How Big Bazaar fell through the cracks

And how SEBI gave it just a slap on the wrists

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Big bazaar, bigger crashout

India’s cement sector hits a wall it didn’t build

Big bazaar, bigger crashout

Back in the day, Future Retail used to be the second-largest organised retailer in India.

At its peak, it ran nearly fifteen hundred stores across more than four hundred cities, pulled in over ₹20,000 crore a year in operational revenue, and traded at over ₹500 a share. For many of us, it was the first look at a real mall-like establishment in India.

But the company collapsed in 2022, with creditors filing admitted claims of ₹27,415 crore against it. And earlier this month, after four years of investigation, SEBI released a 222-page order on what went wrong inside the company before the final fall.

What makes the whole tale more curious, though, is the final monetary penalty imposed by the order: just ₹50 lakh, divided across three people. But that’s all SEBI rules allowed it to do.

So what did Future Retail do to receive this flak? And why did it end the way it did?

How Big Bazaar got India right

To get there, let’s first go back to how Future Retail began.

In 1987, a 26-year old named Kishore Biyani started selling bell-bottoms to a generation that just started to think about ready-to-wear fashion. The company he founded that year was called Manz Wear. Later, he renamed it to Pantaloons and listed it on the BSE in 1992. It did well for itself.

Then, nine years after that, in October 2001, the first Big Bazaar store opened.

At the time, the conventional wisdom in Indian retail in 2001 was that American supermarkets were the ideal norm: think wide aisles, neat shelves, and clinical lighting. But Biyani disagreed, thinking that Indians were intimidated by that aesthetic, and would shop more comfortably in a space that felt like something they already knew, even if it looked chaotic — like a bazaar.

So he made Big Bazaar feel like that, with inventory piled on top of each other and messy arrangements across. By 2009, Pantaloons Retail had over a thousand stores across seventy-one cities and was serving two million customers a week. It was a true revolution in India’s consumer landscape.

When growth stopped paying for itself

However, Future Group had built most of the empire by relying heavily on short-term debt for expansion. It also diversified into segments where it had no obvious advantage. The model could work as long as retail revenues grew faster than the cost of servicing all that debt.

But, by the early 2010s, they weren’t.

The first major sign of strain came in 2012, when the group was carrying around ₹8,000 crore of consolidated debt and could no longer service it through retail cash flow alone. Future Group agreed to sell Pantaloons, the foundation of the retail empire, to Aditya Birla Nuvo for ₹1,600 crore.

Yet, through the rest of the decade, Future Group didn’t stop expanding stores, and naturally, the debt kept growing alongside. By 2015, the financing problem needed a full structural reset, and the company found a synergy with Bharti Enterprises, which was losing money on its own retail venture.

