Reliance's soft drink shake-up

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Reliance’s gladiator push in India’s soft drinks’ market

Carbon Pricing is going mainstream

Reliance’s gladiator push in India’s soft drinks’ market

Summers in India are hot in more than just one way.

Every year, in April-June, various companies battle each other to put their soft drinks in your refrigerator. They prepare to mount aggressive marketing campaigns, ramp up their production capacity, and court retailers and kirana stores with incentives to stock their product. From Coke to Rooh-Afza to energy drinks, every summer, India sees an intense, heated battle of the beverages.

Recently, however, a new heavyweight has emerged on this battlefield: Reliance. The Mukesh Ambani-led giant has announced its intention to invest upto ₹8,000 crores on expanding its beverages business. This is their largest investment outlay in the FMCG sector to-date.

Reliance has been making waves in soft drinks for the last couple of years. It famously mounted an audacious challenge to the duopoly of Coke and Pepsi, by reviving the Campa-Cola brand. That is the flagship of Reliance’s push. Much of its ₹8,000 crore investment will be devoted to Campa-Cola’s expansion. But it is only the most notable of a series of drinks Reliance is bringing to the market.

So why is Reliance investing in such a crowded industry? What are the tides that favor them in this battle? How are its competitors reacting to this offensive?

These are the questions that are bubbling in our minds.

From the past to the present

India's story with soft drinks has been a rollercoaster ride.

It began from 1956, when Coca-Cola entered India and made a major splash among relatively-richer Indians. But this was an older India, where business was seen with suspicion. Politicians across parties accused it of exploiting its monopoly to siphon excess profits back to the United States.

This suspicion reached a fever pitch in 1977. The Janata Party had just won the Lok Sabha elections, becoming the first non-Congress national government in our history. Back then, our pre-liberalisation economy faced unending shortages of foreign exchange. Multinational corporations became a key target of the politicians of the time. That is why India introduced its “Foreign Exchange Regulation Act”, or FERA.

Under the Act, a foreign entity could own a maximum of 40% in their Indian arm. The rest had to be held locally. To the Coca Cola company, that meant it would have to give away its secret formula to an entity they didn’t control. Rather than face that, they simply decided to leave.

That left a huge gap. The government attempted to fill it with its own drink called “Double Seven”. But the business of consumer beverages isn’t an easy one to master. Operational issues plagued the public venture, and it was shut down in a few years’ time.

However, at the same time, private sector firms were out to quench our ever-growing thirst for cold drinks. India’s only manufacturer of Coca Cola was a family business called Pure Drinks, led by Charanjit Singh. The loss of the Coca Cola business spurred him to create his own brand, which he called Campa Cola. Meanwhile, Parle launched a strong cola with Indian flavours, which you’re probably familiar with — Thums Up.

Then came the reforms of 1991. Economic activity was liberalised. This heralded the re-entry of Coke and Pepsi. They bull-dozed through the market, with aggressive tactics on marketing and building retail networks, which helped them get back on top with more than 80% market share.

Their entry overwhelmed Indian brands. Thums Up — perhaps India’s most successful domestic champion — was bought out by Coca Cola. Other brands — including an already-declining Campa Cola — were pushed to the sidelines.

Fast forward to today. India has a lively soft drinks market which keeps growing. Indian carbonated drinks generated an eye-popping $18 billion in revenue in 2022, and that number has only grown since. In 2023, half of all Indian households consumed bottled soft drinks.

But colas are only part of the picture. India’s consumers have a diverse palette, which diverges across age, income levels, region, and more. Today’s soft drinks industry — filled with everything from flavoured milk, to fruit juices, to sugar-free drinks, to fizzy fruit drinks, to energy drinks — reflects that diversity.

Coke and Pepsi don’t control this entire market. In fact, they have struggled to compete in some of these segments. There are others — like Parle Agro (Frooti, Appy Fizz, Smoodh), Dabur (Real juices), Amul, and even regional niche players such as Lahori Zeera or Bovonto.

In 2022, Reliance threw its hat into this ring. It bought the Campa Cola brand for a measly ₹22 crore. It relaunched the brand with the tagline “Naye India Ka Apna Thanda” — a callback to its roots as a nationalist drinks brand.

And this was only the beginning.

