Here's how DMart works

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Is DMart doing well?

Is India bad at being China?

Is DMart doing well?

DMart, as we all know, is one of the largest value retail chains in India. Their quarterly numbers just came out, and there’s been a lot of buzz about it—and rightly so, considering how big they are. With a market cap of over ₹2 lakh crore and a price-to-earnings (PE) ratio of more than 80, they’re a major player. But instead of diving straight into the results, we thought it’d be better to first look at DMart’s business model and what makes it tick.

DMart’s success boils down to a simple yet powerful insight: Indians are value-conscious, and we love discounts. Their strategy is built around this core idea.

DMart follows the “Everyday Low Cost - Everyday Low Price” (EDLC-EDLP) model. This means they focus on procuring goods at the most competitive prices, achieving efficiency in operations and distribution, and passing those savings on to customers by offering consistently low prices. In short, they deliver value for money in a way that keeps customers coming back.

Here’s how DMart’s model works in practice: They buy in bulk and pay their suppliers quickly. This gives them the upper hand in negotiations, allowing them to get better deals—lower prices, bigger discounts, and faster deliveries. Unlike many other retailers that delay payments to vendors, DMart has built strong trust with its suppliers. In return, they get favorable terms.

Another part of their strategy is selling their own products, known as private labels. These private labels offer better margins because DMart controls the manufacturing process and cuts out the middlemen.

The cost savings from all this are passed directly to customers. It’s not about flashy discounts during sales—it’s about keeping everyday prices so low that people know DMart is the best place to shop.

But that’s not the only way they save money. DMart owns most of its stores instead of renting them. Renting retail space, especially in metro cities, can be very expensive. By owning their properties, DMart protects itself from rising rental costs. Their stores are also designed to maximize space, packing in as many products as possible while keeping costs low. This allows them to sell more while spending less.

Another key part of DMart’s strategy is its cluster-based expansion. Instead of opening stores randomly across the country, they focus on growing in specific regions, one cluster at a time. This approach helps them streamline operations, improve supply chain efficiency, and build brand loyalty in each area. It’s a deliberate, slow-and-steady strategy that ensures they grow sustainably without overstretching.

Finally, DMart’s throughput—how much product they sell per square foot—is another factor that sets them apart. Their stores consistently generate some of the highest sales per square foot in the retail industry because they focus on stocking fast-moving, high-demand items.

Every inch of store space is optimized to move products quickly and efficiently, which is critical for their low-margin, high-volume model. Their shelves are packed with everyday essentials like groceries, cleaning products, and household goods—things people need regularly. This keeps customers coming back again and again. For DMart, it’s all about volume: selling a lot of products, even if the profit margin on each item is small.

That said, things aren’t perfect for DMart. There’s been growing chatter about how quick commerce is starting to impact their business. DMart’s core strength has always been customer loyalty, but with more people prioritizing convenience over cost, it’ll be interesting to see how they adapt to this challenge.

Now, let’s dive into their quarterly results to see how they’re holding up in this changing landscape.

For Q3 FY25, DMart reported revenue growth of 17.5% year-on-year, reaching ₹15,973 crore. Their net profit stood at ₹724 crore, reflecting a year-on-year growth of about 5%. While the top line looks strong, the margins tell a different story.

DMart’s net profit margin dropped to 4.53%, down from 5.09% a year ago and 4.57% in the previous quarter. The management pointed to “increased discounting in the FMCG category” as one of the main reasons for this margin squeeze.

The same-store sales growth (SSSG), an important metric for retailers, stood at 8.3% for stores older than two years. This is a decent recovery compared to the last quarter but still reflects the pressure of a challenging economic environment.

Several factors have impacted margins.

