SBI fights the court on what a telecom loan means

When the government plays both regulator and creditor for a key sector.

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

SBI fights the Supreme Court on what a telecom loan means

India's impending solar squeeze

SBI fights the Supreme Court on what a telecom loan means

In 2018, Aircel filed for bankruptcy, and two years later, its resolution plan was approved. It is now April 2026, and the banks that lent it ₹13,000+ crore are still waiting to see any of it back. One of those banks was SBI, who led the consortium.

Last month, SBI went to the Supreme Court asking it to reconsider a judgment delivered in February. In essence, the court told the banks that the collateral they thought backed their telecom loans was never really theirs to claim. And that collateral is spectrum — the radio frequency bands over which mobile data signals are transmitted. In other words, the very foundation of any telecom network.

This sounds like a narrow legal dispute over a single failed telco. But dig deeper, and it’s a question that reshapes how banks in India lend to any business built on a government-granted right. That would encompass telecom, mining, airports, highways, ports, oil and gas — almost every large piece of infrastructure.

To discuss what happened, let’s set some context.

Aircel was a mid-sized mobile operator that competed with Airtel, Idea, and the rest through the 2010s. Like every telecom company, its single most valuable asset wasn’t its towers or its fibre, but its spectrum.

The government sells time-limited rights to use the spectrum through auctions. Aircel paid ~₹6,000 crore across auctions between 2010 and 2016 to acquire these rights for twenty years each. That was the collateral behind the loans that SBI and its fellow lenders gave them in 2014.

When Aircel eventually ran out of money and the Department of Telecommunications (DoT) came asking for ~₹10,000 crore in unpaid licence fees, it filed for voluntary bankruptcy. It entered what’s called the Corporate Insolvency Resolution Process, or CIRP. It is a structured last-chance sale governed by India’s main bankruptcy law, the Insolvency and Bankruptcy Code (IBC). In a CIRP, an independent professional takes over the company, existing management is pushed out, and prospective buyers submit plans to acquire the business and pay creditors back — often a fraction of what they’re owed.

In June 2020, the National Company Law Tribunal (NCLT) approved a plan submitted by UV Asset Reconstruction Company (UVARC). Against the total financial debt of roughly ~₹59,000 crore, UVARC agreed to pay just ₹19,600 crore — a haircut of nearly two-thirds for lenders. Critically, the entire plan assumed that spectrum rights could be transferred to the new owner and eventually monetised.

Six years later, in February 2026, the Supreme Court said they couldn’t be.

The February ruling did two things at once. First, it said spectrum should never have been part of the bankruptcy estate in the first place. Second, it said the money Aircel owed the DoT didn’t belong in the IBC’s ordinary queue of debts either. Both findings were bad news for the Aircel resolution plan, and both have now been challenged. They’re two separate fights, each worth understanding on its own.

What did banks actually lend against?

Let’s start with the spectrum tussle.

The court’s reasoning on spectrum rested on something almost philosophical. Spectrum, it said, is a scarce natural resource. The Union government holds it as a “public trustee“ for the people of India under Article 39(b) of the Constitution, which directs the state to ensure natural resources serve the common good.

Telecom companies don’t own spectrum. They only hold a “conditional, revocable privilege“ to use it. And because spectrum is public property, it cannot be pulled into an IBC proceeding as though it were a regular corporate asset, no matter what a company’s balance sheet happens to say.

SBI’s review petition argues this confuses two different things: who owns a natural resource, and who owns the right to use it.

Yes, the spectrum belongs to the Union. But the rights Aircel bought at those auctions are distinct. The company carried them on its books as an intangible asset. It paid for them through hard-fought bidding, and it also used them to raise debt from banks.

A useful analogy is leasehold property. When the government leases you land for 99 years, you don’t own the land. But nobody disputes that your leasehold is valuable, that you can buy or sell or mortgage it. Banks lend against leasehold property every day.

The stronger evidence on SBI’s side is that the government itself already treats these rights as transferable. India has a formal spectrum trading framework that lets operators sell the right to use spectrum to another operator, subject to DoT approval.

For instance, through this channel, in 2016, Airtel had acquired spectrum from Aircel itself. In the ordinary course of business, the state treats spectrum rights as bankable, tradeable, commercial property. But the February ruling draws a hard line around bankruptcy. Once a company declares it, the same right becomes a sovereign permission that cannot be transferred through the IBC at all.

