India's great health bargain is falling apart

A shoddy payment record could kill universal healthcare

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Why private hospitals are walking away from government schemes

The wires & cables industry run up the hill — with some bumps

Why private hospitals are walking away from government schemes

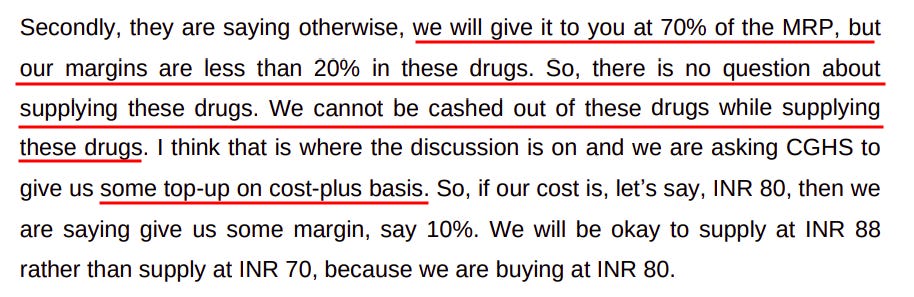

On Max Healthcare’s Q3 FY26 earnings call, Chairman Abhay Soi was asked about the company’s oncology business. There was a problem. The Central Government Health Scheme — which covers central government employees, pensioners, MPs, and judges — had asked Max to supply patented chemotherapy drugs at a flat 30% discount to MRP. But the thing was, hospitals make less than 20% margin on these drugs to begin with.

So they did what any rational economic actor would: they stopped supplying every drug where their margins were below the mandated discount. CFO Yogesh Sareen pegged the impact at a one-time ₹200 crore revenue hit, which would settle into a sustained ₹140 crore annual drag.

Of course, all a company can tell you on an investor call is a sanitised, corporate-speak version of what’s happening. But it seems like there’s an uglier story building up beneath the surface. In August 2025, for instance, around 650 private hospitals in Haryana actually walked away from Ayushman Bharat services for 19 days, leaving up to 1.8 crore registered beneficiaries without cover. They wanted ₹490 crore in pending dues cleared. They had threatened the same thing in January 2025 as well.

These are just some signs of a wider disenchantment. Across India, there’s an interesting structural problem with how the country’s biggest healthcare bargain is wired.

The bargain India struck

India’s healthcare delivery is overwhelmingly private. Roughly 63% of total health expenditure flows through private providers. They house 60% of hospital beds and employ nearly 80% of practising physicians. Public hospitals don’t have the wherewithal to replicate this network. If India wanted universal health coverage, the road was always going to pass through private hospitals.

That’s exactly what the country’s publicly funded health insurance schemes do — buying private medical services at scale. There are three that matter at the national level: CGHS, which covers central government employees, pensioners, MPs, and judges; ECHS, which does the same for retired defence personnel; and the biggest by far, PM-JAY, the beating heart of ‘Ayushman Bharat’, which gives a cashless cover of up to ₹5 lakh per family per year for the poorest 40% of India’s population, and all Indians over 70. On top of these, states run their own programmes — like Maharashtra’s MJPJAY, Telangana’s Aarogyasri, and others.

At least on paper, the mechanics of these schemes are simple. A patient walks into an empanelled hospital with a card. The hospital authenticates them through the scheme’s transaction system, picks the right package from a list of around 2,000 procedures, gets pre-authorisation, treats the patient cashlessly, then files a claim with the State Health Agency or its third-party administrator. The claim moves through scrutiny, anti-fraud filters, and treasury releases, and eventually, the hospital gets paid.

To see where the problem crops up, though, note what the hospital is actually doing. It isn’t selling services to the patient. It’s selling services on credit to the state. For this model to make sense for them, two conditions have to hold at once: the rates have to be economically viable, and the payments have to land within a reasonable window.

While the model is functioning at the moment, both conditions are under sustained pressure. Hospitals’ margins are being squeezed by state mandates, while their working capital is being throttled because payments take more than six months to arrive. That is the genesis of everything that follows.

The first squeeze: getting paid enough

Start with costs; the more visible side of this bind.

While India’s headline retail inflation has hovered around 3-4% in recent quarters, medical inflation was running at roughly 13% in 2025, more than triple the broader economy. Imported devices, patented drugs, specialist clinician salaries have all moved at this rate of medical inflation, not with CPI. Meanwhile, the rates at which the government pays hospitals have moved with neither.