A Bold Bet

Reliance doesn’t just want to capture the cola market, but also other segments in the soft drinks category. Reliance’s consumer products division, at just 3 years old, has become the fastest-growing consumer brands business in India.

They think of India as a massive population which is very price-sensitive. The director of Reliance Consumer Products (and ex-Coke India chairman), T Krishnakumar, said he wants to reach “600 million (60 crore) consumers at the mass end and work closely with neighbourhood stores by giving them margins at today’s cost.”

They’ve already tasted success with Campa Cola, which already exceeded ₹1,000 crores in sales within 18 months of its launch. This is the tip of the spear. But, as we shall soon see, it has plans for other markets besides cola as well.

Reliance is spending its ₹8,000 crore outlay to set up 10 to 12 new production and bottling facilities, which will be operational by March 2027. In the meanwhile, they’re working with 18 facilities that they have set up with strategic partners — as well as some contract manufacturers.

That sorts production out. How do they plan to reach customers? Reliance has focused on three elements to disrupt the market: marketing, distribution and pricing.

The branding game

Each of Reliance’s many drinks is targeted at different population segments.

Take energy drinks. In the last 7 years, energy drinks have practically become commoditised. In 2023, consumption went up by a whopping 30x since 2018, to 570 million liters. PepsiCo’s addictive Sting led this charge, selling at prices 80% lower than Red Bull.

Reliance is trying to breach this market with ‘Spinner’. That name perfectly fits its brand ambassador — legendary Sri Lankan bowler Muttiah Muralitharan. Reliance has also partnered with various IPL teams to drive visibility.

The second category Reliance is aiming at is locally-popular drinks. Local brands such as Lahori Zeera and Bovonto have earned high loyalty among a small consumer base. Coke tried (and failed) to cater to this market with their jeera-based drink RimZim.

To enter this space, Reliance acquired a 50% stake in a 100 year-old drink-maker called Sosyo, which is beloved in Gujarat — with a 29% market share there. Sosyo has its own line of juices and fizzy drinks that Reliance can readily tap and even grow nationally.

A third, and more interesting category is that of rehydration drinks like ORS. While these were long seen as medical drinks, increasingly, these are being sold for regular consumption — while still marketed as being ‘healthy’, because they contain ‘electrolytes’. The market is currently led by ORSL, followed by pharma firms like Cipla. But FMCG firms like Tata Consumer also want a piece of the action. And now, Reliance has jumped into the sector with its new acquisition, Raskik.

They’re backing these drinks with a multi-media advertising push.

Unlike Coke or Pepsi, Reliance enjoys one big advantage — it has its own media ecosystem across channels. It owns stakes in OTT platforms like JioHotstar, as well 72 different TV channels which reach 800 million Indians. Campa Cola is also the co-sponsor of the IPL (along with JioStar) until 2026.

How to reach 600 million Indians

That marketing only works if there’s a way for people to buy their drinks. And so, Reliance aims to reach at least 70% national availability for key beverages like Campa-Cola by March 2026.

The omnipresence of Reliance’s own retail network is a big advantage, here. In FY25, Reliance Retail expanded its store count to over 19,000 stores all over India. It has been opening Smart Bazaars and Fresh stores ferociously. And all those markets can be put to service for moving its drinks.

That being said, most drinks are bought at your neighborhood kirana store. These stores have fridges sponsored by Coke and Pepsi, stocked primarily with their drinks.

Reliance knows this all too well, which is why it has also attempted to disrupt the kirana store channel as well. Its e-commerce app, JioMart, was adding 1.5 lakh small retail merchants every month in FY22 — giving them access to cheaper wholesale. This gives the stores better margins — usually 6-8%, compared to the industry standard of 3.5-5%. In return, Reliance’s products get top visibility on their shelves.

Reliance understands that a majority of India lives in tier-2 and tier-3 towns, and those are the cities it’s targeting. It also partnered with B2B e-commerce startup Udaan to help its drinks penetrate rural markets deeper.

Fighting for your ₹10

The trump card in Reliance’s deck, though, is its cut-throat pricing.

