How India’s PSUs are classified

Finding the shine in India’s public-sector jewels

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

How India’s Ratna system for PSUs works

Why the GST can’t police itself

How India’s Ratna system for PSUs works

India’s listed PSUs account for 8-9% of India’s total stock market capitalisation. Many of them are household names — like ONGC, NTPC, Coal India — and millions of Indians own their shares directly or through mutual funds.

Yet, we found ourselves asking a key question: why are some PSUs called “Navratna“, some others “Maharatna”, and others “Miniratna”? Why does this classification matter all that much?

Well, the Ratna system determines how freely a company can spend, borrow, and expand without waiting for ministerial approval. In a system where government ownership still dominates large stretches of the Indian economy, the Ratna tier a company sits in is effectively a measure of how much it is trusted to run itself.

Last year, Cabinet Secretary T.V Somanathan led a committee to review this classification framework — a system that, at its core, has been largely unchanged for nearly three decades. The report was due before the Union Budget of FY27, but the Budget came and went with no announcement.

However, the review signals recognition that a framework that long ago may not be fit for the India of today.

Whither autonomy?

To understand what needs fixing, you first need to understand how we got here.

After independence, much of India’s economy was centrally governed, and PSUs were expected to be the linchpin of India’s investment planning. Our PSUs had basically become instruments of employment, regional development, and political economy — all at once.

But, by the 1980s, the model had curdled. Every significant business decision inside a PSU necessarily required a sign-off from the corresponding ministry. If a PSU wanted to invest in a new facility, buy equipment, or even enter a joint venture, it had to route its request through many layers of bureaucracy. Managers had formal responsibility for their companies, but no real authority to run them.

The government’s first attempt to fix this was the Memorandum of Understanding (MoU) system, introduced in the mid-1980s. The system entailed annual performance contracts between PSUs and their ministries setting targets for profit, production, and efficiency. While initially promising, the results were mostly limited. After all, the same ministry that set the targets evaluated performance against them — an obvious conflict of interest.

Then, in 1991, India’s economy liberalized at once, while also cutting government spending. This, in turn, left PSUs exposed. With their poorly-run finances, many PSUs were uncompetitive and found it difficult to survive. It was expected that, in order to truly give them autonomy and pressure them to market discipline, they would be privatized.

However, fully privatizing them was politically impossible. For one, there was plenty of opposition from public-sector unions and many parts of India’s bureaucracy. But secondly, in many cases, it would have been undesirable to sell them off, too. PSUs are often designed to serve national interest rather than profit alone.

So, the government had a problem to solve. Its PSUs were hampered by constant intervention from the top-down, which didn’t leave them much room in how they should be run. However, just to achieve that goal alone, it couldn’t sell them off wholesale to the market. How does it find a middle path between both scenarios?

