The cost of Building Your Dreams, Part II

BYD’s trials and tribulations to becoming the world’s largest automaker.

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The cost of Building Your Dreams, Part II

India’s jet fuel problem

The cost of Building Your Dreams, Part II

A couple of weeks ago, we covered one part of the history of BYD.

That part of the story seemed straight out of a movie — between a founder smashing their own prototype, drinking his own battery fluid, interest from one of the world’s greatest investors, multiple near-collapses, and a complete switch in the core business, BYD had it all.

We ended that story on a cliffhanger, when in 2019, BYD was facing its darkest hour.

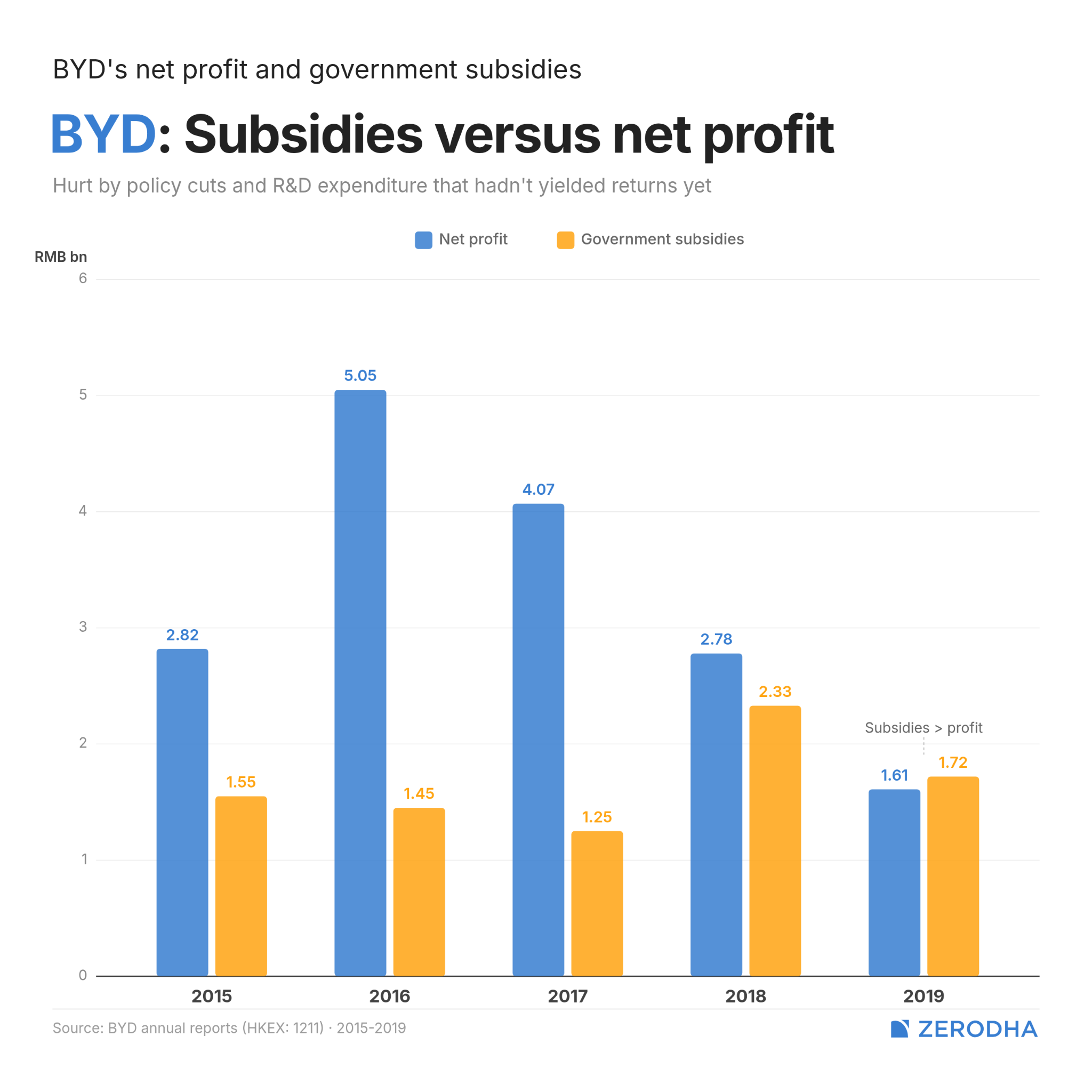

Between 2017-2019, profits had fallen consecutively. The subsidies that had sustained China’s electric vehicle industry were being cut back sharply, leaving BYD hobbled. On top of that, they were throwing tons of money on R&D that hadn’t yet yielded them rewards. And this was all before the pandemic.

But then, in three years, BYD went from selling fewer cars than a mid-sized regional automaker to selling over three million a year. It surpassed Volkswagen as China’s best-selling car brand. It had become the most important automaker on earth — perhaps too important.

This part of the BYD story starts with the very foundation of BYD’s business: batteries.

