One event that changed Reliance’s year

Energy tanks, but consumer businesses soar

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Almost a good quarter for Reliance

When the gas markets broke

Almost a good quarter for Reliance

Reliance, India’s biggest company, released its results last week. For anyone that wants a quick snapshot of the economy, Reliance is a quick, dirty way of checking its pulse — because of how much of the economy it touches. From the fuel in your car, to the data on your phone, to the groceries you might cook with, it’s hard to go a day without bumping into something Reliance sells.

For most of last year, the company’s results looked brilliant. Then, March hit. West Asia erupted in war, and the company’s fate changed. Its largest and oldest revenue-generating segment i.e. Oil to Chemicals, or O2C, took a massive hit this quarter because of the war. That alone was enough to pull down the company’s profitability.

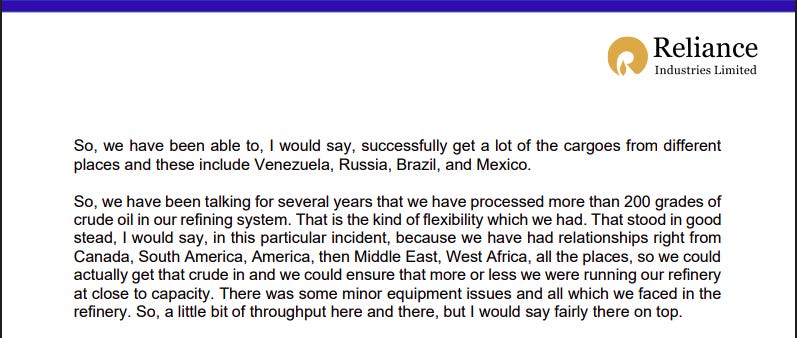

It wasn’t a terrible quarter, still. The company’s revenue actually rose 13% to ₹3.25 lakh crore. It couldn’t earn profits at nearly the same rate, though. Its EBITDA — the money it generates from core operations — fell marginally, while net profit fell 9%.

That’s unusual, isn’t it? Why did the company’s revenue go up while its profits went down? That, too, traces itself to the Hormuz crisis. When oil prices spiked after the Strait of Hormuz was effectively blocked in March, the products Reliance sells became more expensive, pushing revenue up. But the cost of everything that goes into making those products — crude oil, shipping, insurance — spiked even harder, eating into margins.

That’s the story of this quarter.

Refining under stress

Reliance operates one of the world’s largest refinery complexes at Jamnagar. It normally sources nearly half of its crude from the Middle East. When the Strait was blocked, though, that stopped being an option. From 20 million barrels a day, the amount of oil flowing out of the region fell to 4 million barrels, Prices went wild. Dubai crude hit $168 a barrel. Then, QatarEnergy declared force majeure on its entire 77 million ton LNG operation, after its units were struck.

Suddenly, Reliance had to scramble.

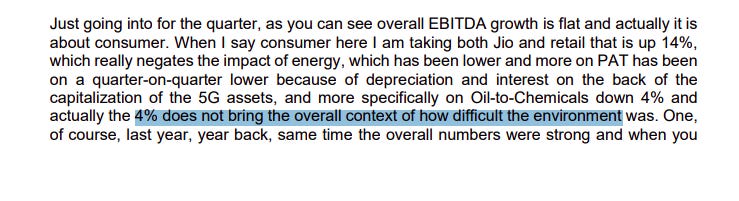

The company had a secret trump card: the Jamnagar refinery could work with any feedstock at all. It could process over 200 grades of crude, and it put that ability to work — sourcing crude from Venezuela, Russia, Brazil, and Mexico.

Of course, flexibility alone wasn’t enough to completely replace supplies, given the sheer scale of the disruption the company faced. Its throughput, as a result, fell by 4%. Meanwhile, the barrels they did process came at enormous costs. Each barrel could cost a premium of as much as $40 above the benchmark. Freight rates, too, surged to 10-15 times normal. Insurance on tankers went from thousands to millions of dollars.

If you didn’t know any better, you would think this would have been a historic quarter. After all, “gasoil cracks” — or the difference between their raw material (crude) and their output (gasoil) — was at $35.4 per barrel. That was up 148% year-on-year.

Only, this wasn’t the sort of environment where one could actually capture those margins. The real cost of crude was far above the benchmark the cracks are measured against.

