India’s two-wheelers drift through a collision of forces

Between premiumization, higher input costs, and a historic oil shock.

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

India’s two-wheelers drift through a collision of forces

India’s biogas problem

India’s two-wheelers drift through a collision of forces

If you filled up your petrol-fueled two-wheeler recently, your pocket probably felt a painful sting. And with petrol prices having been hiked twice in less than a week, that only seems to be getting worse.

If you’re like most of us, who ride a petrol-powered two wheeler to work every day, there’s a thought that has probably crossed your mind at least once this month. Maybe it’s time to go electric. No more waking up to news of another fuel hike. Just plug in at night, ride in the morning.

But then you think about it a little more. What’s the range of an EV? Where’s the nearest charging station? The fact that the Hero Splendor — arguably the bike most symbolic of India — starts with a kick and a grunt and doesn’t need a software update is comforting. The total cost of ownership of an EV is still not convincingly low enough for people to make a complete switch away from petrol bikes, yet.

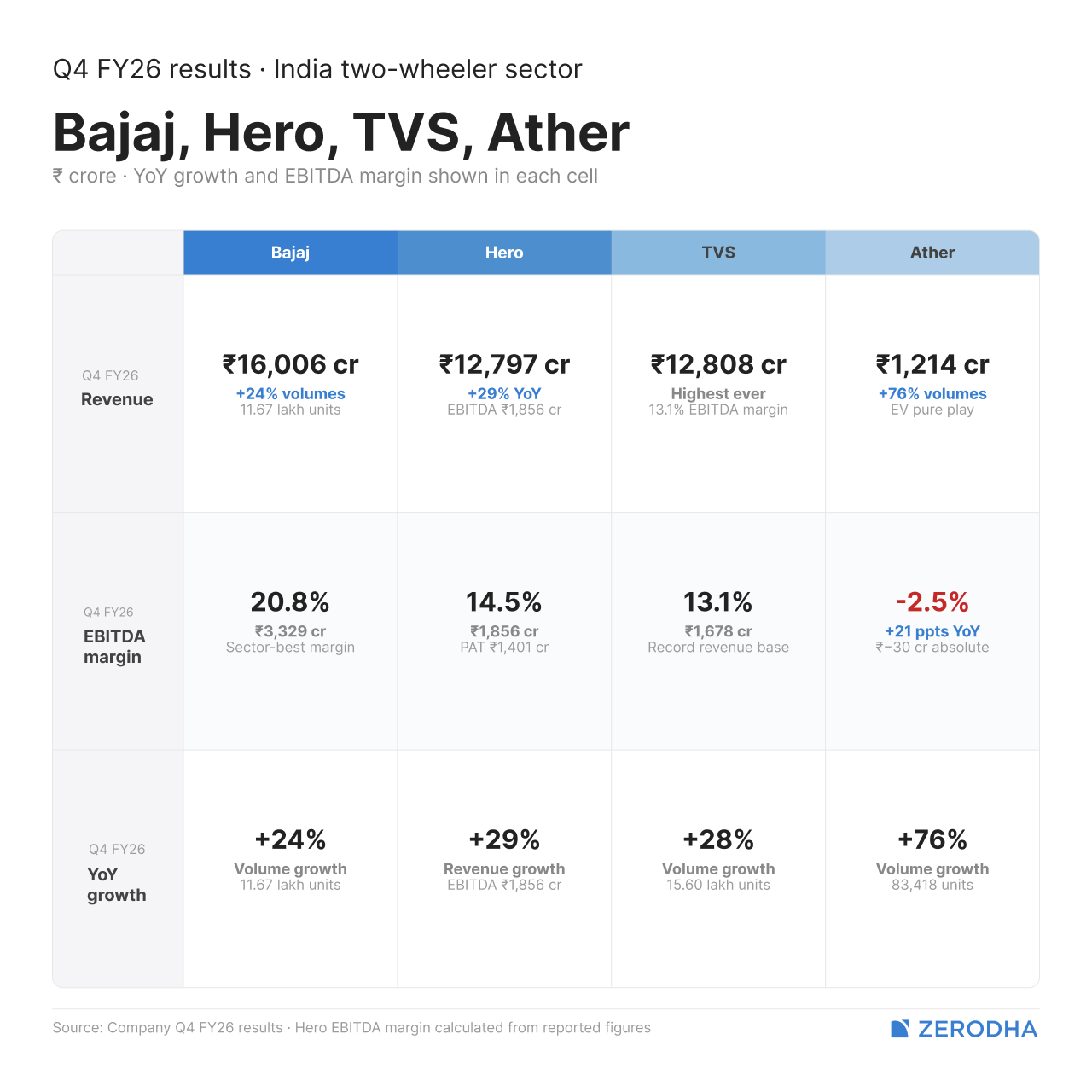

So, we looked at the Q4 FY2026 results of Bajaj Auto, Hero MotoCorp, TVS Motor and Ather Energy to see how the two-wheeler segment is navigating all of this.

The numbers

Bajaj Auto posted ₹16,006 crore of revenue, a 20.8% EBITDA margin, and total two-wheeler volumes of 11.67 lakh units, up 24% year on year. Interestingly, it was the premium end of the portfolio, not the mass market, is what powered the quarter. Its premium brands, KTM and Triumph, delivered a record domestic quarter of nearly 43,000 units, up 43%.

Meanwhile, Hero MotoCorp hit ₹12,797 crore of revenue, up 29% year on year, with an EBITDA of ₹1,856 crore and PAT of ₹1,401 crore. Hero’s growth was broad-based across scooters, EVs, and premium bikes.

TVS Motor reported its highest-ever quarterly revenue of ₹12,808 crore, a 13.1% EBITDA margin, and total sales of 15.60 lakh units, up 28%. Motorcycles, scooters, EVs, exports and three-wheelers all contributed. However, TVS is also very apprehensive of the future, telling analysts that its April dispatches were hit by workforce shortages, raw material delays, and limited container availability, even though retail demand stayed strong.

Ather Energy is the purest EV play of all of them. Q4 volumes hit 83,418 units — up 76% year on year — with total income of ₹1,214 crore and an EBITDA margin of -2.5%, a 21 percentage point improvement from a year ago. The loss is narrowing fast, but Ather remains more exposed to battery costs, rare-earth prices and subsidy policy than the legacy players.

The squeeze

The Strait of Hormuz disruption has undoubtedly been on everyone’s mind this quarter. It has tightened energy and shipping flows, feeding into higher fuel prices, container shortages and costlier energy-linked inputs.

Earlier, we had spoken about how rising raw material costs were eating into the industry’s margins. This quarter, it quite naturally got worse. When energy gets expensive, so does everything that needs energy to produce. That includes the steel, copper and aluminium that two-wheelers are made of.

