India prepares to invest in US stocks

And the financial plumbing that enables it

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

So you want to invest in US stocks?

India’s big bet on rail freight

So you want to invest in US stocks?

Last week, the NSE International Exchange (NSE IX), the international arm of NSE based in GIFT City, launched a platform called Global Access. It lets Indians directly buy and sell US-listed stocks like Apple, Microsoft, and NVIDIA. It works under RBI’s Liberalised Remittance Scheme (LRS), wherein you can invest up to ₹2.3 crore per financial year. This limit is subject to change depending on the USD-INR rate.

But, you might ask, weren’t Indians already buying US stocks? Indeed, several Indian investing apps have offered this for service for a few years now. But the way it worked underneath was a little different.

These apps were essentially wrappers, while the actual trading was handled by relatively-unheard American firms like Viewtrade and Alpaca Securities. Most of these are API broker-dealers: they don’t have their own app, but provide the backend plumbing that others can use, i.e., connections to US markets, trade execution, and custody of shares.

So let’s say when you click “Buy Apple” on one of these apps, it calls ViewTrade’s system, and ViewTrade does the rest. Your money left India under LRS, landed with a US broker, and your shares were held in America. RBI watched the forex remittance. The US broker was regulated by the SEC. But no Indian securities regulator was in the middle of the chain.

That’s where the new Global Access Provider (GAP) framework, prescribed by IFSCA — the regulator for GIFT City — comes in. It now requires platforms offering international market access to operate under a regulated license within the IFSC. NSE IX has partnered with Viewtrade, the first firm to receive this license, to route orders to the US market. Now, your money goes to a designated bank account in GIFT City first. It gets converted to dollars there. You trade through NSE IX, to the US market.

So there’s now an Indian regulatory layer in the pipe that didn’t exist before. On the US side, your investments are covered by SIPC — the Securities Investor Protection Corporation — which protects up to $500,000 per customer if the US broker-dealer fails. Think of it as deposit insurance, but for your brokerage account.

And that’s the news. But the more interesting story, we think, is about what happens to your order once it actually reaches the US market.

How it works in India

Before we go into that, let us give you some context as to what happens in India first.

Let’s say that you buy a stock on Zerodha. Your order goes to our servers, where it’s checked for things like whether you have enough funds, and then to the exchange’s matching engine. An exchange like BSE or NSE maintains a central order book, containing every buy order and every sell order, listed by price and time. The engine matches buyers with sellers with the best price first; and if two orders are at the same price, the one that came in earlier gets priority.

Once a trade is matched, the exchange’s clearing corporation steps in. It inserts itself between buyer and seller, guaranteeing both sides of the deal. If one side defaults, the clearing corporation covers the other. One business day later (or T+1), the shares move to your demat account, and the money goes to the seller.

The detail worth noting here is that in India, every retail order goes to the exchange. Your broker cannot match your buy order with another customer’s sell order internally. The exchange is the market. This is called an order-driven system, and it’s one of the most transparent market structures in the world. There are nitty-gritty details that we aren’t getting into here, but broadly, this is how it works.

How it works in America

Now that we know how things work in India, let’s see how it works in the US.

See, US also has exchanges: NYSE, Nasdaq, and a few more. But when a retail investor buys, let’s say, Apple on Robinhood, the order rarely goes to an exchange. Where then does it go?

Here’s where things start to diverge. In India, your broker can only act as an agent — it takes your order and passes it to the exchange. That’s it. It cannot take the other side of your trade. It cannot match your buy order with another customer’s sell order internally. The exchange is the only legitimate place for trades.

In the US, though, brokers have a lot more flexibility. They’re either registered as broker-dealers, which means they can act as an agent (that can send your order to an exchange), or as a principal (that can take the other side of the trade themselves), or they can send it to a third party market-maker for execution. Most large US brokers, including Robinhood, Charles Schwab, and Interactive Brokers, are broker-dealers. And most of the time, for retail orders, they choose option three.