Their drinks are priced much lower than their key rivals. A 200 ml PET bottle of Campa Cola was initially launched at ₹10 — half the price of the 250 ml offerings from Coke and Pepsi. Spinner and Raskik were also launched at a ₹10 price point. This bottle size, it seems, is India’s most preferred consumption point, which is why Reliance decided to play here.

While it's still early days, you can already see the impact of this price war. In its earnings call for Q3 FY25, Reliance mentions that it achieved 10% market share already in some states. Campa’s aggressive pricing is also hurting local players in tier-2 and tier-3 towns, who cannot compete with their thin margins.

Its biggest competitors are on the backfoot. Coca-Cola and PepsiCo had to respond to Campa’s entry by slashing their prices across different bottle sizes. In FY24, Coke’s net profit fell by 30% to 420 crore — a good chunk of which is owed to this price war.

Other Indian brands were also forced to reduce prices — Dabur cut the price of its Real juices, while Tata Gluco+ incentivised retailers with higher margins. This is also forcing competitors to stock up more on smaller-size bottles than in general.

Reliance's financial muscle means they can keep this price war going for a good while, absorbing thin margins while still running sustainably. In fact, Reliance Retail Ventures, which houses its beverage arm, boasted a net profit of ₹3519 crores in the fourth quarter of FY 2025.

Not an easy road ahead

Reliance, in short, is taking big bets. Early signs have been positive, with impressive sales in Campa-Cola’s first-year and increasing market share across segments.

But then, the rise of a challenger is always exciting. Can it actually beat the incumbents, though? Can it really upset the position of Coke and Pepsi? These are brands that, despite increasing competition over the years, have successfully fortified their control over their market. The price war initiated by Reliance has to be sustained, and its biggest competitors have deep pockets too.

In fact, price isn’t the only way these companies are responding. Varun Beverages, the main bottler of Pepsi in India, has announced an increase in capacity by 20%. Last year, Parle Agro increased its ad spend by 18% and is strengthening its distribution network. Coke, Pepsi and Dabur have planned to up their marketing budgets by around 18-25%. These are players with decades of experience in consumer products, something Reliance lacks.

Reliance has some intrinsic disadvantages as well. One is the Campa Cola brand itself. The name connected with people of older generations, but young people today have not had a lot of exposure to it. So, even though they’re reviving an old band, they’ll effectively have to build brand loyalty from scratch.

Campa Cola also lacks differentiation. Their flavour profile remains the same as Coke and Pepsi. And from what we can tell, Reliance has been lacking in pure product innovation — there isn’t a fresh taste they’re introducing to the market. Even niche products like Paper Boat and Lahori Zeera have built brand recall on the back of their innovative flavours.

Its distribution hasn’t been smooth-sailing either. Many distributors and wholesalers have struggled with frequent delays in supply and limited stock. Stores also often ask for Campa fridges, like Coke or Pepsi, and that isn’t a game that Reliance is playing yet.

But it is undeniable that Reliance has shaken up the industry. For all its challenges, it has seen some positive early signs. And we expect to hear it make waves again.

Carbon Pricing is going mainstream

The World Bank releases an annual report that tracks “carbon pricing” — or put more simply, how countries around the world are making pollution more expensive, essentially using price tags as a tool to fight climate change.