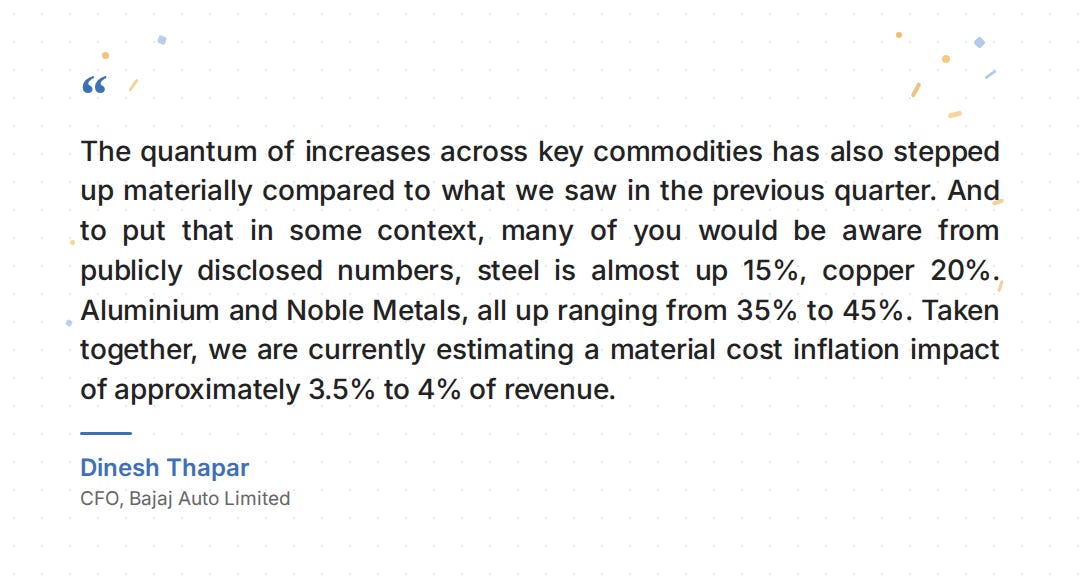

Bajaj’s CFO walked through just how bad it got in quantified terms. Steel costs were up 15%, copper 20%, and aluminium and certain metals had moved sharply. All told, Bajaj is looking at an extra 3.5–4% of revenue being eaten up by raw material costs alone.

Bajaj also said it had covered just ~40% of this through a price hike from 1 April. But hiking the price more would risk pushing away the price-sensitive buyers who make up the bulk of the market.

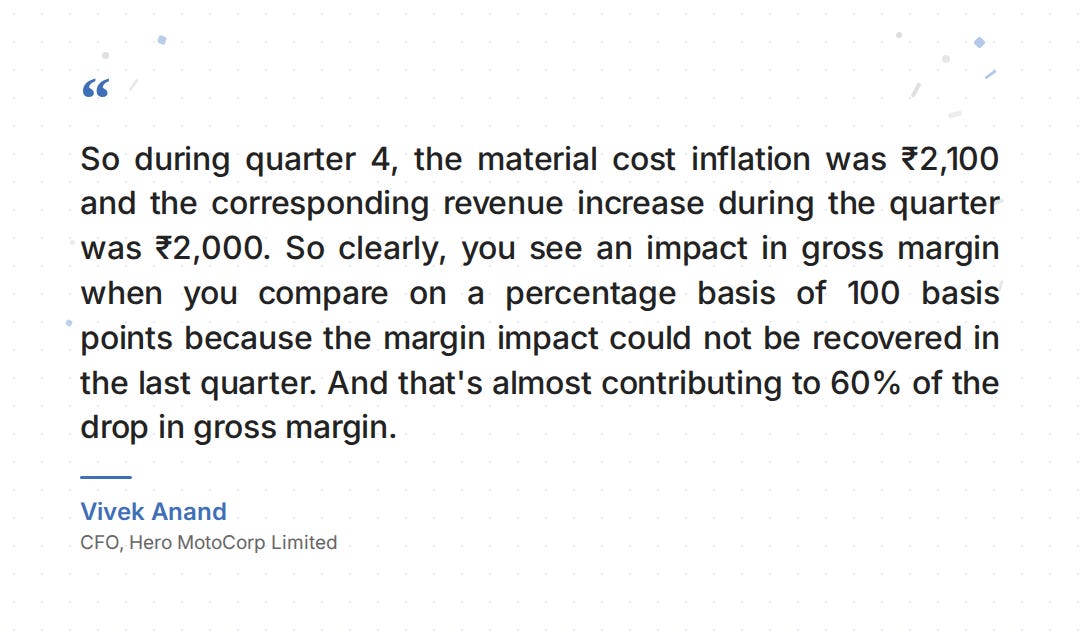

Hero also faced a similar squeeze. Its CFO, Vivek Anand said the cost of raw materials went up by about ₹2,100 for every vehicle it made in Q4. Hero raised prices by ~₹2,000 per vehicle to compensate, which sounds like it nearly covered the gap. But any which way, the margin still shrinks in percentage terms.

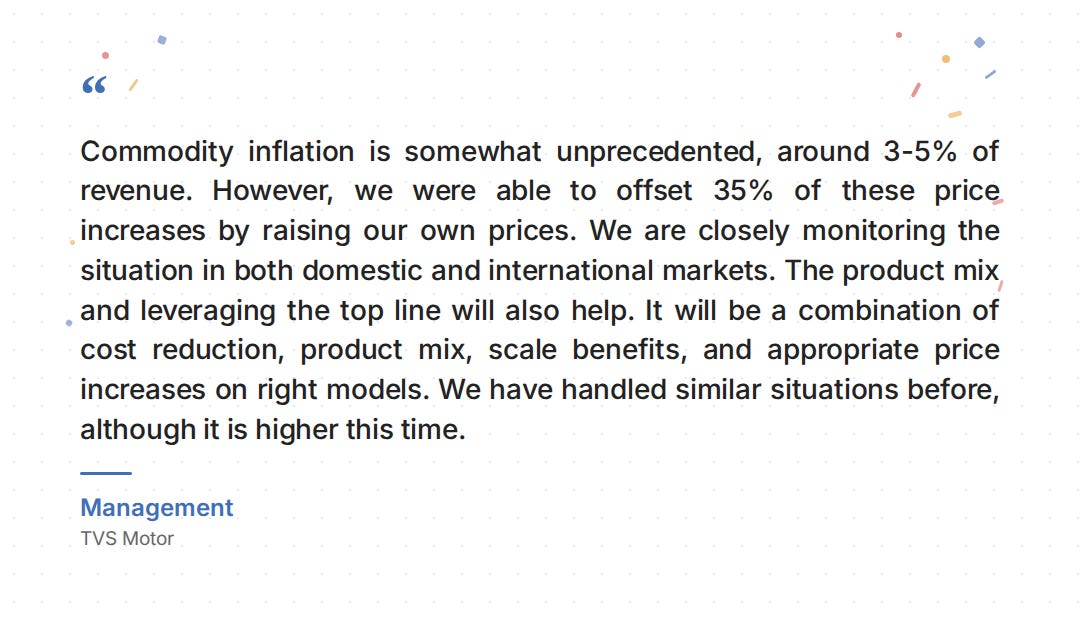

For TVS, commodity costs ate up 3–5% of its revenue, the worst they’ve seen. So far, TVS has only been able to offset about a third of this through price hikes. For the rest, it would rely on cost reduction, better product mix, scale benefits and selective price increases on the right models. They said they’ve handled similar situations before, but this one is worse.

