SIPs, slumps and the AMC machine

How mutual funds survived the sell-off

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Making record money in a falling market: Q4 at the AMC business

The double-edged sword of India’s digital financial inclusion

Making record money in a falling market: Q4 at the AMC business

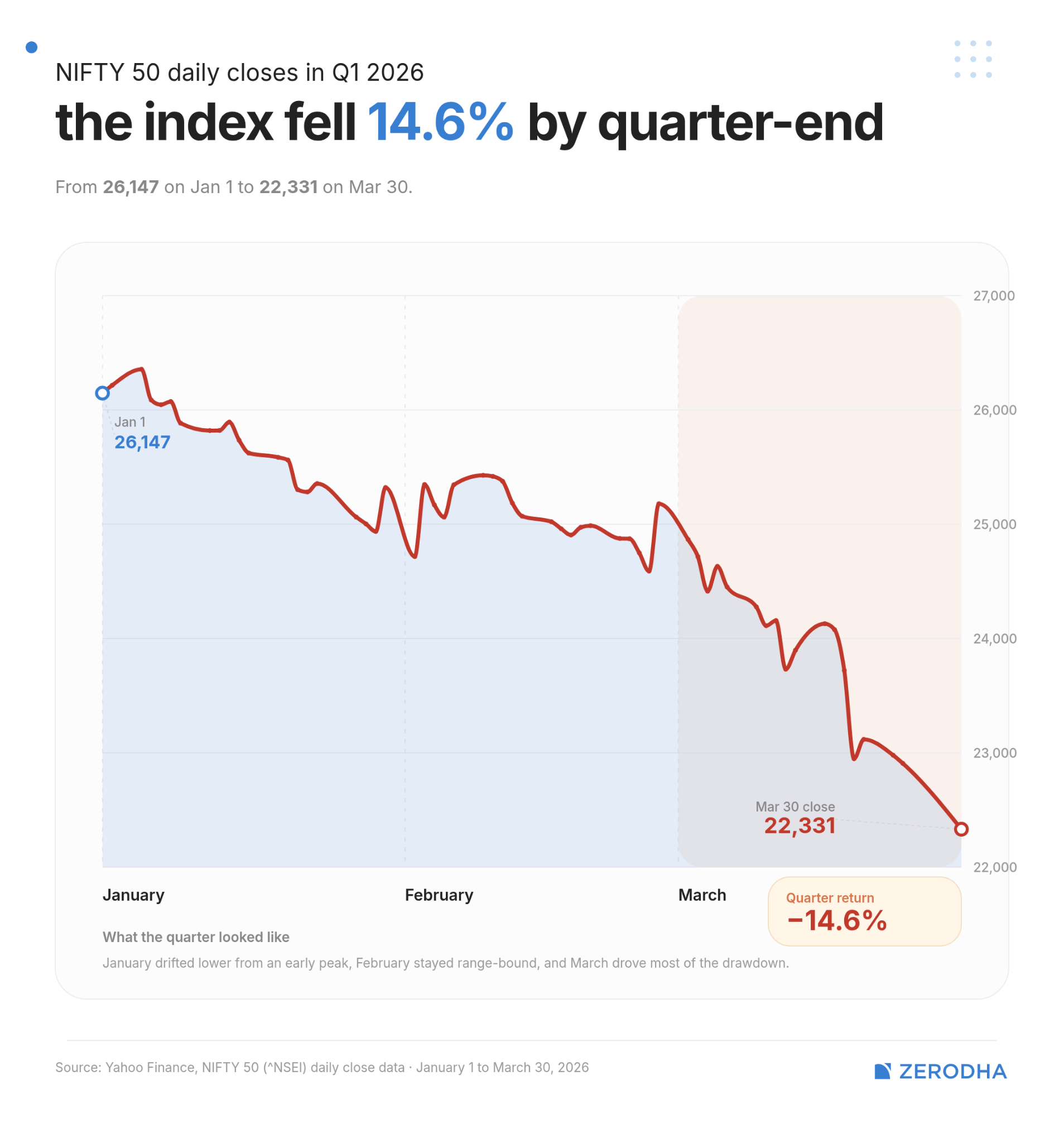

The Nifty 50 fell roughly 14.5% between January and March this year — its worst quarter in two years. In the same three months, the Indian mutual fund industry took in more equity money than ever before. Their net equity inflows for the quarter touched ₹1.24 trillion, the highest on record. In March alone, Systematic Investment Plans (SIPs) brought in an all-time monthly high of ₹32,087 crore.

This is not supposed to happen. Retail money is supposed to flee a falling market. It… didn’t.