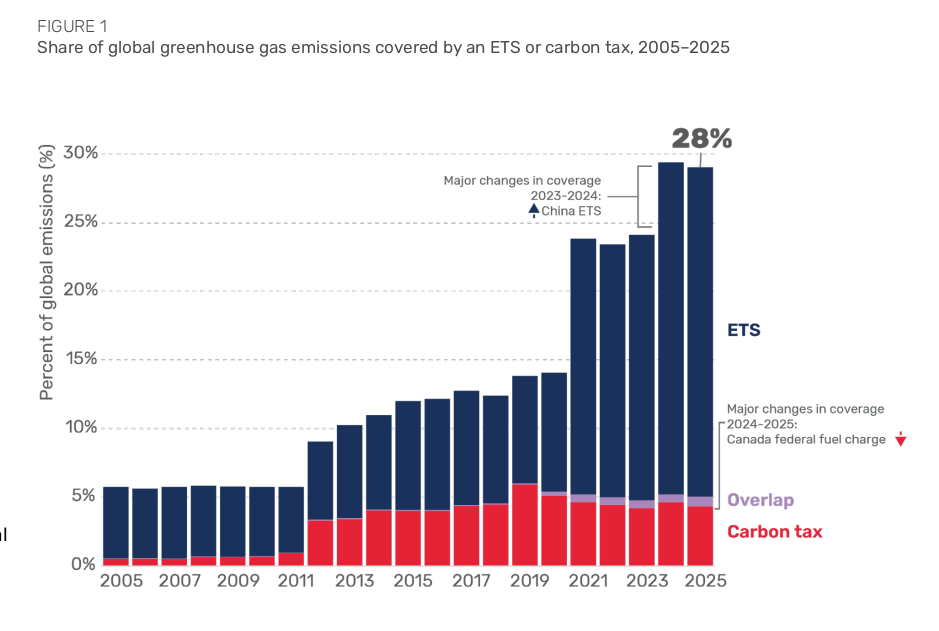

The 2025 edition of the "State and Trends of Carbon Pricing" report shows one big number front and center: 28% of global greenhouse gas emissions are now covered by a direct carbon price. That is, collectively, nearly 15 billion metric tons of carbon dioxide-equivalent emissions that have a price attached directly to them.

That's a big step forward. Back in 2005, only about 5% of emissions were priced. By last year, that had grown to around 24%. In the space of two decades, an increasing number of countries have started to treat carbon pollution more seriously — and a big tool they’re all converging on is putting a price on it.

What exactly is Carbon Pricing?

At its core, carbon pricing is about making polluters pay for the environmental damage they cause. Think of it like a toll road — except, instead of paying for using a highway, companies pay for using the atmosphere as a dumping ground for their carbon emissions.

The idea behind this is simple: if you make something more expensive, people will use less of it. By putting a price on carbon emissions, governments create a financial incentive for businesses to reduce their pollution. Companies that can cut emissions cheaply will do so to avoid paying the carbon price. Those that can't will pay the price, and governments can use that money to fund climate action elsewhere. Meanwhile, if they pass those costs on to customers, their products will have less demand — another balancing force.