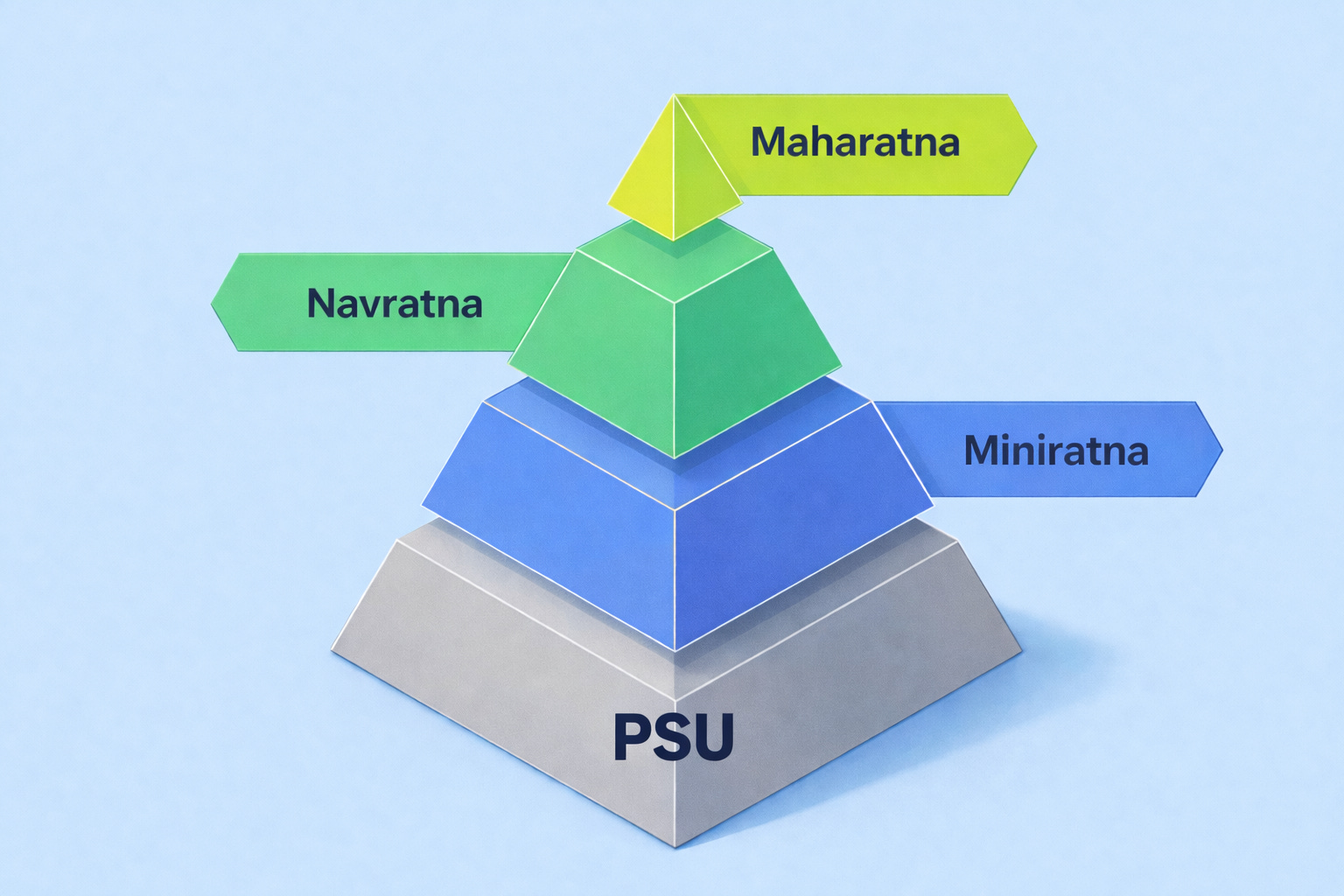

The nine jewels

Enter the Ratna system of classifying PSUs.

In 1997, India named nine public sector companies as Navratnas — a term originally referring to the nine most distinguished advisors to Akbar, the Mughal emperor. Within months, the government also introduced the Miniratna classification for smaller, profitable PSUs. Maharatna, a new topmost tier, followed in 2010.

The result is a three-step ladder. Each stage reflects the size and scale of a company, and how much autonomy they should be granted in making investments. Upgradation to the next stage is subject to periodic government approval, and is based on the performance of the PSU: its revenue, profitability, and so on.

