SpaceX: A valuation built on miracles

Can ambition win over hubris?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

How high can SpaceX fly?

How did Indian carmakers perform this quarter?

How high can SpaceX fly?

It’s hard to know what one should make of SpaceX’s IPO filings. It is, above all, a picture of extremes.

Here’s a sample: this January, the SpaceX board granted founder Elon Musk a billion shares of Class B stock, which would vest in fifteen tranches as the company’s market capitalisation would rise. That isn’t unusual in itself; Musk would get similar performance grants at Tesla as well. What’s new, however, was a condition: for any of those tranches to vest, he would have to ensure a permanent human colony on Mars with at least a million inhabitants

A different grant from this March could give him another three hundred million shares. Those would partly vest, however, once he managed to fly a data centre with a hundred terawatts of compute a year to space. That’s roughly a hundred thousand times what SpaceX has installed today.

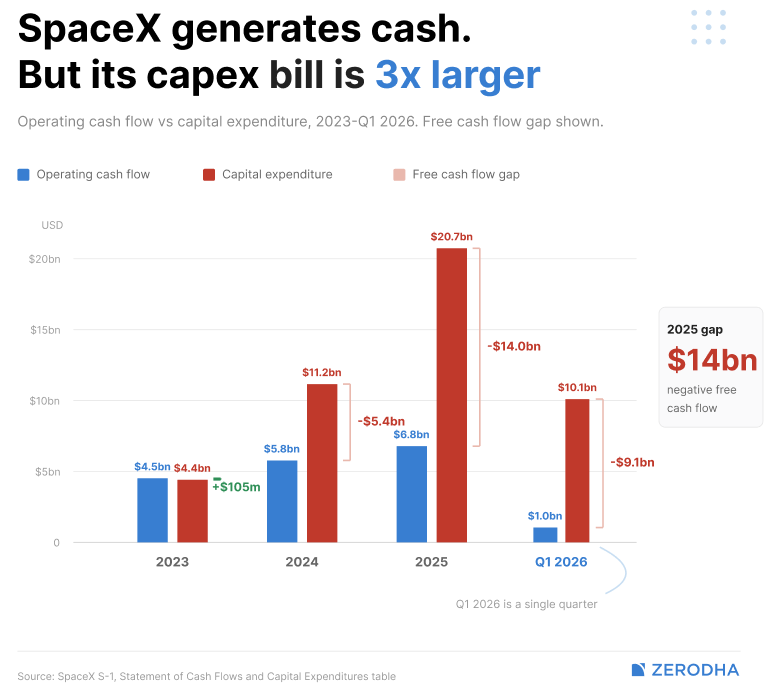

Last year, the same company burned through fourteen billion dollars of cash last year. Its debt alone comes to thirty billion dollars. Its capex bill, last year, was thrice as large as its actual earnings

This isn’t a normal company. It is one built on both ambition and hubris, both of stratospheric proportions. And now, they’re aiming at the world’s largest ever IPO as well. Their recent IPO document gives a rare glimpse into the business beneath the madness. We aren’t sure if we comprehend SpaceX any better because of it, or if our confusion just runs deeper now.

Either way, here’s what we saw.

What’s inside

SpaceX, despite its name, isn’t merely a space business. It’s a hazy amalgamation of many futuristic enterprises.

Its original heart was launch: the business of sending things up to space. SpaceX is the world’s biggest space-faring entity: more prolific than all the world’s sovereign space programs taken together. In 2025, four out of every five kilograms humans sent to space went there on a SpaceX rocket.

The workhorse of its launch program is one of the greatest engineering marvels of the modern world: the Falcon 9. The rocket has flown over six hundred and twenty orbital missions, with a mission success rate of over 99% — the highest of any launch vehicle in the world. The rocket, and its reusable boosters, fundamentally changed space travel. Before it, sending a single kilogram of payload into orbit cost $18,500. Once the Falcon 9 was pressed into regular service, that fell to just $2,700. There’s simply nothing else like it.

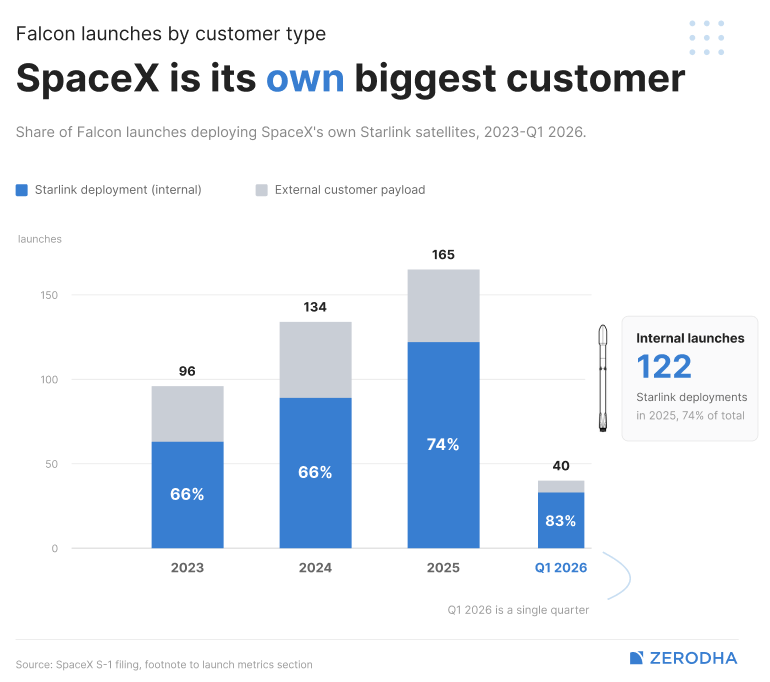

SpaceX counts everyone from young start-ups like India’s own Galaxeye to NASA among its customers. But as the company matures, its biggest customer is turning out to be… SpaceX itself.

