Welcome to Beyond the Charts. A series where we break down what’s happening in the world of finance and the economy through charts, in a way that’s easy to understand.

For all the sources mentioned in this video, check out our newsletter. Link is in the description.

Here’s a piece of geography most people never really think about—until suddenly it starts showing up everywhere in the news: the Strait of Hormuz.

It’s a narrow stretch of water between Iran and Oman, barely 33 kilometres wide at its tightest point. But despite how small it looks on a map, it carries an enormous amount of the world’s energy. On a normal day, around 20 million barrels of oil pass through this corridor, along with roughly a fifth of global LNG supply. In other words, a huge share of global energy trade depends on a shipping lane that, in places, is narrower than many cities are wide.

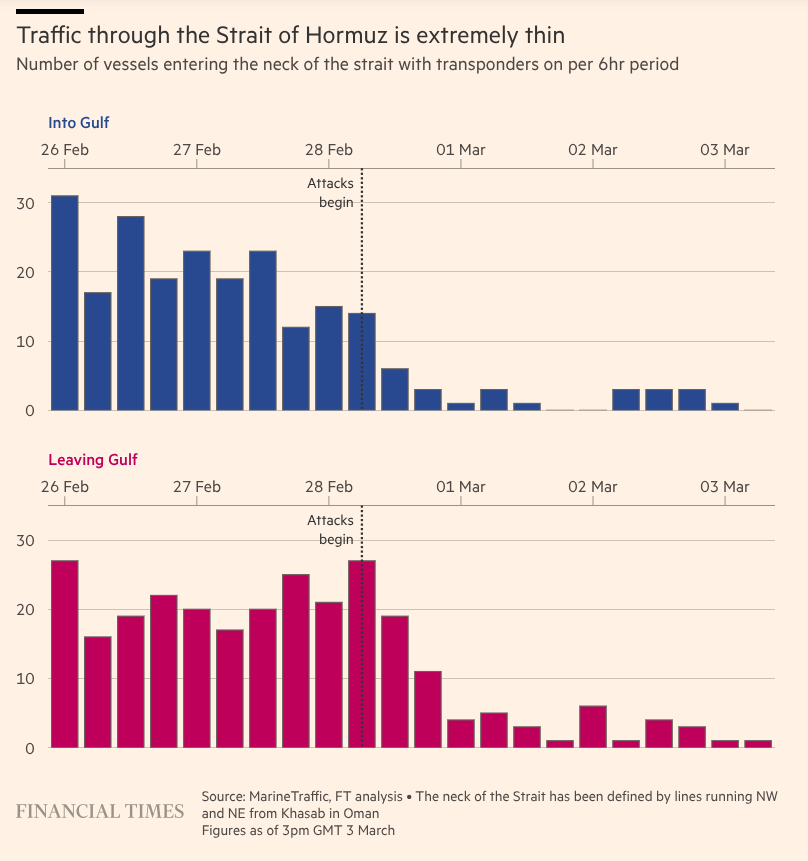

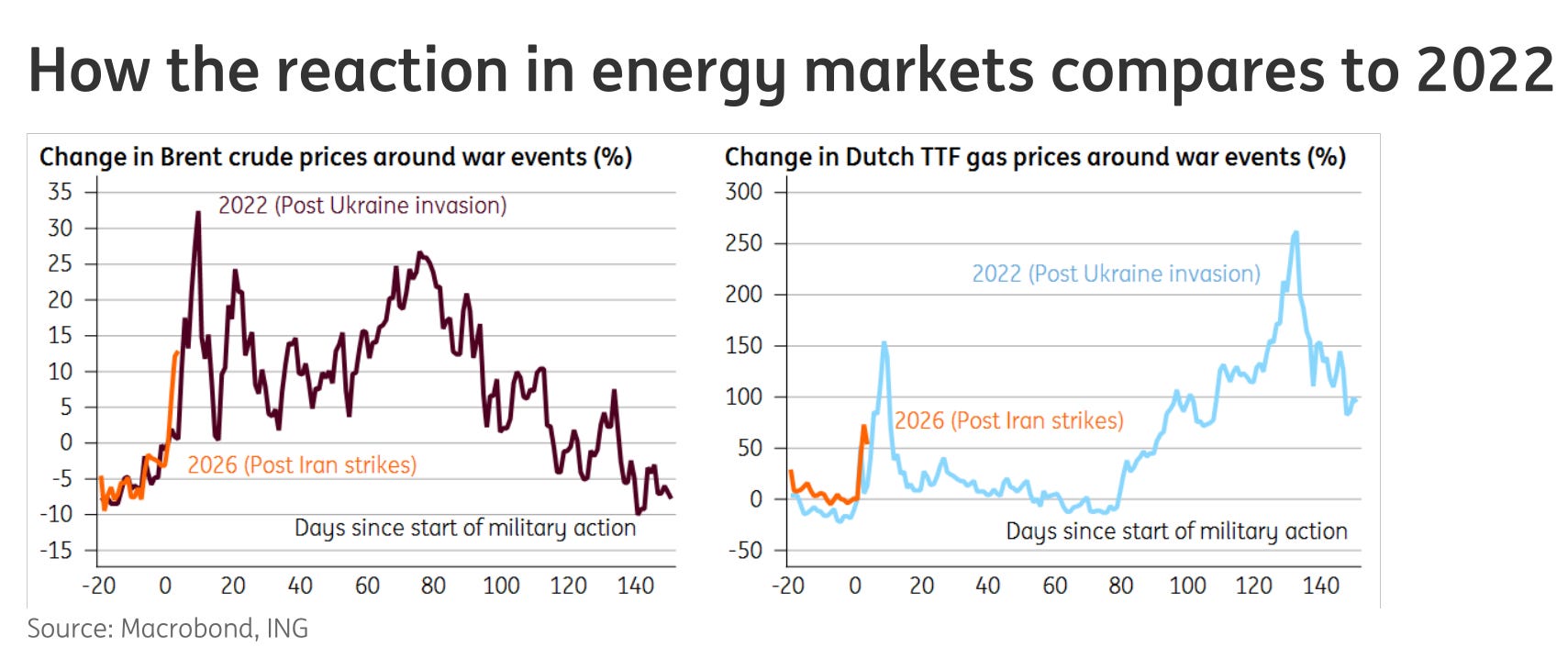

That’s why the war that erupted at the end of February quickly became more than just a regional conflict. After coordinated US-Israeli strikes on Iran and Iranian retaliation across the Gulf, activity in the Strait of Hormuz—the main artery through which Gulf energy reaches the rest of the world—started to slow.

Ships stopped moving. Insurers pulled back. Tankers began waiting outside the strait instead of sailing through it. And that’s how a military conflict suddenly turned into a global economic story. When so much of the world’s energy moves through a single narrow passage, even a small disruption is enough to shake markets.

