Real estate’s three measures of success

And two looming threats

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Three tales of real estate: Q4 at India’s residential developers

Jio and Vodafone don’t like Airtel’s new postpaid plan

Three tales of real estate: Q4 at India’s residential developers

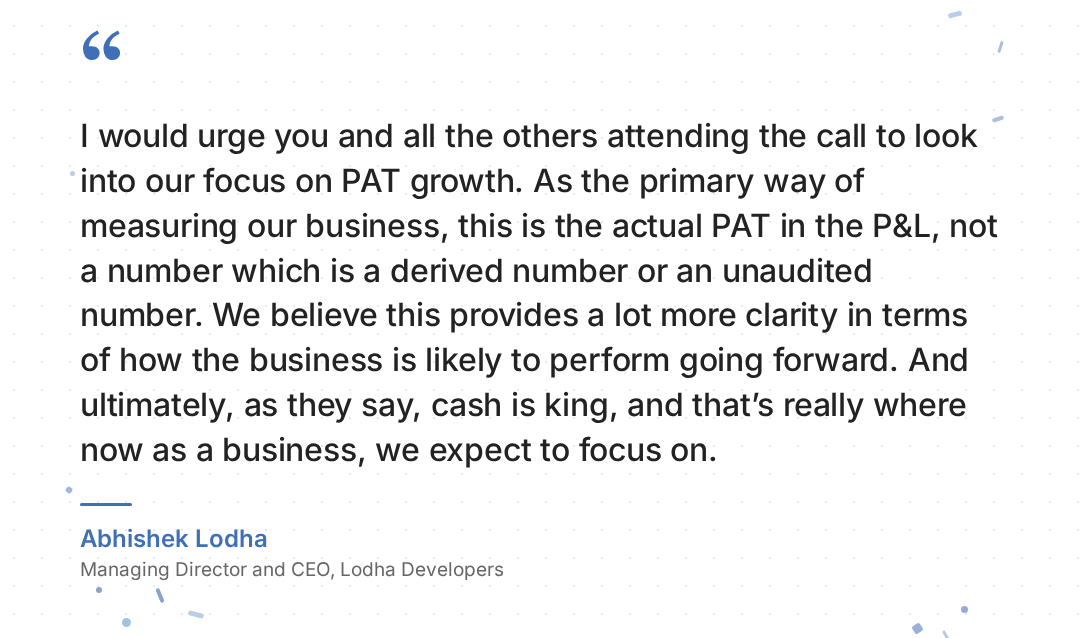

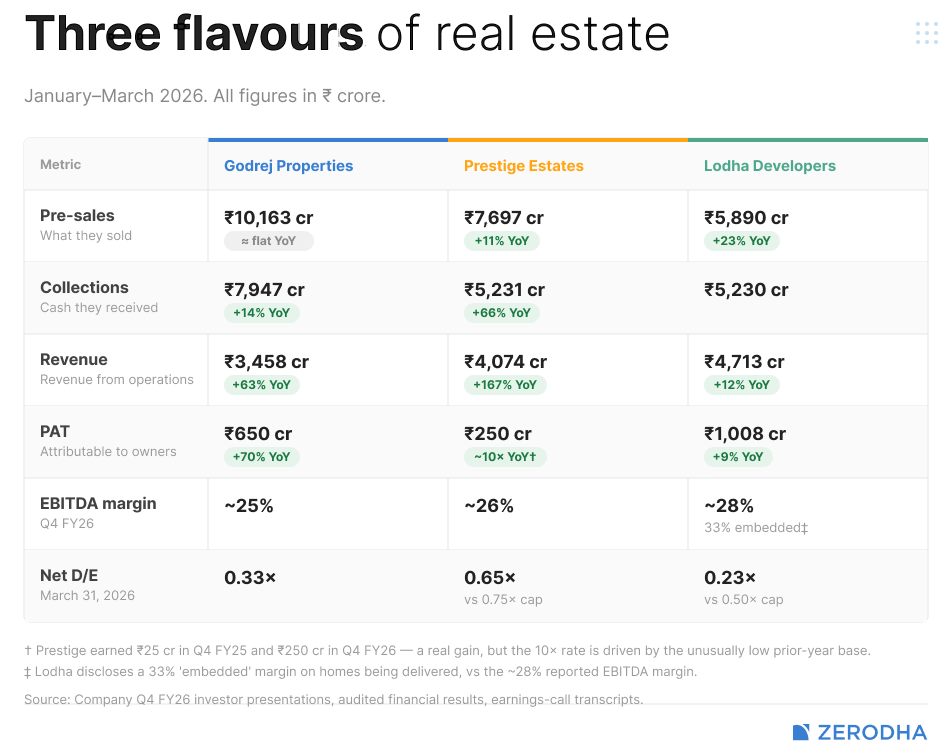

On April 27, Abhishek Lodha, the MD and CEO of Lodha Developers, told investors to stop looking at his company’s pre-sales numbers. That was odd. “Pre-sales” — the value of homes a developer agrees to sell in a period — is a number real estate companies live and die by. Lodha had just reported its strongest-ever quarter on this front, having sold ₹5,890 crore worth of homes between January and March. And yet, Abhishek wanted investors to focus on his company’s actual profit instead. Pre-sales, he said, isn’t a great measure of the underlying health of a real estate business.

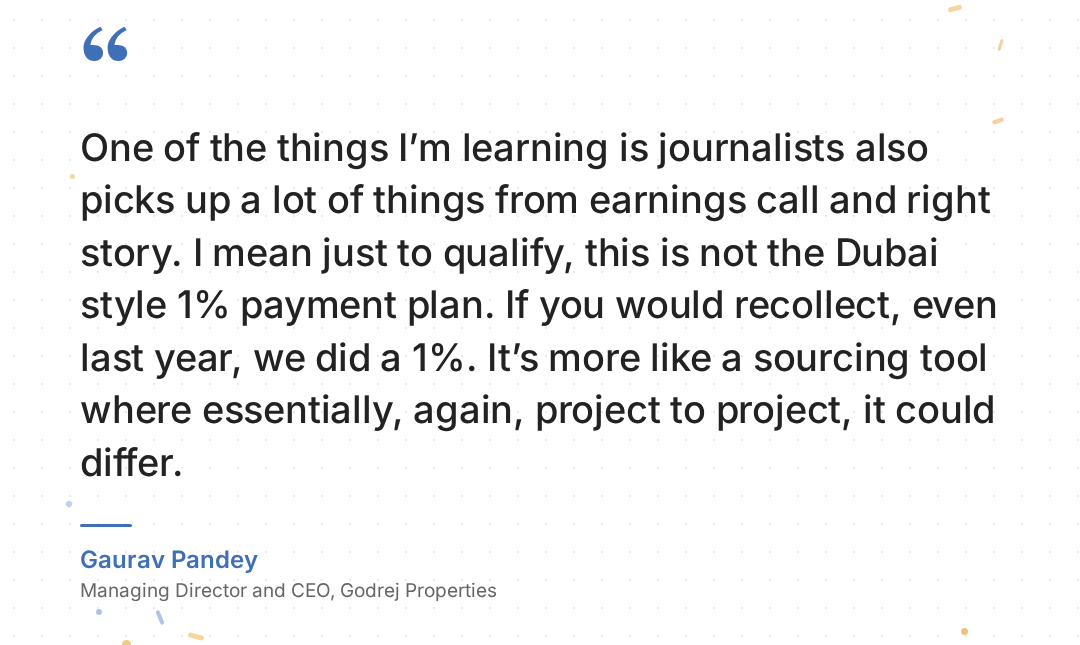

A week later, though, on Godrej Properties’ investor call, chairman Pirojsha Godrej invited investors to focus on… well, pre-sales. Godrej had just announced the largest annual booking value ever published by a listed Indian developer, having sold ₹34,171 crore worth of homes through the year.

Then, a few weeks hence, Prestige Estates’ Irfan Razack told investors to look at something else entirely: revenue. The company’s revenue had grown 71% over the previous year, while profits had more than doubled. Almost as an aside, Razack pointed to an additional ₹65,935 crore of sales that hadn’t shown up as revenue yet.

Three of India’s largest residential developers, in the same quarter, were looking at different metrics. Little of that was management spin. In the business of residential real estate, “pre-sales”, “revenue”, and “profit” mean three very different things. The number a developer chooses to emphasise tells you something about what their business focuses on.

Results, in three shapes

Godrej Properties

Godrej Properties is the largest company we’re looking at today.

For the third year running, it was India’s biggest residential developer by booking value. The roughly ₹34,000 crore worth of homes it sold, last year, was well above its own guidance. Almost a third of that came from the March quarter alone — one of the best the company has ever reported.

