The conjurings of data center finance

How Data Centers Get Financed

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

How Data Centers Get Financed

SEBI’s final word on mutual fund rationalisation

How Data Centers Get Financed

Last month, Blackstone announced a $1.2 billion investment in Neysa, an Indian AI infrastructure startup, to build GPU-powered data centres across the country. It was among the largest data centre cheques ever written in India.

Blackstone is hardly alone. Several big investors — including sovereign wealth funds — have all been circling India’s data centre market.

This wave mirrors what’s already happened in the US, where data centre investment is becoming one of the defining asset classes of our time. Meta and Blue Owl Capital recently announced a $27 billion joint venture to build data centres — the largest deal of its kind in US history. Oracle secured an $18 billion construction loan for a single facility in New Mexico. Heck, this is becoming such a cultural meme that there’s even a game where you run a data center.

Underneath these humongous numbers is a head-scratching, long-winding maze of financial architecture. As a lender, for instance, you may be simultaneously underwriting real estate risk, power procurement risk, construction risk, and most importantly, the rapid depreciation of the hardware sitting inside the building. It’s easier to mismanage all these risks than not.

Previously, we covered how the AI industry may be a bubble. We didn’t get into the nitty-gritties of data centers source that capital. Today, we’ll walk through that question, and then briefly look at how this financial playbook applies to India. Given the complexity of it, we’re likely to miss a few nuances in this primer — hopefully, we cover them in a future edition.

The models

Before we get into the financing, it helps to understand the two broad business models a data centre operator can adopt.

The first is colocation. You build the physical facility — the building, the cooling systems, the electrical infrastructure, the security — and then become a landlord, leasing out space, power, and connectivity to tenants. Those tenants bring their own servers and GPUs, plug them in, and pay rent. In India, companies like CtrlS and STT Global Data Centres run this way.

The second model is compute-as-a-service. Here, the operator doesn’t just provide the building, but also owns the GPUs. They rent out computing power to tenants. Indian firm Yotta, for instance, runs this model.

Then, there are neoclouds. These companies don’t own the physical facility, but own GPUs and sell computing power, while renting the building. We won’t cover them here yet, but Neysa is mostly a neocloud.

This distinction — between a simple landlord and a compute-lord — is the thread that runs through everything that follows.

The development stage

The financial lifecycle of a data centre begins long before any concrete is poured. A developer must secure land, navigate zoning and environmental permits, procure power grid approvals, and even begin negotiating anchor leases with potential tenants. All of this carries plenty of risk. The uncertainty here is the highest because — forget signing tenants — you don’t even know for sure if your project will even be built.

That’s why the people most willing to write cheques at this stage are equity investors.

The project is ring-fenced within a Special Purpose Vehicle (SPV) — a legal entity specifically meant for one data center campus. Equity investors get an ownership stake in the SPV. They expect to make their reward through the value appreciation of the building once it’s made.

But equity is also the most dilutive and expensive form of capital. And every month a developer sits on equity-funded land without a cash flow is a month of lost returns. The primary goal, then, is to resolve all bottlenecks — land, power, permits — as fast as possible and graduate to cheaper debt.

Since both co-locators and compute operators invest in setting up the physical facility, this stage looks the same for both. For compute operators, though, there’s extra complexity — because they need to forecast which chips to order, how many, and when.

Building the powered shell

Once all the permits are secured and the construction contracts are signed, the first foundations are ready to be laid.

In many ways, this is just like any other construction project. What gets built, right now, is the “powered shell“: the physical building, cooling systems, and power grid interconnection. And the financing of such projects is similar to that of infrastructure or construction. Banks and NBFCs give them construction loans, underwriting the risk of building the facility.

The standard instrument used here is the construction-to-mini-perm loan. This typically lasts for 2-5 years — covering the construction period, plus initial operations. Over this time, you build the data centre, move tenants in, let revenues stabilise, and then refinance the mini-perm into something longer-term.

Often, big lenders aren’t fully comfortable underwriting all the development-stage risks. For instance, maybe the power grid is yet to be fixed, and connection delays could wreck the project. In that case, developers sometimes get mezzanine (or mezz) loans for the remaining amount. These sit below senior lenders in the repayment hierarchy, getting paid after them — but in return for that risk, mezz debt also carries a much higher yield.

In the colocation model, this is the extent of the risk. Lenders are okay bearing it because the building itself will ideally last for 2-3 decades. But what happens when we introduce GPUs into the mix?

Construction lenders often avoid underwriting the GPUs and servers themselves, because they depreciate too fast for a traditional lender’s comfort. This also means that, compared to the long duration of a standalone building, GPUs will be perceived as a very different asset — one that is less stable, and more short-term. This is one of the key reasons an operator may need a mezz loan.

In such cases, the financing for the construction and for the GPUs is often split. An operator may get long-term construction debt, and much shorter GPU-backed loans on the side. Alternatively, lenders may demand the entire holding company as collateral if they’re funding GPUs, rather than just the project SPV.

Whither stability?

Once basic construction is done, the financing story splits in two.

