up 25 times in a few months.

Why did the stock move in the first place?

The price

There was something fishy in the lead-up to these SMS campaigns.

In the case of Mauria Udyog, for instance, eleven entities had been trading its price up for a long time. They would place orders within seconds of each other, often in tiny quantities, at prices just above the stock’s last traded price. The resulting movement looked organic. The stock, to naked eyes, would appear to be on an uptrend.

But was there any fraud here?

SEBI had run into this wall before. In many cases before this, people had made synchronised trades, often sending up the price of a stock. To courts and tribunals that heard them, though, this was hardly enough evidence. Buying a stock wasn’t fraud. Selling one wasn’t fraud. If SEBI claimed that such a series of such transactions somehow amounted to fraud collectively — because of how they were timed, or because of what their effect was — it needed to prove it.

For this, SEBI pointed to a few things. One, those eleven entities seemed suspiciously close to each other. They shared addresses, phone numbers, and bank accounts. And money seemed to move between them.

Moreover, Mauria Udyog wasn’t a stock that saw a lot of activity. Over its incredible rise, these eleven entities contributed 40% of all buy volume and 35% per cent of all sell volume. If you stripped just these eleven entities out, the stock’s trading volumes would crater.

That was why this seemed suspicious: why were eleven entities that all seemed linked trading in a stock that barely anyone else cared for? Why did their trades keep marking the stock’s price up? To SEBI, it was more likely than not that there was fraud underneath.

When the SMS campaigns began, a new group joined the fray. They made many small buy and sell orders on the same day — consistently losing money. Together, they lost roughly ₹37 lakh. Their trading didn’t make a lot of sense, but they made up almost a quarter of the trading activity in Mauria Udyog for as long as the campaign ran.

Why would anyone do this?

Here was one clue: it seemed like they were paid for it. One of these traders, for instance, had received ₹23 lakh from a connected company called GBFL. The very next day, he transferred that money to his broker and began trading in Mauria Udyog shares.

To SEBI, their trading seemed like the cost of pulling such a scheme off. Once traders poured in after the SMS campaigns, the stock would have to look liquid. These entities did exactly that: creating the appearance of active trading. It didn’t matter if they were profitable — their job was to make it seem like there was a lot of action in the stock.

But if this was actually fraud, how did it pay off?

The cash-out

All of this was meant to create a group of buyers interested in Mauria Udyog shares. Then came the dump.

A new group of entities — Mauria Udyog’s promoters, employees and contractors — stepped into the market to sell their shares. Many of them hadn’t traded in it before the SMS campaign, and wouldn’t trade after it. They had gathered their shares before the stock’s listing or through off-market transfers, and they sold them at the peak of its SMS-driven frenzy.

The money, however, didn’t stay in their accounts. Instead, it was all drained out instantly — to one of two entities: Linkwise and Vee-em. Curiously, these two entities had odd connections to Mauria. Both their email accounts, for instance, had the same recovery email: lmgupta@mauria.com. Mauria officials signed on their rent agreements. Mauria even listed them as its related parties in its financials.

And most tellingly, Linkwise and Vee-em sent money back to Mauria. They both had their excuses. Linkwise, for instance, claimed that it sold Mauria cattle feed and soya cakes. It even had GST certificates for these sales. Only, why would a company that made gas cylinders buy cattle feed? Plausibly, because cattle-feed doesn’t attract GST — so they could get certificates without actually paying any tax. Beyond that, they couldn’t produce a single invoice or e-way bill. Vee-em had a similar story of its own, but that too was full of holes.

Mauria Udyog’s promoters, however, weren’t the only ones that benefited from this.

There was another network that had off-loaded shares in the SMS-fuelled frenzy. The money then travelled through a series of accounts, for transactions that seemed unremarkable — business payments, loan repayments and the like. It was hard to see exactly where each payment went, rupee for rupee. At the end, though, much of that money seemed to land in accounts controlled by Hanif.

Proving anything, here, was a challenge. SEBI couldn’t map every single payment from start to finish — it had been recycled too many times. But to SEBI, this wasn’t necessary. It could clearly see the net effect: money went, via a series of accounts, to a series of beneficiaries. How it got there was irrelevant. Ultimately, it was more likely than not that this was a way to push out the proceeds of the fraud.