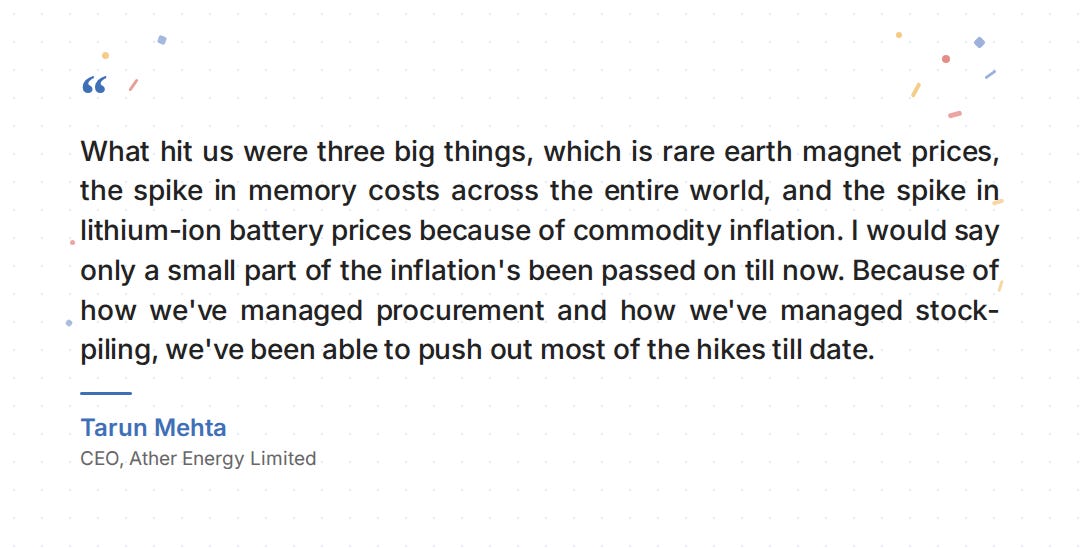

For Ather, the challenge is even more severe. Prices of rare earth magnets, memory chips and lithium-ion batteries — all the key components of an EV — spiked during FY26. Only a small part of the inflation had actually been passed on so far. Ather is sitting on unrecognised cost pressure that will either show up in future margins or price hikes on products that are already more expensive than their petrol or diesel equivalents.

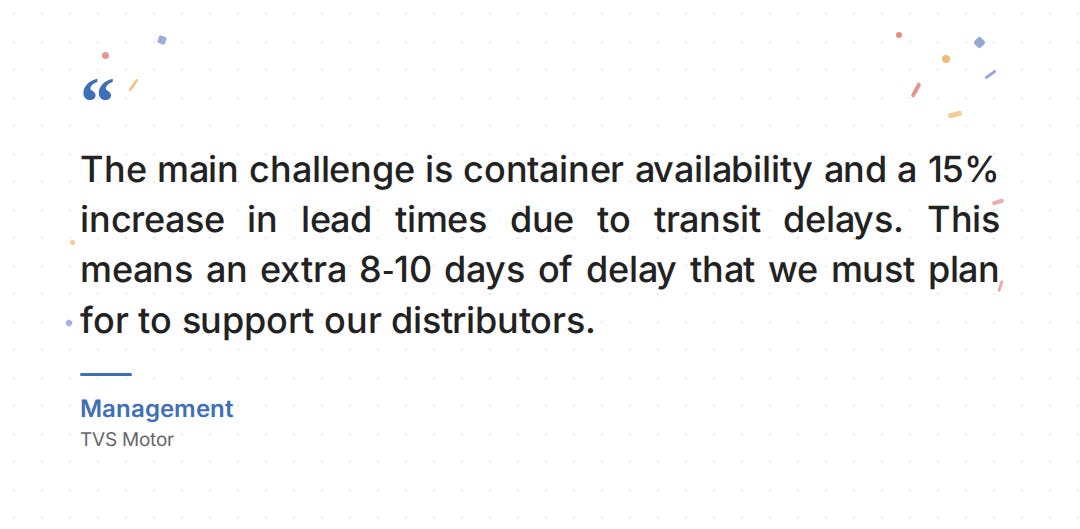

The Hormuz disruption also directly affected exports. For Indian two-wheeler companies that ship to the Middle East, Africa and beyond, it has meant fewer containers and longer waits. TVS told analysts that shipping times had stretched by about 15%, adding 8–10 extra days per shipment.

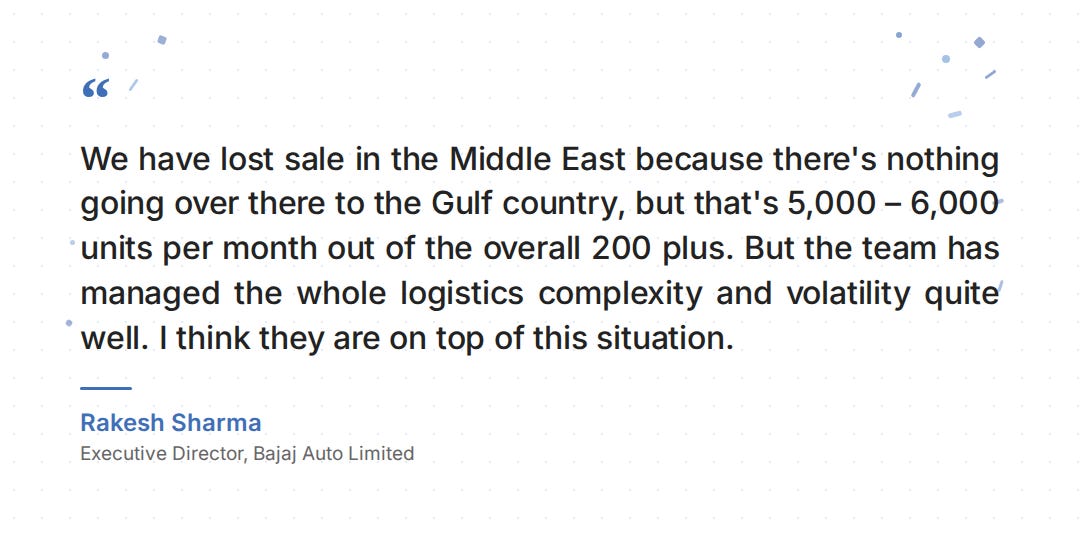

Bajaj said it lost 5,000–6,000 units of monthly sales in the Gulf region, though it managed to reroute shipments to non-Gulf markets well enough that the damage was contained.

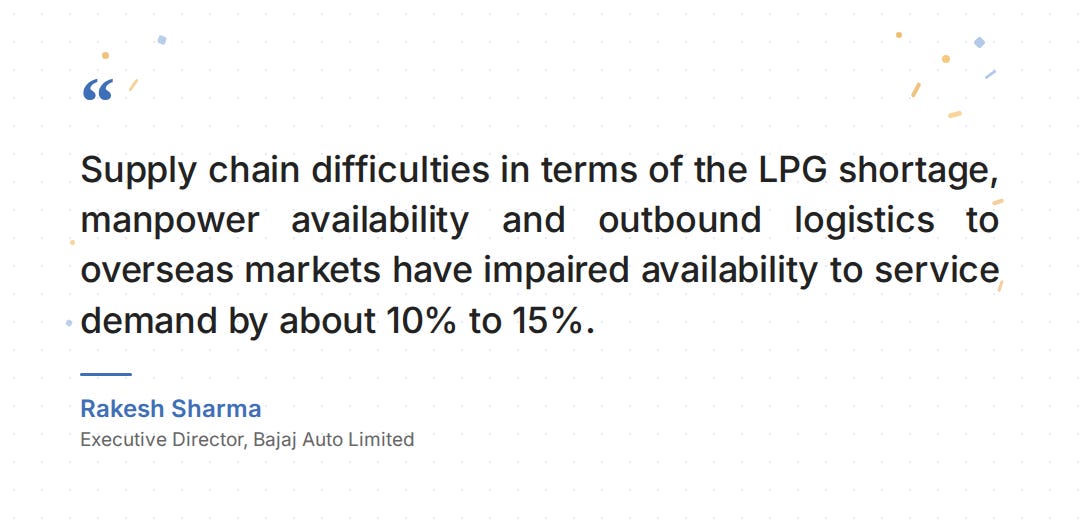

The pressure has also rattled the humdrum of two-wheeler factories. Bajaj estimated that it lost 10–15% of potential demand in April because LPG shortages shut down vendor factories, workers migrated back to their hometowns, and containers simply weren’t available. TVS flagged the same issues. Hero said it kept all its plants running without disruption, but acknowledged the commodity and labour cost picture was “changing every day“.