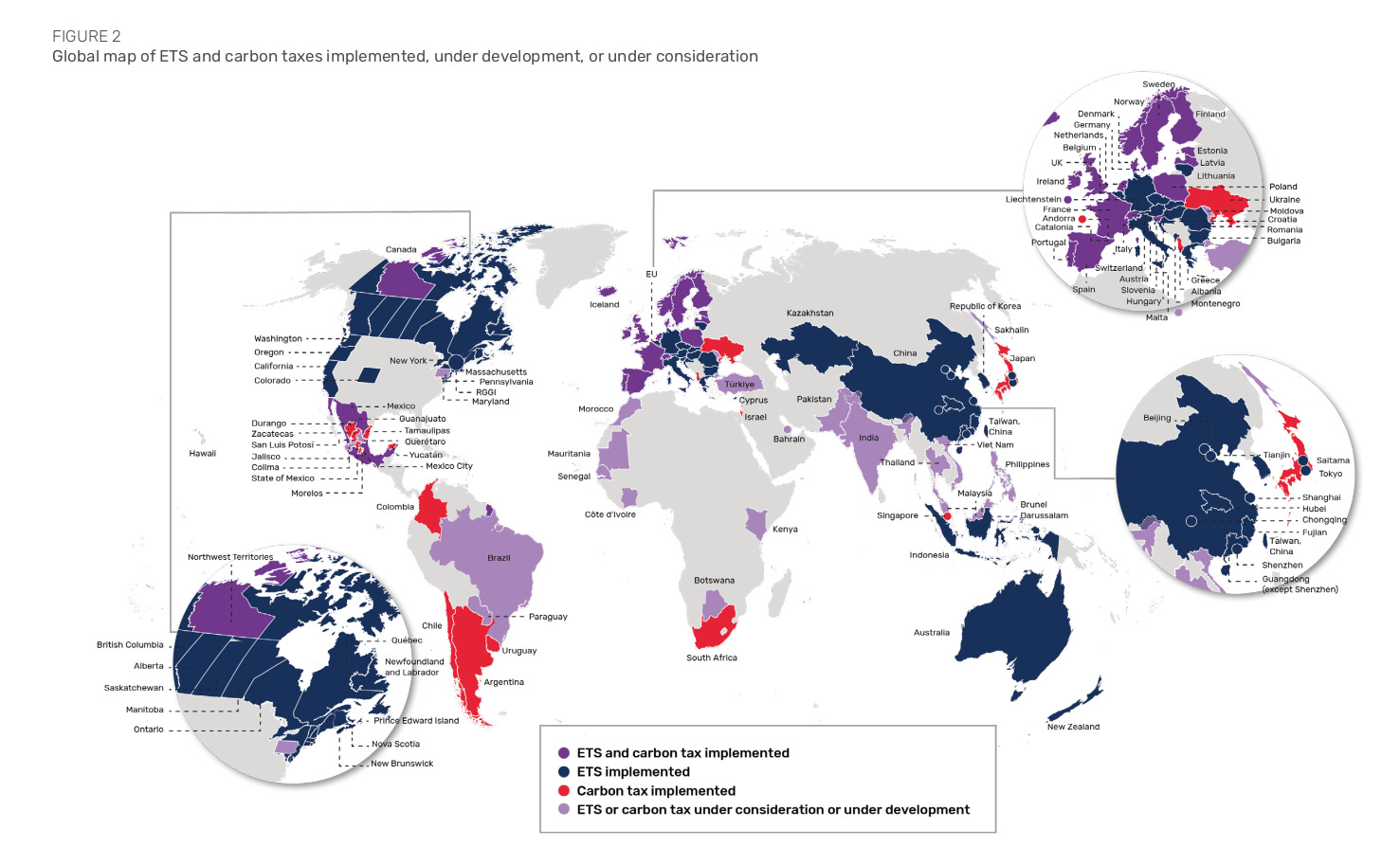

It’s one of the more direct ways in which you can address climate change. Most experts agree that it’s a good idea, even if many believe it’s not enough. That’s why there’s some form of direct carbon pricing in place in economies representing almost two-thirds of global GDP.

Most of the world’s advanced economies — from the European Union, to Canada, to Japan, to Australia — have some kind of carbon pricing in place. The United States is the big outlier in this group, but there too, states like California have put such systems in place.

But this isn't just a rich country phenomenon. Major middle-income economies — Brazil, Mexico, South Africa, Indonesia, and more — have either implemented carbon pricing or are actively moving toward it.

The sheer scale of growth in carbon pricing coverage, though, is largely thanks to one country: China. China has implemented a national emissions trading system — which started with its power sector, but is now expanding to include its cement, steel, and aluminum industries. That single move added 3 billion tons to the total emissions covered under the regime.

What happens to all that money? Like any other tax, it becomes a source of revenue for governments. In 2024, the combined revenue from carbon pricing crossed $100 billion for the second consecutive year. Even adjusted for inflation, this is more than three times higher than what it was a decade ago.

Carbon Taxes and Emissions Trading Systems

There are different ways in which you can do carbon pricing. Some countries prefer direct approaches — the government just sets a specific price per ton of carbon dioxide. Others create market-based systems where companies ‘trade’ for enhanced emission limits, letting supply and demand determine the price they pay. Some use a combination of the two.

Carbon taxes are the most direct, straightforward approach. The government simply sets a rate for carbon emissions, and charges companies based on how much they emit. It's like a fee to pollute. For example, if a company emits 1,000 tons of carbon dioxide and is taxed at $20 per ton, it pays $20,000 in carbon taxes.

The beauty of carbon taxes is that they’re simple and certain. Businesses know exactly what they'll pay for each ton of emissions. On the other hand, this system gives governments very little control over emissions. The government only wields a single, blunt lever — the tax rate. How effective it is in curtailing emissions depends on how companies respond to that rate.

Emissions Trading Systems (ETSs), on the other hand, flip the equation. Instead of setting a price, total cap on emissions — either for a sector or the whole economy — and issue a corresponding number of allowances or “pollution permits.” Each permit allows the holder to emit one ton of CO₂-equivalent.

Companies must surrender permits for each ton they actually emit. If they emit less than their allotment, they can sell excess permits. If they emit more, they must buy additional permits from others. This creates a market for carbon, where the price of permits is determined by supply and demand. The more pollution the system creates, the more expensive it becomes for each entity to pollute.

