Sharp slowdown in bank lending

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

India’s credit-deposit gap may now be a thing of the past

Why does everyone have a hard-on for quick commerce?

India’s credit-deposit gap may now be a thing of the past

Do you remember the RBI Chief sounded the alarm about loans growing faster than deposits in a recent meeting? It had everyone—economists, analysts, and the media—talking. It’s risky for the financial system to be in this situation. To figure out why, let’s rewind and see how we got here.

When COVID hit, everyone went into panic mode. People stopped spending—understandably so. But for a country like India, where 60% of our GDP comes from people buying stuff, this was a big deal. It slowed the economy down, fast.

So what do economic textbooks suggest in such situations? Lower interest rates. When borrowing money becomes cheaper, people are more tempted to take loans and spend more. That is what the RBI did. And guess what? It worked! The economy started showing signs of recovery, helped partially by this and partially by other government measures.

But then came inflation worries. Why? Well, with loans being cheaper and people spending again, coupled with global supply chain issues, inflation seemed inevitable. And sure enough, it happened.

Now, the economics playbook says, "Alright, time to raise interest rates!" The idea is simple: make borrowing more expensive so people think twice before taking loans. But the real world didn’t exactly follow the textbook this time.

From May 2022 to February 2023, something unexpected happened—as interest rates went up, people started borrowing more, not less. Sounds bizarre, right?

Loan growth hit levels we hadn’t seen in a long time, but deposit growth? It stayed pretty average. This created a gap between the two.

Here’s the breakdown of the math behind it: by the end of 2022, for every ₹100 banks collected as deposits, they lent out ₹130. That’s not sustainable. If deposits don’t keep pace with loans, banks face liquidity issues, and the entire system becomes riskier.

Why was this a big deal?

This divide between loans and deposits wasn’t just a minor issue—it was a big warning sign. When banks lend out much more than they hold in deposits, the financial system becomes unstable. Imagine if too many loans went unpaid or a lot of people suddenly wanted to withdraw their savings—banks could fall into serious trouble.

Still, the situation wasn’t as scary as it might sound. The total deposits in the banking system were still significantly higher than the total loans outstanding. The problem was more about the growth rates—deposit growth was lagging behind loan growth temporarily. But the RBI wasn’t about to take any chances. They wanted to stay ahead of the curve and prevent things from potentially spiraling out of control if the situation worsened.

With interest rates already at their peak, the RBI had to think outside the box to tackle the issue. And that’s exactly what they did.

So, what did they do? They pulled out some tricks from their playbook:

A Gentle Push: The RBI gave banks a friendly nudge—what they call "moral suasion"—to focus on growing their deposits. Essentially, they told banks, “Hey, maybe work a little harder to get people to park their money with you.”

Making Loans Pricier for Banks: They increased the risk weightings for certain loans, like consumer loans and those given to NBFCs. That made these types of loans more expensive for banks to give out because they now had to keep aside more assets for them.

New Safety Rules: The RBI also introduced stricter Liquidity Coverage Ratio (LCR) norms that required banks to keep more liquid assets on hand to cover any sudden cash crunches.

Reining in Risky Lending: They flagged retail unsecured loans, gold loans, and microfinance lending as areas of concern, urging banks to be extra cautious.

We too have spoken at length about how RBI has been so cautious about gold loans, unsecured consumer lending, and microfinance lending. You can check out our previous episodes for added context.

Together, these steps contributed to slowing down credit growth.

Fast forward to today, and it looks like the RBI’s strategy is working. Credit growth has started to cool off—it’s now below the deposit growth. The gap that was as wide as 8% last year has now disappeared.

