India leaps to split the atom

with a reactor the world mostly abandoned

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

India leaps to split the atom

The imbalances that make up world trade

India leaps to split the atom

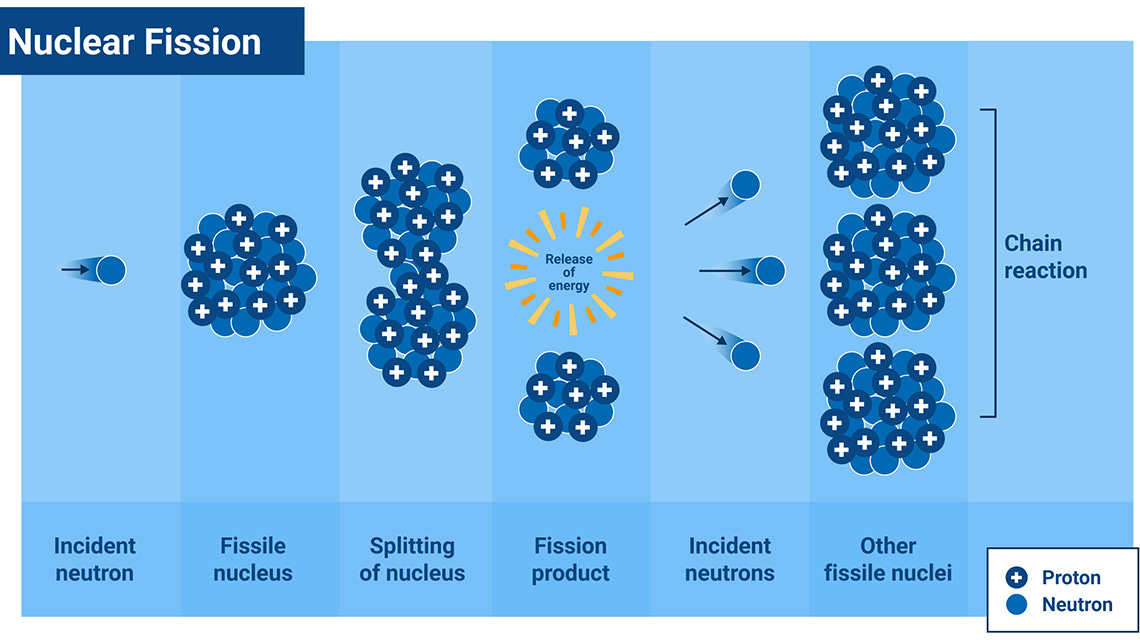

Everything in the universe is made of atoms. An atom has a core called a nucleus, built from smaller particles: protons and neutrons. In most elements, the nucleus holds together just fine. But in very heavy elements like uranium, it’s so packed that it’s barely stable. Fire a neutron at it and the nucleus can split apart. This is nuclear fission.

When a uranium atom splits, two things happen. It releases a huge amount of energy as heat, millions of times more, atom for atom, than burning coal. And the splitting nucleus flings out two or three spare neutrons, which fly off and hit other uranium atoms, splitting them too, releasing more energy and more neutrons.

This is a chain reaction. If it keeps going on its own, without outside help, the reactor has achieved what physicists call criticality.

On Sunday 9th April, inside a reactor hall on the coast of Tamil Nadu, the Prototype Fast Breeder Reactor (PFBR) went critical.

This is a big deal. The fast breeder is the hardest type of nuclear reactor to build and operate. The United States spent decades on the technology and gave up. France built the most ambitious one ever attempted and abandoned it. The UK, Germany, Japan, Italy: all walked away after sinking billions. Only Russia has kept one running for any sustained period.

India has now become the second country to bring a commercial-scale fast breeder to criticality, and once the PFBR is fully operational, it will be only the second in the world to generate electricity from one.

Understanding why India pursued this technology when everyone else quit requires going back to the 1950s, to a physicist who looked at a geological map and saw a problem that would shape the country’s energy policy for seven decades.

Uranium and its isotopes

But before that, let’s briefly dive into how nuclear reactors work.

