Margin crush in a gold rush

Q4 at the jewellery business

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Three colours of gold: Q4 at India’s biggest jewellers

SEBI wants to make municipal bonds great

Three colours of gold: Q4 at India’s biggest jewellers

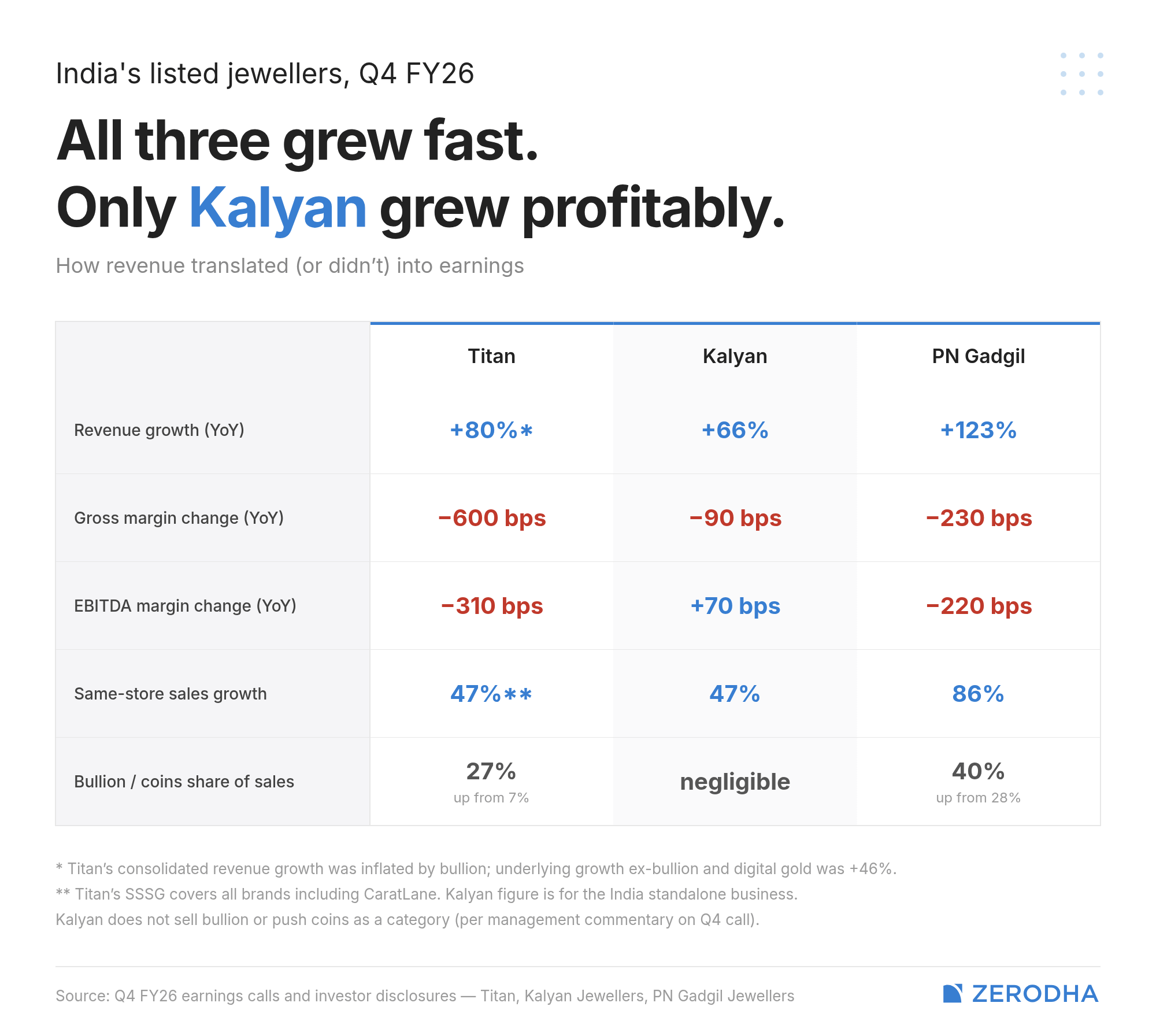

On paper, the March quarter was a roaring one for Indian jewellery. Titan, the largest of the country’s listed players, saw its consolidated income grow by 80% over the same quarter a year earlier. Kalyan grew at 66%. PN Gadgil more than doubled its revenue. If you thought high gold prices would make jewellery harder to sell, surprise! All three of these companies’ sales figures were better than ever!

Or maybe not. Peek underneath the revenue figure, and you see the three companies pull away from each other. Titan saw its gross margin absolutely crater, by 600 basis points. The gross margins of PN Gadgil, too, took a beating of 230 basis points. Kalyan, on the other hand, managed to defend its numbers. The three companies may have shared the same business conditions, but their businesses told three completely different stories.

That divergence is interesting. It shows us how different these companies actually are, in a way that a calmer quarter would have hidden. Those differences will only matter more, going ahead, now that the government has more than doubled import duties on both gold and silver.

What each of them reported

Going by absolute scale alone, Titan had a wild quarter. Its consolidated total income was around ₹27,100 crore — up 80% year-on-year. Some of that came from bullion and digital gold. Even if you strip that out, though, its underlying income came to ₹20,300 crore — still up 46%. Its net profit, at almost ₹1,180 crore, was up 35%.