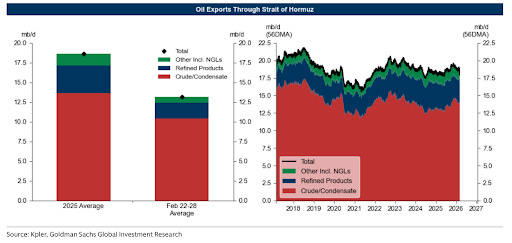

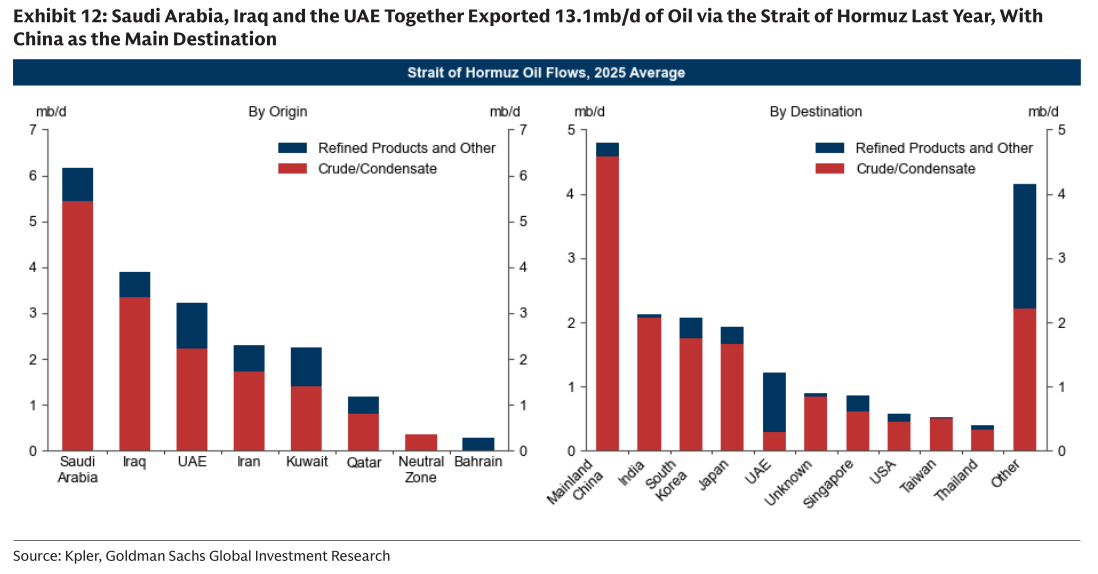

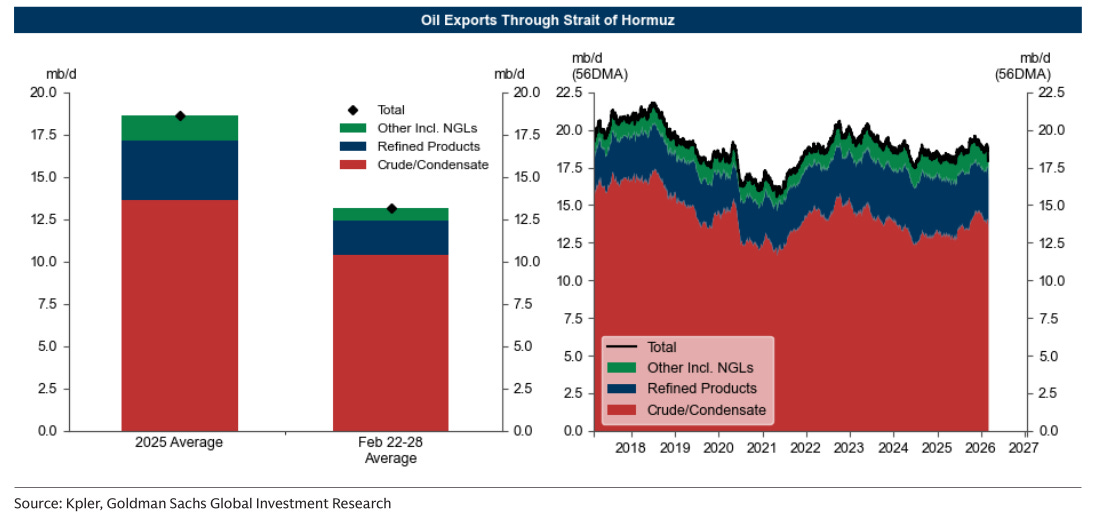

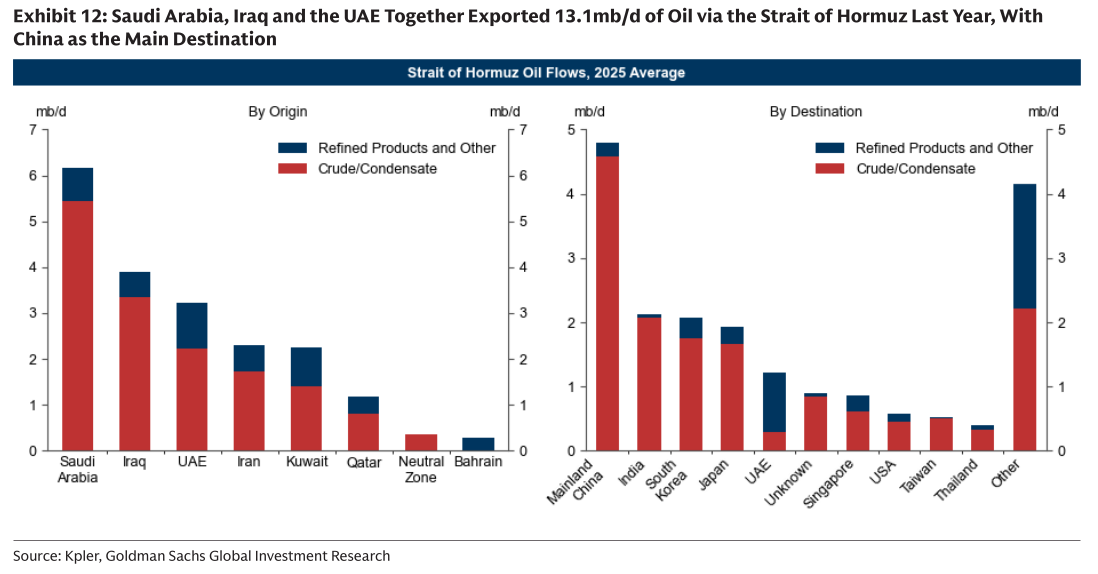

According to Goldman Sachs, nearly 20 million barrels of oil move through the Strait of Hormuz every single day. In 2025 alone, about 13.4 million barrels per day of crude exports passed through this route. Most of that came from three countries—Saudi Arabia, Iraq, and the UAE—which together accounted for roughly 13.1 million barrels per day of those flows.