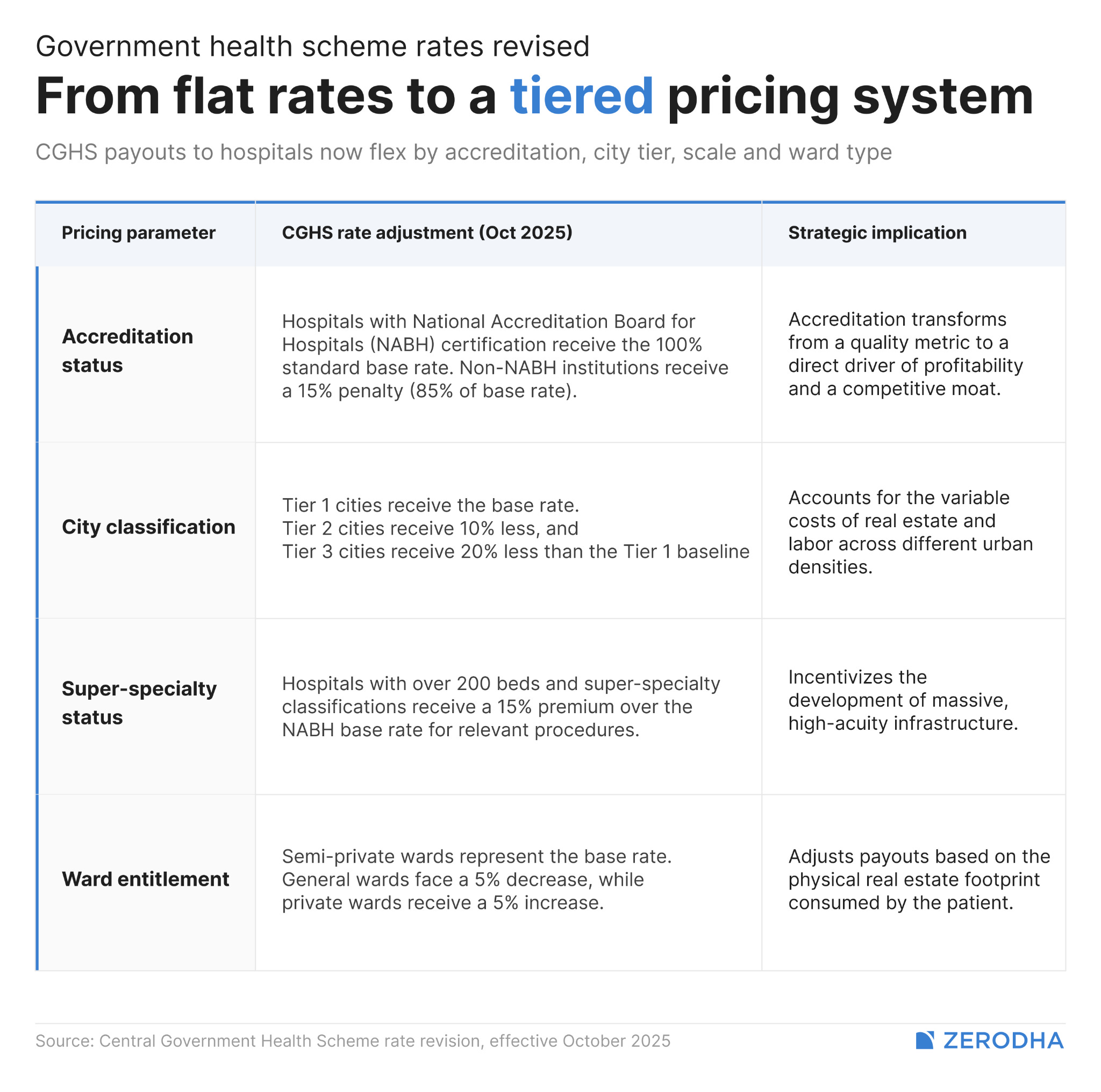

The CGHS package rates, before October 2025, were essentially frozen at their 2014 levels with only piecemeal updates. That’s eleven years. This has created a series of absurdities — for instance, chest X-rays are priced at ₹65 when the raw film costs more than that; or a normal delivery at a NABH-accredited hospital is reimbursed at ₹9,200, against the ₹50,000-plus the same procedure runs at tier-1 city private rates.

In October 2025, the Ministry of Health executed the most significant CGHS pricing reform in over a decade. Roughly 2,000 procedures were repriced. The framework moved from flat rates to a tiered structure based on the type of hospital, whether it is accredited, city tier etc. ECHS aligned with the revised rates from December 2025. Hospital stocks moved sharply on the announcement.

This is a genuine and welcome reset. But it doesn’t quite fix the problem; it only repositions it. There are still margin pressures worth flagging. For example, the package design itself bundles everything together — room, surgeon, drugs, consumables, food — at one fixed price. Anything that ramps up these costs, like clinical complications or an extended stay, eats directly into the margin.

On its own, though, this could have been a manageable headache. Only, it pairs with a second squeeze that turns it into something much worse.

The second squeeze: getting paid on time

A hospital doesn’t just need viable rates. It needs to actually receive the money on a timeline that lines up with its own obligations. If the rates were better, perhaps, some delays would be manageable. If payments came in at breakeven costs, it would only be sustainable if hospitals are paid promptly. But if both pressures hit at once — if rates are low, and there are delays in payment — there’s simply no room to absorb those costs. And both are hitting at once.

In theory, delays shouldn’t be a problem. PM-JAY’s official claim settlement turnaround time, as set by the National Health Authority, is 15 days. CGHS’s own 2023 cashless arrangements with AIIMS institutions said bills should preferably be paid within 30 days.

The reality, sadly, looks very different.

On Fortis Healthcare’s Q2 FY26 earnings call in November 2025, an investor asked the company directly about its government receivable days. The money, its management said, took 6 months to come.

That isn’t a small amount. Government schemes together make up close to one-fifth of Fortis’s top line. All of that money comes in with a six-month payment lag.

This isn’t unique to Fortis. As Health Policy Watch’s reporting on the Haryana suspension documented, hospitals said reimbursements regularly took six to nine months to come in. This isn’t new information either. NITI Aayog’s 2021 report on not-for-profit hospitals had already flagged “perennially delayed reimbursements and long-pending amounts”. The pattern was visible four whole years ago.

Some of this delay is a matter of genuine fraud control. The 2023 Comptroller and Auditor General performance audit on PM-JAY, for instance, found massive systemic discrepancies. 7.5 lakh beneficiaries under the scheme were linked to a single mobile number: 9999999999. Dead patients were shown as continuing to receive treatment. The same patient was often registered as ‘admitted’ in multiple hospitals at the same time. The National Anti-Fraud Unit has flagged 2.7 lakh claims worth ₹562.4 crore as non-admissible due to abuse, misuse, or incorrect entries. As a result, 1,114 hospitals have been de-empanelled and 549 suspended.

There’s clearly a lot of fraud at play. State agencies do need to verify before paying. But there’s a trade-off; an audit infrastructure that catches dishonest claims also slows down honest ones. And the government seems content letting hospitals take the short end of the stick.

The total scale of the lag came into public view through an RTI filed by Dr. Ajay Basudev Bose in February 2025. The National Health Authority’s own response showed ₹1.21 lakh crore in pending dues across India under PM-JAY, against more than 63 lakh unsettled claims. That figure does not appear on the NHA’s public dashboard.

Hospitals were getting rates set below cost on one side, while payments took six months to arrive, on the other. There was no obvious mechanism to fix either quickly. Something had to give. And it has been giving.

What gives, and how each side is reacting

The first visible breaks in the system are state-level shutdowns.

These have been happening for years. As far back as August 2019, around 240 private hospitals in Telangana stopped services under Aarogyasri over ₹1,500 crore in dues. The same pattern has repeated across the country — Punjab in 2024, Andhra Pradesh and Manipur through 2025 — over arrears running into the hundreds of crores. Usually, these disruptions would only end with a partial release of funds after a few weeks.

Meanwhile, something less visible is happening at the corporate level. Big, diversified chains have a lot of freedom to walk away from government scheme economics, by simply rebalancing its mix of patients. They’ve been exercising that ability liberally.

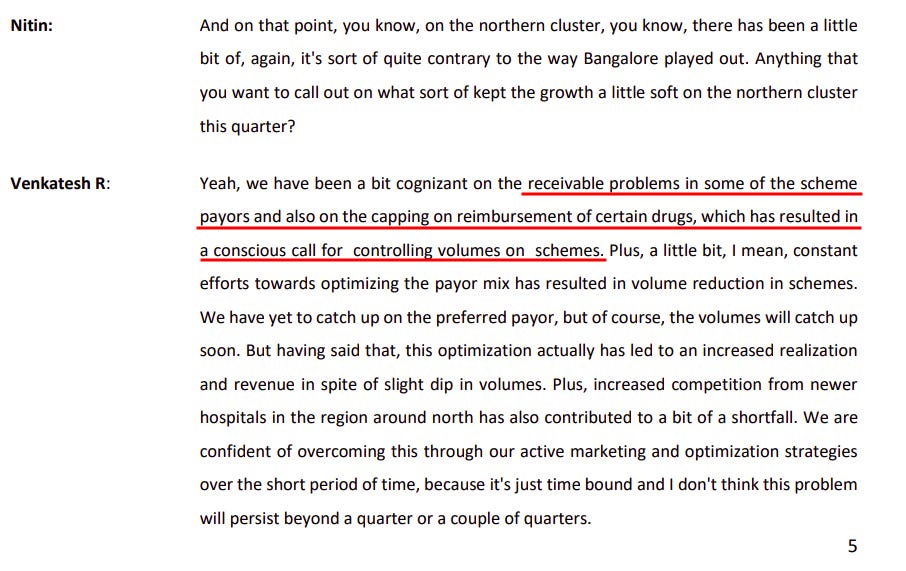

Apollo has done this most aggressively over years. By Q3 FY26, 83% of its inpatient revenue came from cash-paying patients and private insurance. Government schemes were a small fraction of the residual 17%. Similarly, Narayana Health, on its Q3 FY26 call, flagged a conscious decision to control scheme volumes in the northern cluster, citing receivable issues with scheme payors and capping on drug reimbursements.