Back to basics

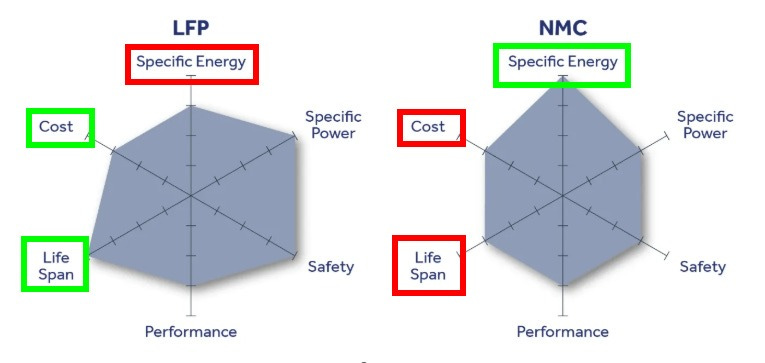

Until 2019, which is when China’s EV subsidies were pulled back, most serious EV makers had converged on the same battery chemistry: nickel-manganese-cobalt, or NMC. After all, NMC batteries pack more energy into a smaller space. Higher energy density means longer range, and range anxiety was the biggest barrier to consumer EV adoption.

But BYD had spent years going in a different direction. Its preferred chemistry was lithium-iron phosphate (LFP), which was cheaper to make than NMC. Additionally, it did not heat up uncontrollably, making it safer to use in an EV. NMC batteries, in contrast, were more likely to catch fire.

However, it was historically hamstrung by lower energy density. The auto industry saw LFP as suitable for, say, buses and taxis, but not competitive for the consumer passenger car market. We’ve elaborated on both these chemistry types in a past story on battery chemistry.

However, BYD’s engineers saw potential in LFP battery packs — particularly in their packaging.

You see, standard LFP battery packs built individual cells into modules, and then assembled those modules into a pack. But each layer of that structure added weight, took up space, and wasted volume.

BYD simply removed that module layer, and made those cells longer and thinner. That created far more space in the same battery pack, which meant more energy. And BYD did all that while also retaining everything else that made LFP attractive: lower cost, longer cycle life, and (improved) heat resistance. Their LFP was ready to compete with NMC batteries. In March 2020, this development was introduced in the form of the Blade Battery.

In an EV, the battery is the largest cost driver. The Blade Battery, then, would provide an immense cost advantage to BYD, which also manufactured its own batteries. This technology unlock basically gave BYD the mandate to set the direction the rest of the market had to follow. In fact, Tesla began using the Blade Battery in its Model Y, too.

Hero product

The commercial consequences of this were immediate.

As we’d mentioned in Part 1, BYD’s car portfolio was heavier on plug-in hybrid EVs (PHEVs), rather than pure battery EVs (BEVs). The hybrids used both a petrol engine and a battery, and the latter was the most expensive component. But now, with the Blade battery, their hybrids became even more attractive for those consumers who weren’t fully convinced about BEVs. Meanwhile, their BEVs also gained range they didn’t have before.

The first car model of BYD that carried the Blade Battery was the Han — a premium electric sedan priced above RMB 2,00,000 (~₹23 lakh at 2021 exchange rates). It was the first Chinese domestic-brand EV sedan to break through that price ceiling. And it sold very well, becoming the first in its class to sell more than 100,000 units in a single year. In 2022, the Han family ranked first in annual sales among B-class and C-class sedans across all of China.

The Han changed what was possible for BYD’s brand. The company had spent nearly two decades making cheap vehicles that often copied designs of other cars. They sold on price rather than desirability. But the Han was the first BYD car that people wanted to be seen in, and not merely a model that people bought just because it was subsidized.

But where the Han was a premium story, the BYD DM-i was a volume one.

Launched in 2021, the DM-i was a PHEV built around a highly efficient petrol engine and a large battery. Its price was directly competitive with equivalent petrol cars, not at the premium plug-in hybrids had always commanded. Official fuel consumption figures were 3.8 litres per 100 km, with a combined electric range of over 1,200 km. For a buyer unwilling to commit to a fully electric car, the DM-i removed almost every objection at no extra cost.

The market’s response was so strong that BYD couldn’t keep up with demand. Its 2021 annual report explicitly described the DM-i models as generating booming orders and persistent supply shortfalls. This was a product that people wanted to buy.