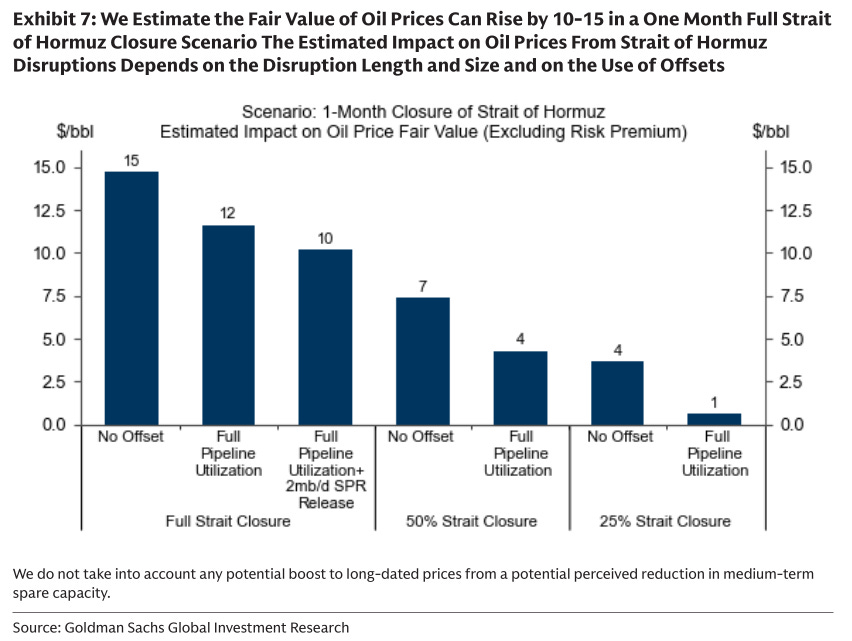

In theory, some oil can bypass the strait through pipelines. In practice, the capacity is limited. The International Energy Agency estimates that only about 4.2 million barrels per day can be rerouted through alternative routes.

And oil isn’t the only commodity that moves through Hormuz.

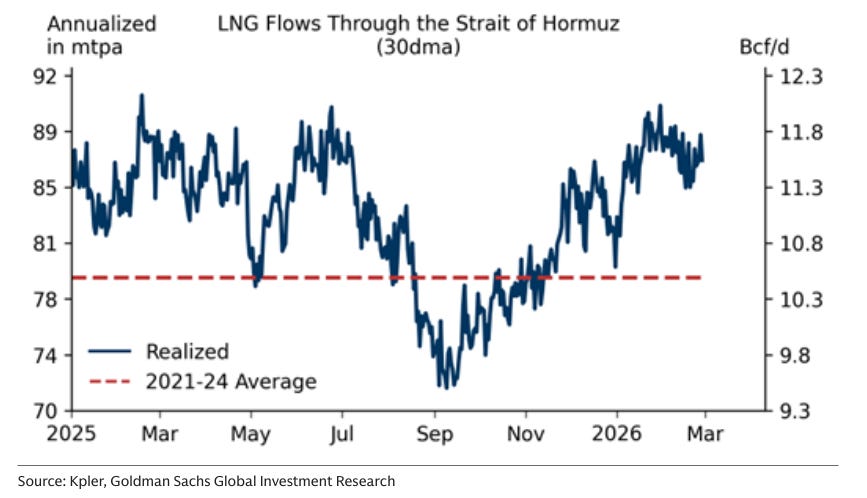

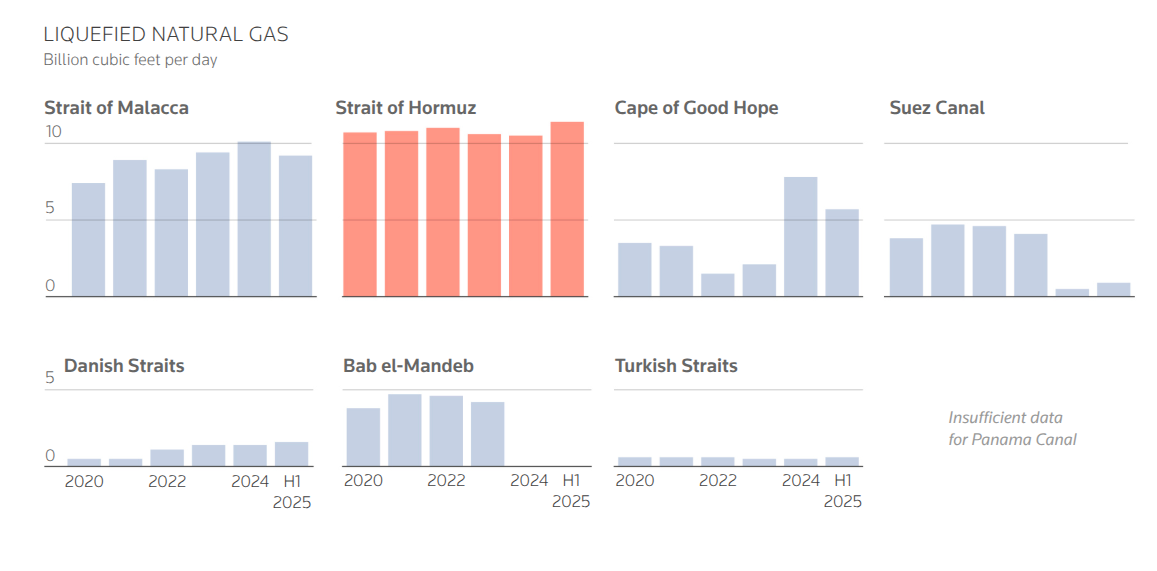

Goldman Sachs estimates that roughly 80 million tonnes of LNG pass through the strait every year—about 19% of global supply—with most of it coming from Qatar.