These headwinds didn’t crush Q4, as revenue grew strongly across the board. But by April, the commodity costs, shipping delays and vendor shutdowns had started catching up.

How they’re protecting margins

So, in the face of these challenges, without relying heavily on price hikes, how did the legacy players protect profitability?

The most important lever that two-wheelers pulled on that front is actually product mix. The logic is simple: a company makes more money on a higher-priced vehicle than on a basic commuter bike. Every company cited “product mix“ as a tailwind on their earnings call.

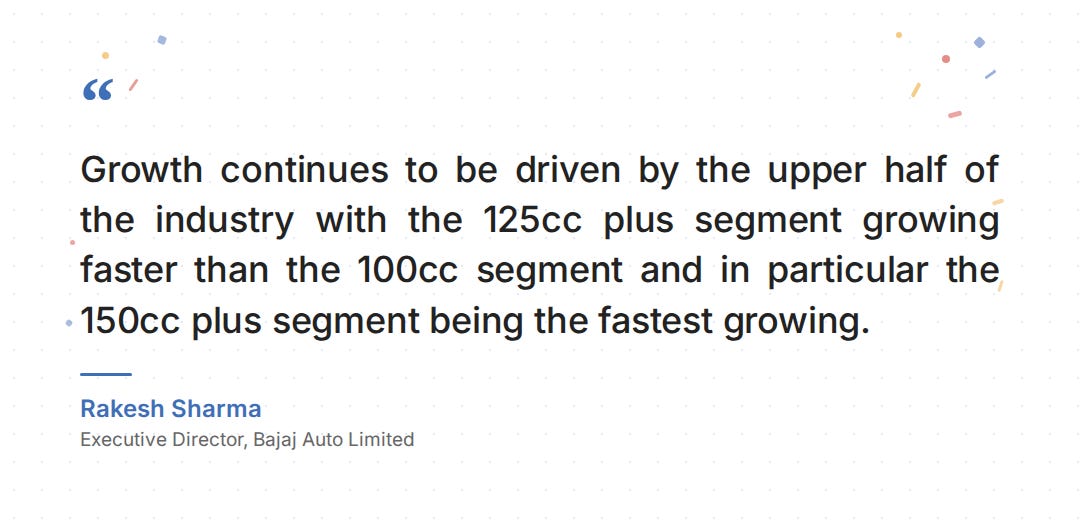

Consider what’s happening at Bajaj. The company launched 10 new Pulsar variants between October and March, and those models already account for half its domestic motorcycle sales. Its KTM and Triumph business hit 43,000 units in Q4, up 43% year on year. The sportier 150cc-plus bikes are selling at twice the rate of the broader market.

But, at the same time, the cheapest motorcycles — the 100cc commuters that millions of Indians depend on, are barely growing anymore.

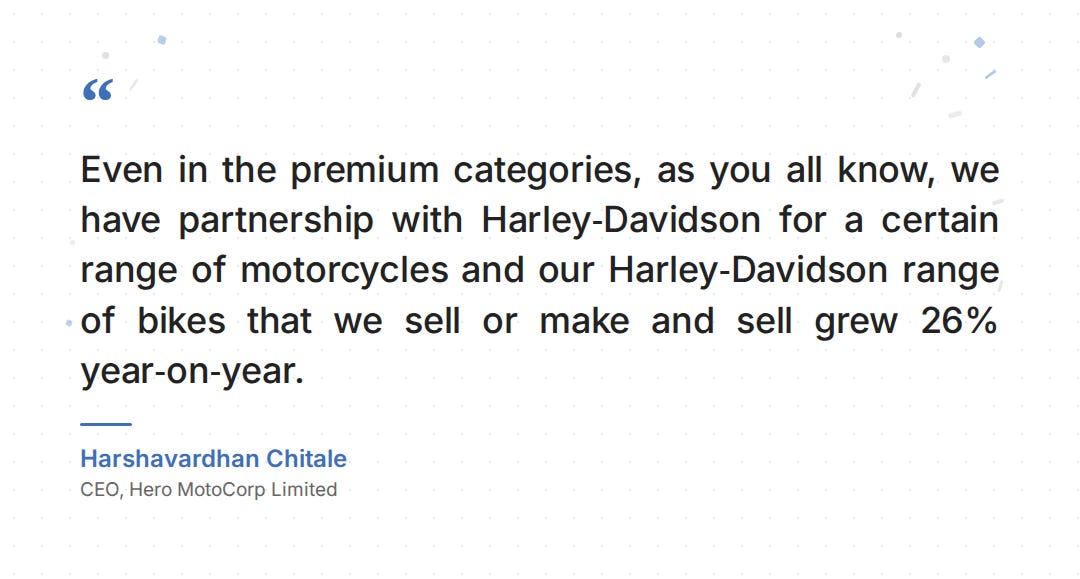

Meanwhile, Hero, which built its entire identity around the commuter bike, is now leaning on its Harley-Davidson range (up 26%) and scooters (up 48%) for growth. TVS’s Ronin, its premium motorcycle, went from 2,000 units a month to over 8,000. Still small in absolute terms, but the direction is unmistakable.

In essence, while the shift towards premiumization was a deliberate top-down choice, it seems to also be driven by the shifting preferences of the consumer market. After all, the growth of commuter bikes is also simultaneously slowing down. This is a structural change in the broad two-wheeler market.

But part of it is certainly also that the entry-level buyer, the one most sensitive to price hikes and fuel costs, is simply not showing up the way they used to. That’s good for margins today, but if the bottom of the market keeps hollowing out, premium demand alone may not sustain the kind of volume growth these companies need.

On the EV side, though, something different is playing out. Ironically, the same Hormuz crisis squeezing ICE margins may also be strengthening the consumer case for EVs.

Never let a crisis go to waste?

If you’ve been tuning into the podcasts our team has been putting out lately, you may have come across our conversation with Kyle Chan, an expert on Chinese industrial policy. Perhaps, the most provocative quote from the episode was this:

“Every day that the Strait of Hormuz is closed and every day that the Iran war continues is a month’s worth of free marketing for Chinese EVs and batteries and solar and clean tech.”

Well, something similar is playing out in India.

Even before petrol prices were actually hiked, the LPG shortages and fuel uncertainty had already started changing how people think about what powers their vehicle. When your cooking gas disappears and petrol feels like it could jump any day, electricity starts to look like the one thing that won’t let you down.