Miniratnas

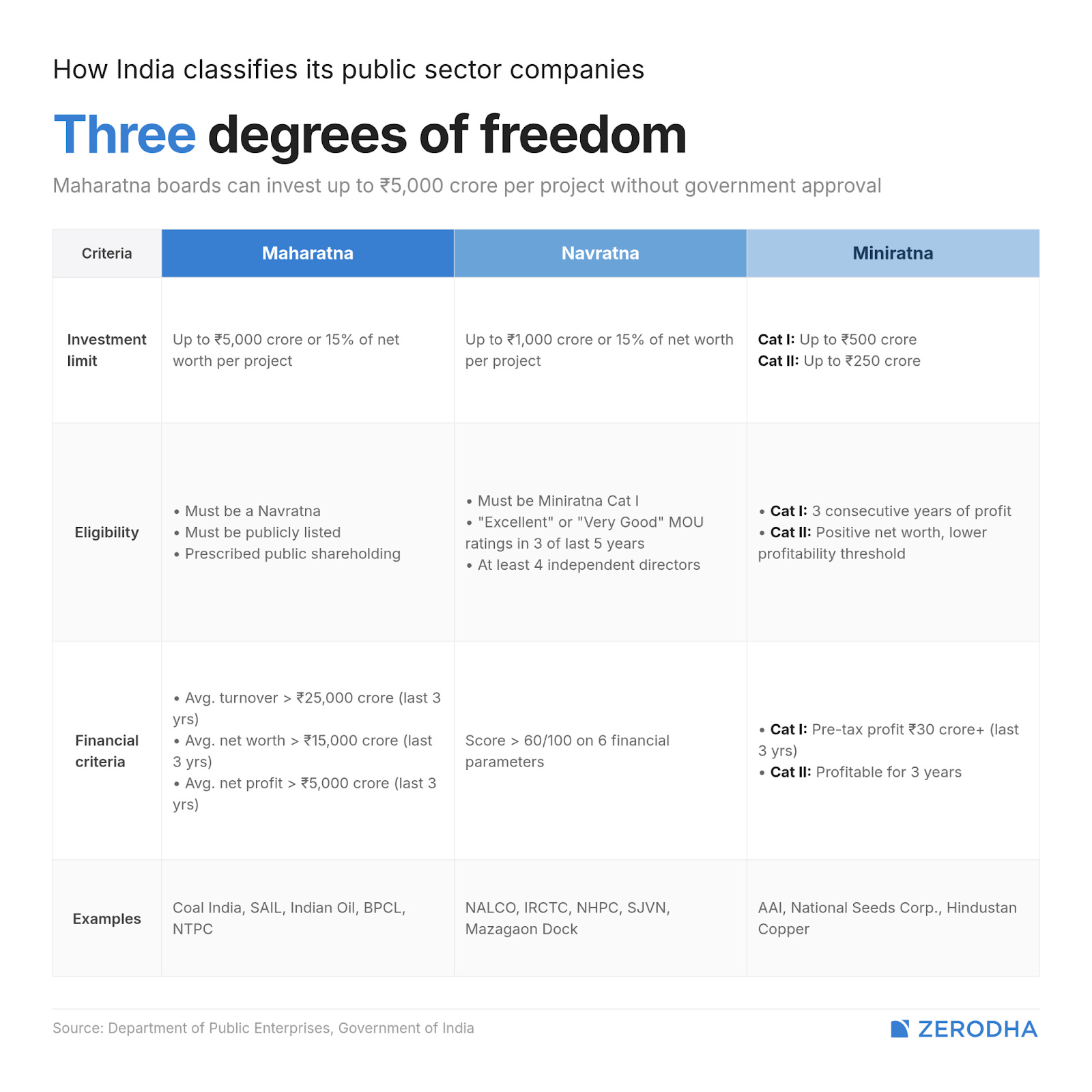

At the base are the Miniratnas, split into two sub-categories. Category I requires the PSU to have three consecutive years of profit, with a pre-tax profit of at least ₹30 crore in one of those years. It unlocks the ability to invest up to ₹500 crore without seeking government approval. Category II has a slightly easier profitability benchmark to meet, with capex autonomy up to ₹250 crore.

There are over 50 Miniratna companies as of today. Most of them are located in sectors that are not as strategic to India. Some are project-specific secondary firms in important industries, or subsidiaries of larger PSUs. Some examples of Miniratnas include Airport Authority of India (AAI), National Seeds Corporation, Hindustan Copper, and so on.

Navratnas

Now, to qualify as a Navratna, a company must meet a few conditions.

It should be a Category I Miniratna

It should achieve “Excellent“ or “Very Good“ MOU ratings in at least three of the last five years

It should score 60 or above on a composite index of six financial parameters — including net profit to net worth, manpower cost ratios, and earnings per share.

Navratna status allows a company to invest up to ₹1,000 crore in a single project without government approval. It can also form joint ventures, float overseas subsidiaries, and raise debt from capital markets within the amount.