But this wasn’t a normal quarter by any means. For one, Titan’s bullion business has become enormous. Consider this: standalone bullion sales went from ₹860 crore in Q4 last year to ₹6,140 crore this quarter — a growth of over 7x in a single year. Bullion made over a quarter of Titan’s standalone jewellery revenue this year, in fact. That shift came with a terrible price: bullion carries almost no margin, and as Titan ramped up bullion sales, its gross margins collapsed by a full 600 basis points from a year earlier.

That said, its jewellery business held its own, with operating profits reaching ₹1,820 crores — ~37% better than last year. But the sort of jewellery it sold shifted slightly, with its share of studded jewellery slipping from 34% to 31%.

PN Gadgil grew even faster. Its consolidated revenue for the quarter, at over ₹3,500 crore, was up 123% for the year. Meanwhile, its net profit came to ₹90 crore, up 46% year-on-year. And yet, the market didn’t take to its results kindly, falling on the day the results came out.

The problem was its margins: the company’s gross margin dropped from 12% a year earlier to 9.7% — a 230-basis-point compression within a year. In fact, as recently as the December quarter, the company made a profit of ₹171 crore — nearly twice what it did last quarter — despite lower revenues. The miss was serious enough, in fact, that PNG filed a separate clarification with the stock exchanges the day after it released its results, specifically detailing why its margins collapsed so much.

The cleanest quarter of the three belonged to Kalyan. Its consolidated revenue was up nearly ₹10,300 crore — up 66% over the same quarter last year. Its net profit, at ₹410 crore, more than doubled from last year.

What sets it apart, though, was that its margins, unlike its two peers, were stable: in fact, its EBITDA margins grew from 6.5% to 7.2%. Individual stores of the company, on average, grew phenomenally well — with same-store sales growth going up 47% over the last year. Most of this growth came from outside south India, and its non-south stores now make up three-fifths of its business: a major shift for a company that built itself in Kerala.

Peering behind the results

This quarter was, in short, one of divergence. There was something structurally different about these three businesses, which pushed their numbers in very different directions. Dig deeper there, and a more interesting picture emerges.

Three businesses under one roof

Jewellery retail isn’t really one business. It is three.

A jeweller usually makes no profit on the gold they sell. The gold they use flows through them roughly at cost — what they buy at market rate, they sell at market rate. Their money comes from how they change the gold in between.

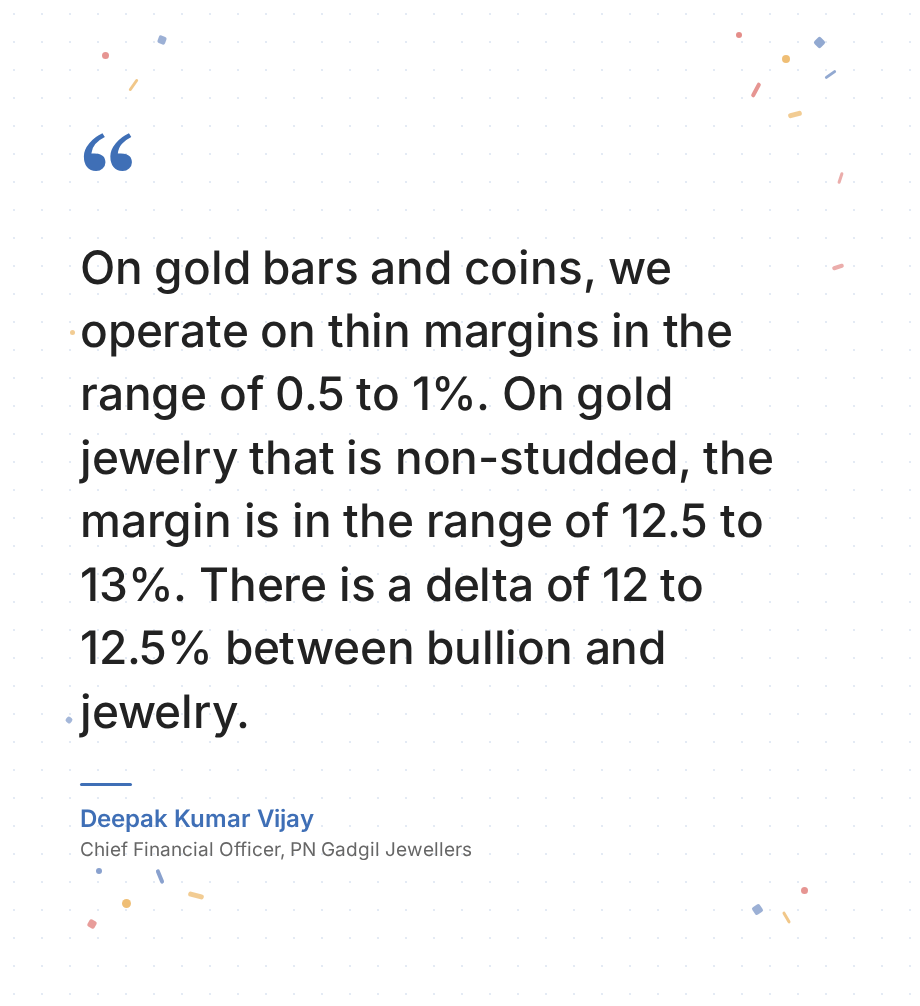

A jeweller can simply sell bars and coins, but the economics are brutal. A customer pays close to the spot price, leaving the retailer a spread of half a percent to maybe one percent. That’s all they get: there is no craftsmanship to charge for, no design, and therefore, no making charges. They’re essentially a bullion intermediary.

