India's oil laws enter the 21st century

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

India’s oil market liberalisation

Asian Paints is in trouble (again)!

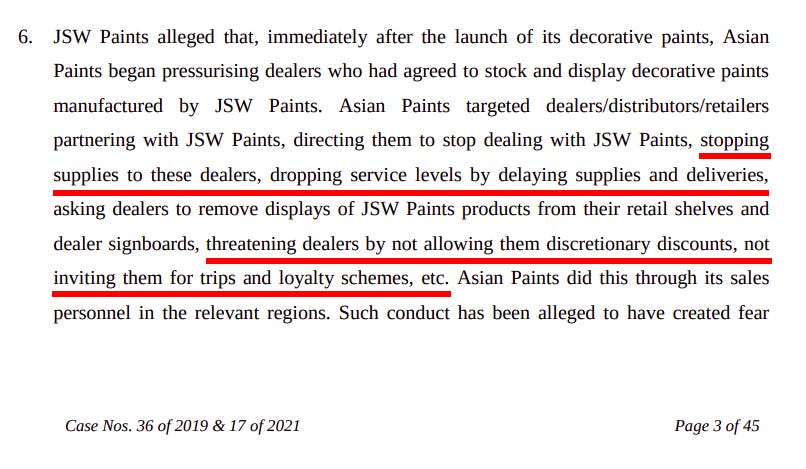

India’s oil market liberalisation

Before we begin, a special note by this story’s lead author:

Hello, this is Mridula; an intern until yesterday. :)

I was part of the team which curates these amazing pieces daily that you guys read/listen to first thing in the morning. As I wrap things up, I want to express my gratitude to everyone in the team who have supported and encouraged me, and given me an experience to cherish. There’s so much effort that goes behind the scenes to give out the best quality possible. I hope you guys have as much fun reading this piece as I had while jotting this down.

To many more learnings and to where curiosity leads ahead!

For decades, India’s oil and gas sector followed a strict set of laws, rooted in the early days after independence. These were written early in our history — in 1948 and 1959 — and despite minor modifications, conceptually, we still occupy the same space.

But now, triggered by key challenges and a shifting global context, India is rewriting its laws. This March, the government changed the very framework around how oilfields were regulated in India. Last week, the Ministry of Petroleum and Natural Gas unveiled the Draft Petroleum & Natural Gas Rules 2025, overhauling the more granular rules we had in place.

Together, these mark a complete shift in the gears for how exploration and extraction of oil and gas works in India. We’ve decided to throw away our post-colonial straightjacket, and are re-framing our energy destiny. Here’s what we’re doing.

Historical overview

When India gained independence in 1947, the new government was deeply suspicious of private companies — especially foreign ones — and for good reason. In those days, it seemed like there was one lesson to take away from the two hundred years gone by: that foreign companies were built to exploit the resources of weaker nations.

The first generation of Indian politicians wanted to ensure that India's resources would benefit Indians as a people. They couldn’t be locked away behind private ownership. Inspired by a wave of socialism that was then in fashion across the world, we believed that the Indian government should be the rightful steward of its resources. Immediately upon independence, India’s transitional government, shaped by this protective instinct, created two foundational laws that would govern India's energy sector.

The Oilfields (Regulation and Development) Act, 1948 (Oilfields Act) set up the core framework around which other regulations would come in. It gave our central government broad powers over India’s oil and gas sector. With this law, the government was made responsible for regulating the space, inspecting operations, and supervising things like exploration and production. The law also gave the government serious teeth: it could penalize violations with jail time or hefty fines, tightening its grip on the entire process.

Under this act, we soon adopted the Petroleum Concession Rules, 1949 (1949 Rules), laying down the basic procedure for companies to explore and extract oil and gas. Under these rules, companies would be given “concessions” — they would have broad, long-term rights over their oil resources, with little government oversight.

In the first decade of independence, though, our priorities shifted. The 1949 rules were much too vague, it seemed, and private companies were being given far too much leeway over core areas like energy. In a planned economy, oil was too strategic to be outside government control.

And so, the 1949 Rules were replaced by the Petroleum and Natural Gas Rules, 1959 (1959 Rules). These new rules brought in a more detailed system, where private operators were given limited, revocable rights. The rules allowed temporary licenses and leases, and extended regulatory control to various operations these players would perform. All of this would come under strict government oversight, with monthly reporting requirements, and a series of protocols.

Why these regulations pinched

Unfortunately, regulations, if they aren’t calibrated well, can choke the very industries they police.