For colocation operators, the data centre now becomes a predictable cash machine. They get on long-term tenants that move in, plug their equipment, and pay rent. The construction guarantees the developer had provided to lenders are now dropped, and cashflows become more stable.

The developer’s goal, now, is to execute a “take-out“, where expensive short-term construction debt is replaced with cheap, long-term financing — like a term loan from a bank, or a bond.

In the US, one popular exit is asset-backed securitisation (ABS). Here, the data centre’s lease cash flows are pooled into a new SPV. Rating agencies evaluate the creditworthiness of the tenant and the stability of the cash flows — the longer tenants stay, the better. If all goes well, the SPV can issue 15-20 (or even 25) year bonds. These bonds are tradeable in capital markets, and therefore are highly liquid — especially if the tenant ends up being a Big Tech hyperscaler like Microsoft or Google.

For compute operators, in contrast, there’s little stability to be found even now. After all, how do you issue a 10-year bond on GPUs that depreciate in just 2-3 years? Few institutional investors want to hold a long-term bond backed by an asset that could be worthless in a couple of years. This makes it very difficult for compute operators to issue investment-grade bonds.

So, compute operators try to enforce revenue predictability in other ways. For one, they may ask for large advance payments. Secondly, they may heavily prefer long-term lease contracts over shorter ones. Neoclouds, specifically, lock in tenants into take-or-pay contracts — if you’re an AI lab that wants compute power for some time, you’ll have to pay the operator for a fixed capacity regardless of whether you fully use it or not.

Naturally, their financing toolkit also looks different. Equity is quite common here. Private credit has also picked up many of these decks, looking for higher yields in exchange for the added risk. Some compute operators have even issued non-investment-grade “junk” bonds.

Where India stands

How much of this financial architecture actually applies to India?

The development stage looks broadly similar. Indian operators, like those elsewhere, still need to secure land, power, and permits. They too fund this largely through equity and promoter capital. But from the construction stage onward, the picture diverges significantly.

In the US, the financial lifecycle is a three-act progression: equity, then construction loans, then a shift to long-term debt through a securitized take-out. But in India, stages two and three are fused into one.

Rather than replacing their loans with capital market instruments, Indian data centre operators typically secure what are called Lease Rental Discounting (LRD) loans — and that too from banks instead of capital markets. In LRD, much like ABS, the borrower pledges their future rental income as security for the loan. Only, these go to a bank rather than a bondholder. These run for far longer than a construction-to-mini-perm loan.

CtrlS, for instance, has promised 45% to 50% of its future rental inflows to secure its borrowings, with term loans stretching out to 2041 — 15 years from now. STT GDC India holds loans maturing as late as FY2043.

This has one key advantage: a single loan fulfils most of Indian operators’ needs without having to repeatedly restructure their balance sheet. But the downsides aren’t small either — it concentrates risk in India’s banking system, which isn’t really equipped to manage GPU-linked exposure. They can’t tap the deep, liquid capital markets that let US developers recycle capital at scale.

Indian operators rely instead on a mix of bank debt, internal accruals, and crucially, equity infusions from the parent company. STT GDC’s credit rating, for example, leans heavily on the “strong parentage“ of its parent company Temasek Holdings, which infused ₹2,450 crore in equity over 3 years to support expansion. Should this link to their parent company weaken, so will their credit rating.

India’s data centre financing ecosystem is functional, but it’s still a bank-and-promoter story, without the benefits of a sophisticated capital market. As our financial markets mature, though, that may well change.

Conclusion

We know that this was a lot to take in — it was for us. But this just scratches the surface!

We’ve only covered the financial side of things here: how capital markets, banks and financial institutions adapt to data centre needs. But to this, you add hyperscalers, neoclouds and AI labs that actually deal with computing power. That’s when our earlier story on AI being a bubble comes in.

More importantly, we’ve barely touched on what this means for India. Our AI data centre boom is slowly, but surely taking off. But we come to this with very different priors. How we deal with risks related to construction, power and land permits will be very different from anywhere else in the world. And those bottlenecks will eventually make themselves seen.

We get the feeling we’ll be talking about this again, before it’s too long.