One layer above, a jeweller can sell plain gold jewellery — unadorned chains, plain bangles, simple necklaces, and the like. This adds extra making charges of roughly 6 to 15% of gold value. They also get to pocket a brand premium, plus a wastage allowance. In all, the gross margin here lands in the 12 to 13% range.

Finally, there’s studded jewellery: pieces with diamonds or other stones. The diamond carries its own mark-up markup, the gold component still earns its making charges, and the design premium is highest of all. Gross margins on a heavily-studded mix can run as high as the mid-thirties.

The three, in other words, are functionally different businesses, with very different dynamics. If you know which of these a jeweller sells, in what quantity, their margins become much easier to understand.

Last quarter, PN Gadgil’s bullion sales, for instance, went up from 28% of revenue to 40%. In each rupee of revenue, in that added share, its margins dropped from ~12% to practically nothing. Titan, too, saw a similar compression. Their lower margins flow almost mechanically from that shift.

But why did the mix shift so drastically?

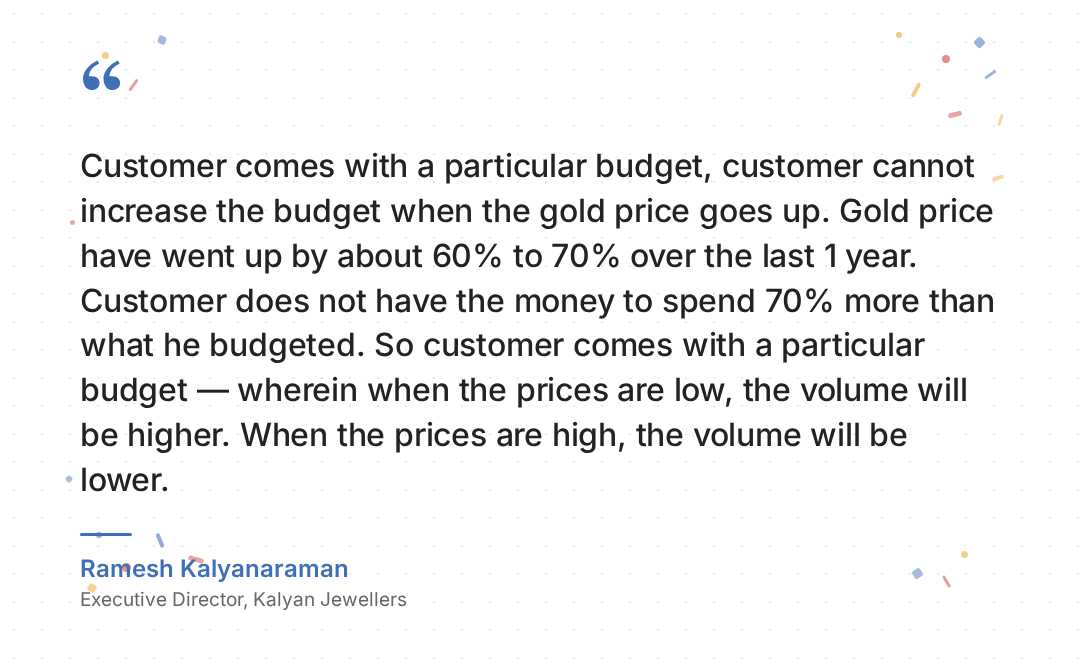

Well, when gold prices rise sharply, customers react very differently. As Kalyan’s management noted, they don’t expand their budgets when gold gets expensive. Instead, they shift downwards. They try to maintain the amount of gold they’re actually acquiring, while cutting down what they pay for design. A customer who came to buy a chain, for instance, might leave with a coin instead.

In a quarter where gold prices went up 60%, this was visible across the board. The question before each company, then, was whether they would lean into the trend or not.

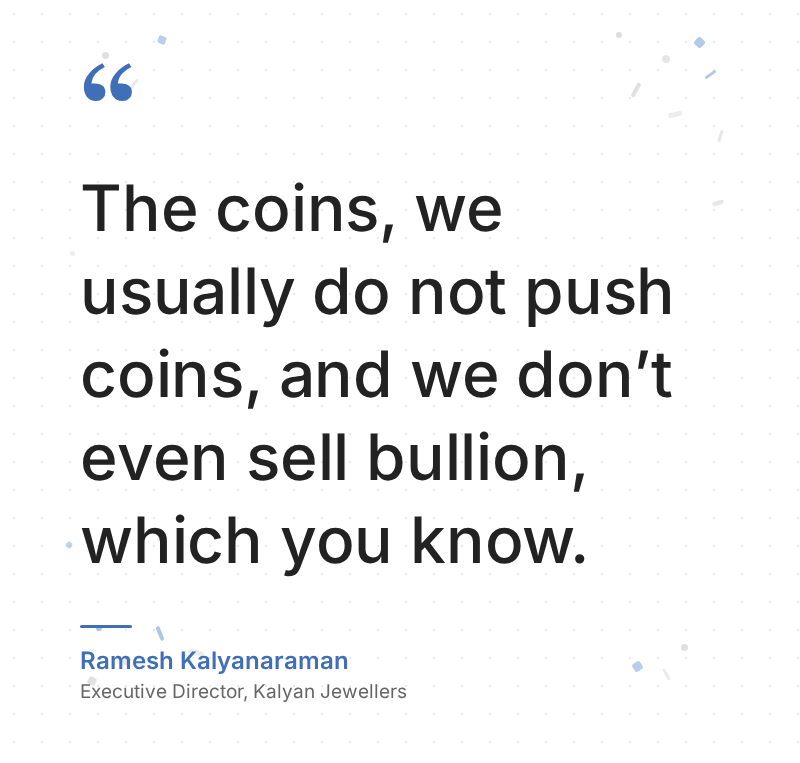

Titan and PN Gadgil chased the trend, letting their bullion sales rise massively. Kalyan — as its management clarified — did not. In fact, Kalyan held on to its high-margin studded jewellery business for dear life. Its studded share stayed essentially flat at 31.2%, while Titan’s slipped from 34% to 31%. While we don’t have year-on-year figures for PN Gadgil, sequentially, its studded ratio fell from 8.2% in the December quarter to 7.3% last quarter.

