Should CSR be compulsory for companies?

Maybe, maybe not

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Should CSR be compulsory for companies?

When competition forces smart innovation

Should CSR be compulsory for companies?

Somewhere, in the fine print of India’s corporate law, sits one of the most unusual policy experiments in the world. Since 2014, any sufficiently large Indian company has been legally required to spend a fixed share of its profits on social causes. Not disclose or report what it spends. Our law mandates that they spend. No other major economy on earth does this.

Other economies — even those philosophically wedded to social spending — have something milder. The European Union’s landmark Corporate Sustainability Reporting Directive, for instance, requires companies to publish exhaustive data about their environmental and social footprint. What it does not do, however, is require them to open their wallets.

Section 135 of India’s Companies Act, 2013, meanwhile, does precisely that.

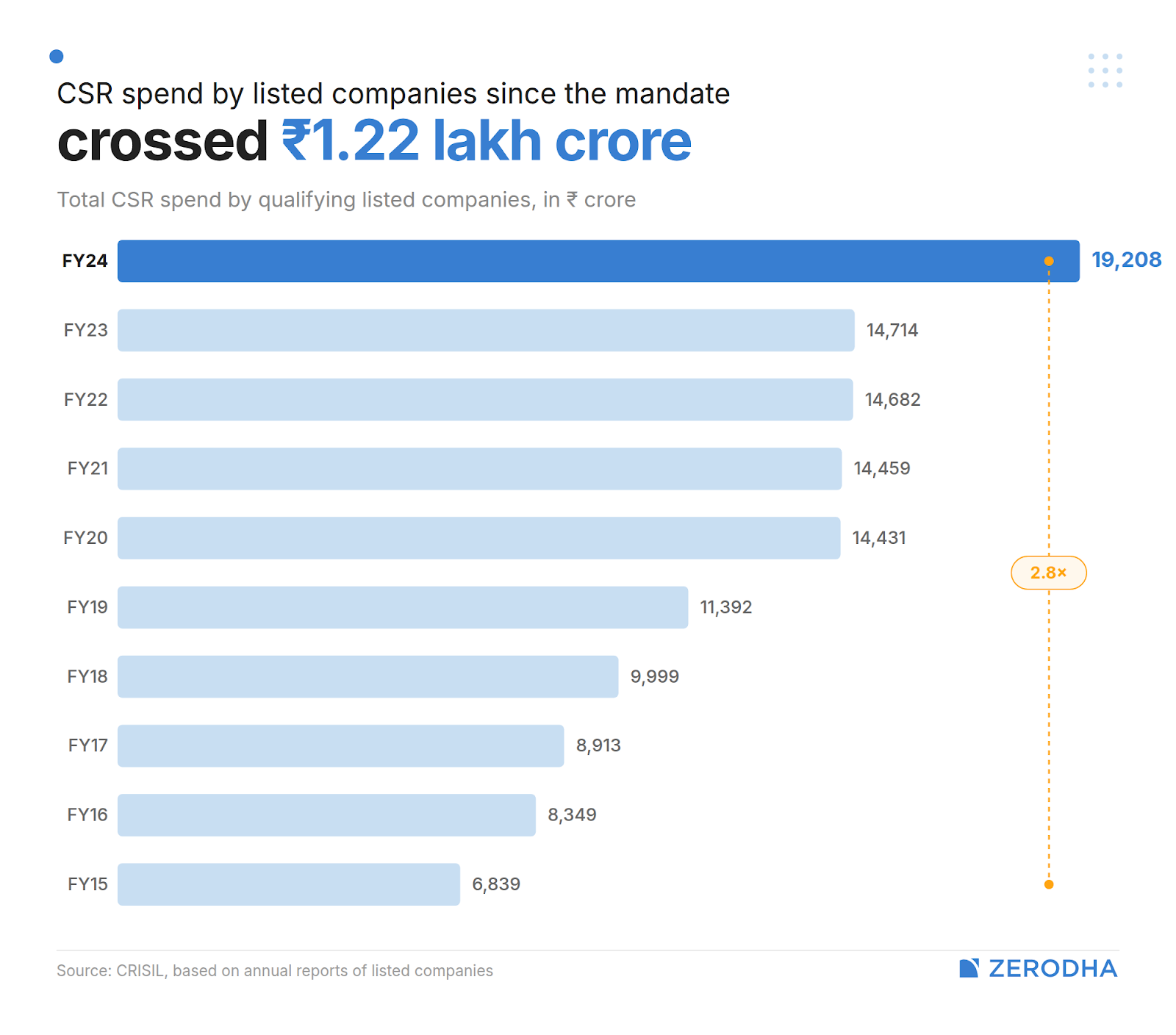

A decade since it kicked in, at least going by the headline number, this has unlocked a flood of capital for social issues. The qualifying listed companies have spent over ₹1.22 lakh crore on CSR activities since FY14. Compliance is near-universal and annual spends are rising.

Yet, a growing body of academic evidence tells a story that is more… complicated.

Why India decided to force companies to be generous

On two different occasions, before the 2013 law, India tried pulling corporate money for social causes voluntarily. In 2009, the Ministry of Corporate Affairs issued CSR guidelines. Another set of guidelines followed in 2011.

The industry ignored both.

SEBI jumped into the act, too. In 2011, it asked top listed businesses to submit Business Responsibility Reports, where they would have to answer 36 broad questions on different environmental and social themes. But they, too, did not require spending.

But in the political context of the day, people demanded more. India’s post-1991 liberalisation had produced extraordinary private-sector growth, but inequality had widened alongside it. When the Companies Bill was being debated in Parliament in 2012, 176 million Indians still lived in extreme poverty, while the top 1% captured 22% of national income.

When the Companies Act was first being drafted, the government attempted a comply-or-explain agenda. If a firm did not spend on social issues, it merely had to disclose why in the Board’s report, with no penalties. When the law went to the Parliamentary Standing Committee, they pushed for mandatory language. The law that was eventually passed, and came into force on April 1, 2014, required spending.

India had become a genuine global first. Mauritius, before us, had experimented with a 2% CSR rule from 2009, They, however, unwound it by 2015. India’s version has only grown since.

