India’s fuel-blending machine enters its next costly phase

Apparently, ethanol is not the only game in town

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

India’s fuel-blending machine enters its next costly phase

India’s wet waste problem is a $50 billion opportunity

India’s fuel-blending machine enters its next costly phase

On 29 May, the Road Transport Secretary of India, V. Umashankar said that India is likely to bring a mandate for blending a biofuel named isobutanol into diesel later this year.

A week before that, the Bureau of Indian Standards had notified fuel specifications for E22, E25, E27 and E30 petrol blends, all of which contain higher proportions of ethanol than the E20 that India currently uses.

And then, later this week, Maruti Suzuki is expected to launch India’s first mass-market flex-fuel car that can run on any levels of ethanol, be it E20 or E100.

All of these announcements took place within a span of a week. Some of these moves may have been in the works for years, but there’s also an unmistakable sense of urgency involved here.

We’ve covered India’s ethanol blending program before. It dates back to a National Policy on Biofuels that dates all the way back to 2018. That policy has achieved a key milestone of 20% ethanol (E20) in all petrol-based vehicles, in an attempt to reduce our oil import bill.

The Strait of Hormuz crisis, to which India has found itself acutely exposed, speeded up some of those timelines. Petroleum minister Hardeep Singh Puri told Parliament in March that the disruption was unlike anything seen in modern energy history.

It is in that context that biofuels are no longer just a climate or farm policy. They are being framed as a strategic hedge to preserve independence.

However, the ethanol blending programme has proven to be a very costly affair on multiple fronts. While those costs are yet to go away, India is seriously considering what comes after E20. This story attempts to make a cohesive narrative out of all these announcements.

Let’s dive in.

Ethanol overcapacity

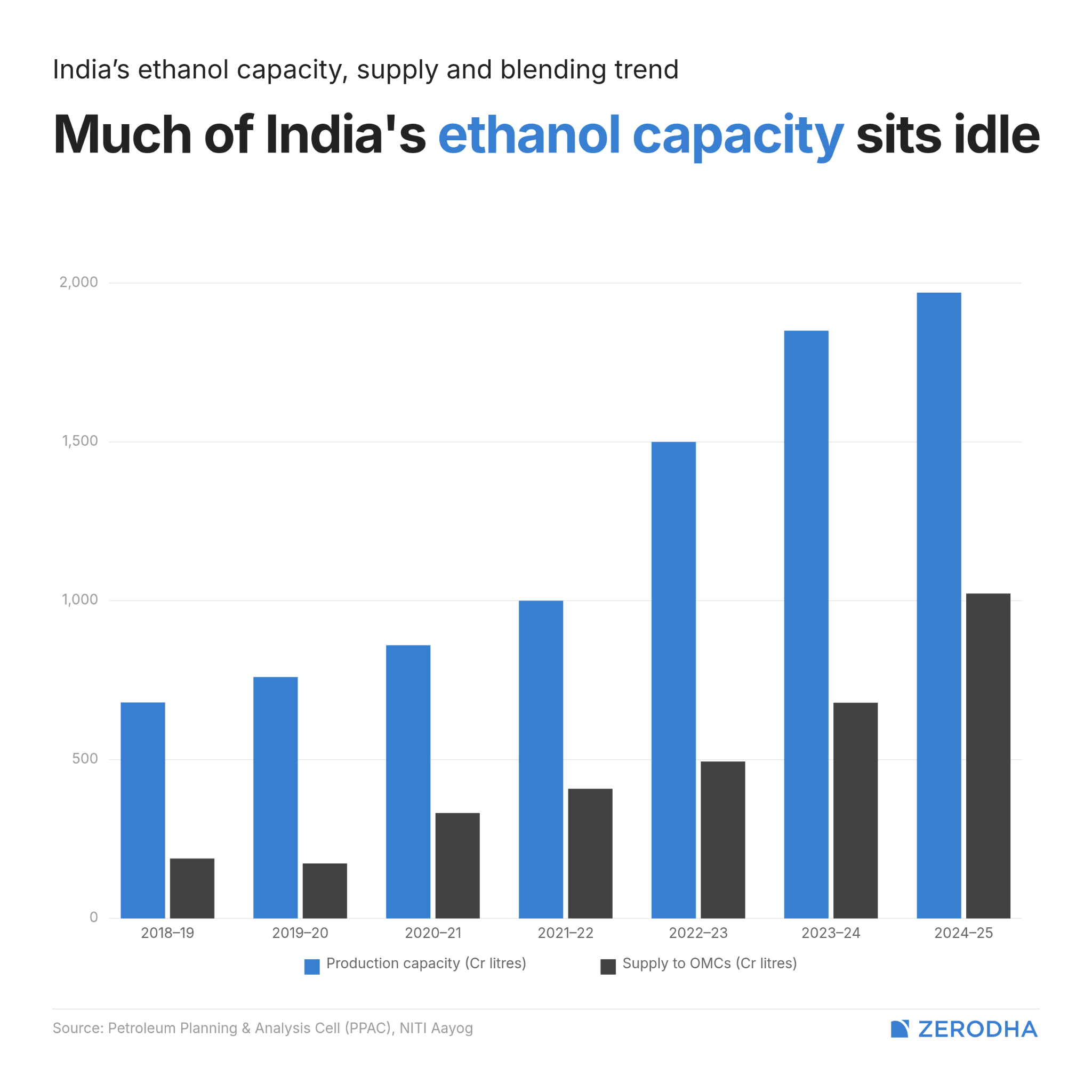

India went from 1.5% ethanol blending in 2014 to 20% by November 2025. From April 2026, E20 is mandatory nationwide. Over the last decade, as per government statistics, the program has substituted around 245 lakh metric tonnes of crude oil. As far as these objectives matter, this has been a successful industrial policy.