That made all the difference.

How the gold actually gets in

That’s the demand side of the story. But there’s a second thing going on at the same time: the way Indian jewellery is sourced is being rewired.

A jeweller can get gold three ways. They can import it via banks, paying customs duty, GST, and dealing with FX rates. They can borrow it via a Gold Metal Loan, where a bank lends physical gold for six to nine months, at a much lower interest rate than a rupee loan. Or they can buy it from customers, through an old-gold exchange programme. The last of these — the exchange channel — is always the cheapest.

Each of these treats gold exchange differently.

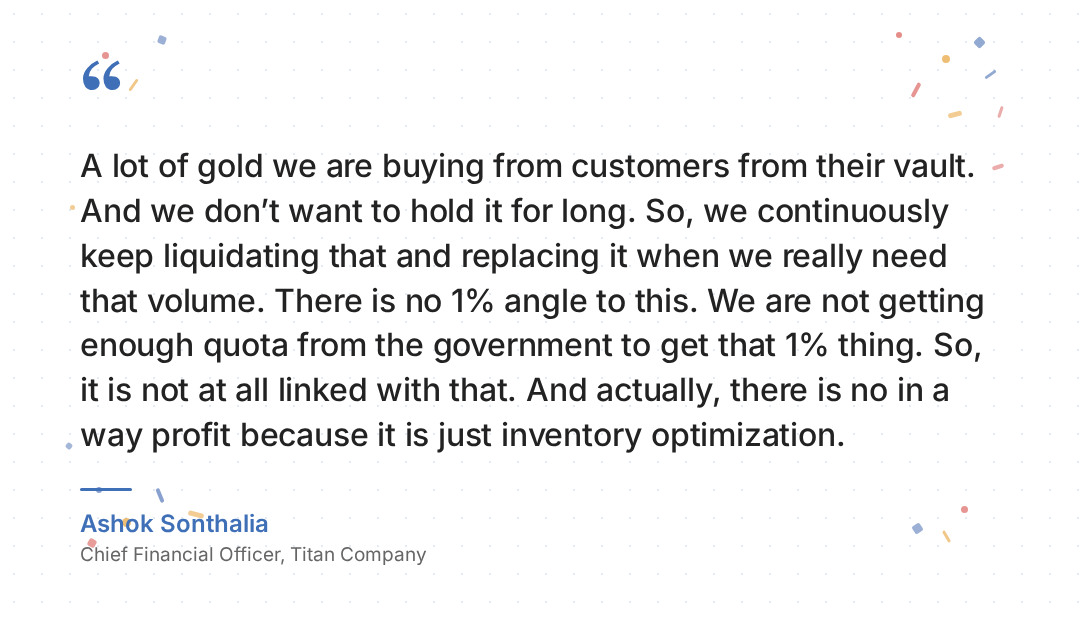

Titan’s is usually the most aggressive. This quarter, their exchange programme was so successful that customers ended up bringing in more old gold than the company actually needed for manufacturing. The surplus was turned into bullion. This was partly why their bullion sales jumped seven-fold: they bought way too much gold and didn’t want to keep it all in their inventory.

PN Gadgil, interestingly, is doubling down further on its old-gold exchange program, making it the centrepiece of next year’s strategy. Old gold is already 40% of PNG’s business. Its management wants to raise that figure to over 50%, through a programme they call ‘Suvarna Bharat’. The company revealed this strategy after the recent import duty hike, claiming that the duty hike would help its margins: as customers would shift to buying new jewellery through old gold exchange,

Think of this from the customer’s perspective. Someone looking to get married this year probably walks into a jewellery showroom this year with the same budget she would’ve had last year. Only, gold has gone up 60% since. Her money can buy much less metal. Exchange is one of the best solutions she has. She can bring in inherited or older pieces, which are valued at close to spot price, and only pay making charges on the new piece. It’s a win-win: the retailer gets cheap gold, while the customer gets to maintain the purchase she planned.

At a more macro level, exchange opens up interesting economic possibilities. With gold imports weighing down our import bills, Indian households sit on something like 25,000–30,000 tonnes of gold. A good exchange program opens up a truly enormous supply pool.

How much growth was borrowed?

There’s a final mystery in these numbers: if gold prices have been skyrocketing, why did sales grow so substantially this quarter?