To run an oil field, you need a variety of things: the ability to explore new fields, the tools and capital to drill deep wells, the infrastructure to transport that oil, the ability to sell it at a fair price, and the legal protection to operate with confidence. Unfortunately, India clipped the wings of its oil companies at nearly every step.

Early on, only government-owned firms like ONGC and Oil India were allowed to explore for oil. The private sector was locked out entirely. Even decades later, when private investment was finally allowed, the contracts were filled with restrictions. Companies needed government approval for everything — from how much they spent to what technology they used. Extra costs could be audited and were often disallowed.

Pipeline infrastructure was also dominated by PSUs. Meanwhile, getting approvals for new projects could take years — choking competition and innovation before it could start.

Even the price at which you could sell fuel was capped through an “Administered Price Mechanism”. Prices of refined fuels like petrol and diesel would regularly be adjusted to suit political needs, no matter what global markets said. While state-owned oil companies were compensated for their losses, the private sector got nothing. As Reliance pointed out, back in 2006:

"When we were issued license to market petrol and diesel in March of 2002, we were promised market determined pricing. But when the Government keeps prices artificially lower at 95 per cent of the outlets, there is no question of competition (from private sector) surviving…"

Much of this control dates back to the nationalisation wave of the 1970s. The government passed special laws to forcibly take over private oil companies like Esso, Burmah Shell, and Caltex, and turned them into public-sector firms like HPCL and BPCL. By the 1980s, nearly the entire oil value chain — from exploration to refining to retail — was under state ownership. The industry was no longer being run for commercial efficiency, but for public control.

After liberalisation in the 1990s, things began to open up. The government introduced bidding rounds for private exploration, and eventually decontrolled petrol and diesel prices. But many of the deeper problems remained: complicated contracts, rigid pricing rules, slow environmental and regulatory clearances, and weak legal protections.

These discouraged long-term investment and kept India off the radar for many global oil majors. Meanwhile, domestic giants like ONGC (Oil and Natural Gas Corporation, India's largest oil company) and Oil India struggled with outdated tools and methods, watching their production decline year after year while the nation's energy hunger grew exponentially.

The final straw

Perhaps the last straw came in 2022, during the Ukraine war.

This was a unique opportunity for Indian oil refiners. Most of the world was shunning Russian crude, sending global prices skyrocketing. Indian companies finally had the opportunity to make use of their refining capacity and fill in the gap. If they could take a risk and refine cheap Russian crude, they could profit hugely.

To the government, however, these were “excess” profits.

It stepped in to impose “windfall taxes”, or special taxes on domestic refineries which were updated every two weeks. From the government’s point of view, this was a clever move. They were getting a cut from a generational stroke of luck. But the move sent shockwaves through the investment community, particularly affecting ONGC, Oil India, Reliance etc.

Eventually, windfall taxes were scrapped in December 2024. But the damage was done. The episode had confirmed, once again, what global investors already knew: India's energy sector remained unpredictable and risky. The system was too opaque, and filled with too much red tape. If an opportunity ever came up, the government would demand its due.

For a country that was chronically insecure about its energy needs, our oil and gas sector has practically stagnated. As the Times of India recently reported, India’s refining capacity grew by just 5% over the last seven years, despite the sector being at the center of “windfall” gains. Oil production, meanwhile, actually declined, falling over 14% from 34.10 million metric tonnes in 2019 to 29.18 million metric tonnes by 2024.

There are many reasons for this, including our looming green transition. Equally, investors just didn’t trust India’s policy environment.

The new reforms

In early 2025, India began a new phase of reform.

The Parliament passed major amendments to the Oilfields Act, which came into force on April 15. This was a complete re-write of the older law. It tore through the red tape to introduce a single, unified “petroleum lease” that would permit everything from prospecting to production. Criminal penalties were done away with, while many previous gaps — like offshore rigs or shale extraction — were plugged into the same framework.

There are other improvements, too. The amendments allow shared infrastructure. They permit companies to take up renewables and carbon capture projects under the same licenses — essentially nudging these companies to transition to greener technology. They also save investors from getting stuck in court, by officially allowing people to go to arbitration in neutral locations like Singapore or London.

The crown jewel of the new law, however, is a “stabilization” clause.

This clause makes an extremely important promise: that the government shall not change the terms of a petroleum lease in a way that hurts the lessee. If they do, the lessee would be compensated. This was practically a tacit admission of our old mistakes, and a promise that they would not be repeated.

So far, these reforms are only to do with crude oil and natural gas extraction. Refining remains outside their purview. But, as PNG Minister Hardeep Puri recently claimed, the stabilisation clause effectively locks in the fiscal terms of these petroleum leases, in a way where the government can no longer play around with refining profits as well. To him, the government will simply not be able to levy windfall taxes after the amendments. Will this promise be kept? We’ll wait and watch.