On top of all that, three other things hit margins:

First, domestic fuel prices haven’t been raised. Jio-BP found themselves selling petrol and diesel at government-controlled prices, even when they were themselves buying crude at $168. Their volumes grew 27% over this period — which in normal times would be great — but at a time like this, it just deepened the loss on every liter.

Second, the government brought back the Special Additional Excise Duty on diesel exports, effective March 27. This was a tax on the sorts of windfall profits Indian refiners earned in the early years of the Ukraine war. This had been wound down to zero, but it was now revived because export margins, at least on paper, looked enormous.

Third, Reliance diverted propane and butane from its petrochemical operations to make domestic LPG — quadrupling supply — because India couldn’t import LPG through the Strait. That’s a national service obligation, but it directly hit their downstream chemical output.

All of this meant that, ultimately, Reliance’s O2C EBITDA fell 3.7%. You can read that as either disappointing or remarkably resilient, depending on how you expected them to handle the current state of the world.

This was upstream. Downstream, the chemicals’ picture was equally rough.

Take plastics. The Middle East accounts for 13% of the world’s ethylene capacity — which is the main raw material that goes into making plastics. It also supplies a quarter of the world’s commodity chemicals. Asia’s entire petrochemicals industry is married to the region’s supply chains, and as those broke, crackers across Asia slashed utilization from 80% to 50-60%. Reliance, thankfully, was relatively insulated from this trend. 75% of its ethylene comes from US ethane, not naphtha. But its polymer margins were still weak, as PVC demand fell 10%.

The concern isn’t Reliance’s financials specifically, however. Those chemicals directly touch important parts of the economy. The company’s management flagged something that goes well beyond its own P&L. In its words, “The biggest impact has been on methanol, which will hit the fertilizer sector.” That is a dangerous development. If it persists into the kharif season, we might soon be asking questions around food security.

There was a final hit Reliance took. Its upstream KG-D6 gas field — the deepwater block off India’s east coast — saw its EBITDA fall 18% as volumes declined from natural reservoir depletion. Meanwhile, the government redirected gas to priority sectors during the crisis, capping the prices they could charge.