Where does the government stand in the queue?

Now, let’s come to the second fight around the queue of debts.

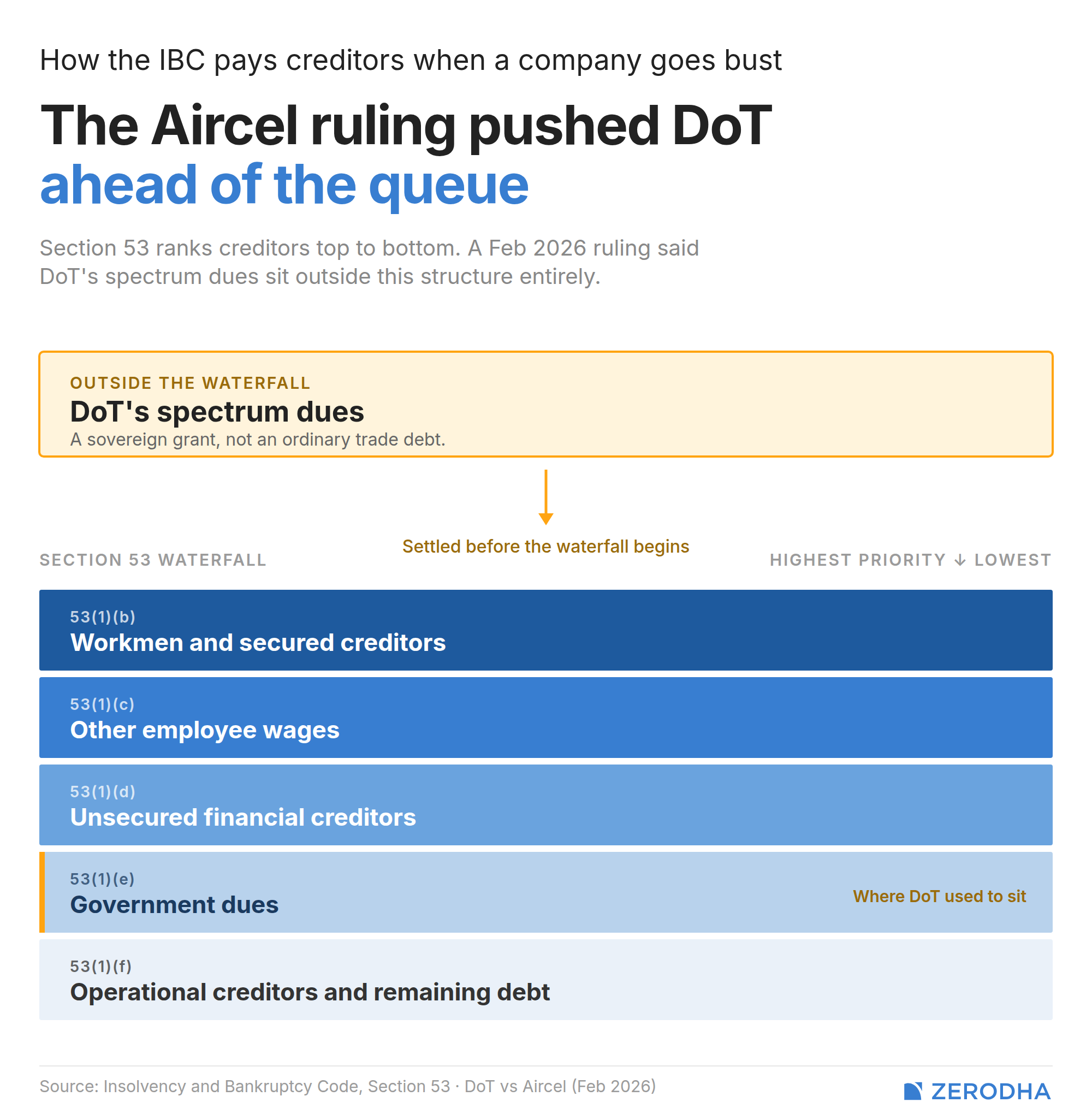

The IBC organises creditors into two broad categories. “Financial creditors“ are banks and bondholders who lend money. “Operational creditors“ are the ordinary counterparties of a business who haven’t yet been paid — like employees, suppliers, and vendors. Under the IBC’s order of priority, financial creditors sit ahead of operational creditors when the money from a resolution is distributed. That hierarchy is what gives bank lending its comfort. A secured loan in India is priced on the assumption that, if the borrower fails, the bank is near the front of the queue.