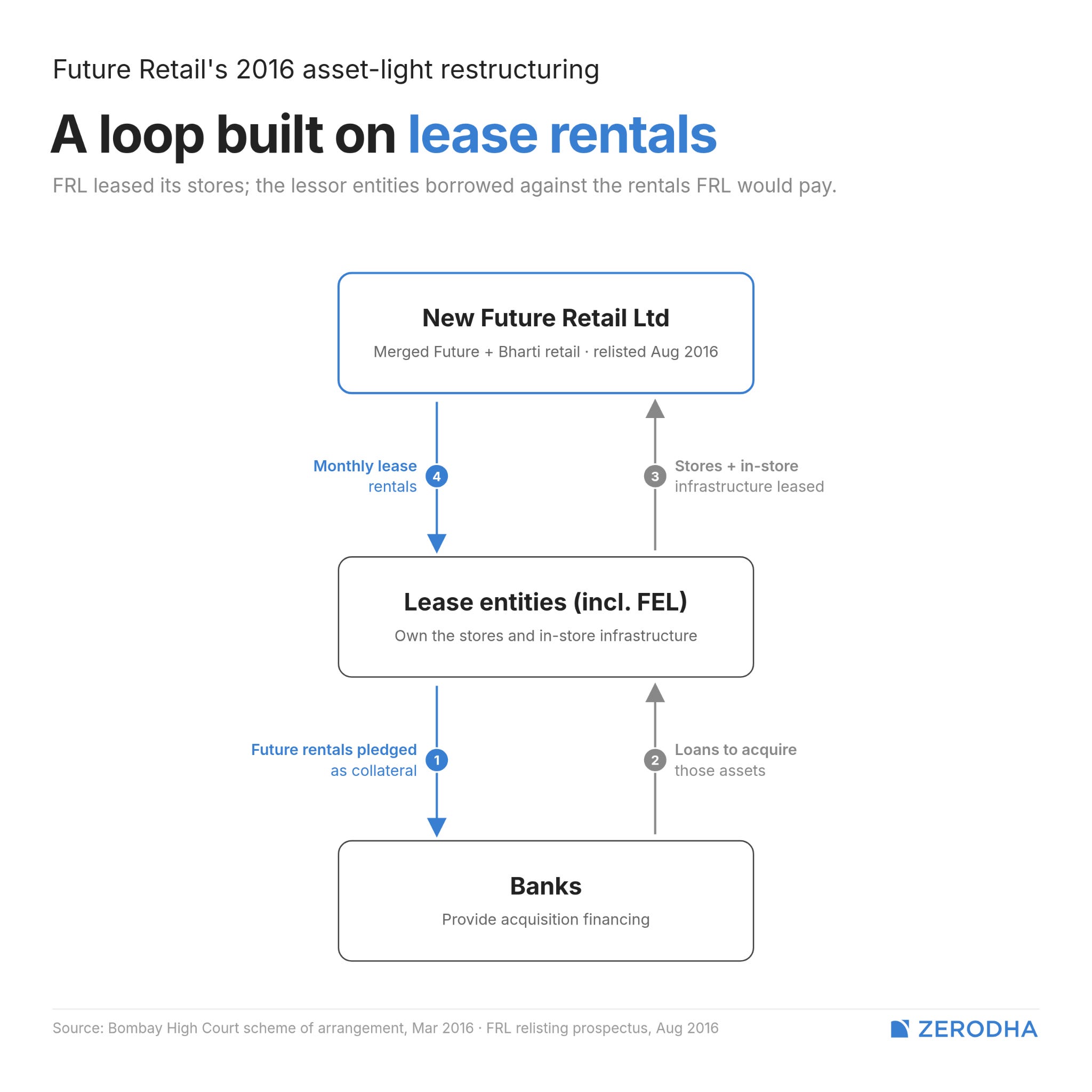

So, in March that year, the Bombay High Court approved a composite scheme that combined the two. The original Future Retail Limited was renamed Future Enterprises Limited. The shell of Bharti’s old retail company took over the stores, was renamed Future Retail Limited, and relisted afresh on public markets in August 2016, with a clean trading history and a lighter balance sheet.

The repackaged version was designed to be asset-light. Both the stores and the in-store infrastructure inside them wouldn’t be owned anymore, but be leased from a set of entities (including FEL) that were legally separate from the group but operationally part of it. When those entities needed money to acquire what they would lease to FRL, they would borrow from banks against the potential future stream of the same lease rentals FRL would pay them. As long as those rentals were paid, this arrangement was fine.

But what it produced was a structure that didn’t show up on the balance sheet of the company shareholders were actually investing in. A retailer with around ₹6,000 crore of disclosed debt was, on SEBI’s eventual reckoning, closer to ₹8,000 crore. The extra Rs 2,000 crore was sitting in the network of entities surrounding the company.

All contingent on the promise of a highly-leveraged retail business paying its dues.

Directors anonymous

The trouble with that network was that almost nobody outside the company could see how it really worked. The Annual Reports listed lease payments as ordinary commercial transactions with vendors. The Audit Committee was told the same. Only when SEBI began questioning the people running the lessor entities did a clearer picture emerge.

To start with, the directors of those entities were a bit unusual. They included drivers, computer technicians, and music composers. While this may be quite possible, one wouldn’t ordinarily expect them to oversee large entities.

But the real thorn in this fact was that SEBI found evidence that they were directors only in name, and not role.

For instance, Bhavesh Wadhel, who was a driver for Future Group, paid ₹15,000 a quarter to be a director of an entity which, by 2021 had ₹333 crore of FRL’s money on its books. Then, Rajesh Sali, who repaired computers for a living, was a director of Unique Malls Private Limited, which held ₹226 crore. They had no role in these entities beyond giving their signature, and none of them had read the papers they signed. They also didn’t attend any meetings — a bare minimum as director.

Additionally, the auditors signed off on the Annual Reports without flagging the entities. The Audit Committee did not know they existed in the form they did.

