How the US Supreme Court killed Liberation Day

And why tariffs might still survive

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The US Supreme Court kills the tariffs

The ₹590 crore banking fraud

The US Supreme Court kills the tariffs

Learning Resources Inc. may well be one of the world’s most consequential businesses. Not because they announced a massive investment or acquisition. Not because they’re changing the world with some revolutionary technology or business model. They’re a humble business, in fact — a family-owned maker of educational toys, based in a small suburb to the north of Chicago.

What makes them so consequential is the fact that they stared Trump in the eye, and pushed him to back down.

Learning Resources is one of the two small businesses that challenged the legality of last year’s “Liberation Day” tariffs, which the US Supreme Court struck down last week. With this, the court closed a chapter on one of the most dramatic international trade episodes in modern history. Did it close the book on it, though? We, at least, don’t think so.

To appreciate what this moment means, and what it doesn’t, it helps to understand exactly how the court reached its decision. That’s what we’re talking about today.

Even presidents have limits

When the United States was drafting its constitution, towards the close of the 18th century, its founders were heavily influenced by a book that had come out shortly before: *The Spirit of Laws*, by the French philosopher Montesquieu.

Montesquieu had spent years trying to understand governments and what pulled them apart. His studies had taken him all the way back to the ancient republics, and there was one thing that he saw repeated through history: power had an ugly tendency to concentrate itself in a few hands. Once too much power was concentrated in this manner, it would rarely leave, and eventually, it would be abused. This is how all governments seemed to degenerate.

How, then, could any government stay fair?

The powers of Congress

Montesquieu’s answer was that you would have to break power up, and distribute it across different parts of a government. Each of its “branches” would all have their own functions and powers, and by design, they would all police each other. Such a system would not rely on rulers being wise or benevolent. The solution to one person’s ambition was, in his telling, the ambition of others.

This was a very real problem for America’s founders, as they sat to create the very first modern Republic. Montesquieu seemed to provide useful answers, and they baked his ideas into the very architecture of their new nation.

The American constitution opens with its governmental structure: establishing the different arms of its government, what each can do, and how they control each other. The very first article talks about the US Congress — the American equivalent of India’s Parliament — and the powers it holds. The first power it gives the Congress is over all sorts of levies and taxes, including “imposts” — an old-timey word for tariffs. If the United States is to impose tariffs on anyone, that has to begin with its Congress.

Donald Trump is the President of the United States, arguably making him the most powerful person on earth. But he’s not part of the Congress. He belongs to a different arm of the government altogether — the Executive. His job, in theory, is to execute the work that Congress wants done. His office comes with sweeping powers, and yet, he cannot take over the powers of the Congress. Controls and limitations like this were the very essence of Montesquieu’s theory.

That embargo extends to the power to impose tariffs. If the President wanted the power to impose tariffs, he would have to get it from the Congress.

The question was: did the Congress ever grant him that power?

Emergencies and special powers

Back in 1977, the Congress handed over a major set of its powers to the President, through the “International Emergency Economic Powers Act”, or IEEPA. If the United States ever faced a serious external threat, this law allowed the President to declare an “international emergency”. And then, as long as this emergency lasted, the President would have the right to do a lot of things — blocking transactions, freezing assets, confiscating property, and so on. After the 9/11 attacks, for instance, the American government used these powers to go after the assets of terrorist organisations.

This comes with a general convention: usually, when a President thinks there’s an emergency, that assessment is given a lot of leeway. Courts might try to limit what a president could do in response to an emergency, but they don’t question the existence of the emergency itself.

That discretion became a battering ram for Trump, in his many international conformations. Getting domestic policy done was often a long slog, but when it came to dealing with the rest of the world, he could simply declare an emergency, and instantly receive a wide legal toolkit. From banning Tiktok to punishing officials of the International Criminal Court, there were few limits to what he could do. In total, he has declared eleven different emergencies over his five years in office.