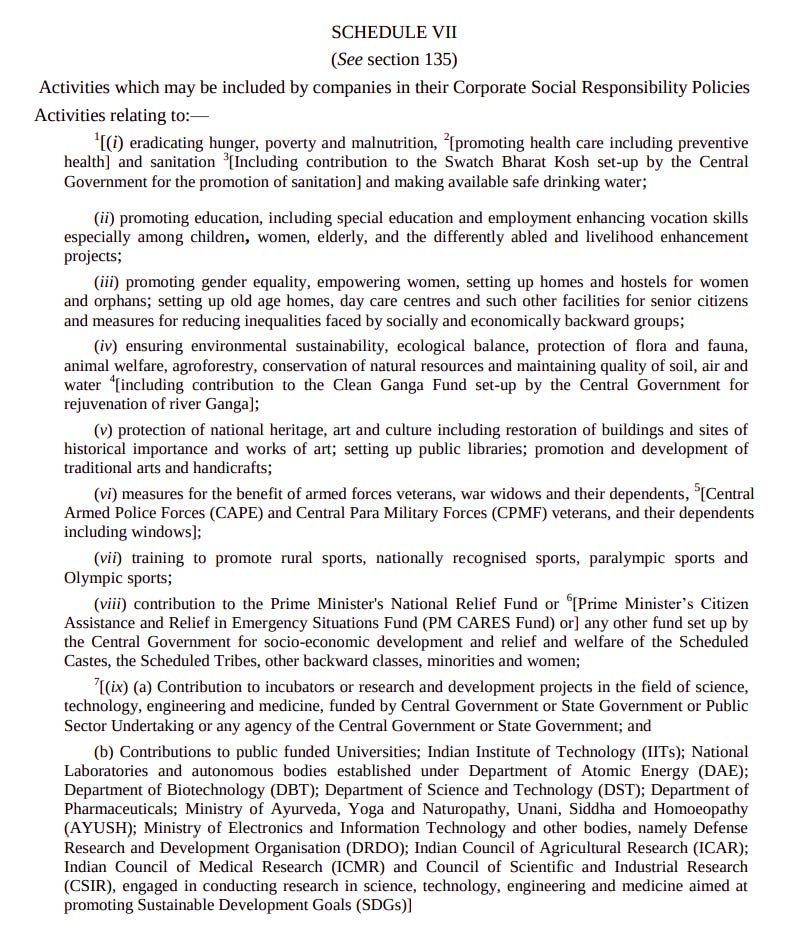

Here’s what the law actually requires: if you’re a company that crosses one of three thresholds — your net worth is above ₹500 crore, your turnover exceeds ₹1,000 crore, or your net profit crosses ₹5 crore — you have to spend at least 2% of your average net profits from the last three years on social issues. That money could go into education, healthcare, hunger eradication, or so on. The law carries a detailed list of activities you can spend on.

Companies spending more than ₹50 lakh must even constitute a board-level CSR committee to oversee the spending.

For a while, companies found it easy to get around these requirements. But amendments from 2021 turned the framework from comply-or-explain to comply-or-suffer. A failure to spend now carries real financial penalties.