But those were bookings. The cash actually coming in from those buyers was a slightly different story. The year’s collections fell just short of ₹20,000 crore — 17% higher than last year, but still short of the ₹21,000 crore management had promised. It’s a minor miss, but it points to something: Godrej’s bookings are running faster than the cash arriving from buyers.

This is the sort of thing that happens when a developer pushes new launches over older projects further along in construction. And Godrej was doing just that: for instance, it ran a pan-India “1% campaign” during the quarter, where buyers put down 20-30% upfront, and then pay just 1% of the price every month until they take possession — a softer payment plan than the industry standard.

The company is loading its pipeline further still. Across FY26, it added ₹42,100 crore worth of future sales potential — enough to keep its pipeline overflowing for years. But for now, that future pipeline probably looks like hard cash and capital commitments in buying land.

Prestige Estates

Prestige, meanwhile, is the fastest growing company in the set.

Its pre-sales through FY 2026, at ₹30,025 crore, were up 76% from the previous year. The Bengaluru-based company has been rushing to capture new markets, and the plan seems to work. The company’s first major foray into the NCR market — Prestige City Indirapuram — booked nearly ₹9,500 crore in sales by itself: a number that major players struggle to meet across an entire portfolio.

More interestingly, its revenue grew by a staggering 71% year-on-year, while profits more than doubled.

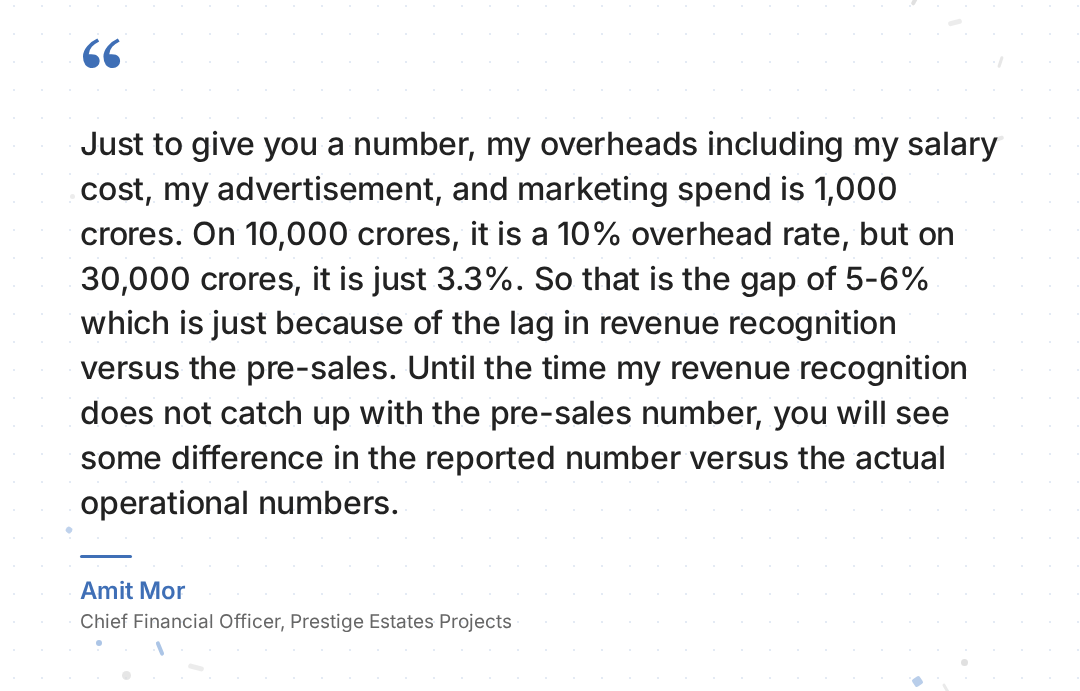

And yet, the company’s margins had fallen to 27% — well below the 30% often quoted as an industry baseline. As its management noted, the company’s overhead costs — salaries, advertising, marketing — had ballooned to about ₹1,000 crore. That’s a pittance compared to its ₹30,000 crore pre-sales. But compared to the revenue actually showing up in its books, of roughly ₹10,000 crore, it looked much bigger.

In other words, Prestige’s expenses are growing today, at the pace of its sales, but the revenue will only show up after years of construction. Until then, its reported margins will remain compressed.

In the interim, the company is buying land aggressively, often on debt — with net debt rising 41% through the year, to almost ₹11,000 crore. To its management, all that debt will, over time, pay for itself. For now, though, that’s only an assumption.

Lodha Developers

Finally, there’s Lodha: the smallest of the three, by pre-sales. It has carved out a corner for itself, though, with a portfolio concentrated almost entirely in Mumbai.

