TCS Quarterly Results: The Good, Bad, and Ugly

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

TCS Quarterly Results: A Mixed Bag

India’s Villages on the Rise: SBI Report Insights

Who Will Guide India’s Growing Investors?

TCS Quarterly Results: A Mixed Bag

Today, we’re diving into TCS’s quarterly numbers. As India’s largest IT company, its performance gives us a good sense of how the entire sector is doing. Let’s break it down.

First, the key numbers. TCS reported revenue of ₹63,973 crores for Q3, which is a 5.6% increase compared to last year. Their profit stood at ₹12,380 crores, up 12% year-over-year. Now, here’s something worth noting—they landed deals worth $10.2 billion this quarter. That’s an 18.6% jump from the previous quarter and a 25.9% increase from last year. What makes this even more impressive is that these numbers were achieved without any mega-deals, which shows a more balanced demand recovery. That’s typically a good sign for long-term growth.

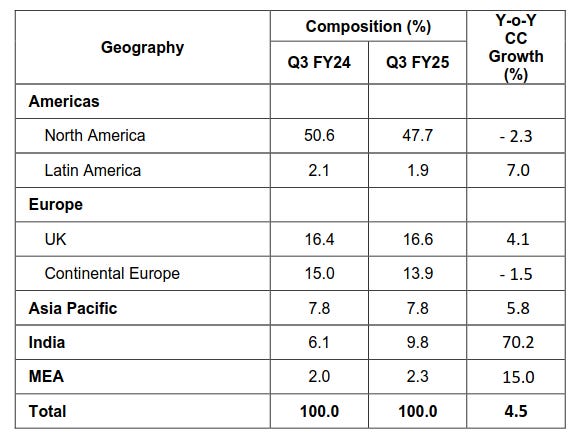

Now, let’s talk about geography. India’s growth of 70.2% looks incredible on paper, but there’s some context here. A big part of this comes from the BSNL deal, which is already about 70% complete and winding down. The Middle East grew by 15%, and Latin America by 7%, but there’s a red flag—North America, TCS’s largest market, shrank by 2.3%. Europe didn’t do much better, with Continental Europe down 1.5%.

When it comes to industries, the picture is mixed. Banking and Financial Services, which make up about 30.5% of TCS’s revenue, grew by just 0.9%. The consumer business saw a small rise of 1.1%, but communications had a steep decline of 10.6%. Manufacturing, which had been strong in earlier quarters, grew by only 0.4%, and Technology & Services dipped by 0.4%. So, while the overall numbers look decent, some sectors are clearly struggling.

Now, let’s look at the challenges because this is where it gets interesting. According to a recent report by Bank of Baroda, four major shifts are happening in the industry that we’ll need to watch closely.

First, there’s Trump 2.0. Yes, politics is starting to influence the tech world. The report points out that Trump’s potential policies around tariffs, immigration, and especially H1-B visas could create a lot of uncertainty. Right now, most Indian IT companies have 50–80% of their U.S. workforce as non-visa-dependent. But if there’s a major change in visa rules, it could significantly impact cost structures.

Second, we’re likely heading into what analysts are calling a “higher for longer” interest rate scenario. This is a big deal for the Banking and Financial Services sector, which makes up about 30% of TCS’s revenue. Higher interest rates often mean businesses cut back on tech spending, especially in capital-heavy sectors like telecom or areas that rely on borrowing.

Third, we’re still seeing the effects of what Accenture called the “compressed transformation” phase during the pandemic. Back then, projects that would normally take 5–10 years were squeezed into 18–24 months. That created a huge but temporary spike in demand, and now the market is adjusting back to normal levels.

Fourth, there’s the AI factor, and this is where it gets interesting. While everyone is excited about Generative AI, the Bank of Baroda report suggests it might actually reduce revenue growth for the tech sector over the next 2–3 years. Why? For every dollar spent on pure Generative AI, companies need to spend around $25 on related services. That’s making it hard to see quick returns on investment.

Lastly, there’s a deeper shift happening in how companies spend on tech. The days of pure cost-cutting through outsourcing are fading. Clients now want pricing based on business outcomes. Instead of massive transformation projects, they’re breaking them into smaller, more focused tasks with clear ROI goals.

When it comes to the AI factor, it’s not just about chatbots anymore. TCS mentioned something interesting—they’re seeing demand for what they call “Agentic AI,” which goes beyond basic automation. But let’s be honest, we should take all the “AI” buzz with a pinch of salt. It’s tough to separate what’s genuinely useful from what’s just hype.

Next, there’s a shift happening in talent. While attrition has risen slightly to 13.0% from last quarter’s 12.3%, the kind of skills companies need is changing fast. TCS reduced its headcount by 5,370 this quarter, bringing it to 607,354 employees. This is their first significant reduction in a while. But it’s not necessarily bad—it reflects the shift in delivery models, where revenue growth no longer depends directly on adding more people.

On top of that, the entire commercial model for IT services might be heading for a shake-up. During the earnings call, there were questions about whether AI could push the industry toward software-based pricing instead of the traditional time-and-materials model. TCS’s management said they haven’t seen this shift yet, but it’s clearly on everyone’s radar.