The advisory firm Praxis Global Alliance estimates the revenue share from state-backed schemes for top private hospitals could drop by 3% to 5% by Q1 FY27 because of selective de-empanelment or capped bed allocation.

The government does recognise the underlying problem. The October 2025 CGHS reset does fix rates somewhat, and ECHS has aligned with it. But there’s also been a tightening on the fraud side, with aggressive de-empanelment and AI-based monitoring of claims. In all, the fundamental issue — the low rate of reimbursement, and the delayed payment — remains as bad as ever.

What this leaves us with

India’s chosen route to universal health coverage was a defensible bet. Public hospitals simply can’t add tertiary capacity at the speed the population needs, so the state purchased it from private hospitals at administered rates. The architecture worked, at least directionally. Out-of-pocket health spending fell from 64.2% of total health spending in 2013-14 to 39.4% in 2021-22, the largest single shift in India’s health financing history.

But the bet only pays off if the state behaves like a credible purchaser of care. The government needs the buy-in of private hospitals for these schemes to work as intended. For that, it needs to ensure that their financial needs aren’t ignored. They need to be paid well, and on time. The system, as currently designed, manages neither.

In the short term, this might look like it’s saving precious government resources. But everyone loses if India’s universal healthcare promise is buried under a mountain of disputes and disengagement.

The wires & cables industry run up the hill — with some bumps

We’ve been covering the wires and cables industry for three quarters now. And throughout that time, the story has consistently been in favor of the industry, which is riding certain structural tailwinds. They’re hitting record revenues, recording strong demand, and making big plans. Meanwhile, the industry as a whole is moving away from unbranded, informal products that used to form a majority of the industry.

This quarter isn’t all that different. Interestingly, their current growth has given way to some problems — some of which lesser companies would love to have.

For instance, this quarter, revenue grew 20-30% across the board. However, the amount of wire and cable that actually shipped barely budged. In fact, one company managed just 2% more volume than last year. And while that’s happening, the industry is also seeing demand absolutely outstrip supply, and it cannot react fast enough to that.

There is no shortage of buzz in this market at the moment.

The numbers

But before that, let’s start with what the numbers say.

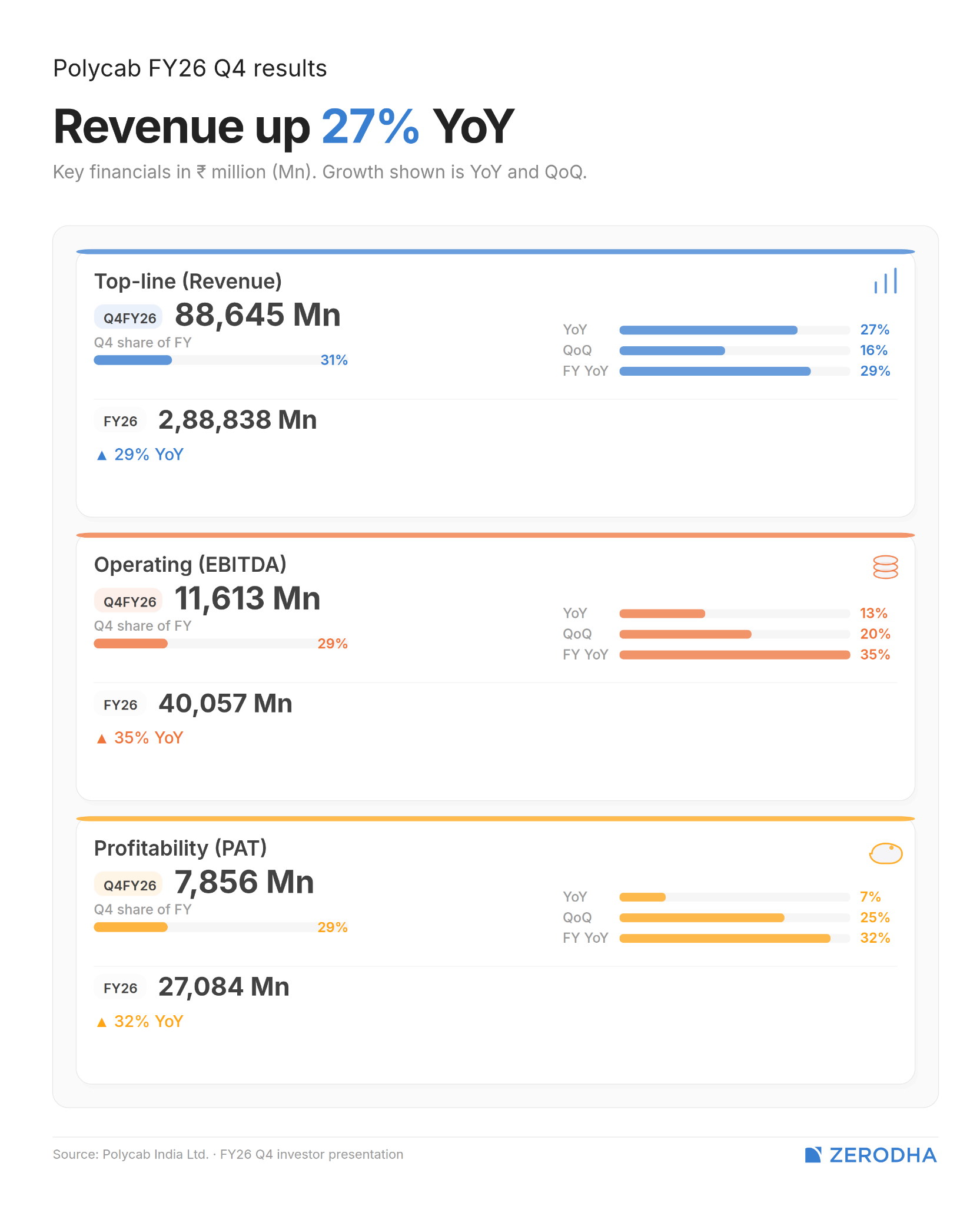

Polycab, the industry leader, posted its highest-ever quarterly revenue at ₹8,864 crore — up 27% from last year. For the full year, it crossed ₹28,884 crore, up 29% year-on-year. Its profit-after-tax (PAT) for FY26 came in at ₹2,708 crore, up 32%. For the fourth consecutive year, Polycab is the most profitable company in the industry.

