Do ATMs still make sense?

The Future of Cash in India

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Are ATMs in India dead?

Are ATMs in India dead?

When was the last time you took cash out of an ATM? The existence of UPI has at least minimized, if not outright removed, the use of ATMs for many people in Indian cities.

But believe it or not, India is sitting on more physical cash today than it has at any point in its history.

According to the RBI’s currency-in-circulation data, the total value of banknotes in circulation in India was 41 lakh crore. That’s actually more than double the level just before demonetisation in November 2016, when banknotes in circulation stood at ~₹18 lakh crore. The currency that demonetisation was supposed to remove has more than come back.

UPI didn’t kill cash. It took over the small, fast, daily transactions: the local tea/coffee shop, the auto, the kirana shop, and so on. But large parts of the country still run on cash for reasons that have little to do with UPI’s technical capabilities.

In much of rural India, where the only bank branch is hours away, cash is just what works. Many of the people transacting in cash, like agricultural labourers, daily-wage construction workers, and small traders in rural and semi-urban India, don’t even have working bank accounts, or have lost trust in them. A lot of transactions in real estate and the unorganized economy are settled in cash precisely to stay outside the formal banking trail.

Then, there’s the question of what kind of cash this is. Of the ₹41 lakh crore in banknotes, roughly ₹35.2 lakh crore is in ₹500 notes alone. The ₹500 isn’t the note you use for everyday spending, though. It sits in wallets, drawers, and almirahs. In a 2023 research paper, the RBI concluded that digital payments are now substituting cash for everyday transactions, but the store-of-value motive for holding cash remains intact. Cash in India has grown not because people are transacting in it more, but because they’re holding more of it.

The demand for physical cash is very much alive. What UPI has changed is how people get hold of it, and because of it, the economics of running ATMs. After all, several ATM operators — including one of the two largest companies that ran the country’s ATM network — have collapsed in the last few years.

But the chain of events isn’t as straightforward as you’d think. And that’s what we’ll be getting into in this story.

Money maker

Let’s start with the fundamentals of how ATM operators make money.

Say you have an HDFC Bank account. You walk up to an SBI ATM and withdraw ₹10,000. Behind the scenes, HDFC Bank (which is your bank) pays SBI a small fee for letting you use their machine. This fee is called the interchange fee.

The interchange fee is the source of margins for an off-site ATM (which is an ATM not attached to a bank branch). An ATM exists because somebody runs them and earns ₹19 every time you use one. Sometimes the owner is a bank itself, paying a third party to manage the machine on a per-transaction basis. Sometimes, the owner is a separate non-bank company called a “white label“ operator (like Indicash or Hitachi Money Spot), whose whole living comes from interchange fees. The model works as long as enough people use each machine repeatedly.

But the fee has barely moved. It was ₹15 from 2012, raised to ₹17 in August 2021, and then to ₹19 in May 2025. Two hikes in 13 years.

Since UPI took over small, daily transactions, an ATM that used to do 200 transactions a day now does a fraction of that. At the same time, the costs of running an ATM machine — from the rent on the ATM cubicle to the diesel for the cash van that comes to refill the machine — have all gone up.

Perhaps the biggest cost increase lies in wages. The new Labour Codes, which standardise minimum wages and benefits across India, are pushing up the cost of the ground-level workforce that runs this industry — like drivers, security guards, and cash custodians.

The Currency Cycle Association, which is the industry body for cash operators, told Business Standard in May 2026 that the industry is now in a “force majeure situation“. That’s a term for when a business can no longer operate as designed because of forces it can no longer control.

Ka-ching no more?

The first major domino that fell victim to a force majeure situation was AGS Transact Technologies.

AGS was the second-largest ATM managed services provider in India. At its August 2021 peak, it had installed, maintained or managed around 72,000 ATMs and cash recyclers across the country. It went public in January 2022 at ₹175 a share.

