Keytruda: The clone wars

India's toughest pharmaceutical challenge yet

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The race to replicate Keytruda

What is CBAM really?

The race to replicate Keytruda

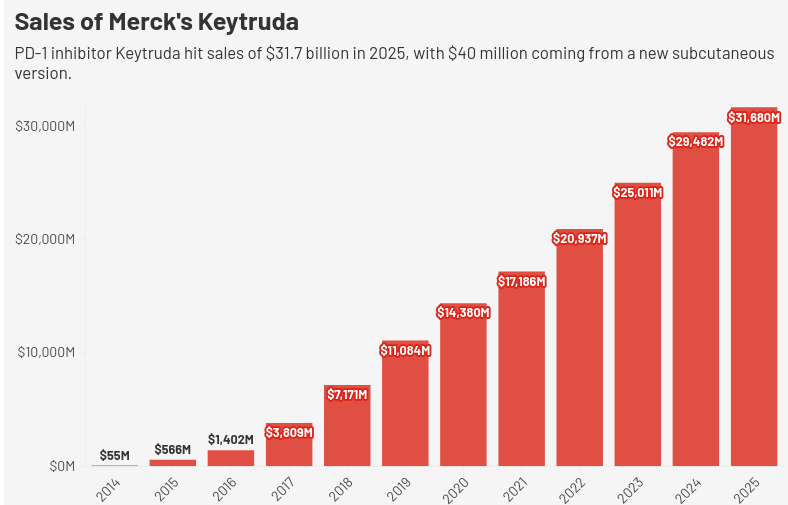

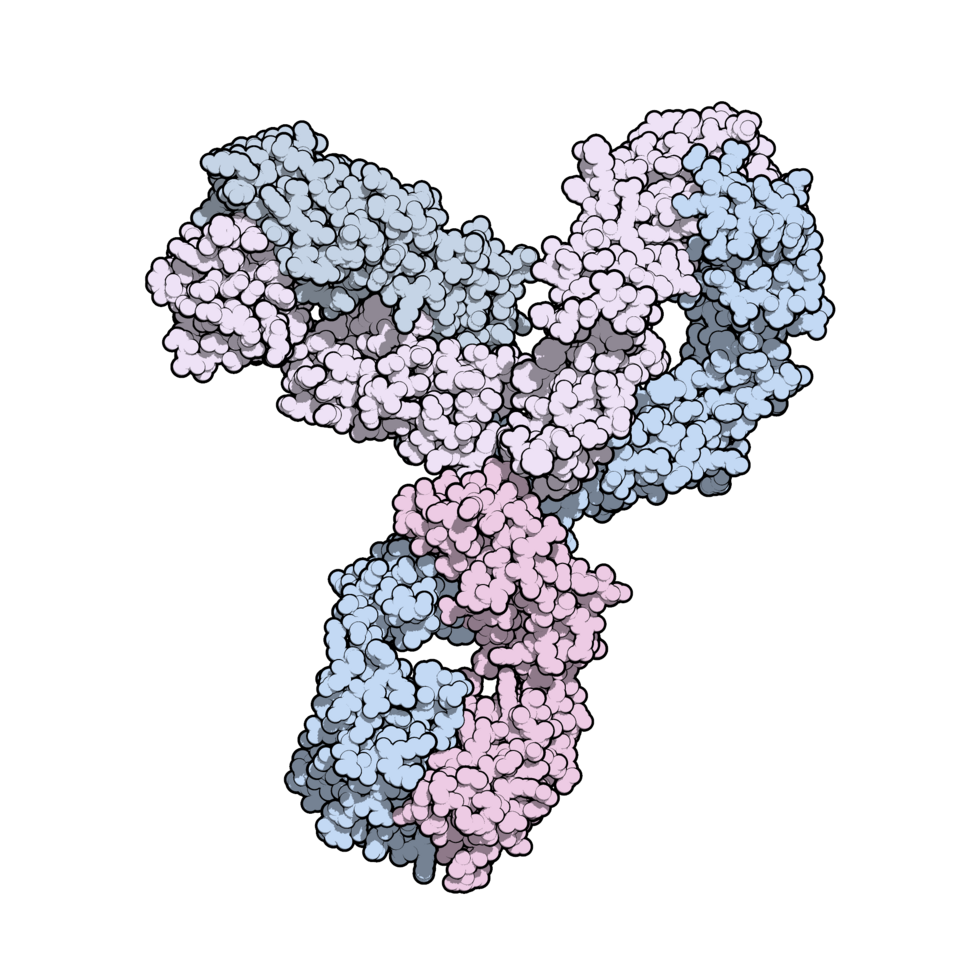

The best-selling drug in the entire world is Keytruda, or more scientifically, pembrolizumab. In 2025 — a single year — it clocked sales of over $31 billion. That puts it in a club of one: well ahead of global blockbuster drugs like Ozempic. That’s for good reason: Keytruda is the literal cure for cancer.