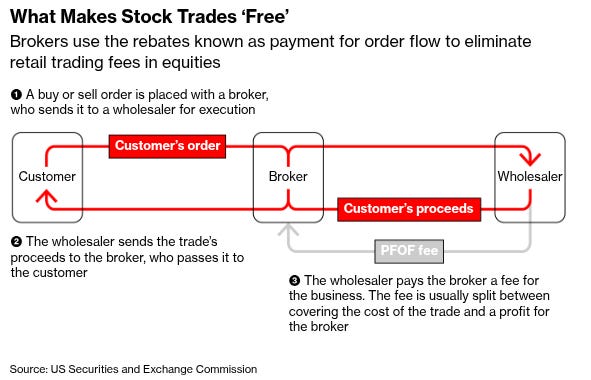

How does that work? Robinhood sends your order to a wholesale market maker, which can be a large trading firm like Citadel Securities. Then, Citadel takes the other side of the trade itself. If you are buying 10 shares of Apple, Citadel sells you those 10 shares from its own inventory. The trade happens inside Citadel’s private systems, not on any exchange.

But why would Citadel want to do this?

Remember, the US has a lot of exchanges. At any given moment, Apple might be trading at slightly different prices on each of them. To make sense of this, the SEC requires something called the NBBO, or the National Best Bid and Offer, which is the best available price at a given instant. Take the highest bid across all exchanges, and the lowest ask across all exchanges, and that’s your NBBO.

If, say, Apple’s bid is $230.00 and its ask is $230.02, there’s a two-cent gap. That gap is the spread. Market makers live in this gap. They buy at the bid, sell at the ask, and pocket the difference. The difference may be small, but do it millions of times a day, across many stocks, in huge quantities, and it can add up to billions.

But the real reason Citadel wants retail orders specifically is that they’re almost risk-free to trade against. When a hedge fund’s algorithm sells Apple aggressively, that’s a signal that it might know something crucial. Taking the other side of that trade is dangerous. But when a regular person buys 10 shares because they like the company, that trade carries no information. The price isn’t going to move because of it. Retail orders are small, relatively more uninformed, and predictable. For a market maker though, that’s the ideal counterparty.

So here’s the deal that’s evolved. Citadel pays Robinhood for the privilege of trading against Robinhood’s customers. This is called Payment for Order Flow, or PFOF. In return, Citadel fills your order at a slightly better price than what’s on the exchange. You pay zero commissions and get a tiny price improvement. Robinhood gets paid by Citadel, and Citadel earns the spread on millions of low-risk trades.

Everyone seems to win. But critics, including former SEC Chair Gary Gensler, have argued this creates a conflict of interest. The broker is supposed to find the best deal for you. But the broker is also getting paid by the market maker. What if a better deal exists somewhere else, but the broker doesn’t look because the current arrangement is lucrative enough?

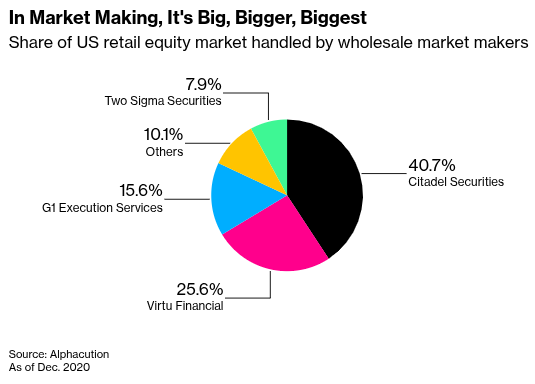

There’s a bigger structural concern, too. The top three wholesalers handle over 80% of US retail equity orders. Nearly half of all US equity trading now happens off-exchange.

The exchanges are supposed to be where prices get discovered and the “true“ value of a stock emerges. But if fewer and fewer trades happen there, that price signal weakens. The SEC proposed reforms in 2022 to push more retail orders back to exchanges, but those reforms were withdrawn in 2025.

In fact, this is the same plumbing that blew up during the GameStop saga in 2021. Millions of retail traders piled into the GameStop stock through Robinhood and overwhelmed the clearing system. Robinhood had to stop people from buying more.

India has none of this — no PFOF, no internalization and no off-exchange retail execution. Everything goes to the exchange.

So, what changes for you?

For the average Indian retail investor, not a lot changes.

The underlying market structure in the US — wholesalers, market makers, payment for order flow — doesn’t disappear just because the order passes through GIFT City first. Once your trade reaches the US, it enters the same ecosystem we just described.

You still remit money under LRS. You still face currency risk — if the rupee weakens or strengthens against the dollar, your returns move accordingly. And US taxes and Indian capital gains rules continue to apply the way they always have.