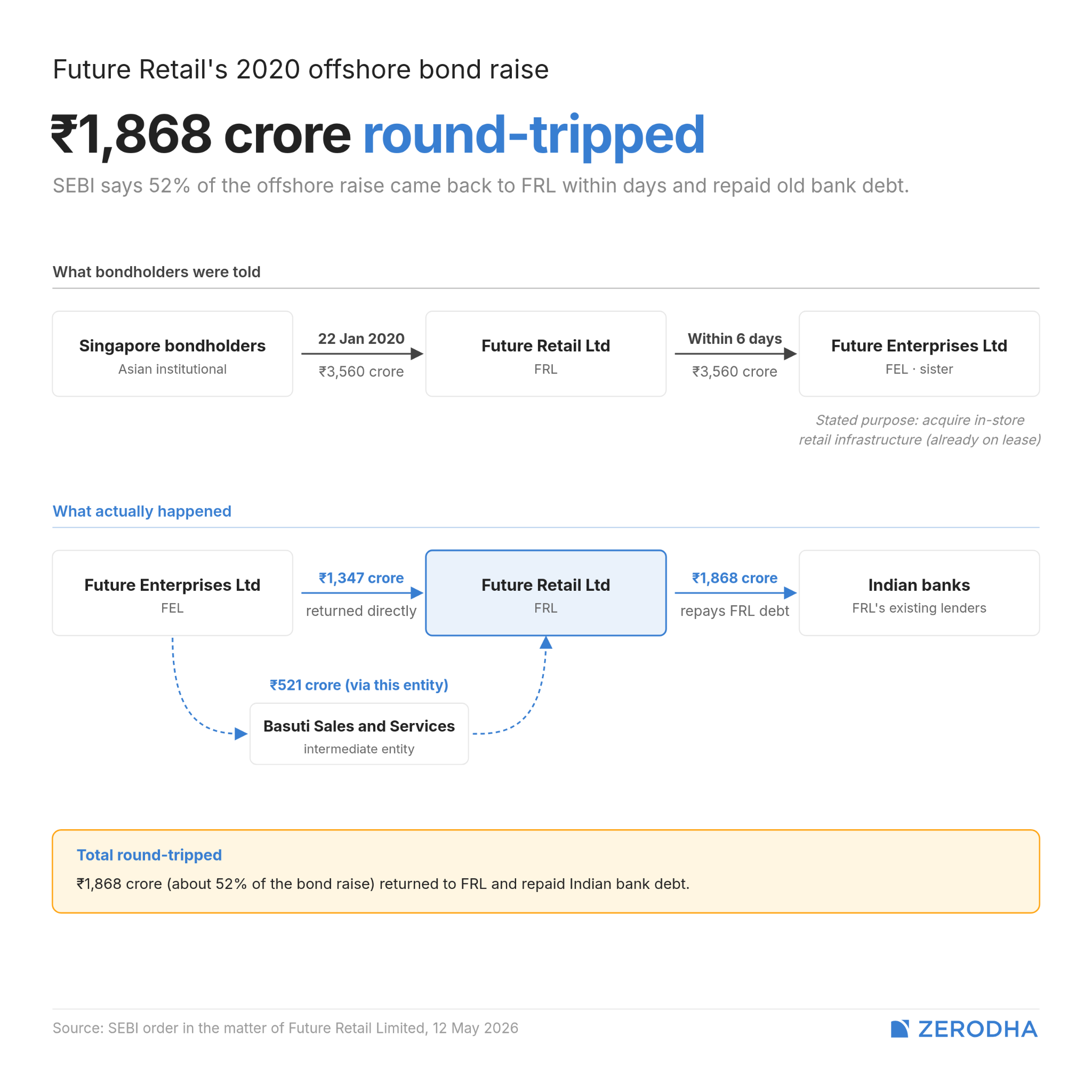

The single transaction that revealed the architecture most clearly was a January 2020 bond raise on the Singapore Exchange for $500 million (~₹3,560 crore at the exchange rate back then). Potential bondholders were told the money would acquire in-store retail infrastructure across India. Six days after ₹3,560 crore landed in FRL’s account, all of it was transferred to FEL, the sister company, as advance payment for that acquisition. The infrastructure was already in Future Retail’s stores on lease.

But over the months that followed, about ₹1,868 crore came back to FRL through layered transfers via FEL, and was used to pay down FRL’s existing debt to Indian banks. That, as per SEBI, wasn’t adequately made transparent to the bondholders.

Reliance’s takeover

By this time, two giant forces were converging on Future Retail.

The first was Amazon, which in August 2019 had invested $200 million in Future Coupons, the promoter entity that ultimately controlled FRL. The shareholder agreement gave Amazon a veto over any sale of FRL to certain “restricted persons“. Notably, that list included Mukesh Ambani.

Which makes the second outside force even more remarkable, because next year, Reliance’s retail arm announced it would acquire Future Group’s retail and wholesale business for ₹24,713 crore. The deal came as a massive lifeline for an indebted business whose health was further worsened by CoVID lockdowns.

Amazon didn’t like this, and successfully filed an injunction at the Singapore International Arbitration Centre. This blocked the Reliance deal from ever formally closing. And while the legal war ran, Future Retail was bleeding cash.

But, by November 2020, the board of FRL seemed to have approved a workaround that could solve everybody’s immediate problem.

The idea was that if FRL couldn’t pay a landlord, that landlord would terminate the lease with FRL. Instead, the landlord would sign a fresh one with a Reliance entity, which would then sub-lease the same premises back to FRL. The landlords got Reliance as a counterparty in place of a defaulting FRL, while Reliance got operational possession of the stores it was already trying to buy. FRL got to keep running its retail business.

Over the next 15 months, it extended to 342 large-format and 493 small-format stores, together about 75 percent of FRL’s retail revenue. Sounds like a win-win-win, right? Yes, but there were two major problems with this.

For one, this arrangement was not disclosed to shareholders.

Secondly, by February 2022, with Amazon’s legal challenges still pending, Reliance concluded it would have to actually act on the operational side regardless of the deal. So, it began terminating the sub-leases unilaterally, and the stores went dark within weeks. On March 16, Future Retail filed a stock exchange disclosure complaining against this sudden closure, and by April, the deal had collapsed in court.

In July that year, the NCLT declared FRL as insolvent, and ordered its liquidation in July 2024 after no resolution plan really worked. Then, eventually, Reliance snapped up operational control of around two hundred Big Bazaar locations, rebranding them under the Reliance Smart Bazaar name.

What SEBI found

Through all of this, SEBI had been investigating. Its probe had begun in 2020, around the time of the Reliance announcement. In July 2024, right before the liquidation was made official, the regulator issued a show-cause notice covering six different categories of charges.

But after 222 pages of reasoning, not much could be made to stick to the Future Group. We won’t cover the dismissal reasons for every charge, but just some of them.

For instance, SEBI alleged fraud charges under Section 12A and the PFUTP Regulations, which cover fraud in dealing with securities. But SEBI could not show that the Annual Reports had induced anyone to deal in FRL’s stock at any particular moment.

Then, SEBI had also alleged that the promoters routed ₹412 crore through promoter-controlled entities to fund their own subscription to a preferential warrant issue by FRL. If true, it would have effectively meant the company was financing its promoters’ fresh share allotment in itself. The Biyanis, however, produced bank statements showing the funds had originated in a separate NCD raise three weeks earlier. SEBI’s order notes that its own forensic auditor had not examined those statements, and the charge was dropped.

Ultimately, the order settled on ₹20 lakh each for Kishore and Rakesh Biyani, and ₹10 lakh for Toshniwal — a total of just ₹50 lakh. These were the three people that, as per SEBI, had full visibility of the network.

Tied hands

Why did so little of what the order describes ended up as being legally punishable? The answer is structural, and the order is unusually candid about it.