The first thing to understand about a disruption in the Strait of Hormuz is that it starts as a logistics problem. The oil may still be produced — it just can’t move.

Allianz Research noted that in the early days of the conflict, more than 200 oil and LNG vessels were anchored outside the strait. Insurers and shipowners were simply unwilling to take on the risk of sending ships through an active conflict zone.

But logistics shocks can quickly turn into supply shocks. If ships stay stuck for long enough, export terminals start filling up, storage tanks overflow, and producers eventually have to slow or cut production.

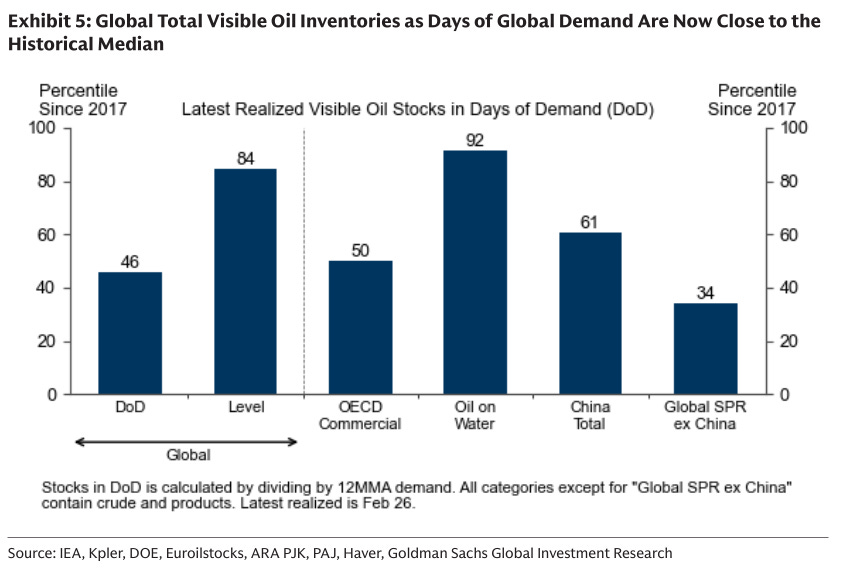

According to Goldman Sachs, global visible oil inventories currently stand at around 7.8 billion barrels—roughly in line with historical levels relative to demand.