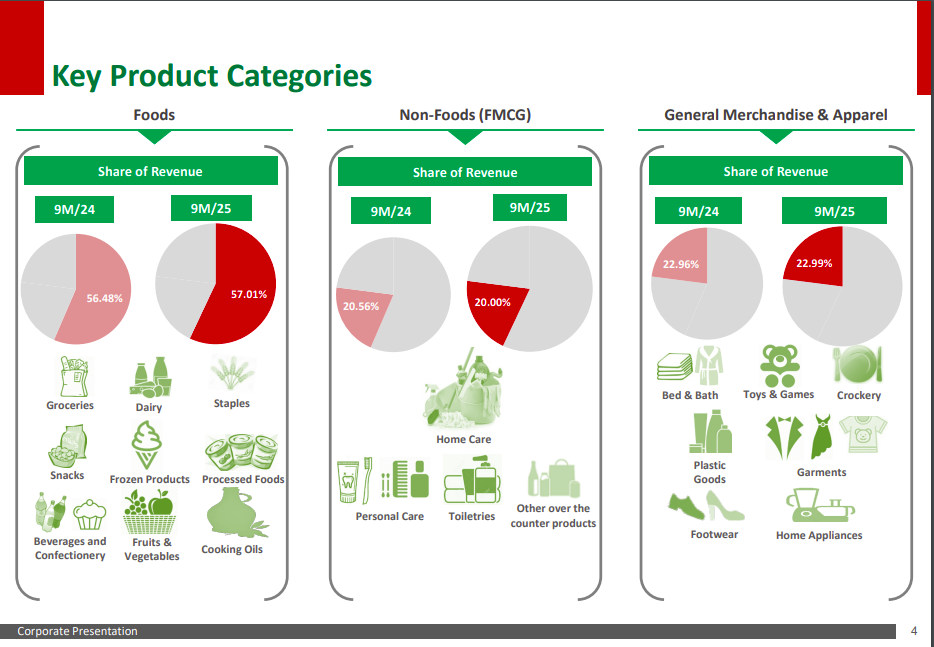

First, the rising share of low-margin food and FMCG products in DMart’s sales mix continues to weigh on overall profitability. Categories like general merchandise and apparel, which typically have higher margins, have seen stagnant growth. In other words, DMart isn’t selling enough high-margin items to balance out the growing share of essential, low-margin products.

Secondly, higher discounting by FMCG companies to stay competitive in metro markets has further squeezed DMart’s margins, as we mentioned earlier.

DMart’s rapid expansion has also added to cost pressures. They opened 10 new stores this quarter, bringing their total store count to 387. While this growth is important, new stores take time to mature and start contributing meaningfully to profits. For now, they add to operating expenses.

Now, let’s talk about quick commerce and how it’s impacting DMart. The rise of players like Blinkit, Zepto, and Swiggy Instamart has changed the way urban customers shop for groceries. For some, convenience is becoming more important than cost. DMart has responded with DMart Ready, its e-commerce arm, which has shown a 21.5% growth year-to-date in FY25.

However, shifting to e-commerce is tricky for a low-margin business like DMart’s. Home delivery significantly increases operational costs compared to the in-store model. In their earnings release, DMart acknowledged this, saying:

"In the rapidly evolving dynamics of the grocery e-commerce market, we are seeing significantly more demand for home delivery compared to pick-up points, and we continue to align our business accordingly."

One last update—they announced that DMart’s CEO, Neville Noronha, is stepping down after more than two decades with the company. Anshul Asawa, a former Unilever veteran, will take his place.

Is India bad at being China?

Over the last century, many ideas shaped the global political economy. One of the most prominent was globalization. When a financial crisis hit India in the early 1990s, the government introduced the New Economic Policy of 1991, which leaned heavily on these growing global trends.

