GIFT City, Explained: What We’ve Learned Running a Fund There

By Nishit Shah and Ankush Datar — Phillip Capital

Hi, I’m Kashish. GIFT City keeps coming up in conversations among colleagues, in the news, on investor forums but most of the coverage stays at the policy level. I wanted to understand how it actually works from the perspective of someone running money through it. Specifically, the wealth management side with details about onboarding, fund structures, tax mechanics, the day-to-day of it.

That’s when we reached out to Phillip Capital, who walked us through everything. This article is based on that conversation. It was originally published on Subtext by Zerodha.

You can also listen to it on Spotify or Apple Podcast.

──────────────────────────────────────────────────────

We, through our presence in GIFT City, namely, Phillip Ventures IFSC Pvt. Ltd , run the Phillip India Billion Opportunities Fund, an open ended CAT-III AIF for onboarding NRI and foreign national clients for investments into India and our firm also runs a Global PMS managing outbound investments as well.. Here’s what we’ve learned, stripped of the jargon.

Why does GIFT City even exist?

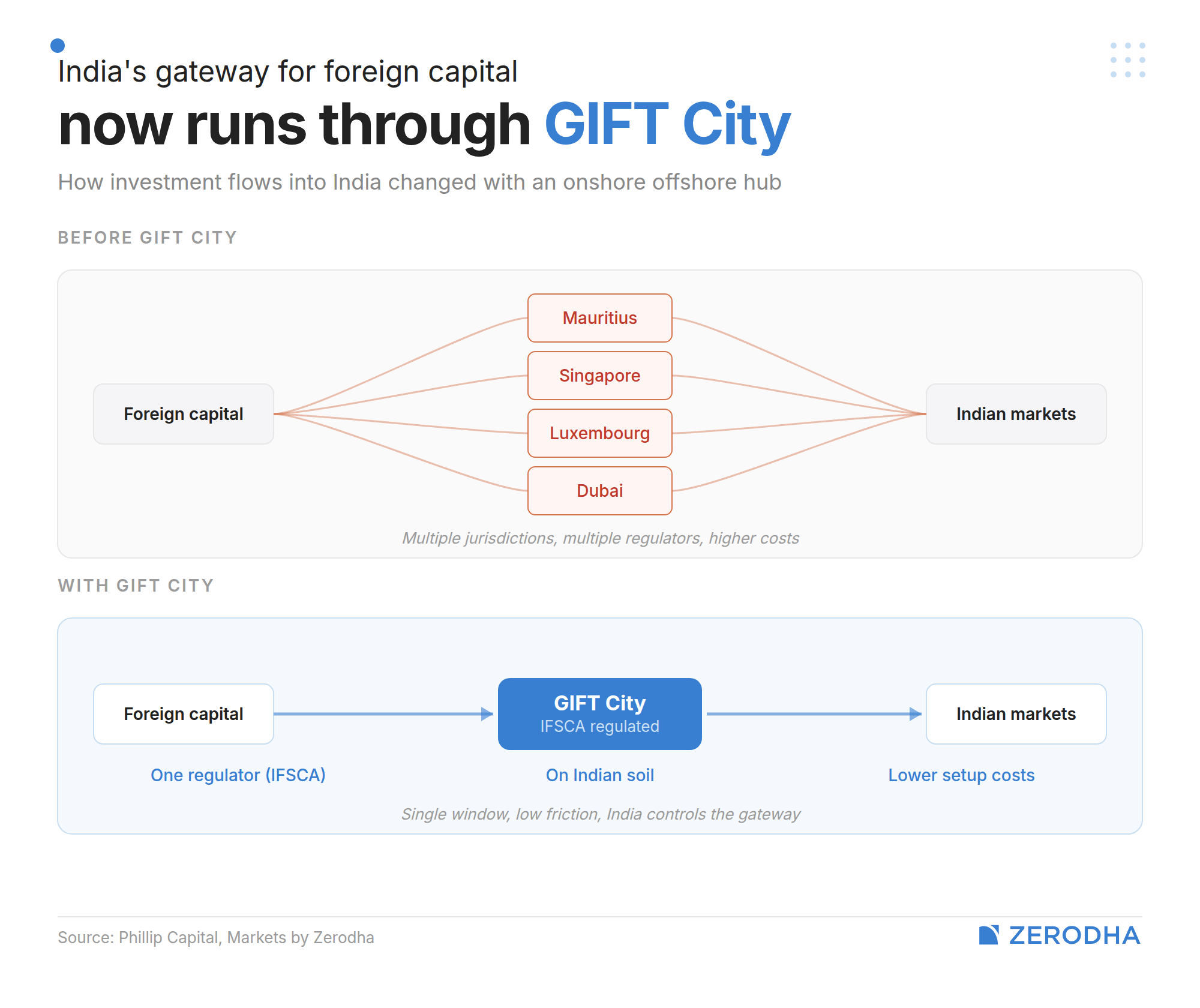

The short version: India didn’t have its own offshore financial jurisdiction. For decades, if large foreign capital wanted to enter India — or if Indians wanted to invest globally — the investments had to be made through Mauritius, Singapore, Luxembourg, or Dubai. Those jurisdictions offered something India’s domestic system simply couldn’t — a single-window, low-friction way to move capital.

If a foreign investor wanted to invest directly into India, they’d have to apply for a PAN card, register as an FPI, open local bank accounts, and start filing Indian tax returns. For an NRI, it meant getting an OCI card, opening NRE/NRO accounts and setting up a PIS account. This is a maze of paperwork across multiple regulators. Most foreign capital looked at that and routed through Mauritius or Singapore instead, where the fund structures were simpler, onboarding was faster, and the regulatory interface was a single entity rather than a patchwork of coordinating with multiple regulators and authorities.

GIFT City wanted to solve that. It was originally the brainchild of Mr. Modi during his time as Chief Minister of Gujarat. When he became Prime Minister, it took real shape. The idea was straightforward — why should India’s financial gateway sit in someone else’s country?

Think of GIFT City as India’s answer to the DIFC in Dubai or the financial centres of Singapore and Mauritius. It sits physically between Ahmedabad and Gandhinagar, but legally, it operates as a Special Economic Zone with its own regulator — the IFSCA (International Financial Services Centres Authority). Though technically on Indian soil, it functions as an offshore jurisdiction.

The real problem it solves

Forget the grand narrative for a moment. The single biggest thing GIFT City does is eliminate friction.