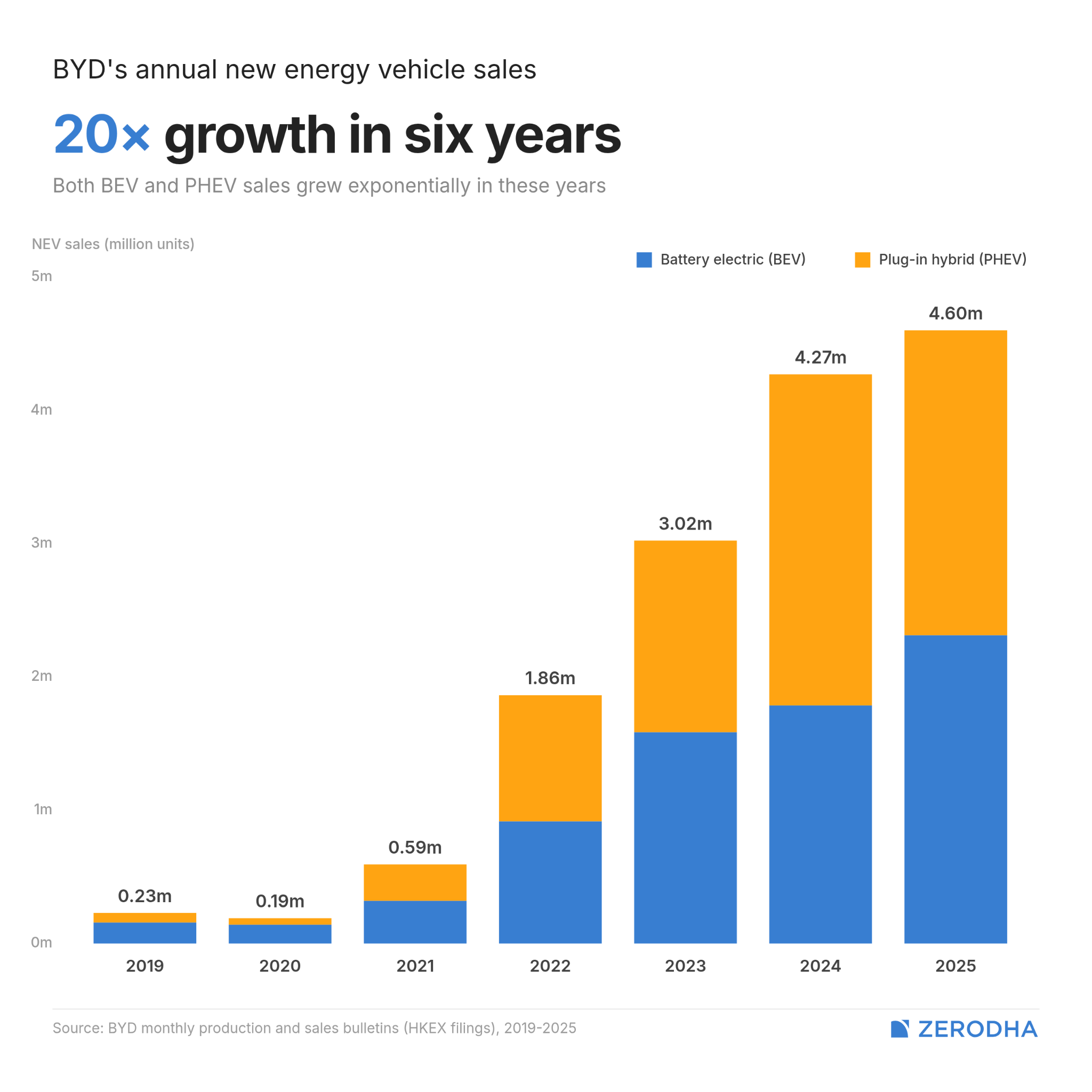

The numbers that followed were unlike anything the global auto industry had seen in decades. BYD went from over 6 lakh NEV sales in 2021 to 1.86 million in 2022 — triple the numbers in a single year. It crossed 3 million in 2023, and ~4.3 million in 2024. BYD was operating on escape velocity, leaving everyone else in the dust.

The factory inside the factory

To understand why BYD could move that fast while its rivals could not, you have to understand BYD’s outsider status.