What changes is the route your money takes. Earlier, your app plugged directly into a US broker-dealer, and your regulatory touchpoints were split — RBI for the remittance, the SEC for the broker. Now, there’s an Indian regulatory layer in between. Your trade flows through GIFT City, under the supervision of IFSCA. That’s a structural improvement, even if it doesn’t change what you see on screen.

This GAP framework is also the route we’re taking to bring US stock investing to Zerodha. We’re working on it, and you’ll hear from us soon.

But regardless of which platform you use, if you’re investing in US stocks or thinking about it, it’s worth understanding the world your money enters once it crosses the border. It looks nothing like what you’re used to at home.

India’s big bet on rail freight

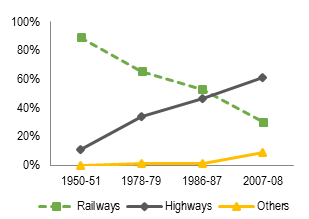

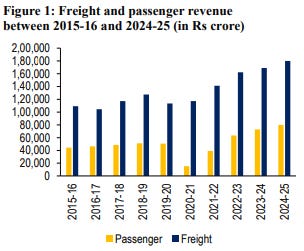

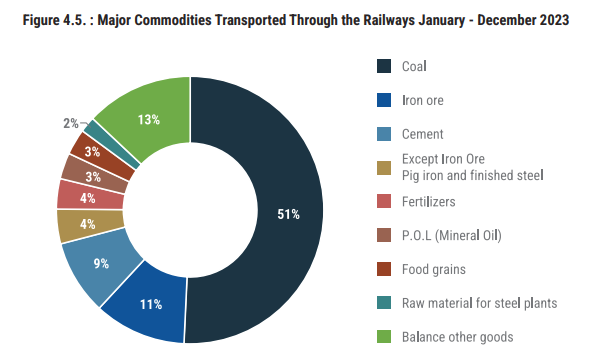

In 1950-51, Indian Railways carried almost 89% of the country’s freight. But today, that share has dwindled down significantly to 18%. Roads, meanwhile, carry 71% of India’s freight today.

This change of fortunes isn’t because rail is bad at moving goods, though. Moving freight by rail costs about ₹1.96 per tonne-kilometre — roughly half of what road transport costs. By that logic, rail should certainly be winning.

But over seven decades, as both passenger and freight demand surged on the same tracks, freight kept getting pushed aside. The network was never redesigned to handle both at scale, and whenever there was a conflict, passengers always won.

India’s logistics costs were long estimated at 13-14% of GDP; however, a recent study revised that down to about 8% of GDP. Even that number doesn’t capture how inefficiently goods actually move across the country. And the gap between rail’s cost advantage on paper and its inability to capture freight in practice is a big part of the problem.