Lodha’s pre-sales, at just under ₹20,500 crore, were well below its peers — even if they were up 16% from last year. This was a little short of what the company itself expected. That, to the management, was partly because of all the volatility the Iran war had created.

By other metrics, though, the company looked rather clean. It had the lowest debt-to-equity figures of the three, at just 0.23x. Its net profit grew 24% over the year, well ahead of its peers — with EBITDA margins of 33%.

Perhaps this is why the company was asking investors to look at profits rather than pre-sales. Profits, it maintained, was the end goal. Pre-sales were simply a means to an end.

The three timelines of a developer

Why is it that three companies in the same industry, for the same time period, are pointing investors to different metrics as measures of their performance?

The answer lies in the sheer weirdness of the real estate industry.

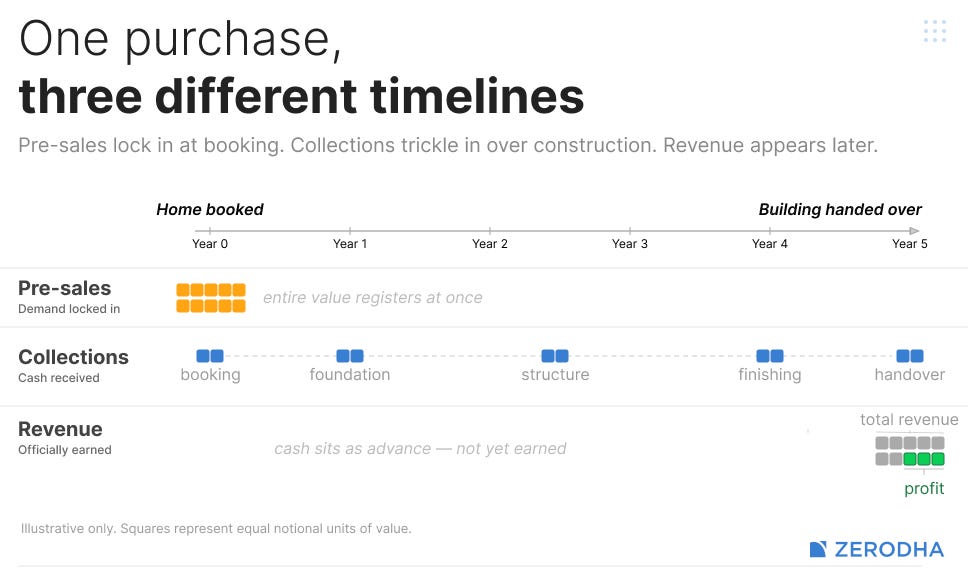

In real estate, a single purchase can play out over the course of years. When you buy a home from a major developer, chances are, you aren’t buying a finished home. You’re just buying a promise. That promise will only come through over 2-4 years of construction.

Of course, you don’t pay the entire amount for your house either, at first. You pay a small fraction when you book a house — 10-20%, perhaps — and then pay the rest in installments as the building goes up, milestone by milestone. In other words, from the point a sale is first booked, it is years before all that money actually shows up in the developer’s accounts.

As money trickles in, though, it creates another mismatch. Until a building finally comes up, a customer has paid the developer a lot of cash for what is, to that point, a paper agreement. They don’t yet have an actual house to their name. The sale has begun, but it isn’t yet complete. The developer hasn’t yet earned that cash. If, for whatever reason, a property can’t come through, they would rightfully have to return it.

Think of what that means. For years at an end, a developer has a large amount of cash in its coffers, which it is still in the process of earning. That is money, yes, but it isn’t revenue. When the company prepares its books, it has to account for that money without claiming it’s theirs.

Developers get around this weirdness with a clever bit of accounting. The actual cash in their account sits on their balance sheet as an asset. They pair it with a liability, however: accounting for it as an advance that might have to be repaid.

It is only once a project is complete and ready to be handed over (or sometimes earlier, when specific accounting milestones are met) that it turns into revenue. This moment is, in some senses, also a verdict. It is when you get a sense of how profitable a project was — how disciplined the developer ultimately was on pricing, project selection and costs.

A real estate developer, therefore, runs on three timelines at once.

First, there’s a sales timeline. This is the value of all homes a developer has promised to sell — which it shows as its “pre-sales” or “bookings” number. This measures all the demand the developer has locked in for its upcoming projects.