Now, the February ruling held that the money Aircel owed to DoT wasn’t operational debt at all. These weren’t payments for goods or services in an ordinary commercial relationship, but arose from the sovereign grant of a privilege. Basically, the court declared that the DoT’s dues don’t fit the IBC’s existing categories. This also possibly meant that the DoT’s claim had to be settled before the IBC’s waterfall even began.

In telecom bankruptcies, DoT is typically the single largest creditor in the room. The court itself noted that failed telcos collectively owe the government around ~₹39,000 crore. If every rupee of that has to be paid first, before banks touch anything, most telecom resolutions stop making arithmetic sense for the long line that’s waiting for their turn.

SBI’s counter here is procedural rather than philosophical. DoT actively participated in the Aircel CIRP process for six years. It filed its claim and voted at meetings of the Committee of Creditors. It never once objected to being classified as an operational creditor. It played the game by the IBC’s rules, all the way through. So, SBI argues, changing those rules now means tearing up a resolution that has already been approved by creditors, sanctioned by the tribunal, and waited on by lenders for six years.

The court went even further with its judgement. It found the timing of Aircel’s filing of voluntary bankruptcy suspicious. It only came after the DoT came asking for money. So, it directed that documents from bankrupt firms like Aircel, Reliance Communications (RCOM), and so on be placed on record, so it could examine whether these IBC filings were honest resolution attempts, or strategic manoeuvres to escape government dues altogether.

That’s a judicial eyebrow raised at the entire telecom sector, suggesting the IBC has been used less as a rescue mechanism and more as a shield.

Underneath both fights sits a deeper problem the IBC was never built for. The law assumes a company’s assets can be transferred relatively freely to a new owner, and that creditors stand outside the business. But in sectors built on government-granted rights, neither assumption holds, since the regulator is also the creditor. The most valuable asset, therefore, is also a permission the regulator can withhold.

What happens if the ruling stands

So, if the court wins, how do the dominoes fall?

The first casualty is the resolutions themselves. Aircel’s UVARC plan and RCOM’s ₹23,000 crore plan were both built on the assumption that spectrum was part of the estate, but it no longer is. UVARC and the RCOM resolution applicants have to decide whether their bids still make economic sense without the spectrum assets. Some of these resolutions may simply collapse, sending the companies into liquidation with nothing but scrap-value assets left to distribute.

The second is the cost of lending to any sector built on government-granted rights. Think mining leases, airport concessions, highway BOT contracts, port concessions, oil and gas exploration blocks, power purchase agreements. If those rights can’t be reliably claimed in insolvency, banks will demand higher interest rates, stricter conditions, or substantially more cash collateral up front. And infrastructure is already a sector that relies extremely heavily on banking channels for capital.

Third: there’s a tension inside the government itself that this ruling brings into the open. DoT wants its dues, but the Finance Ministry wants public sector banks to remain solvent — the same banks that lent most of Aircel and RCOM’s money. The broader state wants 5G rollouts, rural connectivity, private telecom investment, and a functioning infrastructure financing market. These goals are now actively pulling against each other.

The review petition isn’t really about SBI, Aircel, or RCOM. It’s about what a promise means when the state is the one making it. When the government auctions spectrum, licences a mine, or awards a highway concession, what exactly has it handed over? Is it a right, with economic substance, that the company can own, borrow against, and trade? Or is it a permission, revocable in spirit if not in letter, that vanishes the moment the business holding it runs into trouble?

Banks priced twenty years of loans on one answer, while the court has offered another. On that front, while this review looks routine, its implications across the board — from property rights, to how infrastructure loans are priced, to the government’s role — couldn’t have higher stakes.

India’s impending solar squeeze

From this June, any solar project that wants to stay on the right side of India’s energy policy must use cells made in India. Not assembled in India from imported parts — that’s already required — but actually fabricated here.

The problem is that India doesn’t yet have enough of them.