But the incentive machine that made it possible doesn’t have an off switch.

See, starting in 2018, the Centre rolled out an interest subvention scheme where the government bore up to 6% per annum (or 50% of the interest rate, whichever was lower) on loans taken to build new ethanol distilleries or expand existing ones. Over 1,100 sugar mills received in-principle approval. Oil marketing companies (OMCs) like IOCL and BPCL signed long-term procurement agreements at government-fixed prices.

So investors saw three things at once: subsidized capital, a captive buyer, and a government target (E20 by 2025) that implied demand would keep rising. Everyone built at once.

However, this has now caused overcapacity in ethanol. India now has installed ethanol capacity of roughly 2,000 crore litres — against E20 demand of only about 1,100 crore litres. Another 400 crore litres of capacity is expected to come online by FY27. OMCs are absorbing only about 60% of the ethanol being offered to them, and CareEdge expects utilisation to stay at 65-75% for the next three years.

In other words, the government aggressively expanded supply, but without adequate support on the demand side. Part of this also stems from government-fixed price floors for farmers.

This surplus is the engine driving everything that follows. The policy system has to find new demand, or watch those investments go bad. Meanwhile, the procurement agreements are still in place, and the subsidies and administered prices still apply. That will certainly keep capacity coming.

Beyond E20

The most intuitive answer to the surplus problem is to put more ethanol into fuel. That’s what the new ethanol standards launched by BIS solve.

At the same time, the government is pushing flex-fuel vehicles — cars and motorcycles that can run on E85 (85% ethanol) or even E100 (pure ethanol). The Central Motor Vehicle Rules have been amended to recognise these fuels, and E100 is now part of official testing and certification standards in April 2026. IndianOil already sells E100 at 183 retail outlets.

But how meaningful is this, really?

The practical constraints are significant. E85, for instance, delivers nearly 30% worse mileage than petrol, simply because ethanol has less energy per litre — about two-thirds of gasoline’s calorific value. Additionally, a flex-fuel upgrade adds an estimated ₹40,000-50,000 to a vehicle’s price.

Maruti’s own executive, Rahul Bharti, has cautioned that flex-fuel volumes are “unlikely to be significant in the near term“ due to limited models and limited pump availability. It’s a chicken-and-egg problem: OEMs won’t build flex-fuel cars without fuel at pumps, and OMCs won’t invest in E85 or E100 pumps without enough cars on the road.

Even if India raises ethanol blending from E20 to E30, the incremental energy-security gain diminishes with each step-up. As per NITI Aayog’s own planning assumptions, E20 requires 1,016 crore litres of ethanol, while E30 would require above 1,520 crore litres. Those extra 500 crore litres of ethanol displace only about 339 crore litres of petrol on an energy-equivalent basis.

Naturally, these crude numbers assume there won’t be technological innovation to ensure higher ethanol blends work. But even then, innovation also requires a lot of risk capital. And OEMs will be hesitant to spend huge amounts of money on such innovation without assured supply, especially when other proven technologies like EVs and CNG already exist.