Yet, the company behind this sensational drug, Merck & Co., sounds anxious. 2028, the company reckons, might be the best year in its life. From there, things will be downhill. In fact, Merck recently announced new plans for how it’ll cope with life after 2028.

That’s because its main patents — what are called its composition-of-matter patents — will expire in December 2028. Other protections are falling off even sooner. In the European Union, for instance, its “data exclusivity” will lapse midway through the year, opening room for companies to make regulatory filings to sell their drug there, using Merck’s clinical trial data.

In short, Merck will soon hit a patent cliff. An opportunity worth hundreds of billions of dollars will soon be open to pharmaceutical companies across the world. India’s pharmaceuticals sector is already watching the space like a hawk. That moment will also be a boon for cancer patients across the world. Currently, a single 100 mg vial of imported Keytruda can cost as much as ₹2.36 lakh. That translates to an annual cost of ₹40–50 lakh — utterly out of reach for most. As others rush to the space, those costs will fall to a fraction of that amount.

But it won’t be that easy. Re-creating a biologic drug like Keytruda is infinitely more difficult than copying a regular pill.

How Keytruda took on cancer

Fighting cancer is one of the hardest challenges the world’s pharmaceutical industry has ever taken on. The “emperor of maladies” works nothing like an ordinary illness. It is too similar to your body for medicine to work, and too clever for your body’s own defences to kick in. Keytruda found a way to break that bind.

The impossibility of fighting cancer

Cancer isn’t one disease. It can begin for a variety of reasons, across various contexts. Once it takes hold, it can behave completely differently in different patients. There’s no one molecule you can target to fight the disease.

It isn’t just that cancer differs between different patients — different cancer cells in the same patient, in the same tumour are different. Even if you can create a medicine that kills most cancer cells in a tumour, some sub-clones, with different genetics, could survive. This kicks off a Darwinian evolutionary process. As you attack a cancer, the cells that survive build a resistance to your methods. You could kill 99% of a tumour, but the 1% that survives shall create the next tumour, which will be harder to kill.

Cancer demands something smarter than brute force — a system that can recognise cancer cells, adapt as they mutate, and hunt them as they hide.

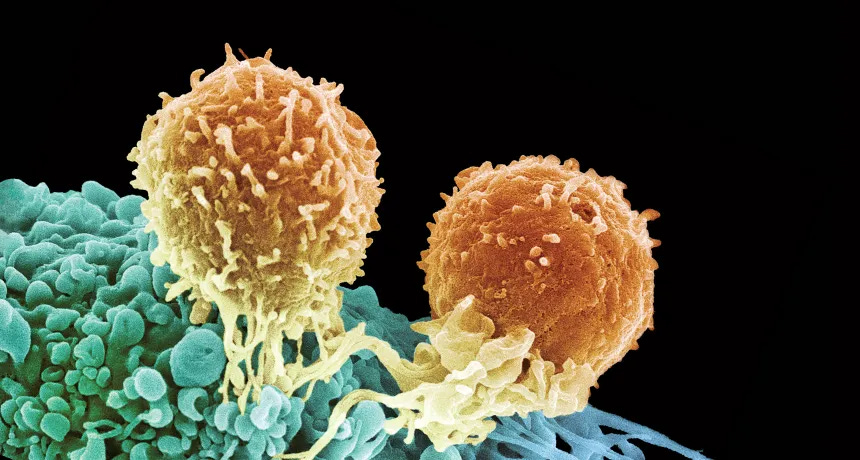

Ideally, your body’s immune system should be capable of performing that role. Cancer cells, because they’ve mutated from your cells, have abnormal proteins on their surface, called neo antigens. Your immune system has ‘T-cells’ that can recognise those abnormal proteins, and attack the cells that carry them. That is, your body has some capacity to fight cancer.

In response, however, cancer can learn to launch a campaign of subterfuge. Cancer cells learn to hide the neoantigens on their surface. And more insidiously, they start activating something with the ominous name programmed death-1 (PD-1). This is a natural off-switch that T-cells have; it tells them to press the brakes on their job of fighting an infection. Cancer cells learn to press that switch, and turn your immune response down. The harder your body fights the cancer, the stronger a response it receives.

How Keytruda does the impossible

Until Keytruda, there were broadly two ways to fight cancer.

The first was chemotherapy: poisoning all rapidly dividing cells in the body. This worked, but crudely — apart from cancer, your gut lining, hair follicles, and bone marrow divide rapidly as well, and chemo would attack them all. You could only hope to kill the cancer before you killed the patient.