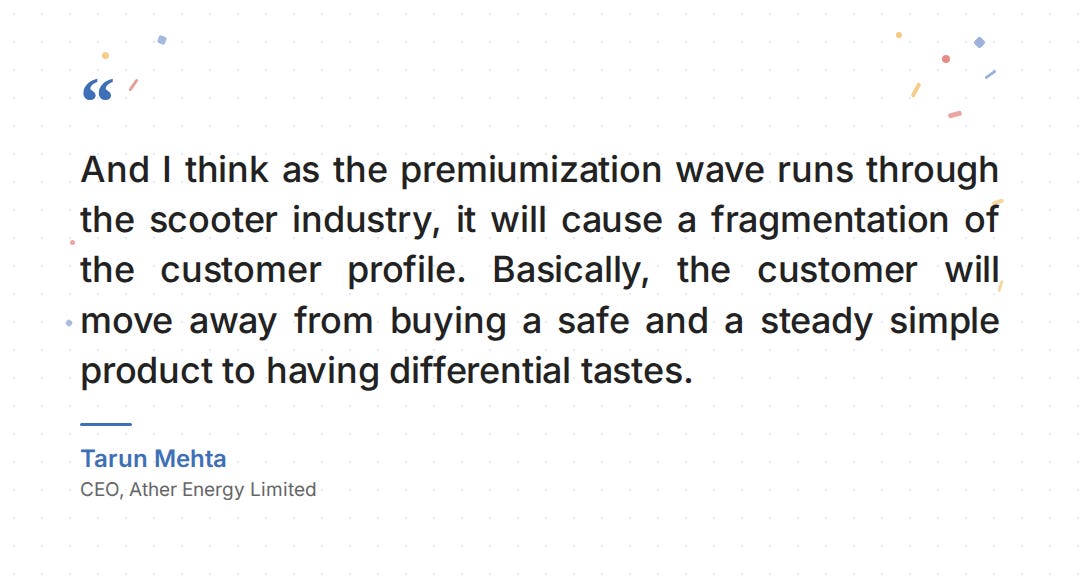

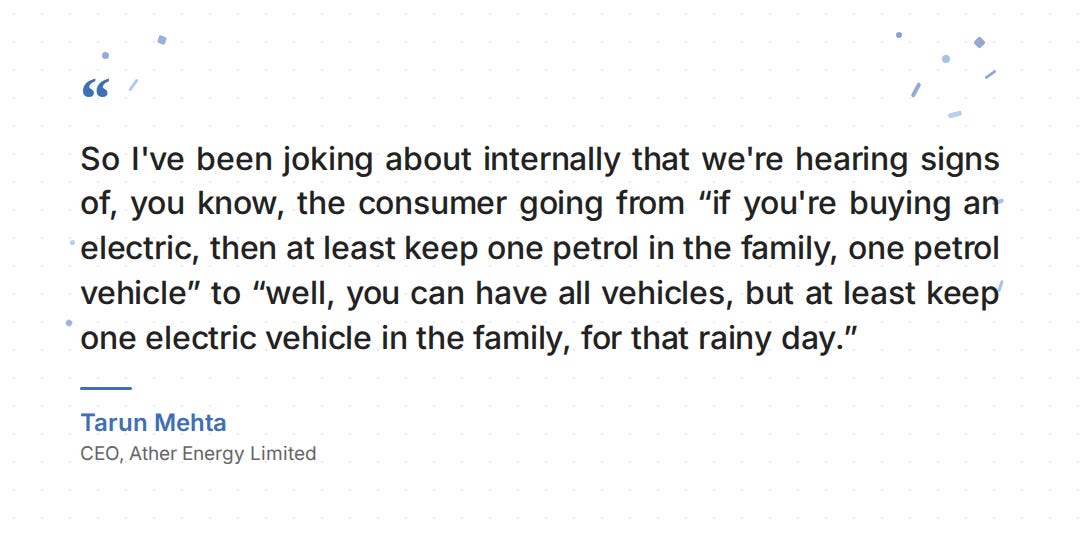

Tarun Mehta, Ather’s CEO, said the consumer mindset is flipping. A year ago, families would say “buy what you want, but make sure at least one vehicle runs on petrol.“ Now it’s becoming “buy what you want, but keep at least one EV in the house, just in case.“

Now, it’s still too early to see this show up cleanly in the two-wheeler EV numbers. Scooter buyers and three-wheeler operators respond to different triggers. But there is an observable shift in sentiment, and with petrol prices now hiked twice in a week, more buyers are seriously considering going electric.

What’s more interesting is that these companies are also starting to make money on EVs. As we covered in our earlier EV story, profitability was the missing piece of the puzzle. This quarter changed that.

Bajaj’s Chetak scooter, for instance, is no longer losing money on each unit it sells. This was nearly unthinkable two years ago.

On the other hand, Ather is still loss-making, but its operating losses shrank significantly. The company also brought down the cost of making each scooter by 9% over the year, partly through design tweaks and partly by switching to cheaper battery chemistry. Most of Ather’s overhead costs are fixed, so the more scooters it sells, the cheaper each one becomes to produce. These are all powerful tailwinds if volumes keep growing. But if they slow down for any reason, those same fixed costs pile back up fast.

Ather also makes money beyond just selling scooters. It offers a paid subscription called Pro-Pack that bundles software, connected services and extended warranties. 93% of buyers opted for it in Q4, the highest ever.

What’s ahead

So, what do we watch out for in the first quarter of FY27?

Well, for one, the commodity costs, particularly that of copper. They were rising anyway, but the Strait of Hormuz crisis has only made things worse. Its impact on two-wheeler sales only began showing up in April, so we have to wait for Q1 FY27 to see how the crisis unfolds.

Secondly, how much of the premiumization trend is sustainable? How much of it is driven because the Indian consumer wants more, and how much of it reflects the disappearance of the Indian middle class that buys commuter bikes? And how much does the answer to that change how long this trend can prop up margins?

Additionally, the PM E-DRIVE incentive window for registered electric two-wheelers ends on 31 July 2026, unless it is extended again. The next quarter might be able to decisively tell us how these companies plan to keep growing through all of that.

India’s biogas problem

In October 2018, India launched a programme called SATAT, or ‘Sustainable Alternative Towards Affordable Transportation’. The plan was to build 5,000 biogas plants across the country, to turn organic waste like cow dung, paddy straw, or kitchen scraps into a clean fuel, biogas, that could piggy-back on natural gas pipelines and pumps. This was to be finished by 2025.

Eight years on, we’re running somewhere between 130 and 170 plants.