See, SEBI is, by mandate, a markets regulator. Its job is to protect investors in securities and to prevent market abuse. It can pursue a listed company that misleads its shareholders through Annual Reports. But the penalty caps for procedural disclosure violations are modest.

It can also pursue such a company for fraud, but the framework requires SEBI to demonstrate inducement to deal in securities, which usually means a measurable impact on the stock price. Misleading shareholders through five years of Annual Reports without a corresponding move in the stock that SEBI’s analysts can point to becomes a regulatory violation, but not necessarily fraud.

Most of the issues raised in SEBI’s order — including questions around off-balance-sheet financing structures, related-party disclosures, and the role of lessor entities — fall into a different regulator’s lane. This is corporate governance territory, where the Companies Act applies, where the Ministry of Corporate Affairs has its own enforcement powers, and where the Serious Fraud Investigation Office can be invoked. But none has engaged visibly with the case so far.

With all that said, what remains for Future Retail is mostly scrap. The liquidator is working through the company’s remaining assets. The Singapore bondholders are pursuing their own legal options. Whether the Serious Fraud Investigation Office will take up the corporate governance side, or whether the Ministry of Corporate Affairs will pursue its own enforcement action, remains unclear.

The empire that took thirty years to build is gone, and the 222-page order published earlier this week is the closest thing to a final word the markets regulator can give. What it leaves behind, more than the ₹50 lakh penalty, is a regulator acknowledging that the framework it has to work with is not quite designed for what failed.

India’s cement sector hits a wall it didn’t build

India’s cement industry had a strong Q4 — companies sold more cement than they ever have. But underneath the headline numbers, the management teams told a more complicated story. Costs spiked from unexpected places, companies started rethinking how much to spend on new capacity, and the fight for better margins pushed them deeper into branding and premium products than the sector has ever gone before.

We looked at the results and concall transcripts of UltraTech, Ambuja and Shree Cement. The cost shock is part of the story, but not all of it. The industry is quietly changing its stance from chasing capacity to defending margins and from announcing new plants to figuring out how to earn from the ones they already have.

The expansion slowdown

For years, the big story in Indian cement has been about who can build the most capacity the fastest. Every quarter, the three biggest players would announce new plants, new targets, bigger numbers. That’s starting to change — and the reasons are different for each company, which tells you something about where the sector really is.

UltraTech is the exception. It crossed 200 million tonnes per annum of installed capacity this quarter, making it the largest cement company in the world outside China. It’s still guiding for ₹8,000–10,000 crore of annual capex, with capacity headed to over 240 million tonnes per annum over the next three years. UltraTech isn’t slowing down on spending.

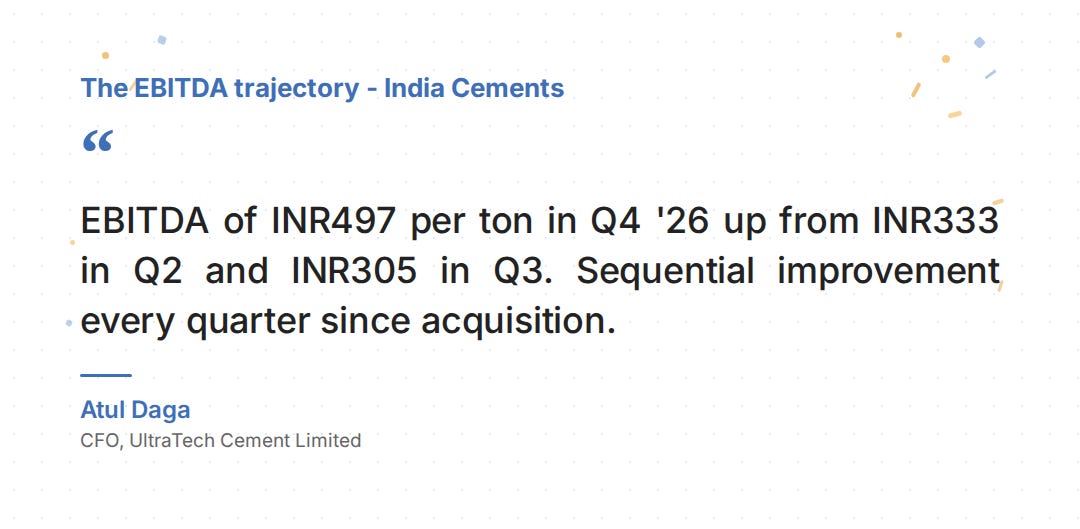

But the more interesting part of its quarter isn’t new factories — it’s the ones it already bought. Both India Cements and Kesoram have been fully rebranded as UltraTech, ahead of schedule. And that rebranding is paying off. India Cements, according to management on the earnings call, went from making ₹333 per tonne in Q2 to ₹497 per tonne by Q4 — same factories, better brand, more money.