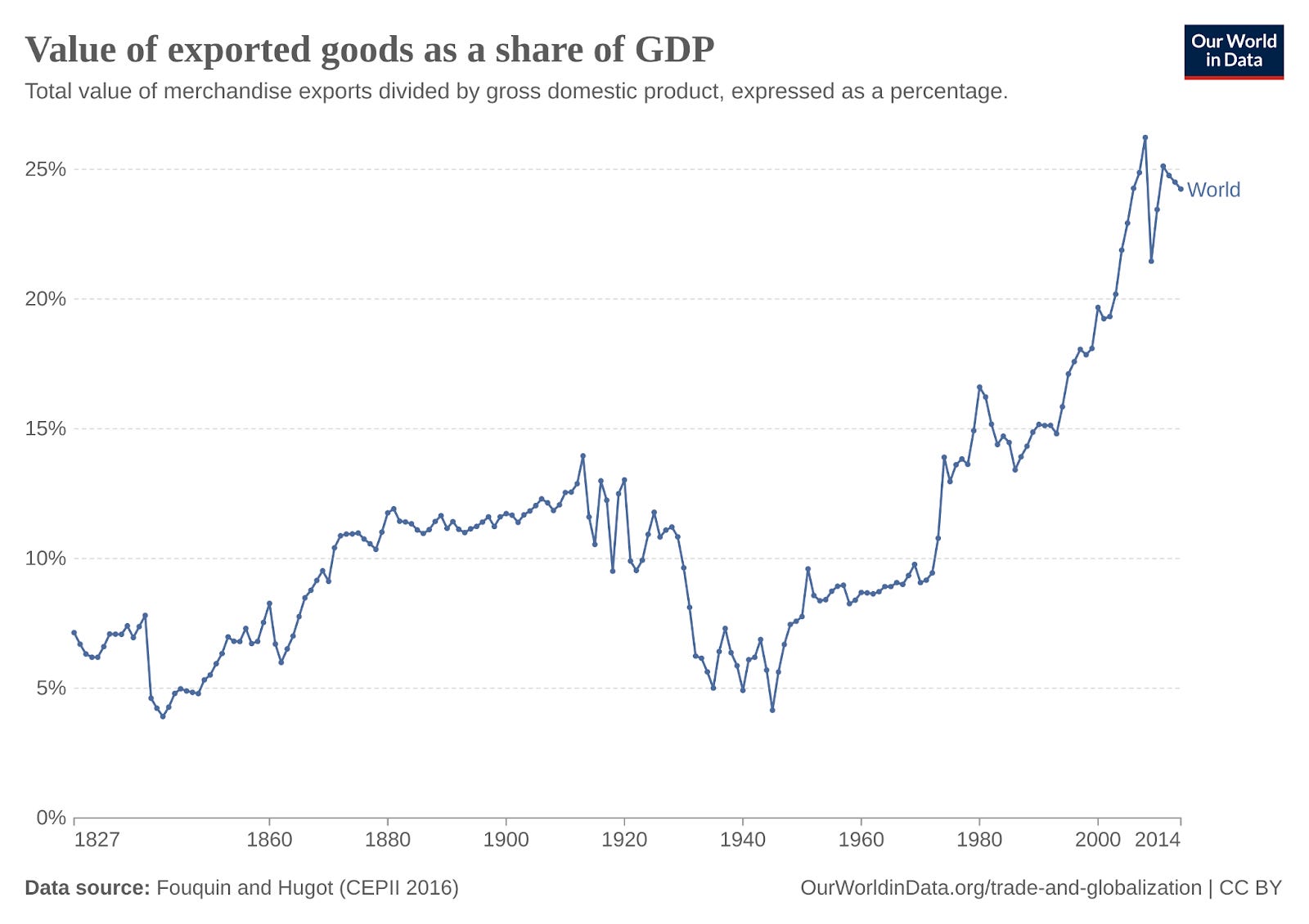

Since then, globalization has only gained momentum. One way to see this is by looking at exports as a share of the world’s GDP. In the 1990s, exports made up about 15% of global GDP. Today, that number is closer to 25%. Many countries have benefited from this shift, but it seems like things might have gone a bit too far.

Between the 1990s and 2008, the world entered what the World Economic Forum calls a phase of “hyperglobalization.” But then came a series of shocks—the 2008 financial crisis, trade wars, frustrated middle classes in developed countries, and growing concerns about relying too much on single trade partners. Together, these factors slowed globalization down to a trickle, a phase often called “slowbalization.”

Now, we’re seeing a shift toward “deglobalization.” The COVID-19 pandemic, the war in Ukraine, widening ideological divides, and the global push for greener economies have made governments and companies rethink their reliance on overseas suppliers. Many are now focusing on “building at home” or working only with trusted partners to ensure stability.

This trend is visible everywhere. In India, it’s called ‘Atmanirbhar Bharat.’ In the European Union, it’s known as ‘Strategic Autonomy.’ In the United States, it’s framed as ‘America First.’ Different names, but the same idea: focusing on self-reliance and closer partnerships. This shift is bringing significant changes both at home and on the global stage. Today, we want to take a closer look at India’s approach to this transformation.

India has plenty of reasons to strengthen its self-reliance, with energy being one of the most important. We are one of the world’s biggest markets for crude oil and solar panels, yet we still depend heavily on imports. Another key area is electronics and semiconductors, where the government’s efforts are starting to make a real impact.

Thanks to programs like the Scheme for Promotion of Manufacturing of Electronic Components and Semiconductors (SPECS), the India Semiconductor Mission, and partnerships with global companies, we’ve made great progress. In fact, we’re now producing enough electronics to meet most of our own needs. On top of that, our exports of electronic products have nearly tripled between FY22 and FY24.