A decade and ₹1.22 lakh crore later

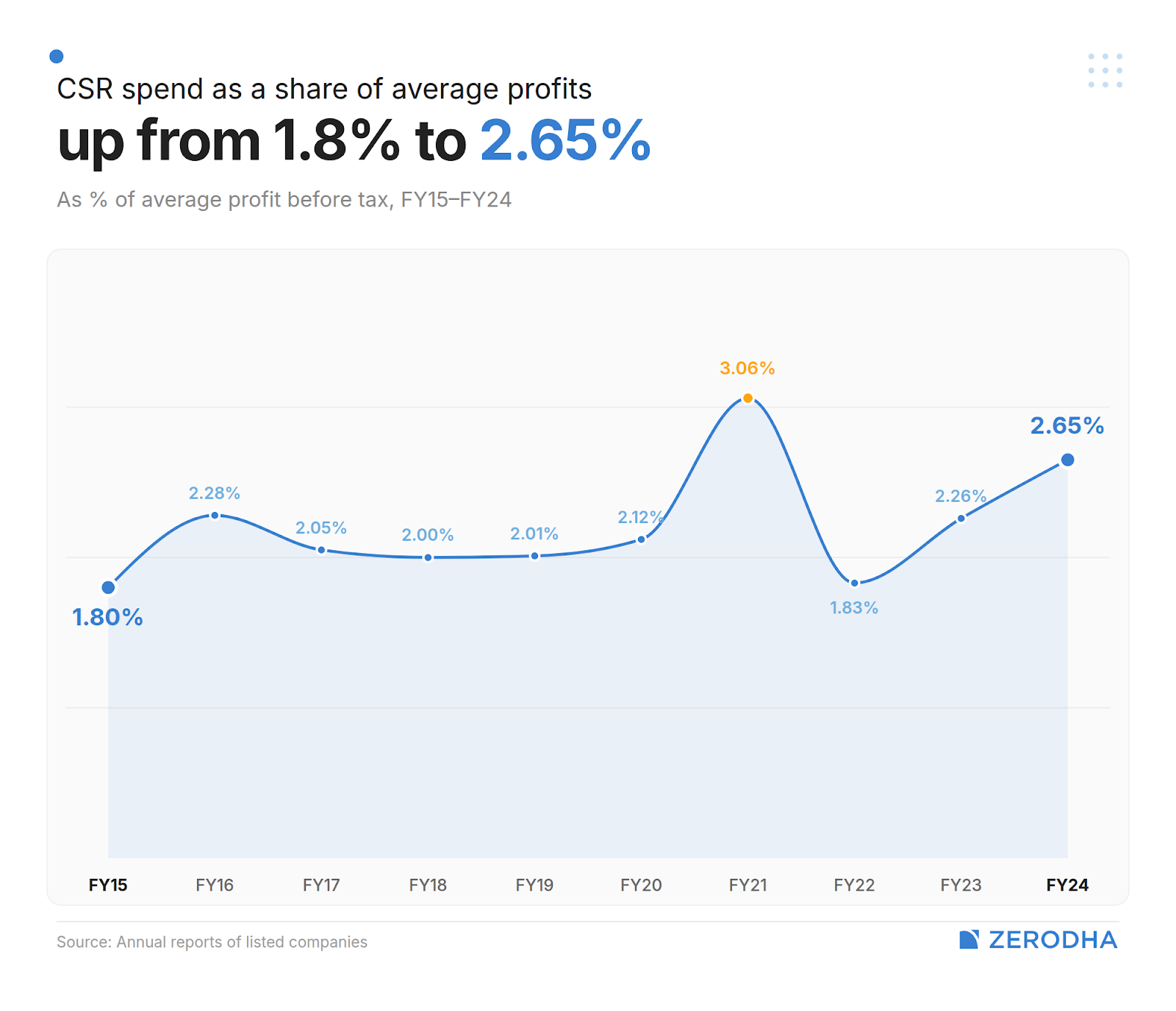

The new law unleashed a gigantic wave of spending. An addition ₹1.22 lakh crore hit the social sector. 63% of that amount — roughly ₹77,000 crore — arrived in just the last five years. In FY24 alone — a single year — companies deployed more than ₹19,000 crore. Two-thirds of companies now spend above the mandatory 2% floor: between FY 2015 and FY 2024, the aggregate spending, as a share of average profits, has risen from 1.8% to 2.65%.

If you wanted to prove that a legal mandate can mobilise private capital, India’s CSR data should be exhibit A.

But there are two structural patterns underneath the headline which tell a more complicated story.