The same story, five times over

This didn’t happen once. Variations of the same playbook were visible across five different companies. There were minor differences across them — like different promoters, and different excuses. In one case, for instance, everyone pinned the blame on a mysterious figure named “Paresh Shah” — even though they couldn’t provide a phone number, an address, or any verifiable trace of this person. In another, BSE’s surveillance system killed the fraud before it could go through, forcing the operators to exit as a loss.

Ultimately, though, they all shared the same pattern: the same artificial price movement, the same SMS campaign, the same sudden jumps in trading volume. And at the heart of all of them was Hanif Sheikh.

In all, SEBI investigated 226 different people and entities. There were three it didn’t find any evidence against, and two that were only guilty of dumping their shares, and not outright fraud. Everyone else, though, was part of this massive scam network. It found nearly ₹140 crore in illegal gains, which it asked these entities to disgorge — along with 12% interest.

Beyond that, it handed out penalties and securities market bans to everyone involved. Hanif himself has been barred from the securities market for seven years, and fined ten crore rupees. His broader network saw bans of four to five years, and fines ranging from ₹5 lakh to ₹1 crore.

The stock market is replete with stories that look too good to be true. Often, that’s because they aren’t true. Many of these scams look obvious from the sidelines, in hindsight. But there’s no guarantee that you’ll see one that’s being played on you. As this case shows you, many of these scams are designed meticulously, over years, with explanations for anything that looks off. At many points, SEBI itself couldn’t prove that something was wrong, instead falling back on what seemed likely to it — and that was after years of investigation. You might not have that benefit.

We can’t speak for other brokers. But if you ever hear Zerodha asking you to invest in some stock, you can be certain that someone’s trying to dupe you.

Are India’s smallest businesses getting loans?

In 2020, two economists at the National Institute of Public Finance and Policy (NIPFP) took a giant government dataset on India’s smallest businesses and asked a simple question: which of them get a loan from a bank rather than a moneylender?

Five years later, the same two economists — Shivani Badola and Sacchidananda Mukherjee — took a newer version of the same dataset and asked a sharper one: which of them are actually starved of credit? The distance between those two questions helps us gauge where it is that India’s entire small-business finance infrastructure is stuck.

The firms in question are unincorporated enterprises, like the corner kirana, the roadside welding workshop, the single-truck operator, the two-person tailoring unit — companies that aren’t registered under India’s Companies Act. There are an estimated 6.5 crore of them employing around 11 crore people: the ground floor of the Indian economy, running on a chronic shortage of money.

That’s a huge shortage. The International Finance Corporation pegged the addressable credit gap for Indian MSMEs at roughly ₹25.8 lakh crore. And formal lenders do not serve this demand. That’s the backdrop against which these two papers are worth reading together.

What happened differently?

The 2020 paper sorted enterprises into a clean binary. You either had an outstanding loan from a formal source like a bank, or you had one from an informal source, meaning a moneylender, a supplier, a relative. Formal was the good outcome, informal the bad one, and the exercise was to figure out what pushed a firm from one column to the other. This framing also carried a hidden assumption: that a formal loan meant the problem was solved.