Companies in this category include National Aluminium Company (NALCO), Central Warehousing Corporation, MTNL, etc. Some recent upgrades from Miniratna status include IRCTC, Indian Railway Finance Corporation, NHPC and SJVN (both of which work on hydropower projects), and Mazagaon Dock Shipbuilders.

Maharatnas

The Maharatna is the top rung, introduced in 2010. These are usually the most critical, strategic PSUs of India — like Coal India, Steel Authority of India, Indian Oil, BPCL, NTPC, and so on.

An eligible company must average ₹25,000 crore in annual turnover, ₹5,000 crore in net profit, and ₹15,000 crore in net worth, all over three years. Critically, a Maharatna must be publicly listed. It is the only tier where external market accountability is baked into eligibility. Maharatna boards can invest up to ₹5,000 crore or 15% of net worth per project without seeking approval, and also undertake acquisitions in India and abroad.

Mixed results

As far as how helpful the classification system has been, the results have been mixed.

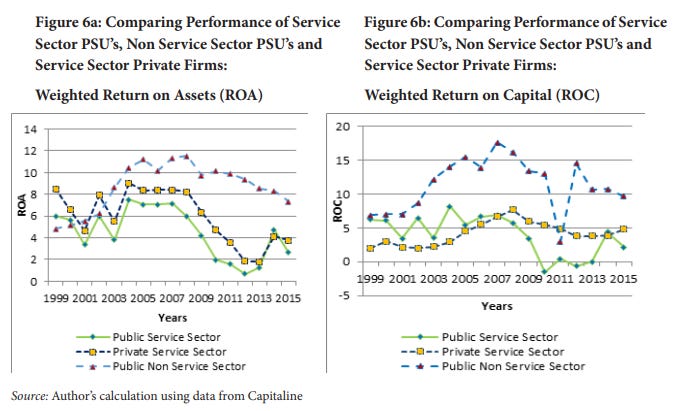

A 2017 paper by economist Ajay Chhibber found that Maharatnas outperformed comparable private firms on return on capital by roughly 4 percentage points and on return on assets by about 2 percentage points. But Navratnas and Miniratnas performed worse than private companies of similar size. Another paper found only 6 Navratnas that were consistently financially sound; the remaining 8 showed financial weakness in many years.

On one hand, the Ratna system can indeed be helpful. NTPC, for instance, has used its Maharatna status to build joint ventures and subsidiaries to execute power projects. It is also using its autonomy to make the pivot from thermal power to renewables.

However, even prior to becoming a Maharatna, NTPC has always been consistently profitable. After all, it signs long-term contracts, which always ensure that the power it generates will be sold to a utility at predictable rates. In such a case, the Ratna system became a catalyst for further success of a firm that was already winning.

But can it save a company that’s failing? Well, if MTNL’s story is to be believed, the answer is no.

See, MTNL was one of the original Navratnas, and has held that status since. Over that same period, it has become one of the most spectacular business failures in India. In FY24, it recorded a net loss of over ₹3,300 crore, and held liabilities worth ~₹34,500 crore; many of these loans were owed to public-sector banks.

However, MTNL’s problem could, perhaps, not truly be solved by more freedom. It was restricted to just Delhi and Mumbai, which are India’s most competitive telecom markets. It was up against private operators with national networks and zero obligation to carry bloat, unlike MTNL did from its monopoly days. Its technology also lagged most of its peers.

Clearly, the Ratna system may be an amplifier for firms with healthy balance sheets. If you’ve performed well enough in the past, and have a high net worth, you are worthy of an upgrade. However, it cannot fix companies with deeper structural problems (like MTNL). A classification system merely based on past performance will be extremely inadequate in transforming a struggling PSU.

Diamonds aren’t forever

Even within the current implementation of the system, issues exist.

For one, enforcement is pretty weak. In fact, seemingly, no PSU has ever been downgraded for lackluster performance — even though in theory, it’s possible. And the most telling example of this is BSNL.