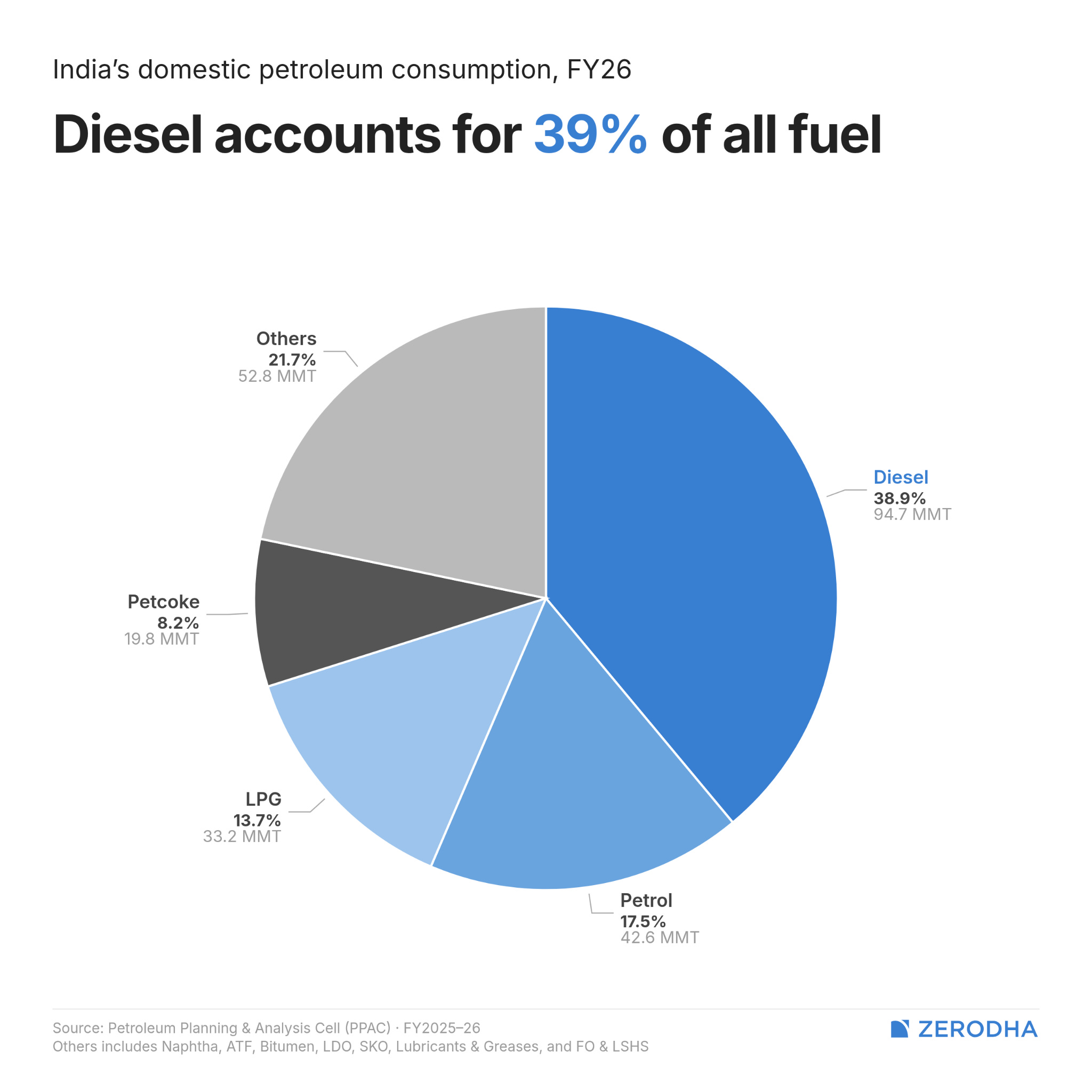

Most importantly, petrol is not where India’s real oil vulnerability lies. We consume more than double the diesel compared to petrol. Trucks, buses, agricultural equipment, railways, gensets — all of them run on diesel. A petrol-blending strategy, no matter how ambitious, can only address a fraction of India’s crude oil dependence.

The isobutanol pivot

India did try to do for diesel what it did for petrol. The government ran trials blending ethanol into diesel, and failed. And the reasons for this are entirely technical.

See, diesel engines work on compression ignition: the fuel-air mixture ignites from being compressed, not from a spark plug. This requires a high cetane number, which is a measure of how easily a fuel ignites under compression. Ethanol has a very low cetane number. When you put it in a diesel engine, you get incomplete combustion, engine knocking, and power loss.

Moreover, ethanol and diesel just don’t mix. Ethanol absorbs moisture quite easily, which is not good for diesel ignition.

So, the government pivoted to isobutanol.

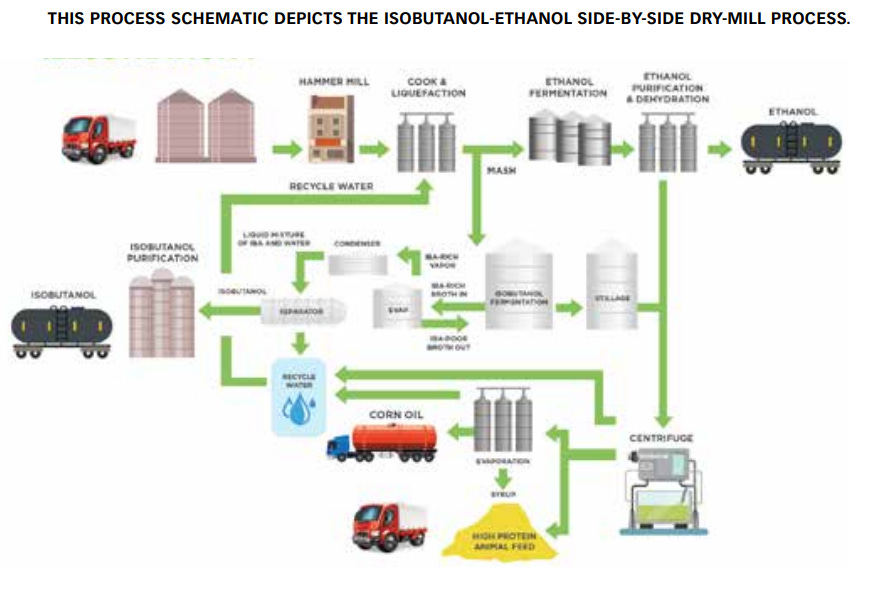

Just like ethanol, isobutanol is also an alcohol. Both can be made from the same raw materials, like sugarcane molasses and maize. They share much of the core infrastructure. But they are not the same molecule. They are produced through different biological processes.

Ethanol is made through the glycolysis fermentation pathway that yeast has been performing for ages. But no organism in nature evolved to produce isobutanol in large quantities. To make useful quantities of isobutanol, you need genetically-engineered organisms.

Isobutanol is better in every way that ethanol isn’t. It has higher energy density than ethanol, mixes with diesel much better, and doesn’t turn into vapour easily under pressure — which is exactly what a compression-ignition engine needs.

The industrial infrastructure for this is starting to take shape. The Automotive Research Association of India (ARAI) is testing 10% isobutanol-diesel blends. BPCL is involved in the validation. In fact, Praj Industries, India’s largest ethanol plant EPC company, has a partnership with Gevo, a US biotech firm that developed a proprietary yeast capable of fermenting sugars into isobutanol instead of ethanol. They’re setting up a demonstration-scale fermentation module at a sugar mill in Maharashtra.

As per the Indian Sugar Mills Association, a 150 kilo-liters (kL) per day ethanol refinery can pivot, with modest investment, to produce 125 kL ethanol plus 20 kL isobutanol each day. The existing surplus capacity becomes the foundation.