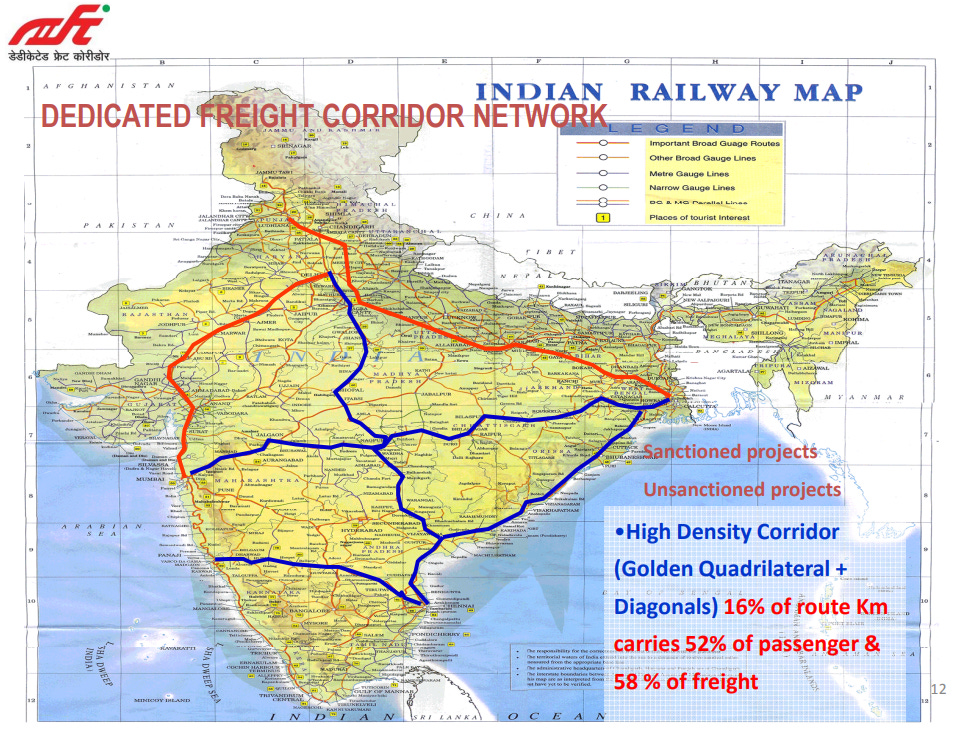

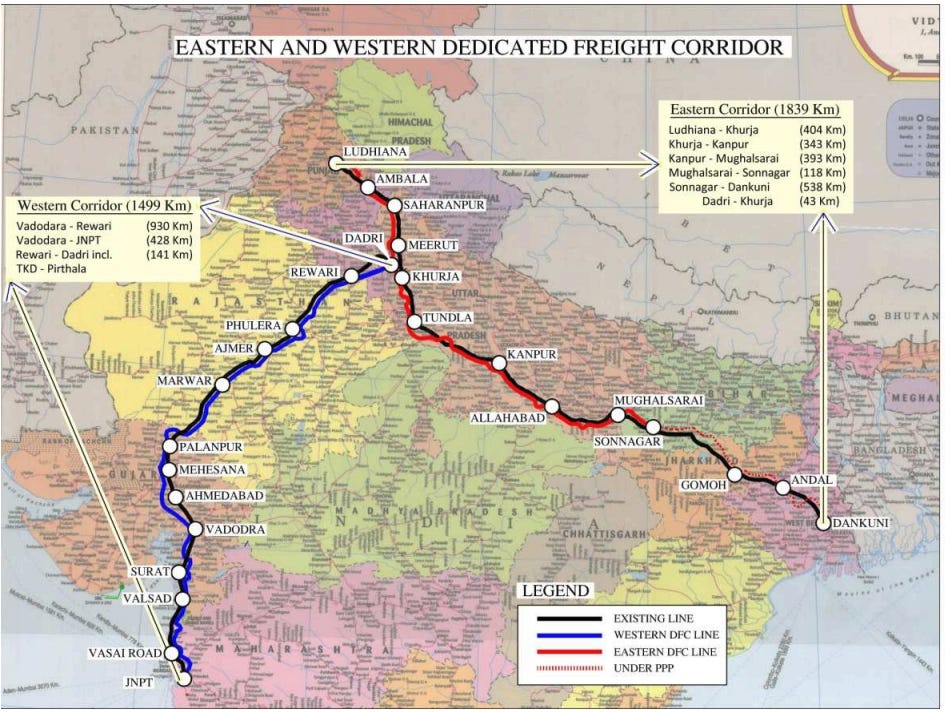

Now, that’s beginning to change. India’s two Dedicated Freight Corridors — the Eastern DFC running from Ludhiana to Sonnagar, and the Western DFC from Jawaharlal Nehru Port Trust (JNPT) near Mumbai to Dadri near Delhi — are now 96.4% operational. Together, they span ~2,843 km — the single biggest bet Indian Railways has made on freight, designed to just move goods more efficiently without competing with passenger trains for space.

This is the story of how Indian freight fell behind, and what these corridors are trying to fix.

Why freight fell behind

Most of India’s rail network runs on what’s called “mixed traffic“ — where passenger and freight trains share the same tracks and the same signals. And when there’s a conflict, the passenger train always gets priority.

In practice, it means freight trains spend a staggering amount of time simply waiting. They’re pulled into loops, which are short tracks that branch off the main line so another train can pass. They’re held at signals, parked in yards while express and mail trains go by.

As a result, Indian rail freight has always been structurally slow. In 2023-24, the average speed of a goods train across the broad gauge network was merely 25 km per hour. That’s barely faster than city traffic.