BSNL is, of course, India’s most strategic public-sector telecom firm, and ranks among the top 30 PSUs by annual turnover, crossing ₹21,000 crore in FY2024. Yet, somehow, BSNL has always been a Category I Miniratna. The reason, quite simply, lies in its lack of consistent profitability, and its inability to pay off debt. Now, ideally, BSNL should probably have been subject to a re-revision of its rating in light of such results, but it still remains a Miniratna.

Secondly, formal autonomy and real autonomy are different things. A World Bank review found that ministerial directives routinely override the formal powers the guidelines grant, intervening in commercial decisions the board is supposed to make independently. CEOs are government appointees serving uncertain tenures, and may be unwilling to take strategic risks that might expire with the next reshuffle. In fact, sometimes, the board of members may include ministerial staff themselves.

The third problem also lies in the boards of PSUs. Enhanced powers under Maharatna and Navratna status are explicitly conditional on having at least four non-official directors, while Miniratnas require at least three. These directors are supposed to provide the external check that a listed company gets from its shareholders.

But as of October 2024, 441 of 750 independent director positions across PSU boards were vacant. This included 200 vacancies on listed PSU boards, making them non-compliant with SEBI’s own governance rules. A system built to function with independent oversight is running, at scale, without it.

Lastly, there’s a sectoral problem. As per the same paper by Chhibber, manufacturing and mining PSUs respond meaningfully to performance contracts, but service-sector PSUs (like airlines and telecoms) don’t. That’s because services are generally more competitive and change faster in the face of new technology. Easy access to soft government loans actively removes the pressure for services PSUs to adapt quickly.

The next version

That’s where the Somanathan committee’s proposals enter. It suggests new Ratna tiers, and criteria that look beyond just past performance and financial size. Without such upgrades, you could be left with outliers like BSNL, which are incredibly strategic to India, but are at the bottom tier of the classification.

Whether the next framework changes any of this is the open question. Reforming the classification is the easy part. Creating downgrade consequences that actually get used, and filling board seats with people who can genuinely push back on ministry interference — all of that is going to be considerably harder.

Why the GST can’t police itself

A working GST system is a fascinating thing.

The tax has a built-in compliance mechanism. Every business that buys something has a financial incentive to demand a proper tax invoice from its seller, because that invoice is how it claims credit, in turn, for the tax that it paid. And so, every buyer polices its sellers. The seller, knowing the buyer will insist on an invoice, reports their sale honestly.

Only, the way India’s GST currently works, this mechanism is stuck, according to a recent paper by Modi and Shah. Well… not that Modi and Shah — Arbind Modi and Ajay Shah.

It wasn’t meant to be this way. But we made a series of design choices around input tax credits and refunds that might sound fair, in isolation — but taken together, have broken the credit chain the GST depends on.

Together, they meant that India’s GST, built to tax consumption, instead drifted into taxing production.

Understanding the GST

Before 2017, India’s indirect tax system was a complicated mess. The central government levied excise duties on manufactured goods, and a separate service tax on services. Meanwhile, each state ran its own value added tax (VAT) regime. Together, this created a mass of different rates, rules, and credit chains.

To you, as a consumer, this created an awkward problem. Imagine you bought a shirt. Everyone that had a hand in bringing it to you — the mill that spun the yarn, the weaver that turned it into fabric, the tailor that cut and stitched it, your local clothing store — might have paid a different kind of tax. By the time the shirt reached you, its price hid half a dozen taxes which different businesses had paid at different points in the supply chain. Ultimately, however, you had to foot the entire bill.

In an ideal world, these stacked taxes would cancel each other out, removing any duplications. The tailor, for instance, would get credits for the tax he paid when buying fabric, which would be adjusted at the next stage. But while there were some such systems in theory, the mess of taxes often didn’t actually allow for it. If the tailor paid service tax for a tempo to transport fabric, that wouldn’t be adjusted against the excise duty on the shirts he stitched.

GST was supposed to end the confusion. It replaced this mess of taxes with a single, unified, destination-based tax. This was a single tax system, which applied at each stage of the supply chain.