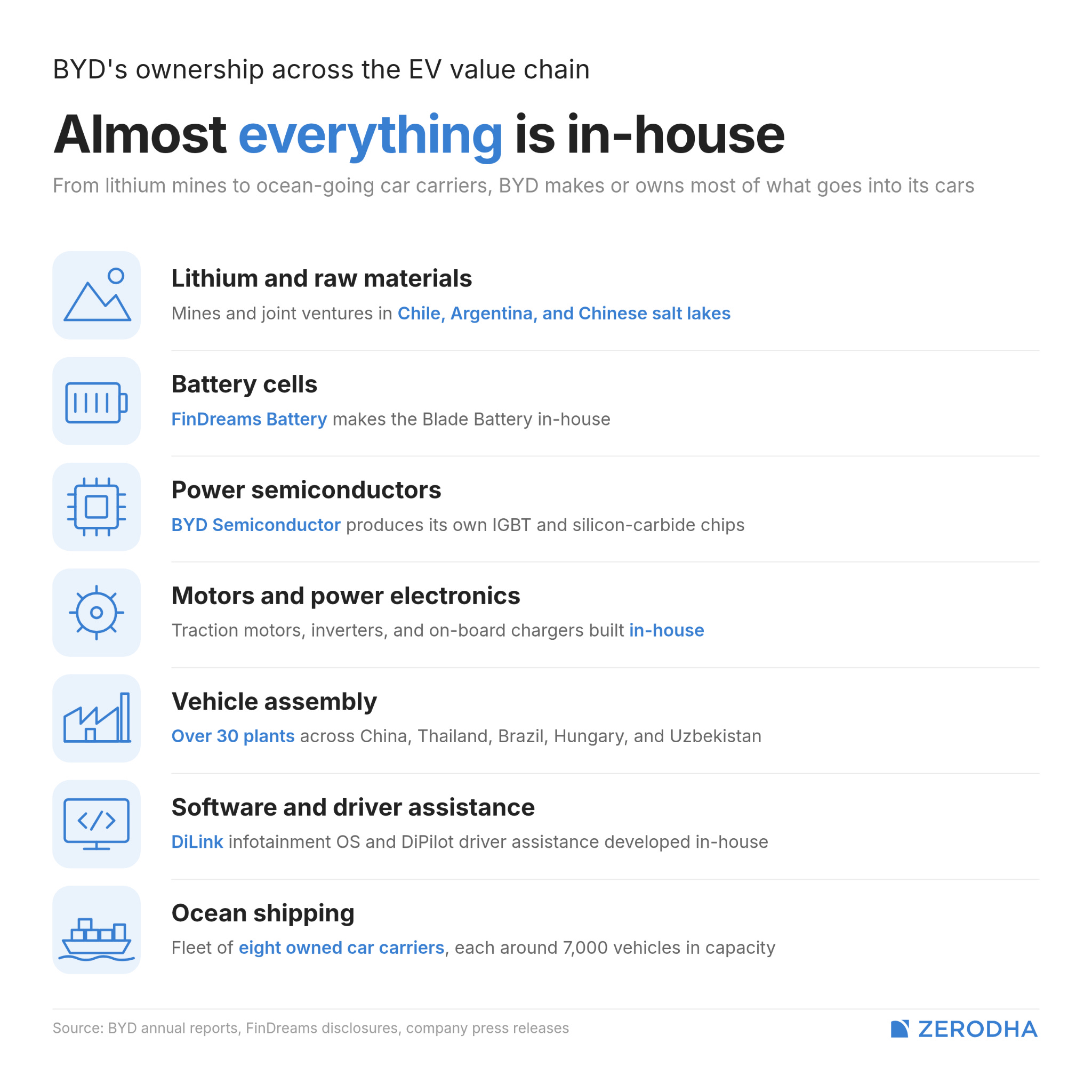

Unlike most of its rivals that started with cars and then went into batteries, BYD’s path is exactly the opposite. BYD is a battery company that built a car business to deploy its batteries at scale. The cars were downstream of the chemistry.

And if BYD was able to decide the playing field of the market — which it finally did with the Blade Battery — then plenty of their other bets would fall in place. The most important of those bets was a level of vertical integration not seen in the auto industry since Ford. Here’s what Nianqiang Wang, the VP of BYD, said:

“After we mastered the core technology [of battery], we started to integrate back to the raw materials and many components ... The biggest advantage [of this backward integration] is cost.”

Around 75% of BYD’s vehicle components are manufactured in-house. In 2019-2020, the company formalised this through their four FinDreams subsidiaries. These weren’t new businesses — they had existed inside BYD for years. Making them independent entities allowed them to sell components to other automakers and to operate with clearer commercial accountability.

Nowhere was this integration more valuable than in semiconductors. BYD had been developing power chips since 2004. IGBT chips are the high-power transistors that control electricity flow from battery to motor. By 2022, BYD Semiconductor was the second-largest Chinese supplier of IGBT chips, with a 22.9% domestic market share.

When the global chip shortage of 2021-22 forced automakers to halt production lines and write off billions in lost output, BYD kept building. Its output grew 156% in 2022.

The integration extends upstream to raw materials. In 2022, BYD partnered with SQM, Chile’s largest lithium producer, to secure stable supply. In 2023, it acquired mining rights in Brazil’s “Lithium Valley.” From mine, to battery cells, to finished vehicles, to even the ships that move the cars to global markets, BYD’s control over their own value chain is unusually gigantic.

This is the model Henry Ford pioneered a century ago. However, the American auto industry spent decades painfully unwinding because it eventually became a cost trap. BYD rebuilt it in a different era, for different reasons, and so far, it’s been a winning formula.

Scrappy winning

BYD’s unimaginable scale became an escape hatch for the defining feature of China’s EV market (and China as a whole) — its tendency to start price wars.

See, China’s subsidy policy for EVs meant that it had become easy for many players to enter the industry. But that also makes the industry prone to having excess capacity, as supply would usually outpace demand. However, no one would be willing to cut capacity because that means losing out on the benefits of scale.

The only rational response, then, is to cut prices until weaker players exit. We recommend our past story on how this is a key feature of the Chinese economy.

For instance, in early 2023, Tesla triggered a price war by cutting its China prices by between 6%-14% across models. The entire industry, both domestic and foreign automakers, followed suit. What had been a managed transition became an all-out price war.

BYD has the scale to withstand this, and has itself triggered price wars. But it’s not immune — its own net profit margin has compressed sharply, sitting at 4-5% as of 2025. Late last year, it lost $45 billion in market cap in a single selloff, as investors reckoned with the difference between revenue growth and earnings growth.

Going global, hitting walls

One answer to BYD’s margin compression in China has been to expand outside its borders.

Passenger vehicle exports grew 334% to ~2.43 lakh units in 2023. Overseas revenue reached RMB 221.9 billion in 2024 (~₹2.6 lakh crore). BYD now operates in more than 70 countries, with factories under construction in Hungary, Brazil, Indonesia, and Turkey.

But the global push has met a geopolitical wall.

The decision to expand globally doesn’t mean overcapacity is evaded. It simply means that other countries get flooded with China’s massive surplus. That, in turn, means that the car brands of those countries begin losing market share.

So, how do they respond? Simple: with tariffs.

In May 2024, the US raised tariffs on Chinese-made EVs from 25% to 100%. The EU imposed definitive countervailing duties in October 2024. The markets where BYD might have moved the most volume just shrank for all Chinese-made cars.

In response, BYD has offered to set up investments in those countries to avoid tariffs. But the complication that no factory can fully resolve is rules of origin. If the batteries come from China, does the car still count as locally made? The EU doesn’t yet have a definitive answer to that.

India represents perhaps the sharpest version of this dilemma. In 2023, BYD proposed a $1 billion manufacturing investment in partnership with Hyderabad-based Megha Engineering. The government rejected the proposal, citing security concerns about Chinese investment. Commerce Minister Piyush Goyal reiterated the position as recently as April 2025: “a no for now”.