But there are signs that these changes have already drummed up some interest among foreign investors.

Any law passed by Parliament, however, only creates a framework: it lays the broad contours for what a government can and cannot do. Beyond that, the Parliament passes the baton to the government, which is tasked with actually bringing a law to life.

That’s why everyone was waiting for rules to be created around the law. It was these rules, and not the Act itself, that would define the nuts and bolts of how the government would behave. These alone could ensure the certainty investors were really looking for.

The Impact of the New Rules

That’s why there’s so much discussion around the Draft Petroleum & Natural Gas Rules 2025.

For one, they change the government’s focus from regulation to governance. On one hand, they actually add obligations — for instance, tightening environmental safeguards, or adding requirements around data transparency and sharing. But they also bring clarity. They make leasing processes clearer and define timelines for approvals. They also expand on the “stabilisation clause” — effectively crystallising how it shall work.

The timing of these rules is deliberate. The government plans to put them in action before allotments are made under the OALP Round X (the Open Acreage Licensing Policy, India's system for auctioning oil and gas exploration blocks) — promising that the 25 hydrocarbon blocks auctioned therein will come under the new framework.

Some concerns remain. Experts warn that this draft could allow the government to change some contract terms, creating uncertainty for investors. Companies could lose their leases if they disagree with government plans. This could further discourage investment, hurting the very growth the rules aim to promote. But these are, on the whole, minor squabbles.

The government is taking suggestions and feedback on the new rules until July 17. To wrap up this major reform process, a big event called Urja Varta 2025 (Urja means “energy” in Hindi) will be held at Bharat Mandapam, where the final version of the rules will be unveiled.

But the real test lies ahead. Will foreign companies actually invest? Will domestic production increase? And most importantly, will India finally achieve the energy independence it desperately seeks?

The stakes couldn't be higher. But the early signs are promising.

Asian Paints is in trouble (again)!

Building a successful, profitable business is tough. It gets tougher when a big whale in the industry deliberately targets you, making it harder for you to survive. That, according to a recent case, might be what’s playing out in the paints industry.

The Competition Commission of India (or CCI) is a government body that, in essence, ensures that companies only get ahead if they beat their competition fairly — not through underhanded means. Recently, they launched a probe against Asian Paints for allegedly "abusing its dominant position," following a complaint from Birla Opus in November 2024.

For the uninitiated, Birla Opus is the paints division of Grasim Industries, and the latest entrant into India’s ₹80,000 crore paints market. Since its launch in February 2024, it has taken the industry by storm, capturing over 10% market share in the decorative paints segment, already becoming the third-largest player.

But they think they would have done even better had Asian Paints not played dirty.

They aren’t the first to make such accusations. A couple of years ago, JSW Paints raised nearly identical allegations against Asian Paints. That time around, after a two year long investigation, the regulator closed the case, finding no evidence of foul play.

But will they find more evidence this time around? Or will Birla’s case too go the same way? Let’s dive in.

Round I: JSW Paints vs Asian Paints

JSW Paints was incorporated in 2016. They spent the first three years developing their product, strategizing, and testing the waters. They finally launched decorative paints in May 2019, in Karnataka.

But a product alone doesn’t make a business. It’s equally important to have distribution. To sell paint in the market, you need a network of dealers. They’re essential touchpoints between manufacturers and customers. Without them, reaching customers is nearly impossible.

Consider this: if you’re craving a soft drink, you won’t search for a Coca Cola-operated store. Instead, you’ll head to your local kirana shop or supermarket (or, these days, an opp on your phone). If they don’t stock Coca Cola, you might end up buying something else — like Pepsi.

In other words, that shop (or app) is fundamental to your ability to get your soft drink. What they stock is what you buy. That’s also the case with paints. Buying decisions in the paint industry are largely influenced by dealers.

(If you want to dive deeper into this dynamic, check out our detailed analysis of the paints sector!)

So, JSW started reaching out to paint dealers, presenting their product and explaining the benefits dealers could gain by partnering with them. Many dealers were convinced and agreed to stock JSW Paints alongside other brands. But Asian Paints allegedly stepped in and blocked this from happening.

According to JSW Paints, Asian Paints actively disincentivised dealers from partnering with them. Dealers were allegedly threatened with stopped supplies or delayed deliveries, and Asian Paints supposedly even withheld discretionary discounts.

Timely deliveries and discounts are critical to dealers. It’s how they stay profitable. When your biggest supplier threatens you with such disruptions, the health of your business is suddenly at risk. Understandably, dealers wouldn’t risk their everything just to add “one more option” to their shelves.