But by mid-2025, the company found itself in freefall. In early 2025, nearly 38,000 ATMs serviced by AGS went dark — including 14,000 SBI ATMs, India Post ATMs, and Yes Bank ATMs. On August 25, 2025, the National Company Law Tribunal in Mumbai admitted AGS to corporate insolvency, and by February 2026 admitted creditor claims against the company had reached ₹13,171 crore. The stock was at ₹5, down 97% from its IPO price.

AGS was the most dramatic failure, but not the only one. White label operators have been hit just as hard. Since they only earn from interchange and run no other line of business, a ₹19 fee that no longer covers cost is an existential problem rather than a margin question. Tata Communications, for instance, divested its white label network Indicash to Findi India in March 2026, exiting the business it had pioneered in 2013.

What’s being built instead

So, what does that mean for the ATM?

Well, the machine itself is changing. The old ATM was a cash dispenser. The new machine is a cash recycler, which still dispenses cash but also accepts deposits, so small business owners can deposit their daily takings without queuing at a branch. The same machine can also do video KYC for a new account, issue a fresh debit card, run a cross-sell on a personal loan, or update a passbook.

In effect, the new ATM sounds a lot like a partial bank branch with no teller.

That’s not coincidental, either. Banks now often use the ATM as a way to offload work from their branches. Anything you used to do at the teller’s counter, except wealth management and lending, you can now do at an ATM.

On the latest earnings call of CMS Info Systems, the largest cash management company in India, Chief Business Officer Anush Raghavan explained what this looks like in practice for one of its clients, ICICI Bank:

“Two years back, they [ICICI Bank] had, I think, about 20% cash recyclers and 80% cash dispensers. Two years since now, since we have been working with them, it has gone the other way. We are 80% cash recyclers and 20% dispensers.”

The contracts under which ATMs are being built are changing too.

In the old model, the operator was paid a fee per transaction. So when transactions dropped, operator revenue dropped. The new model is a fixed monthly fee per machine. That inherently means that the bank takes some of the risk of transaction volumes being low. The operator gets paid more predictably.

In fact, CMS CEO Rajiv Kaul said on the same earnings call that “for all practical purposes, the transaction fee model is dead in the ATM business.” CMS itself walked away from a ₹700 crore contract at ₹19 per transaction — equivalent to ₹75 crore of annual revenue — because the unit economics over the seven-year contract life didn’t work.

In FY26, CMS signed long-term fixed-fee contracts with SBI, ICICI Bank and HDFC Bank that together secured 85% of its FY27 revenue target. With AGS gone and smaller white label operators struggling, CMS now holds a whopping 46% market share in India’s ATM cash management.

Cash rules everything around me

So, with recyclers taking over dispensers, and fixed fees replacing per-transaction fees, what does the broader picture look like?

See, a cash recycler costs roughly ₹6 lakh to install, versus ₹3.5 lakh for a pure dispenser. The economics of these expensive multi-function machines only work if enough people use them for enough things, which means installing them where banks already have customers and where the recycler can act as a branch substitute. In practice, this means the new ATMs are going into urban and tier-1 to tier-3 locations.

Now consider the machines that are being shut down. As per the RBI’s Report on Trend and Progress of Banking in India, between FY24 and FY25, on-site ATMs grew by roughly 5,000, while off-site ATMs declined by nearly 8,000. Off-site is where you find ATMs not attached to a bank branch, like a petrol pump or a small-town market street. These are also the ATMs that white label operators, who run most of their machines in semi-urban and rural areas, have always depended on.