Moreover, BYD’s investments abroad aren’t just under geopolitical scrutiny. In Brazil, for instance, their factories are being investigated for mistreatment of labor. In Thailand, they’ve been accused of unethical sales tactics.

BYD may have trained their sights on the world, but the world has looked back just as strongly.

Cockroach mentality

BYD’s success was hardly written in stone. Nor was its story linear.

Many of its successes weren’t planned, despite spending three decades accumulating battery chemistry knowledge, manufacturing discipline, engineering capability, and vertical integration. There were near-collapses, subsidy dependencies, mass rejections from dealerships, and years when mere survival looked difficult.

After 2019, all that accumulation turned into the unbeatable advantage that BYD is now known for. However, that advantage is inseparable from China — be it its supply chains, its structural overcapacity, or the state’s willingness to support all of those things. It also means their global ambitions are not just a business matter. They carry plenty of worldly baggage, too, as other countries deal with the costs of China’s domestic problems.

Meanwhile, competition in their own country has intensified as the rest of the industry has caught up with them. BYD’s rivals, Chery, Nio and Geely are also threatening its market share, innovating at a fast pace.

All of that is real.

But what’s also real is that two decades ago, if you’d asked anyone whether BYD would make a good car that people want, let alone lead the world’s EV transition, they would have laughed. That thought alone makes the rest of their story incredulous.

India’s jet fuel problem

India wants to become a global aviation hub. Airlines are ordering hundreds of aircraft, airports are expanding at breakneck speed, and passenger traffic is hitting record highs.

But there’s one problem: the fuel that powers all of this is among the most expensive in the world. Typically, jet fuel is the single largest operating cost of running an airline. On top of that, though, the crisis at the Strait of Hormuz has made flights even more expensive by making jet fuel harder to come by.

This story isn’t entirely about the state of jet fuel in India as of today. When we began looking into it, we realized that the cost story is still manageable. There is an interesting, less-talked about policy angle to how jet fuel is treated in India that’s just as important. And this has existed for ages, drastically impacting the economics of running an Indian airline.

That’s the story we’ll be narrating today.

Why you can’t just use cheaper fuel

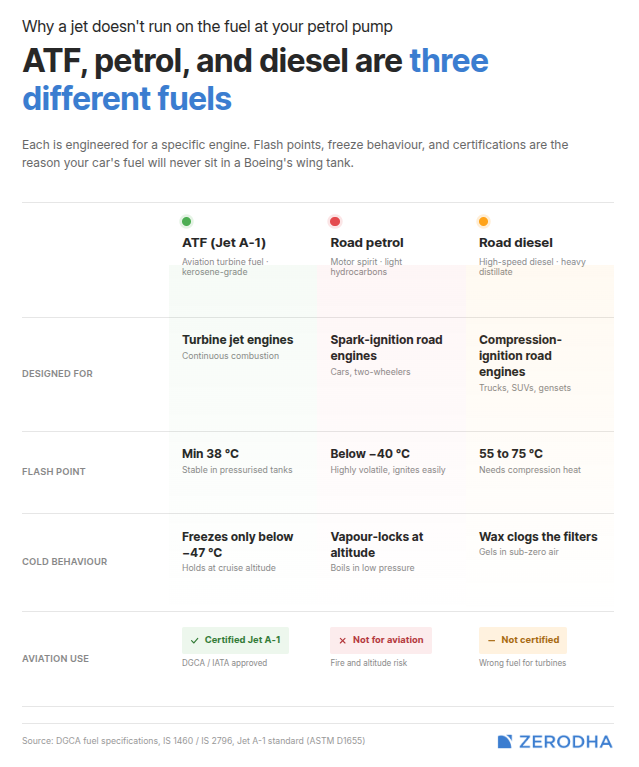

But first, let’s start with what jet fuel isn’t. It’s not petrol or diesel, but rather a very specific form of kerosene. And there are valid reasons for why neither petrol nor diesel suit aircraft.

To begin with, petrol vaporises too easily. In car engines, where it does work, petrol mixes with air and ignites inside a cylinder at ground level. But in an aircraft climbing to cruising altitude, the air pressure outside drops sharply — and lower pressure means liquids turn to vapour more readily. Imagine a bottle of fizzy water: opening the cap reduces the pressure and the dissolved gas rushes out quickly. Something similar happens to volatile fuels at altitude. This also means

The FAA calls this vapour lock — where fuel turns to gas inside the fuel lines or pumps before it reaches the engine, creating pockets that block fuel flow. With petrol, which is already extremely volatile at sea level, the risk at high altitudes is severe. BP’s own safety data sheet classifies petrol as an “extremely flammable liquid and vapour” and states explicitly that it is “NOT for aviation use.”

Diesel’s problem is the exact opposite — it doesn’t stay liquid in the cold. Diesel contains waxy compounds called paraffins. At low temperatures, these paraffins start to form tiny crystals, which clump together and clog fuel filters and lines. This also happens on the ground in cold winters.

In fact, it’s why diesel has its own specific test, called the cold-filter plugging point test, which measures the temperature at which diesel stops flowing through a standard filter.

That’s where aviation turbine fuel (ATF), which is a specific form of kerosene, enters.