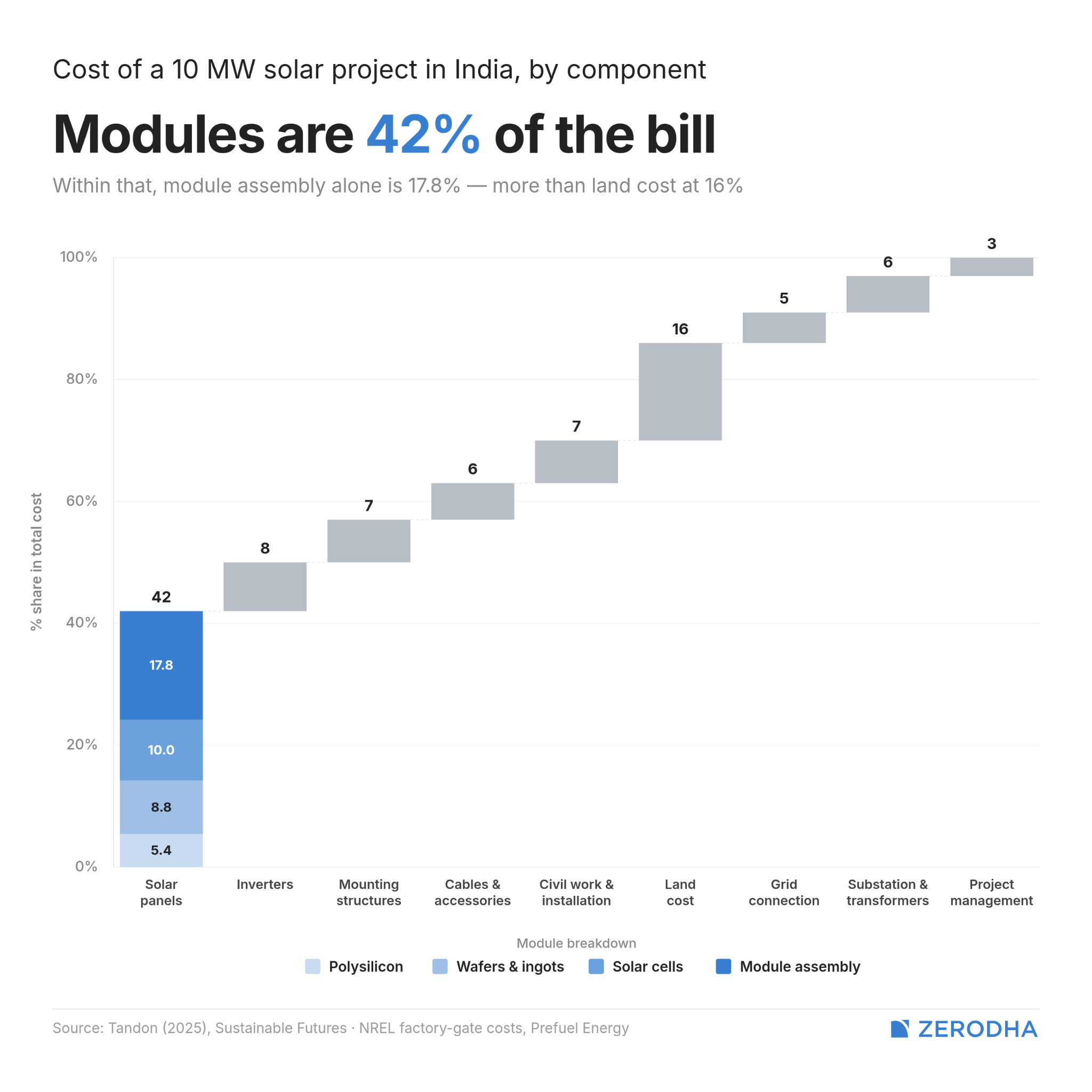

As of mid-2025, India had roughly 27-29 GW of domestic solar cell manufacturing capacity in theory. But what manufacturers can actually produce and ship reliably was estimated at somewhere between 11-13 GW. India needs to be installing solar at ~29 GW per year between now and 2030 to reach its stated target of 280 GW, and we have currently installed ~143.6 GW. Last year, it added 23.83 GW, a record pace, yet still short of what the next five years demand.

This latest mandate is the latest chapter in a much longer story. For fifteen years, India has been wrestling with the same fundamental dilemma. On one hand, we want our own solar industrial base that is not dependent on imports. But on the other hand, import restrictions could make solar projects more unaffordable. In fact, many industry stakeholders are worried that the new rules could create a shortage of solar cells and derail solar projects.