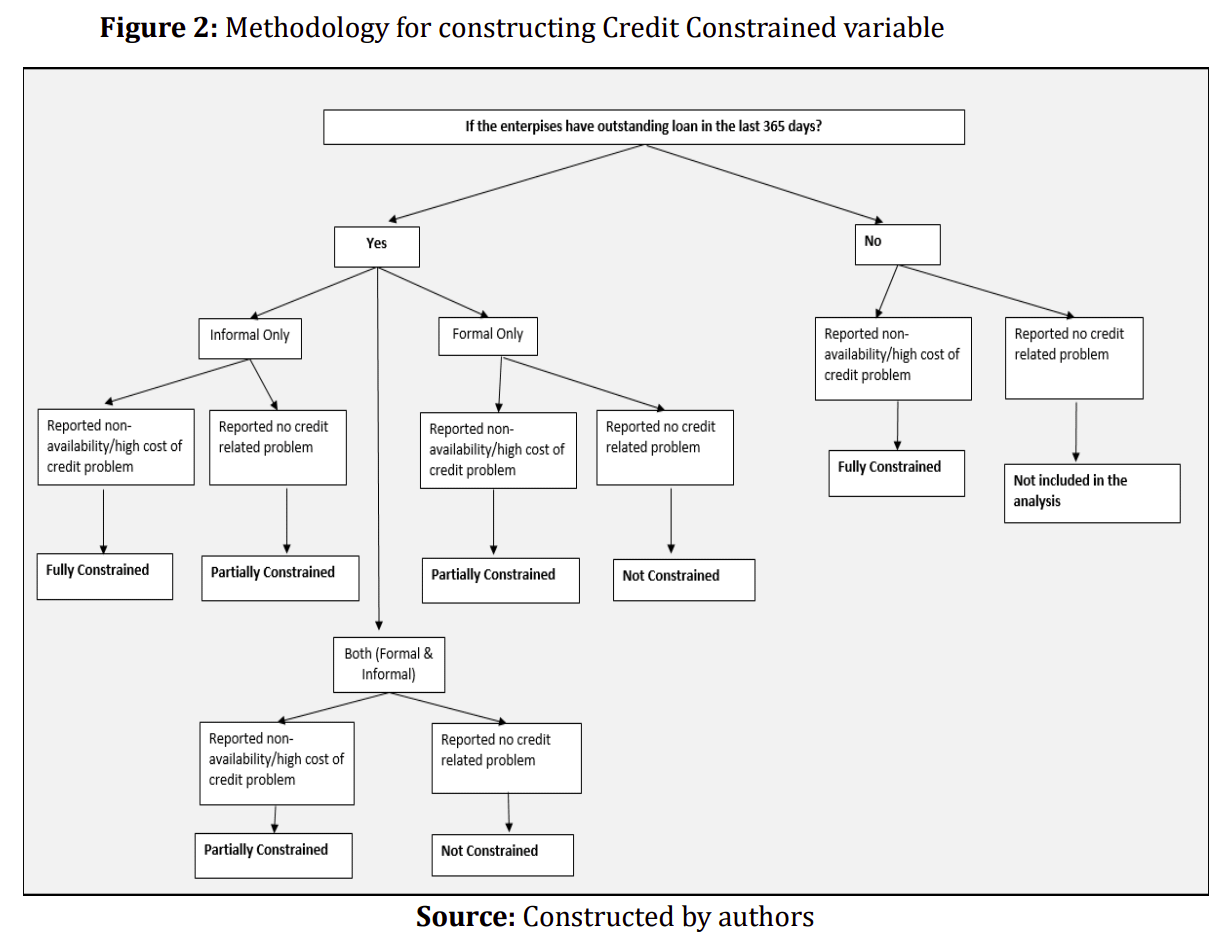

The 2026 paper is built to break that assumption. Instead of formal-versus-informal, it sorts firms into three buckets — fully credit-constrained, partially constrained, and not constrained.

This implies that a firm can now show up as holding a formal loan and still be counted as constrained, because the loan was too small, too costly, or came nowhere near what the business actually needed to grow.