For one, it’s designed to be stable on the ground. Unlike petrol, which catches fire very easily, ATF needs to be heated to at least 38°C before it gives off enough vapour to ignite. That matters when you’re pumping thousands of litres of it into an aircraft sitting on a hot tarmac. Second, it has to stay liquid in extreme cold. At 35,000 feet, the temperature outside an aircraft is around -55°C. The fuel sitting in the wing tanks gets very cold too. ATF is required to keep flowing down to at least -47°C, and in practice, most batches stay liquid well below that.

Most importantly, ATF has to work the same way everywhere. A plane that fuels up in Mumbai might fly to London and then on to New York. IATA’s technical guidance says aviation relies on common international standards because the same aircraft can refuel anywhere on Earth. So, any alternative fuel has to be a perfect substitute, not a rough equivalent.

So ATF is a tightly specified, safety-critical fuel with no easy substitute. Airlines have very limited negotiating leverage over the fuel they buy.

The Indian tax trap

ATF accounts for ~30-40% of an airline’s total operating expenses. Either way, no other single expense comes close. That alone would make fuel pricing a big deal for any airline.

But in India, the way ATF is taxed makes it worse.

For one, it was left out of GST when it was first introduced in 2017, and it still hasn’t been brought in. That means it gets hit twice: once by the Centre, and once by the state.

The central government charges 11% excise duty on ATF. On top of that, every state charges its own VAT. A December 2025 Rajya Sabha response said 21 states and union territories had reduced VAT on ATF. But the same response confirmed that state VAT still ranged from 0% to 29% across India. The same aircraft, flying the same route, can have wildly different fuel costs depending on where it fills up.

For instance, the difference in jet fuel taxes between Delhi and Uttar Pradesh is so major that with jet fuel at roughly ₹96,000 per tonne in Delhi, the 25% VAT adds about ₹24,000 per tonne. In Uttar Pradesh, where VAT is 1%, it adds under ₹1,000. A typical narrow-body aircraft on a Delhi-Mumbai flight burns around four tonnes of fuel. That’s a tax cost gap of roughly ₹92,000 per flight, just because of where you refuel.