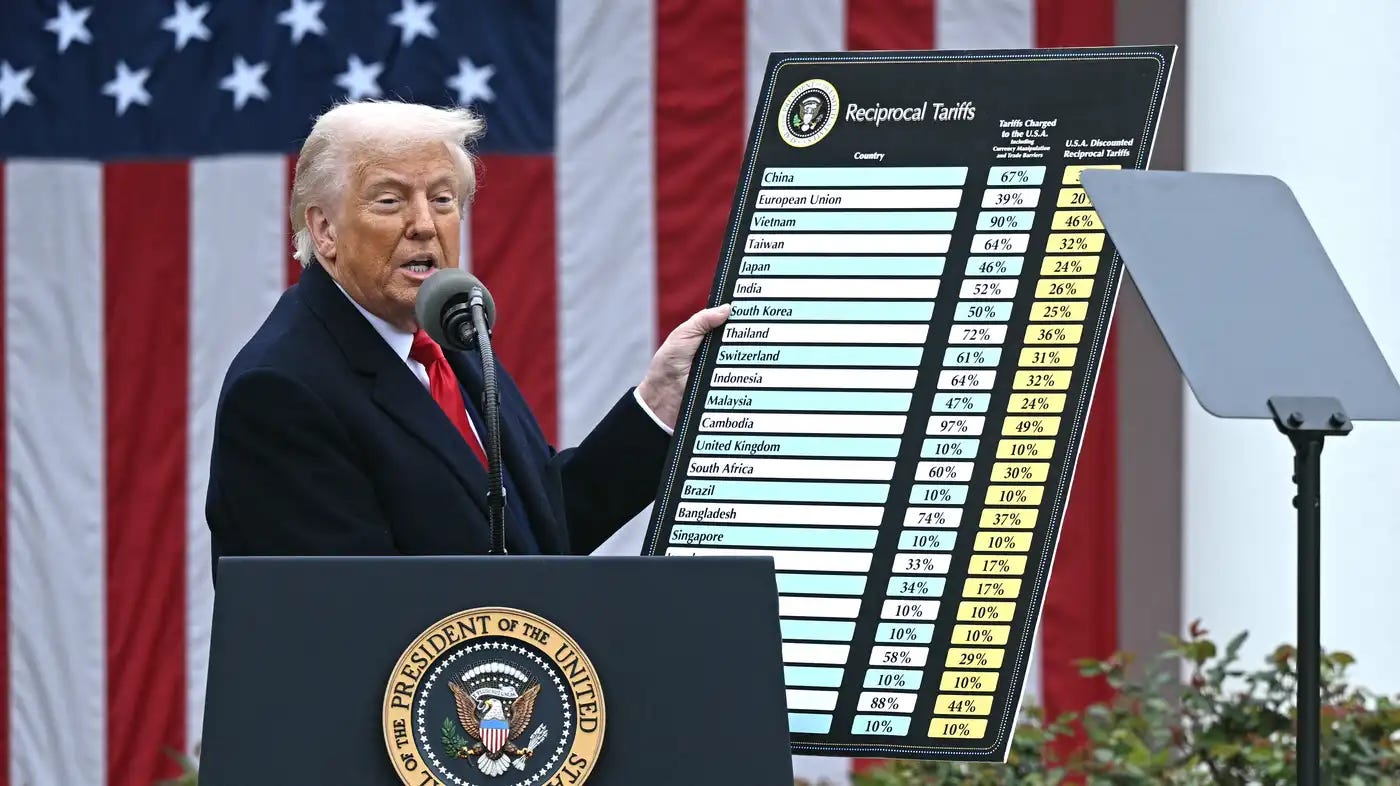

And so, last April, Trump declared that the rest of the world was treating the United States unfairly in how they traded. Things were so bad, he claimed, that there was an emergency. This was the legal basis he claimed to impose his Liberation Day tariffs.

In this case, as before, the Supreme Court didn’t question whether a true emergency existed. But it did ask a narrower question: even if there was an emergency, did Trump have the power to impose tariffs?