SEBI’s final word on mutual fund rationalisation

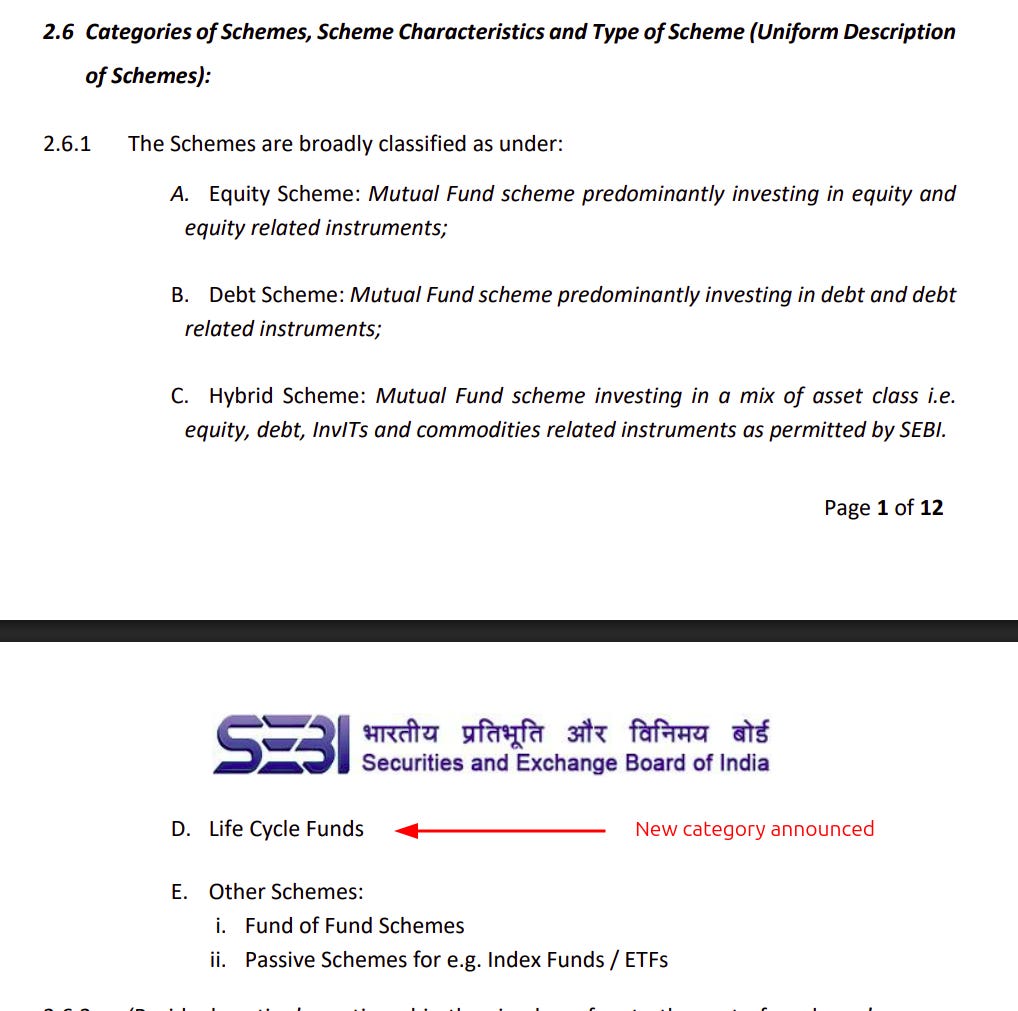

Last July, we wrote about SEBI’s consultation paper on revamping how mutual fund schemes are categorized. That was a draft; a set of proposals open for public feedback. Seven months later, the final circular is out. It looks rather different from what was first proposed. While some part of the original draft survived, some ideas were dropped entirely, and in some cases, SEBI even took a u-turn.

The one change that stands out the most, perhaps, is one of SEBI’s most ambitious moves for retail investors in years: the introduction of lifecycle funds.

Let’s start with a quick refresher.