What the 2026 shock did

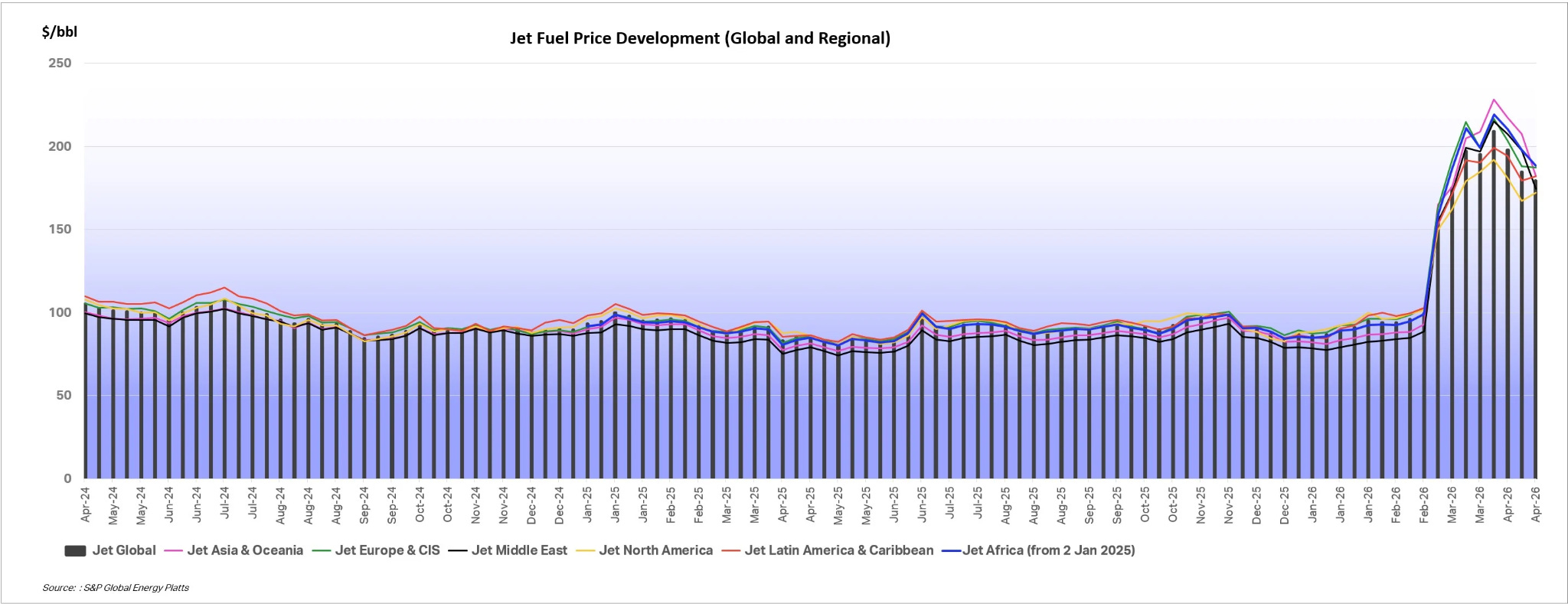

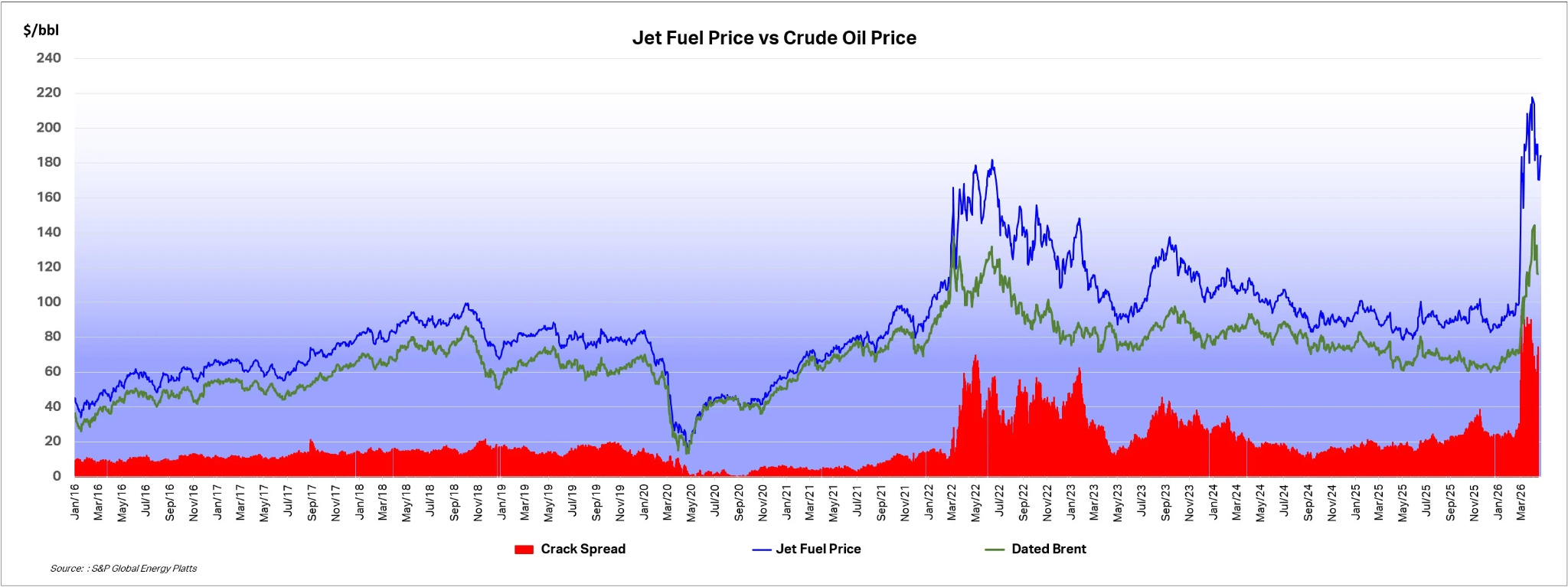

This tax structure was already painful, and existed well before this year. But 2026 was an upending of historic proportions.

According to IATA data, the global average jet fuel price went from $99.40 (₹~9,443) per barrel at the end of February to $195.19 (~₹18,543) per barrel by late March — nearly doubling in under a month.

The gap between crude oil and refined jet fuel rose from $27.83 (~₹2,643) to $81.44 (~₹7,736) per barrel over the same period.

That shock hit the Indian market fast. The Indian Oil briefly posted Delhi ATF at ₹2.07 lakh per kilolitre on 1 April, effectively a doubling from the previous month’s price.

The government intervened by capping monthly ATF price increases for domestic flights at 25%, with only a partial, staggered pass-through of roughly ₹15 per litre for domestic carriers. The revised domestic Delhi price was ~₹1.05 lakh per kilolitre, up from ~₹97,000 per kilolitre in March.

International operations did not get the same cushion, though. ATF pricing for international operations rose by ₹73 per litre in April — nearly five times the domestic increase — making international routes unviable.

What remains unclear is who is covering the gap between the actual market cost of jet fuel and the capped prices charged to airlines. If airlines aren’t paying the full cost, someone else must — either oil marketing companies are taking losses on their books, or the cost is being deferred and will surface later.

The response

The government tried to offset some of the pressure elsewhere. It cut landing and parking charges by 25% for domestic flights for three months, across both major and non-major airports.