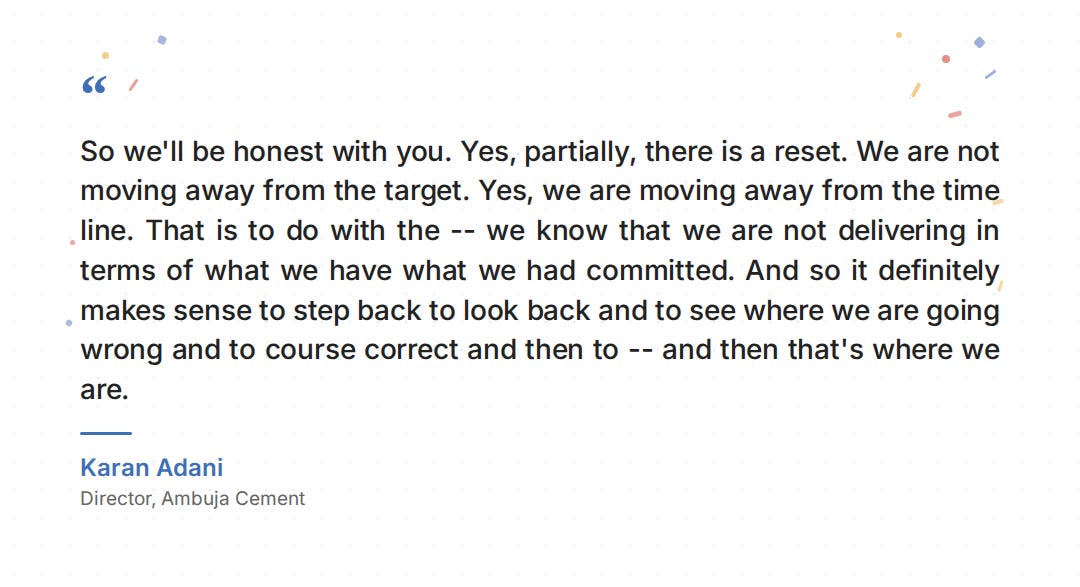

Ambuja’s story is more complicated. When the Adani Group acquired Ambuja and ACC, the ambition was to become the industry leader by doubling the capacity and the volumes. That hasn’t played out as planned. The 155 million tonnes per annum target that was meant for FY28 has been pushed to FY30. FY27 capex has been trimmed.

On the concall, Karan Adani was unusually direct about why the company hasn’t been delivering on its promises. Acquired plants like Penna (46% utilisation) and Sanghi (57%) are still far from running efficiently. There’s been a 3-to-6 month delay on efficiency capex. The honest reading here is that Ambuja went on an acquisition spree, and is now realising that buying capacity is the easy part but making it productive is where the real work begins. Ambuja’s acquisitions, so far, haven’t followed the same path as UltraTech.

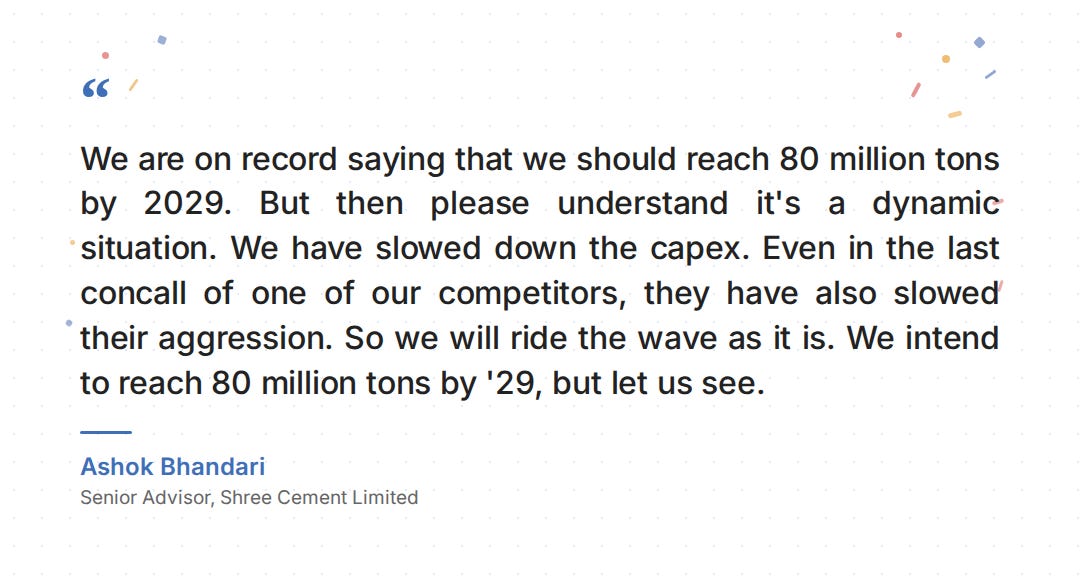

Shree Cement is taking a different approach entirely. It’s the smallest of the three, and it’s choosing not to chase scale right now. FY27 capex guidance is just ₹1,500 crore — earmarked for ready-mix concrete plants, railway sidings and a Meghalaya expansion. Not fresh cement capacity.

The real signal is in what Shree is spending on. It’s railway connections and ready-mix plants, not new cement factories. That suggests the company sees more value in moving and selling cement better than in making more of it.

What does it mean when all three leaders are, in their own ways, rethinking the capacity race? It means the industry has probably added more capacity than demand can absorb in the near term. You don’t need more factories when the ones you have are running at two-thirds capacity. You need to fill them.

The price squeeze

The Q4 numbers look good on paper. UltraTech’s India grey cement volume hit 42.41 million tonnes at 89% utilisation, with EBITDA per tonne at a record ₹1,253. Ambuja hit its highest-ever quarterly volume at 19.9 million tonnes. Shree’s domestic volumes rose 11% year on year. Industry-wide, production grew 8.6% in FY26.

But there’s a gap between what Q4 delivered and what Q1 of FY27 is shaping up to look like. Demand in April and May has softened. Average cement prices were flat at around ₹340 per bag in March 2026, and while companies have tried hiking prices by ₹15–30 per bag in April, it’s hard to make those stick in a fragmented market where buyers can always go to a cheaper brand.