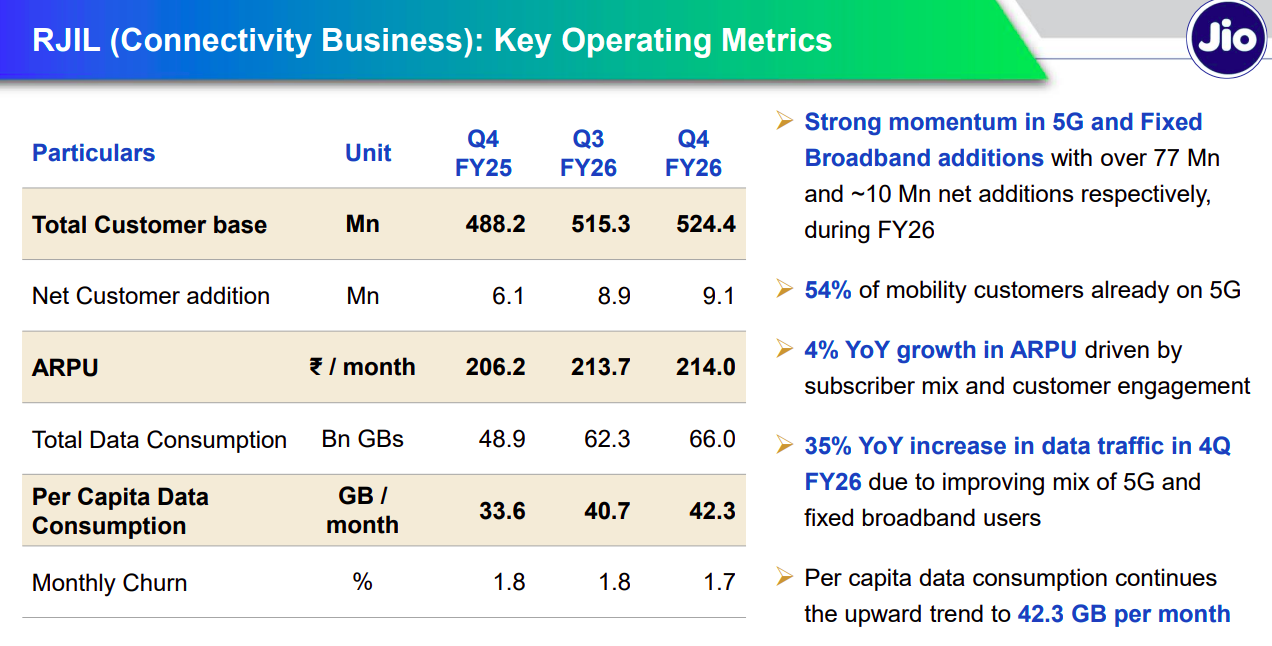

Jio keeps compounding

The good thing about being a conglomerate, though, is that your other businesses can make up for a nightmare quarter in one segment.

One of those was telecom. Jio ended Q4 with 524 million subscribers, 268 million of whom were on 5G alone. That pushed its revenue up 11% — while its EBITDA was up 16% with good margin expansion. That’s remarkable, given that there wasn’t even a tariff hike this year. People were simply spending more on its services. The company’s average revenue per user (ARPU) grew 4% to ₹214 purely from people upgrading plans and consuming more data — which hit 42.3 GB per capita per month.

This expansion was driven, in part, by home internet connections. Jio now has 27 million fixed broadband connections. AirFiber — which uses the 5G network to deliver home internet without laying fiber — drove 75% of those additions. As the company claimed, it added 25,000 to 30,000 — and sometimes as many as 50,000 to 60,000 — homes every single day day.

There’s a catch to those headline numbers, though.

Jio bought its 5G spectrum back in 2022. But the costs of that purchase — the installment payments, the wear-and-tear charges on the network equipment — only start showing up in the books once the network is fully up and running. That’s happening now. Those costs are all hitting Reliance’s books. So even though Jio’s core business grew EBITDA 18% for the year, its actual profit grew only 13%.

The gap between the two is the cost of having built a 5G network. It’s not going away anytime soon

Retail: growing the pie, compressing the margin

Reliance Retail posted a record Q4 revenue, at roughly ₹98,000 crore. This was up 11% from last year, or 14% once you adjust for its FMCG business being demerged into a separate entity.

But interestingly, the EBITDA margin fell to 7.9% from 8.5% a year ago. The reason, it appears, is quick commerce. Reliance has been aggressively scaling hyper-local delivery. Its orders from the segment grew 300% year-on-year. That kind of rapid build-out costs money, however. The more you grow such a business in the short term, the more it drags on overall margins

Reliance’s quick commerce model is fundamentally different from the likes of Blinkit and Zepto. It doesn’t build dedicated dark stores. It turns its 20,000+ existing retail stores into delivery hubs. Meanwhile, its 682 electronics stores and 1,700+ fashion stores now offer two-hour delivery. So, they aren’t selling from a dark store with a few hundred SKUs, but from actual Reliance Digital and Trends stores carrying thousands of products.