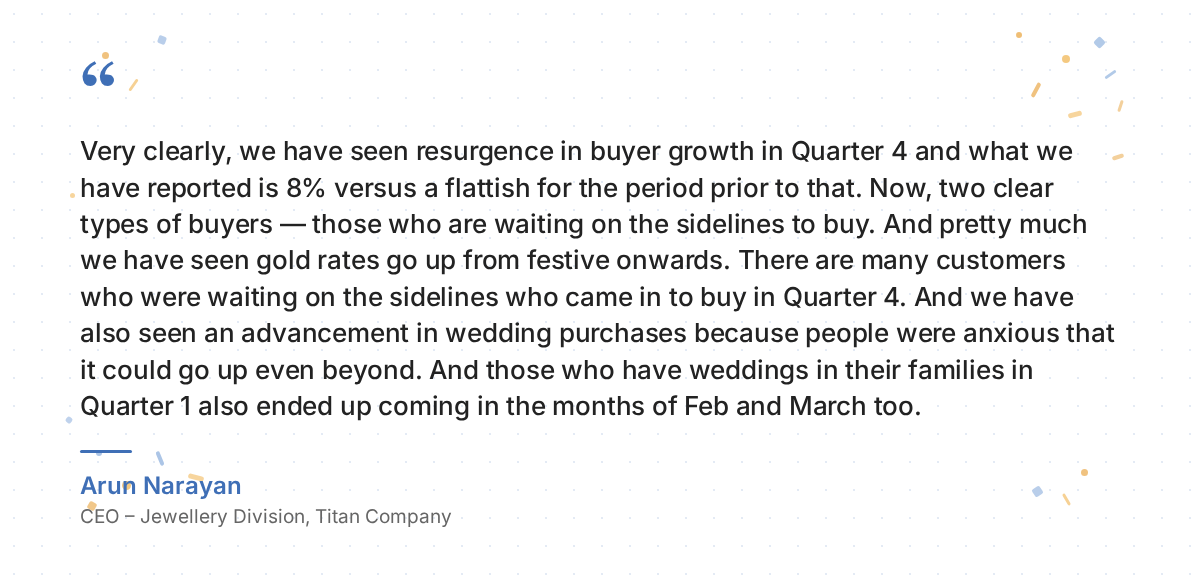

Titan, for instance, reported buyer growth of 8% in Q4 after nine straight months of flat numbers. To the company’s management, though, it’s too early to celebrate. This might come from one-time phenomena. For instance, buyers that were sitting on the sidelines, waiting for prices to stabilise, might finally be capitulating. Two, many people may have made wedding purchases early, afraid that costs would go up even further.

Kalyan offers an even more interesting story for its massive same-store sales growth. We’re currently in ‘aadhik-maas’, a particularly inauspicious month that traditionally mutes wedding demand. This may have pushed many to advance their purchases.

Similarly, the management of PN Gadgil attributes its incredible 86% same-store sales growth to a one-time stack of promotional events.

Their reasons may be different, but the upshot of all of this is the same: it’s hard to tell if these Q4 numbers were actually structural, or if all that business was borrowed from the current quarter. That, we’ll only know with the next set of results.

The customs duty pivot

This was the story of last quarter. It’s unclear if the trends we saw are structural, or if things will soon change. But the future, if anything, is even more uncertain. The ground has recently moved under the industry’s feet.

On 13 May, the government raised the customs duty on gold from 6% to 15%. Silver imports, too, saw a similar change. This is one of the largest single duty hikes the sector has seen in years. All three stocks instantly dropped in reaction to the news.

The move doesn’t touch them all in the same way, however.

Titan seems the best placed to handle the transition. As its management noted, its exchange programme is the largest in the country. It also has other advantages, including its sheer size, which gives it flexibility that its peers do not have.

Kalyan, too, enjoys some structural insulation. It procures heavily through Gold Metal Loan, while hedging most of its price exposure. Most of its stores are owned by franchisees, who may be forced to absorb part of the working capital pressure.

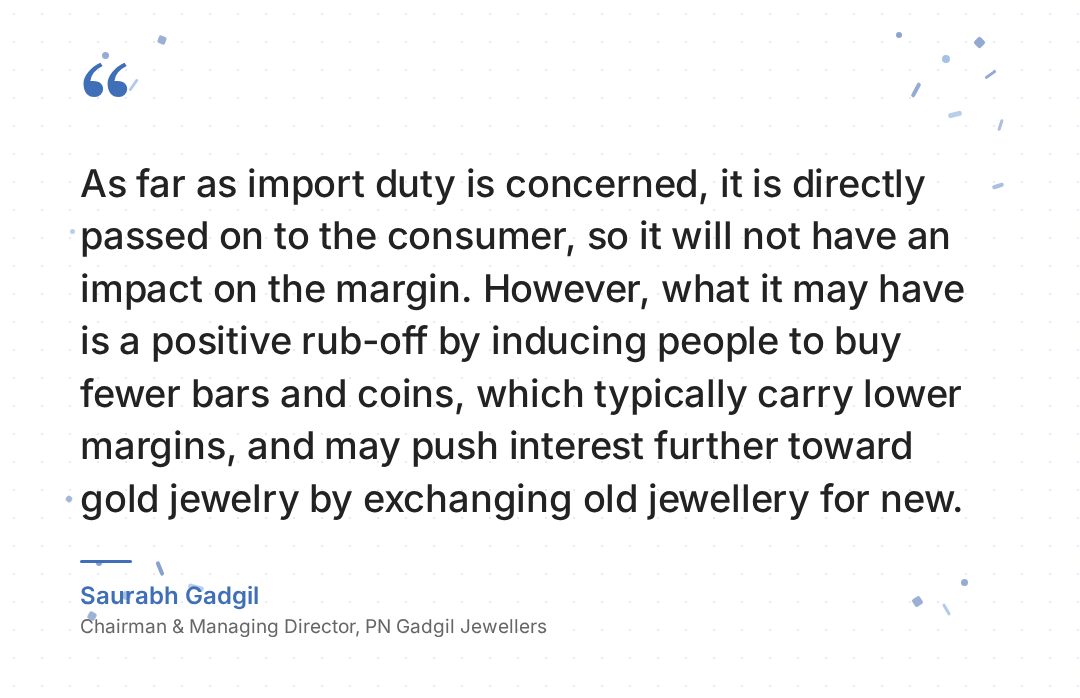

PNG is the most exposed in the short run. As we noted above, though, for now, its management bets that the duty hike will help its margins, by pushing customers away from buying bullion.