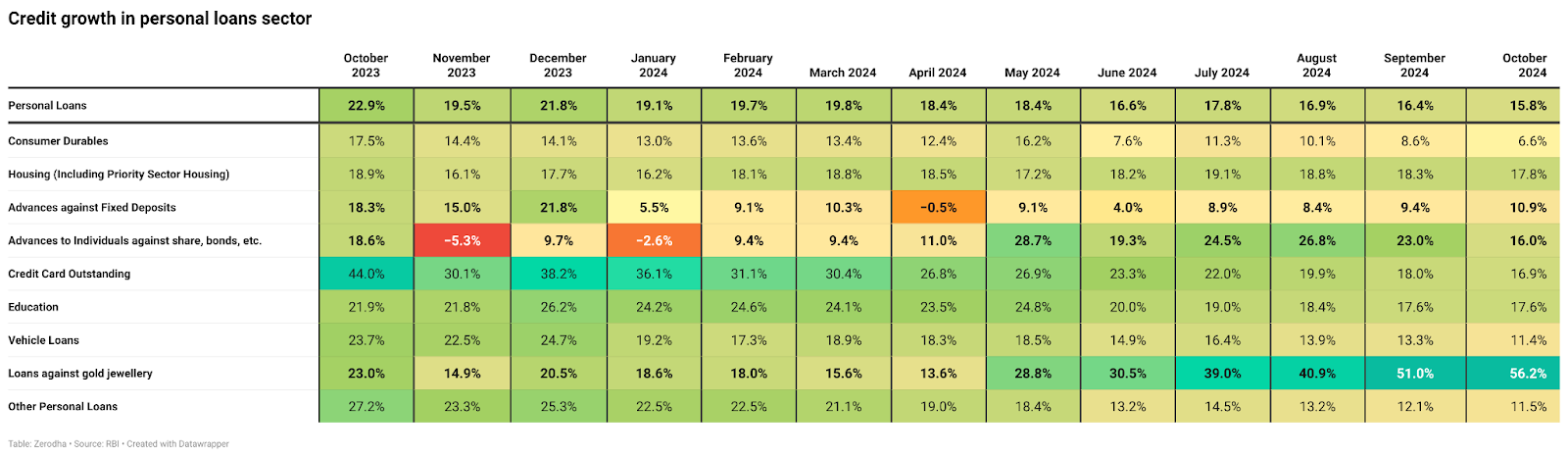

Interestingly, this slowdown is largely because personal loan growth across banks has taken a big hit. These growth rates have on average halved from what we saw a couple of years ago. Let’s break this down:

Consumer Durables: This segment is getting hammered, bad news for fintechs and NBFCs that were handing out Buy Now, Pay Later (BNPL) loans for items like refrigerators, air conditioners, and other home appliances. With demand cooling off, these lenders are feeling the squeeze.

Credit Cards: The story here isn’t any better. Rejection rates for new credit card applications are climbing, and even those who get approved are seeing lower credit limits. Why? Because some big players, like SBI Cards, have been hit with rising NPAs (non-performing assets). This has made issuers much more cautious about extending credit.

Other Personal Loans: Many of these loans fall into the unsecured category, meaning there’s no collateral backing them. With NPAs on the rise here too, lenders are pulling back, leaving this segment declining as well.

Interestingly, amidst all this, housing loans have stayed steady. This suggests that people are shifting their borrowing priorities, focusing on purchases like homes rather than discretionary expenses like consumer goods or leisure. It’s a clear signal that caution has taken over in the lending and borrowing space.

Was this a long-overdue adjustment?

According to the SBI Capital report, this rebalancing was coming for a long time. The credit-to-deposit (CD) ratio had been too high for too long, putting pressure on the banking system.

Historically, there have been episodes of credit and deposit growth divergence persisting for 2 to 4 years. As of November’24, we were in the 31st month of credit and deposit divergence as per a RBI study. Analyzing the past data, the end of the divergence cycle was estimated to be June’25 – October’25. But the cycle ending sooner was not anticipated and that has caught everyone by surprise.

So, where does this leave us? If this current trend continues, we’re likely to see deposit growth fully outpace loan growth in the near future. This would mean a healthier balance for banks and a more stable financial system overall.

But what that would also mean is that interest rates, which had been kept elevated by the RBI for this very purpose, would not have to remain as high. Should this convergence be sustained, a rate cut by the RBI will definitely be on the cards.

Why does everyone have a hard-on for quick commerce?

Quick commerce started as a last-minute ordering app but now seems to look more like a mall. Not only will you get chai, biscuit, tamatar, and free dhaniya there but also a kurta, trimmer, sportswear, and whatnot. The list is endless.