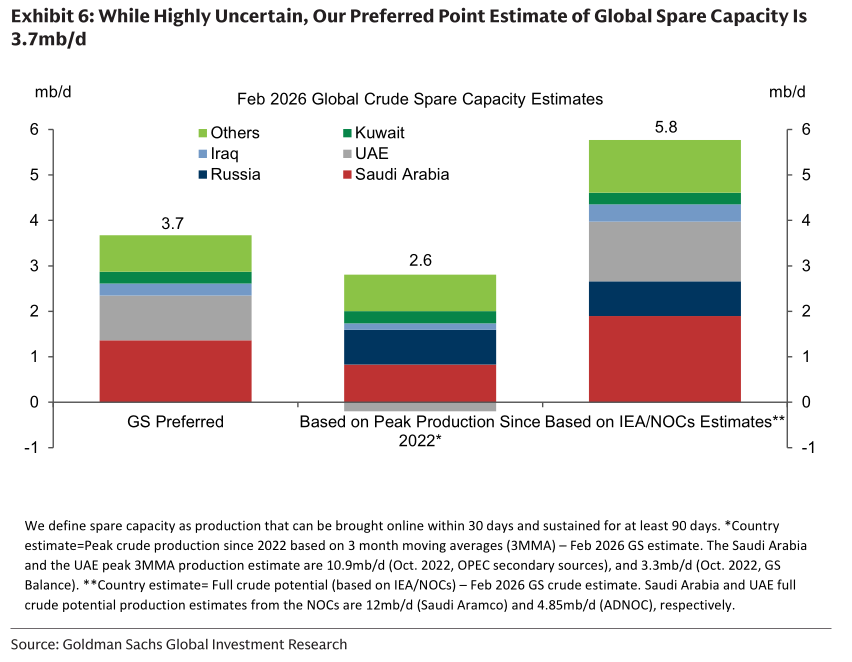

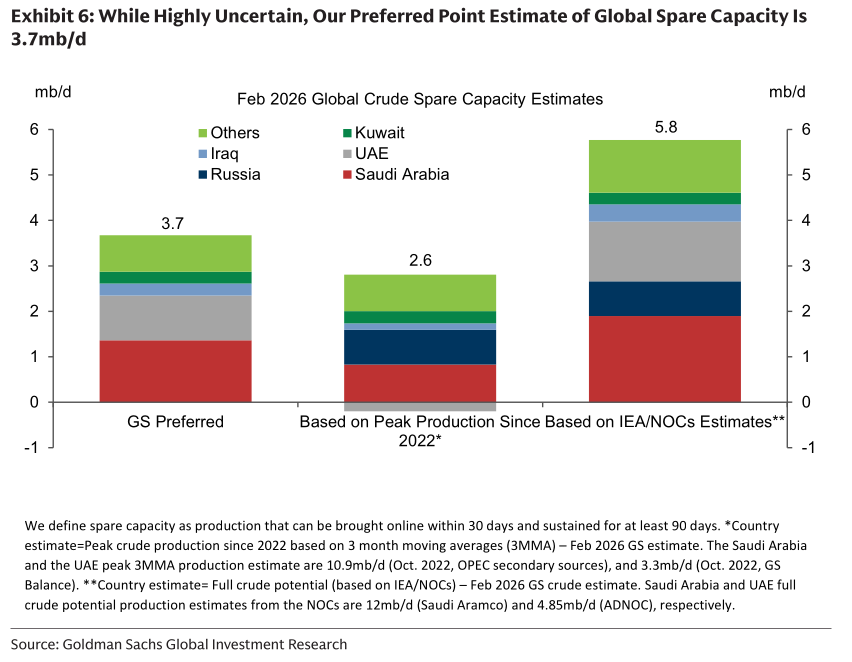

The bank also estimates about 3.7 million barrels per day of spare production capacity worldwide, most of it concentrated in Saudi Arabia and the UAE.

These buffers can help the market absorb a short disruption. They don’t last forever. If the Strait of Hormuz stays disrupted for long enough, those buffers begin to run out. And at that point, what started as a shipping problem turns into a real supply shortage.

One part of the Hormuz story that often gets overlooked is that the strait isn’t just an oil route.

The Gulf exports far more than crude. Petrochemicals, refined fuels, fertilizers, aluminium, plastics, and a range of other industrial products all move through the same corridor. So when tanker traffic slows, it’s not just oil shipments that get disrupted—many of these exports are affected as well.

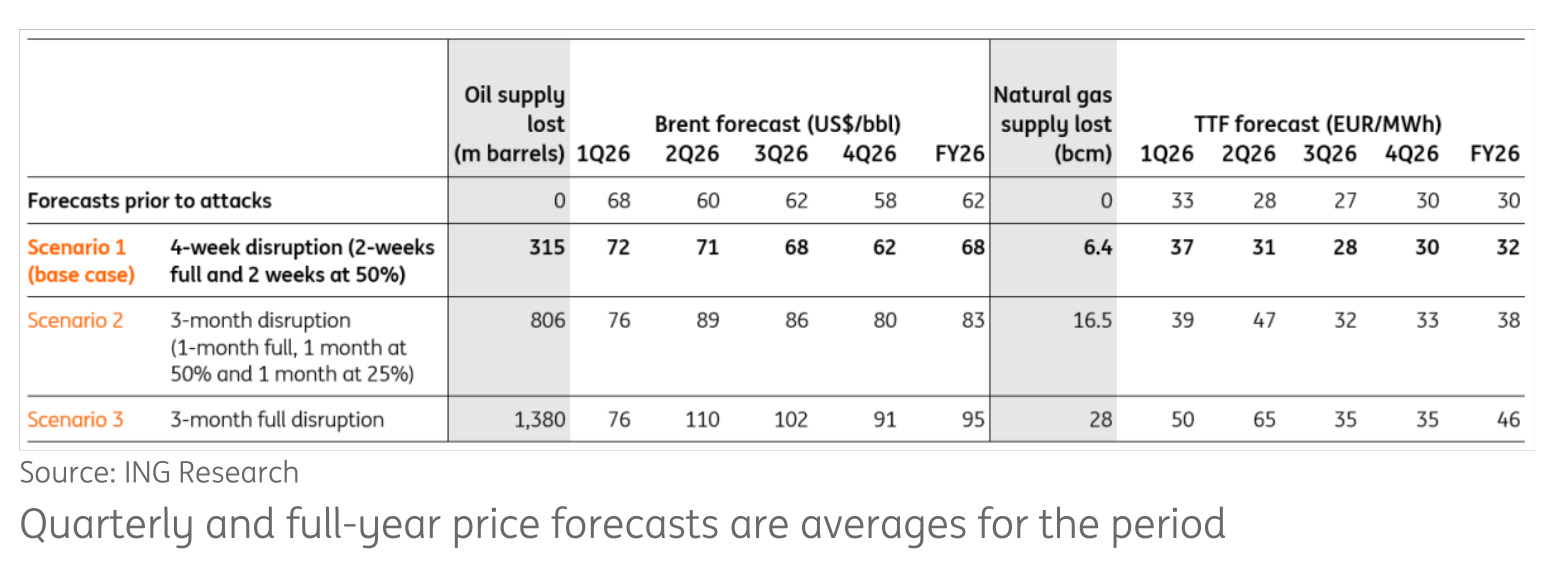

ING notes that if the disruption drags on, the impact won’t be limited to oil prices alone. It can create a broader trade shock—higher energy costs, longer shipping routes, rising insurance premiums, and slower global trade.