With this system, there’s surety around the quantity of emissions. They provide environmental certainty — governments control the total number of permits, so they know exactly how much emissions will be reduced. However, the carbon price itself fluctuates based on market conditions. This can make business planning more challenging, but it also allows businesses to turn good behaviour into money.

Both approaches have their merits. Many experts argue the choice between them often comes down to political and economic circumstances.

Carbon Credits

There’s another part of this ecosystem that works somewhat differently.

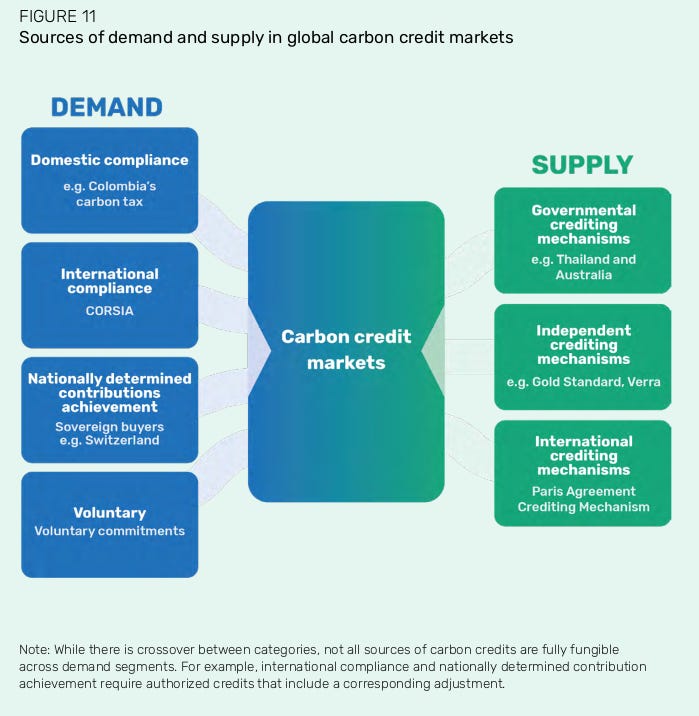

We’ve talked, so far, about systems where companies pay to pollute. On the flip side, though, companies can also be credited for avoiding emissions. This is where “carbon credits” come in.

The basic idea is this: you can create “credits” for companies that reduce emissions or remove carbon from the atmosphere through projects like reforestation or generating renewable energy. Each credit represents a ton of CO₂ that has been removed or avoided elsewhere. If they can then sell those credits, you create a direct economic incentive for good behaviour.

A company that wishes to prove its environmental bona fides — either to keep their investors happy, or sometimes, to meet government mandates — can buy these credits. By purchasing credits, companies can effectively balance out their emissions on paper without having to put in the work of cutting these themselves.

Here's how it works: Let's say a shipping company emits 10,000 tons of CO₂ from its cargo vessels each year, but wants to be “net zero”. The hard way of doing so is to hunt down and invest in new, expensive clean fuel technology. The easy option, on the other hand, is to simply buy 10,000 carbon credits from someone that, hypothetically, is protecting rainforests in the Amazon. Each of those credits represents one ton of CO₂ that is locked in those trees rather than being released into the atmosphere.