Most nuclear reactors run on uranium. You put uranium fuel in a reactor, the chain reaction produces enormous heat, the heat boils water into steam, the steam spins a turbine, and the turbine generates electricity. Conceptually, it’s not that different from a coal plant — except a kilogram of uranium contains roughly two million times more energy than a kilogram of coal.

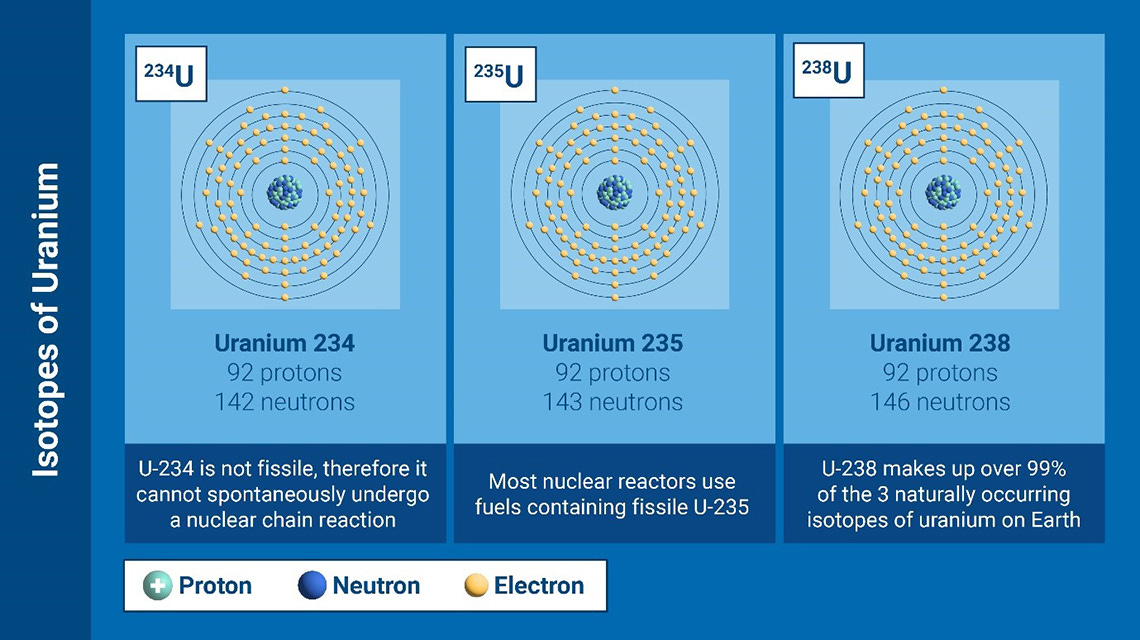

But not all uranium is equal. It comes in two forms, called isotopes. Think of them as siblings: same element, slightly different weight. Uranium-235 has 235 particles in its nucleus, uranium-238 has 238.

That small difference changes everything. Uranium-235 is unstable enough that a neutron can split it easily, releasing energy and more neutrons to keep the chain going. It’s what reactors need. But it makes up less than 1% of natural uranium. The other 99% percent is uranium-238, which is far more stable. It doesn’t split when you hit it with a neutron, rendering it fairly useless for a conventional reactor.

India holds about 3% of the world’s known uranium reserves. If it had copied the nuclear playbook of the US or France, it would have built reactors it couldn’t fuel without importing uranium forever. Which is essentially the situation today: India imports over 70 percent of its uranium, mostly from Kazakhstan and Russia.

But India has something else. The monazite sands along the coasts of Kerala and Odisha are rich in thorium. India holds ~25 percent of the world’s known thorium reserves — enough, by some estimates, to generate 500 GW of electricity for four hundred years.

However, thorium doesn’t work like uranium-235. You can’t put it in a reactor and split it. When you fire a neutron at thorium, it absorbs the neutron, and then, over a few weeks of radioactive transformations, it turns into a completely different element: uranium-233. And uranium-233 does split, making it excellent reactor fuel.

But you need a working reactor to perform this conversion in the first place. You can’t start with thorium. You have to work your way there. At least, that’s what Homi Bhabha did.