An emergency, after all, can’t be a carte blanche for the President to do whatever he wants. And to some of the court, this case specifically brought up a “major question“. If the government claims to have the power to do something with a massive economic fall-out, or which greatly increases the scope of what it can do, the Supreme Court tries to be doubly sure that it’s actually allowed on paper. And this — a worldwide selective tariff regime that touched the entire global economy — was certainly such a case.

The power to declare tariffs belonged to the Congress. If it didn’t specifically give the President that power, he couldn’t use it. So, what did it give?

The powers Trump has

The IEEPA gives a president an extensive set of powers over imports. He can investigate them, block them, regulate them, prevent them, prohibit them… but nothing specifically lets him tariff them. The most he can do is regulate imports. But was a tariff simply a regulation? Or was it something different — less about controlling imports and more about earning money for the government?

This is where the President lost the case.

As the court noted, whenever the Congress wants to give the executive powers to tax something, it says so clearly. Here, they didn’t. The powers the IEEPA gave the President are all meant to block or restrict transactions. If there’s a serious international crisis, the President can sanction a country, freeze their assets, prohibit outsiders from buying property, and more — all without asking Congress for a fresh law.

Tariffs, to the court, are different. They’re a tool by which the government charges money on private transactions. They’re a way for the government to raise revenue. That’s the core of what the Congress is meant to do. Over many years, it has built a very specific, deeply considered toolkit for this purpose. If the President can declare tariffs willy-nilly, that turns the IEEPA into a hidden override switch for that entire regime. Tariffs could have the effect of regulating imports — but that alone doesn’t mean the Congress has given that tariff authority to the President.

This, clearly, irked President Trump.

To our minds, though, this is a little like complaining that a policeman is allowed to arrest you, but isn’t allowed to steal your wallet. It’s easier to see the court’s logic when you think of the sorts of cases the IEEPA was meant to address — the Iran hostage crisis, or the aftermath of 9/11. For situations like that, you can see why the President would be given a wide toolkit, but one without taxing powers.

What comes next

With that, the Supreme Court struck down Trump’s Liberation Day tariffs, as being unauthorised under the law. US customs will now have to dismantle its current tariff collection procedures.

There’s a bigger question ahead: what happens to the tariffs already collected? The US federal government collected roughly $287 billion in tariffs last year, around two-thirds of which was arguably the result of this new regime. That’s not an insignificant sum, This ruling implies the government never had the authority to take that money. Will everyone who has paid tariffs so far be issued a refund? That’s an open question — and the US government could be looking at a lot of ugly litigation ahead.

This isn’t to say that Trump is powerless to impose tariffs. It’s just that the legal route he chose is now closed. He does have alternatives, though they’re harder to push through, and less sweeping in their scope. Some are already in play.

The easiest of these is Section 122 of the Trade Act. Under this law, whenever the President believes there’s a “fundamental international payments problem“ — like a large balance-of-payments deficit, or a risk that the dollar faces serious depreciation — he can put a tariff of up to 15% for 150 days. Trump went for this immediately after the ruling, slapping a flat 15% on imports from anywhere in the world.

It’s not an especially convenient route, though. For one, there’s the 15% cap. Until last week, 15% was an excellent tariff rate to have — we in India were delighted to have a rate of just 18% a couple of weeks ago. That benchmark is now buried. Moreover, its hard to justify these legally. Ever since America abandoned the gold standard, strictly speaking, it cannot have a balance of payments deficit — the value of the dollar currency balances mathematically. Justifying these tariffs in court could be harder than it was the last time. And these can only last 150 days, beyond which, all bets are off.

He has other options too, some of which hand him even wider powers. Under Section 232 of the Trade Expansion Act, for instance, he can impose tariffs to adjust imports on national security grounds — something the Supreme Court has already validated previously. Section 301 of the Trade Act offers broad powers to tariff a country in the case of a trade dispute. And there are more.

But these come with their own safeguards. They need him to bring on board various departments of the government — his Commerce Department, the US Trade Representative, the US International Trade Commission, and so on. Some of these options also require the White House to produce reports, or conduct hearings, to justify its measures. Will he stick to those procedures, in spirit? We have no idea.