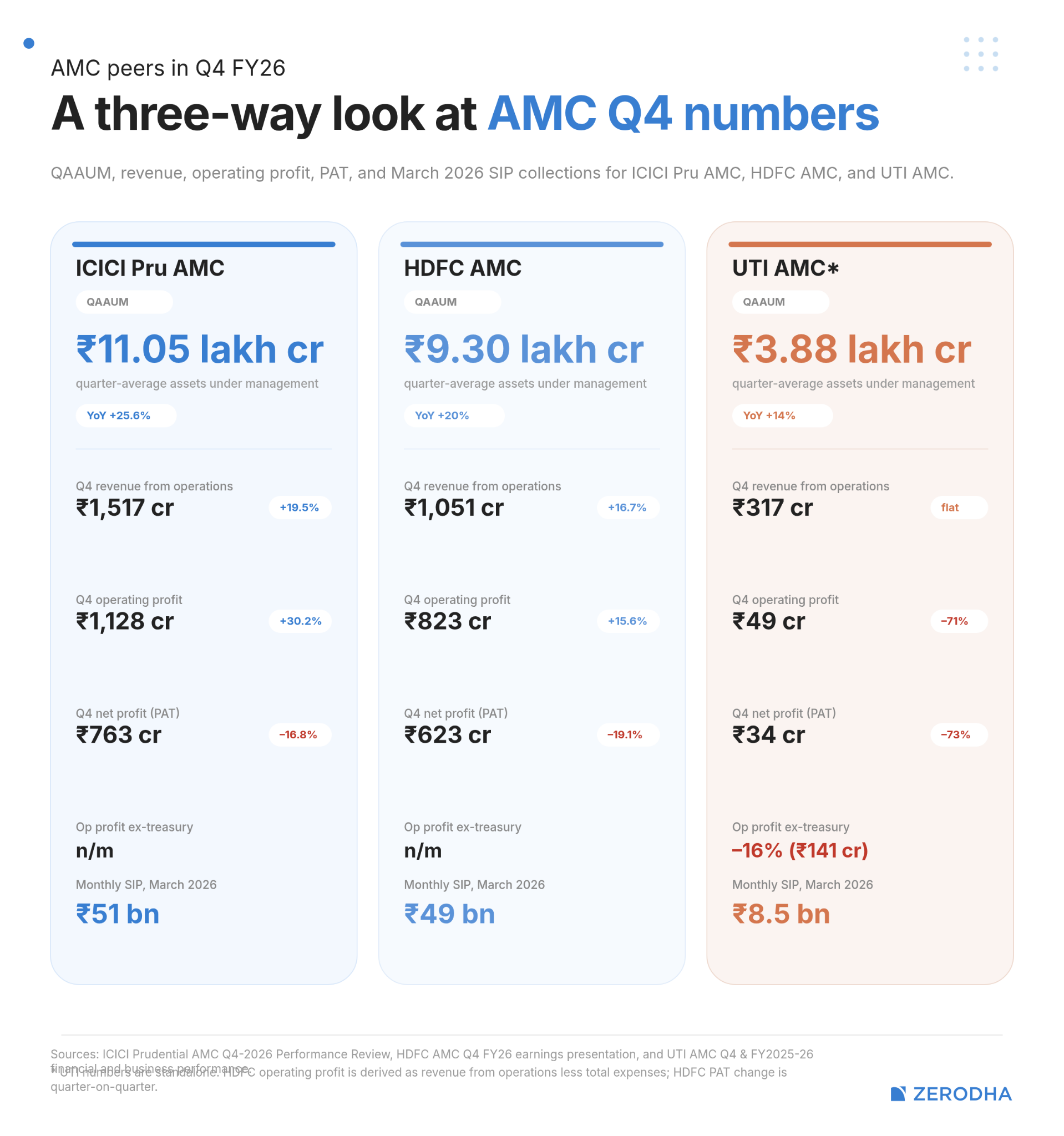

What, then, is happening? For answers, we’re looking at the results of three asset managers. We look at India’s largest AMC by size — ICICI Prudential AMC, which crossed ₹11 lakh crore in average assets this quarter. We also look at HDFC AMC, the AMC with the cleanest margins in the industry — as close to a gold standard as the industry has. And finally, we look at the champion PSU, UTI AMC, which is the oldest of the three, and the only one without a bank parent.

Each is a story of how to survive a fundamentally difficult quarter.

The numbers

Before we get to the industry’s broad fortunes, let’s take a tour of the numbers.