Proof of concept

This is where the story needs a reality check. The pitch that isobutanol is a straightforward bolt-on to India’s existing ethanol infrastructure is appealing. But it understates the difficulty considerably.

What India is attempting with isobutanol doesn’t have a powerful precedent. One of the key inspirations for our biofuels policy was Brazil, the most successful case of an ethanol industrial policy, and a pioneer in flex-fuel vehicles. But there is no Brazil for isobutanol. No country has commercialised isobutanol-diesel blending at scale yet.

The biggest bottleneck to that is obviously biological. In wild-type yeast, which generates ethanol at scale, isobutanol is a byproduct produced in very minimal quantities. To make useful amounts, you need engineered microbes with the isobutanol pathway bolted onto their metabolism.

But unfortunately, isobutanol itself is toxic to the very organisms that produce it. At concentrations of just 1-2% in the fermentation broth, isobutanol starts killing the microbes. Compare this to ethanol, where industrial yeast happily tolerates concentrations of 15-20%. What this means in practice is that with isobutanol, you get a far more dilute broth with lots of unwanted byproducts, which also makes separation and purification more expensive.

Gevo, which is Praj’s partner, seems to have developed a technology that prevents the concentration from ever reaching toxic levels. But this adds capital cost and process complexity that ethanol doesn’t need.

Which is where we also address the matter of cost.

Bolting on isobutanol capabilities to an existing ethanol plant may cost only 20-30% of that plant. But a new ethanol plant costs several hundred crores. A 20-30% retrofit across India’s surplus distilleries is not a trivial investment, especially when the economics of isobutanol production at Indian sugar mill conditions have not been demonstrated at commercial scale.

Additionally, you need significantly more glucose to produce one litre of isobutanol compared to ethanol. That also means you need a lot more maize and other foodgrains (which contain glucose) to make a given amount of isobutanol. And we make most of our ethanol through foodgrains rather than sugarcane.

In our primer, we covered how the ethanol industrial policy is draining our foodgrains, even making us import-dependent on maize — a crop we’ve always been self-sufficient in. In fact, the Economic Survey 2025-26 itself flagged a tension between self-sufficiency in energy and that in food. Isobutanol could worsen this tension further.

Now, isobutanol can also be made through chemical synthesis rather than biological fermentation. But the former would be an expensive process for India. At least with fermentation, existing ethanol plants can be modified. But chemical synthesis will require building new capacities from scratch.

The distance between a validated demo plant and a nationwide-blending mandate backed by commercial-scale production is still significant. And we haven’t even delved into the changes that automakers would need to make to their engines for isobutanol, eventually creating a similar version of the chicken-and-egg problem that plagued ethanol in the first place.

What this means

India’s biofuel programme stands at an inflection point. The energy-security logic has become more urgent than ever, and sugar-based alcohols like ethanol have become part of a serious consideration that involves coal, solar, wind, and nuclear.

But ethanol is hardly a foolproof solution. It delivers less energy per litre than petrol, imposes a mileage penalty that consumers notice, and takes away resources from other parts of agriculture.

At the same time, EVs are catching up. NITI Aayog’s own modelling shows that faster electric two-wheeler adoption materially lowers ethanol demand, just as our industrial policy tries to match it with supply. We also have an industrial policy for EV adoption, but India’s fiscal resources are finite.

The more it invests in a distillery-and-flex-fuel ecosystem, the harder it becomes to pivot if electrification overtakes the ethanol thesis. Industrial lock-in is a real risk with India’s strategy, and the next few years will determine which path India has committed to.

India’s wet waste problem is a $50 billion opportunity

For twenty-five years, India has had a rule on the books: households must keep their wet waste separate from their dry waste. For twenty-five years, almost nobody has bothered. Our kitchen scraps, vegetable peels, and leftover food go into the same bags as plastic and paper. They’re loaded on the same truck, and dumped onto the same growing mountain at the edge of town.

On the 1st of April this year, the government decided to try again, harder. This time around, the new Solid Waste Management Rules, 2026 require four separate streams — wet, dry, sanitary, and “special care” items like batteries or old medicine. They make bulk generators of waste, like apartment complexes or commercial set-ups, legally responsible for processing their own wet waste. And they back the whole thing with penalties, with a digital system that tracks garbage from your bin to its final destination

There are many reasons this might not work out. But a Delhi-based think tank — the Council on Energy, Environment and Water, or CEEW — has put a number on what happens if we do get this right. The wet half of India’s urban garbage, it argues, could become a $50 billion industry, generate 26 lakh jobs, and flip our waste from one of our fastest-growing sources of emissions into something that’s net-negative — in just two decades.

Those are the table stakes we’re playing for. But reading their report also tells you why that bet is so hard to win.