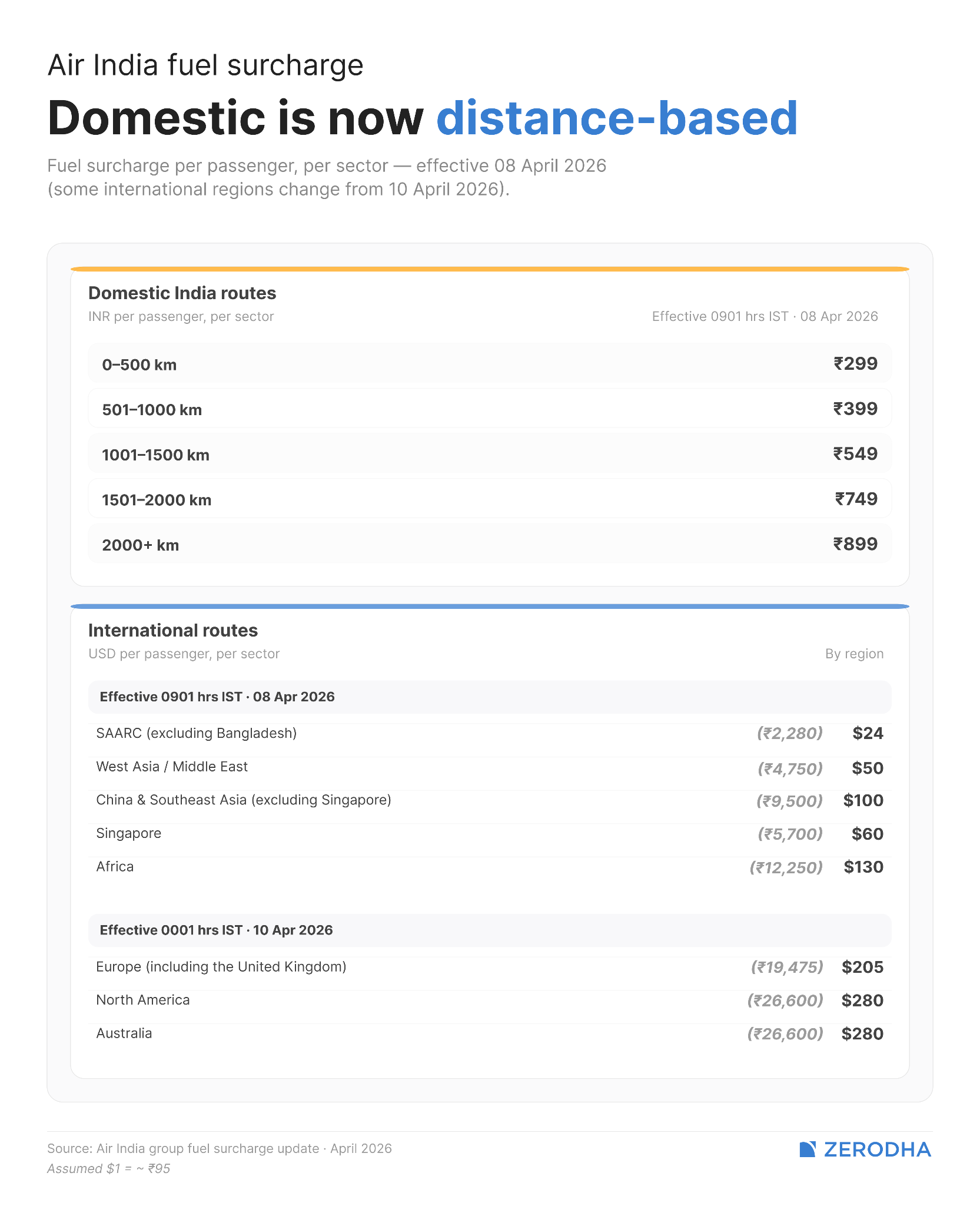

Airlines, meanwhile, shifted part of the remaining cost gap directly onto tickets.

For instance, Air India introduced distance-based fuel surcharges from 8 April — ₹299 for routes under 500 km, scaling to ₹899 for those over 2,000 km domestically, and up to $280 (~ ₹26,600) per route for North America and Australia. These still don’t fully compensate Air India for the international surge. IndiGo revised its own charges from 2 April.

In fact, on April 26, the Federation of Indian Airlines — representing Air India, IndiGo, SpiceJet, and Akasa Air — wrote to the civil aviation ministry warning that the industry was “on the verge of closing down or stopping its operations”. And the numbers explain why. Fuel had spiked to 55–60% of an airline’s operating costs in the current environment.

Their ask was specific: cut the 11% excise duty, push high-tax states to lower their VAT rates, and cap the margins of refineries to prevent extreme spikes in jet fuel prices. In other words, the industry isn’t asking for marginal relief — it’s asking for the biggest components of fuel pricing to be reworked.

Conclusion

These are short-term patches. The longer question is whether India can change what jet fuel is actually made of.

Even if (and that’s a big if) fuel prices cool down eventually, the tax structure won’t fix itself. ATF is still outside GST, and states still charge wildly different VAT rates on it. Most states have cut rates, but some of them still sit at 25% to 29%. And airlines don’t get to choose where passengers want to fly.

The industry isn’t asking for a favour as much as it’s asking for the basics to be reworked. Whether that happens after the pressure fades is another question entirely.

Tidbits

The Department of Telecommunications (DoT) has finalised the adjusted gross revenue (AGR) dues of Vodafone Idea Limited at Rs 64,046 crore as of December 31, 2025, following directions from the Supreme Court of India to consider the company’s grievances, said Vi in a statement. The revised figure is lower than the earlier provisional estimate of Rs 87,695 crore.

Source: Economic TimesIndia’s iPhone exports hit a record high in FY26, reaching ₹2 trillion in the final year of the production-linked incentive (PLI) scheme for large-scale electronics manufacturing, according to data submitted by vendors to the government.

Source: Business StandardSEBI has operationalised the Past Risk and Return Verification Agency (PaRRVA) framework to enhance transparency in performance claims made by market intermediaries.

Source:HinduBusiness Line

- This edition of the newsletter was written by Manie and Vignesh.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Dr. Aradhna Aggarwal on the role of SEZs in economic development

What role do SEZs play in the economic development of a country? When do they succeed and when do they fail, and how did different countries achieve success with how they attracted FDI? How have SEZs worked out for India, and how are they connected to our manufacturing ambitions?

To address these questions, we had a chat with Professor Aradhna Aggarwal. She is one of India’s foremost experts on SEZs, and her work spans industrial policy, international trade, and technology transfer. What follows a really illuminating conversation on international economic development and the Indian economy that might even trump some myths.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