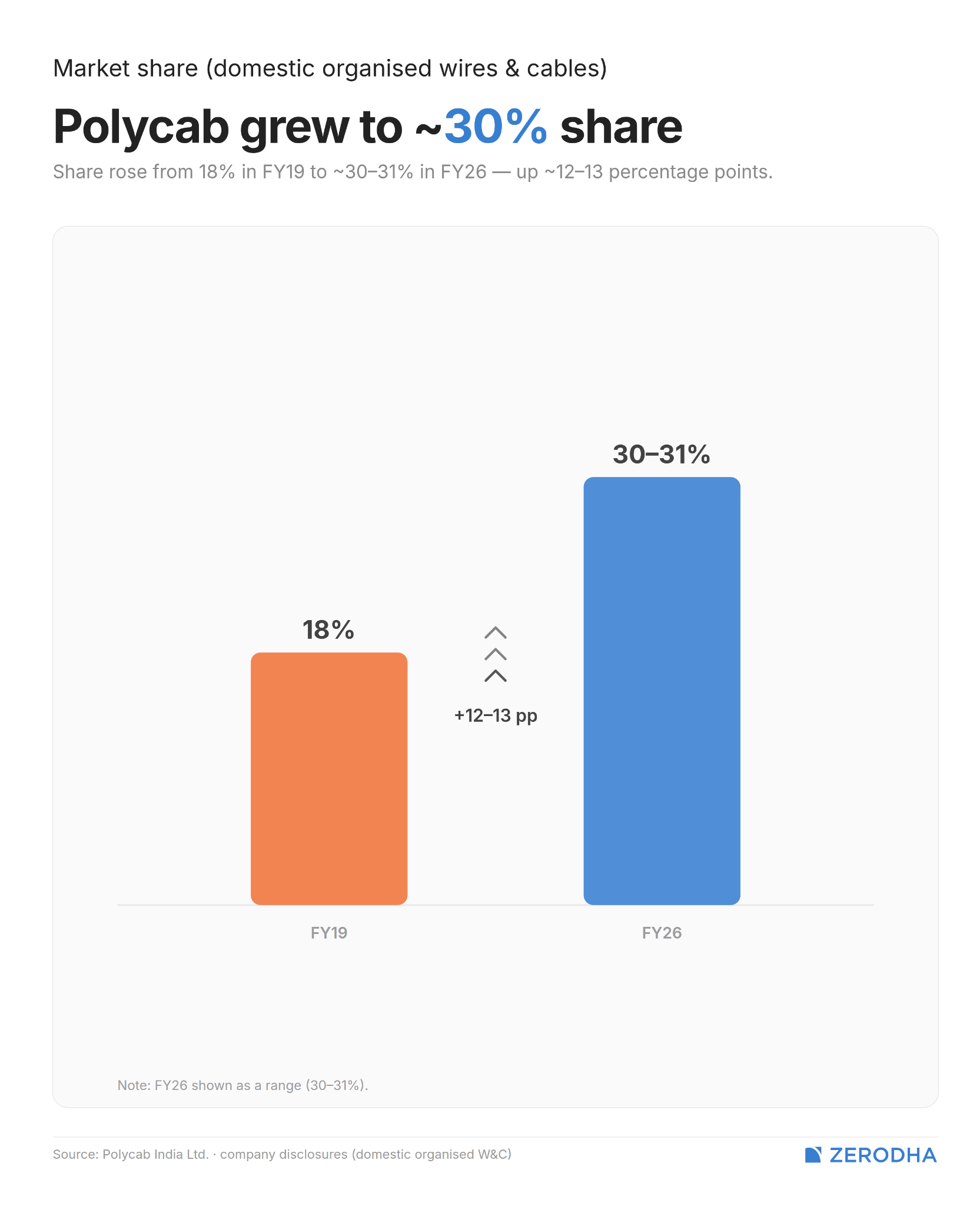

Polycab’s share of the organized domestic W&C market has climbed to 30-31%, up from 18-19% in FY19. In FY26 alone, they gained 3-4 percentage points. It’s very rare for the largest company in an industry to also be one of the fastest-growing.