A big part of this growth comes from smartphones. Just last year, headlines proudly announced that India was assembling 1 out of every 7 iPhones—a milestone we covered in The Daily Brief.

With the launch of the iPhone 16, Indian-made iPhones hit global shelves on the same day as those made in China. For the first time, India also produced the advanced Pro and Pro Max models. This shows that Foxconn, Apple’s contract manufacturer, is gaining confidence in India as a manufacturing hub and even sees it as a potential alternative to China.

Naturally, China isn’t happy. Losing business to a rival—especially one they’re not on great terms with—is tough for anyone. A report from Rest of the World claims that Chinese staff are struggling to get visas to work at Foxconn’s India plants, and those already stationed here are being called back. There are also rumors that shipments of specialized equipment are being delayed. Apple and Foxconn haven’t confirmed any of this, so it’s worth taking with a grain of salt. But if these claims are true, they could seriously disrupt India’s mobile manufacturing progress.

The bigger issue here is the importance of knowledge and technology transfer for any growing industry. India hasn’t been making iPhones for very long, while Foxconn’s teams in China have had years of experience perfecting the process. For India to succeed, Foxconn will need to share that expertise with its Indian teams.

That’s exactly how China became the “factory of the world.” They welcomed foreign companies to set up operations there, offering cheap labor, but only on the condition that technology transfer took place locally. If India wants to achieve true Atmanirbharta (self-reliance), it will need to follow a similar strategy.

If these reports about China blocking technology transfer are true, it’s a challenge India will have to tackle head-on. Overcoming it will be crucial for building a strong and competitive manufacturing industry.

We’ve seen a similar story play out in the U.S. as well. Determined to reduce its dependence on foreign semiconductors, America—ironically, the birthplace of semiconductors—watched its share of global manufacturing capacity shrink from 37% in 1990 to just 10% by 2022. This happened largely because other countries invested heavily in chip manufacturing incentives, while the U.S. government didn’t.

To turn things around, Washington passed the CHIPS Act, convinced TSMC to invest $65 billion, and secured a commitment from them to build three semiconductor factories (fabs) in the U.S. by the end of the decade. But progress has been slow. It’s only recently that the first fab has finally gone live after facing several delays—mostly due to a shortage of skilled workers. The U.S. had to rely on Taiwanese experts to set up the processes, but it seems the worst of those challenges is now behind them.

All in all, while many countries want to move toward deglobalization, the reality is that they still need foreign partners. Our economies are so deeply interconnected that going it alone isn’t easy. If India wants to follow in China’s footsteps and become largely self-reliant, it will have to play the same game China did. That means negotiating—or even pushing—for technology transfers.

Without that, the dream of true self-reliance could slip away. Technology and expertise are essential to building industries that can stand on their own. If we want to make this vision a reality, we’ll need to learn from others and bring their knowledge here.

Tidbits

Zomato and Swiggy are in the spotlight for their private-label ventures—Bistro for Zomato and Snacc for Swiggy. Industry groups like the Federation of Hotel & Restaurant Associations of India (FHRAI) and the National Restaurant Association of India (NRAI) have raised concerns that these services may be using data from partner restaurants to promote their own products. They’re also worried about food safety and unfair competition. This issue might soon reach the Commerce Ministry and the Competition Commission of India (CCI).

Coal India is exploring lithium brine assets in Argentina. It’s partnering with Indian Rare Earths Limited (IREL) to secure critical minerals. This is a big step for India’s renewable energy goals, as it helps Coal India reduce its dependence on fossil fuels. Accessing lithium and other essential minerals will also give the company a strong foothold in the growing green economy.

The Indian rupee recently hit a record low of ₹86 against the US dollar. This drop is mainly due to foreign investors pulling out their money and the dollar’s strong performance. A weaker rupee is a mixed bag—it benefits exporters because their goods become cheaper overseas, making imports more expensive. This drives up inflation, making everyday life costlier for households. Businesses are feeling the pinch too, as the higher cost of importing raw materials puts more pressure on their expenses and affects overall market sentiment.

-This edition of the newsletter was written by Krishna and Kashish

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉 Join the discussion on today’s edition here.

Good Information provided.

I’ve become a Blinkit person, but my mom still chooses DMart 🙃