Montesquieu smiles

The tariffs are not a dead issue by far. Trump has signalled that he’s not backing away anytime soon, Expect all these routes to come into play — with or without proper procedure. Many of them may eventually be challenged in court too, but in the interim, the uncertainty will persist.

That said, this ruling is a major blow to the impunity with which he was acting. It will be harder for him to announce new tariff threats on social media in the middle of the night. Now that he must tap different government authorities to bring this trade agenda to life, expect more points of friction. Every such node opens up room — room that didn’t exist before — to frustrate his tariff agenda just a little. There’s suddenly a minefield of checks and balances ahead. Perhaps none of them stall tariffs indefinitely, but they’ll certainly make the process much harder.

If Montesquieu were alive, one imagines, he would have smiled to himself just a little bit.

The ₹590 crore banking fraud

Three days ago, IDFC First Bank disclosed that it had found potential unauthorized and fraudulent activity in some bank accounts linked to the Haryana government. All of these accounts were being handled through a single branch in Chandigarh, and the amount of the money missing from the bank accounts was estimated at ₹590 crore.

Now, banking is built on trust, and that’s what shapes a bank’s value more than anything else. So, since this case of fraud was made public, the bank lost more than ₹14,000 crore in market cap, falling over 20% intraday. That was its biggest single-day fall since COVID.

Today’s story is about understanding the why, what, and how behind this event.

Let’s start simple. Banks have lots of clients, and the government is one of them. That could mean central government departments, state governments, and even PSUs. These entities park money with banks to run their day-to-day operations.

Now, you’d expect government entities to naturally gravitate toward public sector banks for this. And that’s not entirely wrong. There’s a comfort factor in doing business with banks that are government-backed, and that gives them the perception of safety — like nothing can possibly go wrong. But there’s no rule that government money must sit only with them. State departments are free to empanel banks of their choice, and that includes private ones.

And they do so, too, for a few reasons.

For one, deposit rates matter. Government balances are extremely rate-sensitive. Even 10–20 basis points can shift money, so they’ll prefer the bank with more aggressive pricing. Then, there’s service quality. Government-linked savings accounts hardly stand still — money keeps moving with tax collections, treasury tools, settlement speed, and digital systems. This is where private banks sometimes outshine public ones — though not always.

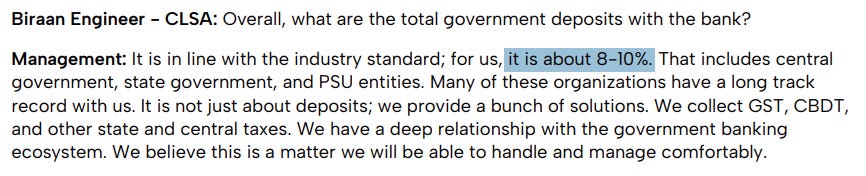

So yes, private banks do get government business. In fact, for IDFC First Bank, total government-related deposits — central, state, PSU combined — are about 8–10% of total deposits, broadly in line with industry standards.

But here’s the catch: government deposits are bulky and not sticky. They do sit in low-cost CASA (or current account-savings account) accounts, which makes the cost of funds look great. But, unlike retail accounts, they can move overnight, and in massive amounts. So while they can help growth and liquidity, they also add volatility.

Now that we have the basics of banking out of the way, let’s get into what actually happened with IDFC.

So, what happened?

This entire episode started with something routine.

About a month ago, a department of the Haryana government asked IDFC First Bank to close its account and transfer the funds to another bank. During that process, the balance didn’t match. The government believed it had “X” in the account, but the bank’s books showed less.

That’s when the rest of the skeletons began to unfold. Soon after, other Haryana government entities started reconciling their balances with IDFC First Bank, and found similar discrepancies. All of these accounts were linked to a specific branch in Chandigarh.