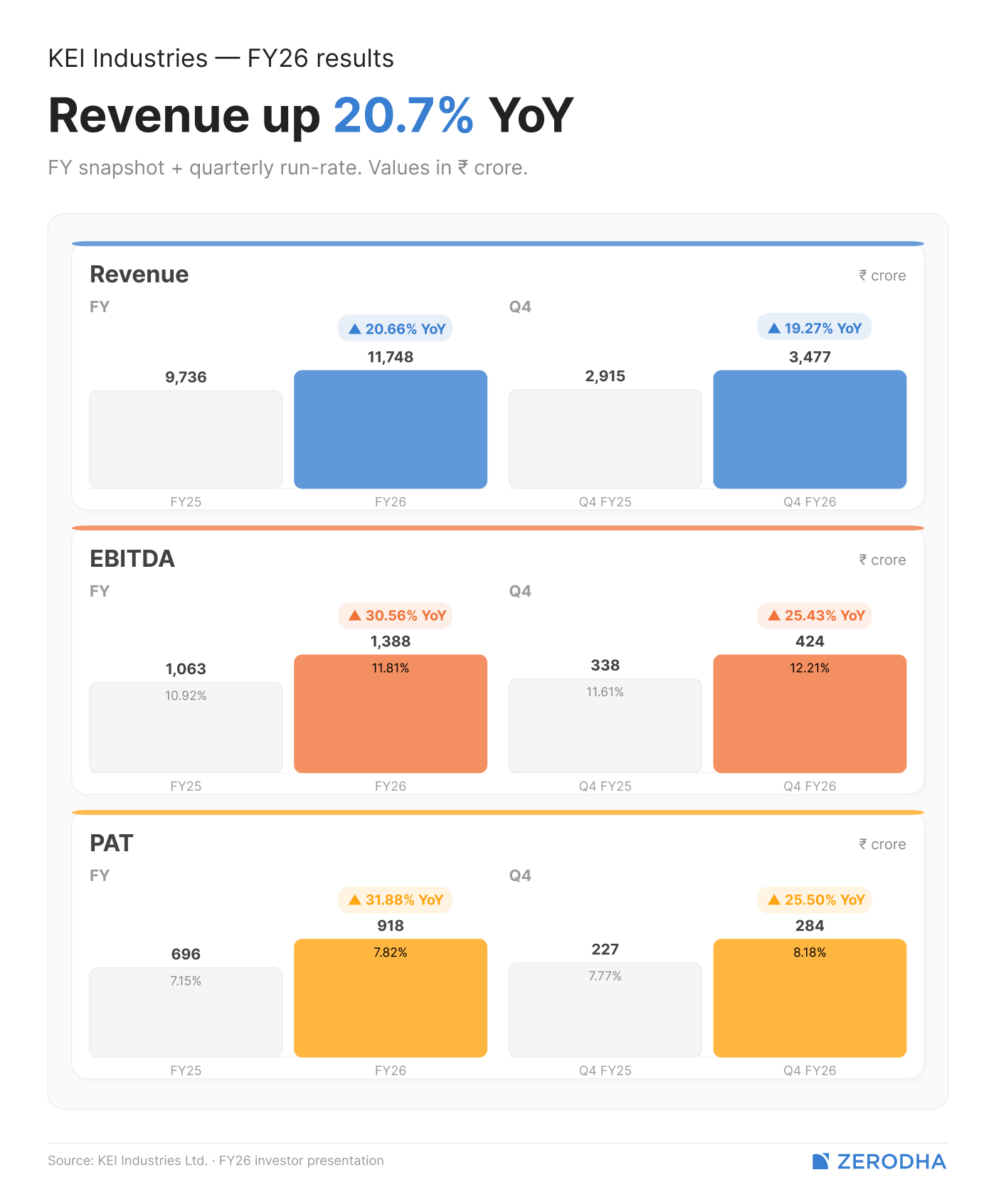

Meanwhile, KEI Industries, the second in line, grew its Q4 revenue by 19% to ₹3,477 crore. Full-year revenue hit ₹11,748 crore, up 21% year-on-year. Its EBITDA margin improved to 12.2% in Q4, up from 11.6% last year — a steady climb that’s been underway for a while now.

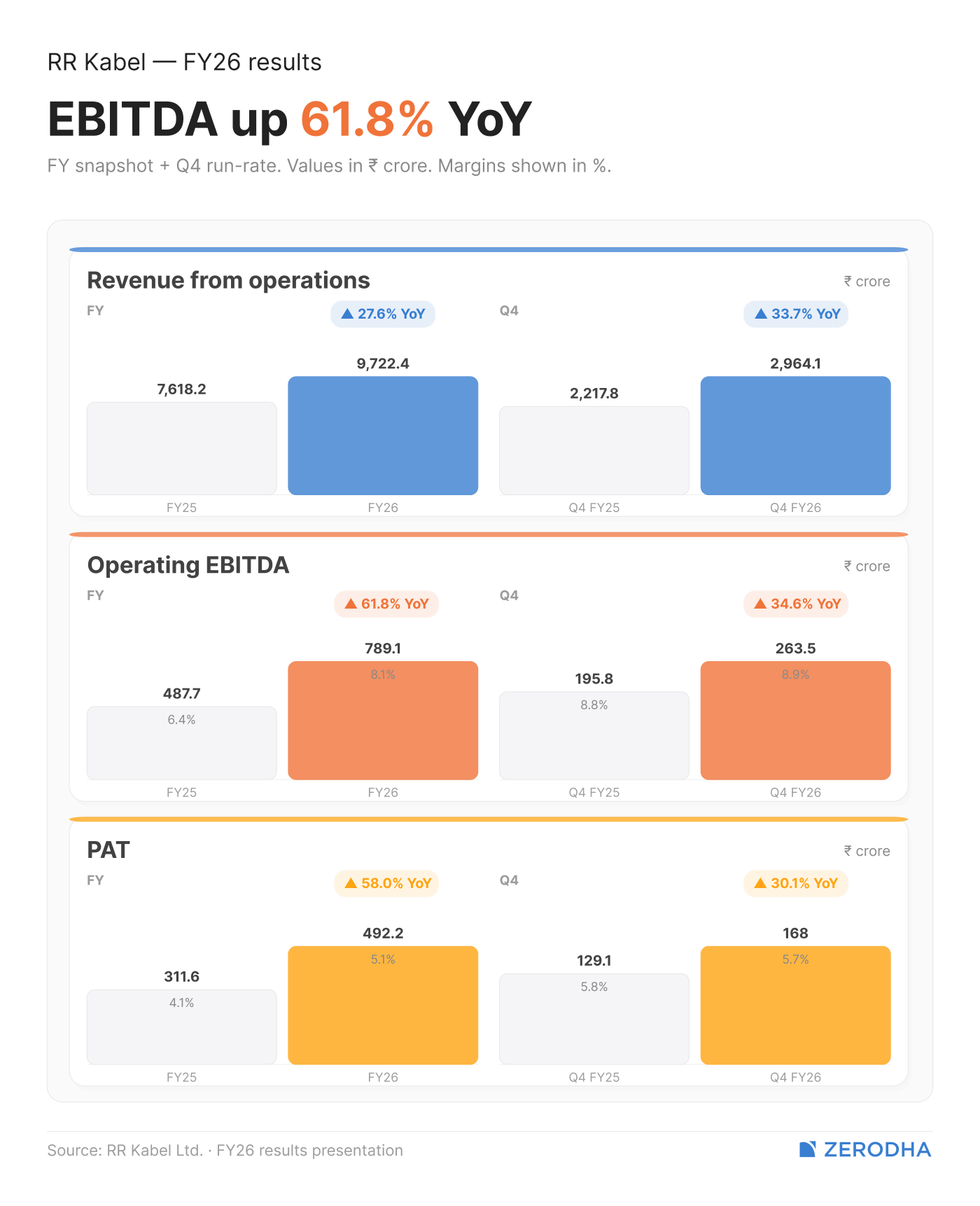

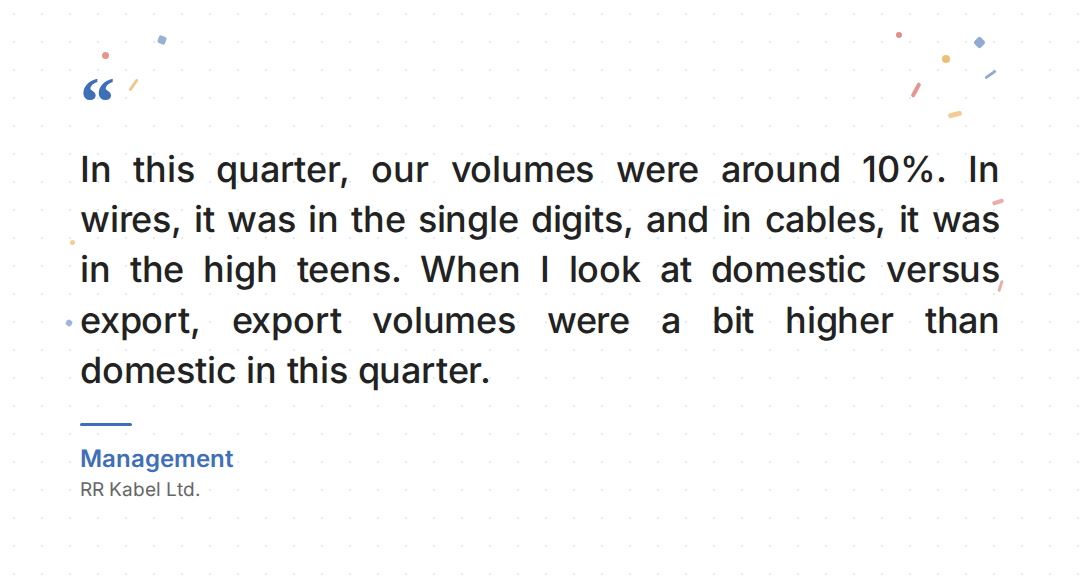

For RR Kabel, the relative upstart compared to its peers, Q4 revenue came in at ₹2,964 crore, up 34% from last year. For the full year, it crossed ₹9,722 crore, up ~28%. Its profit after tax for FY26 jumped 58% to ₹492 crore.