Some Gulf producers do have limited ways to bypass the strait. Saudi Arabia and the UAE, for instance, operate pipelines that allow some oil to reach ports outside Hormuz.

But the capacity is limited. ING estimates these routes can divert roughly 5 million barrels per day. Even after that, around 15 million barrels per day of oil supply would remain exposed to the strait.

That’s why these bypass routes reduce the severity of the shock but don’t remove it entirely. In fact, there’s another complication. Much of the world’s spare oil production capacity also sits in the Gulf, as we saw earlier. So even if producers decide to pump more oil, it still has to move through the same vulnerable corridor.

And while oil usually dominates the headlines, gas markets could feel the sharper impact. Goldman Sachs estimates that the roughly 80 million tonnes of LNG that normally pass through Hormuz account for nearly one-fifth of global LNG supply.

The effects of a Hormuz disruption don’t stop with energy prices. They also ripple through global shipping.

Goldman notes that crude freight rates were already about 50% higher this year, even before the latest escalation, while some tanker routes have reportedly tripled in cost as war-risk insurance surged.

Allianz adds that fuel accounts for roughly 35% of a ship’s operating costs. So if fuel prices rise by 40–50%, freight rates could climb another 15–20%.

And because shipping costs feed directly into the price of traded goods, those increases eventually show up as inflation.