We start with ICICI Pru AMC. The company crossed ₹11 lakh crore in average assets this quarter, a quarter higher than where it was last year — its growth well ahead of the industry’s 21% year-on-year. Its revenues, too, were up ~19.5%. And its operating profits grew even faster, at just over 30% year-on-year, as its operating margin expanded. It was a story of scale economics. The company’s assets went up sharply, pushing up revenues. And as costs stayed flat, its profits widened too.

And yet, the company’s bottom line — its net profit — fell roughly 17% from the December quarter. We’ll get back to this shortly.

HDFC AMC’s quarter, too, looked similar. Its average assets, at ₹9.3 lakh crore, were up about 20% year-on-year. Its revenue climbed almost 17%. And its operating margins stayed around 80% — unparalleled for a Indian financial-services franchise.

That was a strong quarter, by any metric. And yet, like ICICI Pru AMC, its net profit fell almost a fifth from the previous quarter.

UTI, meanwhile, is a different kind of company, and its Q4 was very different as well. The company took a severe beating at a consolidated level — with revenues down 25% from the last quarter, and a net loss of ₹67 crore. That’s the first time in years that UTI’s bottom line was red.

Those figures include a lot of noise from its international subsidiaries, though. Its domestic mutual fund, by itself, is chugging along well. The company’s mutual fund average assets grew 14% to ₹3.88 lakh crore — slower than the industry’s 21%, but growing all the same. Its core profit rose about 3%. And the company held on to its structural moats — including its 24% share of the National Pension System.

It was UTI’s international book that failed. Its overseas subsidiary lost more than a third of its assets in a single year.

The two businesses inside an AMC

As you’ve probably noticed, there’s some weirdness here. Companies with soaring assets under management seem to have taken a serious beating in their net income? How could that happen?

The answer lies in a little line item called “other income”.

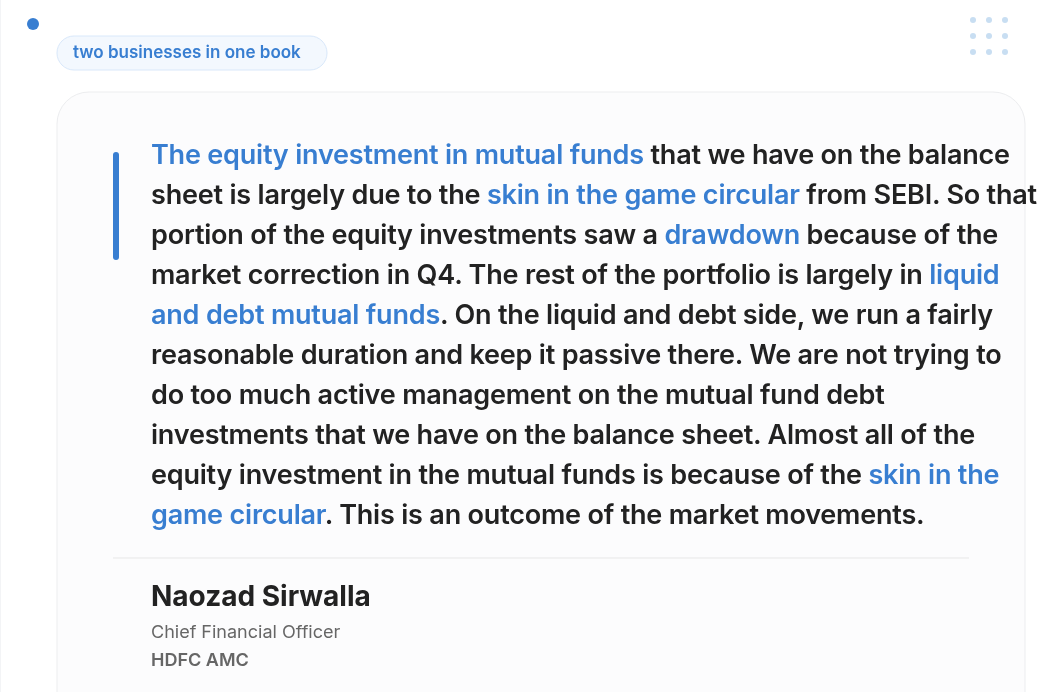

See, every Indian asset manager is required by SEBI to put some of its own corporate cash into the funds it sells. This gives it skin in the game: if someone sells you an equity fund, it should have enough conviction to invest in that fund itself. It’s sensible as policy, but it has a weird accounting consequence: that money sits on the AMC’s balance sheet, and gets marked to market every three months. Any paper gains or losses for the quarter are considered “other income”.

In a way, an AMC’s profit and loss statement essentially tracks two businesses sitting in one company. It has a fee business — where it collects management fees on the money it manages for clients. This is slow and predictable, and scales with assets.