Why the wet stuff is the whole game

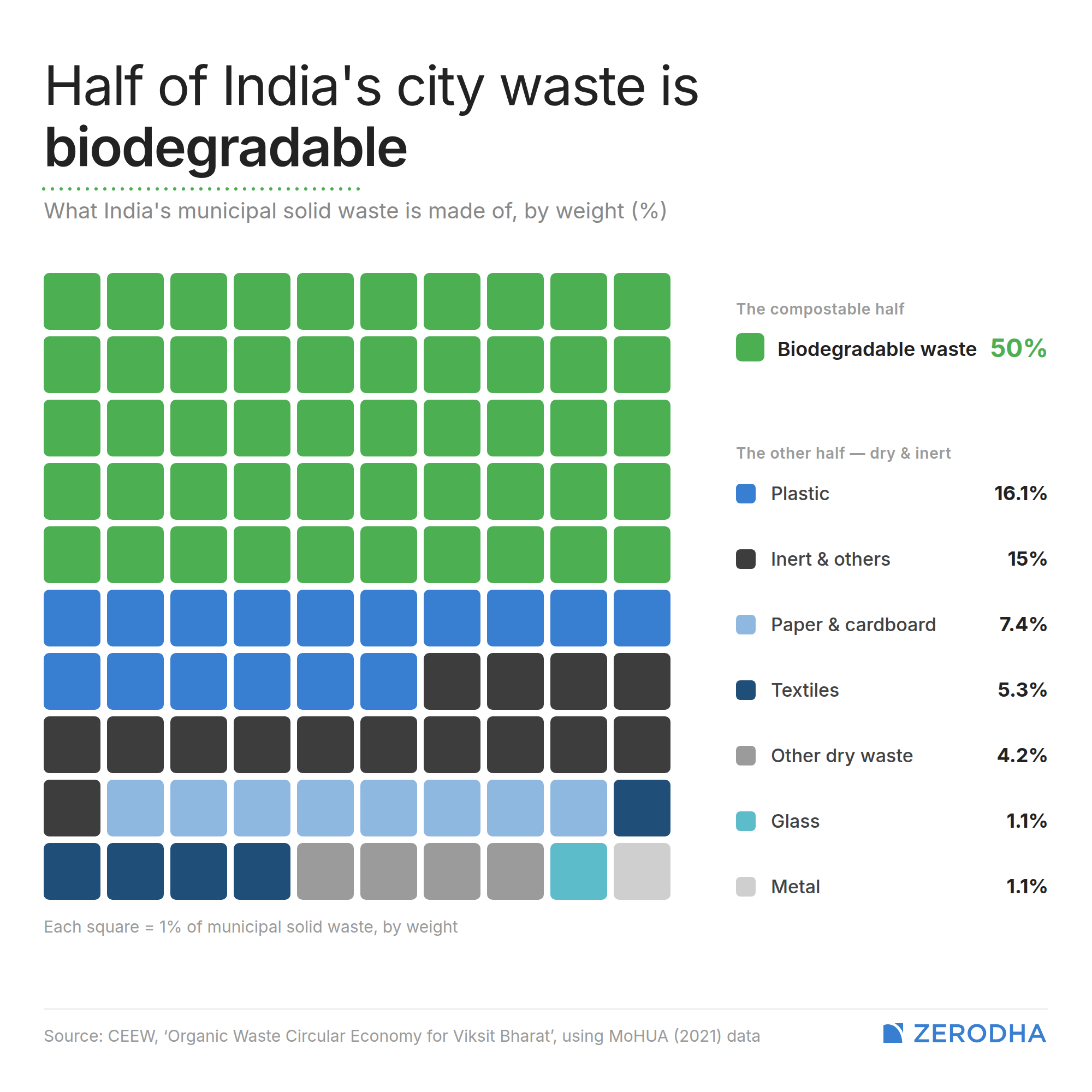

Roughly half of everything Indian cities throw away is “organic” — kitchen waste, market waste, garden trimmings. Technically, this is called the “organic fraction of municipal solid waste”. But you can just think of it as “stuff that rots”. By 2047, CEEW thinks India’s cities will be generating around 208 million tonnes of it every year.

That discarded, rotting material is the single most important thing in the entire waste system, because it’s a contaminant. Mix it in with dry waste and it soaks into paper, rusts metal, and coats plastic in slime. This pushes recyclable material beyond the pale of recovery. On the other hand, if you separate this wet waste out cleanly, the rest of your garbage suddenly becomes worth recovering.

Fixing wet waste, in other words, doesn’t just fix half the problem. It unlocks everything else.