In 2023, about two-thirds of all Falcon launches catered to SpaceX. By 2025, SpaceX’s payloads occupied almost three-fourths of the Falcon’s launches. Why does SpaceX’s internal demand ring this strong? Why does the world’s most powerful launch platform increasingly cater to itself?

Well, increasingly, the heart of SpaceX isn’t space launches: it’s the internet.

Starlink

Over the last few years, SpaceX has created a constellation of thousands of tiny satellites that beam the internet across remote parts of the world, in a service called ‘Starlink’. By the March quarter this year, the service had 10.5 million subscribers, across 164 countries around the world. It was used by both sides in the Russia-Ukraine war; and when Russians were cut off from the service, it changed the tide of that war. It’s currently being smuggled into Iran to get around the country’s internet blackout.

A service like this is only possible because of Starlink’s 9.5 thousand satellites, or about three-quarters of every active satellite in space.

This is increasingly the main cash cow of SpaceX. Starlink revenues netted the company $11.5 billion dollars in 2025, or nearly three-fifths of the company’s overall income. This is the only part of the SpaceX business that generates any meaningful profit, with last year’s EBITDA coming to $7.2 billion.

How many customers will pay for satellite internet, however? The company is currently fanning out across the developing world, looking for customers everywhere from Kenya to Indonesia to add to their service. This has, however, materially decreased their per-customer earnings. Their average revenue per user (or ARPU) used to be $91 a month, back in 2024. By the March quarter this year, it had fallen to $66. The company assumes that it’ll keep falling, until it settles at $31. Can the company’s economies of scale handle such a fall?

The company needs something to sustain its cash flows. Because a new addition to the SpaceX family is burning up all the money it can make.

Artificial intelligence

This February, SpaceX absorbed xAI into its business — a short while after xAI had, in turn, absorbed X (formerly Twitter). Both businesses now sit on the space-faring entity’s books.

The merger was an odd moment for the company. On one hand, it had acquired another major futuristic business. At the same time, though, the company inherited a tangle of related-party arrangements, and a lot of the madness Elon Musk was associated with: from political controversies, to allegations of creating non-consensual sexual imagery.

The new business came with $3.2bn of revenue from 2025. Twitter advertisements alone brought in $1.8 billion in 2025. Then, there were subscriptions, data licensing, and developer access to Grok’s models — which collectively brought in $1.4 billion last year, and are growing twice as fast.

For every dollar it was bringing in, though, it was losing two. The company ran at an operating loss of $6.4bn. On top of that, it spent $12.7 billion in capital expenses — roughly four times revenue — in building out data centres and acquiring GPU clusters at industrial scale. Its margins have been falling, while depreciation alone has overtaken the segment’s earnings.

The company, however, thinks of itself as essentially building for a distant future.

There are signs that this calculation isn’t entirely far-fetched. Just a few months ago, xAI was in a ugly, public feud with Anthropic. It was only this January when Anthropic had banned xAI engineers from using Claude, supposedly because they were using it to build their own models. In February, Elon Musk called Anthropic “misanthropic and evil”.

Just three months hence, though, the companies are now partnering. Anthropic recently announced it would lease the entirety of xAI’s first Memphis data centre, called “Colossus”. It agreed to pay xAI a staggering $1.25bn a month through May 2029 — roughly $40bn over the life of the contract. In other words, a direct AI competitor, with whom xAI had a publicly strained relationship, just decided to rely on it as an infrastructure provider. And for that, it agreed to pay it an amount higher than most public companies’ revenues every single month.

The AI business is currently in an economic wild west; one where all bets are off. xAI might not lead this race, but it’s very much in the arena.

How the money actually moves

Together, this gives us three very different businesses, all of which move at very different speeds.

Collectively, their revenues have been growing rather quickly: from about $10bn in 2023 to nearly $19bn in 2025 — most of which was driven by Starlink. In 2025, they threw off nearly $7 billion in cash. For all the hype, there’s a genuine business here.

But it’s a business that’s investing ungodly sums of money in the future. In 2025, its total capital expenditure was thrice the cash it actually made, at $20.5 billion. Nearly $13 billion of that went into AI data centres alone. And then, in just this March quarter, it spent another $10 billion, a lot of which was again in AI.

That effectively gives the company deeply negative cash flows. The business burnt $14 billion in cash last year, and has already burnt another $9 billion this year.

Where did that money come from? It was raised externally. Last year, SpaceX raised about $26 billion of financing in 2025, most of it debt for AI infrastructure. Another $7 billion came in this March quarter. This is adding up to a serious amount of debt on the company’s books, more than $20 billion of which matures next year alone. The company will also have to pay out an extra $20 billion next year in contractual commitments.

Under the terms of one of the major bridge loans SpaceX took out this year, the net proceeds of the company’s IPO would first go into paying that loan. Contractually, this is what the IPO must do before all else: reduce the company’s debt burden. Any new growth comes after that.

The dream

This is the company that could launch the largest IPO in the world: an audacious but cash-hungry mix of businesses straight out of Star Wars. The IPO could bring in over $70 billion, valuing the company at over $2 trillion. That’s roughly the amount of economic activity the entirety of Australia sees in a year.

What could ever make a business worth this much?