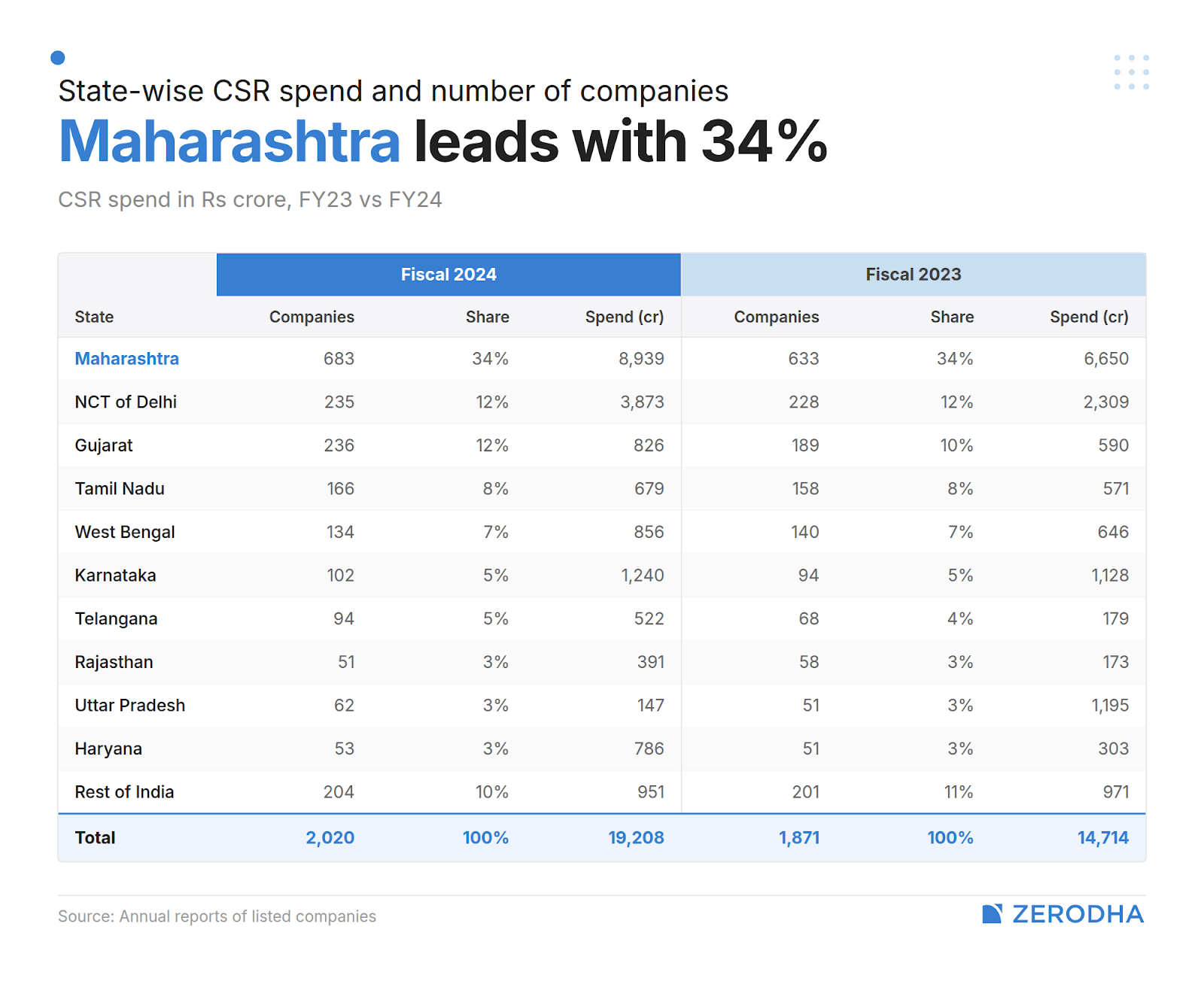

The first is geography. Maharashtra accounts for 34% of all listed-company CSR spend. Delhi takes another 12%. The top 10 states absorb 95% of the total. These happen to include some of the richest parts of our country. Meanwhile, India’s “aspirational districts” — the government’s designation for its most deprived areas — received just 12% of total CSR spend in FY24.

This flows directly from the law. The law has a “local area preference”, which was meant to ensure that communities near corporate operations benefit from their social spending. In practice, this just directs money toward industrial and corporate hubs. But these are already economically vibrant places. Instead of going to those who need it the most, money reaches places with the most business. The government’s own CSR portal acknowledges this skew, describing CSR spending as “supply driven” and noting concentration in industrialised states.

The second pattern is the quiet hollowing out of the NGO ecosystem.

At first, CSR money flowed into India’s NGOs, who were best placed to deploy it. But fly-by-night operators, too, saw this as an opportunity to get their hands on easy cash. Companies found it difficult to identify high-quality, transparent NGOs — particularly in rural areas. Instead, that money was routed through in-house foundations. The share of companies using external implementing agencies fell from 78% in FY20 to just 28% today. CRISIL explicitly flagged this as a challenge in its 2025 yearbook.

As a result, even though the mandate created a large statutory pool of social money, the organisations that had the community-level relationships to actually deploy it were slowly cut out of the pool.