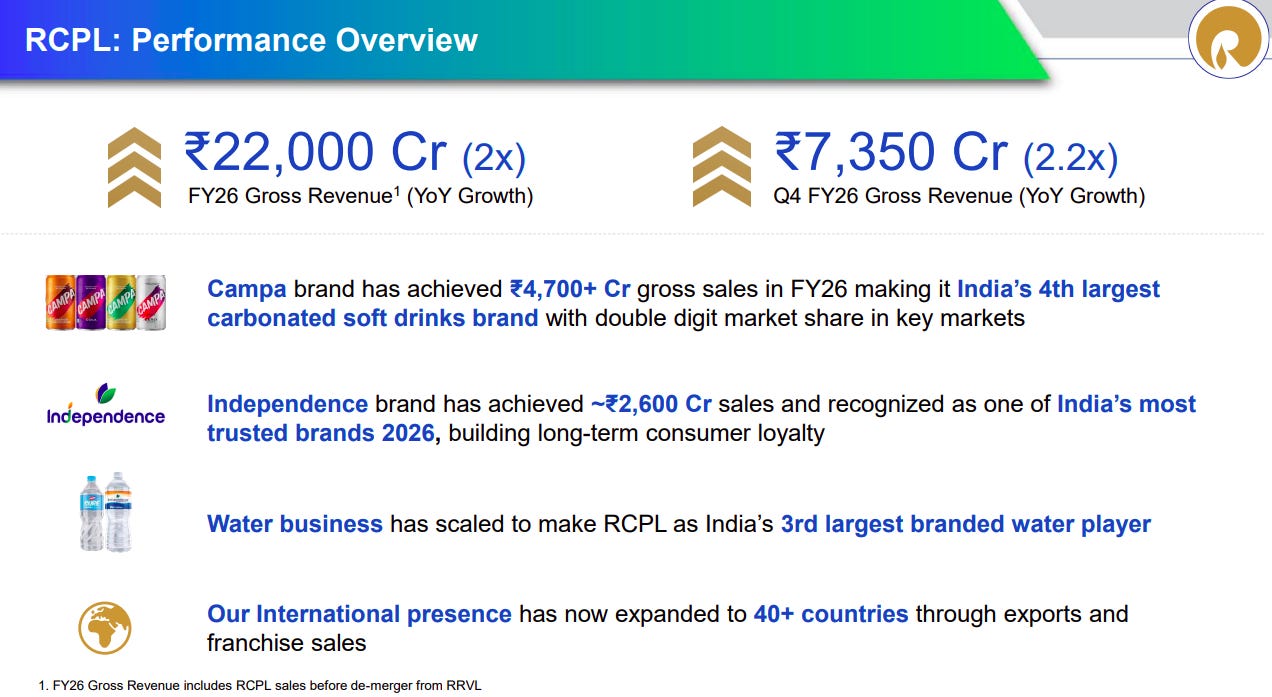

On the FMCG side, meanwhile, RCPL posted ₹22,000 crore in FY26 revenue — roughly double the prior year. The sector’s champion was Campa Cola. The drinks brand earned ₹4,700 crore in these three months, making it India’s fourth-largest carbonated soft drink brand. We’ve written about the Campa story before. In all, the company’s overall beverages category exceeded ₹6,000 crore.

Jio Star and the streaming scale

Reliance’s media business hit 550 million monthly active users in March.

This was led by marquee cricketing events. During the T20 World Cup, Jio Hotstar broke the global concurrent streaming record at 72.5 million simultaneous viewers. The IPL 2026 opening weekend, meanwhile, was the largest ever.

Arguably, however, none of this beat its media arm’s biggest success — Dhurandhar. The franchise crossed ₹3,000 crore worldwide, with both films topping ₹1,000 crore each. This arguably makes Jio Studios India’s largest content studio.

In all, on the content side, the company’s Q4 media revenue was ₹8,372 crore. This was led by digital ad revenue, which hit a record, though TV entertainment ad revenue stayed weak from FMCG spend cuts.

The new energy timeline problem

If there’s one tricky corner of Reliance’s portfolio, it’s the new energy vertical.

In October 2025, management said polysilicon commissioning was “one to two quarters” away. In January 2026, they said all factories — polysilicon, ingot, wafer, glass — would be commissioned “during the current year.”

That timeline, though, appears to be slipping. In April 2026, after FY26 has ended, they’re still targeting “the next few quarters.”

This isn’t to say the company has nothing to show. It already has lines fot Solar PV modules and cells are done. But upstream integration — the key that makes this a fully self-sufficient solar manufacturing operation — is not.

The company has plans that will stretch for years. It’s setting up battery manufacturing, targetting 100 GWh, with a 40 GWh first phase. Its Samsung C&T green ammonia contract — a massive $3 billion deal for 15 years, will start in 2029. But that is three years away. With a pattern of missed timelines, it’s hard to know how to assess these plans.

Conclusion

There are many benefits to being India’s largest company. One of them is that no matter what the world looks like, some parts of your business will always thrive. This time around, it’s Reliance’s consumer businesses — Jio, Retail, FMCG — that are all growing well. More than 55% of the company’s EBITDA now comes from these businesses. In a quarter where the energy side was getting hammered from every direction, they held the whole thing together.

That doesn’t, however, take away from the company’s concerns.

O2C is still its single largest revenue segment. It’s an industry with national importance — after all, India still imports over 85% of its crude. Even if all its businesses have a stand-out quarter, this one segment still looms large for Reliance’s fortunes.

When the gas markets broke

We’ve been covering reports from the International Energy Agency for a while, here at The Daily Brief. These used to be rather unexciting, as things went: a few countries were seeing their demands rise, others were investing in supply, and this would all become relevant, perhaps, ten years from now — as these forces collided at their glacial pace.