But it also has a treasury: its own savings, sitting inside its own funds. These point wherever the markets do.

In a rising market, both can look great. In a falling one, however, the treasury can rack up massive paper losses, eating up the fee business’s profit. In one of NIFTY’s worst quarters in recent memory, these paper losses battered these companies’ books.

If you’re trying to get a read on the core business, especially in a quarter when the markets are down, it’s smarter to look at their operating profits alone. On that basis, ICICI and HDFC’s AMCs both had a fine quarter; their operating profits growing by ~30% and ~16% respectively. On the other hand, UTI AMC still saw a major drop in profits — even setting aside its treasury hit of ₹92 crore, its operating profit was down 16%. [Note: A previous version of this piece incorrectly suggested that UTI AMC saw a loss of 16%.]

Surviving volatility

The AMC industry’s headline numbers look terrible this quarter. Assets under management cratered all through the quarter. In the single month of March alone, the industry’s closing assets fell roughly 10%, from ₹82 trillion to under ₹74 trillion.

This was, to a large extent, a simple consequence of the quarter’s market correction. The NIFTY 50, of course, fell drastically. With it, broader market indices fell 16% as well. Even if investors didn’t pull out, their units became less valuable over the quarter. This all came in a terrible global backdrop, with the West Asian war making everyone jittery.

Not all of it was a simple story of stormy markets, of course. There was a seasonal trend at play; every March, corporate treasuries pull cash out of liquid and money-market funds to pay advance tax and tidy up their year-end balance sheets. These are mechanical outflows, many of which are reversed by April. For the quarter, however, overnight funds bled around ₹40,000 crore in March alone; money-market funds another ₹29,000 crore.

Seasonal variations aside, though, t’s worth asking how long the bleed can last before AMC profits take a beating as well. As the management of ICICI Pru AMC noted, this isn’t one bad quarter; it’s the eighteenth straight month of subdued equity returns. Indian equities have been going essentially nowhere since September 2024.

How, then, should we think of the industry’s fate? Turns out, things look rather… optimistic.

Resilient retail

In a quarter that butchered most portfolios, interestingly, retail money kept flowing into the markets.

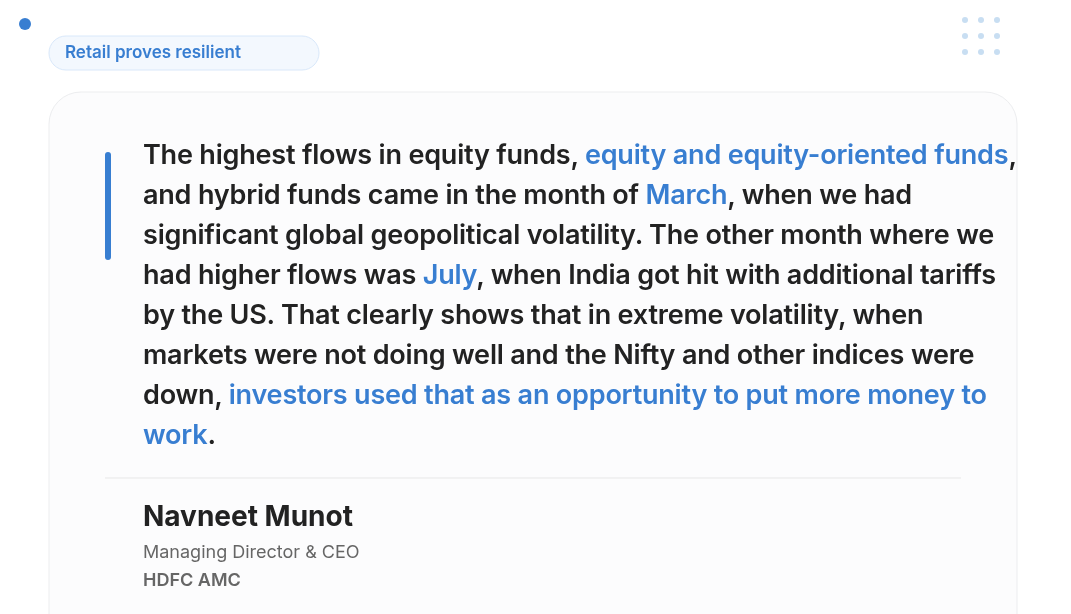

This isn’t random noise. The two worst months for the markets, this fiscal year, were the two months that saw its highest equity flows. As HDFC AMC’s management put it, their highest flows came “...in the month of March, where we had significant global geopolitical volatility. And the other month where we had higher flows was in the month of July, when India got hit with additional tariffs by US.“

Interesting, isn’t it: it wasn’t simply that flows held through bad news; they intensified.