Take a look at how Swiggy in its earnings report literally says you can get everything from A to Z under 10 minutes. It wouldn’t be surprising if these players are taking away business from established companies like Amazon.

Just think about this: Almost 10 years back online quick commerce was basically non-existent. When 10 minute delivery was first introduced in the market, people had one question: ehh, who the hell needs this?

Now, it’s hard for most of us to imagine our lives without it.

Quick commerce is moving at a speed that feels faster than the deliveries themselves. Every day, there’s a new headline. One day, a company is piloting the delivery of medicines in under 15 minutes. The next, another is expanding food delivery to 400 cities in 10 minutes. It’s not just about groceries anymore; it’s about assortment, price, and innovation.

Take Swiggy, for example. They’ve made some massive moves. Recently, they introduced Bolt, their 10-minute food delivery service, which already operates in over 400 cities and contributes to 5% of their total food delivery orders. That’s roughly 85,000 to 90,000 orders daily, delivered in just 10 minutes.

“We believe that speed is a distinctive advantage. When you cut the delivery time from 30-40 minutes to 10, it unlocks human emotions and use cases in disproportionate ways,” said Rohit Kapoor, CEO of Swiggy’s food business.

As Zomato scrapped its 10-minute delivery experiment last year by saying, “it didn’t look like it would turn profitable,” Zepto has quietly begun piloting its own version of ultra-fast food delivery in select cities.

This raises the question: Is the whole larger narrative about people wanting healthier food really the case? How fresh can the food really be if it’s delivered in 10 minutes?

We don't know. Can this 10-minute food delivery become the next big game changer like QC—we will have to see how it evolves.

Coming to quick commerce, it’s not just about speed anymore. Swiggy’s Instamart, for instance, is expanding its focus to offer a wider variety of products and is scaling up its dark stores to handle more inventory. This could mean slightly longer delivery times for some orders, as larger warehouses with more SKUs can make picking and packing more time-intensive. With megapods stocking up to 50,000 items, ensuring every order is ready and delivered within minutes becomes a logistical challenge.

But Swiggy seems to have anticipated this and is already doing something clever to address it.

They’re splitting their delivery approach into two categories: 10-minute and 30-minute deliveries. The idea is simple but effective. For essentials and frequently ordered items, Swiggy uses smaller dark stores or “pods” strategically placed closer to customer clusters, ensuring ultra-fast 10-minute deliveries. Meanwhile, larger orders or less urgent items are fulfilled from larger warehouses, giving the system more flexibility to handle the growing number of products without compromising efficiency.

Zepto, on the other hand, has been steadily increasing its footprint, operating over 350 dark stores across 10 cities and aims to double that by March 2025. They’re not just scaling up but also diversifying—Zepto recently started piloting the delivery of medicines, joining the likes of Blinkit and Flipkart’s "Minutes." Swiggy, too, has entered this space recently.