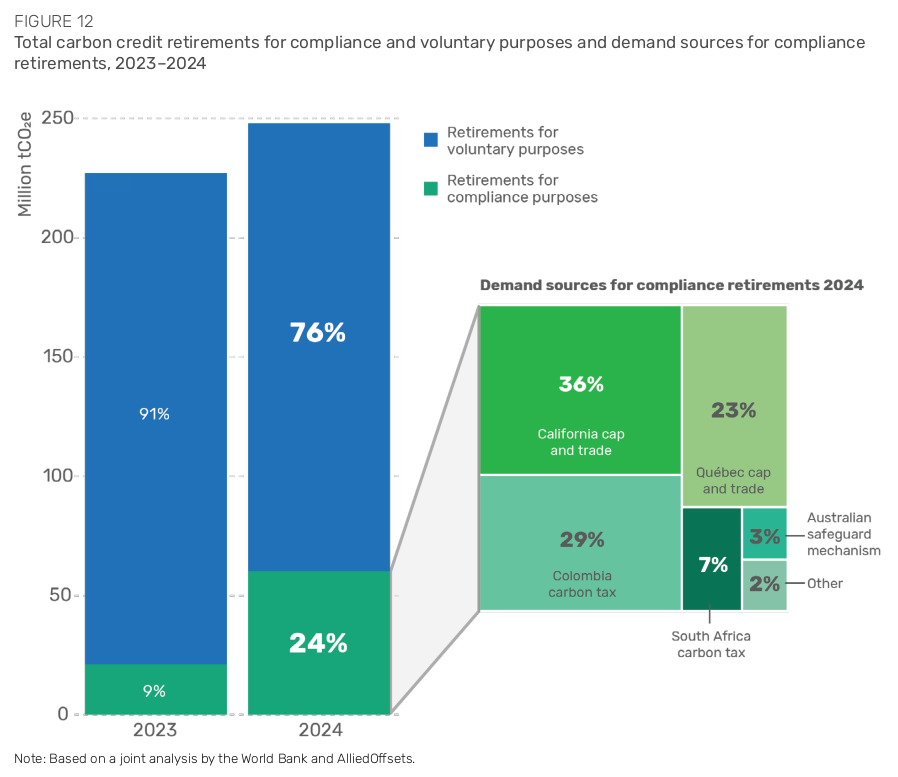

Unlike carbon pricing mechanisms — where you have no choice to opt out once your jurisdiction puts them in place — carbon credits are often voluntary. Many businesses choose to purchase carbon credits to meet self-imposed (or investor-imposed) climate goals. But that doesn’t mean these are just voluntary. Almost a quarter of global credit retirements in 2024 were to meet local compliance obligations. Voluntary and mandatory carbon markets, in a nutshell, are becoming increasingly interlinked.

But the report points to a problem: unretired carbon credits. There are many carbon credits that have been issued but are not yet retired. They're like unused gift cards — they exist, and have value, but haven't been redeemed.

That’s a damning indictment of the system. If there are so many credits that sit unretired, it indicates that there’s a reason nobody wants to claim them. It could be because there isn’t enough buy-in into the system; or that people are suspicious of whether those credits even correspond to something. Either way, if nobody wants to claim credits that others are creating — it raises questions around whether this can actually work as a system that effectively rewards sustainable behaviour. If the underlying idea is that tradable carbon credits would push investment towards genuine climate action, the fact that people don’t really want to use them dampens their credibility as a whole.

There are now nearly 1 billion unretired credits floating around from independent crediting mechanisms. That is a billion tonnes of carbon supposedly saved, which people don’t really care enough to even take credit for. Over two-thirds of these are "legacy" credits — they were issued before 2022, and yet, aren't finding buyers in the market.

The most common unretired credits come from forestry projects (36%) and renewable energy projects (30%). Are people more sceptical about the environmental integrity of these project types over others? We can only guess.

The Challenges

Beyond unretired credits, carbon pricing as a whole faces several other challenges, which the World Bank report highlights:

Coverage Gaps: While 28% coverage sounds impressive, it means 72% of global emissions still aren't covered by carbon pricing. This is concentrated in certain sectors, which are entirely outside the system. For instance, agriculture and land use, which produces over 25% of global emissions, remains almost entirely outside carbon pricing systems.

Price Levels: Many experts argue that carbon prices need to be much higher to drive the kind of decarbonisation required to meet climate goals. The High-Level Commission on Carbon Prices suggested that carbon prices should touch $50-100 per ton of CO2 by 2030, if we’re serious about the Paris Agreement’s goals. The current average price is $5.

Political Economy: Carbon pricing is a deeply political issue. It places real costs on businesses, and can cause political backlash. The report points to British Columbia's carbon tax. The tax helped create jobs and reduce inequality through revenue recycling, but it was still cancelled in March 2025 because it became "too politically divisive."

Coordination and Linkage: As more carbon pricing systems emerge, the challenge of coordinating between them grows. If different countries and systems use different rules, prices, and coverage, any country that operates across borders must deal with growing complexity. This potentially even creates opportunities for arbitrage, where companies game the differences between systems — for instance, by shifting production to the most permissive jurisdictions.