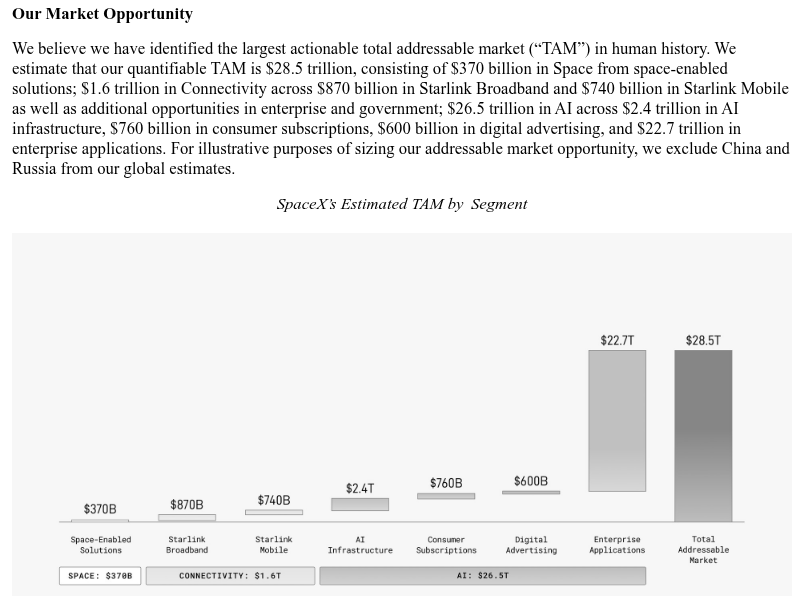

The promise of SpaceX, by and large, lies in the future. The company’s filings claim that it has identified the “largest actionable total addressable market in human history”. In all, the company frames itself as chasing a $28.5 trillion opportunity. Most of that — $26.5 trillion — comes from AI alone. In comparison, space exploration — which gives the company its name — is a relatively small $370 billion market.

Is there a world where the company could get to even a fraction of that?

It spins together a captivating dream. In the vision it sells, its newest rocket, Starship — which is almost twice as tall as Falcon 9, and can carry five times as much — will run at the same frequency as Falcon 9 currently does. This will enable a whole new paradigm: one where it shall run entire data centres in space, manufacture new satellites on the moon, and establish a permanent presence on Mars.

If that vision sounds fanciful, it is.

It depends on a lot of things going exactly right. Starship, which is yet to deliver its first payload to orbit, will have to replicate the Falcon 9’s incredible economics. It’ll have to get around regulatory tussles, while dodging political controversy and sovereign preferences. Meanwhile, its other businesses will have to fall into shape. Starlink will have to expand faster than its ARPU drops, while its AI arm will need to see more cash flow in.

And its erratic, mercurial founder — who is also building cars at Tesla, brain-chips at Neuralink, and tunnels at Boring Company — will have to keep his head in the game through all of it.

This is a tall order. It isn’t a dream most people would agree to underwrite.

Then again, this is a company that makes its CEO compensation contingent on a million humans migrating to another planet. It has both, the ambition to pull off a species-defining achievement, and the hubris to fall flat on its face.

Which side shall prevail? We certainly don’t have a clue.

How did Indian carmakers perform this quarter?

A decade ago, buying a car was a much simpler decision.

You picked petrol or diesel, chose a hatchback or a sedan, and negotiated the best price with your dealer. Today, you are choosing between petrol, CNG, hybrid, and electric.

Your neighbour might talk highly about CNG for the lower running cost. Your colleague just bought an EV and will not stop talking about it. Few might think anything without a diesel engine is a waste of money. And somewhere in all of this, you are trying to figure out what actually makes sense for your life, your commute, and your budget.