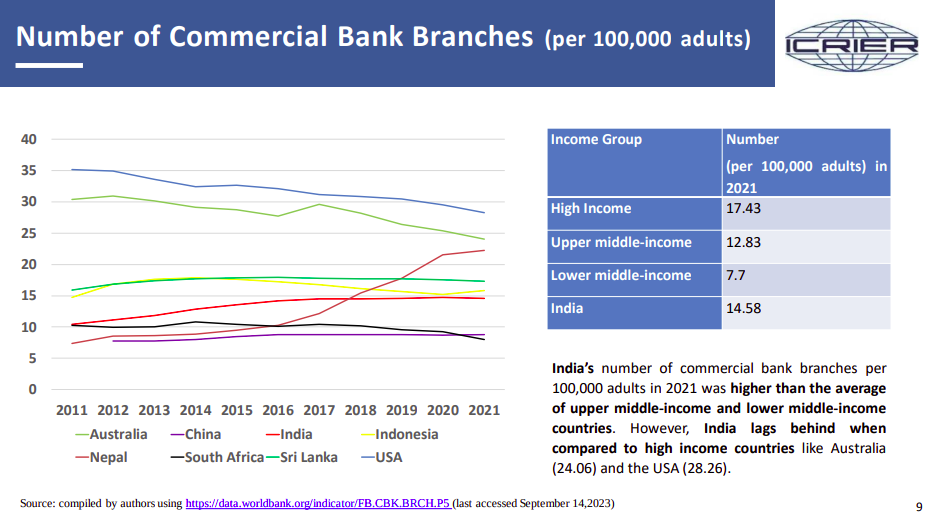

According to an ICRIER consultation report, just 21.6% of India’s ATMs are in rural areas, and India has 21.4 ATMs per 1 lakh adults compared to a global average of ~39.5. Most of the rural cash-access machines that do exist depend on the old, outdated interchange fee model.

Banks haven’t abandoned rural cash access, though. They’re just far less reliant on ATMs.

For one, there are 22,000+ regional rural bank branches (RRBs) across 730 districts. Secondly, business correspondents, who are individuals authorised by banks to provide basic banking services through their own shops, now operate the majority of India’s banking outlets in branchless mode. And then there are micro-ATMs, which are handheld biometric or card-based devices through which a kirana shopkeeper can dispense small amounts of cash from their own till. These grew to nearly 1.5 million units as of 2024.

These substitutes work, but they are different products. A micro-ATM caps your withdrawal at around ₹10,000 and depends on the shopkeeper having that much cash on hand, which they often don’t. A business correspondent operates during their own business hours and is dependent on one person’s reliability and connectivity. An RRB branch has fixed hours and queues. None of them is the equivalent of a 24/7 ATM.

The new infrastructure looks more suited to the areas they’re in. It’ll be a long while before we get to know whether the substitutes are as good as the off-site ATMs being lost. But what is clearer than ever is that the Indian ATM is no longer the humble, lumpy cash machine we have known it to be for so long.

Tidbits

JSW Group has finalized plans to set up a 30 GWh lithium-ion cell manufacturing facility with a joint venture partner, investing over $1.3 billion across two phases. The company is evaluating Southeast Asian countries for the plant to leverage India’s free trade agreements, and will import cells from China in the interim as it aims to deliver its first new energy vehicles by late 2026 or early January 2027.

Source: Business StandardOn June 5, Maruti Suzuki will launch India’s first E100 vehicle — a car that runs on nearly pure ethanol, marking a step beyond the country’s existing E20 blending programme. While industry executives estimate E100 could cut per-kilometre fuel costs by 25–35%, the bigger challenges remain: limited refuelling infrastructure, lower energy density than petrol, and consumer unfamiliarity with flex-fuel technology.

Source: Business StandardRealty firm Anant Raj has signed an MoU with the Haryana government to invest ₹20,000 crore in large-scale data centre infrastructure across the state, expected to create around 6,000 jobs. This is over and above its existing 307 MW expansion pipeline across Manesar, Panchkula and Rai, and follows a ₹4,500 crore commitment in Andhra Pradesh eight months ago.

Source: Business Standard

- This edition of the newsletter was written by Krishna.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Rosa & Tamoghna on India’s Youth Employment Crisis

In India, the more educated you are, the more likely you are to be unemployed. Graduate unemployment among the youth sits at 40%. For those with no education, it’s 3%. We recently spoke to Rosa Abraham and Dr. Tamoghna Halder, two of the authors behind the Azim Premji University’s State of Working India 2026 report, to understand why. Our conversation goes into what’s really driving this paradox — the role of caste and social signalling in education choices, whether waiting for a good job is rational, why the “missing middle” of Indian firms matters, and what the demographic dividend window really means for policy. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Why did Zerodha withdraw the 2nd story from the podcast about Reliance?

Why only single story today?