Is it getting harder to afford a house?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Houses around the world are becoming impossible to afford

What's happening with oil

Houses around the world are becoming impossible to afford

In this story, we’ll dive into what’s being called the worst housing affordability crisis in over a decade. From London to Mumbai, housing markets are at a critical juncture. Let’s break down what’s happening globally and here at home in India.

Housing is a topic worth discussing because the International Monetary Fund (IMF) recently published a series of perspectives on housing markets around the world in its Finance and Development magazine. These insights were fascinating, so we’ve summarized them for you.

First, the big picture: Housing isn’t just about having a roof over your head. For most people, it’s the biggest source of both wealth and debt. It’s central to economic stability and represents security and a sense of belonging. But right now, that dream is slipping away for many, especially young people.

The numbers are alarming. According to new research from the IMF, housing is less affordable today than it was during the bubble that led to the 2008 financial crisis. The crunch is hitting hardest in countries like the United States, United Kingdom, Australia, Canada, Germany, Portugal, and Switzerland. In the U.S., housing affordability has dropped from around 150 on the affordability index in 2021 to the mid-80s by 2024. The UK has seen a similar decline, from 105 to the low 70s. While the IMF’s research doesn’t cover India extensively, we’ll get to the local situation shortly.

One fascinating aspect of this crisis is the psychological element driving it. It’s not just about interest rates—those account for only about a quarter of the changes in affordability over the past fifty years. What’s really pushing prices up is human behavior: the fear of missing out, combined with social beliefs that housing prices always go up. This creates a powerful cycle that keeps pushing the market higher.

There’s also a generational divide. While older generations benefited from rising housing prices since the 1980s, building wealth through home equity, today’s young people are facing a different reality. Many can’t even afford to rent, let alone buy a home.

So, what’s driving this crisis? It’s a perfect storm. High interest rates are pushing up mortgage costs, but the bigger issue is supply. Housing is severely constrained by zoning laws and land-use restrictions. Take Canada, for example. The country needs around 500,000 new homes each year to meet demand, but over the past two decades, they’ve been building just 150,000 to 250,000 annually.

Another surprising element is how house prices behaved during the COVID-19 recession. Unlike previous downturns where housing markets weakened, prices actually surged. Even as central banks raised interest rates to fight inflation, housing prices haven’t fallen as much as experts expected.

There’s also a darker side to the story. Criminal networks and corrupt politicians are using luxury real estate to hide illicit wealth, particularly in cities like New York, Miami, London, and Dubai. In London alone, foreign companies held £73 billion worth of properties in 2018, with 90% of these purchases made through tax havens.

This has sparked a global backlash against foreign buyers. Australia has tripled fees for foreigners buying existing houses. New Zealand banned foreign buyers from purchasing certain residential properties in 2018, and Canada has extended its foreign buyer ban to 2027. Even Singapore, which has traditionally welcomed foreign investment, doubled its stamp duty for foreign buyers to 60%.

Now, let’s look at India. A report by real estate portal Magicbricks shows that the price-to-income ratio in India has hit 7.5, much higher than the globally accepted level of 5. The price-to-income ratio essentially tells you how many years of your annual income it would take to buy a house. Ideally, this number should be 5 or below.

It’s concerning that Indians are now spending around 61% of their income on housing costs. That’s far above the 50% mark considered sustainable. The impact of this varies a lot depending on the city. In places like Chennai, Ahmedabad, and Kolkata, housing remains relatively affordable, with people spending 41-47% of their income on it. But in the Mumbai Metropolitan Region, the number skyrockets to an unbelievable 116%. Delhi isn’t much better at 82%.

There might be some relief on the horizon. A report from Magicbricks suggests that as more housing supply comes into the market, price growth could slow down. Stronger economic fundamentals and better global growth prospects might also lead to a slight drop in interest rates.

Still, the solution isn’t just about waiting for prices to go down. Experts believe we need to address deeper issues. That means cutting through regulatory hurdles, providing targeted support to low-income families, and rethinking zoning laws that limit housing supply. As Alan Kohler aptly put it, “It’s a global housing affordability crisis, but each country is unhappy in its own way.”