What stood out most, though, was the management’s optimism—the most upbeat we’ve seen in two years. They mentioned shorter deal cycles, which typically mean faster client decision-making. They’re also seeing early signs of recovery in discretionary spending, especially in BFSI and retail. They even called out calendar year 2025 as likely to be better than 2024.

Looking ahead, there are a few key things to keep an eye on. First, the BSNL deal, which is 70% complete, will start tapering off next quarter. TCS’s strategy to replace that revenue will be critical. Second, the pace of interest rate cuts in the US could have a big impact on tech spending. Third, the upcoming US elections add a layer of uncertainty. And perhaps the biggest question is how quickly companies can shift their traditional services to AI-augmented offerings without losing revenue from their existing business.

That’s the TCS update for this quarter. The big takeaway? While growth right now might look moderate, we could be at a turning point for the entire IT services industry. The real winners will be the ones who can adapt to these changes while staying profitable.

India’s Villages on the Rise: SBI Report Insights

What do you think has been the most impactful change in our economy in the last decade? Is it the rise of software start-ups? Electronics manufacturing? GCCs? The ongoing stock market boom?

Well, here’s something that people don’t speak about, that might be more important than all of them — looking just at the number of lives it has touched: at the very bottom of our socio-economic pyramid, where people live some of the worst lives India has to offer, there’s been a lot of rapid change. Millions of people are escaping poverty. And what’s more — rural India is leading this charge.

That’s the big takeaway from a recent report by SBI research.

See, in 2011-12, we decided on a poverty line: back then, anyone living on less than Rs. 816 a month in villages, or Rs. 1000 a month in urban areas was considered to live in ‘poverty’. Back then, this pointed to some troubling statistics. Using this line, in FY 2012, more than one-quarter of rural India was impoverished, as was nearly 14% of urban India.

Last year, India completed a mega-survey of how much people consume — called the Household Consumption Expenditure Survey, or the ‘HCES’. And here’s one interesting thing we found: if you adjust that 2012 line for inflation and look at it today, the number of impoverished Indians is a fraction as much. Today, both in urban and rural India, the poverty rate is well under 5%.

This is a striking change. From what the HCES data shows, the very poorest Indians — those in the bottom 5% of its economy — have greatly increased their consumption — and, by extension, their living standards. As a result, almost none of India lives the sort of life we would have considered ‘impoverished’ a decade ago.

Now, this calculation isn’t without its controversies. For instance, many experts think that our poverty line is far too low. If you push the line closer to what other lower-middle-income countries use, a lot more people will suddenly be classified as living in poverty once again. We’ve written about these issues on our blog before.

But, the fact remains: at least if we’re holding ourselves to the standards we set in 2012, we’ve made great progress as a country. Compared to how things looked a decade ago, the lives of hundreds of millions of people have improved quite dramatically — even if they’re still ‘poor’.

What’s even more fascinating is that rural areas, not urban ones, have seen the biggest transformation. A decade ago, the rural poverty rate was nearly double that of urban areas—25.7% compared to 13.7%. But now, that gap has narrowed significantly. Urban poverty is down to 4.09%, and rural poverty isn’t far behind, at just 4.86%.

A decade ago, the living standards of urban Indians were 88.2% higher than rural Indians. That gap has now shrunk to 69.7%. And there’s some evidence that things might continue down this path. At least over the last year, FMCG giants like Hindustan Unilever and Dabur have reported that their rural businesses are performing much better than their urban counterparts.

So, what explains this change? Well-executed government spending is definitely a big factor in this transformation.

Consider roads, for instance. Road access can completely revolutionize a village’s economy. Suddenly, you can access nearby markets for work, or go there to buy and sell things. Government services in nearby areas become far easier to access. All of this adds up to a major improvement in the “ease of living,” and changes the lives of people in that village.

There’s been a sea change in Indian roads over the last decade. India’s national highways have increased by 50% in length since 2014-15. A lot of these have been connected to nearby villages, with over 7 lakh kilometers of rural roads being built under the PM Gram Sadak Yojana. The effect is transformational. These developments have pulled a lot of India’s villages much closer to the heart of its economic fabric.

From free grain distribution, to direct benefit transfers, to schemes targeted at improving farmer incomes — there are perhaps many other such programs that have improved the lives of rural Indians.

As rural India’s living standards improve, its spending habits have changed too. A decade ago, more than half of rural India’s money was spent just on food. Since then, though, this has come down a little, and people are slowly buying a wider variety of things. They’re spending more on conveyance — perhaps because they’re better connected than before. And interestingly, they’re spending a little more on toiletries.

We know — this doesn’t sound like much. But think of what that really means. Over the last decade, a large part of India has graduated from a hand-to-mouth existence. They’ve taken slow, tentative steps towards becoming ‘consumers’ — spending on the odd tempo ride, or a few shampoo sachets. Hundreds of millions of people have just entered India’s economy, though they probably don’t have much money to spend individually. If you are watching this video, you probably don’t relate to them very much.

But if you’re looking to invest in the “India growth story”, the first businesses to reach this cohort of people will certainly be one part of it.