When everyone does CSR, CSR means nothing

Social spending, elsewhere in the world, tells you something about those who spend.

When a company spends generously on social causes, it is a costly, credible signal. Investors could see it as evidence of institutional quality. Customers might interpret it as a proxy for trustworthiness. Employees could see it as evidence of the culture they’re joining.

That signal has value precisely because nothing requires it.

Of course, the signal isn’t the point — the spending is. But those bragging rights, alone, can push a company to contribute. It visibly did so in India, until the CSR mandate destroyed it. Rajgopal and Tantri, writing in 2021, looked at what happened to companies that were voluntarily spending large amounts on CSR before the law came into effect. The generosity of these firms, pre-mandate, had meant something.

Interestingly, after Section 135 kicked in, they no longer saw a point in giving out that signal. And so, they cut how much they spent. This cohort of companies actually slashed their CSR spending from 10.8% of profits to just 3.6%.

After all, why spend if it no longer differentiates you from the crowd? That 2% floor instead became the ceiling.

This might sound vain, but there’s an economic logic to it, worked out theoretically by Albuquerque, Koskinen, and Zhang in a 2019. For a company, CSR can be a product differentiation strategy. Companies that do it voluntarily have more loyal customers, who stick around even when things get rough. This insulates them from economic downturns.

But that only works when relatively few firms do CSR. If everyone’s compelled to do it, the differentiation evaporates, while the cost remains. Strategically, this no longer makes sense.