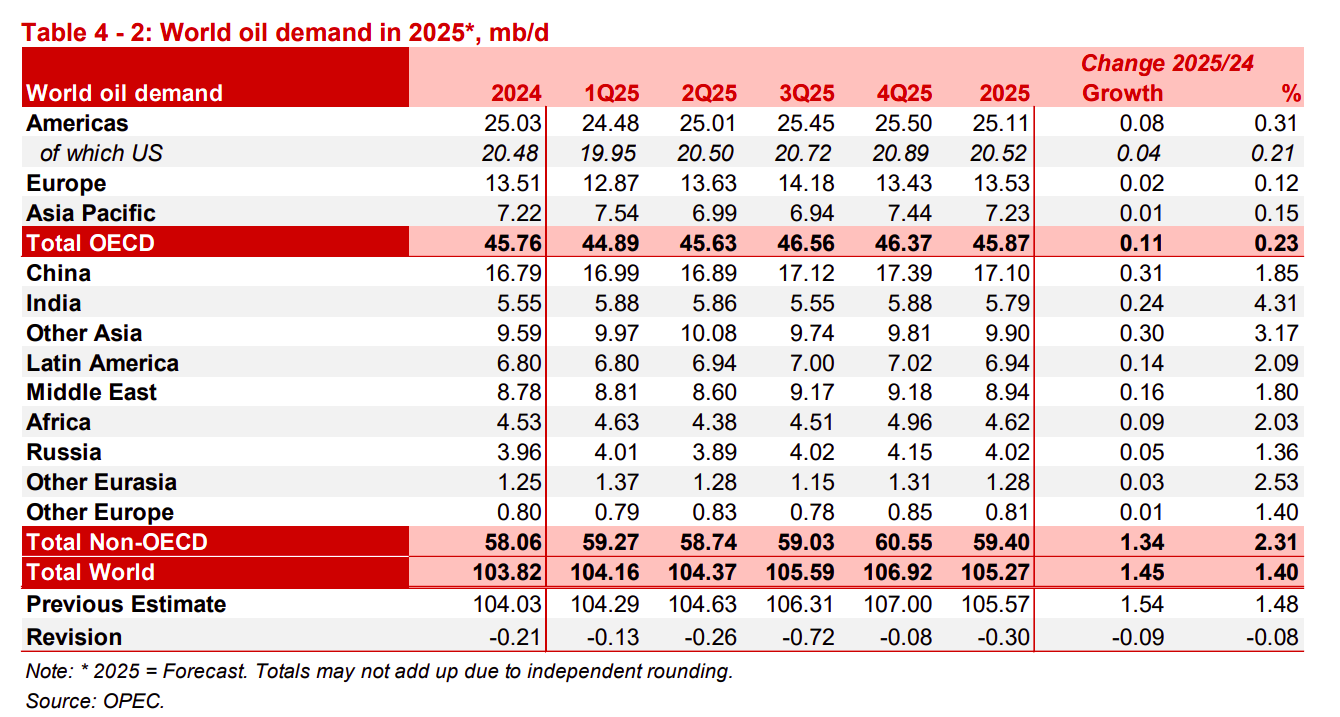

What's happening with oil

OPEC+, the group of 23 oil-producing nations led by Saudi Arabia and Russia, has made two key moves that could shape the energy market in 2025.

First, they decided to delay plans to boost oil production. They had previously planned a 2.2 million barrels per day (bpd) increase starting in January 2025, but now that’s been pushed to April.

Second, OPEC sharply lowered its global oil demand forecast for 2024. They now predict demand will grow by just 1.6 million bpd, down from their earlier estimate of 1.81 million bpd. That’s a 27% cut in their forecast since July, reflecting the tough conditions the oil market faced throughout 2024.

To understand why these decisions matter, let’s look at the global oil market as we approach the end of the year.

In 2024, the world has been consuming about 101 million barrels of oil daily. OPEC expects this to rise to an average of 103.8 million bpd in 2025, with a peak of 105.5 million bpd in the final quarter of the year. However, this growth is slowing noticeably.