The second was more targeted. Some drugs, like imatinib, could hunt for a specific protein that some cancers depend on, and block it. When it worked, it worked beautifully. For instance, imatinib turned chronic myeloid leukaemia, a type of blood cancer, from a death sentence into something manageable. But many cancers don’t come with that molecular target, or they evolve around the medicine — and then, there is little these therapies do.

In both cases, we would attack cancer cells — in one case, by carpet bombing them, and in the other, by looking for specific targets. Keytruda, however, tried something new: it didn’t attack the cancer at all. It just stripped away cancer’s ability to hide from the body’s immune system.

It essentially blocks cancer cells from reaching the “programmed death-1” brakes on T-cells. Without that, your body’s immune system continues hunting for cancer. It is a smarter anti-cancer system; it is adaptable, and targets abnormality rather than static targets, which is why it avoids many of the defects that older therapies came with.

Interestingly, Merck almost didn’t develop the drug. It got the research for Keytruda as part of an acquisition where it wanted something else entirely. Back then, it valued PD-1 therapies at next-to-nothing.

But the drug turned out to be revolutionary.

Take “metastatic melanoma” — a skin cancer that has advanced, and has spread all over one’s body. Before immunotherapy, only one in every twenty patients would survive this for five years. With Keytruda, however, more than one in three patients would survive for seven years. Among those who completed two years with Keytruda, more than nine in every ten patients would survive the next five years.

Most impressively, Keytruda doesn’t just work with one sort of cancer. It’s more of a platform: it’s a single mechanism that works against a variety of cancers. As of 2025, the FDA has approved it for eighteen different types of tumours. In fact, in 2017, it became the first approved cancer drug to be tissue-agnostic; that is, it could help the body fight cancers anywhere, if the cells there were deformed enough to produce enough antigens.

Re-creating Keytruda is a nightmare

It is this remarkable drug that Indian pharmaceutical companies might soon launch themselves at. But recreating a miracle isn’t easy.

Our pharmaceutical industry came up around generics for small molecule drugs. These were simple medicines — like Aspirin, which just has 21 atoms. They had simple, defined chemical formulas. If you knew how, you could make them in a simple lab, with simple chemistry.

Keytruda, meanwhile, is a protein. It is made of over 20,000 atoms, arranged in a massive, three-dimensional structure, with intricate and precise folds. On its surface, there are specific points where complex sugar molecules latch on, and they define how the drug works.

Biological manufacturing

To re-create molecules like this is a different exercise in kind than making generics for something like paracetamol. You just can’t make something this complex in an ordinary chemistry lab.