This bottleneck was concentrated in a few critical routes. India’s “Golden Quadrilateral“ corridor, which connects Delhi, Mumbai, Chennai, and Kolkata, carries 52% of all passenger traffic and 58% of all freight traffic — despite only making 16% of India’s network. The Delhi-Mumbai and Delhi-Kolkata legs, in particular, were highly saturated. Every year, more passenger trains were squeezed onto the same tracks, leaving freight with scraps.

But speed wasn’t the only problem. For decades, capital investment in the railways prioritised making upgrades in passenger capacity. Freight infrastructure, particularly modern terminals and container handling, received far less attention. While the world moved from packing goods to putting them in standardized metal containers that move seamlessly between ships and trains, Indian rail was late to this shift.

There was also a pricing distortion baked into the system. Passenger fares in India have long been kept artificially low, well below the cost of actually running those services. This is cross-subsidized by over-charging freight customers — like steel companies, coal plants, and so on. To some degree, this policy shrank the cost advantage that rail freight enjoyed. And once you added in the speed, reliability, and door-to-door convenience that road offered, shippers preferred trucks more than rail.

What the DFC actually changes

That’s where the Dedicated Freight Corridors (or DFCs) enter the picture.

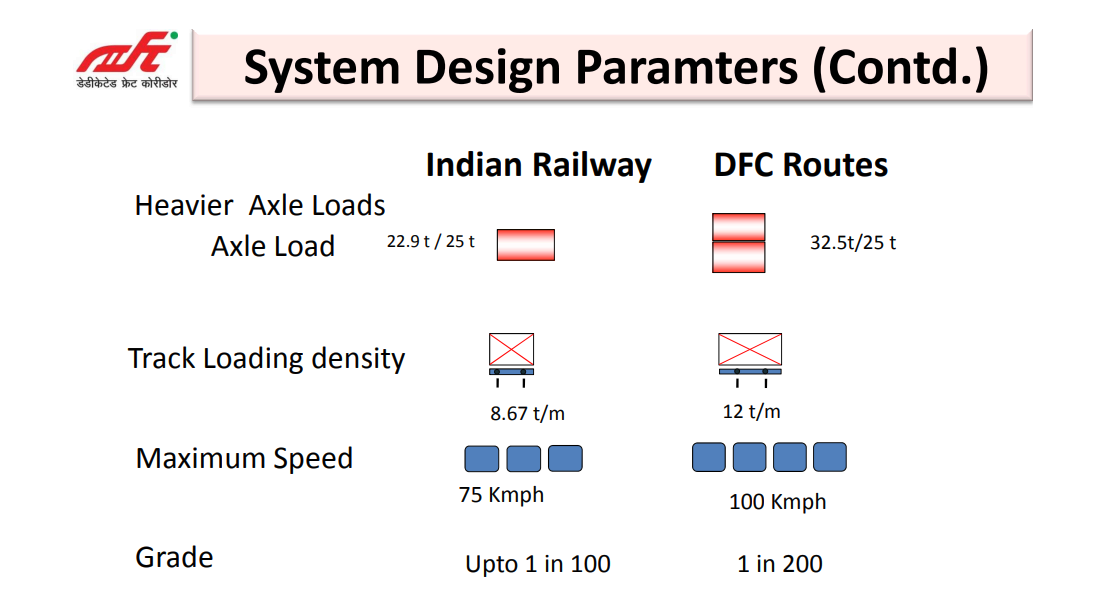

DFCs would contain separate tracks exclusively for freight trains so they no longer compete with passenger traffic for space. But separate tracks aren’t the only sweetener the DFCs offer. Under the program, three fundamental upgrades in engineering standards for freight rail have been made.

The first major upgrade is around the axle load. It refers to the weight pressing down on the track through a single axle of a wagon. The conventional network was designed for axle loads of 20–23 tonnes. The DFCs, in contrast, are built for 25 tonnes, with infrastructure designed to eventually support 32.5 tonnes. Heavier axle loads mean each wagon can carry more, which means fewer wagons per shipment, and therefore lower cost per tonne.

The second upgrade is related to speed. The DFCs are designed for trains running at up to 100 km/h — far higher than the 25 km/h average on standard rail. A typical 613-kilometre freight journey at legacy speeds might take about 24.5 hours one way. But at DFC speeds, that same journey should take half the time. Wagons that previously completed a round trip in about five days might do it in two or three.