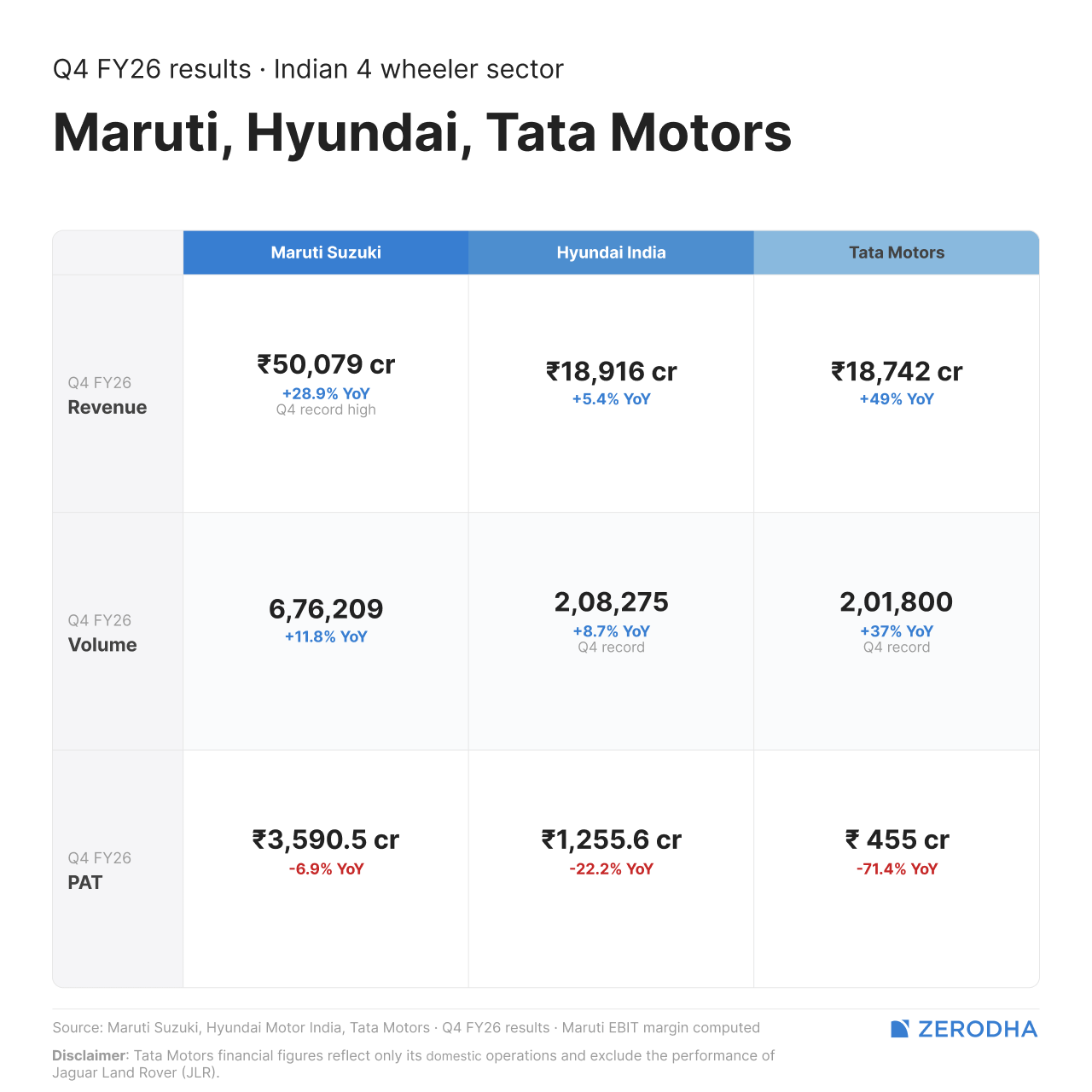

That fragmented demand is visible in the Q4 FY26 results of India’s three largest passenger vehicle companies — Maruti Suzuki, Hyundai India, and Tata Motors. Everyone sold more cars. But who is buying them, what they are buying, and what it costs to make those cars, that is where the real story is.

The scorecards

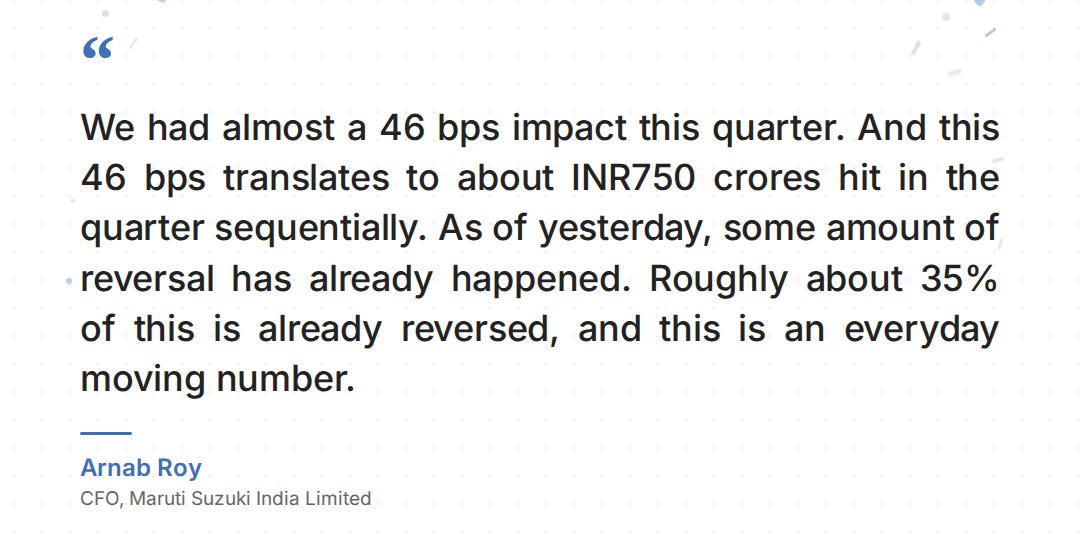

Maruti Suzuki posted net sales of ₹50,079 crore on 6.7 lakh units sold, up 11.8% in volume. EBIT came in at ₹4,409 crore, up 30.4% year-on-year, its strongest operating quarter ever. But net profit fell 6.9% to ₹3,591 crore, but that wasn’t because of the car business. Maruti incurred a paper loss of ~₹750 crore on its non-operational financial investments.

Hyundai Motor India reported revenue of ₹18,916 crore on 2.08 lakh units, up 8.7% in volume. But EBITDA margin dropped from 14.1% a year ago to 10.4%. We will come back to why that happened.

Tata’s India passenger vehicle business crossed 2 lakh units in a single quarter for the first time. Its Q4 revenue was up 49% y-o-y to ₹18,742 crore, while EBITDA margins were at 9.4%. But its volume surge also came off a weak first half of FY26 (or H1 FY26), when the GST cut had not yet landed and Tata was still rebuilding momentum.

At the Tata Motors Passenger Vehicles consolidated level, net profit fell 32%, mainly because of the cyber-attack on Jaguar Land Rover and US tariffs.

Where did the money go?

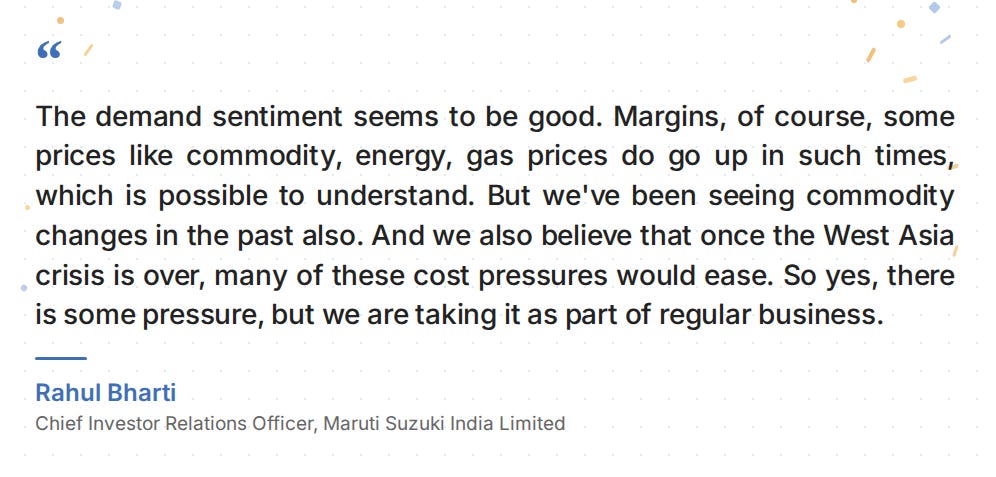

In our last results story, we covered the GST cut, which propped up demand meaningfully enough to offset rising costs elsewhere. But this quarter, the cost side only worsened, and the West Asia conflict added another layer of pressure.