All of this, however, is plain conjecture. There’s a lot to look out for in the next quarter’s results.

SEBI wants to make municipal bonds great

Indian municipal bonds are having a moment.

In February, the Union Cabinet approved the Urban Challenge Fund of ₹1 lakh crore with a rule that at least half of every project’s cost has to come from the market: including bank loans, PPPs, or municipal bonds. The central government, under the AMRUT 2.0 urban mission, is literally paying cities to issue bonds. A first-time municipal bond issuer gets a grant of up to ₹13 crore for every ₹100 crore raised. The BMC has finally said it’s preparing its first ever bond, after 133 years of being asked.

This made FY26 the busiest year for municipal bond issuance ever — nine issuances by December 2025, against three in FY25 and one the year before. We covered this in our primer on India’s municipal bond market a few months ago.

At this moment, SEBI dropped a consultation paper, suggesting a bunch of changes in the municipal bond regulations it first wrote in 2015.

But, to understand what this paper is trying to do, it helps to know where the Indian bond market actually stands. It has many parts.

First, there is the government bond market — G-Secs — which is deep and well-functioning, with ₹150+ lakh crore outstanding, trading every day, used by every bank and insurance company in the country. The corporate bond market, on the other hand, is growing fast but less mature, with about ~₹50 lakh crore outstanding in FY25.

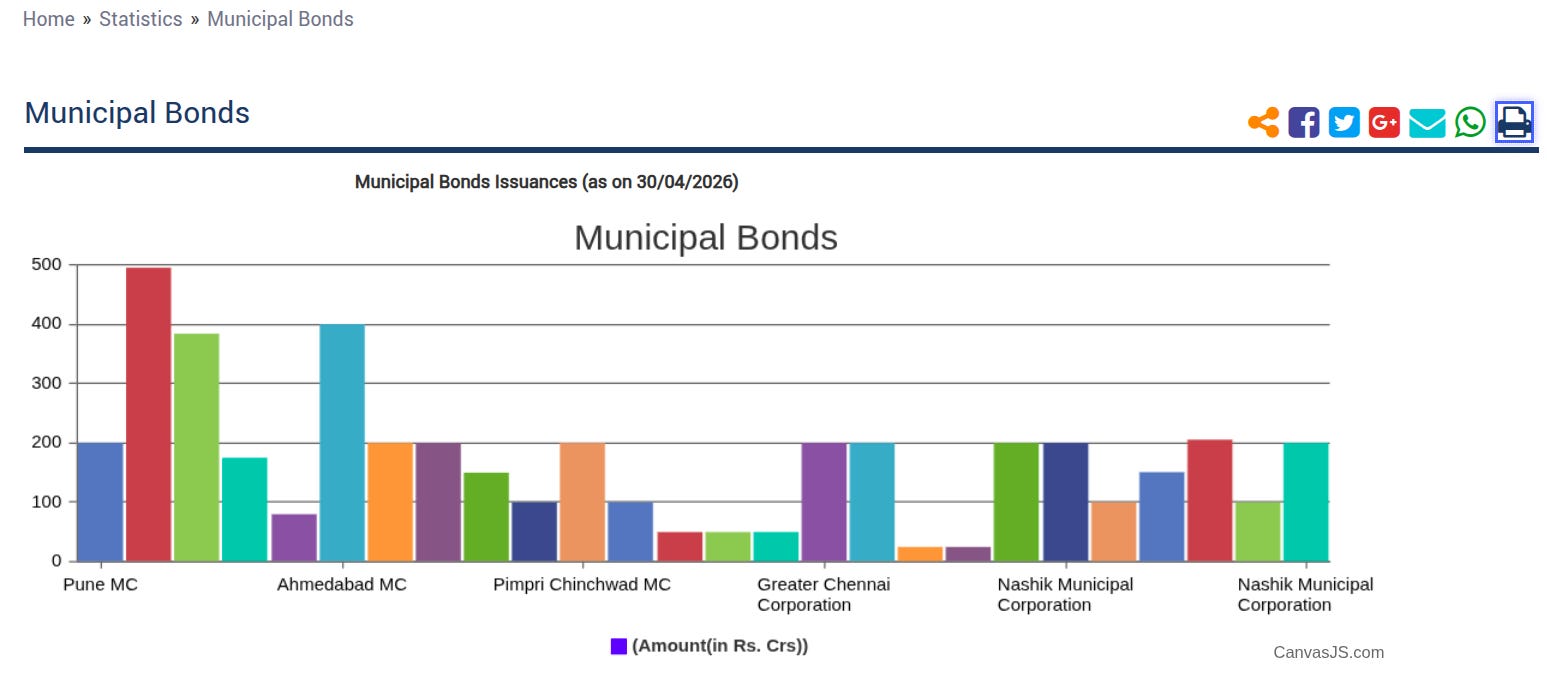

And then there’s the municipal bond market of just ~₹4,500 crore, cumulatively. That’s the amount raised from 22 cities across 31 issuances over eleven years. That’s less than 0.1% of the outstanding corporate bond market.