The country has answered this question in different ways at different points in time for different sectors. Today, we’ll be looking at India’s local sourcing rules for solar, and the matrix of who advocates for it (and who doesn’t), and why.

The architecture of protection

India’s policy for localizing solar supply chains has evolved for over 15 years. And understanding that is key to making sense of the situation today.

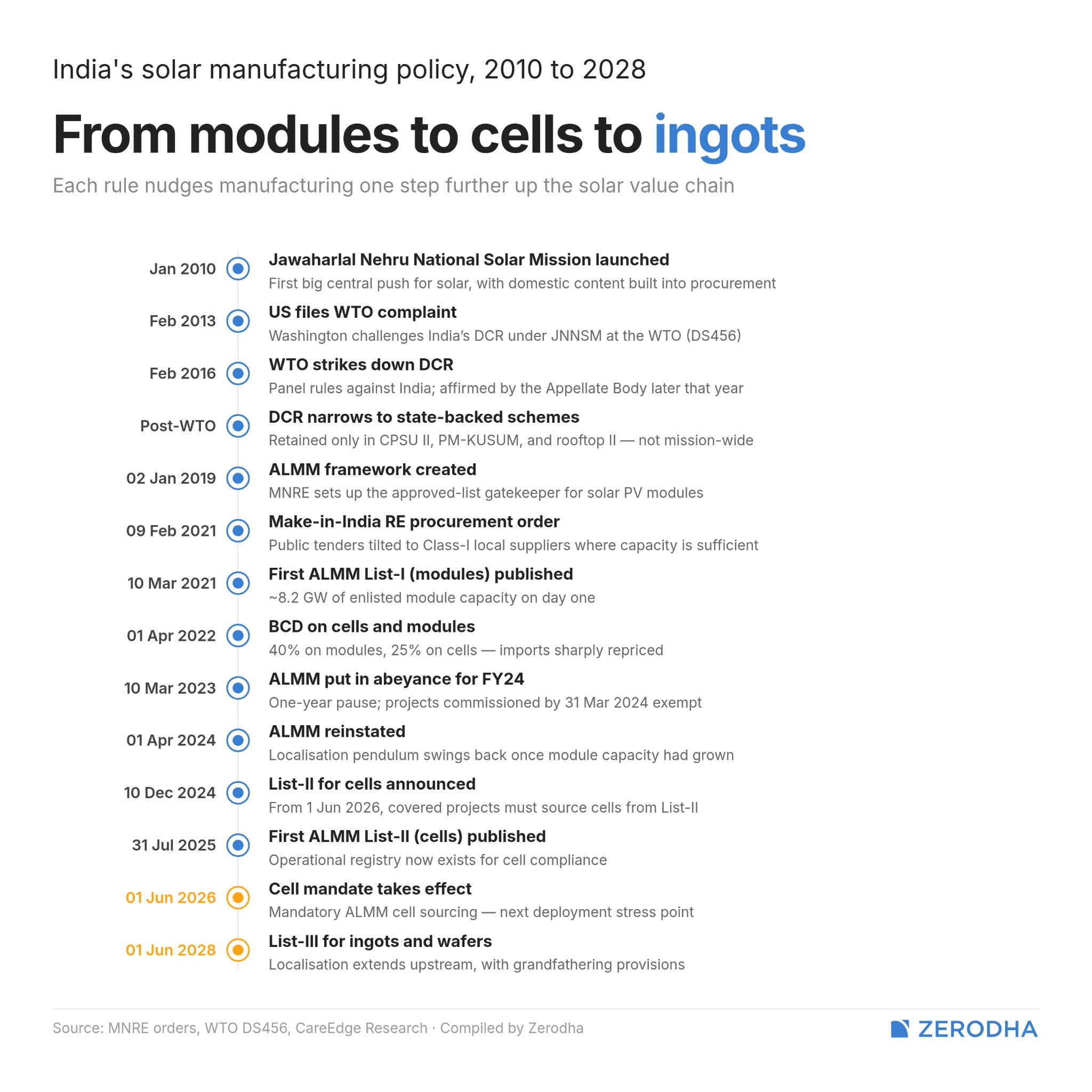

In 2010, we launched the Jawaharlal Nehru National Solar Mission (JNNSM), with an aim to become a global leader in solar power capacity. Under the mission, a domestic content requirement (DCR) was introduced. The idea was that if India was about to build a lot of solar capacity, it should use that demand to anchor a domestic manufacturing base also. Certain projects would be required to use Indian-made cells and modules.