Instead, those companies started looking for other ways to stand out. The firms that cut CSR spending instead increased their advertising budgets by nearly 25%, trying to replicate the brand-building function that voluntary CSR had previously served.

That didn’t work for them, however. Researchers found that firms that made this switch saw their return on assets fall by 8% and return on equity fall by 11.5%, relative to pre-mandate averages. Advertising, it turns out, was a less efficient use of capital than the voluntary CSR those firms had previously chosen. So, the mandate cut down their generosity, while pushing firms into a replacement strategy that actively damaged their financial performance.

Doing good made firms riskier

Oddly enough, the capital markets punished CSR spending as well.

A study by Chauhan, Ghosh, and Jadiyappa ran an analysis, comparing companies forced into CSR spending against those that remained below the legal thresholds. Curiously, the firms mandated to spend experienced roughly an 8% increase in “systematic risk”, relative to those who weren’t.

Systematic risk, or beta, is a measure of how much a stock moves with the broader market. A higher beta means greater volatility relative to the economy. Those stocks’ prices swing harder than their peers.

Weird, isn’t it? Why would being forced to spend on social causes make a firm riskier?

The reason is operating leverage. Before the mandate, CSR was a discretionary expense. Companies could cut back in bad years, and scale up in good ones. This made it behave like a variable cost. After the mandate, they developed a quasi-fixed obligation — 2% of average profits — backed by financial penalties. No matter how that year’s business was, their previous profits weighed down the year’s P&L.

When a firm’s cost structure becomes more rigid, profits become more sensitive to revenue fluctuations. A drop in revenue now produces a steeper drop in earnings, because its costs don’t budge. The firm’s earnings become more cyclical. Its stock co-moves more aggressively with the market. And so, beta rises.

Another study found that the announcement of the mandate caused a 4.1% drop in share prices for anyone forced to spend — a decline that actually exceeded the 2% spending requirement itself. The market was pricing in more than just the cash outflow. It was looking at compliance costs, managerial distraction, and this operating-leverage effect. Other research found mandatory CSR also increased corporate debt yield spreads by around 43 basis points, adding financing costs on top of the equity risk.

There is also an irony to its tax treatment. CSR expenditure is explicitly not tax-deductible under Section 37 of the Income Tax Act, The government actually added a specific carve-out to deny this deduction. So, companies pay the 2% levy and cannot offset it against taxable income. This operates like a tax, but one that can’t be adjusted against what a normal business would attract.

All of this became a reason for companies to avoid qualifying for the CSR expense, and they found innovative ways to avoid it. Gangopadhyay and Homroy, found an unusually large cluster of companies reporting net profits that happen to fall just short of the ₹5 crores threshold that triggers the obligation.

How come? The firms near the threshold started inflating R&D expenditure, which is tax-deductible, to bring reported profits below the trigger. The spillover was oddly positive. These firms filed more patents and announced more new products than their peers. All of this was motivated by avoidance, not innovation. Another study found that mandatory CSR firms adopted more conservative accounting practices, recognising losses faster and gains more slowly, because CSR obligations are pegged to reported net profits. Conservative accounting, in this context, has become a tool for minimising a regulatory burden.

So did it work?

This isn’t to argue that CSR is worthless. It moved real money towards real needs. ₹1.22 lakh crore went to education, healthcare, and sanitation over a decade. During COVID-19 alone, nearly ₹7,000 crore in CSR funds went to healthcare infrastructure.

But the evidence suggests that while it increased the quantum of CSR, it reduced its quality. It made firms reluctant to spend because the signal that spending created was diluted. It also made firms riskier.

In other words, this was a trade-off. Maybe even a good one. But not one without problems.

How do India’s informal firms shape innovation?

The story of economic development, at its simplest, goes like this: poor countries have large informal economies, rich ones don’t.

As we’ve covered before, informality is usually a sign of an economy that is yet to fully develop. As incomes rise, firms formalize — they register, pay taxes, follow regulations — and the shadow economy gradually shrinks. And as they formalize, they also gain scale and increase productivity.

The journey in the middle of both these places is what’s really hard to navigate. And India is very much in that middle.