Looking Ahead

The 2025 report from the World Bank shows real progress on a promising idea. For a long time, carbon pricing was merely a clever idea. It seems to have moved to the implementation phase. The question now isn't whether carbon pricing will play a major role in global climate action – it already does. The question is of how we can make this system effective.

There’s a hard time limit for us to solve the issue. The window for limiting global warming to 1.5°C is rapidly closing. If we want a hope at beating this, it means carbon pricing systems need to be both larger, and more effective at driving rapid decarbonization.

Tidbits

Five Bidders Submit Plans for ₹57,185 Crore Jaiprakash Associates Insolvency Case

Source: Business Standard

Jaiprakash Associates Ltd (JAL) has received five resolution plans under the corporate insolvency process, according to a regulatory filing made on Wednesday. The company, which owes creditors ₹57,000 crore, was admitted into insolvency under a June 3, 2024 order by the NCLT Allahabad Bench. While the company did not disclose the names of the bidders, sources indicate the five interested parties include Adani Enterprises, Vedanta, Dalmia Bharat Cement, Jindal Power, and PNC Infratech. The deadline for submitting resolution plans was June 24, following initial interest from 26 companies earlier in April. The bids were opened in a lenders' meeting held on Wednesday. Suraksha Group, which had earlier acquired Jaypee Infratech, is believed to have been disqualified for not meeting eligibility criteria.

Adani Total Gas, Jio-bp Tie Up to Cross-Sell Fuels Across Retail Networks

Source: Mint

Adani Total Gas Ltd (ATGL) and Jio-bp have announced a strategic partnership to sell each other’s fuels across select retail outlets. As part of the arrangement, ATGL will begin selling Jio-bp’s petrol and diesel at its stations, while Jio-bp will install ATGL’s CNG dispensing units at its own fuel outlets. ATGL currently operates 650 CNG stations, while Jio-bp has a retail footprint of 2,000 fuel outlets across India. The collaboration is expected to enhance availability of multiple fuel options including CNG, petrol, and diesel across both networks. This marks the second significant interaction between Adani and Reliance after RIL acquired a 26% stake in Adani Power’s Madhya Pradesh project in March 2024. The move allows both companies to leverage infrastructure and improve fuel accessibility without duplicating investment.

HUL Demerges Ice Cream Business; Unilever to Hold 61.9% in New Entity

Source: Business Line

Hindustan Unilever Ltd (HUL) has announced the demerger of its ice cream business, including the Kwality Wall’s brand, into a newly formed listed entity named Kwality Wall’s (India) Ltd (KWIL). As part of this restructuring, shareholders of HUL will receive proportional shares in KWIL, while the Unilever Group will acquire a 61.9% stake in the new company. This stake will be held by Magnum Ice Cream Company, a Netherlands-based entity, through a share purchase agreement. Following the demerger, an open offer will be made to public shareholders of KWIL. The move aligns with Unilever’s global restructuring plan aimed at creating focused business verticals. The ice cream business, once listed separately, is expected to operate independently with its own strategic and operational focus.

- This edition of the newsletter was written by Manie and Prerana.

📚Join our book club

We've started a book club where we meet each week in JP Nagar, Bangalore to read and talk about books we find fascinating.

If you think you’d be serious about this and would like to join us, we'd love to have you along! Join in here.

🧑🏻💻Have you checked out The Chatter?

Every week we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

“What the hell is happening?”

We've been thinking a lot about how to make sense of a world that feels increasingly unhinged - where everything seems to be happening at once and our usual frameworks for understanding reality feel completely inadequate. This week, we dove deep into three massive shifts reshaping our world, using what historian Adam Tooze calls "polycrisis" thinking to connect the dots.

Frames for a Fractured Reality - We're struggling to understand the present not from ignorance, but from poverty of frames - the mental shortcuts we use to make sense of chaos. Historian Adam Tooze's "polycrisis" concept captures our moment of multiple interlocking crises better than traditional analytical frameworks.

The Hidden Financial System - A $113 trillion FX swap market operates off-balance-sheet, creating systemic risks regulators barely understand. Currency hedging by global insurers has fundamentally changed how financial crises spread worldwide.

AI and Human Identity - We're facing humanity's most profound identity crisis as AI matches our cognitive abilities. Using "disruption by default" as a frame, we assume AI reshapes everything rather than living in denial about job displacement that's already happening.

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