Recap: RBI's concerns, cash floods mutual funds, inflation, and housing push

This is the seventh weekly brief. We publish a new episode every day to help you understand the biggest stories in the Indian markets. But we understand that you may be busy and don't have the time to listen to the daily episodes. So don't worry; we've got you covered.

Every week, we'll publish a new episode simplifying the biggest stories of the week so that you can still look smart in front of your friends.

Check out the audio here:

And the video is here.

In this week's episode, we look at these stories:

RBI governor is worried about a lot of things

It’s raining cash for mutual funds

Inflation is not inflating

The govt wants to make housing affordable for all

RBI governor is worried about a lot of things

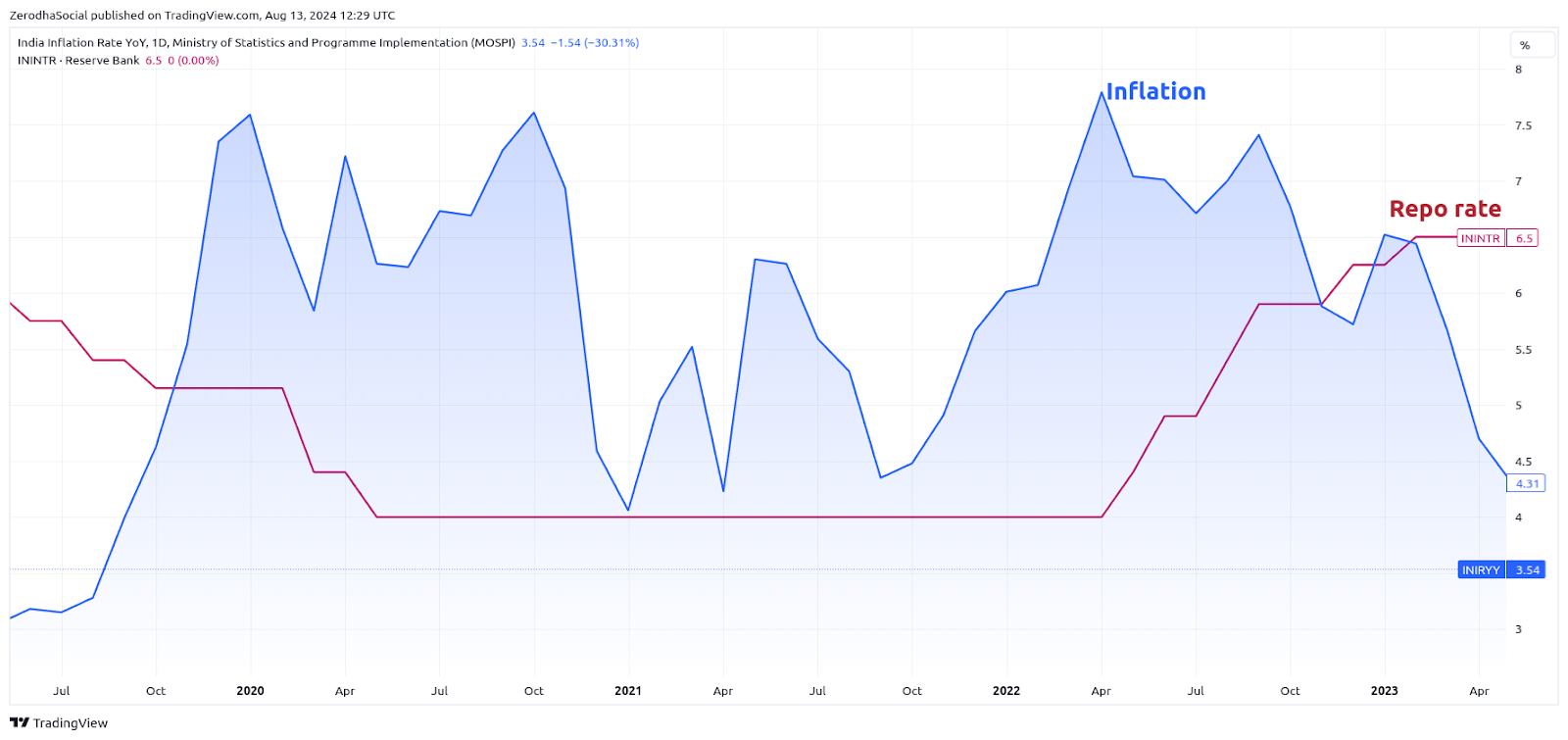

Last week, the RBI had its policy meeting, and as expected, they decided to keep the repo rate unchanged at 6.5% for the 9th consecutive meeting.