Then, there’s a cash timeline. Every pre-sale sets up a trickle of cash which arrives, in parts, over years. The amount of cash the company has received makes for its “collections”. That’s the actual money the company is generating today.

Finally, there’s an accounting timeline. This counts how much revenue a developer can finally book as its own. This is also when you learn how much profit all those years of development have actually yielded.

If real estate was a stable, slow-growing business, these three timelines would march together. As companies closed old projects, they would begin new ones, with a steady pipeline that turned sales into cash, and then into revenue. But Indian real estate isn’t a stable, slow-growing business. Companies have been launching, selling, and building at a pace far ahead of what revenues they recognise.

This opens the door to very different strategies.

One, a developer can chase scale. They can launch as much as possible: buying a large amount of land, turning it into a stream of new projects, and accepting that cash and revenue will follow years later. Two, it can chase profitability — building a small number of higher-margin projects, where each home brings in more profit per square foot, and discipline matters more than volume. Finally, it can chase completion — focusing on finishing what it has already sold, so that revenue and profit quickly follow bookings.

Or, more simply, it can chase pre-sales, profit margins, or revenue. Each creates a completely different financial profile. We saw a demonstration of just that in this quarter’s results.

The market gets harder

Meanwhile, the wider market is becoming harder to operate in.

A year ago, India’s residential market was a relatively easy space to operate in. Interest rates were down. Inflation was benign. Premium and luxury buyers were lining up behind new properties. It was the ideal market for a large, branded developer.

But the picture has changed since.

According to Knight Frank, home sales across India’s top eight cities, last quarter, fell about 4% from last year. Launches, meanwhile, were still climbing, outpacing sales for the fourteenth quarter in a row. In the March quarter, they outstripped sales by over 10,000 units. Increasingly, developers are sitting on ever-larger amounts of unsold inventory.

For now, prices have held up across major cities. Developers sustaining this, to some extent, through schemes and incentive programs. Perhaps that is where Godrej’s 1% campaign comes from.

At the other end, meanwhile, funding is becoming more expensive to arrange. Bond yields are rising, with the 10-year government yield crossing 7%, to the highest it has been in twenty months. The Iran war has made commodities more expensive. That, in turn, has made it more expensive to build a house, with costs rising by around 5%.

These developers may have sold thousands of crores’ worth of houses last quarter, but those houses will be built over years. The costs involved — of raising money, buying material, and more — aren’t yet clear. We’re years away from finding out how profitable they’ll be.

What does that mean for these companies? Can Godrej convert its enormous pipeline into hard assets for cheap enough? Will Prestige be able to fund its massive expansion, as margins fritter and debts rise? Will Lodha struggle to draw new buyers, in a market where sentiment might be turning?

None of these answers will be clear for a while. That’s simply the nature of the real estate cycle. But we’ll stay tuned in.

Jio and Vodafone don’t like Airtel’s new postpaid plan

On May 19, Bharti Airtel launched something it called Priority Postpaid. The pitch was that, compared to others, postpaid customers would get a faster, more stable connection especially in crowded places like concerts, markets, and at peak hours.

Three days later, Jio and Vodafone Idea told a parliamentary committee the service should be paused. Their complaint, in essence, was that this might violate India’s net neutrality rules. We’ll explain what this means eventually.

The reaction was instant. The government’s communications committee opened a probe, The Department of Telecom (DoT) is reviewing and TRAI also started asking questions.

This isn’t the first time this is happening though. In 2020, Vi launched a plan called RedX — premium speeds for premium customers, while Airtel launched Platinum. Both promised faster 4G to anyone paying above a threshold. Three days after Airtel’s launch, Jio complained to TRAI, who, within a week, froze new sign-ups. Both plans were dead in months.

Six years later, the same three companies are in a similar fight, but with different context.

Same tower, different lane

Let’s start with how a plan like Priority Postpaid works.

Priority Postpaid is structured across five plans with OTT bundles stacked on top. Existing postpaid users get the upgrade automatically. Prepaid users have to migrate to postpaid to access it.

The technology underneath is called network slicing. Every signal between your phone and the nearest cell tower travels on a chunk of “radio spectrum” that telcos bid for in government auctions. Until 5G, that spectrum was one shared pool; every user drew from the same well of their telco provider. What slicing does is partition that pool into separate, reserved lanes, each with its own guaranteed bandwidth, latency, and reliability.

For instance, say one slice is for a hospital that needs ultra-low latency. Another for a stadium where 80,000 phones are uploading at once. Another for connected cars. Another, in Airtel’s case, is for postpaid retail users.