Let us give you a concrete example from our own business. At Phillip Capital, over 30% of our PMS assets under management comes from NRI clients. To onboard an NRI through the traditional domestic route, the process takes 30 to 45 days . As we shared earlier, the client needs a PAN card, an OCI card, a savings bank account, a PIS account, a trading account, a demat account, and finally a PMS account. That’s 50 to 60 signatures across forms. If someone signs in blue ink one time and black the next, the bank rejects it. It’s a grind.

Through our GIFT City fund? Onboarding takes two to three days. No PAN card needed. No OCI card needed. No PIS account. Minimal documentation. For second and third-generation NRIs who may not even hold an OCI card, this is a game-changer.

Now scale that logic to a foreign national, say, someone sitting in London or New York who’s bullish on India. Before the inception of GIFT City, they would need to register as an FPI, get a PAN card, open local bank accounts, and start filing Indian tax returns when choosing a route to invest. Most of them look at that and say: why bother? In contrast, through a GIFT City fund structure, all of that goes away. The fund handles the operational complexity. The investor just invests.

Adding to that, in India, you need to deal with multiple regulators & authorities. In GIFT City, there’s one unified regulator: IFSCA. For operators like us, that alone simplifies life furthermore.

What’s encouraging is that IFSCA has been proactive. They’ve been allowing innovation for new products, new regulations, and studying global best practices. They’re stringent — they don’t want GIFT City to earn a bad reputation — but they’re also pragmatic and forward-looking. The traction from global banks, family offices, and domestic fund houses setting up shop there is the proof of things going well. After recent geopolitical events in the Middle East, we even saw a rush of NRIs wanting to open a bank account in GIFT City as a safer alternative.

One more operational advantage worth mentioning is cost. Setting up a fund in, say, Singapore or Mauritius means paying legal counsel in dollars. Skilled manpower is expensive and harder to access. But, GIFT City, being in India, brings all of those costs down significantly while still operating under the highest international standards.

Money going out: The outbound story

For Indian residents wanting global exposure, GIFT City has opened doors for investors to invest globally through regulated fund management entities in India, which was not possible earlier due to there being no platform for the fund managers to set up shop.

Before GIFT City, your options were limited. You could invest in a domestic mutual fund that ran an international fund-of-fund — say, a Nasdaq ETF or a Hang Seng fund. That worked until the RBI’s aggregate industry limits were breached, after which many fund houses stopped accepting fresh inflows into international schemes. Or, if you had serious money — $100,000 or $200,000 — you could open an account in Singapore or the US directly. For smaller amounts there were limited avenues.