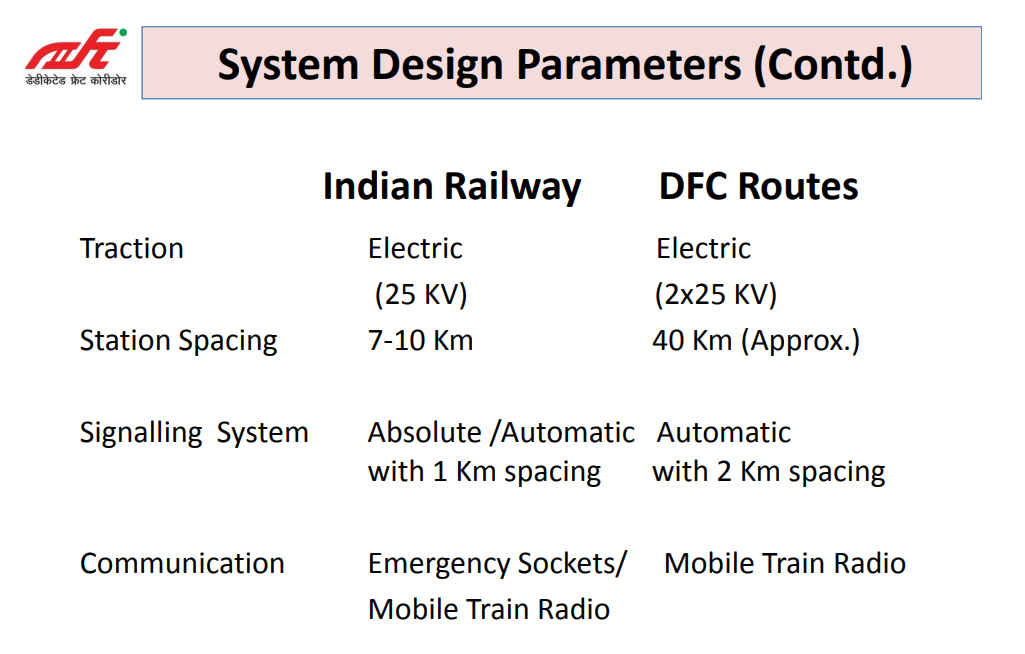

Lastly, signalling. The DFCs use automatic signalling with 2-km block spacing — the track is divided into short segments, each controlled by its own signal, allowing trains to follow each other at much closer intervals. That means more trains per hour on the same stretch.

There are two DFCs that are fully operational today. The Western DFC was designed primarily for container traffic, connecting ports in Western states like Gujarat and Maharashtra to north India. The Eastern DFC handles mostly commodities like coal, minerals, fertilisers connecting eastern India’s mining belt to the rest of India. Between them, the two corridors cover the most congested and economically critical freight routes in the country.

So far, the DFCs seem to have been effective. In FY24, DFC operations averaged 241 trains per day, and by February 2025, that had climbed to 371 trains per day. The Eastern corridor runs on an average speed of 46 km/h, while the Western DFC runs on 55 km/h — a much-needed step-up from 25 km/h.

More importantly, the DFCs free up capacity on the conventional network. When freight trains no longer clog the Delhi-Mumbai or Delhi-Kolkata mainlines, those paths become available for more passenger trains. They provide an urgent, long-term relief to an otherwise-bottlenecked system.

Future plans

Now, 96.4% commissioning sounds nearly complete, but the significance of the remaining few percent isn’t well-reflected in just the number.

The Western DFC’s final stretch — a 102-km segment from Vaitarna to JNPT, India’s largest container port — is still being completed. Track laying is largely done, electric locomotive trials have commenced, full commissioning is targeted by March 2026. But, until that last leg is active, the Western corridor can’t meet its full potential.

Freight companies in the private sector are watching closely at this development. Take, for instance, the Container Corporation of India (CONCOR), which is India’s largest rail container operator. On their recent earnings call, they mentioned how the completion of this final stretch would create a rare “pure DFC“ circuit which, in a rare instance, would have no passenger trains at all. Over the next three years, CONCOR projects 15% annual growth in their export-import business, with the JNPT connection being a key part of that.