In 4G, lanes were shared. Prioritising one class of customers meant directly slowing down everyone else. That’s what made RedX and Platinum offerings in 2020 impossible to defend. In 5G, though, the network can hold a fixed share of capacity aside for the postpaid slice even when the prepaid lane fills up. A traffic jam in one lane doesn’t slow the other down.

Slicing only works on 5G standalone — meaning the full 5G stack, built end-to-end on a brand-new 5G infra. The alternative, non-standalone, is just 5G radios bolted onto the old 4G infra. Which is also why Airtel can do this right now..

Jio has run standalone since launch in late 2022, but hasn’t ventured into consumer slicing. Airtel only finished its standalone transition in early 2026, and Priority Postpaid is its first commercial use. Vi runs mostly non-standalone, with limited standalone rollout.

Who’s saying what?

Now.Jio, the company that complained in 2020, is currently the most measured. It feels network slicing is a legitimate use of 5G capabilities, but says that retail products of this kind should be launched only after regulatory approvals, with authorities examining the technical parameters carefully. If we were to read between the lines, they don’t want to kill this idea, because they’d also want to eventually do this.

Vi, the company that violated in 2020, is now the loudest critique. Its submission calls Airtel’s plan “discriminatory” and asks for it to be put on hold pending regulatory clarity.

Airtel, the company whose Platinum plan got killed in 2020, is back doing essentially the same thing in a more sophisticated form.

It’s also worth considering where in the market each of them stands right now. Jio has the standalone infrastructure ready and wants to monetise it eventually, so it can’t condemn slicing outright. Vi can’t match Airtel’s investment and is bleeding postpaid subscribers: this move from Airtel may well take away high-value customers away from them. Airtel has the infrastructure ready and the highest-paying postpaid base in the industry; it has the most to gain from going first.

But where is this contention even coming from? It’s all about net neutrality: the principle that Internet Service Providers (ISPs) must treat all internet communications equally.

It’s a simple idea, but open to interpretations, hence the confusion.

What do the rules say?

India’s net neutrality framework came in stages. The first part came in 2016, when TRAI banned discriminatory pricing — the rule that killed Facebook’s Free Basics and Airtel Zero. Both schemes had let some apps run free for users while every other app ate into their data plan. But with the 2016 rule, telcos could no longer charge different rates for different content.

The bigger rule came next. In 2017, TRAI issued formal recommendations on net neutrality, which the DoT accepted in July 2018. The government wrote the rule into every telecom licence in the country. The rule itself was simple: internet providers couldn’t discriminate against content — no blocking, no slowing things down, no giving certain types of traffic preferential speeds.

But there were two exceptions where the rule didn’t apply. One was “reasonable traffic management“, which included handling congestion, security, and emergencies. The other was “specialised services“ — like remote surgery, critical IoT, and autonomous vehicles — which were things that genuinely couldn’t run on the regular network.

That being said, a specialised service couldn’t be a substitute for ordinary internet, and rolling one out couldn’t make ordinary internet any worse for everyone else. The exceptions, then, were just exceptions.

But in 2020, a hole opened up. That year, TRAI submitted detailed recommendations on what “traffic management” looked like and what was allowed. The DoT never adopted them. So today, India has a 2018 framework with no clarity on what counts as “reasonable traffic management” now that 5G technology actually lets a telco set aside whole network slices for paying customers.

This is the gap Airtel is operating in. Its argument is simple: net neutrality is about content, not customers. Priority Postpaid doesn’t favour Netflix over YouTube. It favours a postpaid user over a prepaid one — but once that postpaid user is on the network, every app they open is treated the same.

The strongest counter-argument is one made in the US. It says that telcos are stretching the specialised services exception into a loophole it was never designed for. The exception was meant for things that physically couldn’t work on the regular internet at scale, and not ordinary services that ran faster for high-paying customers.

In the US, the 2024 net neutrality order was clear: consumer slicing wasn’t what the exception was meant to cover. T-Mobile took the hint and kept its slicing limited to enterprise and emergency services. Singapore, meanwhile, went the other way — Singtel openly sells 5G+ Priority Passes to consumers for a few dollars at a time, no regulator pushing back.

The postpaid premium has disappeared

The technical fight is interesting, but it’s downstream of something more basic. Indian telecom has a revenue problem.