The Three Stage Nuclear Programme

Homi Bhabha, the physicist who founded India’s atomic energy programme, saw this in the 1950s. He designed a three-stage nuclear programme, a relay race where each generation of reactors produces the starting material for the next.

In the first stage, natural uranium is burned in conventional reactors. While the reactor runs, some uranium-238 in the fuel absorbs stray neutrons and slowly transforms into plutonium, a man-made element that, like uranium-235, can be split to produce energy. India has been running stage 1 reactors for decades.

The second stage uses that plutonium in a fast breeder reactor, which is the core of our story. This reactor does something no conventional reactor can — it produces more fuel than it consumes. And it can convert thorium into uranium-233.

Then, in the final stage, thorium reactors running on uranium-233 are built. India is less dependent on uranium imports as a result. It’s running on fuel made from its own beaches.

However, each stage feeds the next. Not a single one of them can be skipped. And we are now at Stage 2.

Science non-fiction

A reactor that produces more fuel than it burns sounds almost out of science fiction. The magic trick is in what happens to the spare neutrons.

See, when a uranium atom splits, it releases two or three neutrons. Only one is needed to split the next atom and keep the chain reaction going, while the rest are surplus. In a conventional reactor, those surplus neutrons go to waste.

However, a fast breeder puts them to work. The reactor core is surrounded by a “blanket” of uranium-238. Surplus neutrons fly into this blanket, get absorbed by uranium-238 atoms, and convert them into plutonium fuel. If designed well, the blanket creates more new fuel than the core burns. Load thorium into the blanket instead, and the surplus neutrons convert it into uranium-233.

But this trick only works with fast neutrons, the high-energy kind that come straight out of a fission reaction. And this is where the engineering nightmare begins.

In conventional reactors, the coolant is water. Water carries heat away from the core, but it also slows neutrons down. Think of it this way: when a neutron hits a water molecule, it’s like a billiard ball hitting another ball of similar weight, transferring energy. In a conventional reactor, this is useful, because slow neutrons are actually better at splitting uranium-235.

But in a breeder, slow neutrons can’t convert uranium-238 or thorium into new fuel efficiently. The breeding ratio collapses. You need the neutrons fast. So you need a coolant that carries heat without slowing them down.

The answer to that conundrum is liquid sodium. When a neutron hits a sodium atom, it’s like a billiard ball hitting a bowling ball. The neutron bounces off without losing much speed. Sodium also transfers heat brilliantly and operates at low pressure. The PFBR circulates 1,750 tonnes of it.

But sodium is not an easy element to handle. It is one of the most reactive elements on Earth. It reacts and starts exploding when it comes to contact with water or even air. Now imagine 1,750 tonnes of it circulating inside a reactor that also needs water to generate steam. The sodium and water are separated by thin metal walls in the steam generators. If a wall cracks, they meet.

To buffer this, breeders add an intermediate sodium loop: radioactive sodium from the core transfers heat to a second circuit of clean sodium, which then heats the steam generators. It’s a safety layer, but it also means more plumbing, more welds, and more places for sodium to leak into the air and catch fire.

This is the reason most fast breeder reactors ever built were abandoned.

Failures all across the world

Take, for instance, France’s Superphénix, the world’s first commercial-scale breeder. It went critical in 1986, but was fully abandoned in 1998. In that span, it spent more than half the time being shut down.

Japan’s Monju, meanwhile, reached criticality in 1994, but shut down 14 months later after a sodium leak caused a fire. It didn’t restart for fifteen years, and when it did, it shut down again after 3 months when refueling equipment collapsed into the reactor vessel. In the 2 decades of its existence, it was only truly operational for 250 days, while costing ~$12 billion.

Germany’s Kalkar breeder was never commissioned. The site is now an amusement park. Russia’s BN-600, the world’s longest-running breeder, kept going, but only because its operators tolerated conditions that would have shut reactors elsewhere, suffering 27 sodium leaks and 14 sodium fires between 1980 and 1997 alone.