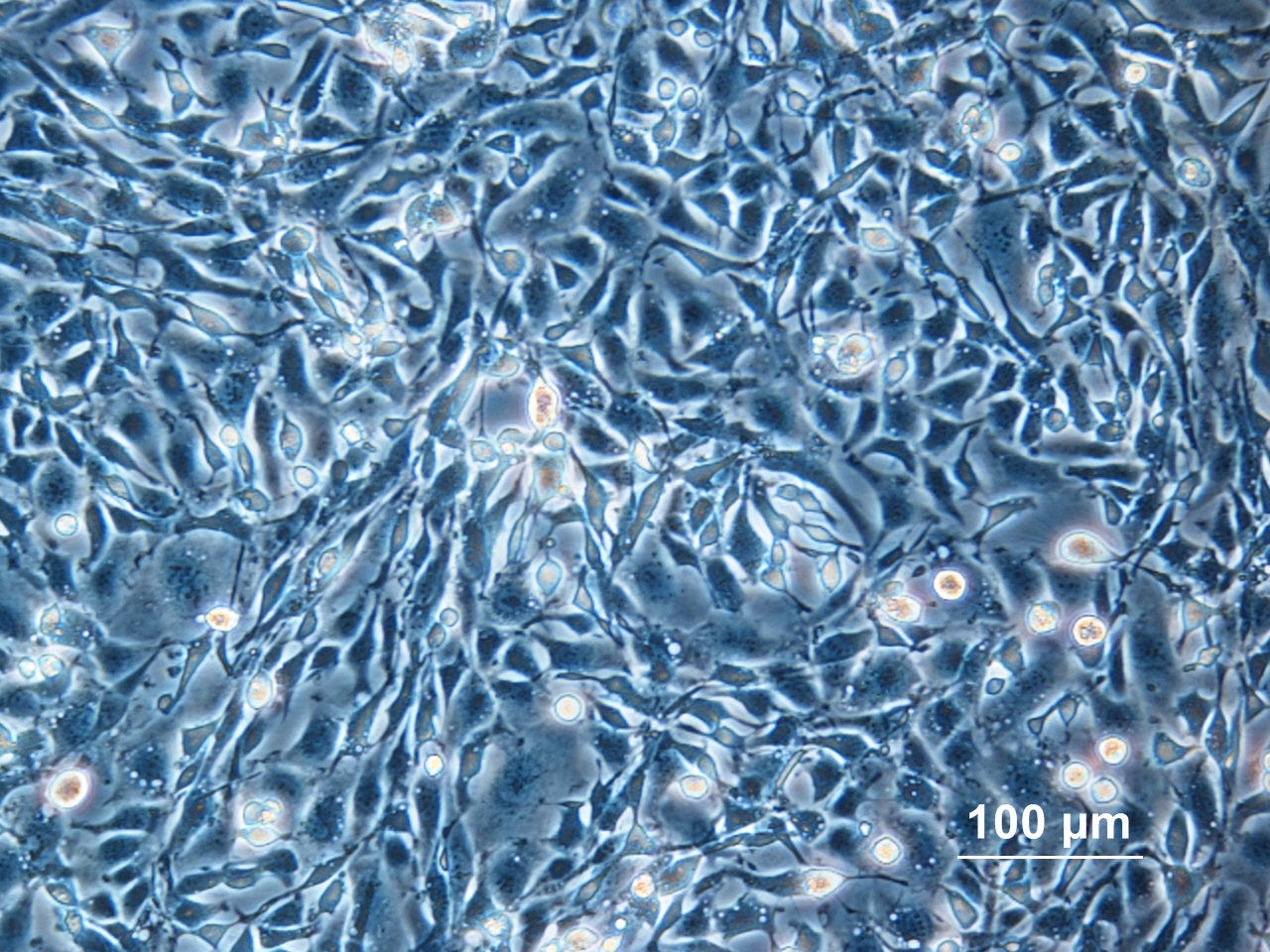

Instead, you put living cells to the task. You inject these cells with genetic material that can create the drug. More often than not, cells from the ovaries of Chinese hamsters are used for this work. You grow these in giant industrial bioreactors, where you must ensure precision. You’re trying to coax these cells to work perfectly — manufacturing a specific, enormous protein, folded correctly, decorated correctly, across thousands of litres of production. To get it right, you need to control every single variable you can: from temperature, to the nutrient feed, to acidity, and so on.

Even then, you won’t get it perfectly right. Even Merck’s own Keytruda varies slightly from batch to batch. That’s just how living systems work. The best you can hope for is to get something “highly similar” to the original.

But some mistakes can be fatal. In 2002, for instance, a small manufacturing change to a biologic ended up causing an epidemic of pure red cell aplasia across Europe — where those who took the drug could no longer create red blood cells. These mistakes aren’t visible in any real sense, until the damage is done.

What this complexity means

All this complexity means that even if someone’s patent over a biologic runs out, you can’t just copy the drug. You’re running a decade-long research project, reverse engineering and recreating a complex protein. This costs $100–300 million — compared to the $2–5 million cost of a standard generic.

The same complexity is also visible in how regulators treat these “biosimilar” drugs. A generic just has to prove it’s absorbed by the body the same way as the original for approval, after looking at a few dozen patients. A biosimilar developer, meanwhile, has a much harder task. They have to prove, at a molecular level, that their protein is structured the same as the original — down to the sugar molecules on its surface. They have to show it can be purified without losing its shape. They have to demonstrate it doesn’t trigger some sort of terrible immune reaction the original doesn’t.

In fact, until recently, they also had to run a full set of clinical trials — although that is now being relaxed.

All of this is to say: for any company that’s looking at Keytruda’s 2028 patent expiry, the race started a long time ago. To make the first wave of biosimilar launches, you need to be nearly done already.

The race ahead

Many Indian pharmaceutical heavyweights have their eyes trained on this window. To get there, though, the industry will have to evolve itself. Right now, it is still geared for small-molecule generics. It lacks both the capacity and the experience to run such a project end-to-end.

But it has to start somewhere.

One answer, for the industry, is to partner with foreign firms that have more experience with such work.

At the head of this pack is Zydus Lifesciences. In late 2025, it secured exclusive rights to commercialise a pembrolizumab biosimilar developed by Germany’s Formycon — one of Europe’s leading biosimilar specialists. Formycon will take care of the technical side of things; while Zydus is more of a marketing partner, at least for now — it will use its commercial presence in the United States and Canada to sell the drug. Zydus plans to file for approvals with the US FDA this year.

The company has just acquired a biologic manufacturing facility in California. Over time, it might start manufacturing as well.

Dr. Reddy’s Laboratories, meanwhile, has a more hands-on approach. In mid-2025, it entered a partnership with Iceland’s Alvotech — to co-develop the drug. Both companies will share costs, manufacturing, and regulatory responsibilities equally. Dr. Reddy’s already has its own biologics manufacturing facility in Hyderabad. This partnership, now, helps it build capability. That said, its regulatory filings are likely a few years away.