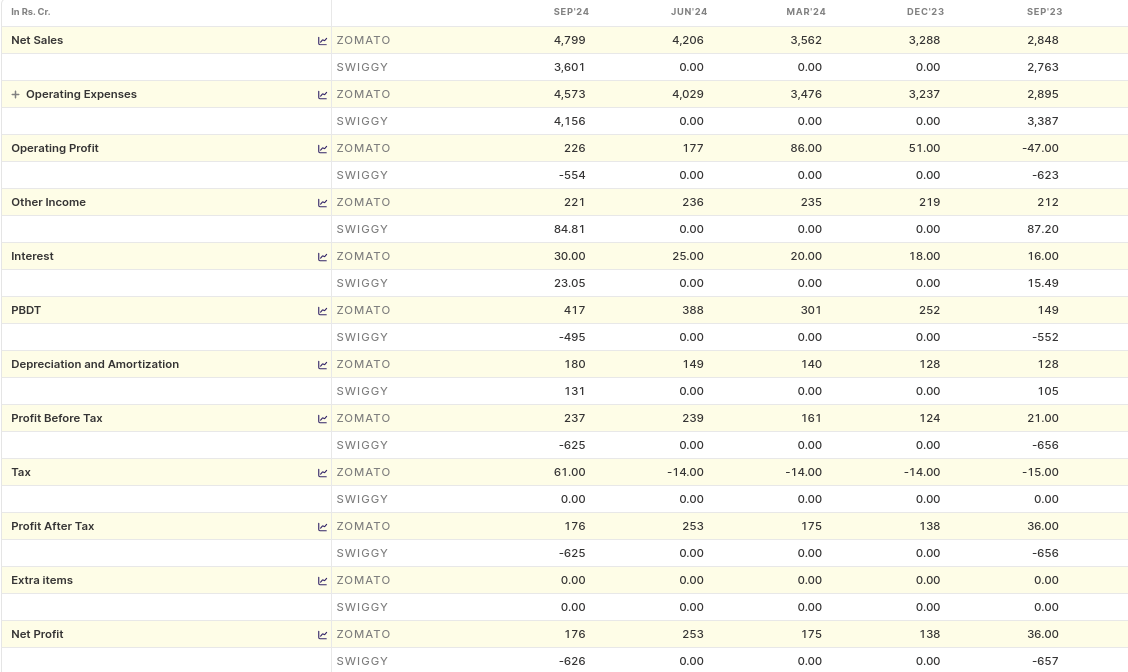

Swiggy posted its first-ever quarterly earnings post IPO and it reported consolidated revenues of ₹3,601 crore in the second quarter of FY24, up 30% year-on-year. However, its net loss narrowed only marginally to ₹626 crore, largely due to heavy investments in its quick commerce segment.

If we compare, Zomato reported ₹4,799 crore in revenues, up 69% YoY, and managed to post a net profit of ₹176 crore. Zepto, meanwhile, reported a gross order value of over ₹5,500 crore with an average order value (AOV) of ₹515 and an estimated take rate of around 23%, currently leading the pack.

The scale of competition is intense. As of September 2024, Swiggy has 609 dark stores with plans to double this number by March next year. Blinkit leads with 791 dark stores and aims to cross 1,000 by the same timeline. Zepto’s ambitions are equally aggressive, intending to grow from its current 350 stores to over 700 in the next year.

The race is not just about volume but also about efficiency and innovation.

And then there’s the broader narrative. Platforms like Myntra have entered the quick commerce game with "M-Now," promising 30-minute deliveries of fashion and lifestyle products. Amazon is gearing up to launch its quick commerce service, codenamed "Tez," by the end of this year. Meanwhile, Flipkart’s "Minutes" is gaining traction in the grocery arena and is also entering the pharmacy segment

Yet, amid all this innovation, there are challenges.

A recent JPMorgan survey found that 59% of Kirana stores in Mumbai are struggling to compete with quick commerce platforms due to their inability to match discounts, even though Aadit Palicha, CEO of Zepto, mentioned that they are not killing Kiranas.

The regulatory environment is also evolving.

The Competition Commission of India (CCI) might decide not to act on allegations of predatory pricing against quick commerce players, citing a lack of market dominance. Meanwhile, Finance Minister Nirmala Sitharaman lauded the potential of Indian quick commerce startups, calling them global trailblazers and urging policymakers to ensure fair competition while supporting traditional retail.

The overall question that I have isn't whether it will survive but how this space will continue to evolve.

Tidbits

India's services PMI dipped slightly to 58.4 in November, marking 41 months of expansion. While hiring hit a 19-year high, input costs surged, and selling prices rose sharply, reflecting inflationary pressures amid robust domestic and international demand.

Vodafone Group will sell its remaining 3% stake in Indus Towers for ₹2,800 crore to repay debt. This move, part of its global restructuring, cements Bharti Airtel's dominance in the tower company while highlighting Vodafone Idea's financial struggles.

Saudi Arabia faces mounting challenges to its oil dominance as OPEC+ members push for higher production, and U.S. shale competition grows. With $1 trillion in infrastructure projects needing high oil prices, Riyadh faces a dilemma: defend prices or retain market share, potentially reshaping global energy dynamics.

India's banking liquidity surplus reached ₹1 trillion, boosted by government spending. However, upcoming tax outflows and forex interventions are likely to tighten liquidity, potentially raising borrowing costs in the short term.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉 Join the discussion on today’s edition here.