Nuclear physicist Thomas Cochran summarised the record: fast reactor programmes had failed in the US, France, the UK, Germany, Japan, Italy, the Soviet Union, the US Navy, and the Soviet Navy. Globally, an estimated $100 billion had been spent.

What next?

The Indian PFBR’s own history fits the pattern of delays, if not outright disaster. Construction began in 2004, with a completion target of 2010. That was missed and pushed to 2013-14. Yet again, the new target was missed. From then on, the Department of Atomic Energy announced “next year” every year. Costs more than doubled from the original ₹3,500 crore budget to nearly ₹8,200 crore.

The final stretch raised questions. In March 2024, Prime Minister Modi visited Kalpakkam and announced that fuel loading had begun. But the Atomic Energy Regulatory Board hadn’t yet given clearance — that only came four months later. Full fuel loading started in October 2025. Criticality came on April 6, 2026, 22 years after construction began.

Criticality means the chain reaction sustains itself. It does not mean the reactor is generating electricity. The PFBR must still complete low-power experiments, secure further AERB approvals, connect to the grid, and demonstrate sustained commercial operation. This is the stretch where Superphénix and Monju fell apart.

Today, nuclear power is 3% of India’s electricity. The PFBR adds 0.5 GW, which is about the same as one large coal plant. The target is 100 GW by 2047, a twelve-fold increase.

More breeders are planned at Kalpakkam, but construction hasn’t started. The SHANTI Act, passed in December 2025, opened nuclear to private companies for the first time. But current policy discussions have focused on conventional and imported reactor designs, rather than fast breeders. The breeder programme remains under the Department of Atomic Energy, running on its own timeline.

Meanwhile, China is approaching the thorium problem from a different direction entirely. In 2025, it built the world’s first experimental thorium molten-salt reactor, using molten fluoride salts instead of sodium. If that approach works at scale, China could reach the thorium endgame faster and without the sodium risk that has wrecked breeder programmes worldwide.

There’s no way to tell whether Homi Bhabha’s bet would ever pan out. But for a dream that was riddled by failures even in the richest of countries, India’s achievement is certainly a worthwhile inflection point for nuclear energy.

The imbalances that make up world trade

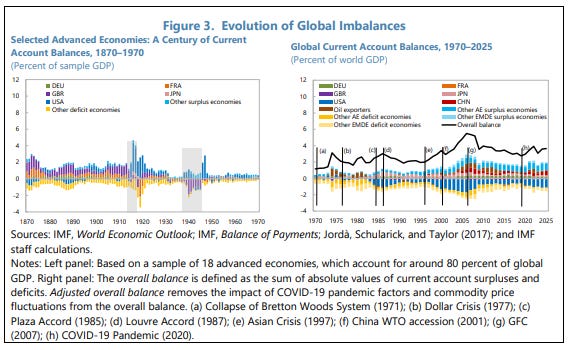

Global imbalances had been healing, slowly but steadily, for most of the decade after the 2008 financial crisis. Then they started widening again.

Some countries consistently spend more than they earn. Others consistently earn more than they spend. The gaps that result — surpluses and deficits flowing across borders in the form of capital, goods, and services — are as old as modern trade. The position of various countries maintaining surpluses or running deficits has always changed.

In and of itself, a surplus or deficit isn’t bad. But what’s unusual about the present moment is the scale and the persistence. The US now runs a current account deficit worth ~4% of its GDP. The US, China, Germany, and Japan together account for about two-thirds of all global imbalances. And these positions have become stickier over time: the average duration of a surplus or deficit spell has roughly doubled since the 1980s.

Against this backdrop, the IMF published a policy paper recently. It attempts to dive into the core of what drives global imbalances and what kinds of policies can actually resolve them.

A useful way to think about it

To understand what drives imbalances, economists typically start with a simple accounting identity: a country’s current account balance equals its national saving minus its domestic investment. We won’t get into the math of it, but we’ll try and explain what it means intuitively.

Say a country imports more than exports goods. How does it finance those net imports? It could either borrow from abroad, attract foreign investment, or sell assets. In effect, capital inflows, or investments, increase relative to savings.