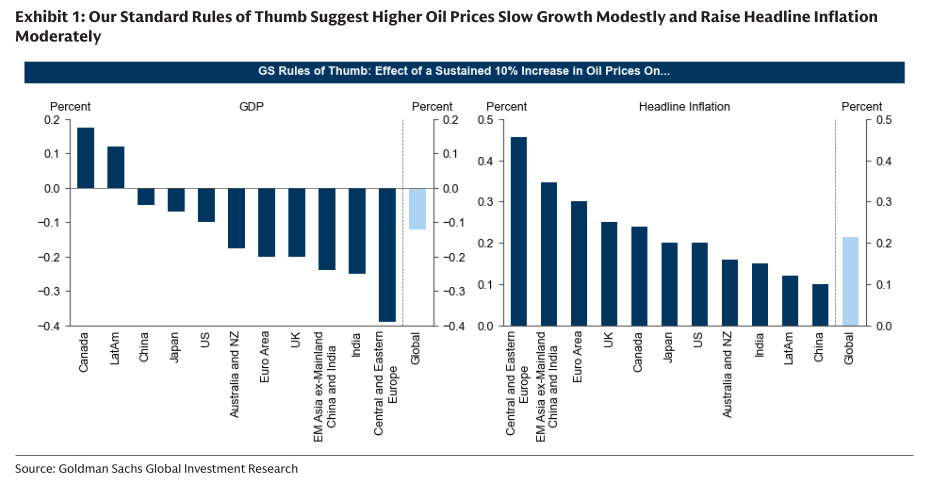

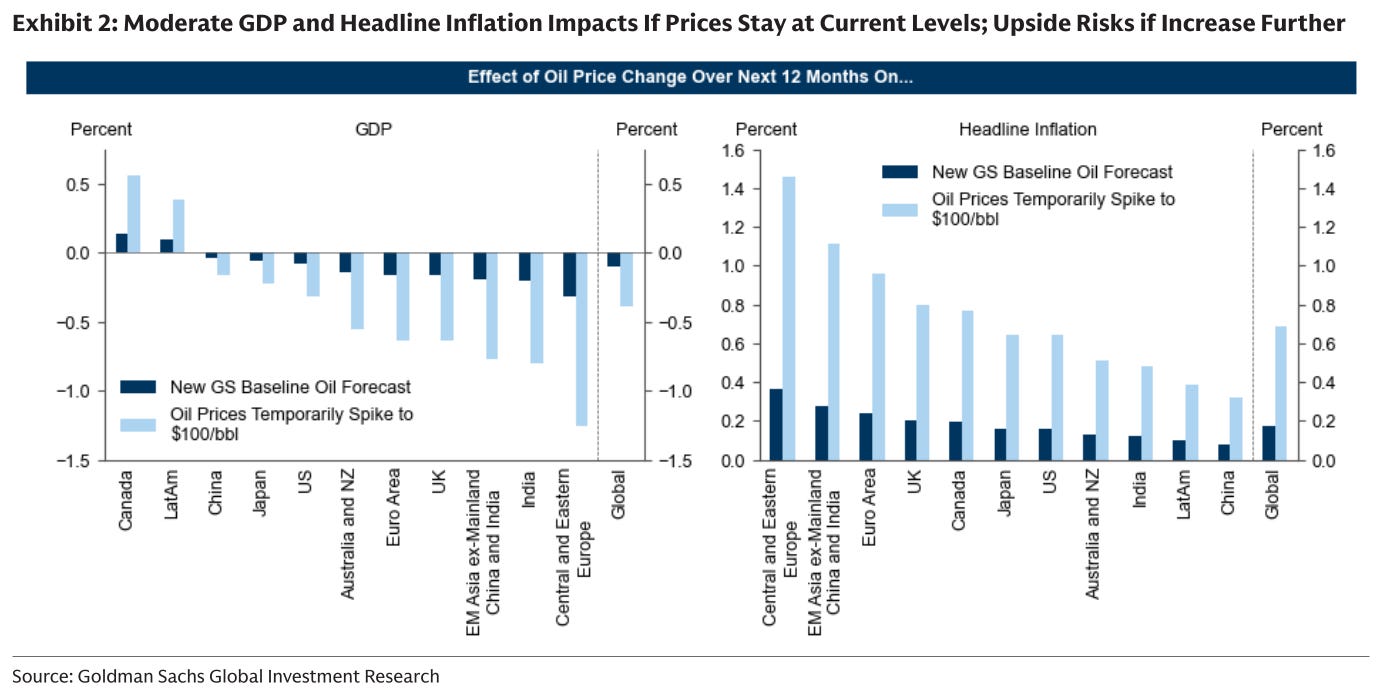

Goldman’s macro analysis gives a rough sense of the scale. In its baseline scenario, the shock adds about 0.2 percentage points to global inflation and reduces global growth by around 0.1 percentage points.

In a more severe scenario—where oil moves closer to $100 per barrel—inflation could rise by about 0.7 percentage points, while global growth slows by roughly 0.4 percentage points.

For India, the exposure is significant. The country imports around 85% of its crude oil, and roughly 40% of those imports pass through the Strait of Hormuz, as per ING.