ICICI Pru AMC’s management said something similar: “when the markets are down, people tend to also increase their SIPs.” That is, ticket sizes were going up, not down, when the markets were down. Retail investors, it appears, are learning to buy the dip.

Much of this money, increasingly, is invested passively. As the management of ICICI noted, there’s a new crop of young, “digital native” investors that are entering the markets exclusively through SIPs. These investors are hard to shake off: they keep money in the markets for years at an end. As the management of UTI noted, for instance, 97% of their SIP book is more than five years old.

India’s retail investors, in short, are emerging as a strong counter-cyclical force. When the markets go down, they’ve become shock absorbers, putting a floor to its misfortune.

Responding to the squeeze

Market volatility, however, isn’t the only pressure AMCs are dealing with.

For one, there’s a flip side to the rise of retail passive investing — the active funds AMCs offer are losing their appeal. That hurts their earnings. The blended fee an AMC earns per rupee invested in a passive product is much lower than what they earn from active products. ICICI, for instance, earns roughly 67 basis points on the assets in its equity book, but just 10 basis points on its passive book. That’s almost a sevenfold gap.

There are also new regulatory pressures on the industry. SEBI’s new Base Expense Ratio framework, which took effect on April 1, removed a 5-basis-point allowance that AMCs used to keep with themselves instead of charging exit loads. This is profit that’s simply lost.

How is the industry surviving these pains?

For one, all three companies simply passed much of the regulatory hit downstream. That 5-basis point allowance used to be paid out as distributor commission. When the hit eventually came, it landed on those commissions too. All three rolled out lower distributor commission structures the moment the new rule took effect. As UTI’s management said, rather bluntly, “whatever impact is there that we’ll be passing on to the intermediaries.“

AMCs are also trying to diversify their businesses to meet market shifts. While surrendering the bulk of retail investing to passive funds, they’re pushing hard into higher-margin alternate products — Portfolio Management Services (PMS), Alternative Investment Funds (AIFs), private credit, and a newer category called Specialised Investment Funds (SIFs). These come with their own economics. As ICICI Pru AMC’s data shows, PMS and AIFs earn a gross yield of around 200 basis points of assets, and roughly 98 basis points net of distributor commissions. That’s nearly ten times what passive earns.

Take SIFs, for instance. They’re a brand new product, with a ₹10 lakh entry ticket. ICICI launched its first two SIFs in January and crossed ₹19 billion in assets by March. The other two are planning their own SIF launches as well.

Finally, to diversify their offerings, these companies are all moving abroad, with outposts in GIFT City and Dubai’s International Financial Centre. GIFT City offers a wrapper for both inbound foreign capital and outbound Indian investments, with better tax treatment. Dubai opens up the wealthy Indian diaspora in the Gulf. Both are long bets.

But there are risks to this diversification. UTI, for instance, suffered a terrible 35% collapse in international assets, as foreign investors rotated away from India.

Two questions, three bets

In all, India’s AMC businesses seem reasonably unscathed, in a quarter that should, by all accounts, have been brutal. But there are a few questions worth asking of the business.

One, what happens, in the long term, to active funds? Across the industry, for instance, only 13% of large-cap schemes have managed to generate any alpha over their benchmark in the last ten years. Does this imply that they’ll simply keep losing out to passive investment?

Two, can retail interest stay around forever? Sure, eighteen months of subdued returns hasn’t broken the SIP discipline. Can they survive twenty four? Thirty? Is there a point where there’s a rout?

You can see each of these companies’ recent pivots as an answer to these questions: they’re chasing new products and new geographies, not because they’re building on a base of resilience, but because they’re reading the tea leaves. The AMC business lives on diversification. That is, evidently, a lesson that applies to its operations too.

Will these work? Well, as Nimesh Shah, the CEO of ICICI AMC, said on their investor call: “I always like an environment where the customer is slightly asking more questions before investing. It is always a very healthy kind of sales when customer is a bit skeptical.“

The same, of course, goes for his own business as well.

The double-edged sword of India’s digital financial inclusion

In Oct 2024, the Indian government announced something that would have seemed fanciful a decade earlier: UPI had processed 1,600 crore transactions in a single month. Not 1,600 crore rupees, but 1,600 crore separate payments. UPI had, in under a decade, transformed from a government experiment into the backbone of everyday economic life for hundreds of millions of people.

The international attention has been extraordinary. The IMF has studied it. Singapore adopted it. France uses it at the Eiffel Tower. The NPCI has been in talks to export the infrastructure to other countries. UPI is indeed one of the great success stories of the digital age.