Who Will Guide India’s Growing Investors?

India’s investing scene is going through an incredible transformation. Just look at the numbers—back in March 2021, there were about 4 crore registered investors. Fast forward to today, and we’re at 11 crore.

What’s mind-blowing is how fast this growth has been. It took 25 years to reach the 4-crore mark. But from there, every additional crore of investors has come quicker. The next crore took about 3.5 years, the one after that just a little over a year, and the latest one? Barely five months.

It’s a huge milestone for India’s markets. But while we’re celebrating this surge in investors, there’s another side to the story that’s worrying: the number of registered investment advisors (RIAs) has been shrinking.

In 2021, there were 1,334 RIAs in the country. By August 2024, that number had dropped to just 927. To make things more depressing, not all of these 900 odd RIAs do advice. Many of then are F&O tipsters from Indore. If you only consider the number of RIAs who profile holistic financial planning, at best, there might be just about 200 RIAs in India. That’s it. 200 advisors for 11 crore investors.

Why is this happening? It boils down to how tough it’s been to get and maintain an RIA license. The rules have been so strict that many advisors have decided it’s just not worth the hassle.

And this isn’t a good sign. Think about it—our markets are growing, the number of investors is exploding, and yet the pool of advisors who can guide these investors is shrinking. No market can thrive like this. Advisors are critical for helping people navigate the complexities of investing, and we need more of them, not fewer.

The framework for RIAs was introduced in 2013 by SEBI. The idea was to regulate financial advisors so that investors could get professional, unbiased, and ethical advice.

Since then, the regulations have only become stricter, which was great for protecting investors but made life harder for advisors. Recognizing this imbalance, SEBI has recently rolled out a bunch of updates to make the profession more accessible while still keeping investor interests at the forefront.

Let’s look at what the major changes have been -

1. A move from net worth to deposits

Previously, if you wanted to become an RIA, you needed a minimum net worth of ₹50 lakh for firms and ₹5 lakh for individuals. Considering that India’s per capita income is just $2,700, these requirements were a major roadblock for many aspiring advisors.

Now, SEBI has replaced the net worth requirement with a deposit system:

Advisors with up to 100 clients need to deposit ₹1 lakh.

The deposit increases with the number of clients but is capped at ₹10 lakh for firms with over 1,000 clients.

This is a big relief. It lowers the entry barrier, allowing more professionals to join the advisory space while still offering some protection to investors.

2. Easier educational qualifications

Earlier, becoming an RIA meant having a post-graduate degree or a professional qualification, along with relevant work experience.

That’s no longer the case. Now, a graduate degree is enough, and there’s no mandatory work experience required. Advisors still need to pass NISM certification exams, but here’s the kicker—they only need to take a refresher exam every three years to stay updated, instead of redoing the entire certification process.

This change makes the profession more accessible without compromising on the quality of advice.

3. Higher fee limits and more flexibility

SEBI has also revamped the fee structure:

The maximum fee under the fixed fee model has been increased from ₹1.25 lakh to ₹1.51 lakh per family per year.

Advisors can now switch between the fixed fee model and the Assets Under Advice (AUA) model at any time, with no restrictions on how often they can change.

These updates make things more flexible for advisors while also aligning fee limits with inflation.

4. Corporatisation threshold raised

Under the old rules, advisors had to corporatise if they had more than 150 clients. This increased the level of compliance.

Now, that threshold has been raised to 300 clients or ₹3 crore in annual fees, whichever comes first. This gives smaller advisors more breathing room before they’re required to set up as a corporate entity.

These changes are a big step in the right direction. By lowering barriers like net worth and educational requirements, SEBI is encouraging more professionals to join the industry. And by updating fee structures and corporatisation thresholds, they’re making the profession more sustainable for existing advisors.

For investors, this is a win too. More advisors mean more choices, better competition, and, ultimately, better guidance.

Tidbits

NHPC Ltd., India’s largest hydropower generator, plans to acquire the combined 16.2% stake held by its public sector co-promoters—NTPC Ltd., Power Grid Corp. of India, and Power Finance Corp.—in PTC India Ltd., a leading power trading firm. Each promoter holds approximately 4.05% in PTC India, which has paid over ₹320 crores in dividends since its inception.

Emami Ltd. has rebranded its two-decade-old male grooming brand from Fair and Handsome to Smart and Handsome to capture a larger slice of the expanding ₹32,000 crore male grooming market. Currently, the company operates in a limited ₹700 crore segment dominated by creams and face washes. The rebranding allows Emami to launch diverse products aligned with shifting consumer trends, as young men increasingly use an average of five grooming products daily

India’s food delivery leader, Swiggy, announced that its quick-commerce service, Instamart, will soon operate as a standalone app while remaining accessible on the main Swiggy platform. Currently serving 76 cities, Instamart offers 10-minute delivery for over 50,000 products and is projected to reach over 100 million users, as stated by Swiggy’s MD & Group CEO Sriharsha Majety.

-This edition of the newsletter was written by Anurag, Pranav and Bhavya

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉 Join the discussion on today’s edition here.