That means higher oil prices can affect India through several channels at once: higher import bills, wider current account deficits, more inflation pressure, rupee volatility, and potentially tighter monetary policy.

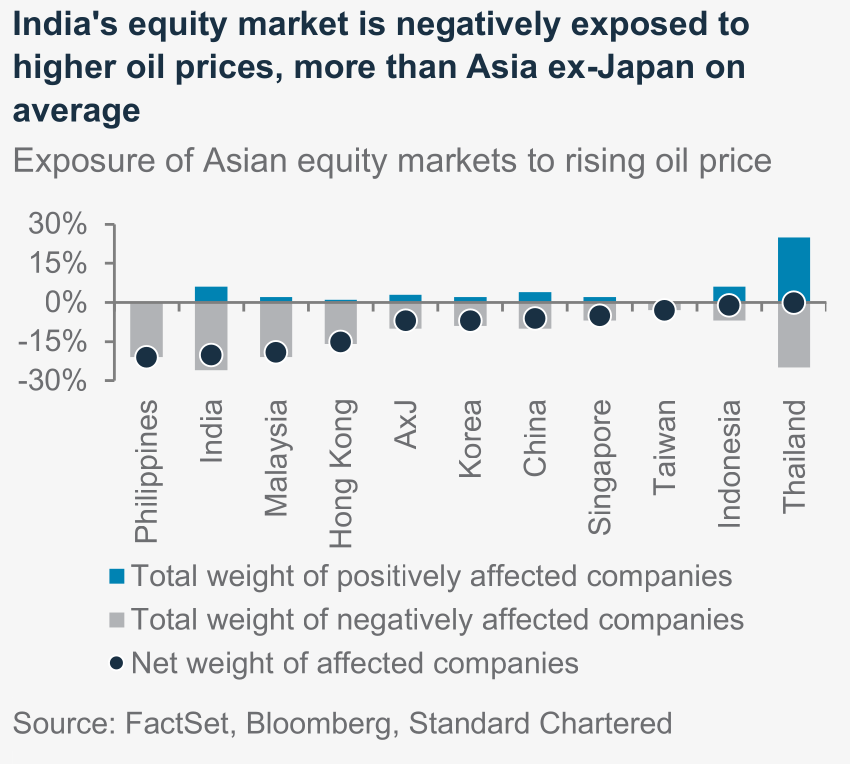

Standard Chartered adds another dimension to this. According to the bank, roughly 20% of the Indian equity market is negatively exposed to higher oil prices, which makes this not just a macroeconomic issue but a market one as well.

That’s it for this edition. Thank you for reading. Do let us know your feedback in the comments.

ZionDon is a puppet of Adelson. There has never truly been any independent US president since JFK. But Trump's servility knows no bounds.