So, no surprises here—borrowing costs stay the same for now. Why did they make this call? The RBI is playing it safe, keeping a close eye on inflation, especially food inflation.

Since November 2023, food inflation has consistently stayed above 8%. This is a big deal because food and beverages make up about 45% of the overall CPI inflation basket. So, when food prices go up, it pushes headline inflation up too. That’s why CPI inflation has been above the RBI’s target of 4% for most of the year, except for this month when it dropped slightly. But that drop is mainly due to the base effect since inflation in June 2023 was at a high of 7.4%.

The RBI is concerned because rising food prices affect everyone. Imagine going to buy your favorite snack and finding out it costs more than it did last month—not great, right? The RBI knows that high food prices can really pinch people’s wallets, so they’re keeping a close watch to make sure things don’t spiral out of control. Until they’re confident that inflation will stay under 4%, interest rates aren’t likely to budge.

In his recent speech, RBI Governor Shaktikanta Das highlighted this concern. He mentioned that high food inflation impacts household inflation expectations. Basically, if inflation stays high, people start to believe it’ll stay that way, which can lead to higher wages and living costs. This, in turn, can cause companies to raise prices, making inflation even stickier.

But that’s not all the governor talked about. He made some important observations and announcements that I’ll break down:

On Credit Growth and Deposit Growth:

Last month, the RBI governor pointed out a growing gap between credit growth and deposit growth and called for a better balance. He reiterated this concern in the policy meeting. He said that alternative investment avenues, like mutual funds and debt funds, are becoming more popular, leading to slower deposit growth compared to the rate at which banks are lending. If this gap continues, it could expose the banking system to structural liquidity issues.

The governor is worried that these alternatives are drawing money away from traditional bank deposits, which are critical for banks to fund loans. He’s urging banks to get creative and find ways to attract more deposits.

On Unsecured Loans:

The RBI has been keeping a close watch on the rapid growth of unsecured loans since the pandemic. At one point, these loans were growing at a staggering 32% year on year, though it’s now moderated to 28%. The governor noted that measures taken in November 2023 to make personal loans more costly for banks are having an impact.

However, some segments of personal loans are still growing at a fast pace. The governor raised concerns about people taking out personal loans for consumption purposes, which could become a macroeconomic problem.

It’s not just personal loans that are on the RBI’s radar. The governor also mentioned home equity loans, or top-up loans, where people borrow extra money on top of an existing loan, like a home loan, as well as other collateralized loans like gold loans. The RBI has noticed that some banks aren’t following the rules when issuing these top-up loans.

Given the RBI’s recent crackdown on various issues, from KYC to underwriting—as seen with Paytm, Bajaj Finance, Kotak Bank, and HDFC Bank—it looks like some regulatory action might be coming for lenders that aren’t playing by the rules with top-up loans on houses and gold.

On UPI Changes:

Now, onto some good news! The RBI announced some exciting changes for UPI. First, they’re raising the limit for UPI transactions when it comes to paying taxes. Right now, the limit is ₹1 lakh per transaction, but they’re bumping it up to ₹5 lakh. So, if you’ve got a big tax bill to pay, UPI’s got your back.

But there’s more! The RBI is also introducing something called Delegated Payments through UPI. This is a pretty cool feature—it means you can allow someone else, like a family member, to make UPI payments from your account up to a certain limit, even if they don’t have their own bank account linked to UPI. So, if you’re tied up and need someone to pay a bill for you, they can do it directly from your account. This is going to make digital payments even more flexible and convenient.

So, while the RBI is keeping a tight grip on inflation and credit growth, they’re also making sure digital payments continue to evolve and become even more user-friendly.

It’s raining cash for mutual funds

The mutual fund flows data for July just came in last week, and it's clear that domestic investors are still incredibly bullish on the markets. In July alone, investors poured in ₹43,000 crores into mutual funds. While that’s a slight dip from the ₹45,000 crores in June, it’s still a massive figure. Just to put it in perspective, mutual fund flows during the same time last year were only around ₹9,400 crores.

The pace of inflows into mutual funds this year has been nothing short of remarkable. So far this calendar year, net equity inflows have totaled about ₹2.4 lakh crores. Compare that to the first seven months of last year, when it was just ₹80,000 crores, and you can see how stunning this year’s numbers are.

A big part of this surge in inflows is thanks to strong SIP (Systematic Investment Plan) flows and the money going into new mutual fund schemes, also known as NFOs (New Fund Offers).

Let’s start with SIP flows. On average, gross SIP inflows have been around ₹20,000 crores each month, but the net SIP flows—after accounting for redemptions—are about ₹8,500 to ₹9,000 crores. The popularity of SIPs has skyrocketed over the last four years, becoming a go-to investment option for many.