What SEBI is doing with this paper is trying to make the municipal bond market look like the corporate bond market. The corporate bond market itself isn’t deep — and the municipal market is being asked to play catch-up to a market that hasn’t fully figured itself out.

There’s another way to think about it. The municipal market is so small that nothing SEBI does to it really matters — even a doubling of activity would be a rounding error in India’s broader bond universe. But then, the market is so small that any structural change might compound dramatically. The unlock, if it comes, will look outsized.

We don’t really know which reading is right yet. But what we’ll narrate to you is the reforms in the paper, divided into supply-side and demand-side changes.

The supply side

First, we start with supply.

The reason there are so few municipal bonds is that there are so few municipal bodies that can issue them. Of the roughly 4,000 urban local bodies in India, only a few dozen run audited, accrual-based accounting, have healthy credit ratings, and have the structured payment mechanisms that bond investors require. Most municipal bodies are tiny, financially opaque, and politically constrained.

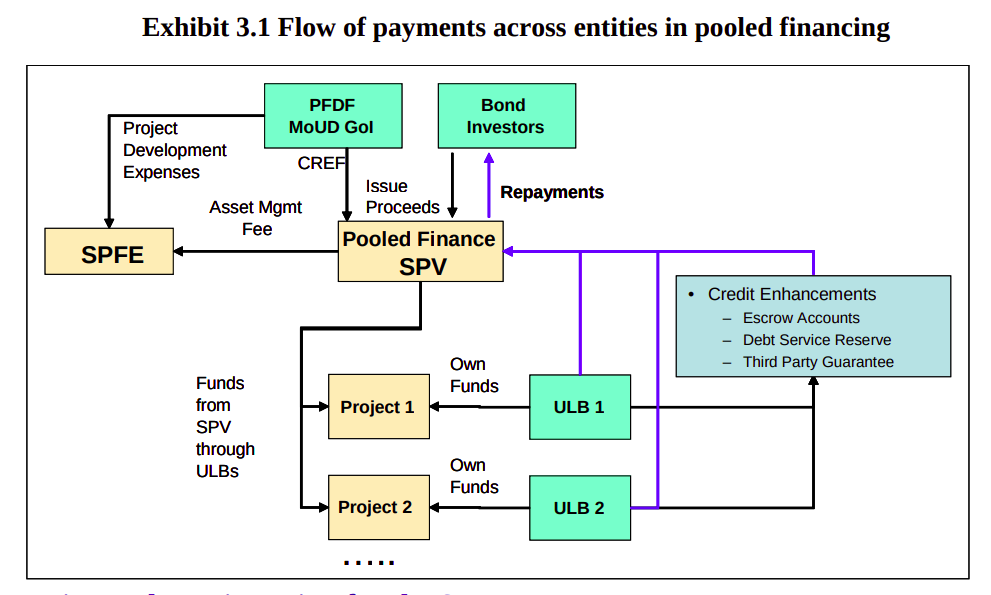

Obviously, it’s beyond SEBI’s mandate to fix that. But what it can do is widen the doors for the cities that are ready. And the biggest move in this direction is their new framework for pooled financing.

The idea itself isn’t new. Several small cities come together and set up a special purpose vehicle (SPV). Instead of the cities themselves, this SPV issues a single bond on their behalf. Money raised flows down from the SPV to the participating cities. Repayments flow back up, as each city pays into the SPV, and the SPV pays the bondholders.

This design solves the size problem: a small city like Agra, for instance, can’t justify the fixed costs of an issuance on its own. This includes merchant banker fees, rating agency fees, legal fees etc. Its balance sheet is also not strong enough to attract investors. But, ten cities like Agra, combined, can clear both bars. The risk gets spread across multiple issuers, which makes the bond easier to rate and sell.

The Government of India formalised this concept in 2006 through the Pooled Finance Development Fund scheme, but nothing translated into actual meaningful issuances. What SEBI is adding now is the operational playbook that was missing earlier. It has introduced a new disclosure framework for SPVs created to pool borrowings across cities.

Before raising money, every city in the pool has to sign and disclose a formal agreement with the SPV, which can be set up either as a trust or a company. The structure also comes with a layered escrow system. Each city will maintain its own interest payment and sinking fund accounts, and that money will then flow into matching accounts at the SPV level. On top of that, the SPV must always keep reserves equal to one full year of interest payments.

The framework also clearly lays out the kinds of credit support these pooled structures can use — including cash collateral, equity support from state governments, access to state finance commission devolutions, and partial or full guarantees from development finance institutions like the World Bank.

Importantly, the rating agency assessing the bond cannot just rate the SPV in isolation. It also has to evaluate every individual city in the pool, making it harder for weaker municipalities to hide behind a stronger pooled structure.

The paper also formally enables ESG debt securities for municipalities. Green municipal bonds already worked under a 2022 circular but this brings social, sustainability, and sustainability-linked bonds in line. The fit is obvious — city projects are mostly related to water, transport, waste, and solar.

The paper also tightens end-use restrictions. What this means is that no more than 25% of bond proceeds can go to working capital. The rest has to fund the capex of the project itself, and there’s a flat ban on using proceeds for “general purposes“. This ensures that the bond money is primarily directed towards infrastructure more than anything else.