Why this matters

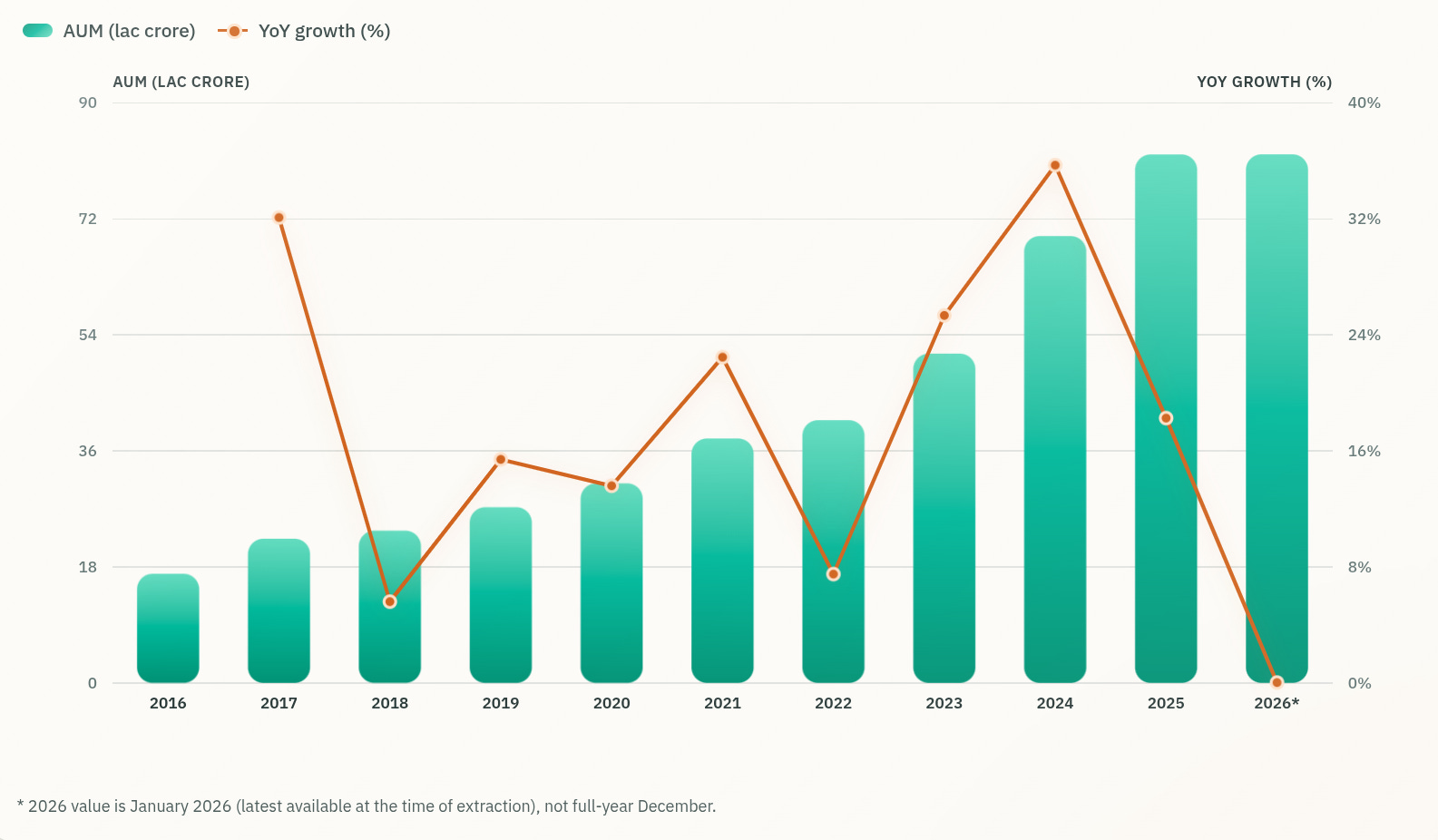

India’s mutual fund industry manages about ₹81 lakh crore today. Back in 2017, when SEBI first came out with its categorization rules, that figure was just around ₹20 lakh crore. While the industry quadrupled, over the years, the basic regulatory architecture hasn’t moved.

Here’s the original problem: before 2017, fund houses would launch dozens of schemes with fancy names that, under the hood, all did roughly the same thing. A single AMC would have funds with fancy names — like “Growth Plus Fund” or “Dynamic Returns Fund” — all of which would hold nearly identical portfolios. Investors had no way of telling them apart. So, SEBI came out with a straightforward fix: one scheme per category per fund house, with clear definitions of what each category meant.