Now, talking about NFOs—the inflows here have been nothing short of impressive. This year, new mutual fund schemes have raised a whopping ₹51,700 crores. Last year, this number was just ₹17,800 crores. People are really going all in on new thematic schemes targeting sectors like defense, manufacturing, energy, and tourism. It’s a clear sign of a bull market when everyone’s going crazy over the latest investment themes.

Mutual fund flows are a key reason why the Indian markets have been so resilient this year. But it’s not just mutual funds driving this strength—you’ve also got equity flows coming in from the provident fund, the national pension scheme, and insurance companies. All these automatic flows have been steadily growing, showing how the investor base in Indian markets is deepening. It’s a great sign of confidence and interest in India’s growth story.

Inflation is not inflating

So let’s start by talking about the latest inflation numbers.

In the aftermath of the pandemic's reopening, inflation spiked and has remained above the RBI’s target of 4%. In response to the inflationary shock, the RBI increased interest rates from 4% to 6.5%. Since then, it has kept the interest rates unchanged because inflation has remained stubbornly high despite the high interest rates.

But the inflation data for July came in, and CPI inflation fell to a 5-year low of 3.5%. In July 2023, it was at 7.44%.

That’s a very big drop, and you might be thinking that this is really good news and hoping that the RBI will start cutting interest rates.

But don't get excited just yet. There's nuance to this.

The drop in inflation is because of base effect. I know that sounds like a made up thing, but let me explain. Inflation is typically measured as the year-over-year percentage change. That means if inflation, or any other economic metric, was unusually high or low in the previous year, it creates a "base" that can make the current year’s changes look more extreme than they actually are.

If prices were very high last year (the "base" year), even a small drop this year might seem like a significant decrease when we calculate it as a percentage. This is because we are comparing this year’s numbers to last year’s unusually high numbers, making the fall look bigger than it really is.

For example, in this case, the headline inflation rate back in July 2023 was 7.44%, which is a very high number compared to the long term averages. And now, because prices are starting to rise at a lower rate, inflation has fallen to 3.5%.

this fall

This fall is almost entirely because the point of comparison is an outlier. So this fall in inflation won't last. Once the base effect normalises inflation will return to its trend.

Having said that, let me briefly talk about the July inflation numbers.

Headline inflation, or CPI inflation, fell to 3.5% from 5%, but as I explained, this was because of the base effect. If you look at food prices, they are still rising, but at a slower pace.

Core inflation, which removes food and energy, rose from 3.1% to 3.4% because of the increase in telecom tariffs, which we have spoken about in previous episodes.

Last year and even the last few months, food inflation was high due to supply chain disruptions and adverse weather conditions, creating a base effect that makes this year’s inflation rate appear lower, as I mentioned earlier. Now the hope is that this year’s expectation of a good monsoon will become reality and food inflation will fall. So far, monsoons are progressing well, and let's hope they continue that way.

In some good news, energy inflation has fallen 11 months in a row. In July, it dropped by -5.5%, which is a bigger drop compared to June's -3.6%.

The main reason for this big drop is the continued decrease in LPG prices. The stabilisation of global crude oil prices has also significantly reduced fuel inflation. Despite geopolitical tensions, oil prices have remained relatively stable due to increased global supply and subdued demand, especially from China.

The govt wants to make housing affordable for all

Let’s talk about how the government is trying to make housing more affordable for everyone.

In India, owning a home is a big deal. It’s not just a place to live; for many, it’s the most important asset they own. In fact, over half of all household wealth in India is tied up in property. And it’s not just an Indian thing—governments all over the world push for homeownership because it gives people a sense of financial stability. But India has a huge housing shortage, with some estimates saying we’re short by 5 to 10 crore homes. Plus, not many people here take out home loans compared to other countries.