Similarly, if you have an export surplus, what do you do with the money you have? You’re more likely to save it, lend it to others, or invest elsewhere. Your own economy might not be able to absorb all of it — meaning that savings is relatively higher than investment.

Through this lens, Japan’s persistent export surplus reflects high corporate savings with subdued domestic investment in comparison. Meanwhile, the US runs the world’s largest trade deficit, reflecting household dissaving and strong investment demand.

Essentially, the current account and capital account are mirror images of each other. And trade in goods and services is the biggest driver of current account balances.

If a country imports more than it exports, the difference ideally has to be financed by capital coming in from abroad — and vice versa. Causation can therefore run in both directions. American dissaving widens the US deficit, but so does a surge of foreign capital seeking dollar assets. The US runs a persistent deficit partly because the rest of the world wants to hold dollars.

The IMF’s saving-investment frame is useful because it shows how domestic investment policies shape the world economy. But it’s not the only lens. At the end of the day, this equation is an accounting identity, and doesn’t always have to reflect the primary cause of massive trade imbalances — those can exist for other reasons, too.

Why this matters

The problem with large imbalances is what happens when they unwind.

An orderly unwinding is manageable: saving and investment gradually shift, relative prices adjust, and the global economy absorbs the change without drama. A disorderly unwinding is something else entirely. That looks like abrupt capital flow reversals, sharp asset price corrections, and deep recessions.

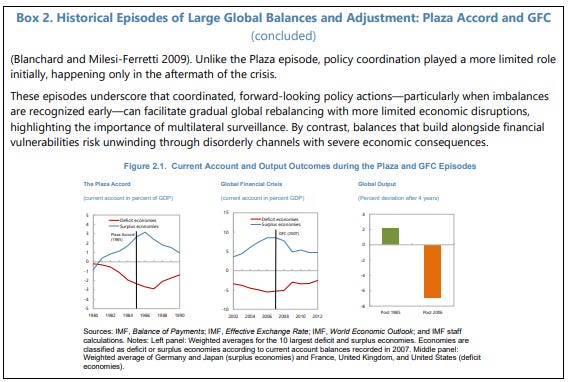

The 2008 financial crisis is the clearest example: imbalances that had built up alongside financial vulnerabilities unravelled violently, with no coordinated policy response until the damage was already done.

Countries running large deficits are particularly exposed. They depend on continuous capital inflows to finance the gap between what they earn and what they spend. When global financial conditions tighten — or investors reassess their pockets — they can face a sudden stop: rising borrowing costs, exchange rate volatility, and a sharp compression in domestic demand.

Surplus countries may look safer from the outside but create their own distortions. The excess savings they channel abroad push down global interest rates, which can encourage excessive risk-taking and leverage in recipient economies.

And crucially, surplus countries face little market-driven pressure to adjust. After all, they’re net lenders to the world. But markets will eventually discipline a country that borrows too much. This structural asymmetry was flagged all the way back in 1943 by economist John Maynard Keynes.

There is also a political economy dimension. Even when trade increases aggregate incomes, the gains are diffuse and the losses are concentrated — specific regions, specific industries, specific workers. That concentration fuels protectionist sentiment, which produces tariff escalation, which tends to reduce output without correcting the underlying imbalance. This is a trap that the current moment seems particularly prone to walking into.

Not all imbalances are cause for alarm, though. A developing economy running a deficit to finance productive investment may be behaving rationally. The concern is specifically about imbalances driven by policy distortions, that persist beyond what fundamentals justify, and that accumulate alongside financial vulnerabilities.

What’s driving the current widening

The recent widening reflects a striking pattern: the US and China, the two largest contributors to global imbalances, are moving in opposite directions.

In the US, the post-pandemic period has produced a near-perfect storm of current-account-widening forces. Household saving rates have fallen sharply. Fiscal deficits have expanded significantly. Business investment has surged, partly on the back of AI-driven spending. Each of these, through the saving-investment lens, pushes the deficit wider. All the while, they’ve still been running a wide trade deficit.