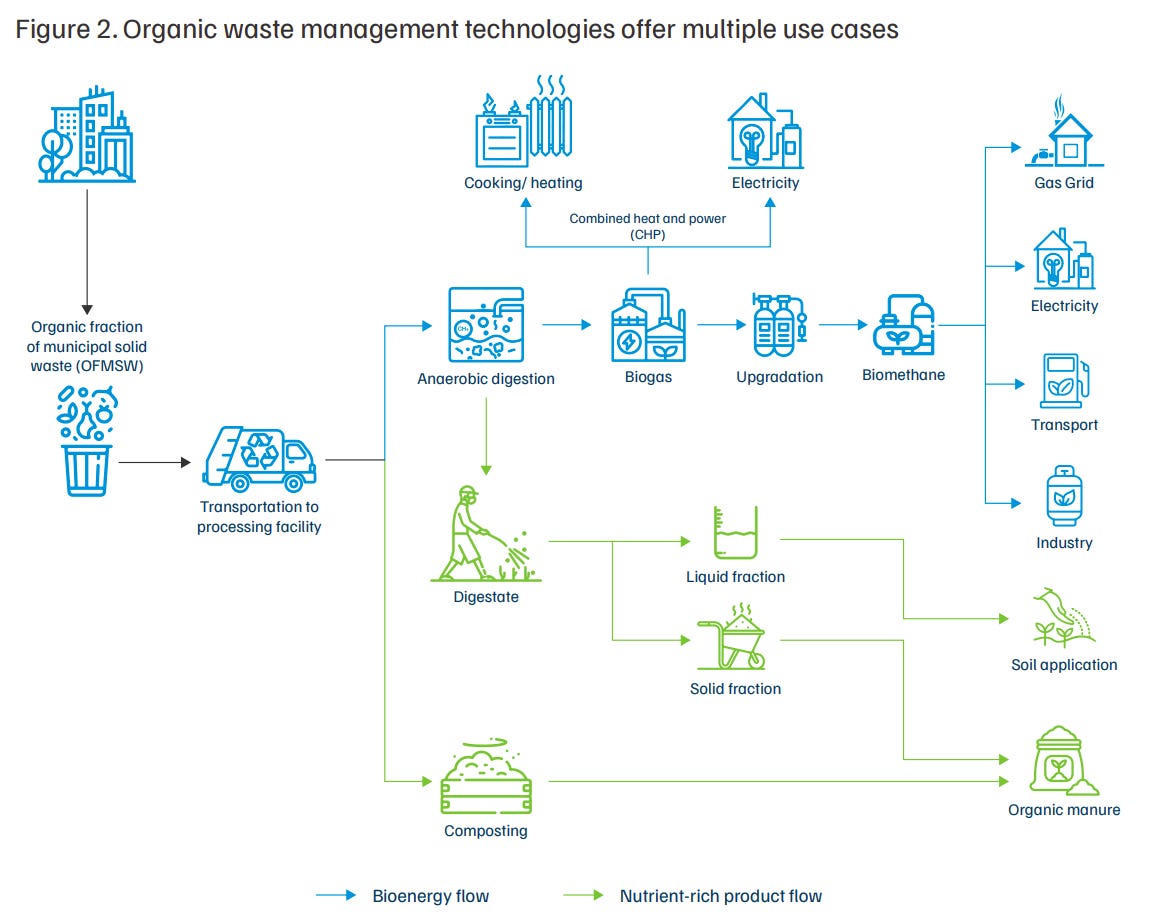

How do we fix it, though? There are two serious options we have. One, we can compost it — let it break down in the open air, with oxygen, into a soil-like manure. Or you can run it through “biomethanation” — seal it in a tank without oxygen and let bacteria turn it into biogas. This, as we wrote earlier, creates fuel that can run everything from CNG buses and PNG kitchens.

Composting gives you fertiliser. Biomethanation gives you fertiliser and fuel.

Right now, the split is wildly lopsided. Composting handles about 96% of India’s treated wet waste; biomethanation just 4%. CEEW’s report is, essentially, an argument about how fast that ratio could shift towards biomethanation — and what we gain, and lose, depending on this.