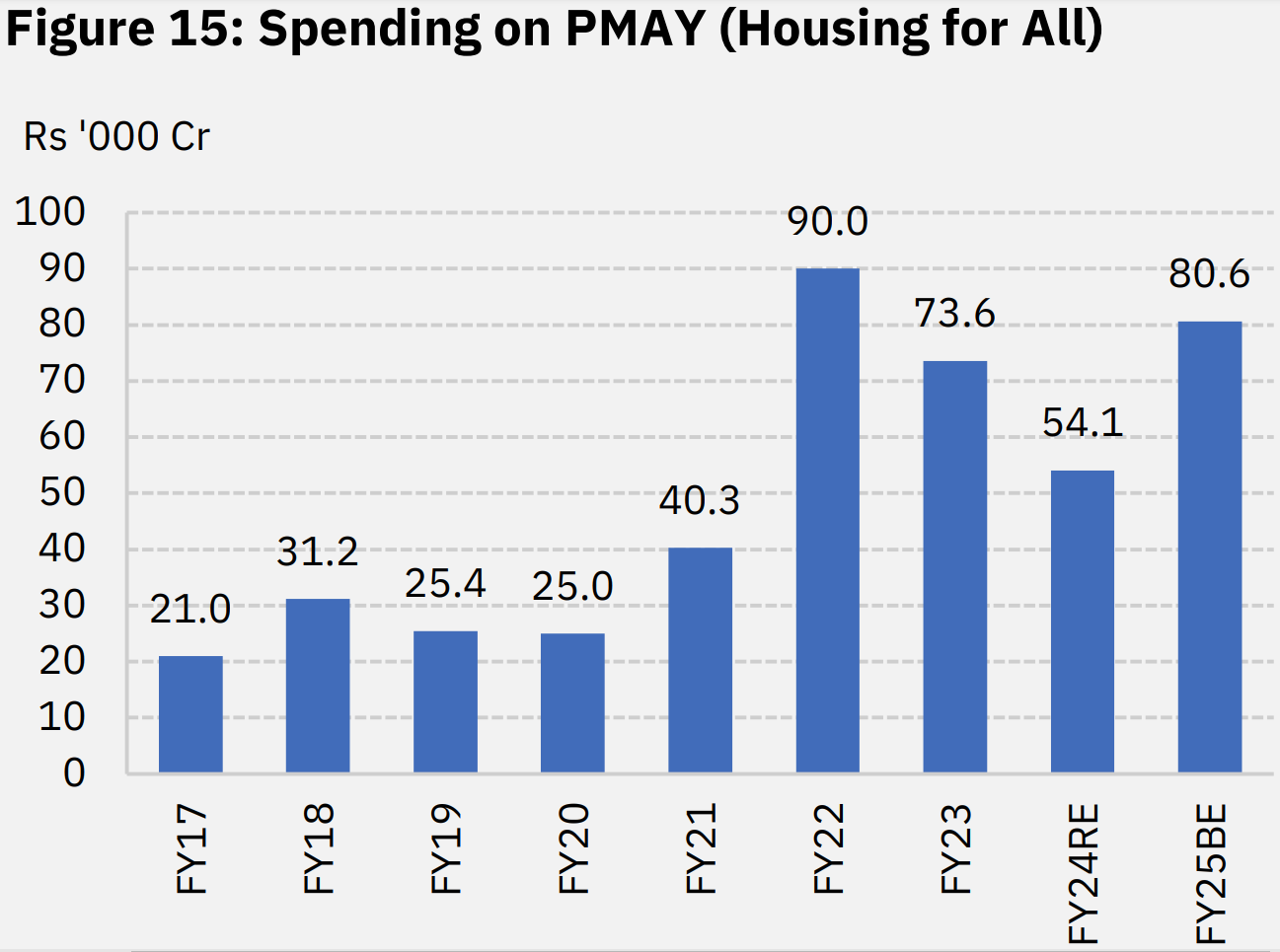

Back in 2015, the Indian government launched the Pradhan Mantri Awas Yojana (PMAY) to tackle this issue. The goal? To make housing affordable for the poorer sections of society through things like subsidies, financial help, and encouraging the construction of affordable homes, whether by the government or private companies.

The scheme has two parts: one for urban areas and one for rural areas. By June 2024, around 80% of the houses targeted under the urban scheme were built, while the rural part hit most of its goals. Sure, there have been some complaints about the quality of the houses or whether the right people got them, but we’ll dive into that in another episode.

The first version of the scheme was supposed to wrap up in 2022, but it got extended to 2024. In the recent budget, the government rolled out a new version to build 3 crore more homes in urban and rural areas. The cabinet just approved the Pradhan Mantri Awas Yojana-Urban, so here’s what you need to know:

Over the next five years, the government plans to help 1 crore urban poor and middle-class families either rent, build, or buy a home at an affordable price. They’ve set aside ₹10 lakh crores for this. To make sure banks and housing finance companies don’t get burned by defaults, the Credit Risk Guarantee Fund has been boosted from ₹1,000 crore to ₹3,000 crore.

The government is also offering incentives to developers to build affordable homes, and for buyers, they’re providing interest subsidies.

But here’s the catch: the new scheme isn’t as generous as the old one. They’ve capped or reduced the maximum subsidy, the interest subsidy, the loan amount, and the property value.

Even though the new scheme is a bit more restrictive, Jeffries research suggests it still covers about 60–70% of the loans given under the old scheme. For the housing market, this is good news, especially for housing finance companies that focus on affordable housing.