However, the WTO disagreed with our local content rules. In 2013, the US filed a formal complaint arguing that India’s DCR measures discriminated against imported cells and modules. By the time the Appellate Body ruled, India had lost cleanly. The broad, mission-wide content requirement was found inconsistent with India’s obligations to free trade.

But rather than abandoning localisation, India redesigned it. The DCR was narrowed and tied to government-backed schemes, including public-sector enterprise tenders, an agricultural solar scheme, and a grid-connected rooftop programme. This was more acceptable rather than a more blanket requirement applied across the entire private market.

The most architecturally significant instrument, though, is the Approved List of Models and Manufacturers (ALMM), launched in 2019. This is a government registry of domestic solar products that project developers must source from in order to comply with the rules. It consists of two lists: List-I covers solar modules, and List-II covers the solar cells that modules are made up of. List-I has been operational since 2021, while List-II takes effect this June.

And in a sign that the government’s ambition runs considerably further, an ALMM List-III is in the works. It goes even more granular into the solar supply chain, covering ingots and wafers, and is scheduled for June 2028.

Now, most of these were non-tariff barriers. After all, tariffs weren’t exactly a WTO-compliant measure. However, in 2022, India imposed a basic customs duty (BCD) of 40% on imported solar modules and 25% on imported cells. The push towards indigenisation couldn’t be more explicit.

Voting with wallets

But each time India tightened its local sourcing rules, the industry (or a part of it, at least) found efficient ways to express its displeasure.

After the original DCR baskets were introduced under JNNSM, project developers reported that domestic cell prices jumped 15-16% after bids had already been awarded, making the committed project economics unviable. Some threatened not to sign power purchase agreements at all. By 2017, DCR tenders had all but disappeared from the market. Developers simply preferred to build projects without the constraint, even if that meant working around the policy entirely.

The introduction of the customs duty in 2022 forced developers to hoard modules before the policy kicked into effect. In the first quarter of that year alone, developers imported approximately 9.7 GW of solar modules — a 210% jump from the same quarter a year earlier. Once the duty took effect, module costs rose by ~40%.

Meanwhile, those who couldn’t stockpile looked for other exits. Some of them may not have been legitimate — for instance, in 2024, several solar companies were investigated for ₹1,900 crore in customs duty evasion. Additionally, under the law, power project developers could use a preferential 5% import duty scheme for their projects, which would have been much lower than the BCD. However, the government anticipated that escape route and quietly revoked the clause.

In September 2022, a ministerial review meeting was convened with solar industry executives. The minutes are unusually candid. Industry participants said the combined impact of ALMM enforcement and BCD had slowed installations, and a domestic supply-demand mismatch was creating bottlenecks. Moreover, they also alleged that some manufacturers were exploiting their newfound protection through price manipulation.

The government’s response was revealing. In March 2023, the ministry postponed the ALMM from coming into effect for an entire financial year. It was an admission that domestic supply had not kept pace with policy ambition, and that forcing compliance in those conditions would have caused real damage to the installation pipeline.

However, on the other side of the argument lay the manufacturers, who opposed the project developers. After all, the ALMM list acted as protection for domestic manufacturers, ensuring steady demand for their products from project developers. With imports priced out or gated, domestic products commanded higher margins.

A study covering India’s auction experience from 2014 to 2017 found that DCR had raised the cost of solar power by ~6% per unit generated. Indian panels were ~14% more expensive than international alternatives during that period. Crucially, the same study found limited evidence that Indian manufacturers had broken into export markets in a significant way. So while the protection existed, it wasn’t all that effective for local project developers.

In late 2024, CRISIL estimated that domestically manufactured cells were still 1.5 to 2 times more expensive than Chinese alternatives, even after accounting for the hefty customs duty. If the June cell mandate takes full effect without relief, CRISIL calculates that project capital costs could rise by ₹5-10 million per megawatt, with tariffs going up by ₹0.40-0.50 per unit. For developers who locked in bids before this policy was announced, that’s a structural problem with no easy fix.