The greener the plan, the fewer the jobs

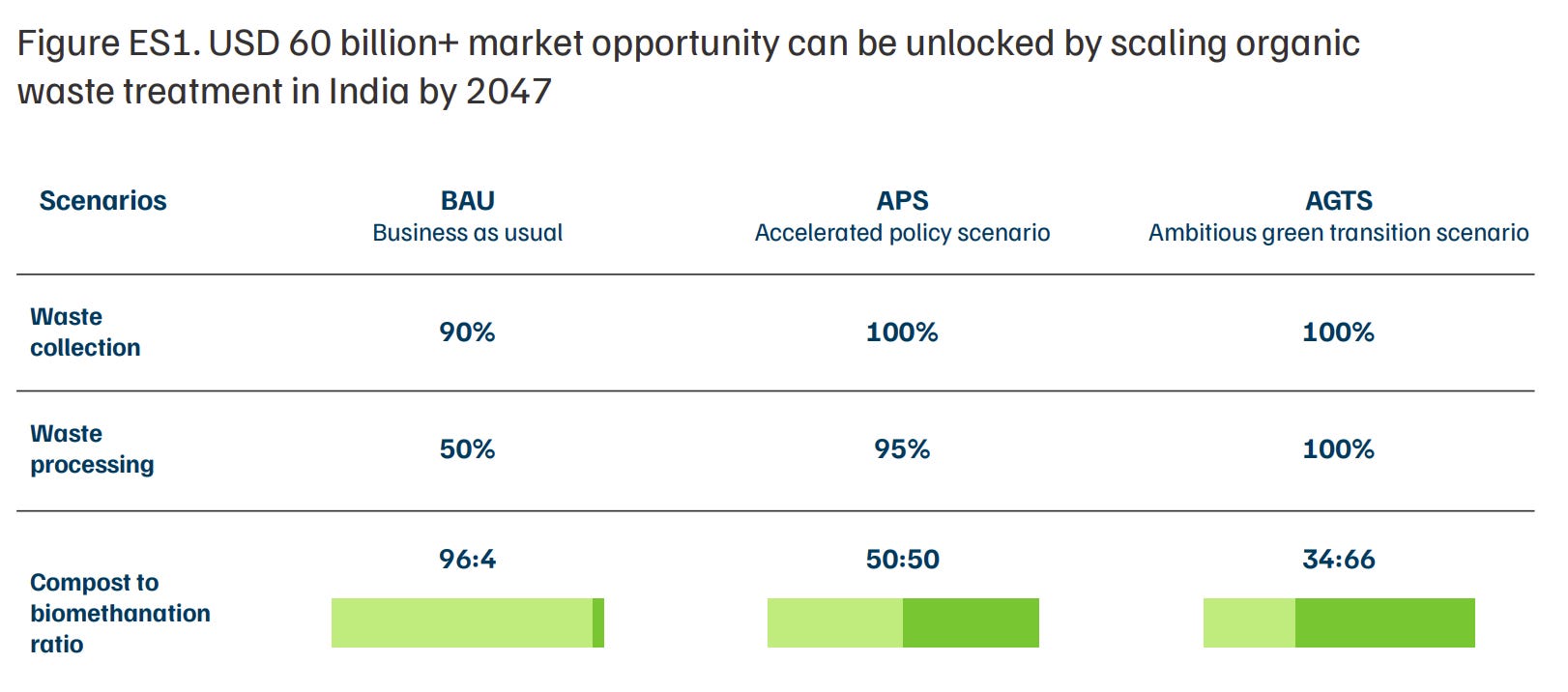

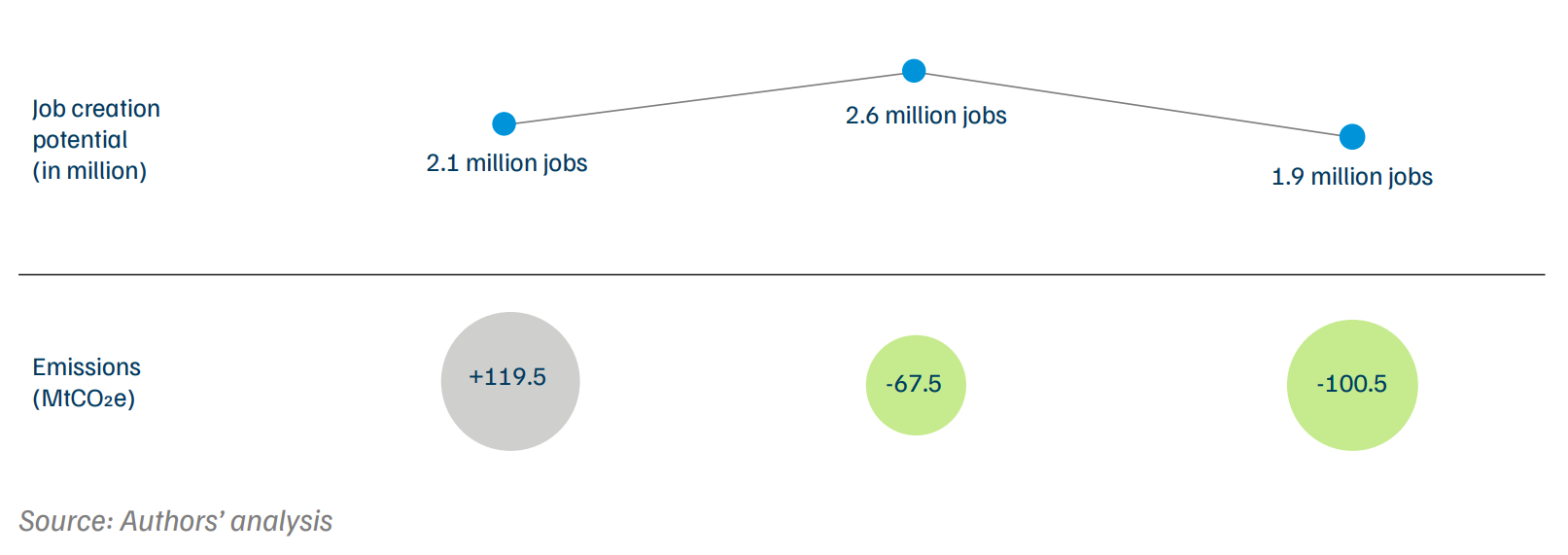

There are, essentially, three futures ahead of us.

We could stick to business as usual. We keep muddling along, get nowhere, and the sector stays a net emitter. If we aspire for more, though, we could move to an ambitious-but-balanced path: where we collect everything, treat almost all of it, and split it evenly between composting and biogas. And if we really get our stuff together, there’s a flat-out green path: we treat all our wet waste, and tilt the mix hard toward biomethanation — let’s say two-thirds gas, one-third compost.

The greener you go, the deeper the emissions cuts are, and the bigger the market becomes: from a $10 billion business at the bottom to over $60 billion at the top. Take those numbers as ballpark figures, not forecasts.

That said, a bigger market does not always translate into more jobs. If we stick to how we do things, our waste industry will employ 2.1 million people. A balanced path could lift that to 2.6 million. But the greenest, most ambitious path — the one that creates the biggest market and brings the deepest emissions cuts — only creates 1.9 million jobs.

That is, the most aggressive green scenario produces fewer jobs than doing nothing at all.

This is the central tension of the whole transition. It comes from a simple difference between the two technologies. Composting is labour intensive. It keeps people employed across thousands of small and mid-sized sites.

Biomethanation, on the other hand, is capital intensive. It needs sealed industrial plants with pumps, digesters and gas-cleaning units, all run by a small crew of technicians. It creates more value. It is also environmentally better; biogas can displace fossil fuel and chemical fertilisers more powerfully than compost alone. But every step in that direction replaces a crowd of low-skill compost workers for a handful of trained plant operators.

So India faces a genuine choice: do we want to give people employment in bulk, or do we choose a path that cuts the most carbon? You can’t have both. This is ultimately a political choice, not a technical one.

But who’s actually buying?

There’s another even more basic problem. That $50 billion “market” will only exist if there are buyers. And there’s a distortion that can keep them away. The two things this industry produces — manure and biogas — both must compete against products the government deliberately keeps cheap.

The manure that comes out of a composting plant, or the wet slurry left over from a biogas digester, is principally a direct substitute for chemical fertiliser. It can also rebuild the organic carbon that decades of urea have stripped out of India’s soil. But it comes at a price. Meanwhile, in 2025, the government spent over ₹1.7 lakh crore subsidising chemical fertilisers. A bag of urea is so cheap, and so familiar, that asking a farmer to buy heavy, bulky organic manure instead is like asking them to set their wallet on fire. After all, city compost has existed for decades; but most of it sits unsold.