The copper effect

Now, let’s start with some of the problems we mentioned earlier.

Polycab’s wires and cables segment grew 30% in revenue this quarter, but that wasn’t really driven by volumes, which grew in low single digits. For instance, KEI’s volume growth this quarter was just 2%. RR Kabel managed ~10%, with wires growing in mid-single digits and cables in the high teens.

So where did all that revenue growth come from? Well, mainly from price hikes, owing to inflation in the biggest cost driver of the industry: raw material.

In our past coverage, we’ve spoken about how tricky pricing gets when the price of copper spikes — and copper and aluminium make up 70% of the cost of making wires & cables. Companies may or may not want to fully pass on price increases in a single go, and all three players diverged in terms of their pricing strategies in this respect.

However, copper inflation continues to be persistent enough to negate differences in those strategies.

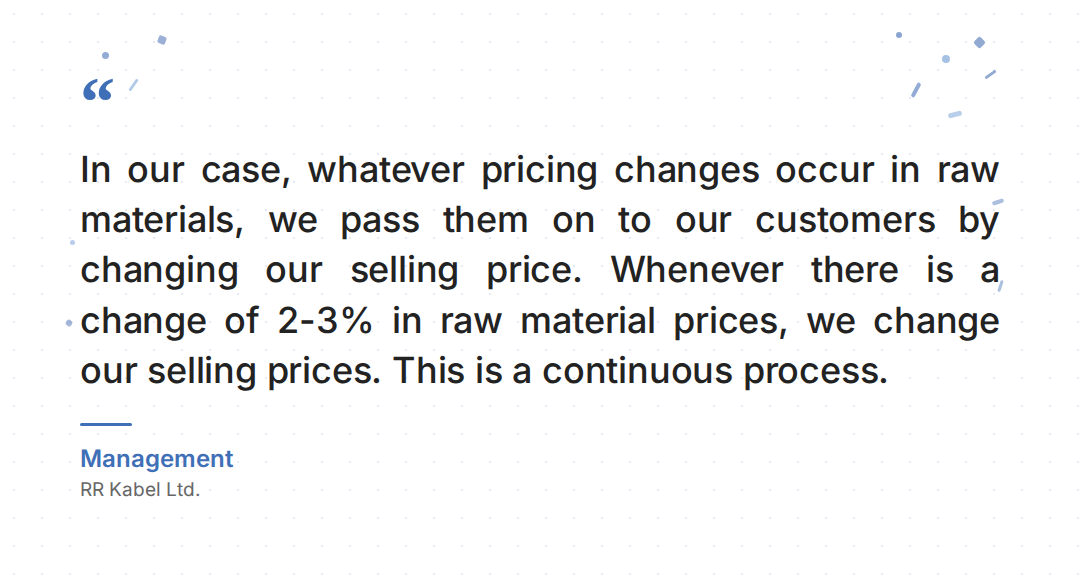

Average copper prices rose nearly 16% over the year, and aluminium climbed about 10%. Polycab hiked prices by 18-19% just between January and March. RR Kabel adjusts its prices every time raw materials move by 2-3%. KEI, in fact, puts a mechanism in its institutional contracts to pass on copper price inflation.

Now, last quarter, in anticipation of the price hike, retailers pre-stocked on wires & cables. However, that pre-stocking effect had dwindled down this quarter because retailers may have found the price too high. But what that could also mean is that, unlike last quarter, they couldn’t correctly predict the quantum of a future price hike.

That, of course, would happen if there was an unpredictable event. And this quarter, we can probably tell what that event was: the Strait of Hormuz crisis.

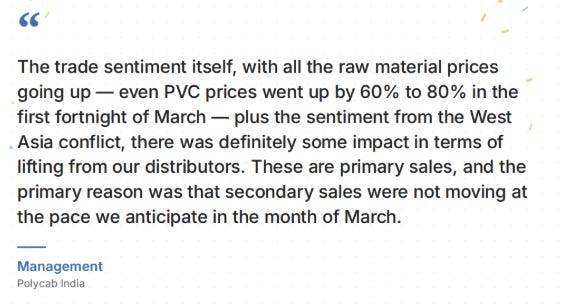

Partly due to the situation in Iran, prices of PVC (which is used to sheath the wires) shot up 60-80% in the first half of March. After all, PVC is a byproduct of oil, which was directly impacted by the crisis. Distributors pulled back on purchases because their own customers weren’t buying at the usual pace. It’s why Polycab admitted that they were expecting much stronger volume growth in Q4 than what they got.

The export reshuffle

The crisis at the Strait of Hormuz also contributed to volume compression through the export channel.

See, the W&C exports have largely been a bright spot all year. The industry had diversified smartly in response to US tariffs, pivoting to Australia, Europe, and the Middle East. But this quarter, owing to tensions in West Asia, that story took a sharp turn.

For the W&C industry, the immediate hit was on freight, as shipping lines simply refused to carry cargo to the Middle East. Finished goods sat in factories with nowhere to go. Material that had already shipped in February got stuck mid-route, unable to reach its destination. KEI, in fact, lost an estimated ₹50-60 crore in exports because of this.

RR Kabel was hit in a similar way. Products that were meant for the Middle East couldn’t leave the factory in March, and their inventory swelled with goods stuck in transit. The Middle East is also a big deal for RR Kabel, making up about 40% of their exports, which translates to ~12% of total revenue.

The workarounds exist, but are expensive. KEI described how containers are now being routed to Fujairah — a port in the UAE that’s still accessible — and then transported overland to Abu Dhabi and Qatar. It costs a lot more than the normal route. Most customers are splitting the extra freight cost 50-50 with KEI. But where contracts were priced on an FOB(Free On Board) basis (meaning the buyer pays for shipping), the full cost increase falls on the customer. They’re willing to absorb it because they need the material.

But the story took another meandering turn because of this. This disruption has pushed companies back towards a market they had been avoiding — the United States. This is a sharp deviation from the narrative over the last few quarters, where firms had to pivot away from the US because of steep tariffs.

Now, with tariffs having (somewhat) settled and the Strait of Hormuz disrupted, both KEI and Polycab have re-established their distribution networks in the US. KEI’s US order book stood at ₹50–60 crore as of March 31. Polycab noted that US and European grid infrastructure is 50–60 years old and desperately needs upgrades. North America was already 40% of Polycab’s FY26 exports.

That being said, the full-year export numbers still look strong despite the March disruption. KEI’s exports grew 45% to ₹1,833 crore. RR Kabel derives 30% of its W&C revenue from exports.

The capacity ceiling

Part of the volume story is driven by higher raw material prices and geopolitical uncertainty. But, on the other hand, volume growth is also limited by the current capacity constraints of the companies.