Protected, but not yet competitive

The case for absorbing these costs rests on a familiar industrial-policy argument: short-term pain in exchange for long-term supply-chain sovereignty. If local-sourcing rules force capital into Indian manufacturing, and if Indian manufacturers eventually achieve the scale to compete on price, the higher costs now are really investments in future resilience.

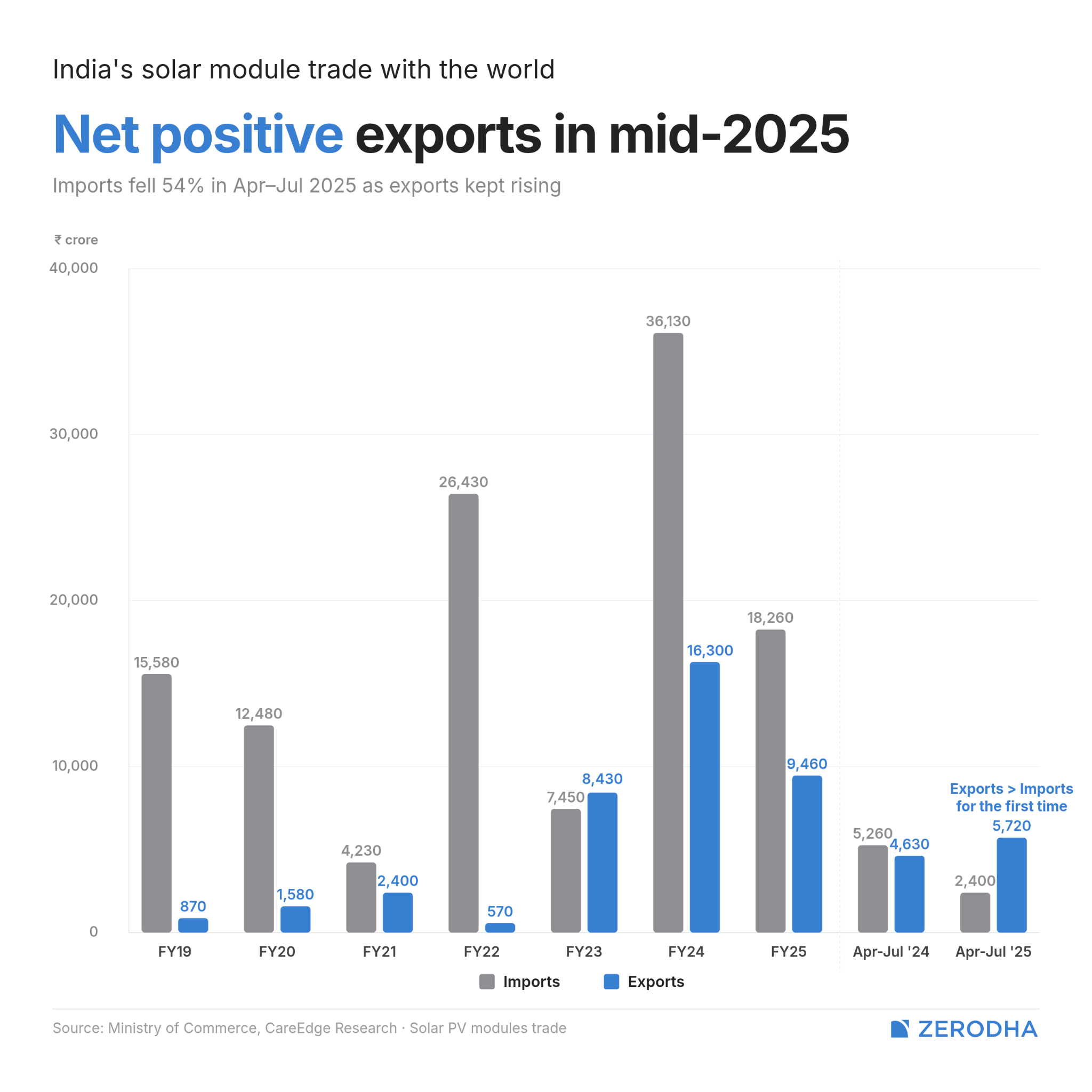

Now, India’s module manufacturing capacity genuinely did scale under protection — from roughly 11 GW in 2019 to somewhere between 60 and 120 GW by mid-2025, depending on which estimate you use and what it is measuring. Module imports as a share of India’s consumption fell from ~45% to around 25% between 2020 and 2024. That is real, measurable industrial development.