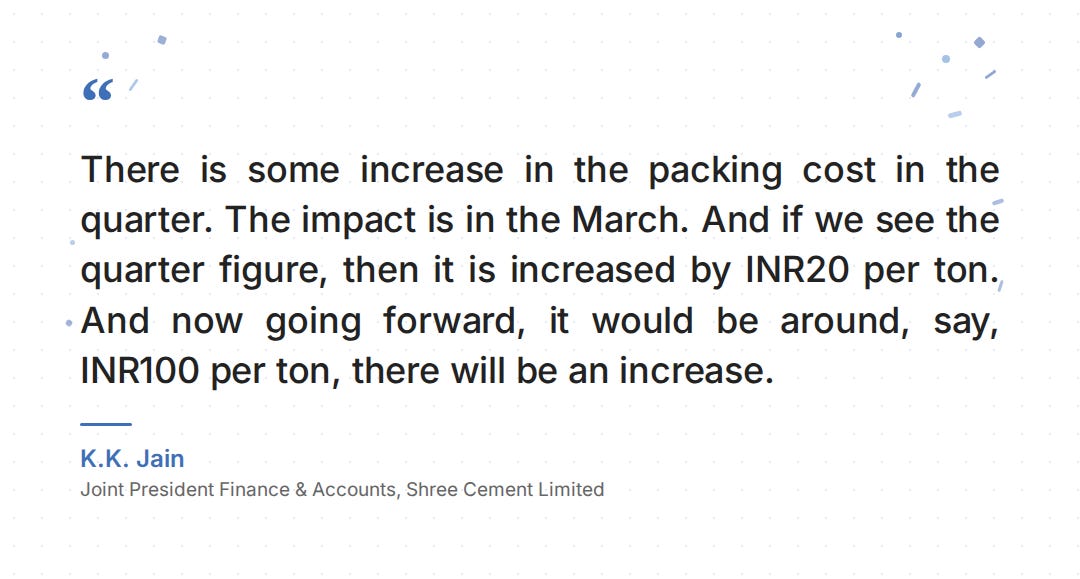

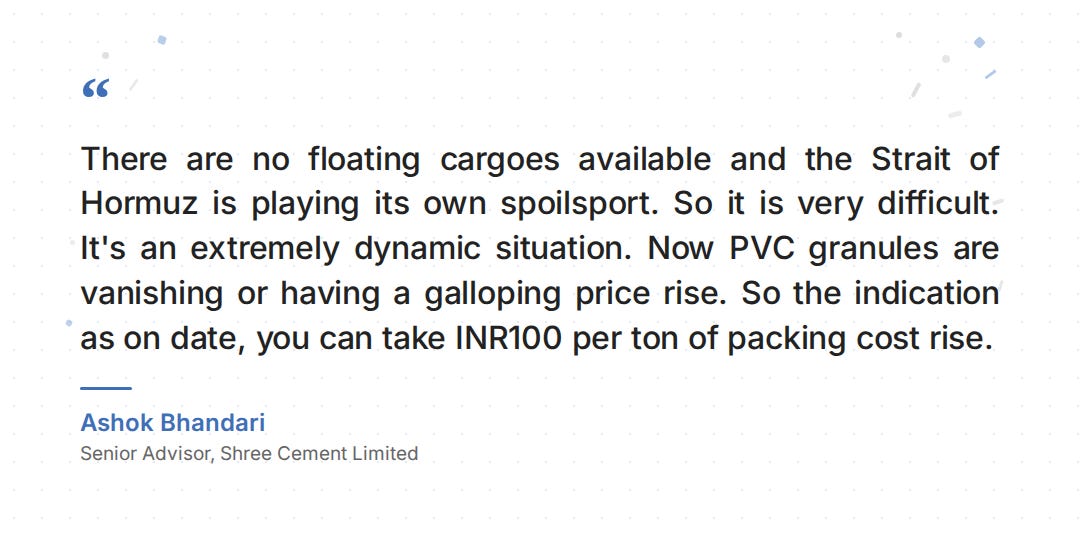

At the same time, costs are rising from multiple directions — fuel, freight, packaging, raw materials. Shree’s management expects another ₹100 per tonne increase going forward.

There’s also a timing problem that makes this harder to read from the outside. Cement companies carry 45 to 90 days of fuel inventory. That fuel isn’t charged at what it cost when it was bought — it’s charged on a weighted-average basis. So when fuel prices spike, the impact doesn’t show up immediately. Every new, expensive shipment gradually pushes up the average cost of the entire stockpile.

That means the March cost shock will keep bleeding into Q1 and Q2 results, even for companies that stocked up early. Shree, for instance, says it never carries less than 90 days of fuel inventory — but even with that buffer, it expects fuel costs to rise 10–12% in Q1.

So companies are entering FY27 squeezed. Managements are flagging softer demand, pricing power is limited, and costs are going up.

The reason bag costs spiked traces back to the West Asia conflict. Propane and butane — the raw materials used to make polypropylene — can also be turned into LPG, which is cooking gas. When the conflict deepened and energy supply fears grew, Gulf refineries chose to prioritise LPG over petrochemical feedstock. Polypropylene supply shrank. Bag manufacturers were getting only 60–70% of their contracted supply, and raw material costs surged nearly 70% in two months.