Depending on how you measure it, the informal sector accounts for somewhere close to half of our GDP, and over 85% of the workforce. These are firms that produce real things, like textiles, garments, furniture, and food, but do so outside the formal regulatory and tax system. Many of them, as we’ve covered before, are tiny household operations that aren’t very productive. Others may still be unregistered, mid-sized manufacturers with significant output.

This is where the standard development story gets complicated.

See, informal firms still compete with formal ones for similar resources. And since they’re informal, they skirt many rules that formal rules have to compulsorily adhere to. They’re not bound by labour laws governing minimum wages, working conditions, or severance. They don’t carry the overhead of formal compliance. That, in some cases, gives them an advantage that formal firms don’t have.

An intriguing new paper by management researchers Bibek Bhattacharya, Sudhanshu Maheswari and Ashneet Kaur looks at what happens inside formal Indian manufacturing firms when that competition intensifies.

Let’s dive in.

The hypothesis

The hypothesis of the paper starts with the idea that informal firms are cheaper — almost by design.

For a formal manufacturer trying to compete, this is a structural problem, not an operational one. You can try to cut costs, but there’s a floor below which you can’t go without breaking the law. And the informal competitor doesn’t have that floor.

The obvious response is to get better — to offer something the informal sector can’t easily replicate. But differentiation tends to require investment, spending on R&D and new technology, and so on. For the average small or medium-sized formal manufacturer, most of that is simply not viable. Access to capital is constrained, technical talent is expensive, and the returns on formal R&D investment are uncertain and slow.

So the paper asks a different question: is there a cheaper form of innovation that resource-constrained firms can reach for instead?

The answer it proposes is something the researchers call “innovation time off“. It’s the practice of giving employees discretionary time to experiment with new ideas, explore better processes, or think about improvements to products and marketing. Google’s famous 20% time policy, which reportedly gave engineers the space that produced Gmail, operates on exactly the same principle.

The implementation at an Indian SME is considerably more modest, but the underlying logic is the same. If you can’t buy innovation, you might be able to create the conditions for it to emerge from within. However, it’s worth noting that this “innovation” doesn’t refer to new technology or products. It relates primarily to process-level improvements.

The paper’s central hypothesis is straightforward. Formal firms facing greater competitive pressure from informal rivals should be more likely to turn to this kind of frugal, employee-driven innovation as a response. Managers, confronted with a competitive threat they can’t match on cost, redirect their attention toward building internal capability cheaply.

The main finding

To test this, the researchers used data from the World Bank Enterprise Survey of Indian manufacturing firms, conducted between 2013 and 2014. Informal competition was measured through a separate survey question asking how much of an obstacle the practices of informal competitors were to the firm’s current operations.

The hypothesis, it seems, held up: the more intense the informal competitive pressure a firm reported, the more likely it was to offer employees innovation time off.

When the pressure doesn’t translate

The main finding is that informal competition increases the likelihood of innovation time off. But the paper also asks: under what conditions does this relationship weaken? When do formal firms facing informal competition not respond by investing in employee-driven innovation?

The paper finds two factors that dampen the effect of informal competition. And in a way, they are very relevant to the broader Indian economy.

The first is whether the formal firm is located in a Special Economic Zone (SEZ).

SEZs in India offer formal firms tax exemptions, simplified regulatory procedures, better physical infrastructure, and a more predictable operating environment. These advantages allow firms inside SEZs to close some of the cost gap with informal competitors through policy rather than through internal effort.

As a result, the competitive threat from informal firms is less salient for SEZ-located manufacturers. The threat from informal firms feels less urgent to formal firms, and hence, the impulse to pursue frugal innovation doesn’t arise in the same way.

The second condition is labour flexibility.

Historically India’s labour laws have made workforce adjustment difficult for formal firms, and this rigidity itself is one of the structural reasons informality has remained so prevalent. Informal firms don’t have to comply with employment protection requirements at all, which gives them yet another dimension of operational agility. But some formal firms do possess meaningful labour flexibility — either through the nature of their contracts, or the composition of their workforce.