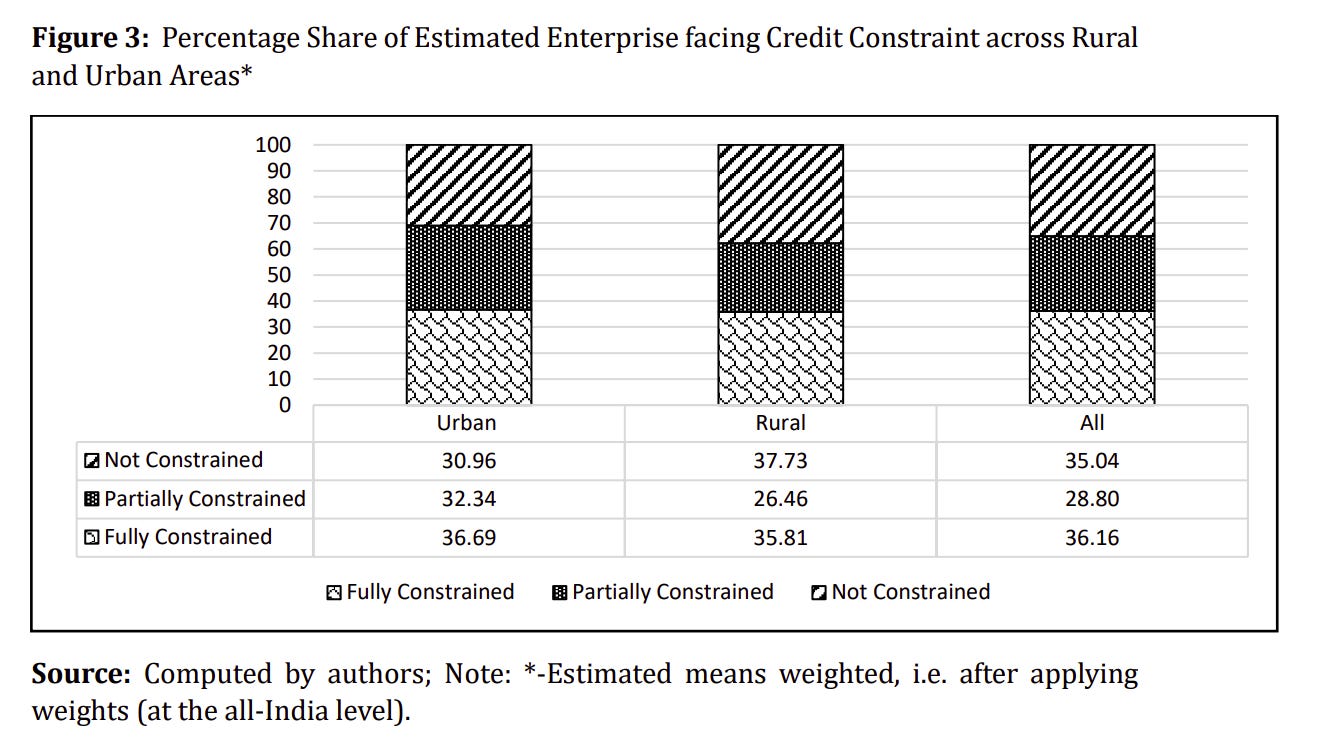

On the newer measure, only 35% of these enterprises are not credit-constrained at all. Roughly 36% are fully constrained and another 29% partially so. Basically, nearly two-thirds of India’s smallest businesses are unfortunately running on less credit than they could productively use.

One caveat worth mentioning is that the 2020 paper used the old NSSO enterprise survey; the 2026 paper uses its replacement, the Annual Survey of Unincorporated Sector Enterprises of 2022-23. The two aren’t perfectly comparable, so some of the differences between the papers may reflect the change in the ruler, but not in the thing being measured.

Smallness is the original handicap

Start with the headline finding that’s universal regardless of the ruler change: size predicts credit. Bigger turnover, more assets, more workers, a longer operating history — every one of these factors makes a lender more comfortable. Firms that have them borrow formally far more easily than firms that don’t.

The 2026 paper only sharpens this truth. Size makes you more likely to get a loan and less likely to be constrained. The relationship between size and credit isn’t linear. It curves, with the biggest reduction in constraint coming as very small firms grow into merely small ones, then flattening out. The handicap is worst precisely at the bottom.

Why does smallness bite so hard? It’s not because tiny firms are bad bets, but because they’re illegible ones. A lender looking at a two-person workshop with no filed accounts and no paper trail doesn’t get a lot of trust.

Which brings us to the most interesting shift in the paper.

Data, the new collateral?

You see, for most of the history of Indian lending, creditworthiness meant the assets you could pledge, like land, machinery, and gold. If you couldn’t put something on the table the bank could seize, you didn’t get the loan, or at least found it hard to get one. That world still exists, there is another logic that’s rising: where creditworthiness is built less from what you can pledge and more from what you can prove with information.

In the 2020 paper, all systems of record, from GST registration, business registration, books of account to internet use raised the odds of formal borrowing. In 2026, though, each one lowered the odds of being constrained in rough times. None of them is collateral. But all of them are data that allows a lender a more transparent look at an otherwise opaque little firm.

The single strongest signal of the lot, swamping every other variable in both papers, is whether the firm has a bank account. A bank account isn’t merely money, but also a stream of transactions a lender can read.