Input tax credits

Running through it was a single thread — a credit mechanism that neutralised upstream taxes. Every business would get tax credits for anything they bought. Whenever they made a sale, they could adjust these credits against the tax they were due to pay. As a result, the extra tax paid at any one step only applied to the value added at that step, and nothing else. In this system, when you came in as the last link of the chain — when you bought that shirt — you only paid one tax on it.

This made input tax credits (ITC) a key load-bearing pillar in the system. It wasn’t a concession or subsidy. It was what prevented the GST from collapsing back into the cascading mess it replaced.

At least in theory, the GST was India’s version of what’s called a “consumption-type VAT” — where businesses could deduct tax for all the inputs they purchased to make something, including capital investments. This is the global standard. It ensures that people’s consumption, and nothing else, yields tax. To economists, this is the most neutral way of charging such a tax. If you start taxing specific business decisions — like something that makes capital-intensive methods more expensive than labour-intensive ones — you can end up creating all sorts of weirdness in the economy.

Three restrictions

There was, however, one complication. In the eyes of the government, input tax credits could become a path for misuse; people would claim bogus credits, and try to avoid paying tax. So, it began creating restrictions.

First, it created a wide list of blocked credits. There are many things the GST law denies credits on: motor vehicles, food and beverages, health insurance, works contracts related to immovable property, club memberships, and so on. In isolation, this made sense: these were all effectively personal expenses that people billed to businesses. If a company was footing the bill for its director’s meals, the government shouldn’t subsidise that meal further with a tax credit.

Only, this list often catches genuine business inputs. If a logistics company rents a warehouse, or a tour operator buys vehicles to take people to a nearby attraction, these expenses are clearly core to their businesses. But they’re blocked from receiving credits for this. The tax paid on them instead gets baked into their bills as a cost, which adds to the final price of whatever is sold downstream.

Second, the refund rules are narrow. Sometimes, a business pays more GST on its inputs than it collects on outputs. The classic case is that of exporters: they sell at zero per cent GST to foreign buyers, but purchase inputs at full GST rates. If the GST is to behave like a consumption tax, in a case like this, the government should refund any excess tax a business has paid. India does so — but only in two specific cases: exports and “inverted-duty” structures, where the tax rate on inputs exceeds the rate on outputs. In other cases, that excess tax simply carries forward indefinitely as an entry on a ledger.

Even where refunds are permitted, there are restrictions. That has strange consequences. For instance, an exporter can’t claim refunds for capital goods. If you run a pharmaceutical company that sells to Europe, for instance, you can claim refunds for any chemicals or APIs you buy — but not on the machines you use to make that medicine. Similarly, if there’s an inverted duty, refunds aren’t permitted for services or capital goods. Imagine you sell packaged goods for instance — with 5% GST — while paying 18% GST for the cold storage services you need to transport them to the market. Because that’s a service, you don’t get a refund.

Third, and finally, there’s a web of procedural conditions. To claim tax credits, the suppliers of a business must have filed returns and reported the invoice correctly. If your supplier defaults, you lose the credit, even if you paid tax in good faith, and have the invoice to prove it. There are a variety of other process-based restrictions — each designed to plug a problem. In isolation, they make sense.

But as we’ve seen repeatedly on The Daily Brief, most bad outcomes come out of something that sounds sensible.

When the ITC system breaks

Let’s return to the self-policing mechanism we started with.

The magic of the GST, at least in principle, is that it enforces itself. Instead of an expensive tax enforcement system, it relies on peoples’ self-interest. Buyers watch sellers themselves; because they want their own tax credits, they demand GST-compliant invoices from their suppliers. As this game of incentives works itself through the supply chain, it creates an automatic audit trail that any tax authority can check.

Some of that is actually happening. According to recent research, the GST has pushed many businesses into formality, while making a serious dent in undocumented transactions.

But this relies on one fact: buyers have to trust that those tax credits and refunds will come through.

Choosing amongst trade-off

If there’s too much friction in claiming credits, the system breaks down. Why insist on proper invoices if some rule stops you from getting credits? Every gap gives sellers the room to underreport what they sell. As these gaps accumulate, the system drifts back toward what Modi and Shah call “the high-evasion equilibrium of the pre-GST era.” This is a particularly bad problem with services, which are intangible and often supplied informally, making them harder to audit without a trail of invoices that makes them legible.