GIFT City changes that.

Through our platform, for example, we now offer access to US-listed equities. Even with $5,000 or $10,000, you can start building a global portfolio. Previously you would have to open an account with a broker who would be having a third party arrangement with an external broker to give you access to the global markets. LRS limits still apply though — you’re capped at $250,000 per person per year for remittances — but those limits are generous enough for most individual investors.

And since your investments in GIFT City are denominated in dollars, you automatically get a currency hedge. The Indian rupee has historically depreciated against the dollar by roughly 3-4% annually on average — and over the last 15 months, the depreciation has been steeper. That tailwind adds up over time.

Beyond individual stock access, the fund management ecosystem is growing as well

Let us explain. Say, an Indian AMC sets up a fund in GIFT City, and that fund — the “feeder” — pools investor money and channels it into a larger global fund or directly into overseas securities. As an investor, your experience feels familiar, since you’re investing in a fund run by a brand you recognize, in a regulated setup. But behind the scenes, your money is being deployed globally through GIFT City’s infrastructure. It’s essentially the same idea as the Nasdaq or S&P fund-of-funds that domestic AMCs used to run, except it’s domiciled in GIFT City instead of onshore India.

And that distinction matters, because unlike domestic fund-of-funds, these aren’t subject to the same RBI industry-wide caps that forced so many international schemes to stop accepting fresh money. And as the ecosystem matures, investors should expect thematic exposure too, not just broad S&P 500 or Nasdaq funds, with narrower slices like AI, cloud computing, or medical devices that don’t have listed equivalents in India.

Money coming in: The inbound story

Local AMCs have been especially active because they already have NRI client bases and are now offering these clients a far smoother onboarding and investment experience through GIFT City structures. As we explained in the start of the article, there are multiple operational benefits for a foreign national or NRI to choose the GIFT city route to invest.

The vehicles being used are primarily AIFs — Category I, II, and III. We specifically run a Category 3 III open ended AIF. Global family offices are also increasingly setting up in GIFT City, drawn by the presence of global banks, the regulatory clarity, and — frankly — by how well India’s growth story is selling internationally right now, especially with recent valuation corrections making the market more attractive.