Even with production cuts totaling 5.8 million bpd—roughly 6% of global daily demand—oil prices haven’t climbed significantly. Brent crude, the global benchmark, is trading around $73-$74 per barrel, far below the $80-$85 range that countries like Saudi Arabia need to balance their budgets.

The decision to delay production increases and maintain cuts reflects OPEC+’s response to these market realities.

This year, oil demand has been weaker than expected. China, a major driver of global oil consumption, has been hit by an economic slowdown. Manufacturing activity has been sluggish, consumer spending is underwhelming, and oil imports haven’t picked up as anticipated.

In the U.S. and Europe, high interest rates have slowed economic activity, which has further reduced demand for oil. Even in emerging markets like India, demand growth has been steady, but it hasn’t been strong enough to make up for the global slowdown.

Adding to OPEC+’s challenges is the increasing oil supply from non-OPEC countries. The U.S., now the world’s largest oil producer, is pumping oil at record levels, essentially canceling out the supply cuts OPEC+ has made since 2022. Meanwhile, countries like Brazil and Canada have also stepped up their production.

OPEC+ is in a tough spot. They need higher prices to support their economies, but increasing production risks flooding the market and pushing prices even lower. By keeping supply tight, they’re trying to stabilize prices while holding onto their market share.

At the start of the year, things looked more promising. OPEC expected strong demand growth of nearly 2 million barrels per day (bpd), driven by China reopening and recovering global economies. But those hopes have faded.

China, which accounted for over 60% of global oil demand growth in the last decade, struggled in 2024. Sluggish factory output and weak demand in the petrochemical sector have hit oil consumption hard.

The story wasn’t much better elsewhere. Europe faced stagnant growth, and the U.S. saw slower-than-expected growth due to rising borrowing costs. Globally, high interest rates have dampened economic activity, reducing demand from energy-intensive industries and transportation.

Meanwhile, the shift toward renewable energy and electric vehicles (EVs) is beginning to show its impact. EV sales surged in 2024, especially in Europe and China, cutting into gasoline demand. While this transition is gradual, its effects are becoming more noticeable.

In theory, OPEC+ supply cuts should push prices higher. But in practice, the market has balanced itself through several factors:

Non-OPEC production is booming. The U.S. is pumping oil at record levels, and Russia has kept exports flowing despite sanctions. This extra supply has offset much of OPEC+’s efforts to reduce output.

Demand growth is weaker than expected. A sluggish global economy has softened oil demand, especially in transportation and manufacturing.

Traders are cautious. The International Energy Agency has predicted a potential oversupply of 800,000 bpd by 2025, thanks to rising production from non-OPEC countries. This bearish outlook is keeping prices from climbing.

For oil-importing countries like India, OPEC+ decisions have significant consequences. If supply remains tight and prices go up, consumers will face higher fuel costs, potentially driving up inflation and affecting everything from transportation to food prices.

On the other hand, if global demand stays weak and prices remain low, countries like India could benefit from smaller import bills.

But the bigger picture is worrying for OPEC+. Their control over the market is slipping. With demand growth slowing and competition from non-OPEC producers increasing, OPEC+ is facing a tough fight to stay relevant in a rapidly changing energy landscape.

Tidbits

Jubilant Bhartia Group is acquiring a 40% stake in Hindustan Coca-Cola Holdings for around ₹12,000 crore. HCCB, which saw a 10% revenue growth to ₹14,021 crore in FY24, aligns with Coca-Cola’s divestment strategy and Jubilant's diversification goals, signaling a potential public listing.

Google’s Gemini 2.0 AI model offers a 9% performance boost over its predecessor, introducing advanced agentic AI features. This positions Google to challenge Microsoft and OpenAI in the AI race, catering to businesses with cutting-edge multimodal capabilities.

US inflation rose to 2.7% in November, with core CPI remaining sticky at 0.3%. While a Fed rate cut is widely anticipated, stubborn inflation complicates the path for sustained monetary easing.

- This edition of the newsletter was written by Bhuvan and Krishna

Thank you for reading. Do share this with your friends and make them as smart as you are 😉 Join the discussion on today’s edition here.