UltraTech took a ₹90 crore hit on packaging in March alone. That was concentrated in a single month — not spread across the quarter. Ambuja said the shock hit mostly in the last week of February through March, and that it cost the company some volumes too — bags were both expensive and hard to get. Shree’s guidance was the most specific: packing costs rose ₹20 per tonne in Q4, with another ₹100 per tonne expected in Q1. And the problem isn’t limited to polypropylene — PVC granules, used in other packaging materials, are also becoming scarce.

The other cost pressures are at least partially manageable. Companies can switch between petcoke, coal and alternative fuels to control energy costs, and both Shree (61% green power) and UltraTech (43%) have been investing in renewables for years. Freight can be brought down over time by moving more cement by rail instead of road.

Packaging is different. Most Indian cement still moves in 50-kg bags through the retail channel — the same channel all three companies are trying to grow — and when the raw material for those bags dries up because of a conflict thousands of kilometres away, there isn’t much a cement company can do about it in the short term.

The branding play

If pricing power is weak and costs are climbing, companies need another way to improve what they earn per tonne. That’s where branding comes in.

Cement reaches customers through two channels. Trade sales go to retail dealers, who sell to individual home-builders and small contractors. Non-trade sales go in bulk to large builders, infrastructure projects and government contracts. Trade is more profitable because it’s brand-driven — a homeowner building a house will pay a premium for a name they recognise and trust.

Non-trade is won on price, often through competitive bidding, which means thinner margins. Within trade, premium cement — higher-grade products marketed for specific uses like waterproofing or high-strength construction — commands ₹20–25 more per bag than regular cement.

This is why all three companies are pushing to increase their trade and premium mix — it’s the only reliable way to improve what you earn per tonne when you can’t raise prices across the board.

UltraTech’s play is integration. Now that India Cements and Kesoram are fully rebranded, those volumes are being pushed through UltraTech’s stronger retail dealer network instead of lower-margin bulk channels. Trade sales rose to about 66% in Q4, up from 64% the previous quarter — a direct result of the acquired volumes getting access to better distribution.

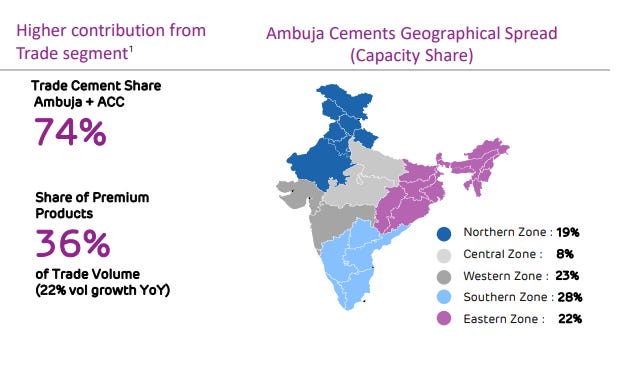

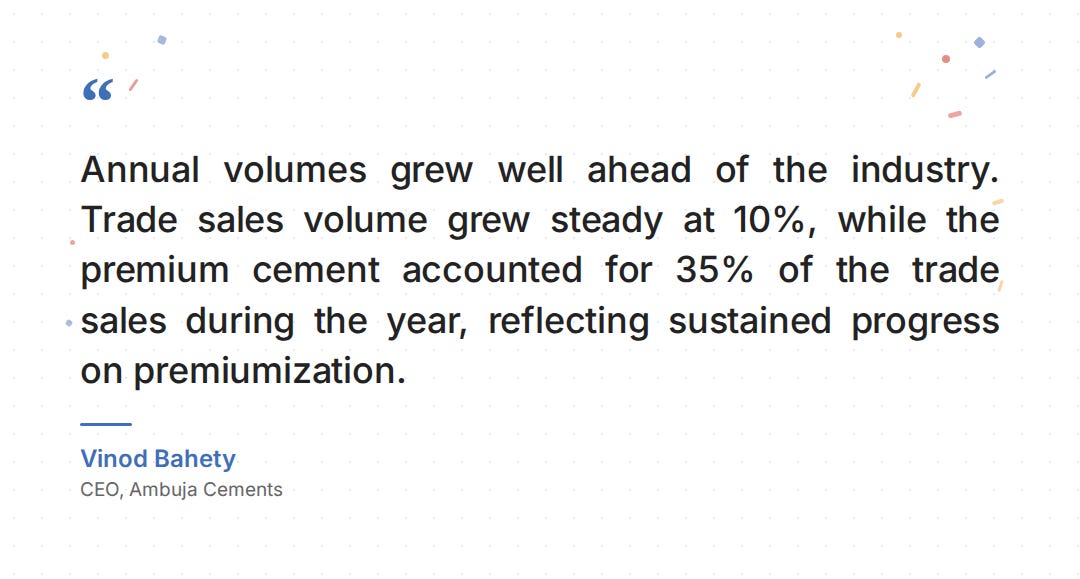

Ambuja is pushing even harder. Trade sales jumped to 74% from 68% the previous quarter, and premium cement reached 36% of trade sales, and annual volumes grew well ahead of the industry.

But the question is whether all of that is translating into better prices. The price Ambuja gets per bag had barely moved quarter on quarter, even though it’s selling more premium cement than before. The problem is the same the broader market can’t hold price hikes, even selling more premium product doesn’t automatically mean earning more per bag. Ambuja spent roughly ₹70 per tonne on branding in FY26, a bet that only pays off once the price per bag starts moving up too.