We never thought these reports could become the site of intense drama.

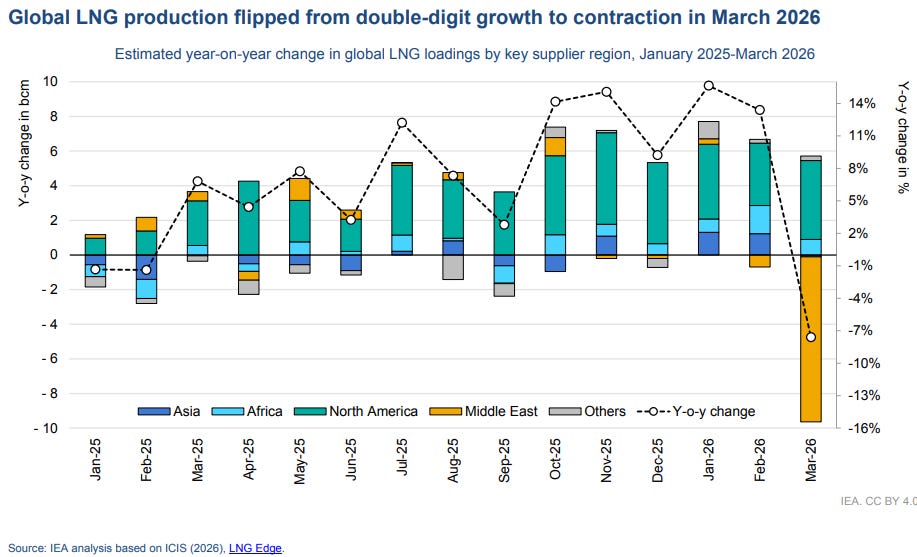

But that’s the world we live in, now. The IEA just released its Gas Market Report for this quarter. It’s a picture of chaos. The West Asian war has thrown the world’s energy markets into a topsy-turvy spin. All assumptions are now off; all projections have been torn asunder. Before the war, the world expected to see a massive “LNG wave”; fundamentals, alone, were supposed to push countries to massively ramp up how much natural gas they used. That story is now effectively dead — at least for the next couple of years, if not longer.

Instead, the big question is: how long must we wait before we can start re-building?

A market that was working

To understand just how wrong things have gone, you need to see how different we thought things would be, going in.

Three years after Russia’s invasion of Ukraine had sent prices sky-rocketing, the world’s gas markets were finally making a recovery. Supply was catching up with demand. Prices were settling down through the second half of 2025, and into 2026.

New liquefied natural gas plants were coming online, one after another. Last year, the United States opened a new liquefaction and export terminal in Plaquemines in Louisiana. Soon afterwards, LNG Canada began production out of two new LNG export terminals on Canada’s West coast. In February this year, then, America’s Corpus Christi export facility in Texas saw a massive expansion. The gas was well and truly beginning to flow.

Some of these projects were massive. Nearly half of all the new LNG that arrived on global markets between October and February came from the Plaquemines plant alone.