Airtel’s ARPU — the average monthly revenue per user — was ₹257 in the quarter ending March 2026, the highest in India. That’s only around $3 a month. For comparison: China’s ARPU is around ₹600; Europe’s is over ₹1,000; the US is over ₹4,300 — all many multiples of our benchmark. And our industry has spent tens of billions of dollars combined on 5G spectrum and capex since 2022, without getting adequate returns to match.

So far, ARPU has grown only by raising prepaid prices. The 2024 round of hikes pushed prepaid tariffs up by 17–20%. The problem is that this growth has run into a wall, which shows up in one number.

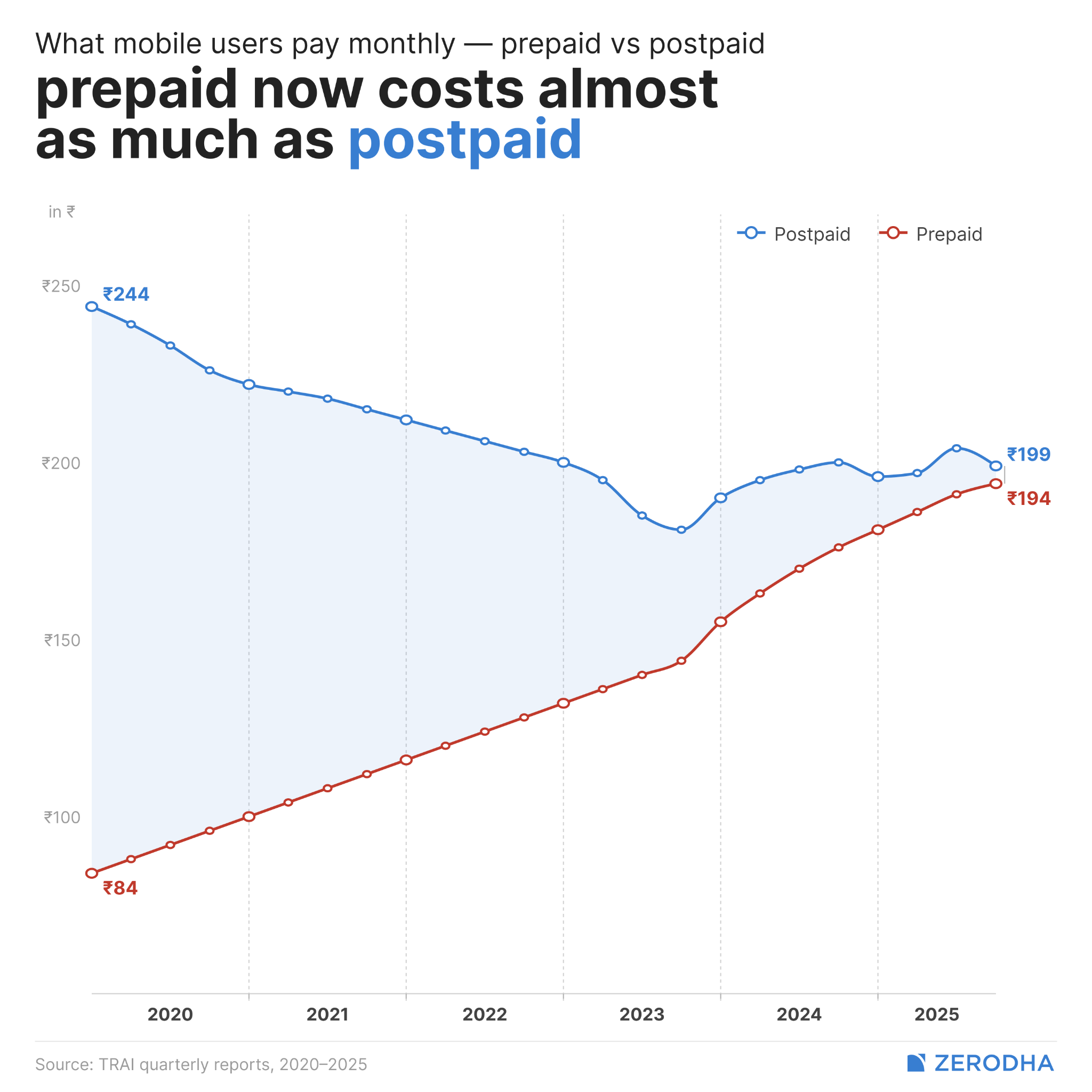

According to TRAI data, in 2020 the average monthly spend on prepaid was ₹84 and on postpaid was ₹244. A gap of ₹160. By 2025, prepaid averaged ₹194 and postpaid ₹199. A gap of ₹5. The premium that postpaid users used to pay over prepaid users has, for all practical purposes, vanished — a 97% collapse in five years.