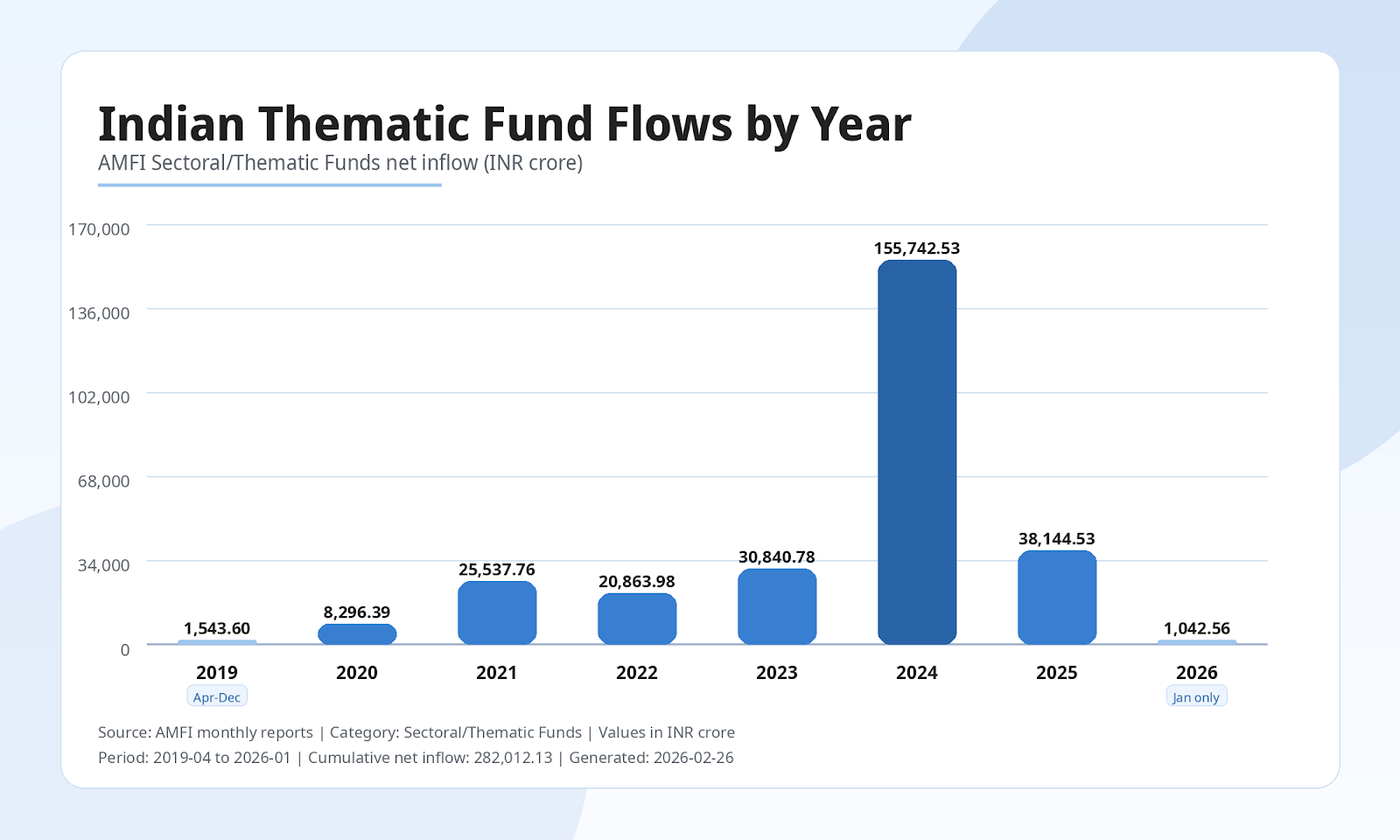

That brought much-needed order. But by 2025, the old classifications had fallen behind the times. There were new asset classes like REITs and InvITs, now, which didn’t exist in 2017. Meanwhile, thematic funds had exploded in popularity, with investors pouring over ₹1.5 lakh crore into them in 2024 alone — more than large-cap, mid-cap, and small-cap funds combined. Many of these thematic funds held suspiciously similar portfolios, but on paper, they worked within SEBI’s framework.

Meanwhile, goal-based investing — an idea that had become central to retirement planning in countries like the US — still didn’t have a proper framework in India. It was a glaring hole in India’s investment landscape.

SEBI’s consultation paper, released in July 2025, attempted to address all of this. And now, we have a final circular which tells us what actually made it through, and what didn’t.