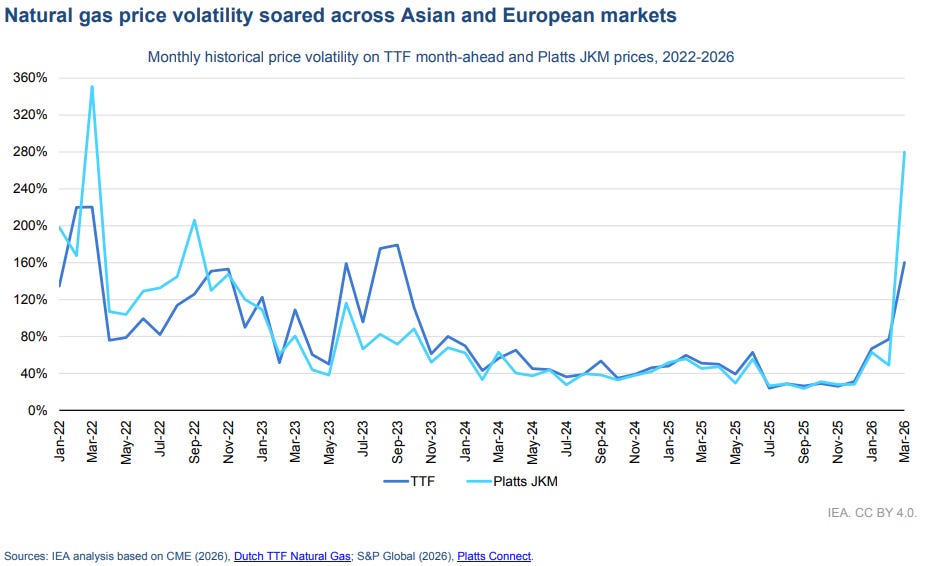

This expansion was pulling prices down. By early 2026, European gas was trading roughly a quarter cheaper than the year before. Asian prices had fallen even more.

As prices came under control, demand followed. After years of suppression — a response to the crisis that the Ukraine war kicked off — gas use was creeping up across Asia. Europe, too, was returning to natural gas. By the winter of 2025, LNG made for over 40% of all the gas the continent burned, up from a third the year before. The IEA, back then, had projected that global gas demand would grow by 2% across 2026.

This, it seemed, foretold a coming “wave”. Enormous new projects would keep coming up in the coming years. Qatar, alone, would add 70 billion cubic metres of new capacity.

Buyers across Asia and Europe were waiting to absorb this capacity. India was one of them. We had been short of cheap LNG for many years, by this point. Indian industry had been quietly switching out of gas — moving to naphtha, fuel oil, even diesel — because gas had become too expensive. But the drought was getting over, and we would soon join the market.

Then the wave broke.

The break

The Strait of Hormuz effectively closed on March 2.

We’ve probably written about those 33 kilometers more than any geographical feature on earth. The same thin sliver of water was also the main route for all the natural gas exports coming out of Qatar and UAE — which, together, were responsible for roughly a fifth of all the LNG sold on the planet. When the strait closed, the floor fell off the bottom of that supply.

Prices shot up instantly. By March, gas in Europe was trading at $18 per million British thermal units, the highest monthly average since the worst of the Ukraine war. In Asia, spot prices climbed to nearly $21 — nearly twice the $11 industrial users were paying under long-term contracts. If you had made your plans based on those long-term prices, they were effectively ruined.

Meanwhile, the volatility in the markets went wild. According to the IEA, European gas markets were swinging at their most disorderly pace since autumn 2023. In Asia, the last time they had been this wild was the chaos of early 2022, in the very first weeks of Russia’s invasion.

As one supply route was choked, all the markets that relied on it — India, Pakistan, China, Bangladesh — scrambled for alternatives. Those lost cargoes, after all, had to come from elsewhere. Asian buyers ended up sourcing roughly thrice as much LNG from North America in March as they had just a year ago. From West Africa, they bought more than six times as much.

Every ship from those distant ports, meanwhile, had to travel much farther. This pushed up shipping costs. Rates for LNG carriers roughly tripled in early March, the steepest day-on-day jump on record.

Different countries were differently positioned to absorb the damage. China’s LNG imports, for instance, fell by one-third. India’s by a sixth. Meanwhile, Pakistan, which relied on Qatar for nearly all of its LNG, saw imports collapse by around 70%. Everyone relying on that gas — power plants, fertilizer factories, even entire industrial estates — was suddenly shuttered.

The ceasefire has done little to quell the issue. The strait is still not open. Iran is now charging tolls of more than a million dollars per ship, while the United States has imposed a counter-blockade on Iranian ports. The hot war may have cooled, but the chokehold on global energy has not.