It wasn’t just JSW Paints that was making this claim. Another dealer, Balaji Traders, also approached the CCI later — alleging that Asian Paints unfairly revoked its “Critical Retailer” status when they began dealing with JSW Paints. Their case was combined with JSW’s for a joint investigation into Asian Paints' anti-competitive behavior.

At first glance, the CCI found the allegations serious enough to warrant a deeper investigation. It ordered its Director General (DG) to look into the matter. But ultimately, the final verdict did not find Asian Paints guilty.

The Asian Paints Defence

So, how exactly did Asian Paints manage to defend itself?

The CCI did agree with JSW Paints on one thing: Asian Paints was dominant. It sat at the heart of India’s decorative paints industry, with a presence no competitor had come close to challenging over the last decade. Its dealer network was sprawling, and dealers were deeply reliant on it for inventory, credit, tinting machines, and incentive schemes. In theory, this gave Asian Paints the power to choke out any new entrant, if it chose to.

But did it actually do so? To the CCI, there was no reason to believe so.

JSW Paints’ alleged that Asian Paints used its dominant position to block their entry. Specifically, they claimed it pressured dealers — through threats, delays, or cuts in incentives — to avoid doing business with JSW.

To test this, the Director General looked at dealer additions. Between 2019 and 2021, Asian Paints added 1,217 dealers. JSW Paints, meanwhile, added 1,591 dealers. The DG argued that if Asian Paints were really foreclosing the market, JSW wouldn’t have been able to expand its dealer base faster than the market leader.

That logic raises questions. A new entrant like JSW, starting from zero, naturally has a larger pool of dealers to tap. Its growth rate is likely to be higher in the early stages. By contrast, Asian Paints already had much of the market covered. They were making incremental additions to a vast network, where JSW was setting a network up from scratch. So, raw dealer additions, in isolation, say little about whether any pressure tactics were invovled.

Still, the DG had little else to go on. JSW claimed that 1,378 dealers had been pressured into cutting ties — but only 15 came forward, and most of them offered little in the way of concrete proof. In fact, some later filed affidavits supporting Asian Paints.

There were other allegations too: that Asian Paints downgraded retailers like Balaji Traders, or interfered with JSW’s warehouse leases. But in each case, Asian Paints offered business justifications — delayed payments, declining sales, or expired contracts. And in most cases, the data held up. The CCI found nothing definitive linking these actions to JSW’s entry. These could just as easily be “business as usual.”

JSW also alleged that Asian Paints had effectively forced its dealers to become exclusive suppliers of its paints, letting nobody else in. But they simply couldn’t prove it. There was no such agreement on paper, and they couldn’t put together enough evidence to show that there was such an agreement in fact.

Asian Paints’ defense boiled down to this: it was doing what it always did. Yes, it was strict with its dealers. Yes, it had standards. But no, it wasn’t punishing them for working with a rival.

JSW couldn’t disprove that narrative. And under Indian competition law, that's crucial. Under competition law, few things are black and white — something that’s wrong in one case maybe fine in another. Everything depends on context. The bar JSW Paints had to clear was high. It wasn’t enough to show that a business’ actions might have had a negative effect — you have to show that such an effect was intended to kill competition, and that it couldn’t be reasonably explained otherwise.

In the end, JSW simply failed to clear that bar.

But it looks like Birlas are coming back to seek revenge.

Round II: Birlas case

This time around, the Birlas, like JSW before them, think Asian Paints is using its heft to push them out of the paints market.

They have explicitly called out Asian Paints for aggressively pursuing exclusive deals with dealers and resorting to various strong-arm tactics to influence dealer behavior. They’ve listed detailed allegations — reducing discounts, manipulating credit limits, revoking loyalty memberships, threatening dealership cancellations, and more — if dealers choose to work with other brands.

Birla Opus is trying not to fall short the way JSW Paints did. They even brought in an independent third party to conduct an extensive market survey on the pressure Asian Paints allegedly exerted.

There’s one claim Birla made that would be particularly egregious if true: apparently, dealers were pressured into returning Birla Opus’s new tinting machines. Tinting machines are crucial to expanding a paint brand. See, paints companies don’t manufacture every single shade under the sun. Instead, they give dealers basic paints and colorants, along with “tinting machines”. These machines create the specific shade a customer wants. In a way, they are the final connection between the paint brand and customers.

Tinting machines, in a way, guarantee dealer loyalty. They’re similar to the branded fridges you see in kirana stores, that push the owner to stock a certain kind of cola. They usually just work with one brand of paint, and are customised for their products.