The government has also been building out the supporting infrastructure. As of early 2026, the Gati Shakti Cargo Terminal programme has approved 306 new terminals, of which 118 are already operational. This matters because rail’s cost advantage is measured terminal-to-terminal.

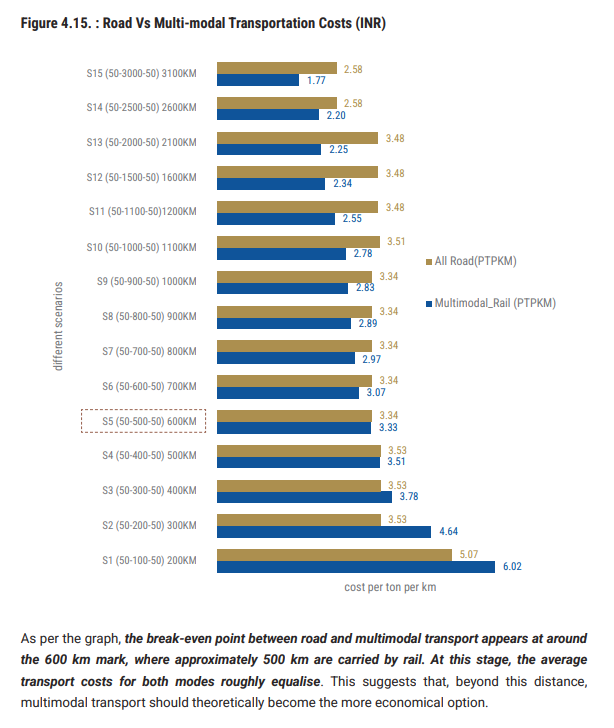

The first and last mile of delivery — getting goods from a factory to the rail terminal and from the destination terminal to the warehouse — is still done by road. If that stretch is long or inefficient, it can erase rail’s cost edge entirely. A government study found that rail only beats road on cost once the main journey exceeds ~600 km, and that assumes the first and last miles are short, around 50 km each. Terminals are what convert a fast corridor into an actually competitive logistics option.

There are also plans for more corridors. Detailed project reports are under examination for an East Coast corridor from Kharagpur to Vijayawada, an East-West corridor, and a North-South sub-corridor. None are sanctioned yet, but they signal that the DFC model will eventually extend beyond the Golden Quadrilateral.

Conclusion

The DFCs are the clearest bet India has placed on reversing seven decades of freight share erosion. The capex has been enormous — nearly ₹1 lakh crore so far. But the corridors alone won’t be enough.

The binding constraint now is the ecosystem around them. For instance, terminals need to be operational and mechanised, first-and-last-mile connectivity has to improve, and the freight mix needs to diversify beyond coal into containers, automobiles, and other categories where road currently dominates. Road freight doesn’t stand still either, as trucking is getting more efficient and highways are improving.

If DFC’s work, they’ll lower the cost of moving things across India by, well, quite a mile.

Tidbits

Canada’s Cameco signs $1.9 billion uranium deal with India

Canadian uranium giant Cameco has signed a $1.9 billion supply deal with India to provide 22 million pounds of uranium from 2027 to 2035. The agreement supports India’s plan to sharply expand nuclear power capacity to 100 GW by 2047. It also signals improving India–Canada ties after recent diplomatic tensions.

Source: BloombergTata Steel to invest ₹11,000 crore in Jharkhand

Tata Steel will invest ₹11,000 crore at its Jamshedpur plant to develop advanced low-carbon “green steel” technology. The move aims to produce higher-grade steel while reducing emissions. Tata Motors also plans to invest in hydrogen-powered trucks at the same facility.

Source: ThePrintSEBI fines Coffee Day Enterprises ₹38 lakh

SEBI has imposed a ₹38 lakh penalty on Coffee Day Enterprises for financial misstatements and disclosure lapses. The action follows a probe into inaccuracies in the company’s financial reporting. The debt-laden firm, which runs Café Coffee Day, is already undergoing insolvency proceedings.

Source: ET Now

- This edition of the newsletter was written by Krishna (co-written with Faisal and Somnath) and Vignesh.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Fascinating breakdown. Many Indian investors assume global investing works just like our markets, but the US market structure is completely different. India’s exchange-driven system is actually far more transparent than most people realise. The new GIFT City layer at least adds some regulatory comfort for investors.

Excellent depth and explanation