Why the market won’t snap back

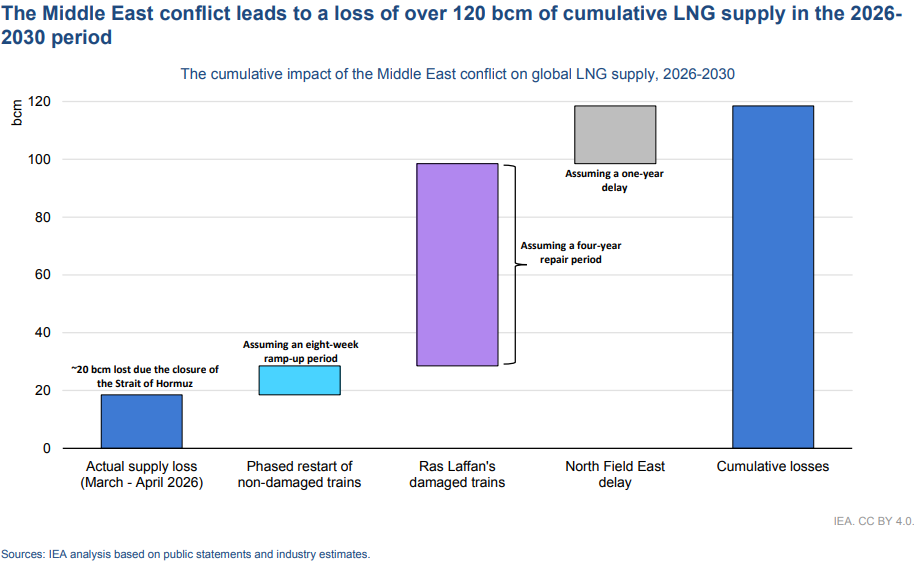

Ras Laffan is the world’s largest LNG export terminal. It has fourteen “liquefaction trains” — the giant industrial systems that take natural gas, supercool it until it’s liquid, and load it onto ships. On the night of 18 March, two of those trains were damaged in Iranian missile strikes.

Qatar supplies roughly a sixth of the world’s LNG. With those drone attacks, almost a fifth of that capacity was destroyed. According to QatarEnergy, the repairs will take three to five years.

It’s hard to rush this. The equipment that goes into an LNG plant is enormously specialized. You can’t order a replacement gas turbine off-the-shelf.

Before the war, Qatar had been preparing the largest expansion of LNG capacity in the country’s history — a project called North Field East, with 44 billion cubic metres a year of new capacity. It was scheduled to start coming online in the second half of this year. Construction has been suspended for now, however, and that timeline has slipped by more than a year. A second project, North Field South, was supposed to follow in 2028. There are no longer any public timelines for it.

All of this is to say: even if the war stops today, and the strait opens immediately, the gas market won’t simply return to normal. When you add up all the damage of the war — the damaged units, the lost production, the delayed expansions — the IEA estimates that the war effectively destroyed around 120 billion cubic metres of LNG supply between 2026 and 2030. Roughly 15% of the new LNG the world had been anticipating, as part of the supposed LNG “wave”, is gone.

The IEA frames this tactfully: the crisis, to them, has delayed the LNG wave by two years. The reality, arguably, is that any medium-term energy outlook has simply broken down. The wave was based on an assumption: that there would be enough new LNG by the end of this decade that it would finally be enough for the developing world to leap ahead. That world may well be outside our reach.

How the world is reorganising

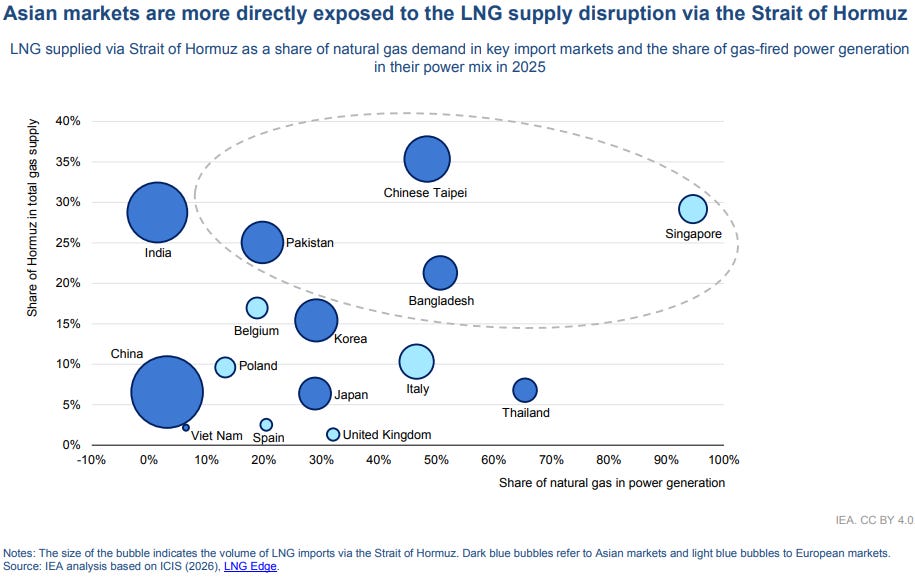

The Hormuz crisis may have sent gas prices up across the world, but it didn’t affect the whole world in the same way. The countries that were the most dependent on supplies from the Persian Gulf were those that, when the Strait was shut, were hit hardest. India, for instance, sourced roughly nearly 30% of all its gas, and 60% of its total imports, through the Strait of Hormuz. Others in our neighbourhood were struck even worse. Pakistan, for instance, imported all its LNG from Qatar alone. Bangladesh imported about 60% of its LNG via the strait.

