Is the Rupee Losing Its Power?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The Rupee Drop Story Simplified

SEBI Brings Transparency to Mutual Funds

The Rupee Drop Story Simplified

You’ve probably seen all sorts of gloomy, depressing news about the Rupee off late. Newspapers carry alarming headlines like “The Rupee falls to an all-time low against the Dollar” every second day. The RBI’s name gets dragged in often — either for not enough, or for doing too much, depending on who you ask.

But what does all this really mean? Why does the Rupee fall? Why does the RBI have to get involved?

This is one of those weird controversies that are (a) crucially important to India and its markets, and (b) so niche that there are basically just three-and-a-half people who actually understand what’s happening.

That’s why we’re going to try and make things as simple as we can for you. But stick with us; we’re going to cover a lot of territory. To get you started, here are five big ideas that will get you up to speed on currency markets.

Idea I: Currencies don’t have any real value

There was once a time when a country’s currency had a fixed underlying value: usually linked to the gold in its coffers. Over the last hundred years or so, however, that system kept breaking down, until it was dismantled completely in the early 1970s.

Ever since then: over the last fifty years or so, the world’s currencies don’t really have any innate value. They’re only worth something because people think they’re worth something. You’d think this was a recipe for chaos and disaster, but somehow, this weird new system has survived for decades, without too much chaos.

Idea II: Forex markets decide a currency’s ‘price’

This lack of innate value creates a challenge. Whenever you need to buy or sell a particular currency — and you basically need to do so in any cross-border transaction — you need a price.

Imagine you’re importing chocolates worth $10 from the United States. The person selling those chocolates only accepts Dollars. But all your money is in Rupees, which is completely useless to them. You need some way of turning your Rupees into Dollars. The problem, however, is that the value of both currencies is imaginary: neither has any real basis for their value.

Thankfully, there are massive foreign exchange markets that offer you an ‘exchange rate’ at which you can convert different currencies.

Idea III: Exchange rates are determined by supply and demand

How do foreign exchange markets come up with an exchange rate in the first place? Well, like the price of everything else, it depends on demand and supply.

If you’re importing chocolates from the United States, for instance, you’re asking for dollars, in exchange for Rupees you’re willing to give away. You demand Dollars and supply Rupees.

If you work in the United States and send money home, you’re earning Dollars, that you turn into Rupees. You supply Dollars, and demand Rupees.

If you buy Google stock while sitting in India, you’re spending Rupees for an investment in Dollars. You supply Rupees, and demand Dollars.

And so on.

Every day, foreign exchange markets get millions of requests from people who are willing to both buy and sell the Rupee in exchange for other currencies. These requests set the ‘price’ of the Rupee in other currencies. When there’s more demand for the Rupee than there are Rupees to sell, its price goes up. That is, it ‘appreciates’. When the opposite happens, the price of the Rupee goes down. That is, it ‘depreciates’.

Idea IV: Exchange rates change your country’s business dynamics

Imagine you have a factory that makes shoes, which you export to people abroad for Rs. 1000 a pair. Your customers are all in the United States and pay for your shoes in Dollars.

You started this business when each Dollar cost 80 Rupees, so each pair of shoes cost your customers $12.5. Now think of two scenarios:

One, the Rupee appreciates, until each Dollar costs 70 Rupees. Your shoes suddenly become more expensive — they cost more than $14 per pair — though you didn’t do anything wrong.

Two, the Rupee depreciates, until each Dollar costs 90 Rupees. Your shoes become cheaper for your customers — they now cost $11 per pair — even though you didn’t improve your manufacturing processes in any way.

See, the exchange rate is very important. It has a very real impact on businesses. It changes the price of getting a loan from abroad. It changes how attractive your company is to investors. It changes the price at which you can import raw materials, or export your products.

It also has an impact on regular people like you and us, by the way. For instance, almost all of the petrol we use is imported from abroad. So the price you pay for petrol depends on the price of the Rupee. When the Rupee falls in value, your petrol becomes more expensive.

Idea V: Where there are markets, there are traders

A lot of the activity in foreign exchange markets comes because of genuine business: people trading with each other, people working and sending money home, people investing in other countries — that sort of stuff.

However, two other participants drive a lot of currency trading.

One, some traders speculate on currency markets. There are all sorts of instruments — including leveraged instruments like currency options — that currency markets allow you to bet on.