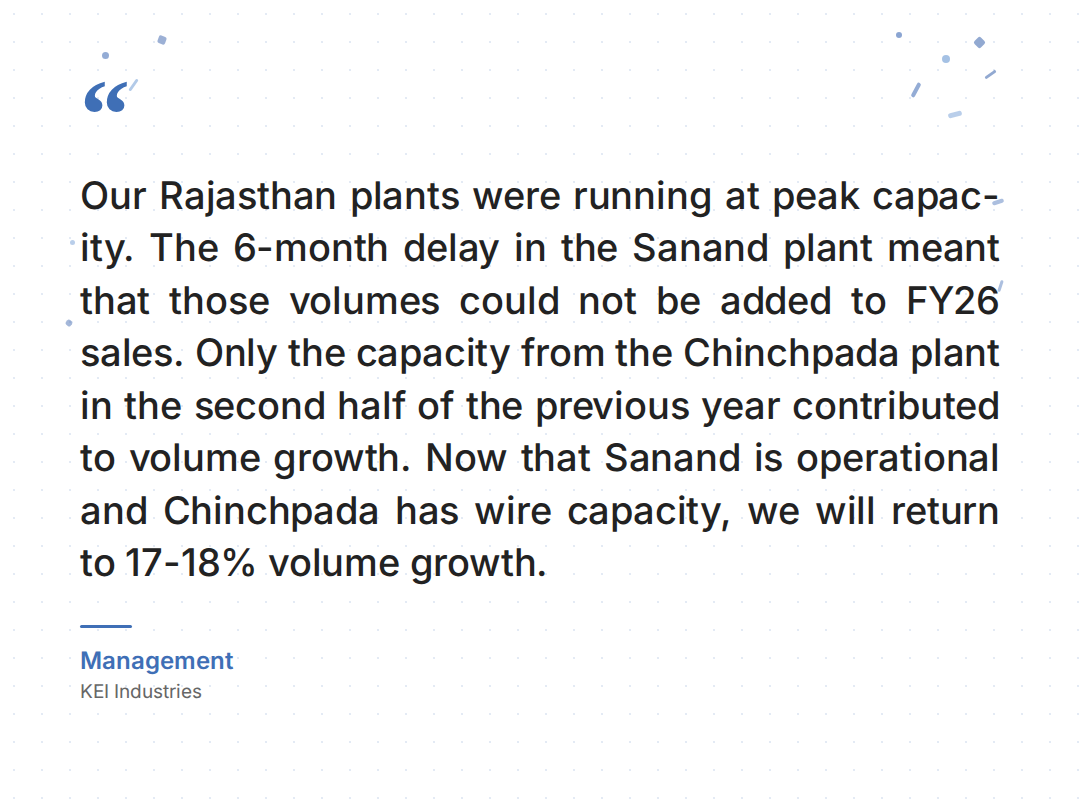

For instance, KEI’s cable plants in Rajasthan were maxed out for the entire year. They simply couldn’t push any more product through those factory lines. Their big new plant in Sanand, Gujarat got delayed by six months. It only started production around late December 2025, and barely contributed to Q4 sales. KEI’s management noted that the low-volume growth was directly due to capacity constraints.

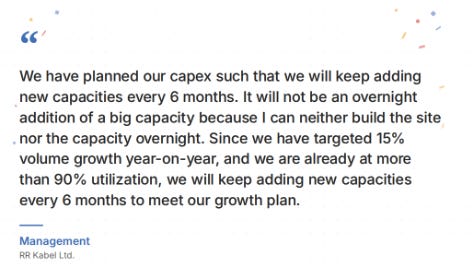

RR Kabel is in a similar spot. Its cable lines are already running at over 90% utilization. They’ve designed their entire ₹1,200 crore expansion plan around adding new capacity every six months, because at their growth rate, even a small delay creates a bottleneck.

Polycab has a bit more room, sitting at about 75% utilization. But even they felt the squeeze in March, because Q4 is typically the strongest quarter for this industry. About 90% of Polycab’s business runs through its distribution channel. When secondary sales slow down, the dealer stops buying from Polycab. That’s what happened this March. Polycab’s management said their volume growth expectations for March were significantly higher than what they got.

The industry’s response to all of this is straightforward: invest in more factories.

Polycab invested ₹1,480 crore in capex this year, with 90% going into wires and cables. They’re on track for ₹6,000-8,000 crore by FY30 under their strategic plan, Project Spring. KEI is spending ₹600–700 crore annually over the next two to three years; Sanand Phase 2, dedicated to extra-high-voltage cables, should be ready by March 2027. RR Kabel is ramping up its ₹1,200 crore programme, with the majority of spending happening this year.

However, it will be long before this capex is fully built, much less contribute to returns.

The next waves of demand

Even as the industry scrambles to add capacity, the nature of demand is shifting. Two things stood out this quarter.

Data centers

We’ve heard this mentioned in passing before, but this time, all three firms brought it up explicitly as a major opportunity.

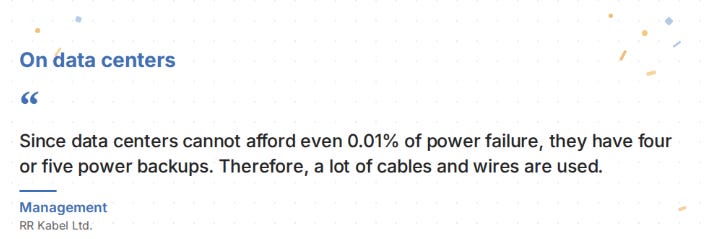

See, a data center can’t afford to lose power for even a moment. So they need to have multiple backup systems beyond their core power supply. Each of those backups needs its own set of cables. So, the amount of cabling that goes into a single data center is enormous compared to other buildings.

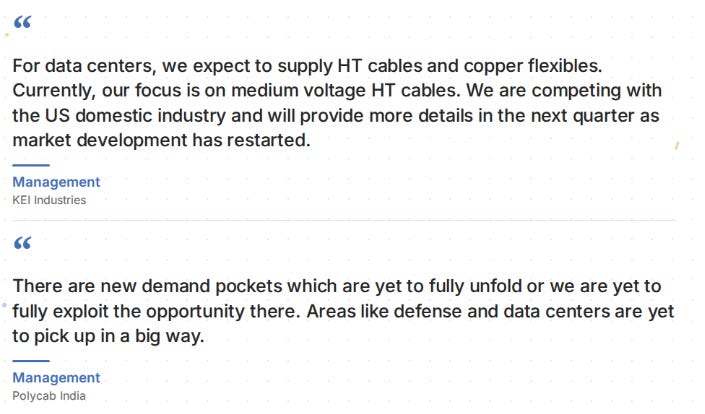

KEI, for instance, plans to supply medium-voltage cables and copper flexibles to data center projects. Polycab listed data centers alongside renewables and defense as sectors where the opportunity hasn’t fully opened up yet. None of these companies are earning meaningful revenue from data centers today, but the bet is on the next three to four years, as India’s data center buildout gathers pace.