For these firms, the response to informal competitive pressure may run through a different mechanism. Rather than investing in internal innovation, they might choose to manage cost pressure by adjusting headcount — hiring and firing as per demand. It’s a rational competitive response, but it means the innovation channel gets weaker.

Caveats

There are a few caveats to these findings.

For one, the survey only asks whether firms grant employees this time — not whether anything useful comes of it. A firm could answer yes and have genuinely nothing to show for it: no new products, no process improvements, no measurable outcome. The paper is a study of the adoption of a practice, but not of its effectiveness. Whether innovation time off in resource-constrained Indian manufacturing actually produces better outcomes is a separate question that this paper doesn’t answer.

Secondly, what’s also worth acknowledging is the time period of the data. The findings come from a dataset that’s over a decade old.

Since then, India has changed in significant ways. GST was introduced in 2017 and has measurably pushed some activity into the formal economy, the regulatory environment has shifted, and digital infrastructure has expanded substantially. There are legitimate questions about how precisely these findings would replicate today.

But the informal sector in India is still enormous. It still employs the vast majority of the workforce, and the fundamental structural dynamics the paper describes haven’t been resolved. The broad direction of the findings is likely still valid, even if the precise magnitudes have shifted.

The unintended cost of protection

The policy implications that emerge from these findings are, well, complicated.

Both SEZs and labour flexibility are policy instruments that India has used to help formal manufacturers compete. As we’ve covered before, they can be highly valuable to India’s economic development, while also formalizing our economy further.

But the paper’s findings suggest they work with a side effect: by reducing the pressure that informal competition creates, they also reduce the likelihood that firms respond through this kind of low-cost, employee-driven innovation.

That’s not a reason to abandon SEZs or labour reform, and increasing formalization of the economy is certainly an aspiration worth striving for. However, policies that shield formal manufacturers from the cost disadvantages of informality may need to be paired with explicit incentives to invest in internal innovation capacity. Otherwise, protection enables survival without necessarily enabling growth beyond it.

This conundrum is less about how innovation works, and more about how a developing country is forced to fight through its constraints.

Tidbits

Bharti Airtel has secured a $1 billion investment in its data centre subsidiary Nxtra Data from Alpha Wave Global, Carlyle, and Anchorage Capital. This to expand its network footprint across India. Airtel is also investing in the round.

Source: Business StandardThe government hiked ATF prices by over 115% to Rs 2.07 lakh per kilolitre. This reflects the full pass-through of surging crude prices to aviation fuel. IndiGo has already added a Rs 10,000 fuel surcharge on long-haul international routes in response.

Source: Business TodayTVS Motor posted its strongest-ever March with total sales surging 25% to over 519,000 units. EV sales jumped 44% to nearly 39,000 units, three-wheeler sales rose 46%, and international business grew 25%. The numbers cap a record quarter for TVS on sales, revenue, and profits.

Source: LiveMint

- This edition of the newsletter was written by Kashish and Manie

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

On Informal Competition:

Big retailers (including online ones that offer fast home delivery) often don't source from informal suppliers because their papers are often not in order. e.g. Big retail only stocks garbage bags with thickness >= legal minimum. But many kirana shops stock the thinner, cheaper ones. So the access to big, organised markets is limited for the informal sector in some cases.

"the survey only asks whether firms grant employees this time" to be sure, it should have cross-checked with employees too.

Good article.

While the arguments about relaxing the location where CSR money can be spent and possible tax relief sound fine, the other arguments against CSR spending seem out of place

Reduced CSR spending due to reduced visibility/bragging rights is difficult to understand. If someone wants to brag, they can still make arguments like"we contribute more than mandatory requirements, do not need regulations to force us to spend as we like to contribute" or "contribution was made mandatory taking into account our CSR spending" if someone really wants to be overboard….

Capital market does not punish because of CSR, they punish due to lack of revenue/profit growth…as also happens during wars, interest rate hikes, tariffs etc…if at all CSR spending makes a dent P&L, then ways to increase revenue/profits should be explored, knowing apriori that this expenditure is certain and mandatory

So yes, CSR is certainly a wonderful initiative and should continue going forward