The most ambitious Indian firm, though, is Biocon Biologics. It’s the only Indian company attempting to build a pembrolizumab biosimilar on its own, end-to-end, at its manufacturing facilities in Bengaluru and Malaysia. Last month, it named pembrolizumab as part of a pipeline of 17 cancer medicines it intends to commercialise. If this works, Biocon would be the first Indian company to take a biosimilar this complex to global markets, without a foreign partner leading the way.

These aren’t alone. Several other Indian pharmaceutical companies — Intas, Aurobindo Pharma, Serum Institute, and more — are at various stages of developing or licensing their own pembrolizumab biosimilars. The field only gets more crowded from here.

Meanwhile, Merck won’t take the competition silently. It has spent years preparing for this moment. Beyond its core patent, it has filed over a hundred additional patent applications, covering manufacturing processes, specific treatment methods, formulations, and more — with some protections stretching well into the 2030s. For instance, it just launched a new, injectable version of Keytruda, over which its rights will last for even longer.

As new competitors come for its turf, Merck will try to shift patients onto new versions of its drug. The patent cliff, in other words, may end up looking more like a long, managed slope.

A challenge worth conquering

Here’s one way of looking at what Keytruda means to India’s pharmaceutical industry.

This is, of course, a commercial opportunity — one of the largest the global biosimilar market has ever produced. But equally, it is a challenge worth stepping up to. Biologics are a new frontier for the industry. And Keytruda’s enormous market might just be the incentive it needs to conquer it. Seen that way, this is a test of whether the industry can evolve to handle a more challenging landscape.

It won’t be easy. But there are hundreds of thousands of Indian cancer patients for whom a ₹40 lakh annual treatment is no better than a death sentence. They, at least, will be rooting for the industry to prevail.

What is CBAM really?

Imagine you run a steel plant in India. You’ve been selling to European buyers for years, and your prices are competitive.