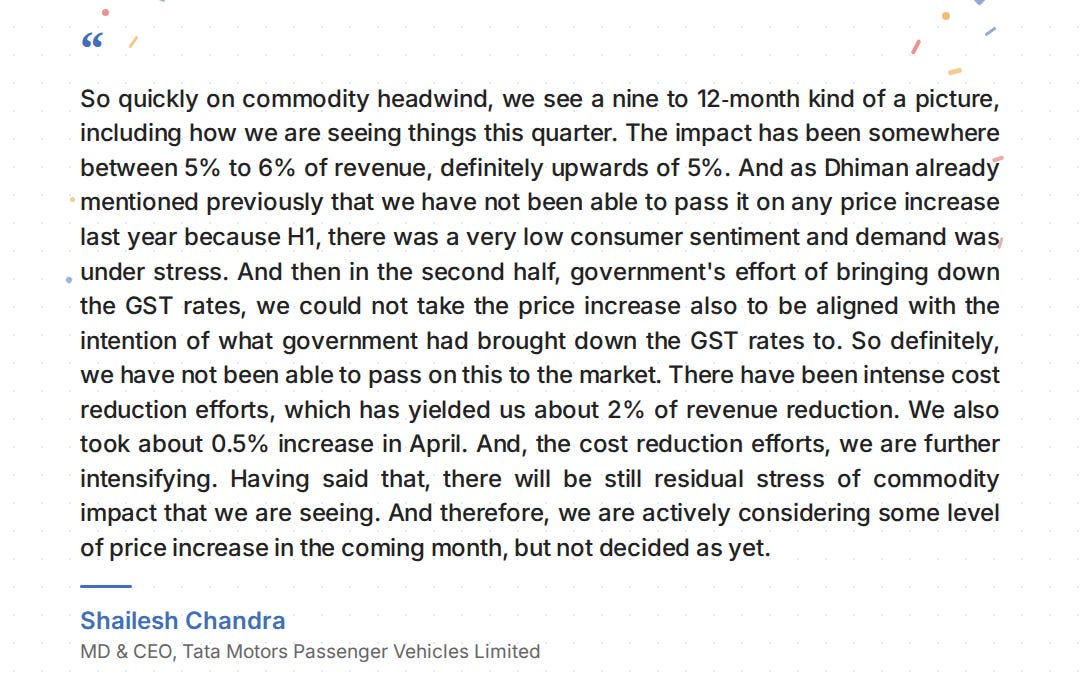

For Tata, the cost of raw materials (steel and aluminium) had gone up by more than 5% of revenue over the past year. Put differently, for every ₹100 worth of cars Tata sold, more than ₹5 extra went to raw materials than the year before. About 2-2.5% had already hit in FY26, and a steep additional 3.5 to 4% increase was coming through this quarter.

What’s more, Tata didn’t pass any of the rising costs to consumers through all of FY26.

The logic behind it was this: demand was fragile in H1, and in the second half the company did not want to undercut the consumer benefit of the GST cut. So it absorbed the entire hit internally through cost reduction of ~2% of revenue.

But that still left a gap. Going forward, they might end up passing some costs. But if that happens, it will have to be done carefully without disturbing customer value. This is as delicate as a balancing act can get.

Meanwhile, Hyundai’s response to rising costs was somewhat opposed to Tata.

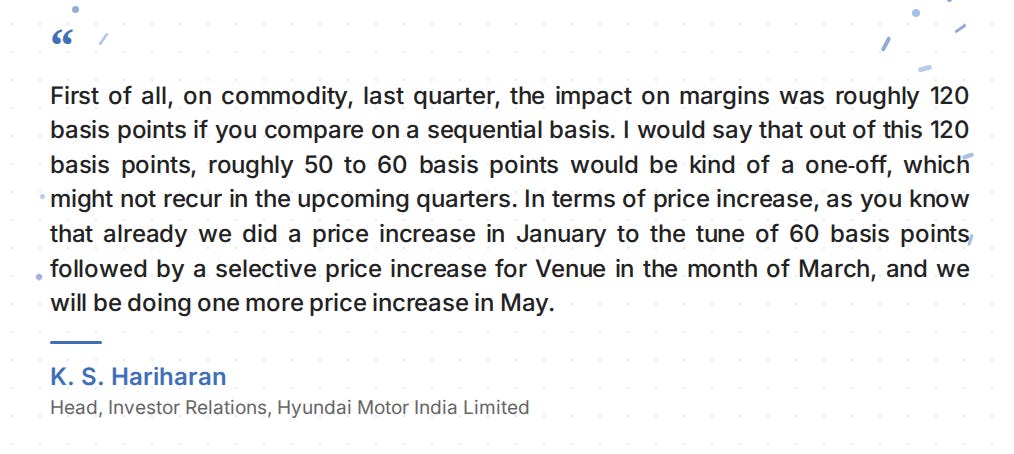

Commodity inflation ate about 1.2 percentage points off margins in a single quarter. Hyundai actually passed on costs multiple times through the year, with one more flagged for May. It also tightened the discounts that dealers could offer buyers. When demand is weak, carmakers allow larger discounts to sell more. But after the GST cut, Hyundai pulled those back.