Europe, in contrast, got less than 3% of its gas from the strait.

This asymmetry was why the crisis was felt, the most deeply, in our corner of the world.

India’s case is interesting. India’s largest LNG buyers — Petronet, GAIL — get most of their gas through long-term contracts with Qatar. Once that supply was frustrated, our only option was to shift to the spot market. Here, prices were three or four times what we paid under existing contracts. We were big enough to matter, exposed enough to feel the shock, and yet, we lacked the ability to simply absorb high prices. We couldn’t simply buy out the supply in other markets. The price was too high to clear. Our only option was to manage the chaos.

That’s what we did. In early March, the government invoked the Essential Commodities Act of 1955 — a law most commonly applied for food shortages — to ration gas. With this, while some users were still allowed unrestricted access to gas, others saw their quotas chopped. Industrial users, for instance, saw their gas supply fall by 10 to 30%.

Our gas markets had been liberalising for the better part of two decades. The crisis, though, sent us right back into command-and-control mode, where the government decided which sectors get gas and which don’t.

Others responded in their own ways. Pakistan introduced a four-day work week to cut industrial gas use. Bangladesh cut supplies to fertilizer plants and power stations. Thailand ordered two decommissioned coal-fired power units to restart. Japan and Korea, too, lifted operational restrictions on coal-fired power. Across Asia, in fact, annual gas use in the power sector could drop by 60 to 65 billion cubic metres.

That is, as prices went up, everyone didn’t mechanically pay a higher price. They made choices on what to give up.

How long, then?

Which brings us back to the question we started with: how long is it before gas markets return to normal?

The honest answer is years. Even if the war ends immediately, the damage it caused will take years to undo. The repairs alone will take years. All the expansion projects that were to come up shortly will now be pushed out.

Three years ago, when Russia cut off Europe’s gas, rich countries took the hit. They immediately bid up prices, paid whatever they had to pay, and absorbed the hit. This time, the worst of the shock has fallen on a different part of the world, where countries can’t simply outbid their way through.

Where Europe paid, we have to ration.

Tidbits

[1] India’s industrial growth slows sharply in March

India’s IIP growth likely slowed to ~2% in March, down from 5.2% in February, hit by weak manufacturing and energy output. Higher input costs, supply disruptions, and softer exports dragged activity, though government capex and infrastructure demand remain supportive.

Source: BusinessLine

[2] India–New Zealand FTA to boost trade and investment

India and New Zealand will sign a free trade pact on April 27, aiming to double trade to $5 billion and attract $20 billion investment over 15 years. The deal gives duty-free access for Indian exports while protecting sensitive sectors like dairy.

Source: BusinessLine

[3] Sun Pharma to buy Organon in $11.75 bn mega deal

Sun Pharma will acquire US-based Organon for $11.75 billion, marking India’s largest pharma deal. The move will boost Sun’s scale, expand its specialty drugs and women’s health portfolio, and nearly double revenue with strong margins.

Source: Reuters

- This edition of the newsletter was written by Aakanksha, Krishna and Pranav.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

How can Indian IT flip the AI script ft. Ameya P

The age of AI agents has, so far, been a thorn on Indian IT’s side, at least as far as valuations are concerned. Its business model is getting stale each passing day - that’s understood. There might be a possibility that Indian IT might just adapt to the new paradigm. But what does adaptation for Indian IT look like? What are the forms of inertia they will have to overcome to successfully change themselves? And even if they do adapt, will they be able to defend their new business?

To unpack all this, we spoke to Ameya P, a veteran in the global IT industry, and a prolific technology investor well-known for his investing takes on X. It’s an incredibly nuanced conversation from an expert who understands the nitty-gritties of what each AI development brings forth for this industry.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