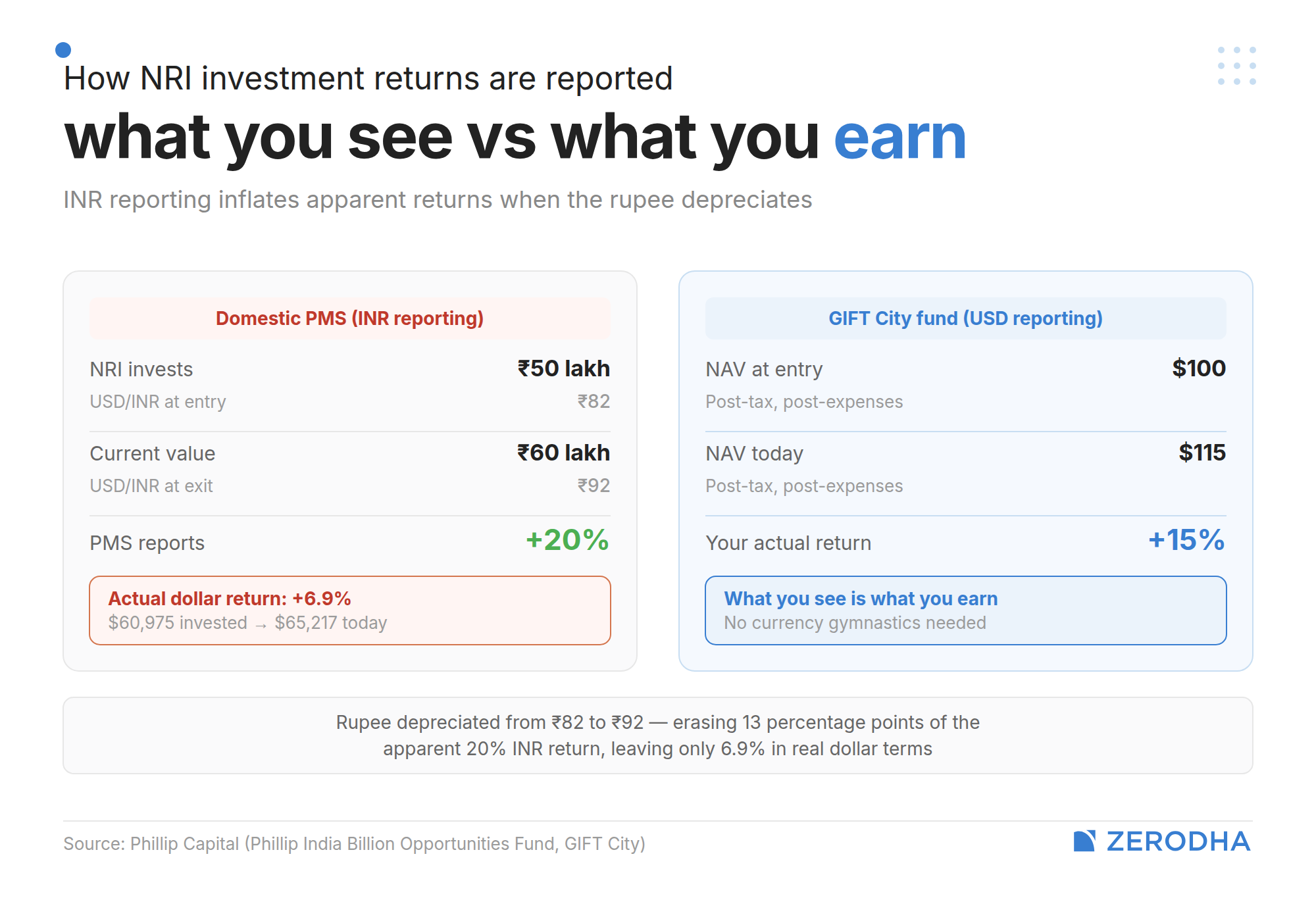

A practical advantage for inbound investors currently is reporting. When an NRI invests through our domestic PMS, we report returns in rupee terms. But the client remitted dollars. If the rupee depreciates between the time they invested and the time they exit, their dollar-denominated return is lower than what our INR reporting shows. This creates confusion.

Through our GIFT City fund, the NAV is published in dollar terms, post-tax, post-expenses. What you see is what you actually earned. No mental currency gymnastics.

The Tax Reality

This is the single biggest misconception we encounter, and we partly blame WhatsApp University for it. GIFT City is not tax-free.

If you’re an Indian resident investing through a GIFT City fund into global securities, you still owe capital gains tax in India. You must report your income and pay up, same as any other investment. What is different though, is that there’s no GST on management fees and other charges levied within GIFT City. That’s some savings for investors, but it’s not “zero tax.”

For NRIs, the advantage is more tangible. When an NRI invests directly in Indian stocks, TDS gets deducted by the bank, and they must file Indian tax returns at year-end. Through a GIFT City fund, the fund itself handles Indian taxation at the fund level. The NRI investor doesn’t need to file returns in India, but file in their country of residence.

If that country is the UAE, where there’s no capital gains tax, they effectively pay only the Indian tax at the fund level and nothing more. If they’re based in any other country, where for example the short-term capital gain tax is 25%, and the Indian tax already paid at the fund level is 20%, they only owe the 5% differential in that country as India has DTAA with several countries. This is just a broad example of how it works and clients should consult with their tax advisors for a more granular understanding.

So, Should You, a Retail Investor, Care?

Yes, but with a caveat.

We always tell our clients: it’s not India or global. It’s India and global. Over the last 15-18 months, global markets have significantly outperformed Indian markets. That’s a reminder of why diversification matters.

GIFT City gives you a regulated, accessible vehicle to get that global exposure. You can open a bank account there, hold assets in dollar terms, and invest in a growing range of funds and direct equity options. For retail investors, the mutual fund feeder route through GIFT City is probably the most practical starting point, especially since many domestic international fund schemes remain closed to new inflows.

But don’t go overboard. A small, consistent allocation to global assets is the right approach. The temptation to shift everything offshore when global markets are running is a mistake. Think of it as diversification, not a switch.

The proof of concept is established, the volumes are growing across products, and the regulator has earned credibility. There have been talks of some companies even setting up their IPOs through GIFT City. For anyone — NRI, foreign national, or Indian resident — looking to move capital in or out of India through a regulated, low-friction, cost-efficient structure, it’s the most compelling option available today.

Nishit Shah is Principal Officer & Vice President PMS at Phillip Capital India Pvt. Ltd. and has been with the firm for over 10 years. Ankush Datar is part of Nishit’s team, working in the PMS team and assisting in fund management, for over 7 years at Phillip Capital.

Covers a bunch of things. Great work!

This is a great article.