However, embedded in that story is a claim that digital financial inclusion is an undoubtable force for good. But how? Does it improve, say, access to credit? Does it improve quality of life, and if yes, then how so? On the other hand, does digital inclusion open up new threats like cybercrimes?

A recent paper by researchers Abhishek Kumar, Sushanta Mallick and Apra Sinha asks some of these questions by analyzing one specific angle: the effect of digital financial inclusion on the long-term consumption of households. The answer is more complicated than the popular story suggests.

What is financial inclusion?

Before we get to the findings, it’s worth understanding what financial inclusion is supposed to accomplish.

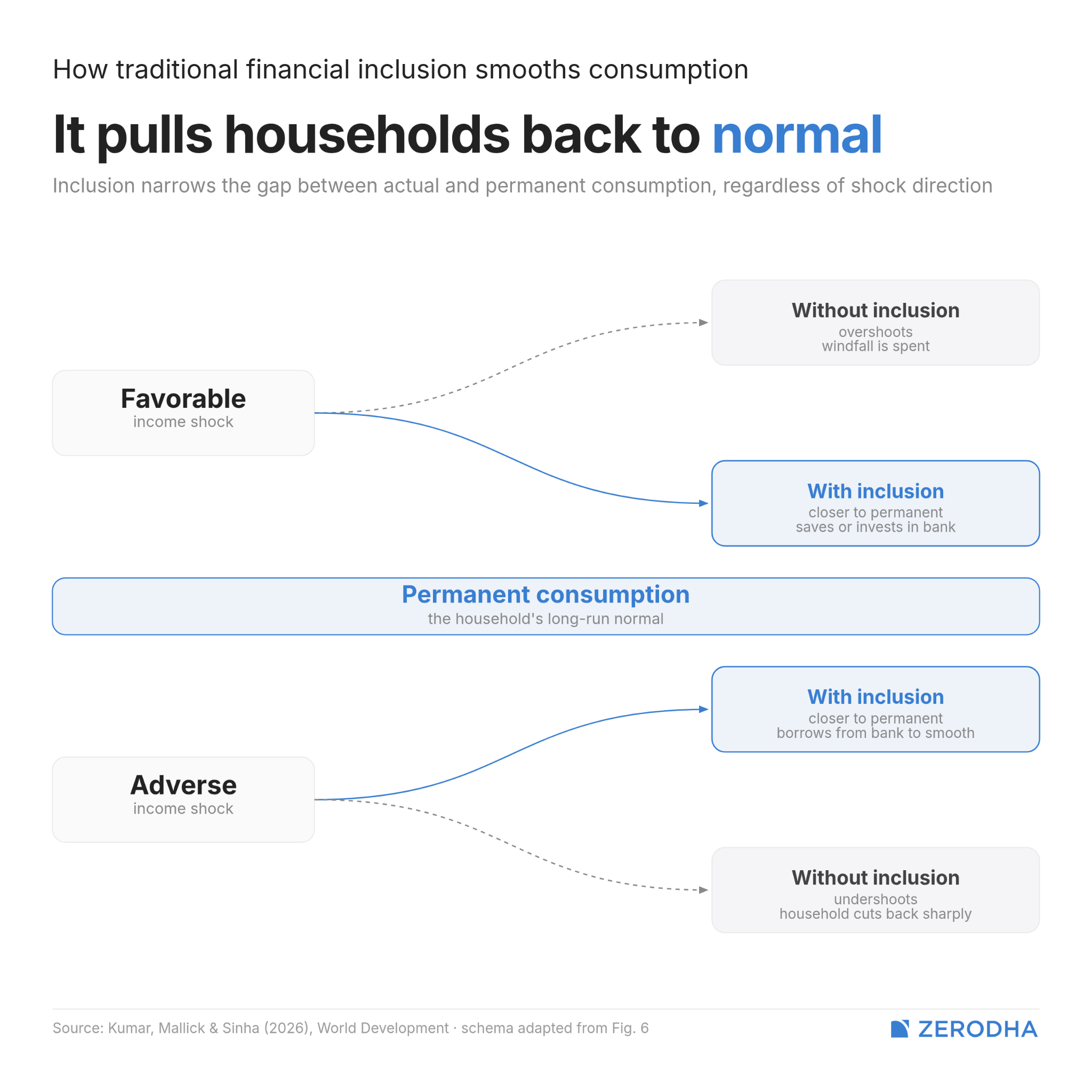

See, households face good years and bad years, windfalls and crises, months when income is steady, and months when an illness or crop failure cuts it down sharply. However, on average, a household would ideally spend roughly the same amount. Economists call this “consumption smoothing“. You borrow in bad times, save in good times, and your actual spending stays close to what your long-run income can support.