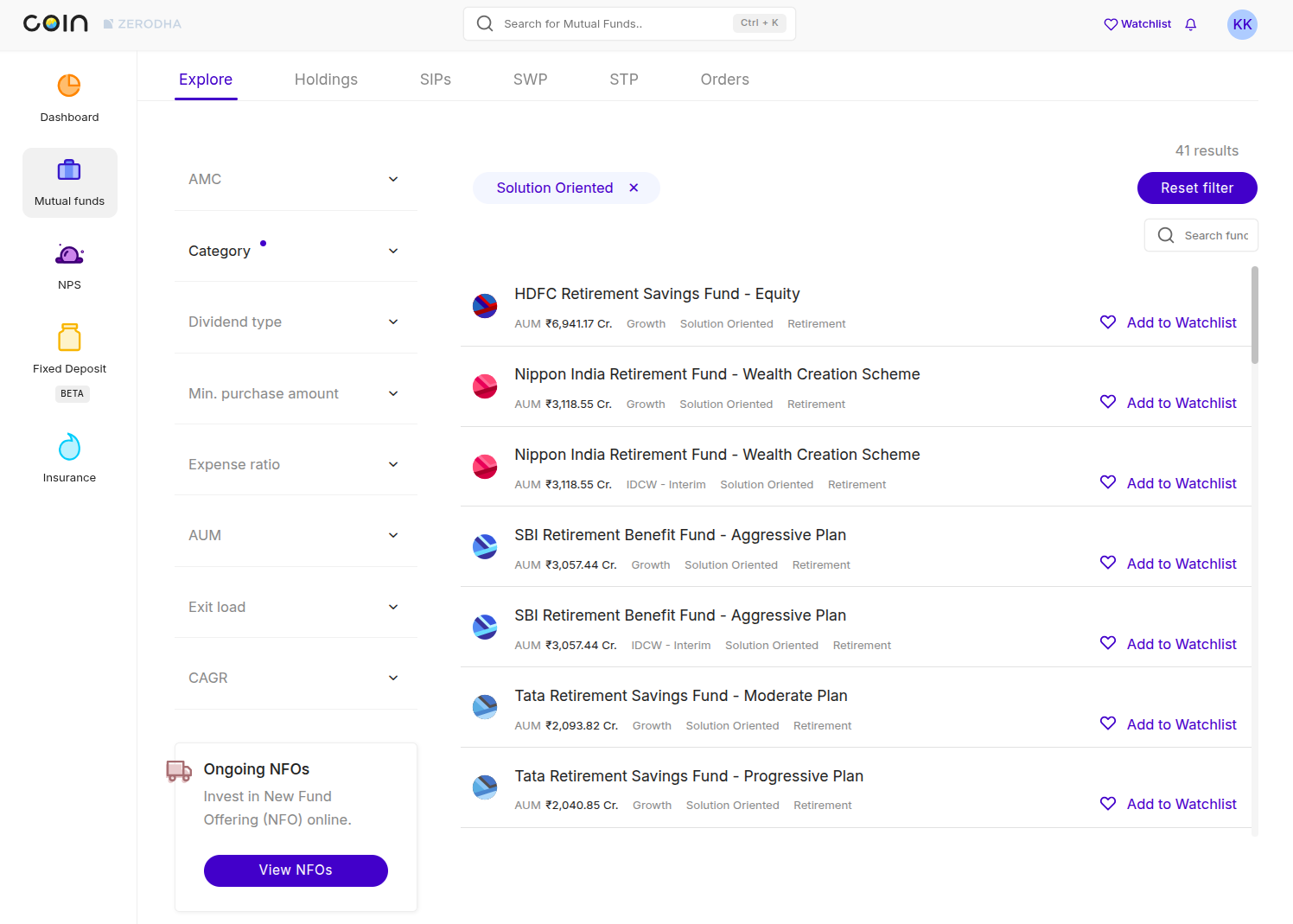

Solution-oriented schemes are gone

Here, perhaps, is the biggest reversal from the consultation paper.

Last July, SEBI proposed expanding its “solution-oriented” category. These were schemes designed for specific goals like retirement funds and children’s education funds. Their allocations would suit the solutions they were catering to: so, for instance, something meant for younger investors would be more equity-heavy, while middle-aged investors would be given something more hybrid. Similarly, if someone’s financial goals were nearby, they would be offered a debt-heavy scheme.

This seemed like a reasonable expansion of investor choice.

The final circular does the opposite, however: instead of expanding them, SEBI has discontinued solution-oriented schemes entirely. Existing schemes in this category, too, must immediately stop accepting new subscriptions. They’ll eventually be merged into other schemes with similar asset allocations and risk profiles.

To be fair, these schemes were less a “product category” than a mere label, as Dhirender Kumar from ValueResearch put it. There’s nothing a solution-oriented fund really does that regular funds don’t. A rupee that goes into your retirement fund isn’t too different from a rupee that goes into a balanced fund. If you want, you could withdraw money from your retirement fund and take a vacation; it’s not as though the fund is monitoring what you do. There’s very little that the label actually means. It’s usually just marketing.

In killing these funds, though, SEBI made space for a new product, which made a lot of sense but had not existed in India yet.

Enter lifecycle funds

Here is the biggest development from this circular: SEBI has elevated ‘lifecycle funds’ (also called target-date funds) from a brief mention in the consultation paper to a full-fledged, standalone category with detailed rules.

Here’s how they work: you pick a fund based on the year you want to achieve a financial goal — say, retirement in 2050. In the early years, when you’re far away from your target date, the fund invests heavily in equities. This makes sense: after all, you have decades to ride out market volatility, so you might as well chase returns. As 2050 gets closer, though, the fund starts shifting how it allocates your money, toward safer assets like debt. By the time you’re within a year or two of your goal, when swings or crashes in the market can hurt you the most, a majority of your corpus shifts to low-risk instruments, insulating you from the worst risks.

The potential of these funds

The introduction of these funds is a big deal; target-date funds completely transformed retirement investing in the United States. Their beauty lies in the fact that they’re a behaviour-friendly product. Most people don’t want to — or don’t know how to — rebalance their portfolio every few years. Few people sit down at age 45 and think, “I should shift 15% of my equity allocation into short-term bonds.“ Target-date funds solve this by making that reallocation automatic.

These funds were invented in the early 1990s by Wells Fargo. For a while, they were relatively obscure. In 2006, however, the US Department of Labor allowed them as default investment options in 401(k) retirement. That was the turning point. Suddenly, money flooded in.

A decade later, by 2017, US target date funds had crossed $1 trillion in assets. By the end of 2025, their assets had passed $5.2 trillion, growing 21% in a single year. Vanguard alone manages nearly $1.8 trillion in target-date funds. About 62% of American workers in their twenties with a 401(k) retirement account now hold target-date funds.

Will we see something similar in India? That depends on execution. The US boom was powered by a specific regulatory push. India doesn’t have an exact equivalent. But if NPS or EPFO-linked structures were to adopt a similar default mechanism, the potential is enormous.

But the case for these funds is strong. Just about 8% of our population invests in mutual funds. Financial literacy, too, is a major challenge. A product that simplifies people’s decision-making, in such a space, could be revolutionary. Instead of asking investors to do complicated maths, balancing between fourteen types of equity funds and eleven types of debt funds, you can just say: “When do you want to retire?“

The answer tells you where to put your money. The rest will be handled for you.