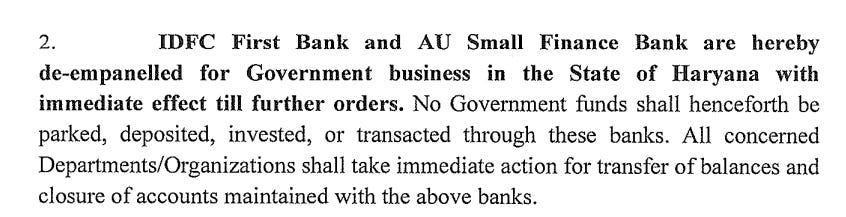

On February 18, the Finance Department of the Haryana government issued a notice revising its guidelines for dealing with banks. In that notice, it explicitly stated the “de-empanelment of IDFC First Bank and AU Small Finance Bank for any Government business in the State of Haryana.”

Following its internal review, IDFC First Bank disclosed that the aggregate discrepancy across the identified accounts was about ₹590 crore. Of this, ₹490 crore was the gap identified during reconciliation. Another ₹100 crore was actually provisioned by the bank itself in case it found more gaps, even though no such gap was identified at the time.

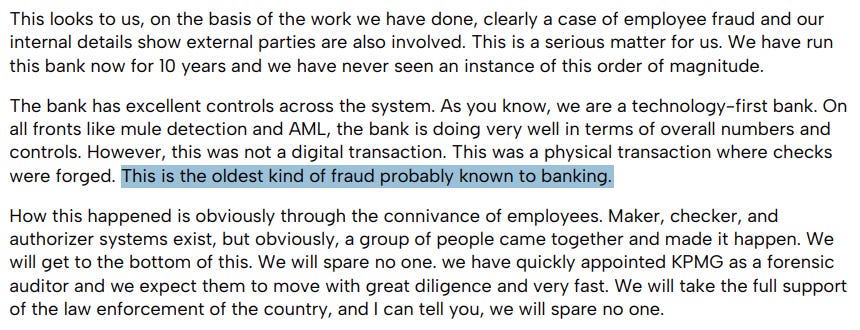

This gap wasn’t the result of a complex cyber hack. V. Vaidyanathan, CEO of IDFC First Bank, called it “the oldest kind of fraud probably known to banking” — that is, forged physical checks and fake authorization letters.

Here’s how it went down. The debit instructions came supposedly from the client. However, the cheques presented were forged. It turns out that bank employees passed the entries, and the funds were transferred to external beneficiary accounts.

Now, banking operations for cheques typically run on a “maker–checker–authorizer” system. One person initiates it, another employee checks it, and a third authorizes it. The whole point is independence. But that’s not what happened here. In this case, that chain allegedly broke because the people involved acted together — possibly with a third party outside the bank. In essence, they colluded.

As a result, four suspected bank officials have been suspended. The matter was placed before a Special Committee of the Board, the Audit Committee, and the full Board. A forensic audit by KPMG has been initiated, and police complaints have been filed.

The bank has said there was no senior management involvement, and that this was pulled off by individual employees. The bank has also sent recall requests to other banks where the money was transferred, asking them to lien-mark suspicious beneficiary accounts. Those banks are cooperating as part of the recovery process.

The aftermath

On the earnings call, the management of IDFC was faced with an uncomfortable question: how did this go on? Didn’t monthly statements go out? Didn’t alerts trigger? Management acknowledged that transaction alerts, monthly statements, and balance confirmations are system-driven and were sent.

This raises an obvious tension: if the statements reflected the debits, why weren’t they flagged earlier? And not just by the bank, but also by the Haryana government.

From the bank’s side, the line is clear: if it’s their responsibility, they’ll own it. If other parties are involved, they’ll pursue that through legal channels — though they’ve also said they don’t want to litigate unnecessarily with the government.

{kind=link}

Now, banks do have insurance coverage for employee dishonesty of about ₹35 crore. But that’s tiny relative to ₹590 crore. Financially, this is not a rounding error. The entire ₹590 crore will pass through the P&L, subject to recoveries. That’s more than the Q3 profit (₹503 crore) they reported recently. Management had earlier guided for a strong last quarter, expecting profitability higher than the previous ₹500 crore baseline. Even after this hit, they still expect to remain profitable, though not as high.