The problem is that this requires working financial infrastructure. You need a bank account to save. You need access to credit at reasonable rates when income drops. Without either, households get thrown around by every shock. You might spend too little when times are bad because they have no buffer, or spend erratically when cash suddenly arrives. Financial inclusion, in theory, could fix this by bringing households closer to their permanent, steady-state level of consumption and reducing the fluctuations.

But this refers entirely to traditional modes of financial inclusion, which mostly involve banking channels. What the paper asks is: does digital financial inclusion actually do this? Or does it do something else entirely?

Traditional financial inclusion and digital financial inclusion are not the same thing. Traditional inclusion means access to a bank account, a post office account, or formal credit — these are institutions that come with relationship-based lending and meaningful reductions in borrowing costs. Digital inclusion means access to an e-wallet: a mobile application that lets you make payments and transfer money, like Paytm, Fino, Airtel Payments Bank, and so on. This category does not include individual bank apps.

These are fundamentally different relationships with money. And the paper sets out to test how each of them impacts fluctuations in consumption when there’s a shock or a windfall.

To measure this, they use data from the All India Debt & Investment Survey (AIDIS) of 2019, which covered over 100,000 households nationwide. From this data, they first estimate what each household’s “permanent consumption“ should look like. This forms a steady baseline, predicted by wealth, education, occupation, age, and location.

Then, they calculate each household’s actual deviation from that baseline. A household spending wildly above or below its long-run baseline has high transitory consumption. Ideally, financial inclusion, if it’s working as advertised, should bring transitory consumption down.

The wallet isn’t the bank

The findings cut against the received wisdom on digital financial inclusion.

Traditional financial inclusion, or having a bank account, is associated with lower transitory consumption. It brings households closer to their permanent spending baseline, exactly as economic theory predicted. When something goes wrong, like a sudden medical emergency that demands expenditure, traditionally-included households are better able to absorb the shock and keep their spending steady.

And that makes plenty of sense. After all, traditional bank account access sharply reduces the interest rate on loans for households, by somewhere between 0.8-2.4%. Low-income households, though, don’t have that kind of access — which is partly the reason for the rise of non-banking financial infrastructure.

However, the researchers find that digital financial inclusion does the opposite. As per the data, households with e-wallets showed higher transitory consumption than those without. What that means is that their spending is more volatile and further from their long-run baseline.

What e-wallets do is make spending easier and more frictionless. The authors use that fact to argue that the very features that make UPI so convenient also lower the psychological barriers to spending. The tap of a phone doesn’t feel the same as parting with cash. For households that are already stretched, that frictionlessness may mean spending more than they should when money comes in, rather than saving it or using it to cushion future shocks.

E-wallets also reduce borrowing costs, but only by 0.23 to 0.33 percentage points — hardly as strongly as traditional banks. They simply don’t come with the financial infrastructure that makes consumption smoothing actually possible.

The consumption effects are also driven primarily by households that actively transact, not merely those enrolled. What that means is simply having access to a wallet, in other words, isn’t enough to move the needle — the behavioral effects only kick in with active use.

The poorest pay the price

The paper’s most consequential finding is about who really bears the cost of this.

Household wealth, the authors find, is the biggest determinant of how digital payments drive transitory consumption. For the poorest quartile of Indian households, digital financial inclusion is most strongly associated with overspending relative to long-run income. But as you move up the wealth ladder, the picture changes. Among wealthier households, digital inclusion instead begins to help with consumption smoothing.

The reason is fairly obvious. Wealthier households have other financial buffers, like savings, assets, and most importantly, access to traditional banks. For them, an e-wallet is an additional convenience sitting on top of a functioning financial system. They might overspend slightly in good times, but they have the capacity to absorb it.

For poor households, the e-wallet is often the only layer of financial infrastructure they have. They don’t have a savings cushion. They can’t borrow cheaply when things go wrong. What they have is frictionless access to spend whatever cash they happen to have on hand. That leads to greater fluctuations in their consumption patterns, not less.

This asymmetry also shows up in the paper’s analysis of which direction consumption tends to swing in each case. Most of the time, traditional inclusion helps households by cushioning negative income shocks. In contrast, digital inclusion is usually found to drive up transitory consumption without doing much to help in bad episodes.

In essence, the wallet is not much more than a spending tool. It is not, at least for poor households, a financial security tool.