Think of this as a trade-off. When credits flow easily, the in-built compliance loop works better, even if it creates room for people to game the system. When credit flow is limited, people game the system less, but it’s easier for them to defect from the system entirely.

Most OECD countries let credits flow freely first, and catch fraud later, using data analytics and risk-based audits. India’s approach is precautionary: we deny credits upfront to prevent bad actors from claiming them. This minimises the risk of a fraudulent credit getting through. But it does so at the cost of denying legitimate credits to honest businesses. Our approach — of blocked credits and restrictive refund formulas — has no real global peer.

And that, in turn, compromises the self-policing mechanism of the GST in the first place.

The cost of our choices

To Modi and Shah, there are three costs that we unwittingly pay for our choices.

One, there’s a hidden gap between what a business owes on paper and what it effectively pays. Imagine you buy a strip of paracetamol — which theoretically comes with 5% GST. Only, the pharma company pays 18% on the machines it uses to make your tablet, and because it can’t claim a refund, it pushes that extra cost down to you. That GST then cascades through the supply chain, exactly as so many taxes did before the GST. Your bill might just show a GST of 5%, but in fact, much more of your money has gone to the government. It would be simpler for the government to charge a clean 10% GST with refunds passing through the system.

Two, this has a cascading effect on India’s competitiveness. Imagine somebody imports the same strip of paracetamol from another country, with a simpler tax system. They pay a clean 5% GST, while the Indian manufacturer’s prices carry an embedded tax in them. The import is structurally cheaper than our own produce.

The opposite happens with our exports. Even though the export itself carries no GST, an exporter’s prices contain the burden of whatever GST they paid on capital goods. This makes them less competitive than their peers from elsewhere in the world.

Three, this drags on our growth itself. In many ways, our GST system makes capital investments unattractive. This effectively raises the effective price of new machinery, compared to labour. This creates a bias, in our businesses, towards less productive methods. Ironically, in major industrial states — like Gujarat, Maharashtra or Tamil Nadu — it was easier to get credits for capital goods before the GST. A lot of the wealth of any economy comes from the investments of the past. A slow drift towards less investment, over time, is a drift away from growth.

China used to have many of the same problems as us: its VAT originally covered just goods, not services — and restricted credits for capital goods. But between 2009 and 2016 they ran a series of reforms, ending with a modern consumption tax system, with broad input tax credits. This brought major productivity gains all through. Those same gains are available to India as well.

The path to better gains

The authors lay out a roadmap for reform. We need to make tax credits move more easily, slashing through all restrictions — combined with simple, automatic refunds. We have the digital infrastructure for it; we just need the will to push things through. In fact, they go so far as to suggest that we need a single tax slab, to cut through most complications.

Modi and Shah end with a philosophical observation. Our systems assume that people behave in bad faith — and treat them accordingly, denying first and asking questions later. That, ultimately, hurts the system itself.

Tidbits

Wipro has agreed to acquire Mindsprint, the IT and digital services unit of Singapore’s agri-business giant Olam Group, for $375 million. The deal comes bundled with an eight-year services agreement in which Olam commits $100 million annually to Wipro — taking the total contract value past $1 billion.

Source: Economic Times

The Strait of Hormuz crisis has brought exports from Sojat — which accounts for a ₹4,000–5,000 crore annual henna trade — to a near standstill, with around ₹250 crore worth of consignments stuck at ports and production down nearly 80%. Traders say the disruption is worse than COVID, with factories that once ran 24 hours now operating half-shifts, and workers returning to their home states.

Source: Business Standard

With the West Asia conflict adding currency pressure on top of existing liquidity stress, Indian banks are offering their highest certificate of deposit rates in nearly two years to attract short-term funds. CSB Bank offered the highest rate at 8.32% for 91 days, while HDFC and IDBI offered 7.6% for 33-day funds.

Source: Economic Times

- This edition of the newsletter was written by Manie and Pranav

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