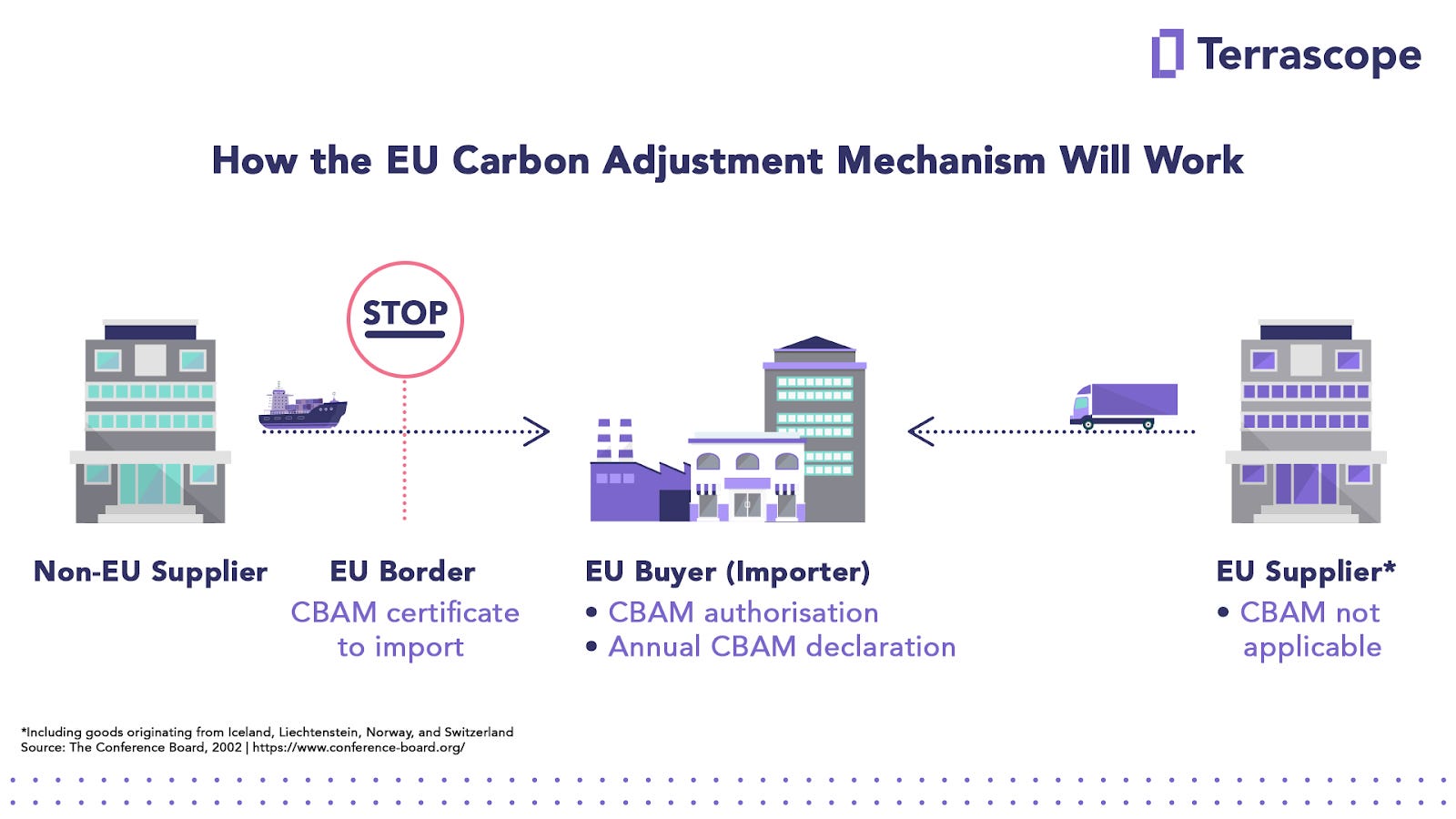

Beginning January 1st this year, though, that might change significantly. Every tonne of steel you now ship to Europe will be supplanted with a carbon tax, calculated based on how much CO2 your plant emits. This goes to the European kitty that funds its net-zero goals.

This is the Carbon Border Adjustment Mechanism, commonly called CBAM. And after much planning, it finally entered what the EU calls its “definitive phase” starting 2026.

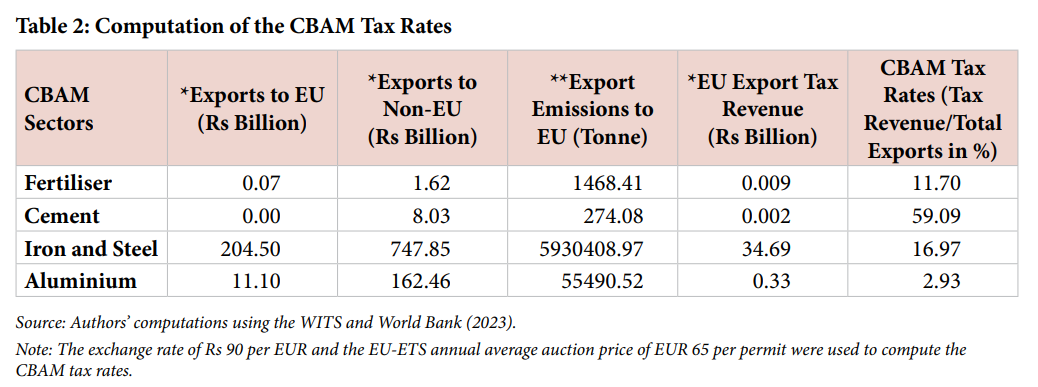

India, the second largest producer of steel in the world, sends ~₹20,000 crore worth of steel to Europe every year. CBAM has been a massive point of contention between both blocs, because crucially, that same steel is going to be a lot more expensive for our producers to make and sell.

We’ve mentioned CBAM in passing multiple times before on The Daily Brief. In fact, beyond CBAM, Europe’s new carbon-related rules are the root cause behind why giants like Tata and Jindal Steel are overturning their European carbon-intensive plants to clean, hydrogen-fueled machines.

A paper from CSEP, a policy think tank, has tried to answer the most important question this raises: what should India actually do about CBAM? Their most striking finding isn’t truly about the fear of exports falling, but is more so about money. But to get there, we need to understand why CBAM exists at all.

The problem Europe was trying to solve

Since 2005, Europe has been running a carbon pricing system called the EU Emissions Trading System, or EU-ETS. Here, the EU sets a cap on how much carbon-dioxide (CO2) all covered industries can collectively emit. Every company in a covered sector — like steel, cement, power, aviation — needs a permit for every tonne of CO2 it emits. And these permits are auctioned and traded — as of early this year, one permit cost ~€65.

The more the EU tightens the cap each year, the fewer permits there are, and the more the prices of permits go up. As a result, companies are nudged to invest in cleaner production.

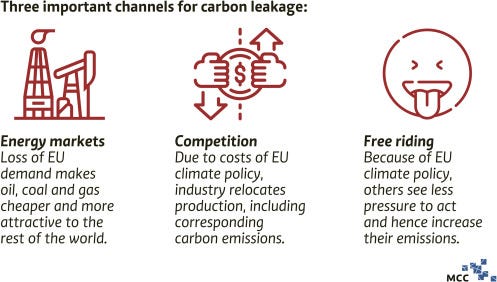

But this poses a conundrum for the competitiveness of European steel. If a European plant has to pay €65 for every tonne of CO2, its steel gets more expensive to make. Meanwhile, steel from India or China lands in Europe far more cheaply. European steelmakers lose business not necessarily because they’re less efficient, but because their foreign competitors don’t carry the same burden.