From a balance sheet point of view, it will hurt them far less. Their scale and capital strength far exceeds this one event. Their net worth is over ₹46,000 crore, deposits of about ₹2.8 lakh crore and a liquidity ratio of more than 100%. The Haryana government deposits themselves were only about 0.5% of total deposits. Post-announcement, roughly ₹200 crore flowed out — a drop in the ocean relative to the overall deposit base.

In fact, the RBI has indicated no broader systemic risk from this fiasco. And looking at the numbers, it’s hard to argue this is a capital event.

But reputation is a little different from capital. Deposits are trust money. Once shaken, especially in government circles, the ripple effect matters more than the absolute amount.

The Haryana Finance Department has already de-empanelled IDFC First Bank (and AU Small Finance Bank) for government business in the state, with immediate effect, directing that no government funds be parked or transacted through these banks until further orders. That’s not small. Government relationships are long-cycle businesses. They take years to build, but can freeze overnight.

Now zoom out

Does this mean private banks are unsafe for government money? Well, not really. Government deposits for IDFC First Bank are 8–10%, which is broadly the industry normal. Many large private banks handle GST collections, CBDT processing, and treasury services. This isn’t new territory.

But what this incident does add is narrative risk. When something goes wrong at a public sector bank, it’s politically easier to frame. With a private bank, scrutiny tends to be much sharper.

Does that automatically mean government money shifts back to PSBs? Not necessarily.

Large, well-capitalized private banks with robust controls will likely retain mandates. But mid-sized banks will face tougher questions. For instance, AU Small Finance Bank got caught in the crossfire and lost government business despite not being at the center of the fraud. But that kind of spillover is unlikely for names like HDFC Bank or ICICI Bank.

Another tension in this case was that this fraud took place despite high levels of digitalization in banks. In previous calls, management emphasized being highly digitized, with 98–99% e-KYC, e-mandates, and so on. Yet this fraud bypassed digital rails entirely, happening through physical instruments. No matter how advanced digital systems are, legacy physical processes remain weak spots, especially when human collusion enters the picture.

Management has said they will introduce additional system-based confirmation alerts for high-value branch transactions, and add AI-based signature checks with mandatory human double confirmation. Will that eliminate collusion risk? Perhaps not, but it raises the cost of pulling it off again.

Damage control

So what happens next?

In the short term, we’ll see provisioning by the bank, recovery attempts, and forensic findings in 4–5 weeks. There could also be discussions around shared liability.

In the medium term, IDFC First Bank will tighten controls and layer more digital oversight onto physical processes. Across the system, government accounts will likely face greater scrutiny.

But in the long term, this is about reputation rebuilding. Markets punished the stock not because of a credit loss, but because of governance. That hits differently.

The fraud itself may get absorbed in the profits of a single quarter. But the brand damage, if mishandled, could linger much longer.

Tidbits

Adani eyes Formula 1 comeback at Buddh Circuit

Adani Group is working on a plan to restart Formula 1 at Greater Noida’s Buddh International Circuit, as part of its bid to acquire debt-laden Jaiprakash Associates. The circuit comes bundled with the deal. If revived, F1 could return to India after over a decade, pending clearances and financial closure.

Source: ET NowCentre pushes floating solar with draft policy talks

The renewable energy ministry has begun consultations with states on a draft floating solar policy to unlock projects on water bodies. India has just 700 MW installed so far due to unclear rules and site data gaps. The new roadmap aims to ease land constraints and give developers clearer approvals.

Source: Business StandardSEBI issues show-cause notice to Zee

SEBI has sent a show-cause notice to Zee Entertainment in a long-running fund diversion case dating back to 2019. The company says it will respond and continues to deny the allegations. Zee claims the prolonged probe hurt strategic moves, including its failed merger with Sony.

Source: The Hindu BusinessLine

- This edition of the newsletter was written by Pranav and Kashish.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