Two, there are Central Banks. Central Banks often buy or sell their currencies, thereby creating artificial demand or supply. By doing so, they can push their currency in any direction they like.

With all these ideas out of the way, let’s dive into what’s really been happening.

In the post-COVID years, the price of the Dollar has been exceptionally high compared to most international currencies:

There are many reasons for this. A lot of the world’s economies have looked extremely weak since COVID struck. The United States, meanwhile, has done very well, with above-average GDP growth and an exceptionally tight labour market. On top of this, investors are terrified of investing in most of the world right now and have parked much of their money in the ‘safe’ American market. Because of this, a lot of money has steadily poured into America in the last few years.

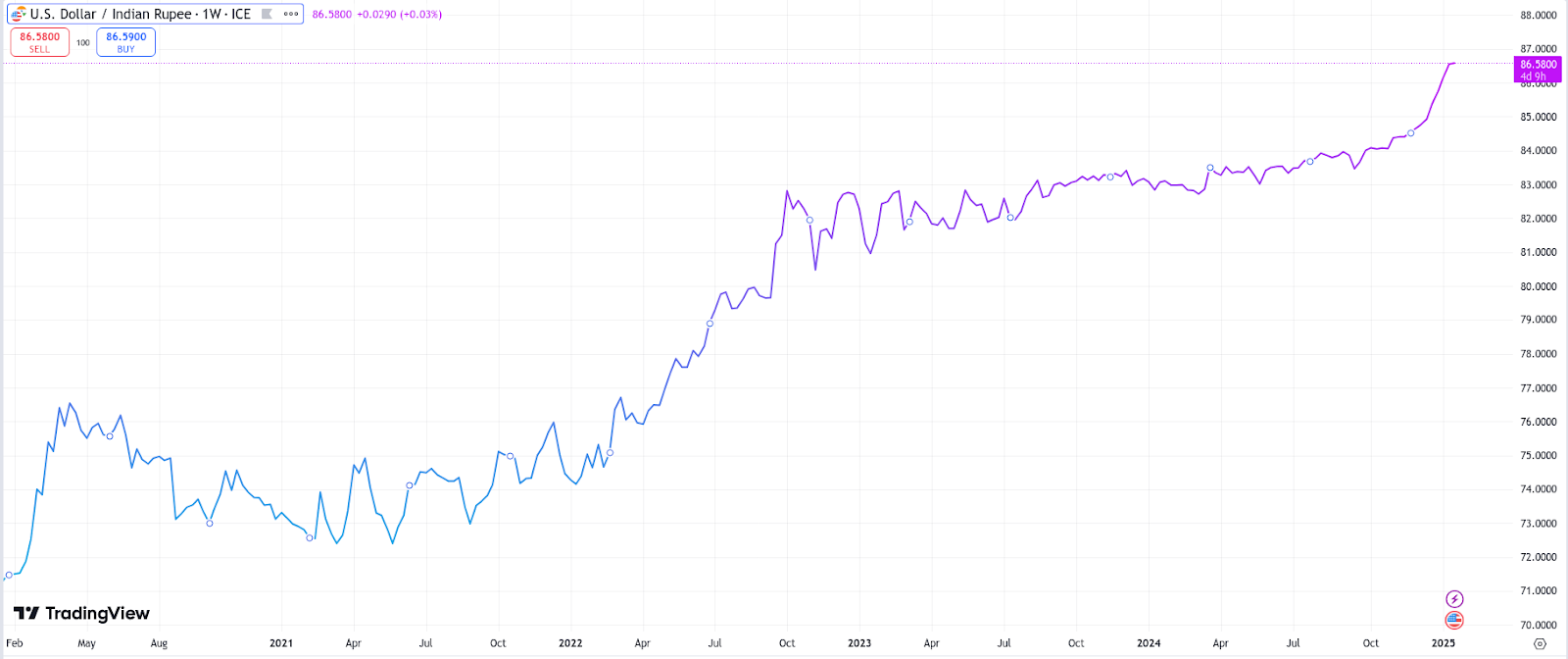

You see this effect when you compare the Dollar to the Rupee. Over the last few years, the Rupee has constantly fallen against the Dollar. The latest fall — to an all-time low of Rs. 86.5 per Dollar, is just a continuation of this trend:

But here’s the thing. In comparison to the rest of the world, this is hardly any movement at all! Pretty much every country has seen their currency fall against the Dollar off-late. If anything, the Rupee’s fall has been quite gentle, compared to what most other countries have seen.