Despite all of that, Hyundai’s EBITDA margins fell by 4 percentage points year-on-year. But that’s also because, on top of rising input costs, their new Pune plant was adding fixed costs before being fully operational. Additionally and a one-off labour code provision pushed up employee costs by nearly ₹100 crore in the quarter.

Maruti looked the least squeezed operationally. It actually made more money per car than it did the previous quarter — partly because it gave smaller discounts, and partly because of favorable currency movements on exports. They had deliberately not raised prices, though, because they didn’t want their sales momentum to slow down. A successful balancing act in terms of pricing.

Interestingly, Maruti’s belief is that the West Asia crisis is temporary, and once it is over, many of these cost pressures will lapse. They are taking it “as part of regular business“ — a riskier approach compared to other companies.

Who is buying these cars?

So costs went up, and pricing alone could not fully cover the gap. But margins did not entirely collapse either, and that’s because carmakers sold more premium, higher-margin models.

For Maruti, the share of first-time buyers jumped from about 42% in the first half of 2025 to 51% in Q4. Many were two-wheeler owners upgrading to their first car after the GST cut made entry-level models more affordable.

But these new buyers did not behave the way first-time buyers used to. A decade ago, the first would probably be an Alto. In 2026, the best-selling car is the Dzire, a sedan. The Victoris, a mid-SUV, reached 50,000 sales faster than any Maruti model before. Most importantly, a ~₹9 lakh Dzire earns the company more per unit than a ~₹4 lakh Alto would.

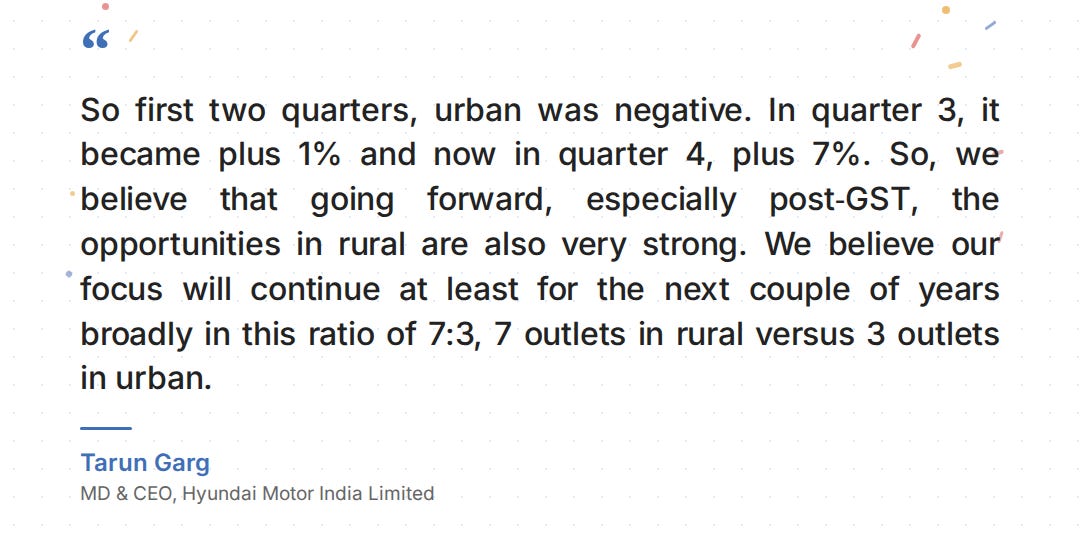

Hyundai’s growth came from rural India and CNG car models, and there are reasons for both.

Firstly, rural incomes have held up through good monsoons and government transfers, and Hyundai is deliberately putting 7 out of every 10 new outlets in rural areas. Rural penetration notched up from 22.6% in Q1 to 24.7% in Q4.

But the CNG push is not just about offering another fuel option. In many tier-2 and tier-3 towns, CNG refuelling infrastructure has expanded, making it more practical for buyers. CNG’s share in Hyundai’s sales went from 13% to 18% year-on-year. And this isn’t just in rural areas; urban demand also turned positive at 7% growth this quarter, after being negative in H1 2026.

In Tata’s case, its compact SUVs Nexon and Punch were the top sellers. CNG and EVs together now account for over 40% of Tata’s portfolio.

Across the board, the picture of the premium mix driving growth is largely similar. But the sceptical question is whether this mix shift is durable. If the GST-led first-time buyer wave fades, the mix could shift back towards lower-margin models. Even if the premium mix stays, how long does it cushion against elevated commodity costs?

That is where the supply side becomes important. Last quarter, we talked about order books swelling, but factory capacity falling painfully short of fulfilling them. That constraint now has a concrete response.

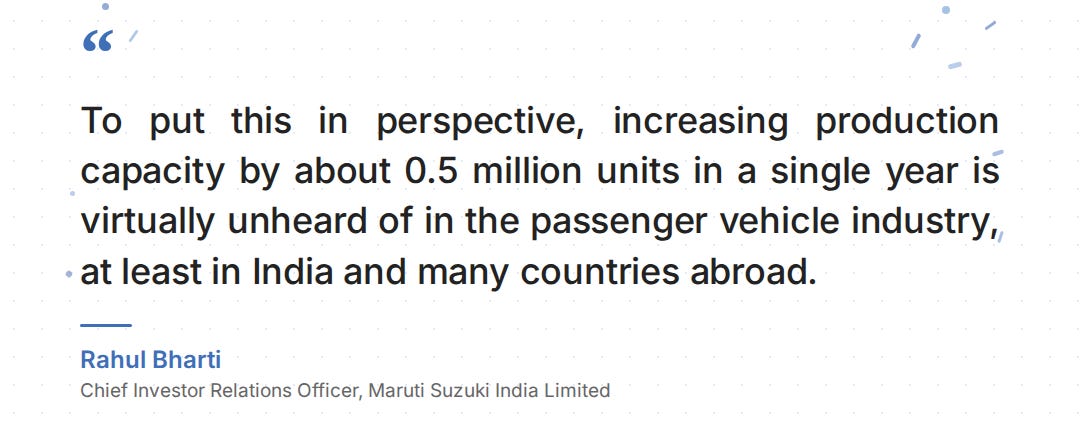

Maruti, for instance, is commissioning two plants simultaneously, adding 500,000 units of capacity in a single year, which management called “virtually unheard of“. Meanwhile, Hyundai’s Pune plant is running at 1.3-1.4 lakh units in two shifts, with expansions taking it to 3.2 lakh units by 2030.