This is weird because, well, postpaid is supposed to be the high-margin segment. At Airtel, 7-8% of customers are on postpaid but they generate 12-13% of mobility revenue. It has lower churn and longer commitments with predictable bills. Every telco wants postpaid users. But why would any prepaid user migrate today?

That’s the engine driving Priority Postpaid. Slicing may not entirely be about better network experience for the sake of it. It certainly also provides another reason for the postpaid premium to exist again by giving the postpaid user something a prepaid user will find it hard to have, no matter how much they recharge for. Then, you sell migration from prepaid to postpaid.

The numbers work out the way Airtel needs them to. The cheapest Priority Postpaid plan is ₹449 a month. A prepaid user spending around ₹300 a month who migrates pays roughly 50% more. Multiply that across the conversions Airtel projects, and you have the next leg of ARPU growth without needing another politically painful prepaid hike.

What makes this an irresistible move commercially is that the 5G standalone network is already built. The slicing capability is just software running on top of it. Moving a user from the regular slice to the priority slice is essentially going to cost zero. Almost the entire monthly uplift from a prepaid-to-postpaid conversion flows straight through to operating profit.

Questions without answers

Airtel’s strongest defence is also its weakest. Its submission tells the parliamentary committee that the 5G network is currently running at only 38% of its capacity. Postpaid users account for just 4% of that load. Even after Priority Postpaid pushes postpaid up to maybe 6%, there’s still around 60% spare capacity for everyone else. So no one is being slowed down.

That’s true today, but will it be true at scale? We can’t say for sure. The 2020 TRAI objection to RedX and Platinum was never about immediate slowdowns. It was about what happens when the network loads up. As more Indians shift to 5G and data usage keeps climbing, that 60% spare capacity shrinks.

At some point, keeping a guaranteed lane for postpaid has to come from somewhere. It’ll show up as everyone else’s spectrum being taken away for priority customers.

Another claim from Airtel is that since prepaid customers earn them most of their revenue, they have no incentive to harm those customers. The intent of Priority Postpaid isn’t to make prepaid worse, but to make postpaid visibly better, so that high-value prepaid users migrate. If migration works as designed, average prepaid quality doesn’t have to fall for the strategy to pay off.

The DoT now has two decisions to make. Is customer-tier prioritisation, like what Airtel is doing, a net neutrality issue at all, or not?

Does retail consumer slicing qualify as a “specialised service” which is technically allowed under the law, or is that stretching the legal limits of the definition?

How DoT lands on these decides more than whether Airtel keeps Priority Postpaid. It decides what kind of internet 95% of Indians get to use for the next decade, and more importantly, will telco operators able to increase their ARPU, or will have to get more creative in trying to achieve that.

Tidbits

[1] Byju’s founder sentenced to six months in Singapore jail

A Singapore court has sentenced Byju’s founder Byju Raveendran to six months in jail for contempt of court, saying he failed to comply with multiple orders related to his assets. The ruling adds to mounting legal pressure as global investors and lenders pursue recovery claims linked to the edtech firm’s collapse.

Source: Economic Times

[2] Extreme weather devastates India’s Alphonso mango crop

Maharashtra’s prized Alphonso mango crop has suffered losses of 85–90% in key growing regions due to extreme heat and El Niño-linked weather disruptions. Export demand has also weakened amid the Iran conflict, hurting farmers, traders, and businesses linked to the mango supply chain.

Source: Reuters

[3] SEBI plans pilot for tokenised corporate bond trading

SEBI will launch a pilot project to test tokenisation of corporate bonds using distributed ledger technology (DLT), with rollout expected in 6–9 months. The regulator believes tokenisation could improve liquidity and enable faster, more automated settlements in India’s corporate bond market.

Source: The Hindu

- This edition of the newsletter was written by Pranav and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Rosa & Tamoghna on India’s Youth Employment Crisis

In India, the more educated you are, the more likely you are to be unemployed. Graduate unemployment among the youth sits at 40%. For those with no education, it’s 3%. We recently spoke to Rosa Abraham and Dr. Tamoghna Halder, two of the authors behind the Azim Premji University’s State of Working India 2026 report, to understand why. Our conversation goes into what’s really driving this paradox — the role of caste and social signalling in education choices, whether waiting for a good job is rational, why the “missing middle” of Indian firms matters, and what the demographic dividend window really means for policy. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