Birla Opus claimed their machines were genuinely superior — 40% smaller, operable via tablet, internet-connected, and capable of providing dealers with useful inventory management data. But Asian Paints, they claim, was getting dealers to send them back.

Asian Paints allegedly dangled additional incentives, like extra 1–2% discounts for dealers who ditched competitors' machines. Territory Sales Officers from Asian Paints reportedly went as far as delaying approvals of credit notes (refunds or purchase adjustments), subtly signaling that business would be smoother if dealers stayed exclusive. In doing so, it effectively blocked newer, better technology from reaching customers.

Birla provided a list of over 100 dealers who returned their tinting machines due to Asian Paints’ alleged intimidation.

Will Birla succeed where JSW failed?

Will this case go any differently than the one filed by JSW Paints?

On the surface, CCI continues to believe that Asian Paints dominates the paints industry. It can push Birla out if it wants. And at least on the surface, Birla has put together enough evidence to show that it may have tried to do so. The CCI has now ordered the DG to investigate further.

Now, the ball is firmly in Asian Paints’ court. The big question is: can assurances of “business as usual” cut it once again?

Tidbits

Earlier, we said China’s chip dreams have been running into hurdles — inefficient tech, patchy supply chains, and a leaky Big Fund. But this week, there’s a surprising vote of confidence — from the other side.

NVIDIA CEO Jensen Huang called Chinese AI models “world-class” — specifically naming DeepSeek, Alibaba and Tencent. This came at a Beijing supply chain expo, just a day after the US greenlit sales of NVIDIA’s downgraded H20 chips to China. “It’s crucial for American companies to establish roots in China,” he told state TV.

Source: Business StandardWe’ve looked at TRAI’s pricing cap on public Wi-Fi and how it was designed to unlock digital access. Now, TRAI’s pricing playbook is back in the news — this time, in space.

The Department of Telecommunications looks set to approve TRAI’s controversial satcom spectrum pricing — despite protests from telecom operators. The regulator wants satellite internet providers like Starlink, OneWeb, and Jio Satellite to pay a modest 4% of their adjusted gross revenue, with no upfront spectrum auction. Telcos say it creates an uneven playing field, as they pay far higher levies (up to 21%) and bid billions for spectrum.

But TRAI insists that satellite spectrum is a shared resource globally — not something to be auctioned.

Source: Business StandardWe looked at the complex and fascinating pharmaceuticals industry in more than one story. There’s a big update in that sector.

Anthem Biosciences' $395 million IPO was fully subscribed on its second day, reflecting strong investor confidence in India's pharmaceutical sector. The company, based in Bengaluru, specializes in early-stage drug discovery and is well-positioned as global pharma firms seek alternatives to Chinese suppliers.

Source: ReutersBeyond The Daily Brief, we also have a show called Who Said What. In one of those episodes, we looked at what experts were saying were the problems with GST. Luckily, there seems to be a bright spot.

Now, the Prime Minister's Office has approved a significant overhaul of India's Goods and Services Tax (GST) framework, marking the first major changes since its implementation eight years ago. The proposed reforms aim to streamline the tax structure by reducing the number of slabs and simplifying procedures, with a key recommendation being the elimination of the 12% slab, potentially moving items to the 5% or 18% categories.

Source: Economic Times

- This edition of the newsletter was written by Mridula and Kashish.

📚Join our book club

We've started a book club where we meet each week in JP Nagar, Bangalore to read and talk about books we find fascinating.

If you think you’d be serious about this and would like to join us, we'd love to have you along! Join in here.

🧑🏻💻Have you checked out The Chatter?

Every week we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

“What the hell is happening?”

We've been thinking a lot about how to make sense of a world that feels increasingly unhinged - where everything seems to be happening at once and our usual frameworks for understanding reality feel completely inadequate. This week, we dove deep into three massive shifts reshaping our world, using what historian Adam Tooze calls "polycrisis" thinking to connect the dots.

Frames for a Fractured Reality - We're struggling to understand the present not from ignorance, but from poverty of frames - the mental shortcuts we use to make sense of chaos. Historian Adam Tooze's "polycrisis" concept captures our moment of multiple interlocking crises better than traditional analytical frameworks.

The Hidden Financial System - A $113 trillion FX swap market operates off-balance-sheet, creating systemic risks regulators barely understand. Currency hedging by global insurers has fundamentally changed how financial crises spread worldwide.

AI and Human Identity - We're facing humanity's most profound identity crisis as AI matches our cognitive abilities. Using "disruption by default" as a frame, we assume AI reshapes everything rather than living in denial about job displacement that's already happening.

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