But those gains are concentrated almost entirely in module assembly, where you take solar cells and assemble them into panels. They’re not a technically demanding step in the solar value chain. Moving further upstream requires progressively more capital, more sophisticated technology, and considerably more patience.

India’s export performance tells this story more honestly than the headline capacity numbers do. Solar equipment exports have picked up, mostly in modules, and mostly to the United States, which made up a whopping 97% of India’s solar exports. But the US isn’t buying Indian because Indian products are higher quality. Washington has erected its own barriers against Chinese solar equipment through anti-dumping duties. In that case, India is mostly a beneficiary of American geopolitical anxiety rather than global competitiveness.

And, as we’ve covered before, China’s grip on the upstream remains overwhelming. Three-quarters of India’s solar imports by value still come from China. Even as late as 2024, CRISIL estimated that cell imports as a share of India’s total consumption were still running around 80%, nearly all from China.

This is the bind the June 2026 cell mandate is trying to break. But whether that logic holds depends on how much effective cell capacity actually exists when the mandate kicks in. It’s has already established that effective operational output can be far below headline capacity. And developers have flagged the limited domestic availability of high-tech TOPCon cells, which provide more efficient generation that large-scale utility projects increasingly require.

The further upstream you go, from cells to ingots, the story gets thinner. India’s first commercial ingot-wafer facility — a 2 GW plant — only came online in FY25. The government has already announced ALMM List-III for ingots and wafers. But it’s quite likely that the same supply-demand tension the country is navigating right now for cells will almost certainly replay two years from now for one step further up the chain.

Conclusion

India is not going to abandon its solar industrial policy. The direction has been set — localise further, move upstream, and reduce dependence on China.

But the prime complaint of industry stakeholders is that they’re never left with enough of a buffer to adjust to the policy changes. The June cell mandate arrives at a moment when the gap between what the policy demands and what Indian manufacturing can reliably supply is still uncomfortably wide.

Meanwhile, India is simultaneously trying to accelerate solar installations faster than it has ever managed before. A supply squeeze that slows commissioning even by a year directly undermines our highly-ambitious clean-energy targets. Building the wall and building the road at the same time is hard, and India has to figure out how to do both.

- This edition of the newsletter was written by Kashish and Manie.

Tidbits

The Reliance group’s Jio Financial Services and Munich-based insurance major Allianz group have signed a binding agreement to establish a 50:50 joint venture spanning general and health insurance, formalising a partnership first announced in July 2025.

Source: Business StandardThe Indian government has authorized blending ethanol and synthetic hydrocarbons with Aviation Turbine Fuel (ATF) to boost Sustainable Aviation Fuel (SAF) production and reduce reliance on oil imports amidst Middle East conflict-related disruptions. This move broadens the definition of jet fuel to include biofuels, aiming for 1% SAF blending for international flights by 2027.

Source: LiveMintIndia is set to import a record 2.5 million metric tons of urea in a single tender, at nearly double the price paid two months ago, as the Iran conflict disrupts global supplies. The record purchases, covering about a quarter of India’s annual imports, are set to tighten global supply and push prices higher, which have already surged due to the war in the Middle East.

Source: Reuters

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

How can Indian IT flip the AI script ft. Ameya P

The age of AI agents has, so far, been a thorn on Indian IT’s side, at least as far as valuations are concerned. Its business model is getting stale each passing day - that’s understood. There might be a possibility that Indian IT might just adapt to the new paradigm. But what does adaptation for Indian IT look like? What are the forms of inertia they will have to overcome to successfully change themselves? And even if they do adapt, will they be able to defend their new business?

To unpack all this, we spoke to Ameya P, a veteran in the global IT industry, and a prolific technology investor well-known for his investing takes on X. It’s an incredibly nuanced conversation from an expert who understands the nitty-gritties of what each AI development brings forth for this industry.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

The structural problem isn't the bankruptcy — it's the dual role. When the state auctions the right, writes the regulation, and holds the largest receivable, the creditor waterfall can't clear. Every airport, mine, and spectrum block in India is now priced against that same unsettled boundary between a licence and an asset.

Very interesting and well articulated!