On the flip side, you have China, the world’s largest exporter. It generates more than it consumes. Its industrial policy has tilted the economy further toward exports, channeling government support to export-oriented sectors while reducing transfers to households. The excess flows abroad to investments — in fact, China is one of the biggest holders of US treasuries.

Additionally, the collapse of the real estate sector has crushed domestic demand. Households, uncertain about the future, have responded by saving more. The excess flowing abroad as a current account surplus.

Demographics compound all of this. Ageing populations in Germany, Japan, and China structurally raise saving rates. After all, as workers approach retirement, they accumulate wealth, and the pension systems in these economies don’t fully cover the gap. This isn’t a cyclical force that reverses when conditions improve — it’s structural, and it runs in the same direction as the cyclical forces currently widening imbalances.

The IMF estimates that forces of this kind — fiscal, cyclical, structural — explain roughly half of the post-pandemic widening in the US and China’s current account balances. The other half is harder to attribute cleanly to any single cause. But the broader point stands: the drivers of the current widening are overwhelmingly domestic.

Which raises the natural question — if that’s what’s producing the imbalances, what can policy actually do to correct them?

What policy can and cannot do

On that note, the IMF paper explores three policy levers most commonly proposed — tariffs, sector-level industrial policy, and economy-wide interventions. Each has distinct effects on the current account, and the results are often counterintuitive.

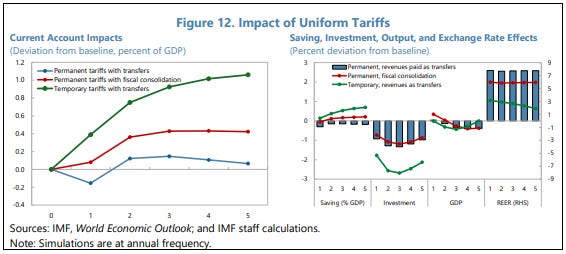

Tariffs

Start with tariffs. The intuition behind using them to fix a trade deficit seems straightforward: tax imports, buy fewer of them, and the deficit shrinks. In practice, though, permanent tariffs are broadly neutral on the current account.

The mechanism runs through the exchange rate. When a country imposes tariffs, demand for imports falls. But this also reduces the supply of the country’s currency in foreign exchange markets, causing it to appreciate. That appreciation makes exports more expensive and imports cheaper, offsetting the original effect. Hence, the current account ends up roughly where it started.

Retaliation compounds the problem. For instance, around 73% of US tariffs on China are met with retaliatory measures within 12 months; around 61% of EU tariffs on the US face the same response. When tariffs are reciprocated, they stop behaving like country-specific interventions and start behaving like global shocks — dampening the already-limited current account effect while reducing output on both sides.

Industrial policy

Sector-level industrial policy — which includes production subsidies and directed credit — has similarly ambiguous effects. The outcome depends on whether the policy raises or lowers aggregate productivity.

Effective industrial policy boosts incomes, which leads households to spend more and save less. With higher incomes, people import more, which worsens the current account of the implementing country. Misallocated policy, where support is directed to sectors without genuine competitive advantage, depresses productivity and raises precautionary saving. Weirdly, that would improve the current account.

The clearest path from policy to current account runs through what the IMF calls “macro industrial policy“. This refers to economy-wide interventions that aren’t just limited to subsidies and cheap credit, but also foreign exchange management and financial repression.

This is, in essence, China’s approach. The People’s Bank of China has for decades accumulated foreign exchange reserves on a large scale, preventing the renminbi from appreciating and sustaining the competitiveness of Chinese exports. Capital controls prevent Chinese households from moving savings abroad. A thin social safety net and restrictions on consumer borrowing suppress domestic consumption and force saving. State-controlled interest rates channel savings toward investment in priority sectors rather than household spending.

The combination works. China holds one of the largest net foreign asset positions globally — the accumulated result of two decades of this approach. But the consumption levels of Chinese households are lower than they would otherwise be.