This problem is why the government now pays ₹1,500 a tonne in “market development assistance” to help organic manure sold out of registered plants close the gap. Only, the subsidy on chemical fertilisers runs into tens of thousands of rupees a ton. In giving a smaller subsidy for a bulkier substitute, we might give it a gentle nudge, but we’re unlikely to genuinely shift a farmer’s choice.

Then, there’s the question of trust: as long as we struggle to cleanly segregate our waste, there’s no guarantee what people get. Compost made from mixed municipal waste, currently, can carry heavy metals or glass shards. A farmer who gets one bad batch won’t risk their livelihood on it again.

The report suggests testing as a possible fix: every batch of compost could be certified at an NABL-accredited lab before it’s sold. That’s the same level of national accreditation that backs medical and industrial testing. This is expensive and unglamorous, but without a credible quality stamp, “organic manure” is just a sack of unknown sludge, and no subsidy can fix that.

Fuel comes with a rhyming issue. Biogas could, in theory, insulate Indian households from the LPG import bill. India brings in about two-thirds of its cooking gas from abroad, leaving our poorest families exposed to global price spikes, like the one currently being pushed by the Hormuz crisis. For the moment, though, LPG cylinders are themselves subsidised, and the gas grid hasn’t reached most homes. That’s a hostile environment for biogas-for-cooking to reach the scale we need.

The entire “market” of its $50 billion rests on the bet that India will reform its fertiliser and fuel subsidies, so that alternatives have room to look more attractive.

Which brings us back to the rules

Notice that none of the hard parts, here, are technological. We know how to compost. We know how to build a biogas digester — Indore runs Asia’s largest plant of its kind. The technology has been proven to work.

What doesn’t work reliably is everything around it. We struggle to arrange for clean feedstock, sign workable contracts, or incentivise buyers to embrace their output. In other words, the barriers to this $50 billion market opportunity aren’t technological, but human.

This is why the new rules matter so much. It is also why they may not be enough.

The biggest bottleneck, here, is feedstock quality. A biomethanation plant fed mixed, contaminated waste can crash completely. These plants are biological; they rely on having the healthy bacteria of the right types. Upset or stress them, and the plants collapse. Composting is more forgiving, meanwhile, but contaminated compost is unsellable.

There’s only one answer: get clean, segregated wet waste in. If we fail that step, everything else fails. The SWM Rules 2026 are, fundamentally, the government’s attempt to legislate away the input problem — getting clean wet waste, separated at the source.

Clean feedstock, though, is only half the issue. The other half is how cities hire the people who run these plants. Most municipal tenders are still awarded on what’s called “L1” — where the lowest bid wins. On paper, this looks prudent. In practice, it’s a race to the bottom. Operators quote prices too thin to actually run a plant well, cash in on whatever subsidy comes with building it, and then let the facility limp or die. Worse, many contracts still pay operators by the tonne of waste they haul, not the quality of what comes out. They’re incentivised to mix in heavy rubble to bump up the weight of their intake, ruining the very feedstock the plant needs.

CEEW thinks L1 procurement should be replaced by QCBS — quality-and-cost-based selection — where a bidder’s track record and plant performance count for most of the score, with price only counting for the rest. It also suggests tying payments to output: clean compost and delivered gas, not tonnes trucked.

Sadly, experience teaches one not to be too hopeful. Rules requiring segregation have existed, in one form or another, since 2000. The reason Indore became a standout national success isn’t that it had better technology than anyone else. In the words of one expert CEEW interviewed, success stories like Indore tend to come down to “strong administrative leadership rather than widespread compliance.” A determined municipal commissioner actually went door-to-door until the city started segregating its waste.

But you can’t base an industry on the promise of determined civil servants.

Nothing about India’s wet waste problem is unsolvable. The only thing keeping us from a $50 billion industry is the least glamorous capability there is — of pushing people to get the basics right. That’s often the hardest thing to solve.

Tidbits

ARAI has rolled back a requirement that forced automakers to obtain separate domestic value addition (DVA) certificates for export models under the auto PLI scheme. If an export variant’s bill of materials is identical to the domestic version, the existing DVA certificate will now suffice — a relief for manufacturers who argued the extra paperwork added months of compliance burden.

Source: Business StandardIndia has added silver grains, powder, and other 99.9% purity forms to the restricted imports list, requiring prior authorisation from the DGFT. The move comes after silver imports hit a record $12 billion in FY26 — up from $4.8 billion the year before.

Source: Economic TimesPresident Trump signed an executive order creating a voluntary framework for the US government to review national security risks of advanced AI systems for up to 30 days before public release. Trump had delayed signing a similar order in May over concerns it could hamper America’s AI lead — the final version keeps participation optional and limits the review window, with the NSA director deciding which models qualify for scrutiny.

Source: Business Standard

- This edition of the newsletter was written by Manie and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Rosa & Tamoghna on India’s Youth Employment Crisis

In India, the more educated you are, the more likely you are to be unemployed. Graduate unemployment among the youth sits at 40%. For those with no education, it’s 3%. We recently spoke to Rosa Abraham and Dr. Tamoghna Halder, two of the authors behind the Azim Premji University’s State of Working India 2026 report, to understand why. Our conversation goes into what’s really driving this paradox — the role of caste and social signalling in education choices, whether waiting for a good job is rational, why the “missing middle” of Indian firms matters, and what the demographic dividend window really means for policy. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Very Good Read.

QCBS nice touch maybe next decade someone will come up with QECS, quality efficiency cost safety.

Bingo !!

Every genuine problem has a fix but without efficient administration and policies (largely through government and boards) all processes and technologies deliver zero net productivity on a scale.