Manufacturing keeps drawing the short straw

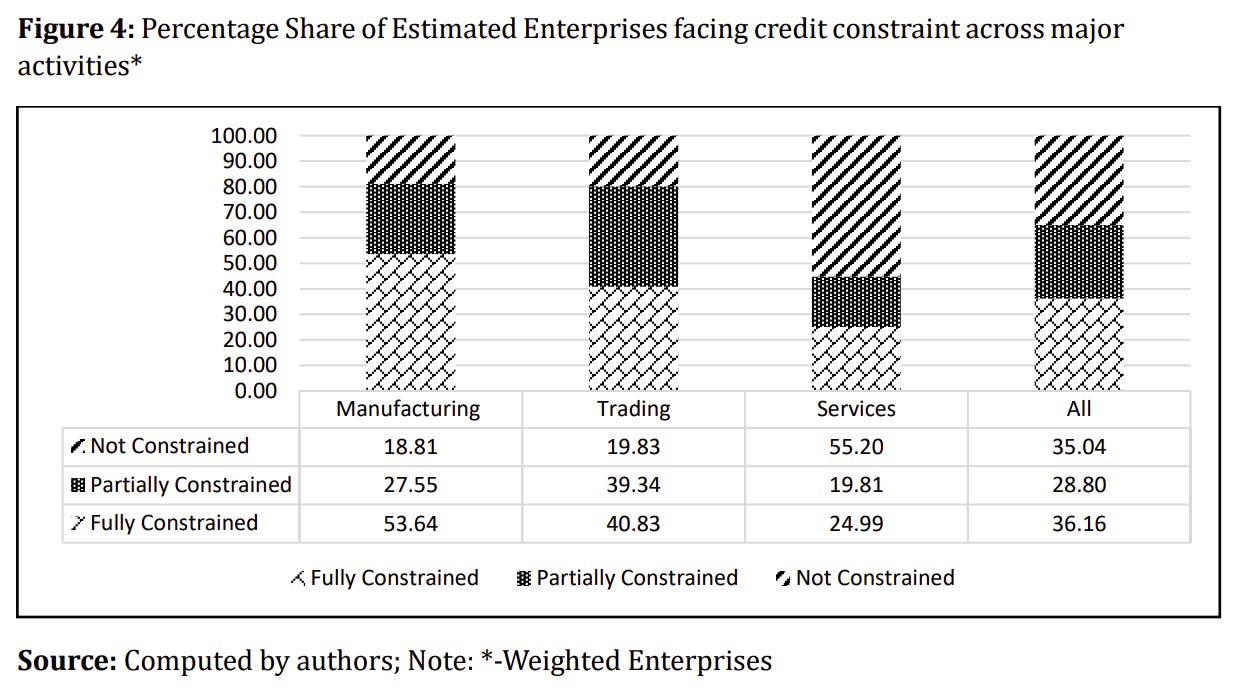

Across two decades of Indian research, the manufacturing sector keeps showing up as the neglected child of formal finance. That hasn’t changed in 2026, as the new paper identifies manufacturing as the single most credit-constrained category of business in the country. More than half of manufacturing units are fully constrained, against roughly a quarter of service firms.

As per the paper, a manufacturer comes out about 8% likelier to be fully credit-constrained than an otherwise identical services firm. The raw borrowing patterns say the same thing. Of the manufacturers who borrow at all, over half go to informal lenders, against about 25% of service firms. And where formal money actually lands, manufacturing holds a low share of ~15% of all outstanding loans to these enterprises, while services take more than half. Partly, this also reflects India’s heavy tilt towards services compared to manufacturing.

Manufacturing is, on the face of it, the sector you’d expect banks to like: it’s where the fixed, seizable assets sit, the machinery and sheds that can be easily used as collateral. So why is the asset-heavy sector the hungriest?

The papers are far more confident about the observation than the reasons behind it, so this is worth holding loosely. But they may include reasons we’ve discussed before on the Daily Brief. For instance, manufacturing may simply read as riskier to a lender because it can often be starved of working capital, or it often runs on tight margins which only come with scale. As per the 2020 paper, heavier exposure to operational shocks like power cuts, input shortages, sudden dips in demand pulled credit access down.

The reasons could be varied. But either way, manufacturing is the sector the country is trying hardest to expand, but also, sadly, the one our credit system serves worst.