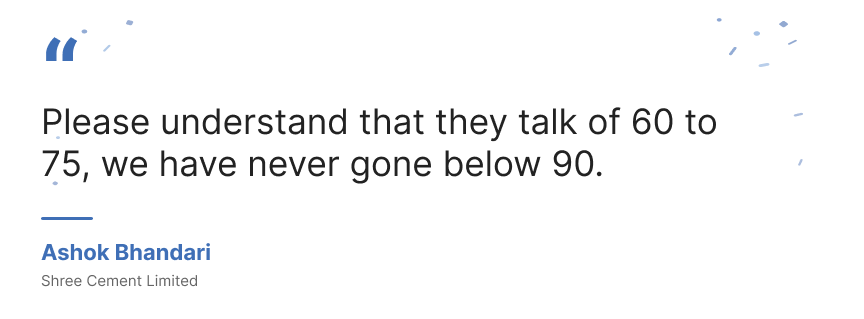

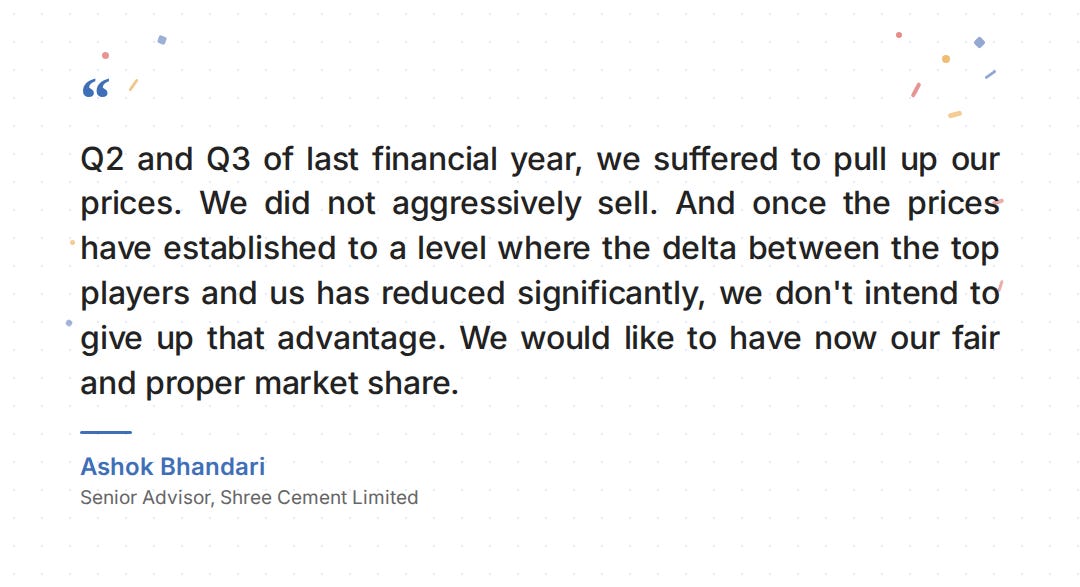

Shree took a more deliberate approach. Over the past two years, it raised premium products from 15% to 22% of trade volume. But in Q2 and Q3, it deliberately held back on selling aggressively — sacrificing some volume to close the pricing gap with UltraTech by about ₹15–20 per bag. Once that price point was established, it chased volume in Q4 and sales rose 11%. The risk here is that Shree’s trade share actually fell to a multi-quarter low of 64% in Q4, which suggests the volume push came partly through the lower-margin non-trade channel. So Shree gained on price architecture but may have given up some ground on mix.

What comes next

ICRA expects profitability to moderate in FY27 as rising input costs eat into margins. Two things will decide whether that plays out. First, monsoon — IMD’s early forecast projects rainfall at 92% of the long-term average, which is below normal, and two of the three companies have already flagged it as a risk. Weak rains hurt rural incomes, and rural housing is a significant source of cement demand — so even though heavy monsoons slow construction directly, a poor monsoon can dent demand from the other end.

Second, West Asia — if tensions ease, bag, fuel and freight costs could soften faster than anyone currently expects. If they don’t, the margin squeeze only gets tighter. Either way, FY27 will be the year the industry finds out whether all the capacity it built over the past few years can actually earn.

Tidbits

1. India’s goods exports robust in Apr despite supply chain disruption

India’s merchandise exports as well as imports for April surged in double digits despite the supply chain disruption amid the ongoing conflict in West Asia following the joint attack by the US and Israel on Iran in February.

Source- Business Standard

2. Iranian Foreign Minister says Hormuz open to all except those at war with Iran

While addressing the intensifying maritime crisis in West Asia, Iranian Foreign Minister Seyyed Abbas Araghchi on Friday clarified that the Strait of Hormuz remains accessible to global shipping, with the sole exception of vessels from nations “at war with” Tehran.

Source- Hindu BusinessLine

3. India’s free trade deal with Britain hits steel hurdle before rollout

India’s free trade deal with Britain, initially expected to be implemented by May, has hit an expected hurdle over the UK’s new steel import curbs, India’s trade secretary Rajesh Agrawal said on Friday.

Source- Reuters

- This edition of the newsletter was written by Aakanksha and Vignesh.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Kyle Chan on China’s industrial power and entrepreneurship

If you enjoy The Daily Brief, here’s something we bet you’ll like. We recently spoke to Kyle Chan, one of the sharpest minds we read to understand China - we’ve often featured his insights on The Daily Brief. Our conversation dives deep into the dynamics that shape China’s manufacturing landscape. It goes into the nature of Chinese entrepreneurship, how China’s price wars affect innovation (and vice versa), why China’s policies are far less all-knowing than people assume, and how China wields its manufacturing prowess as a geopolitical power. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