The collective action problem

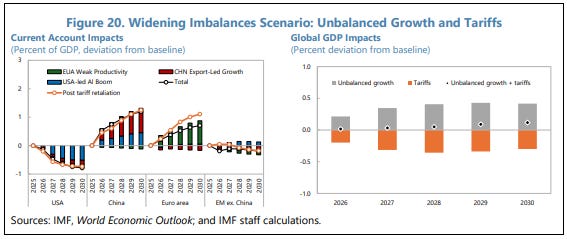

Given what actually drives imbalances, the solution has to be domestic and macroeconomic. The IMF modelled what two different paths forward might look like.

In the first, current trends continue and tariffs escalate: the US maintains large fiscal deficits, China doubles down on export-led growth, and all three major blocs raise tariffs by 20 percentage points. The result is a modest reduction in global output and almost no change in current account balances. Tariff escalation, even aggressive tariff escalation, barely moves the underlying imbalances.

In the second, the major economies reform simultaneously. The US moves toward fiscal consolidation and rolls back tariffs. China expands social spending, reduces industrial policy distortions, and allows the yuan to adjust. Europe boosts public and private investment and raises productivity.

The result is the opposite: current account imbalances narrow meaningfully — China’s surplus falls by over a percentage point of GDP, the US deficit improves — and global GDP rises in all three regions. Countries that move together do substantially better than countries that move unilaterally, because the reforms in one economy amplify the effects of reforms elsewhere.

The reason this is hard is structural. Market discipline eventually forces deficit countries to adjust — rising borrowing costs and, in the limit, a hard stop. Surplus countries face no equivalent pressure. There is no market mechanism that compels, say, Germany to spend more or China to consume more. The adjustment burden falls asymmetrically on the deficit side, which means surplus countries can always wait.

In fact, when Keynes understood this problem, he proposed an international clearing union as a solution. Such a union would have imposed costs on both persistent surplus and persistent deficit countries. The proposal, however, was rejected.

The gap between what works and what is politically achievable has rarely looked wider. The world’s major economies are, at the moment, moving in the opposite direction from the coordinated domestic reform that the evidence suggests is necessary — cutting deals on tariffs while leaving the underlying saving and investment dynamics largely untouched. How long that can continue before markets force a more disorderly resolution is, at this point, the more pressing question.

Tidbits

India’s auto retail sector closed FY26 at an all-time high of 2.97 crore units, growing 13.3% year-on-year. Five of six vehicle categories set new annual records. Two-wheelers reclaimed pre-COVID peaks with 2.14 crore units, passenger vehicles crossed 47 lakh for the first time, tractors breached 10 lakh units, and three-wheelers set a third consecutive record with EVs now accounting for over 60% of that segment.

Source: Business Standard

AUM in index funds and ETFs has surged from ₹1.63 lakh crore in 2020 to over ₹15 lakh crore in January 2026, per NSE Indices. The number of passive fund folios has crossed 5 crore. January 2026 also marked the 63rd consecutive month of positive net inflows into passive schemes.

Source: Business Today

Pakistan-brokered US-Iran talks collapsed after 21 hours in Islamabad, with JD Vance saying Iran refused to commit to giving up its nuclear programme. Trump responded by ordering the US Navy to blockade all ships entering or exiting Iranian ports, effective Monday morning. The ceasefire technically holds until April 22, but the blockade effectively puts the two sides back on a collision course. Source: CNBC

- This edition of the newsletter was written by Aakanksha and Manie

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

{kind=link}

Understanding the oil market ft. Rory Johnston

A month-long closure of the Strait of Hormuz, a critical route for ~20% of global oil, has severely disrupted supply, triggering fuel shortages and panic across Asia, with India already facing an LPG crunch. While a ceasefire offers relief, the deeper issue is systemic dependence on a single chokepoint. To unpack this, we spoke with Rory Johnston, an oil market expert known for his typically bearish, adaptive view. Despite past shocks, he sees this disruption as fundamentally different and far more concerning.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

What i like about the daily berief from zerodha is that ... each and every concept is explained from the scratch... leaving no ambiguity ( atleast for a novice like me ) . loved the explanation... thanks alot a guys... keep up the good work... appreciate your efforts... 👏

Nice info