Moreover, global CO2 emissions don’t actually fall — volume production just shifts to countries with looser rules. Economists call this carbon leakage.

For years, the EU managed this through free allowances, handing certain industries some permits at zero cost to cushion them from import competition. But, of course, this subsidy blunted the carbon price signal, and imports still came in with no carbon cost at all.

Perhaps, the most sure-shot solution was to burden imports with the same carbon emissions requirement. That’s what CBAM aims to do. Meanwhile, free allowances are being phased out until 2034.

How it works

Here’s how CBAM is enforced on-ground. When a company imports steel into the EU now, it has to surrender CBAM certificates equivalent to the carbon embedded in that steel. In numerical terms, an EU carbon price is paid for every unit of CO2 intensity in the product.

The catch is in how that CO2 intensity is measured. Importers can get their emissions independently verified, paying based on their actual production. If they don’t, though, the EU applies default values by country of origin. For India, that default is 4.2 tonnes of CO2 per tonne of steel, while for China, it’s 3.1.

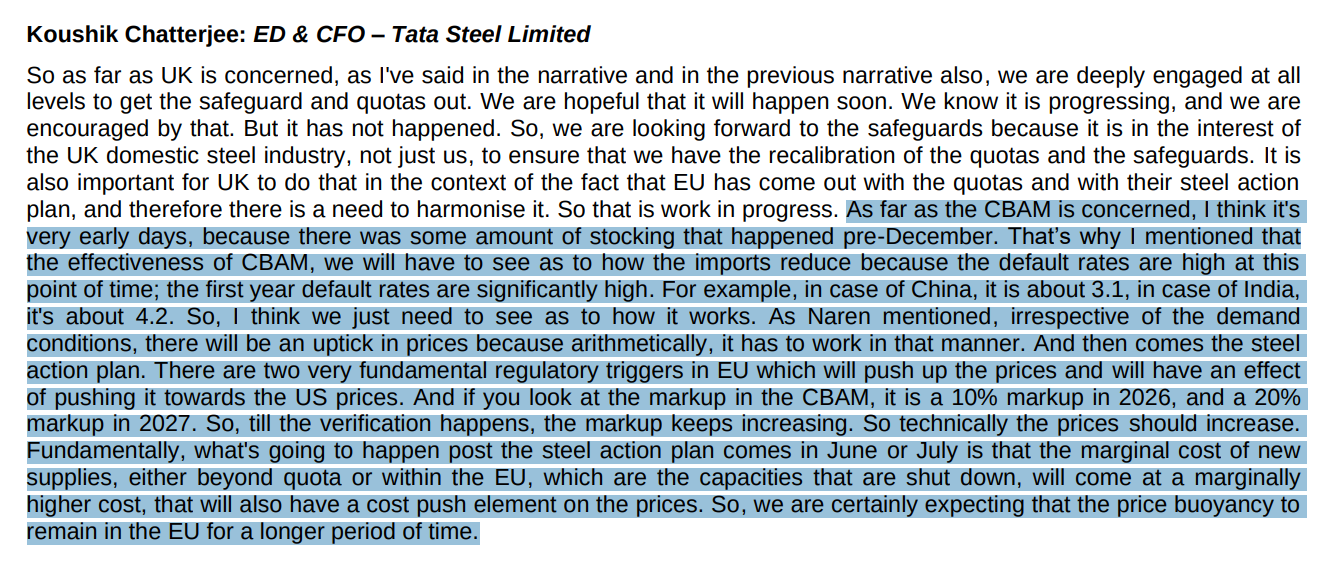

In a recent earnings call, Tata Steel was quite honest with the consequences of this:

“...the first year default rates are significantly high. For example, in case of China, it is about 3.1, in case of India, it’s about 4.2. So, I think we just need to see as to how it works. As Naren mentioned, irrespective of the demand conditions, there will be an uptick in prices because arithmetically, it has to work in that manner. And then comes the steel action plan. There are two very fundamental regulatory triggers in EU which will push up the prices and will have an effect of pushing it towards the US prices.”

On top of that, unverified importers face a markup:

“And if you look at the markup in the CBAM, it is a 10% markup in 2026, and a 20% markup in 2027. So, till the verification happens, the markup keeps increasing. So technically the prices should increase.”