Why so? Here’s one possible factor: through this time, the RBI has played an unusually big role in guiding the price of the Rupee. It has recently been very active in currency markets.

Here’s a gist of what it did:

Whenever there was a surge of foreign currency coming into India, the RBI bought a lot of that currency, and kept it with itself, as its “foreign reserves”. All this money would have otherwise been exchanged for Rupees, causing the Rupee to appreciate. The RBI has, in essence, kept the Rupee down.

When the price of the Rupee went down too fast in foreign markets, the RBI ‘defended’ its price. It sold the same foreign reserves it had accumulated in better times, buying Rupees in exchange. In essence, it artificially propped the price of the Rupee up.

Our foreign reserves have fluctuated wildly over this period:

This isn’t new. The RBI has always stepped into foreign exchange markets from time to time. You’ll see similar moves from the central banks of most emerging markets. However, the RBI ramped up this activity quite a bit after August 2022. And the results are clear—the Rupee-Dollar exchange rate has barely moved since then.

To many observers, it feels like the RBI has practically fixed the Rupee’s exchange rate and is refusing to let it move. This has created a lot of worry. The exchange rate plays a big role in how business works in a country. If the RBI keeps the Rupee’s value too high, it makes us less competitive as an exporting nation, allowing countries like Vietnam or Indonesia to win important contracts instead of us. On the other hand, if the Rupee’s value is kept too low, it becomes harder for us to import essential goods like oil or steel, which pushes up prices across our economy.

Economists believe that markets discover the ‘right’ price of something, by balancing supply and demand. When you interfere with the markets, odd things happen. As the economists Anand, Felman, and Subramanian point out, for instance, the RBI’s actions created a weird opportunity, where it became much cheaper to take loans from abroad than to approach Indian banks. This pushed many companies to do that — replacing their domestic borrowings with foreign capital. As they pay off these loans, the price of the Rupee could fall even lower:

In a recent paper, though, the RBI pushes back against this narrative.

It claims that markets don’t always reflect any deeper fundamentals about an economy. Many short-term factors can distort prices. In particular:

Foreign portfolio investors often invest with short time horizons and buy or sell something based on momentary price movements. This creates a substantial amount of volatility — as large sums of money can enter or leave a country overnight.

In times of excessive market froth, speculators bring a lot of “hot money” to currency markets, making bets that don’t reflect underlying trade activity.

These sources of money are temporary and volatile, and mess up the ‘real’ prices of a currency. To the RBI, these affect currency prices much more than a country’s actual economic condition.

This can be a problem — especially in emerging markets, which are relatively illiquid, and where a small amount of activity has the ability to cascade into a full-blown crisis. The world saw this first-hand in the Asian Financial Crisis of 1997, for instance. Back then, lenders panicked about Thailand’s ability to service its loans, which set off a massive chain reaction that sent most of East and Southeast Asia into a multi-year crisis. Ever since, emerging markets have always kept a watchful eye on currency markets.

The way the RBI sees things, its interventions are solely meant to eliminate volatility from the markets. It’s not trying to fix prices — it just wants to fix abnormal spikes and dips in prices.

Key Takeaways

We know this has been a lot to follow. But as an investor, here are your three big takeaways:

It’s important not to get too emotional about how high the Rupee is. These price movements are baked into the fabric of the international monetary system. It’s better to have a low price than the wrong price.

The exchange rate changes many economic dynamics in a country — from trade to investment, to inflation. As an investor, understanding these ripple effects can help you anticipate opportunities and risks, such as export-oriented industries benefiting from a weaker Rupee or import-dependent sectors facing cost pressures.

Currency markets have a big player—the RBI—which is ready to spend thousands of crores to keep things balanced. That’s something we should keep in mind when thinking about any potential investment.

SEBI Brings Transparency to Mutual Funds

The Securities and Exchange Board of India (SEBI) recently announced an important change in how mutual funds in India present their performance to investors.

In a new circular, SEBI directed mutual fund companies to disclose a metric called the Information Ratio (IR) for all equity-oriented schemes. This measure will be updated daily on mutual fund websites and will also be available in machine-readable formats on the Association of Mutual Funds in India (AMFI) website.

But what does this mean, and why is it so important? Let’s break it down.