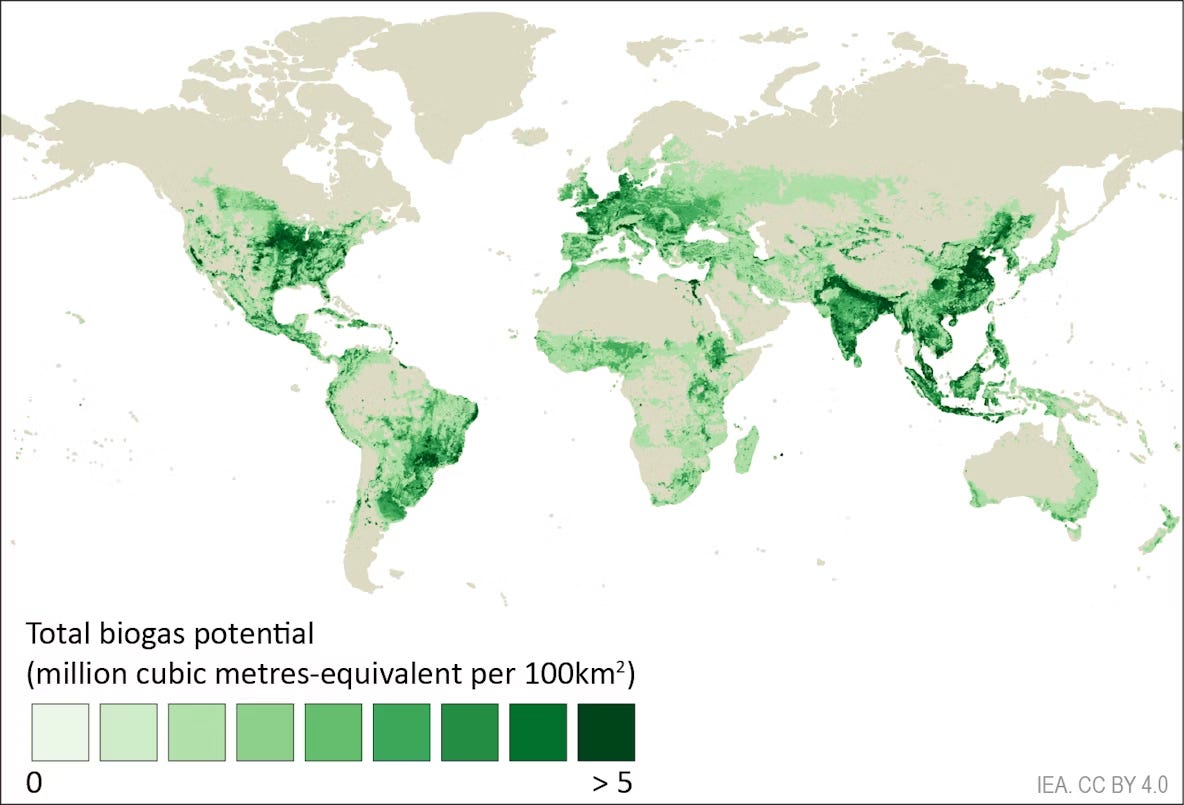

According to the International Energy Agency’s 2025 Outlook for Biogas and Biomethane, India’s sustainable biogas potential, alone, is larger than our entire natural gas consumption. We could potentially meet all our natural gas needs by just tapping our biogas potential. But we’re stuck utilising less than 5% of it. By volume, India sits on the largest organic waste base of any country in the world. Almost none of it is converted into anything useful.

By all accounts, biogas should work. Then why, after a decade of policy effort, have we barely moved the needle? And can we change that?

What biogas actually is

A biogas plant is, functionally, an industrial-scale stomach.

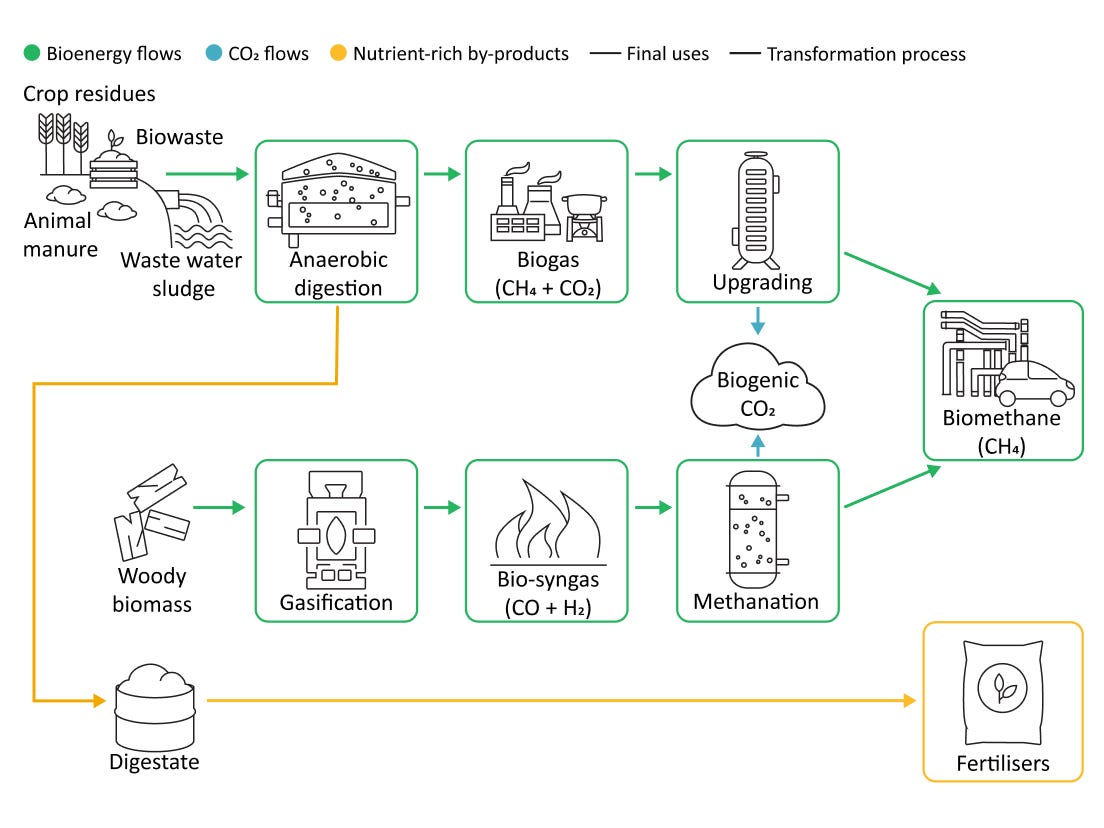

Organic waste goes inside a sealed tank called a “digester”, where it’s broken down by bacteria that thrive without oxygen, much like bacteria in a cow’s gut break down grass. As they work, they release a mixture of gases. That mixture is biogas: roughly 55-65% methane and 35-44% carbon dioxide, with traces of other gases.

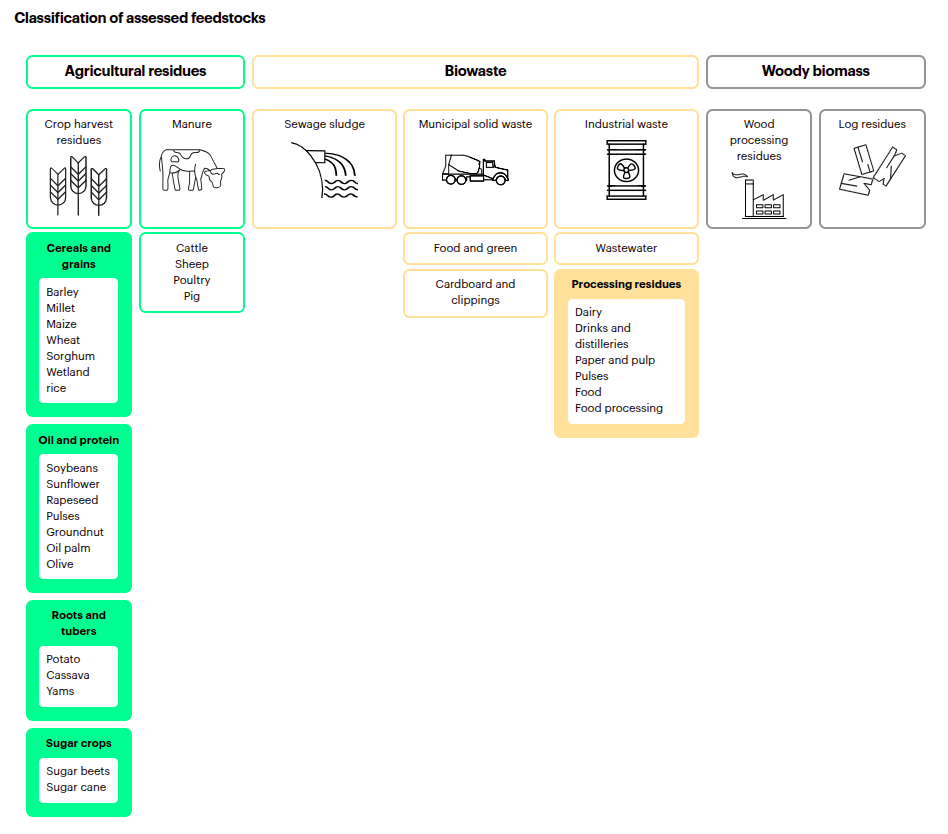

You can feed a biogas plant almost any organic matter. In India, they typically run on five feedstocks: cattle dung, agricultural residue, the pressmud left over from sugarcane crushing, municipal solid waste, and sewage. The bacteria don’t particularly care where their carbon comes from. What they care about is that the supply is consistent, the moisture is right, and the input isn’t contaminated.