Let’s put it this way: an unverified Indian steel plant that produces at 2.5 tonnes CO2 per tonne of crude steel, actually gets charged as if it emits 4.2 tons, plus a growing markup. Clearly, verification is the more efficient choice, but what prevents more Indian firms from doing it is that they don’t have in place the data systems needed for it.

What the CSEP paper found

This is the context in which the CSEP paper becomes important.

The researchers built a detailed economic model of India and ran three scenarios. In the first, India does nothing and just pays the full CBAM charge to Europe. Secondly, India introduces its own domestic carbon tax at the full EU rate. In the last one, India introduces a carbon tax at half the EU rate while also paying some CBAM.

The scenario where India does nothing and just pays Europe is, by CSEP’s account, the worst for us. When CBAM tax revenue flows outside rather than staying in India, it causes currency depreciation. This, in turn, raises the cost of imports and squeezes household purchasing power. Urban households get hit harder than rural ones, because they earn more of their income from manufacturing sectors that CBAM directly squeezes.

In the second scenario, if India introduced a full domestic carbon tax on CBAM-exposed sectors, it could generate revenue worth ~1% of GDP by 2030. To put that in absolute terms: in the full domestic carbon tax scenario, India could generate ₹2,93,000 crore in carbon tax revenue in 2026 alone. At last, at even half the EU rate, CSEP assumes that revenue is closer to 0.5% of GDP. In contrast, In the first do-nothing scenario, the EU collects only ₹5,500 crore from India’s exports.

The revenue gap between India acting and India not acting is enormous — and it all stays in India if India moves first. Under CBAM, the charge an importer pays to Europe is calculated as the difference between the EU carbon price and whatever the exporter’s home country has already charged. If India’s domestic carbon price equals the EU rate, the CBAM charge drops to zero. If it’s half the EU rate, the CBAM charge halves.

What the FTA didn’t fix

Last month, we covered India’s landmark free trade agreement (FTA) with the EU — the largest trade deal for either side.

The FTA resolved longstanding disputes over textiles, auto, and pharma. But on CBAM, India got virtually no exceptions or special treatment from the EU. What we received instead was a “Rebalancing Mechanism“ — a provision that would only kick in if CBAM was shown to have specifically undermined the trade benefits India was promised under the FTA. It is a safeguard against future harm, not a carve-out from CBAM itself.

CBAM, it seems, is not a negotiating position for the EU. It is foundational climate policy, and India will have to adapt rather than negotiate around it.

What India can actually do

The most immediate lever of adaptation is improving the verification process. Indian steel producers who can demonstrate their actual carbon intensity is below the 4.2 default have a strong financial incentive to get verified quickly. For large players like JSW or SAIL, this is a relatively solvable problem. But for smaller producers, it’s a steep learning curve.

Another significant lever is domestic carbon pricing. India has been developing something called the Carbon Credit Trading Scheme (CCTS) — essentially India’s own version of EU-ETS. If India has a functioning domestic carbon price, Indian exporters can offset it against their CBAM liability.

The CSEP paper’s argument is to start a domestic carbon price now, at a lower rate consistent with India being a developing economy, and use the revenue to support affected industries and households through the transition. The EU’s climate ambition, in a way, becomes a useful pressure on India’s own industrial decarbonisation — something India will have to do eventually regardless.

But every year Indian exporters go unverified, the markup climbs. Every year India delays domestic carbon pricing, that revenue accrues to Europe instead. India’s best course of action is not to reject, but to respond to CBAM in a way that keeps some value at home.

Tidbits

India Cancels 75,000 Tonnes Soybean Oil Imports on Price Rally

Summary: Indian traders canceled 65,000-75,000 tonnes of South American soybean oil imports for April-July delivery, booking $40-$60 per tonne profits as prices climbed from $1,080-$1,100 to $1,140-$1,147.50, anticipating record South American crop supply pressures ahead.

Source: Business Line

CDSCO Streamlines Drug Testing Approvals from June 2026

Summary: India’s drug regulator CDSCO will issue immediate testing permissions upon application receipt from June 1, 2026, eliminating upfront scrutiny delays, allowing companies to begin laboratory testing while detailed technical review continues, aiming to accelerate new drug approvals.

Source: BS

Ford India GBS Central to Electrification Plans, Says Executive

Summary: Ford Business Solutions’ Chennai hub, with 12,000+ employees, has evolved from back-office operations into Ford’s largest global technology center driving AI, vehicle software, and enterprise transformation, with India engineers contributing to Ford’s new common EV platform development.

Source: Business Line

- This edition of the newsletter was written by Pranav and Krishna.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

I'm an oncologist in training and I loved reading the article on Keytruda. The race to recreate/produce biosimilars is already on.

Please tell me what your research framework for such topics look like - How do you go into so deep in these topics?

I really loved the articles on Copper.