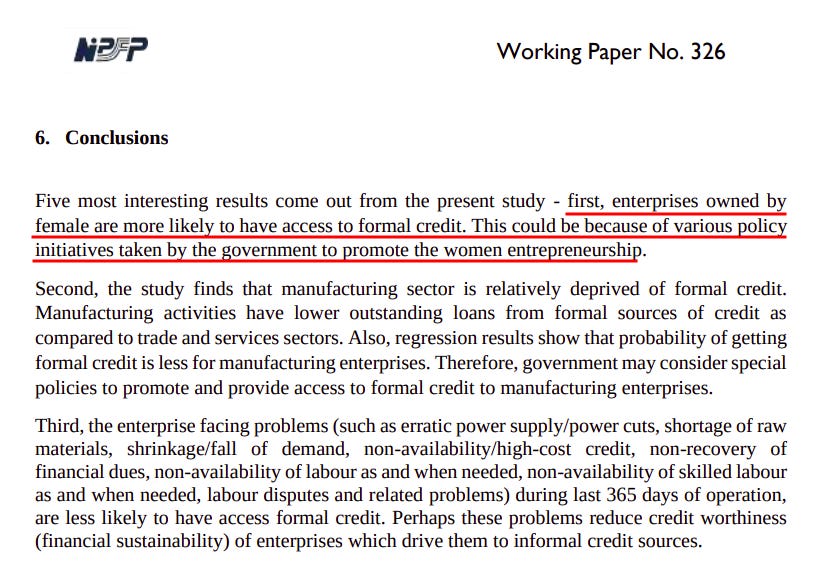

The gender puzzle

The 2020 paper also found something very interesting on gender lines: women-owned enterprises were more likely than men’s to hold a formal loan. The authors credited the wave of targeted schemes — like MUDRA, Stand-Up India, dedicated women’s credit lines — which were meant purely to push formal money toward women entrepreneurs.

But the 2026 paper somehow finds the mirror image. Female proprietors are more likely to be credit-constrained, not less — around 4% more likely to be fully constrained than comparable male-owned firms.

So which is it? Do the schemes work or don’t they? The resolution isn’t that the world reversed itself between 2016 and 2023. It’s that the two papers are measuring different things. “Did she get a formal loan?“ and “Did she get enough credit?” are separate questions. A woman entrepreneur can clear the first bar and still fail the second, because the loan is smaller, dearer, and further short of what the business needs than a comparable man’s would be.

The wider evidence only further spotlights the disadvantages female entrepreneurs face. An independent study using the very same 2022-23 dataset found women-owned firms less likely to get formal credit. When they did, they received smaller amounts. SIDBI put the credit gap for women-owned MSMEs at around 35%, against roughly 20% for men.

So, the 2020 report finding, read next to all this, looks less like a triumph and more like a measurement catching only the easy half of the problem.

The caste and geography fault lines

The 2026 paper opens up two further seams the earlier one didn’t touch.

The first is caste. The newer data lets the authors ask whether owners from Scheduled Castes, Scheduled Tribes and Other Backward Classes face steeper constraints. It finds that they’re significantly more likely to be fully or partially constrained than upper-caste owners.

One intuitive reason for this could be the historic lack of wealth that puts marginalised castes a lap behind. They tend to hold fewer assets and less land that they can pledge as collateral. Long exclusion from the relationships and references that formal lending ran on doesn’t help — which is why these borrowers have historically leaned so hard on moneylenders in the first place.

The second seam is geography. You’d expect urban firms, packed around bank branches, to be the better-served ones. Instead, rural enterprises come out less constrained. Roughly ~75% of the loan value rural firms carry comes from formal lenders, against about ~66% in the cities.

This difference, however, may be explained by the same phenomenon that determined access for female entrepreneurs — while more of them got credit, it was hardly enough.

See, India spent decades building priority-sector lending rules that compel banks to direct a slice of their lending to agriculture and small rural enterprise, regional rural banks, cooperative societies, and the vast self-help-group and microfinance networks that, in this data, count as formal credit. The urban micro-firm never got a delivery system built with the same intent. But rural units skew heavily toward the tiniest, own-account kind — the very category the same paper shows is most constrained of all.

So the rural advantage is real, but it is swimming against the current of what rural firms mostly look like, which arguably makes the reach of that inclusion machinery more impressive, not less.

Where the frontier has moved

The most useful thing these two papers do, read side by side, is mark a change in what we think the problem is. For twenty years the question was whether India’s smallest firms could get through the door of the formal financial system. That door has genuinely opened wider. On the old measure, that’s progress. On the new one, though, it barely makes a dent.

Tidbits:

Russia has started importing petrol from India by sea after Ukrainian drone strikes destroyed nearly 25-30% of its refining capacity. At least 60,000 tonnes have already been dispatched, with plans to import up to 4,00,000 tonnes a month.

Source: ET NowITC is entering the cola business for the first time, wanting to compete with Coca-Cola, PepsiCo, and Reliance’s Campa in India’s growing soft drinks space.

Source: ETAdani Group and Abu Dhabi’s IHC have signed an MoU to build a massive aluminium plant in Odisha with a $11.5 billion investment. The plant could increase India’s total aluminium capacity by nearly 50%.

Source: ET- This edition of the newsletter was written by Pranav & Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how large language model usage changed over the past eighteen months, through the public usage data of one busy AI marketplace.

Join us on WhatsApp, where we share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

This is a reminder that your edge will not come from finding secret tips; it will come from not falling for them, keeping risk small, and buying researched businesses only at sensible prices.