You can use raw biogas straight out of the digester. You can pipe it into a village kitchen to replace firewood, or burn it locally to generate electricity. But those uses are limited. To plug into the modern gas economy — with CNG vehicles, household PNG connections, or industrial gas lines — you have to clean it further. You have to strip out the CO₂, other gases, and moisture, leaving behind a stream that is 95-98% pure methane.

That cleaned-up gas is called ‘biomethane’. If biomethane is compressed for transport and storage, it gets a different name: Compressed Biogas, or CBG.

Chemically, this biomethane is the same methane we get in conventional natural gas. It’s the same molecule — same calorific value, same combustion profile, same physical properties. And so, every piece of infrastructure that India’s building to move natural gas — City Gas Distribution pipelines, CNG pumps, household PNG connections — can carry biomethane without modification.

If we build more biogas capacity, a lot of the infrastructure we need thereafter will already be in place.

When the digestion process is done extracting gas, it leaves behind a physical residue: a wet, nutrient-rich sludge called fermented organic manure. That residue is, in principle, high-quality organic fertilizer.

Why biogas matters more than it sounds like it should

Think about this for a moment: we have a fuel that takes waste, runs on the infrastructure we are already building, and produces fertilizer as a byproduct. The case for scale looks self-evident.

And then, it comes with second order benefits.

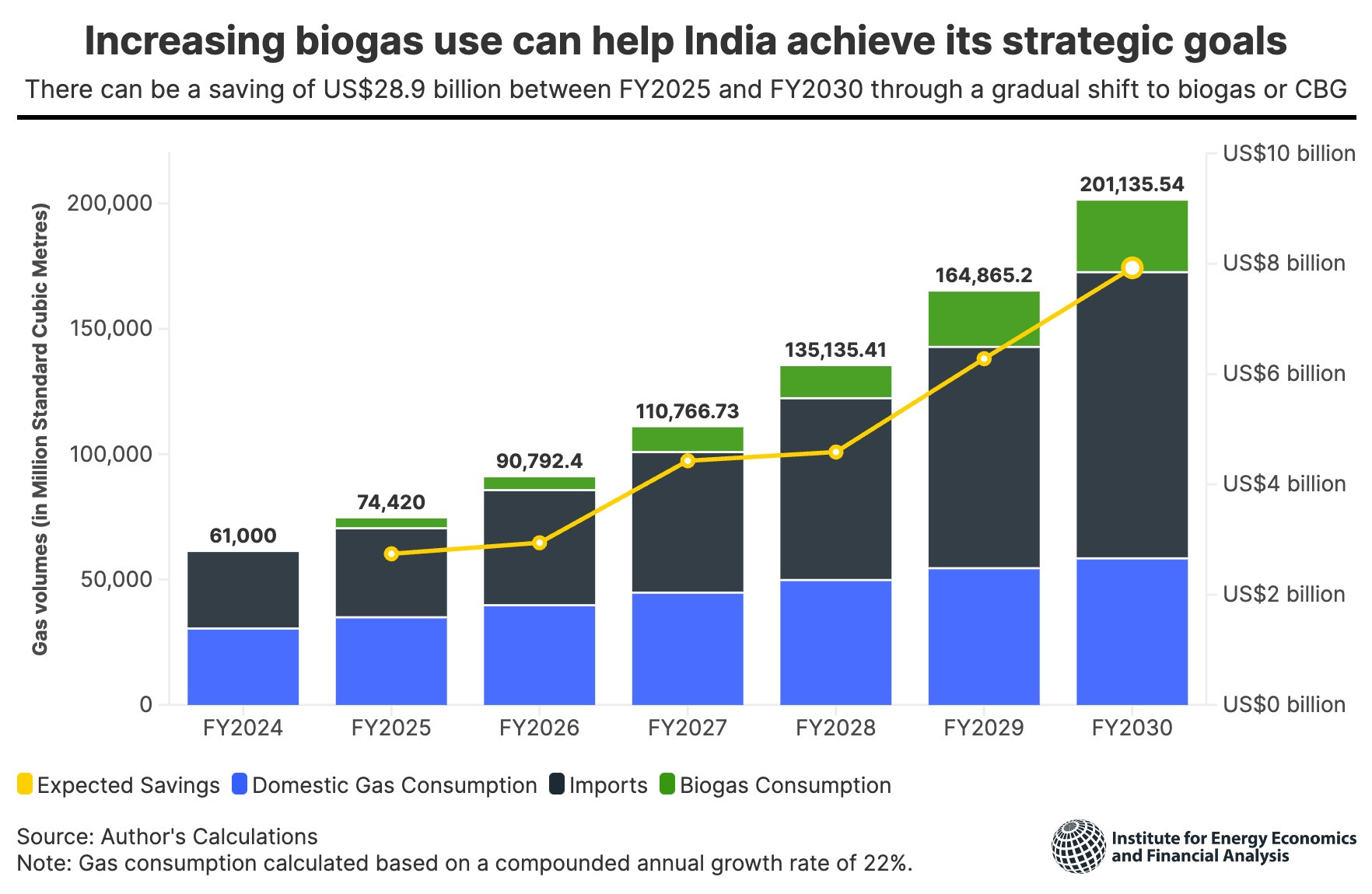

The first is that it slashes down our import bills. India imports roughly half its natural gas as LNG, and those imports are only slated to increase; as the government plans to raise the share of gas in our primary energy mix from around 6% today to 15% by 2030. That’s a lot of money flowing outside. According to the Institute for Energy Economics and Financial Analysis, if India can scale biogas to displace just one-fifth of our natural gas by 2030, we will save around $29 billion on LNG imports by FY 2030.

This has clearly caught the government’s interest. In November 2023, the National Biofuels Coordination Committee mandated phased CBG blending into both transport CNG and household PNG — much like blending ethanol into petrol. We were targeting 1% blending in FY 2025-26, which would scale up slowly to 5% from FY 2029. This ‘Compressed Biogas Blending Obligation’, or CBO, plugged a massive hole in our biogas program: one of the reasons SATAT couldn’t garner any interest was that no one would buy what these plants produced. The CBO closes that gap. Even a 1% mandate is a massive guaranteed offtake, which could seed a new sector.

Second, biogas could also become central to our push for clean cooking. India has been trying to move its households to gas-based cooking, instead of primitive sources like firewood or cow dung. Through the Pradhan Mantri Ujjwala Yojana, we expanded active LPG connections to roughly 318 million households. But that creates a terrible dependency: India imports about two-thirds of its LPG. This puts us at the mercy of global markets. A crisis like the one we’re seeing in the Middle East can send prices skyrocketing. In times like this, our poorest households quietly fall back to wood and dung.

One way out of this bind is to set up village-level biogas plants, which run on the same cattle dung and crop residue that the village already produces. This could completely insulate these villages from global volatility.

Third, there’s fertiliser. India spent around ₹1.88 lakh crore on chemical fertilisers in FY24, importing massive quantities of urea and DAP in the process. The slurry that comes out of a CBG plant is, in principle, a direct substitute for synthetic fertilizer. The Department of Fertilisers now pays ₹1,500 per tonne as Market Development Assistance for fermented organic manure sold from CBG plants. If that market actually develops, every tonne sold does two things: trimming India’s fertiliser bills, while improving CBG plant economics.