Tata’s problem is different, though. It is not short on factory space. But the Tata Sierra, which has seen strong bookings, is stuck because its casting suppliers for the new engine cannot ramp fast enough. Tata is bringing in additional suppliers to plug the gap.

Every company is placing a different bet

Beyond the quarterly numbers, there is a longer-term question that all three dealt with. What kind of cars should companies be building for the next 5-10 years?

Of course, in business, this question is inescapable. But one reason it has become harder to ignore now is the recently-finalized CAFE 3 norms, which cap the carbon dioxide emissions a carmaker’s entire fleet can emit on average. If you sell mostly petrol cars, the average of your fleet gets too high compared to what the norms allow. You need more CNG, hybrid, or electric cars to bring it down.

The CAFE 3 norms are stricter than their predecessor rule set. If companies do not bring their averages down in time, they face three choices. They either face penalties, or they have to restrict how many petrol cars they sell, or they cross-subsidise green vehicles by charging more for petrol models.

In that context, each company is playing a different long-term game.

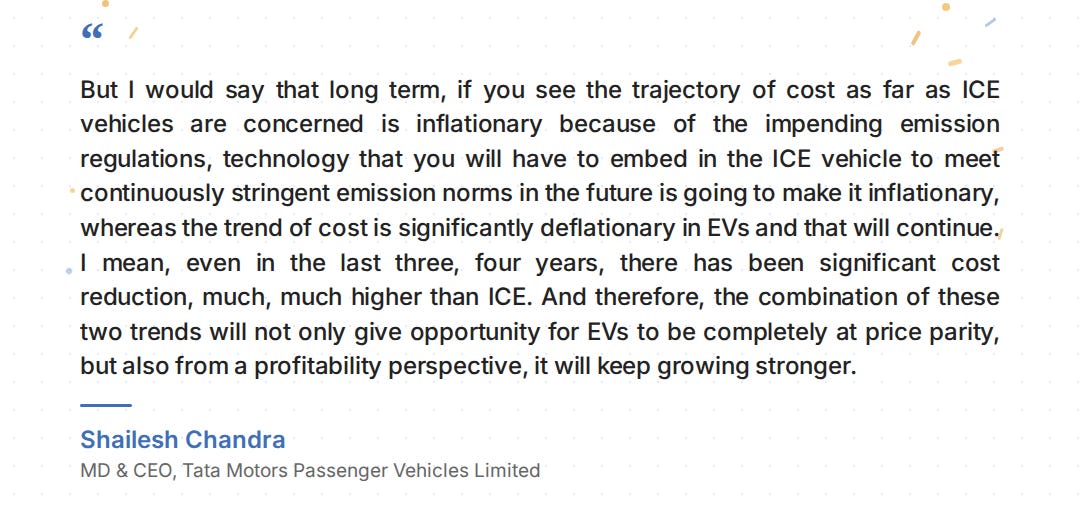

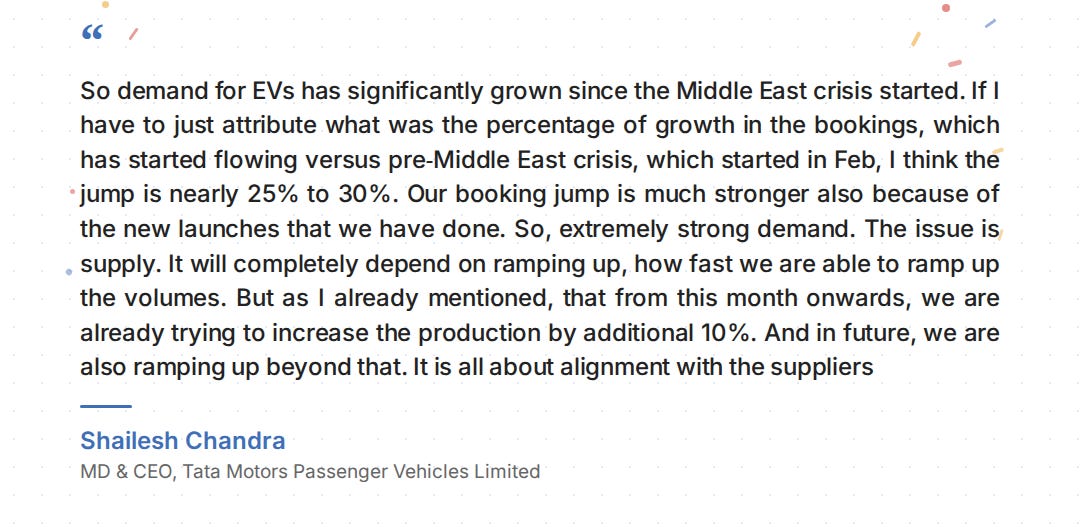

Tata, of course, is the largest four-wheeler EV player in India, with over 40% market share and 92,000 units sold in FY26. They expect the cost of making petrol and diesel cars to only go up because of tighter norms, while EV costs will keep falling as batteries get cheaper and production scales.

In fact, CEO Shailesh Chandra went as far as saying EVs will not just reach price parity with petrol-based cars, but also become more profitable eventually.