The specifics

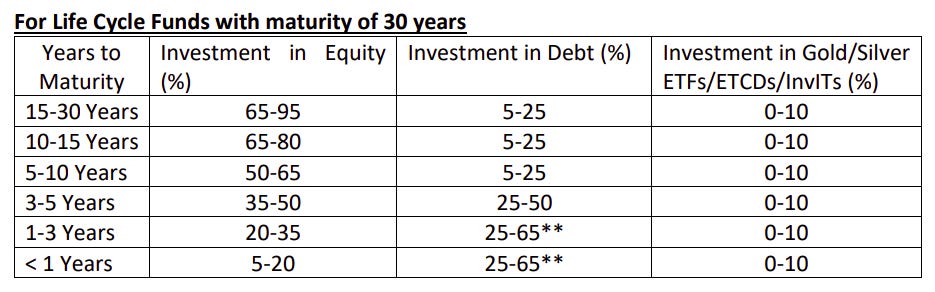

These funds come in many flavours. For instance, the AMC can decide whether it’ll follow active strategies or passive ones. Similarly, they can pick different tenures — ranging from 5 to 30 years, in multiples of five. SEBI has laid out specific glide paths for different fund tenures. A 30-year lifecycle fund, for instance, starts with 65-95% in equity and ends with just 5-20% in its final year.

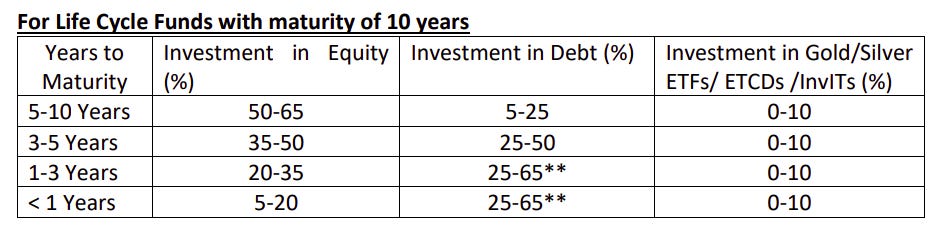

A 10-year fund starts with 50-65% equity and follows a steeper de-risking schedule.

The point of a target fund — and the way they work best — is to have you commit to a term, and then stick to it. To enforce this discipline, SEBI has built in steep exit loads: 3% if you pull out within one year of investing, 2% within two years, and 1% within three. The message is that these lifecycle funds are meant for those who can stay the course.

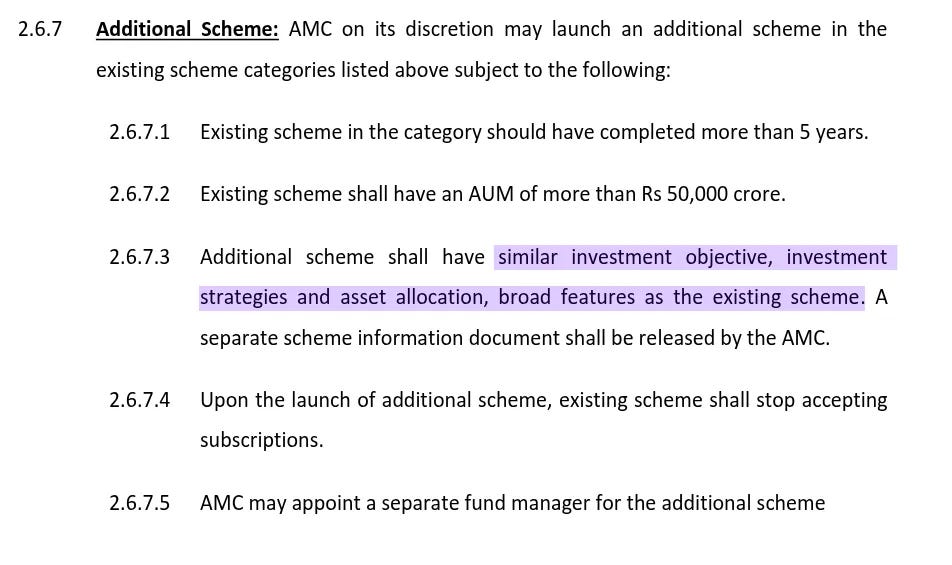

The mega-fund duplication idea? Dropped

In the consultation paper, SEBI had proposed something curious: allowing AMCs to launch an additional scheme in the same category, provided the original scheme was at least five years old and had over ₹50,000 crore in assets under management.

The logic was that a fund could become so large that it starts to have market impact problems. At that point, minute changes in their allocation, of even a few basis points, could send prices swinging — making it much harder for the fund manager to buy or sell stocks.

Only, the proposal raised more questions than it answered. For one, the new fund had to mirror the original’s investment strategy. What, then, was the point? How would investors differentiate between the two? In a roundabout way, this threatened to re-introduce the duplication problem SEBI had spent years eliminating.

SEBI, too, saw the issue with their proposal. The final circular makes no mention of it.

Thematic funds: real differentiation, or else

One of the defining trends of the Indian mutual fund industry, in recent years, has been the explosive growth of thematic and sectoral funds. Thematic fund inflows, for instance, jumped from about ₹31,000 crore in 2023 to over ₹1.4 lakh crore in 2024.

There was a catch, however: often, despite different names, these funds held very similar stocks. A “PSU equity fund” and an “Infrastructure fund” from the same AMC, for instance, could both end up loading on large PSU bank stocks. Then, an investor that bought both would think they were diversified, even though they weren’t.