Finally, think of what this could do to our stubble problem. Every winter, paddy stubble burnt in Punjab and Haryana drags Delhi-NCR into a crisis of breathing air. The same paddy straw could become a valuable feedstock for biogas plants, which a farmer can be paid to sell rather than burn. This is one of those rare interventions that doesn’t depend on coercing farmers, but instead gives them a better alternative.

In short, biogas solves many of our problems at once. Few policy levers have this much potential. But then, what went wrong?

Why did it fail?

India generates roughly 62 million tonnes of usable organic waste every year. According to the IEA, we could potentially make around 87 billion cubic metres of biogas in a year.

But there’s a big barrier to getting there: logistics.

One of the most important numbers in biogas math is 50 kilometres. See, the inputs for a biogas plant, unlike crude oil or coal, aren’t concentrated in small regions. They’re spread thinly across millions of smallholder farms. Before processing, this is all waste — bulky, rotting mass with low calorific value. There’s only so far you can take it before transportation costs are too high. According to both CEEW and the IEA, transporting baled biomass beyond about 50 kilometres from the plant gate destroys project economics.

In practice, that’s the physical limit for how far a biogas plant could draw supplies from. India can’t scale this sector the way it scaled, say, oil refining. You can’t concentrate capacity in a small number of massive plants. One has to build hundreds of decentralised plants, each with its own 50-kilometre catchment area.

Within that circle, feedstock arrives in seasons. Most agri-residues peak post-harvest and soon disappear. Paddy straw shows up for a few weeks in October and November. Pressmud comes only when sugarcane is crushed. But a CBG plant needs to run 365 days a year to recover its capex. And so, it must collect waste during the harvest window, and then store it through an entire year.

The moment a plant starts operating, it’s hit by local supply economics. There are no government-defined benchmarks for the price of waste. Prices vary wildly from region to region: paddy straw that costs roughly ₹2,800 a tonne in Punjab can cost ₹3,600 a tonne in Chhattisgarh. And these prices change by hundreds of rupees over the course of a single season.

As a result, Indian biogas plants run at an average capacity utilisation of around 35%, with some running as low as 20%. According to the IEA, if we could only lift average utilisation from 35% to 44%, we would easily meet our 2030 blending targets without commissioning a single new plant.

And then, once a plant does produce gas, it runs into another logistics problem. Only ~15% of operational CBG plants are connected to the City Gas Distribution pipeline network. The other 85% have to truck their output in pressurised cylinders to depots hundreds of kilometres away. A plant in rural Madhya Pradesh selling to an HPCL outlet in Bhopal, in effect, has to run a trucking company alongside its gas business.

This is one place our subsidies have failed. India rewards building plants, but not running them. It makes more sense for an operator to commission a facility, bank the subsidy, and sit on a half-running asset, than spending on logistics. Generation-linked tariffs — paying per kilogram of gas actually delivered — would fix this.

Finally, our plants have too much slurry, with no buyers for that residue. The slurry can pile up, ferment, and then poison the bacterial culture in the plant.

The three layers

All of this means we can’t build a biogas network indiscriminately. The ideal biogas ecosystem would have three layers stacked on top of each other.

At the base would be small-scale, decentralised biogas plants — village digesters, farm-level units, wet-waste plants serving hotels, airports, and apartment complexes. With good planning, these can bypass the 50-kilometre problem, because the feedstock and the burner are in the same village — or even the same building. Our colleagues at Rainmatter have been quietly backing this for some time, with investments in companies running farm-level digesters, agri-waste-to-energy startups, and integrated waste management platforms at bulk waste generators.

In the middle comes industrial-scale CBG — 5-50 tonne-per-day facilities, which feed into the networks of oil marketing companies. This is where the 50-kilometre problem is most acute, and where the CBO mandate will be tested first. Private capital has begun showing up here: Reliance Industries has committed roughly ₹65,000 crore to setting up 500 CBG plants in Andhra Pradesh, as part of a national target of 2,000 plants. The first of these broke ground at Kanigiri in April 2025.

Finally, there’s the City Gas Distribution network — with long-distance pipelines, household PNG connections, and CNG outlets. This is the long-term structural answer that could make larger plants work. Without it, every plant would have to maintain its own distribution network. We’re lacking here; India has around 1.61 crore active PNG households today, against a long-term target of 12.64 crore by 2034. A better grid could ensure that the entire biogas economy eventually operates at scale.

The CBO mandates 3% blending from the current financial year. This requires thrice as much physical CBG supply as we currently have, by March next year. That’s a big gap, and we don’t expect the number of biogas plants in India to multiply. But what could change is their average utilisation rate.

That’s the number we’ll keep looking at.

Tidbits

Adani, Vedanta, Hindalco and Hindustan Copper are opposing a move to bring fire-refined high conductivity (FRHC) copper rods made by secondary refiners under the same Bureau of Indian Standards specifications as their own output, arguing scrap-based players lack the technology to consistently hit the 99.99% purity needed for electrical applications. The standoff has left roughly 400,000 tons of copper wire rod trading outside the quality control regime.

Source: ReutersGoogle unveiled a redesigned search box meant to handle longer, chatbot-style queries, a new Gemini 3.5 Flash model pitched as its best yet for coding, and Gemini Omni, which can generate video from a mix of text, image and audio prompts. The company also launched a $100/month developer subscription tier.

Source: Business StandardThe National Solar Energy Federation of India has petitioned the Central Electricity Regulatory Commission to raise the ₹10/unit ceiling on power exchanges, saying it leaves generators and energy storage firms unable to recover losses incurred during weak-demand periods and is choking investment in storage. The plea comes as peak power demand hit a record 260.45 GW on Tuesday amid a heatwave.

Source: Reuters

- This edition of the newsletter was written by Vignesh and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

{kind=link}

If you’re a woman who feels intimidated by the world of money, In Her Interest is meant for *you*.

Most women share a complicated relationship with money.

On one hand, women are expected to be exceptionally good with it. They manage household budgets, track expenses, stretch money, save for emergencies, and make a hundred tiny financial decisions every month.

When money conversations turn more formal, though; when they shift to investments, insurance, taxes, or business finances, they suddenly defer to someone else — a father, husband, brother, the family CA, or “the finance person” in the family.

To us, this weird duality seems to creep in because most women have never had a friendly, low-pressure place to learn their way around it.

That’s what In Her Interest, a Zerodha initiative, is trying to create. In Her Interest hosts small, in-person sessions where women can ask normal money questions without being judged, sold to, or drowned in jargon. The next few sessions cover finance for entrepreneurs in Gurugram, smart money management in Mumbai, investing basics in Pune, and the basics of mutual funds in Hyderabad. If you’re a woman who has been meaning to get a little more comfortable with money — or know someone who might — this is a fantastic place to start!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

The tipping point for 2W EVs will happen at about 115/- to 125/- rupees per litre. (For 3W EVs it has already happened with prices of CNG going close to petrol). Reasoning - apart from the lower cost per km

1) Battery buy back schemes by manufacturers as well as on the street.

2) No more worrying about adulterated fuel.

3) No more stress about PUC (and rising cost of PUC)

4) Up front 5 years insurance = no more harassment by Vasooli guys.

5) Much lower maintenance and easy home charging

An EV is pretty much going to be like a ball-pen, use, throw, but the re-cycling will take care of everything else.

What we need badly, now, is battery swapping instead of huge investments in charging infra.