Extra-high voltage (EHV) cables

Then, you have the heavy-duty extra-high voltage (EHV) cables, which carry power over long distances, like from a solar farm to the grid. They’re complex to make, need specific certifications, and earn better margins than regular cables.

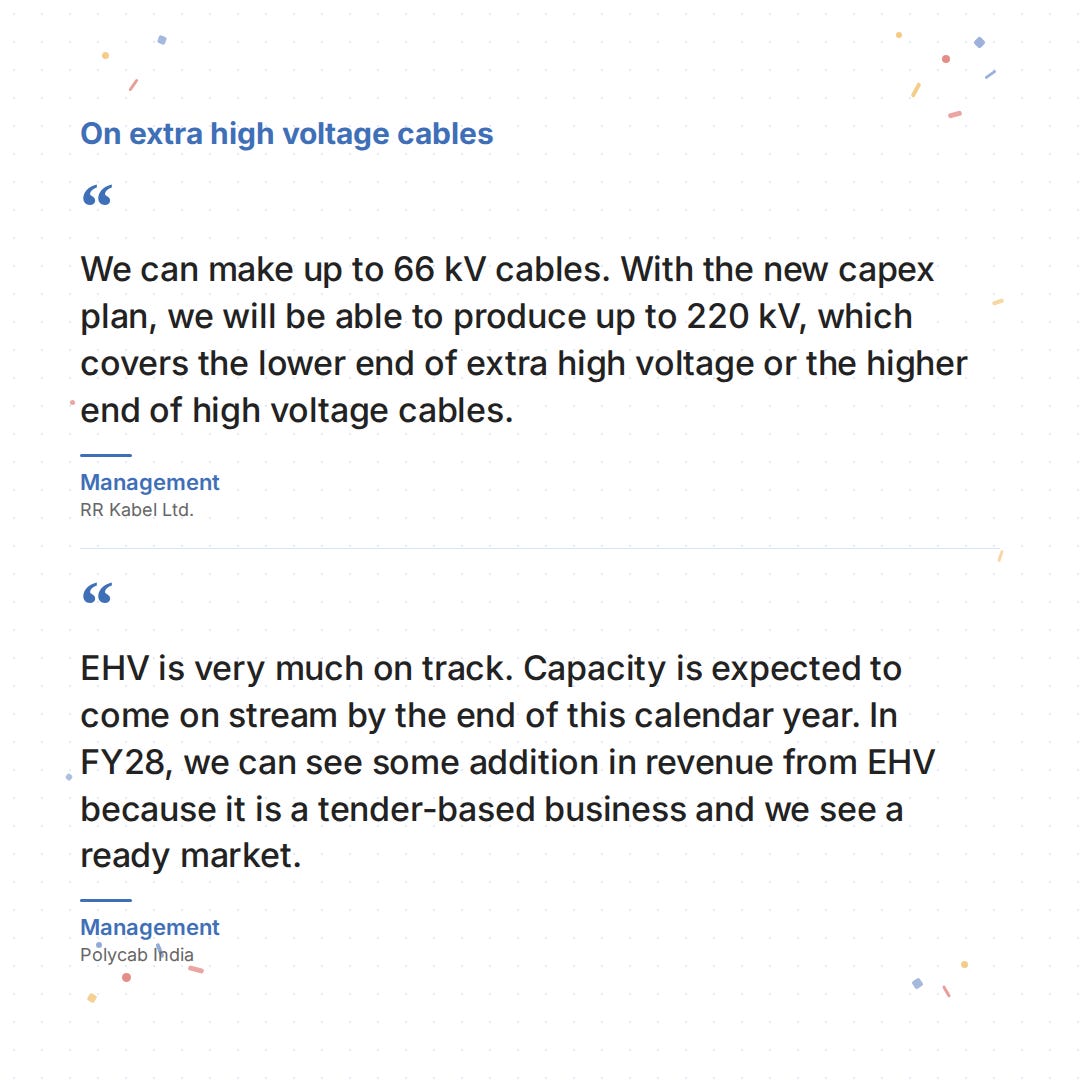

KEI has been the most aggressive here: its EHV sales hit ₹559 crore for the year, up 82%. Their order book for EHV alone is ₹625 crore, with another ₹233 crore worth of orders where they’re the lowest bidder and likely to win. RR Kabel, meanwhile, is upgrading its capability from 66 kV to 220 kV, with new capacity rolling in through FY28.

Polycab’s EHV factory is expected to come online by the end of this calendar year — and they pointed out that half of India’s EHV cable consumption is currently met through imports. That’s a lot of domestic demand just sitting there for whoever can make the product.

As we’ve covered before, cables have been outpacing wires as the primary growth engine for this industry. That trend briefly flipped in Q3 when distributors hoarded wires ahead of a copper price spike. In Q4, though, the usual trend returned.

What comes next

The demand picture for wires and cables has rarely looked this clear.

India added a record 55.29 GW of non-fossil power capacity in FY26, nearly double the previous year. The Union Budget allocated ₹12.2 lakh crore in government capex for FY27. Add private investment, and Polycab estimates ₹36–37 lakh crore will be invested in FY27, with a large share going into sectors that feed directly into cable and wire demand: utilities, metals, oil and gas, manufacturing, and so on.

But the supply side hasn’t caught up yet. The next few quarters will come down to how soon the factories match the order books. KEI is guiding for 17–18% volume growth in FY27, mostly from Sanand. RR Kabel is targeting 16–18%. Polycab expects to keep delivering 1.5 times whatever the market grows at.

If those targets hold, that could unlock a new phase of growth for an already-rapidly growing industry.

Tidbits

Torrent has grabbed 38% market share in India’s semaglutide race

As per industry data, Ahmedabad-based drug maker Torrent Pharma has taken a significant early lead in the generic semaglutide market, grabbing a nearly 38% share within a month of launch.

Source: Economic Times

Ola Electric gets nod for mass market scooter from ICAT

EV major Ola Electric has announced that its mass market electric scooter, S1 X+ (5.2 kWh), has been approved by the International Centre for Automative Technology (ICAT), a government certified testing agency under the CMVR (Central motor vehicle rules).

Source: Hindu BusinessLine

Cloudflare to cut about 20% workforce as AI adoption reshapes operations

The internet infrastructure and cybersecurity company Cloudflare said it would cut about 20% of its workforce as the company restructures operations around the rapid adoption of artificial intelligence tools, and forecast second-quarter revenue slightly below Wall Street expectations.

Source: Reuters

- This edition of the newsletter was written by Kashish and Vignesh

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Kyle Chan on China’s industrial power and entrepreneurship

If you enjoy The Daily Brief, here’s something we bet you’ll like. We recently spoke to Kyle Chan, one of the sharpest minds we read to understand China - we’ve often featured his insights on The Daily Brief. Our conversation dives deep into the dynamics that shape China’s manufacturing landscape. It goes into the nature of Chinese entrepreneurship, how China’s price wars affect innovation (and vice versa), why China’s policies are far less all-knowing than people assume, and how China wields its manufacturing prowess as a geopolitical power. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

I am unsuprised about the government scheme not working, it was too good to be true