There’s a social dimension to this too. The paper finds that traditional financial inclusion remains unequally distributed across caste lines, with SC/ST households significantly less likely to be traditionally included than general category households. Digital inclusion, by contrast, is more evenly spread across social groups. Ironically, the more equitable form of inclusion is also the one that, for poor households, makes financial volatility worse.

In fact, the paper also finds that the consumption gap between digitally included and excluded households is actually wider than the gap between traditionally included and excluded households. That’s despite the fact that the wealth gap between the digital groups is much smaller — a reflection of how evenly spread digital financial infrastructure has been in India.

More than access

Of course, none of this means that digital financial inclusion is bad in any absolute sense. Their point is more precise: access alone is not the same as financial empowerment. Policies that treat digital inclusion as a substitute for traditional financial infrastructure, rather than a complement to it, are likely missing the most important part of the picture.

Two policy directions follow from the findings. The first is digital financial literacy — helping households understand not just how to use mobile wallets, but how to use them without falling into patterns of impulsive spending. The behavioural forces driving frictionless spending are real and powerful, and the finding that the problem is most acute for the poorest households suggests that targeted interventions could have meaningful impact.

The second is regulatory attention to the lending practices that have grown up around the fintech ecosystem. India’s digital lending landscape — like buy-now-pay-later apps, or instant credit lines embedded in payments apps — has expanded rapidly. If digital inclusion is to deliver the financial resilience that policymakers have promised, the credit ecosystem around it will also need to do the same.

India’s UPI story is, by any measure, a genuine achievement. But infrastructure is not the same as outcomes. Getting a wallet into someone’s hands is not the same as making them financially secure. And for the households at the bottom of the income ladder, the wallet alone may not be enough.

Tidbits

[1] CEA flags energy imports as key risk to India’s growth

Chief Economic Adviser V Anantha Nageswaran warned that energy price volatility due to West Asia tensions is a major risk for India. Heavy dependence on imported fossil fuels makes growth vulnerable, especially impacting small businesses and farmers. He said boosting productivity and digital infrastructure is key to offset shocks.

Source: Economic Times

[2] India floats mega fertiliser import tender before sowing season

India has issued a global tender to import 85 MT of fertilisers to build reserves before the key kharif season. The move comes amid rising global prices and supply risks due to West Asia tensions, as India remains heavily dependent on imports for key inputs.

Source: Economic Times

[3] Rice exporters seek govt help over China GMO issue

Indian rice exporters have asked the government to intervene after China rejected shipments citing GMO concerns and suspended some firms. The move has caused financial losses and uncertainty, with exporters seeking quick resolution and clarity to protect trade.

Source: BusinessLine

- This edition of the newsletter was written by Pranav and Manie.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

How can Indian IT flip the AI script ft. Ameya P

The age of AI agents has, so far, been a thorn on Indian IT’s side, at least as far as valuations are concerned. Its business model is getting stale each passing day - that’s understood. There might be a possibility that Indian IT might just adapt to the new paradigm. But what does adaptation for Indian IT look like? What are the forms of inertia they will have to overcome to successfully change themselves? And even if they do adapt, will they be able to defend their new business?

To unpack all this, we spoke to Ameya P, a veteran in the global IT industry, and a prolific technology investor well-known for his investing takes on X. It’s an incredibly nuanced conversation from an expert who understands the nitty-gritties of what each AI development brings forth for this industry.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

On the surface, fundamentals remain strong.

But beneath that, multiple forces are beginning to reshape the sector.

Leadership uncertainty at major institutions like HDFC Bank is starting to influence valuations across the market reminding us that confidence is not built on numbers alone, but on clarity and stability at the top.

At the same time, regulatory shifts are providing support.

Simplified capital rules are making it easier for banks to reflect their financial strength, improving flexibility and transparency.

But the bigger picture is more complex.

Globally, a new risk is emerging one tied to the very technology driving market optimism.

The rapid expansion of private credit funding into AI infrastructure is raising concerns about overvaluation and systemic exposure.

If expectations shift, the impact could extend beyond tech and into the financial system itself.

Back home, the direction is clear.

Indian banks are preparing to scale globally, with expectations of greater representation among the world’s largest institutions.

And alongside this growth, regulators are tightening oversight ensuring that riskier activities are separated from core banking operations to protect stability.

This is what transition looks like:

Pressure and progress happening at the same time.

Short-term uncertainty.

Long-term strengthening.

Because in banking, true resilience is not built when conditions are easy But when systems evolve before stress fully appears.

Hey guys - thanks again for the stories.

Just FYI - I think you are reading UTI's financials incorrectly. For UTI, the treasury operations are included in revenue rather than in other income, that's why we see so volatile financials for the company.