To understand the significance of this move, we first need to explain what the Information Ratio is and why SEBI wants mutual funds to disclose it.

At its core, IR is a simple financial metric that helps investors evaluate a mutual fund's performance relative to its benchmark. What sets IR apart from other metrics is that it considers the crucial element of ‘risk’.

And beyond just numbers, IR is also looked at as a judgement metric for a mutual fund manager’s skill. It helps investors figure out how consistently and effectively a fund manager can beat the benchmark while managing the risk that the fund undertakes. Think of it this way, a fund manager can have one or two good years, but that tells you nothing about their skills. In a bull market, it’s often hard to lose money even if you try. But fund manager performance should be measured over long periods of time, and the information ratio is one helpful metric in evaluating the skill vs luck of fund managers.

So, in straightforward terms, IR shows how much extra return a mutual fund generates for every unit of additional risk it takes compared to its benchmark index.

If this still feels complicated, let’s use an example to simplify it.

Imagine two mutual fund managers—let's call them Manager A and Manager B. Manager A generates a 30% return in a year, while Manager B delivers a 40% return. At first glance, Manager B seems like the better performer. But if Manager A takes on much less risk to achieve that 30%, while Manager B takes significantly more risk to achieve 40%, the story immediately changes.

And this is why IR matters. If you judge a fund only by its past returns, you may not get the full picture of how it will do in the future. During stable or bull markets, higher-risk funds often do well because momentum is on their side. But, in turbulent times, those same funds can get hit the hardest.

IR not only looks at how much return a fund delivers but also talks about how efficiently those returns are generated, given the risks involved. A higher IR means a fund is better at managing this balance and offers more value for every unit of risk you take with your money.

Of course, for a long time, mutual funds have disclosed metrics like beta, alpha, and sharpe ratio, etc. and each of them serves a specific purpose. For example sharpe ratio tells us how much return a fund generates for each unit of risk it takes.

But the thing is, none of these metrics capture both, excess returns and performance consistency, as effectively as the IR does. So, by mandating daily disclosure of this metric, SEBI aims to give investors a clearer and more holistic view of a mutual fund’s performance.

In India, this is particularly important. That’s because investors usually buy mutual funds in our country almost solely based on past returns.

And as you’ve probably realized by now, while returns are a key part of the equation, they don’t tell the full story. A fund delivering high returns but taking on excessive risk might not be the best choice for long-term investing, and this is exactly what the IR addresses. So the next time you are evaluating active mutual funds to invest in, this information ratio is a useful metric to consider.

But all that said, while SEBI’s mandate is a great step forward, the bigger challenge will be in making this metric a standard part of how investors evaluate mutual funds. If people continue to focus only on high returns without considering the risks involved, the purpose of metrics like the IR will be lost.

Tidbits

Perplexity AI has made a bold $50 billion bid to merge with TikTok's US operations, aiming to combine TikTok’s massive user base with its AI expertise. The move could reshape digital advertising and alleviate TikTok’s regulatory challenges, positioning Perplexity AI as a tech sector disruptor.

The CCI fined Goldman Sachs ₹40 lakh for failing to notify its ₹1,070 crore Biocon Biologics investment under regulatory norms. Strategic rights tied to the investment triggered mandatory disclosure, underscoring the importance of compliance in financial transactions.

MRF is driving growth with EV-specific tyres for major OEMs and contributions to India’s defense projects like Sukhoi jets and Tejas aircraft. With export revenue surging 20–25%, MRF aims to increase its global share while investing heavily in manufacturing to meet demand.

-This edition of the newsletter was written by Anurag and Pranav

Every day, each team member shares something they've learned, not limited to finance. It's our way of trying to be a little less dumb every day. Check it out here

This website won't have a newsletter. However, if you want to be notified about new posts, you can subscribe to the site's RSS feed and read it on apps like Feedly. Even the Substack app supports external RSS feeds and you can read One Thing We Learned Today along with all your other newsletters.

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉 Join the discussion on today’s edition here.

You guys mentioned the Business Standard article, but conveniently did not the mention that the authors heavily insinuate that decreasing borrowing costs of major businesses was perhaps the goal. They even go as far as calling it a "subsidy" at the nations expense, and clearly the intended trickle-down effect did not happen.

Nice write-up. I like the narrative on how demand and supply plays an key role in world currencies and exchange rate determination. Keep up the good work!