Tata’s EV bookings actually jumped 25-30% after the West Asia conflict began, as fuel uncertainty pushed more buyers to consider charging at home. What remains to be seen is how much of a structural force this is. There’s the possibility that if petrol stabilises, some of that demand could fade.

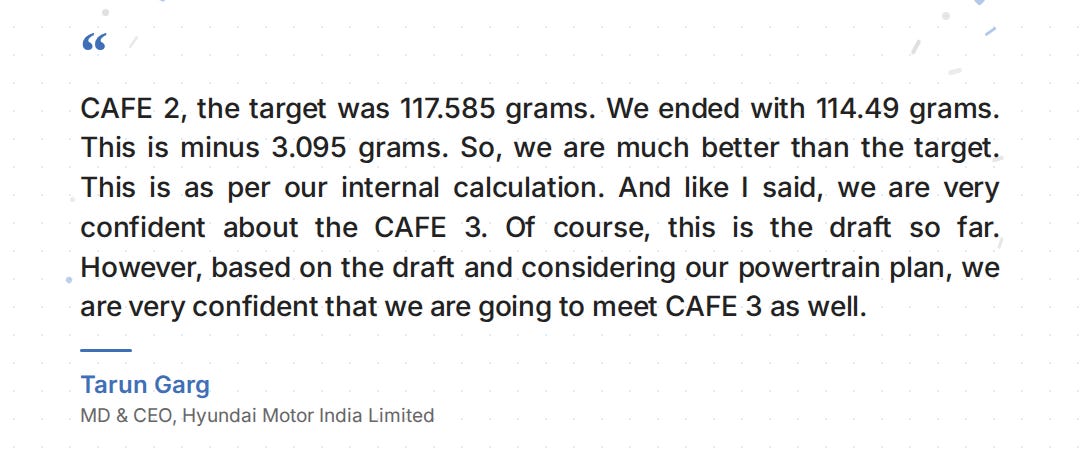

Hyundai is also confident about meeting the CAFE 3 threshold as well. But it isn’t going all-in on EVs the way Tata is. This year, Hyundai is launching its first localised electric compact SUV space alongside a new petrol-based mid-SUV. But it also leans heavily on CNG, which already accounts for 18% of its sales and helps bring the fleet average down anyway. For Hyundai, EVs are just one among many green options.

Maruti’s first fully electric car, the e-VITARA, has begun production in Gujarat. It is also building a charging network targeting over 1 lakh points by 2030 to support the model. But Maruti also noted that the final CAFE 3 draft is not yet notified, and that it encourages all green technologies, not just EVs.

That is why, much like Hyundai, EVs are only one part of Maruti’s roster which also includes biofuels, flex-fuel readiness, CNG, and strong hybrids. It is making sure it has an answer no matter which way the market goes.

And there’s no answer to that yet because the nature of growth of each green technology is quite different.

For instance, we know that rural India and CNG are among the fastest growth drivers right now. But at the same time, public charging infrastructure in tier-2 and tier-3 towns barely exists. The household buying a CNG car in a small town, and the household considering EV in a metro are two very different buyers. Building for both at the same time is particularly expensive.

What to watch in FY27

So, what do we watch in the coming year?

First, pricing power. Hyundai raised prices in May, Tata took its first increase in April, and Maruti has announced hikes from June. The GST benefit is still fresh in buyers’ minds. Q1 of FY27 itself could tell us how much of this demand recovery can survive a cost pass-through.

Second, plant utilisation. New plants carry fixed costs whether they run at 50% or 90%. If demand holds, these investments pay for themselves through scale. Otherwise, they become a drag on margins.

Third, EV traction beyond early adopters. Tata is furthest on this curve. In contrast, both Hyundai and Maruti have more calculated bets. We are still in the midst of finding out how different green technologies in India will progress.

Tidbits

[1] Tata Electronics to begin chip packaging at Assam plant

Tata Electronics plans to start semiconductor chip packaging at its upcoming OSAT facility in Assam, initially serving automotive and industrial clients. The company is fast-tracking operations to prove manufacturing capability early, with the plant expected to scale up sharply by year-end.

Source: Economic Times

[2] India may extend and expand e-two wheeler subsidies

The government is considering extending the PM E-Drive scheme with fresh funding to continue supporting electric two-wheelers. Officials are looking at higher subsidies as India pushes electric mobility to cut dependence on imported oil and accelerate EV adoption.

Source: Mint

[3] West Asia tensions may push subsidy bill 50% above target

The government’s subsidy expenditure could overshoot budget estimates by nearly 50%, mainly due to rising fuel and fertiliser costs linked to the Strait of Hormuz crisis. Higher LPG and fertiliser subsidies may significantly increase fiscal pressure if energy prices stay elevated.

Source: Financial Express

- This edition of the newsletter was written by Pranav and Vignesh.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

If you’re a woman who feels intimidated by the world of money, In Her Interest is meant for *you*.

Most women share a complicated relationship with money.

On one hand, women are expected to be exceptionally good with it. They manage household budgets, track expenses, stretch money, save for emergencies, and make a hundred tiny financial decisions every month.

When money conversations turn more formal, though; when they shift to investments, insurance, taxes, or business finances, they suddenly defer to someone else — a father, husband, brother, the family CA, or “the finance person” in the family.

To us, this weird duality seems to creep in because most women have never had a friendly, low-pressure place to learn their way around it.

That’s what In Her Interest, a Zerodha initiative, is trying to create. In Her Interest hosts small, in-person sessions where women can ask normal money questions without being judged, sold to, or drowned in jargon. The next few sessions cover finance for entrepreneurs in Gurugram, smart money management in Mumbai, investing basics in Pune, and the basics of mutual funds in Hyderabad. If you’re a woman who has been meaning to get a little more comfortable with money — or know someone who might — this is a fantastic place to start!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Spacex success requires successful launch and escaping the gravity of markets doubts

. A moonshot