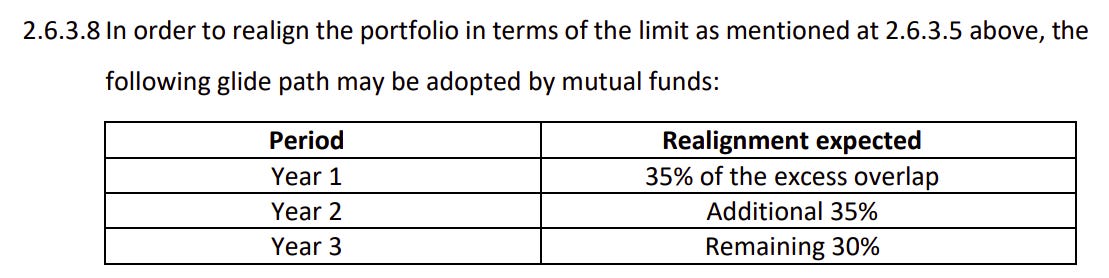

SEBI’s fix, proposed in the consultation paper and confirmed in the final circular, is a 50% overlap cap. That is, no two sectoral or thematic funds from the same fund house can hold portfolios that overlap by more than half. Existing funds will get a three-year glide path to comply — they’ll have to resolve 35% of the excess overlap in Year 1, another 35% in Year 2, and the remaining 30% in Year 3. If they can’t, they’ll have to merge.

This is sensible, even if the timeline is a little generous. Three years is a long runway, and fund houses will likely spend the early phase figuring out just how much shuffling is required before doing the minimum.

The smaller changes

Beyong this, there are few other tweaks round out the circular. We’ll cycle through them quickly:

One, since 2017, SEBI had forced fund houses to choose between offering a value fund or a contra fund, but not both. Despite their different philosophies — value investing looks for fundamentally underpriced stocks, while contrarian investing bets against prevailing market sentiment — SEBI thought the two ended up with near-identical portfolios. But the consultation paper proposed allowing both. The final circular confirms it. To ensure that they’re different, no more than 50% of the portfolios of the two funds can overlap. There are currently only three contra funds in the market, so this could open the door for more launches.

Two, debt fund naming has been simplified. The term “duration” might sound confusing, so it’ll now be replaced with “Term.”

SEBI has also introduced sectoral debt funds. Until now, there were sector-specific equity funds, but not for debt. Now, however, you can now invest in bonds from a specific sector — though SEBI has restricted this to five sectors: Financial Services, Energy, Infrastructure, Housing, and Real Estate.

Finally, the fund-of-funds framework has been formalized. What was previously a loose “Other Schemes” bucket now has a detailed structure with specific categories, naming conventions, and strict caps on how many FoFs an AMC can launch.

A cleaner framework

This is a significant new chapter in SEBI’s attempt at cleaning up the mutual funds landscape, which began in 2017. The core architecture remains intact, but these tweaks are meaningful. There are important new ideas — like lifecycle funds — and critical fixes to the imbalances the markets were developing.

Of course, every such change comes with their own challenges. Take lifecycle funds: with ~40 AMCs, each of which can launch up to six lifecycle funds, you’re looking at ~240 variants. Do we just add another layer of “which one to pick?”

That clean-up, however, is an endless cycle. On the whole, we’re excited to see how this works.

Tidbits

Global smartphone market to shrink 13% due to memory chip crisis: The AI boom’s demand for advanced memory has drained global supply, and IDC now expects smartphone shipments to fall from 1.26 billion in 2025 to 1.1 billion this year. Manufacturers are killing off entry-level models and pushing consumers toward pricier devices — IDC says cheap smartphones are essentially gone for good.

Source: Business StandardHyatt wants to 5x its India hotel count in five years: Hyatt’s CEO, speaking at the HOPE hospitality conference in Goa, said the market warrants five times the company’s current 55 India hotels within five years. Hilton and Marriott are also aggressively expanding, and Leela’s CEO noted the country only has ~30,000 luxury keys for 1.4 billion people.

Source: ReutersLeela Palaces bets on India’s luxury room shortage: Leela’s CEO said FY27 growth will be driven by a structural supply crunch in luxury hotels, with affluent spending holding up even as broader consumption slows. Occupancy hit 71% and RevPAR climbed 20% in the December quarter.

Source: Reuters

- This edition of the newsletter was written by Manie and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading,” where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Even I wrote about it a while back

https://www.linkedin.com/pulse/3-trillion-guessing-game-chirag-pachisia-lryrf/?trackingId=%2BTT%2Fzt9jDVsADeGv2zdo6Q%3D%3D

I think the lifecycle fund is a great introduction however current NPS structure generally take care of this, until lifecycle fund can introduce gold, invit etc as part of fund it still better to be in NPS as NPS doesn't have the heavy exit load. Also any formula created by AMC will not be as accurate as person having the flexibility to create there own allocation because the exit date can change for people, life doesn't have certainly as mathematical equations