And then, there’s a small, technical line on refinancing. Until now, cities could use bond money to retire existing bank loans without disclosing what those loans looked like. The paper fixes that — issuers now have to disclose all the details of the loan being refinanced.

The demand side

But supply needs to be matched by adequate demand. And almost nobody in India can buy a municipal bond.

This requires understanding a distinction that’s central to how the municipal market, much like any bond market, currently works. It’s the split between private placements and public issues.

See, a private placement is sold directly in large lots to a handful of institutional investors — like insurance companies, pension funds, mutual funds. A public issue is sold to anyone, including retail investors, often in small denominations. Of the 31 municipal bond issuances since 2015, 28 have been private placements.

Now, private placements can get listed on a stock exchange after issuance, and once listed, anyone can theoretically buy them in the secondary market. But the trading lot is set at the face value of the bond. Since SEBI’s existing rules don’t specify any minimum face value for municipal private placements, issuers default to ₹1 lakh per unit. A retail investor wanting to buy a single listed municipal bond in the secondary market needs ₹1 lakh minimum just to participate. That’s too steep a barrier.

The first big demand-side move in the paper fixes exactly this: the minimum face value for privately placed municipal bonds gets formally set at either ₹1 lakh or ₹10,000, with the ₹10,000 option available only for plain-vanilla bonds. SEBI made a similar adjustment for corporate bonds in July 2024, which brought a wave of retail investors into corporate debt for the first time. The plain-vanilla restriction is a consumer protection measure because complex structured bonds can get mis-sold to retail, so SEBI is keeping retail capital exposed only to simple, predictable cash flows.

A ₹10,000 trading lot, on a listed bond with a healthy credit rating yielding 8%, is genuinely accessible to retail. And it plugs municipal bonds into the same digital distribution infrastructure that corporate bonds now use.

The more crucial retail unlock comes not from making private placements more retail-friendly, but from getting cities to do more public issues. After all, public issues are designed for retail from day one. They advertise broadly, allocate quotas to retail and high-net-worth-individual (HNI) categories, and use small face values by default. For instance, in Oct 2025, Surat had a public bond issue at a face value of ₹1,000, allocated 15% of the issue to retail, and got oversubscribed by eight times. Indore did the same in 2023 — the retail category alone was oversubscribed nearly six times over.

It seems Indian retail investors are indeed receptive to municipal bonds. The question is whether more cities will choose this route.

This is where the paper’s other demand-side moves come in. There’s a new provision letting issuers offer incentives to senior citizens, women, retail individuals, and defence personnel. This could take the form of a slightly higher coupon or a discount on the issue price. It’s a small sweetener that’s limited to initial allottees, but it gives public issues a way to compete with bank fixed deposits and post office schemes for retail savings.

What this can and can’t do

SEBI’s job here is to fix the regulatory plumbing, but it can’t do much more than that.

On the supply side, the binding constraint is municipal readiness. Most of the 4,000 municipal bodies in India don’t have audited accrual-based books. Most rely on grants from higher tiers of government for the bulk of their revenue. Most have property tax collection efficiencies that wouldn’t survive a credit rating. Most have no track record of issuing in capital markets and no internal capacity to prepare one.

SEBI can’t make a city collect more property tax, or affect the fiscal positions of cities. Until that happens, the supply of bondable cities stays narrow.

On the demand side, even with retail access, the secondary market doesn’t really exist. Most institutional buyers hold to maturity. There are no dedicated market makers and pricing is opaque. A retail investor who can now buy a municipal bond at ₹10,000 still can’t easily sell it before maturity, which makes the product less attractive than the headline yield might suggest. Liquidity follows scale and breadth — both of which depend on more cities issuing more bonds more frequently. Which loops back to the supply problem.

Whether you read that as a meaningful step or as housekeeping for a market still too small to count probably depends on how much of the rest of the urban finance push is going to land. Either way: it’s a small, coherent push in the right direction, on a market that has, until very recently, refused to move at all.

Tidbits

Dr Reddy’s has rolled out its generic semaglutide injection in Canada, becoming the first Indian company to commercialise a low-cost version of the blockbuster diabetes and weight-loss drug in a G7 country. The launch comes after Health Canada cleared the once-weekly injection in April, after having earlier blocked it.

Source: The Hindu BusinessLine

The DGFT has shifted silver bars of 99.9% purity and certain other categories from the “free” to the “restricted” import list, meaning importers now need a government permit to bring them in. The move follows a steep hike in customs duty on gold and silver from 6% to 15% effective May 13, and is aimed at curbing the import bill and easing pressure on the rupee amid West Asia-driven volatility.

Source: The Hindu BusinessLine

Dutch lithography giant ASML has signed an MoU worth $11 billion with Tata Electronics to supply tools and expertise for India’s first commercial 300mm semiconductor fab in Dholera, Gujarat. The deal was inked during PM Modi’s visit to the Netherlands.

Source: Reuters- This edition of the newsletter was written by Pranav and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Kyle Chan on China’s industrial power and entrepreneurship

If you enjoy The Daily Brief, here’s something we bet you’ll like. We recently spoke to Kyle Chan, one of the sharpest minds we read to understand China - we’ve often featured his insights on The Daily Brief. Our conversation dives deep into the dynamics that shape China’s manufacturing landscape. It goes into the nature of Chinese entrepreneurship, how China’s price wars affect innovation (and vice versa), why China’s policies are far less all-knowing than people assume, and how China wields its manufacturing prowess as a geopolitical power. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