Food Wars are Far from Over

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube.

In today’s edition of The Daily Brief:

Is Zomato beating Swiggy?

Can India be the world’s next data center hub?

Is Zomato beating Swiggy?

Swiggy and Zom… ahem, Eternal (yeah, it’ll take us some time to get used to that name) are out with their recent quarterly results. On the surface, this looks like a regular quarterly story. Revenue is up, quick commerce is burning cash, food delivery is more or less steady… you know, the usual.

But under the hood, something quite interesting is unfolding. Both these companies are trying to find their way to Meanwhile, a series of players, old and new, are entering the market and making their own bids at disrupting the disruptors. If you’re following this sector, that’s something to keep an eye on.

Before we get to that, though, let’s give you the broader picture first.

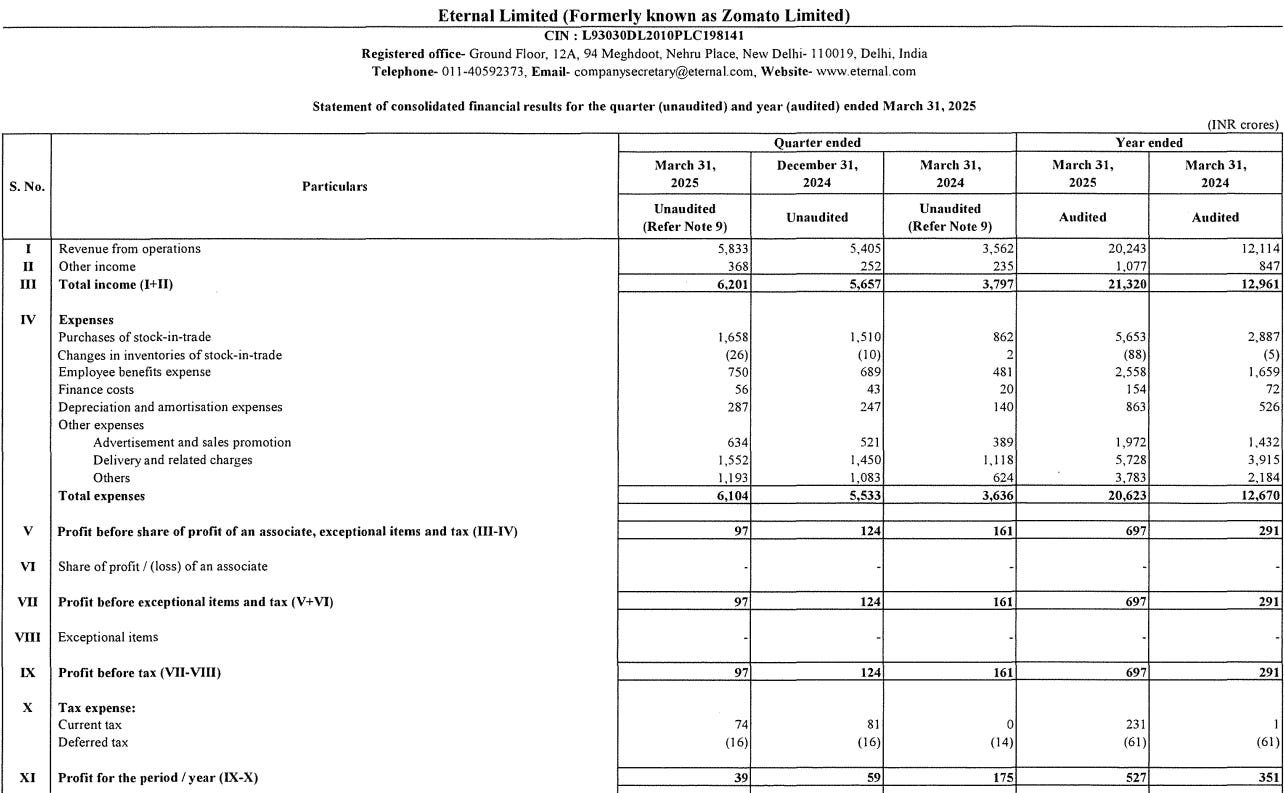

The overall results

Eternal’s adjusted revenue grew 60% year-on-year, last quarter, to ₹6,188 crore. But a lot less of that income translated into profits. Net profit fell 78% YoY to a mere ₹39 crore, pulled down by a lot of cash burn at Blinkit.

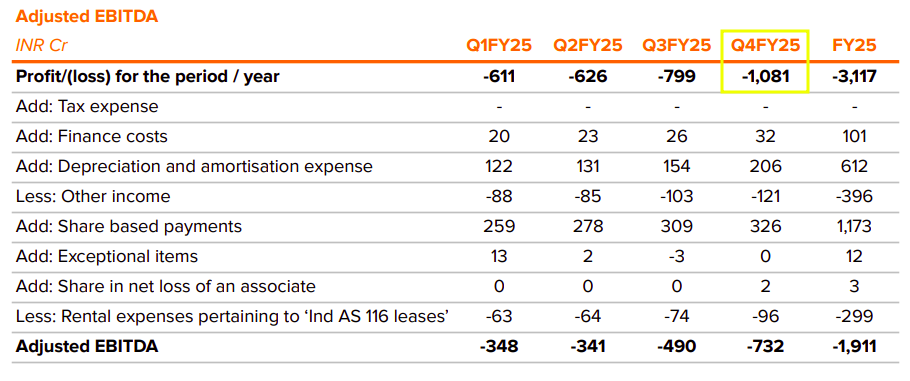

Swiggy’s adjusted revenue, meanwhile, rose 44.4% year-on-year to ₹4,718 crore.

But their losses ballooned through the year. They shot up to ₹1,081 crore, up 95% year-on-year.

So, essentially, despite making much more money than a year ago, Swiggy is still spending roughly one-fifth more than it’s able to earn.

What explains this divergence? Why are both companies’ profit numbers looking worse, despite record revenue growth figures?

The profitability puzzle

The short answer? Everyone’s throwing money at the same problem: how to make instant grocery delivery profitable — or at least make sure it stays alive.

A quick note before we get into this, though: Zomato has started talking about ‘Net Order Value’ (NOV) instead of ‘Gross Order Value’ (GOV). This reflects the impact of its discounts more accurately. If you account for order values based purely on the MRP of what you sell, that tends to skew your topline, because that’s not what you’re actually selling things for. Swiggy hasn’t done this yet, however. So, for now, we’ll look at GOV for both since that will be easier to compare.

With that little bit of accounting trivia out of the way, let’s get started. We’ll go business-by-business, because that’s where the nuances start to matter.

Food delivery still works

For both businesses, food delivery continues to make money.

Swiggy’s food GOV hit ₹7,347 crore this quarter, up 17.6% year-on-year. It posted an adjusted EBITDA of ₹212 crore, or a 2.9% margin. (If you’re wondering what ‘EBITDA’ means by the way, it basically measures the ability of a business to churn out cash, without taking all kinds of other costs into account. Here’s a fuller definition.) But what’s interesting about this figure isn’t the margin itself — it's where its food delivery customers are coming from. Here’s what its management said:

“30% of users acquired through Instamart in the last 6 months were new to Swiggy and have started ordering from food as well.”

Its groceries delivery business, in a sense, has become a way of drawing new customers. Meanwhile, Bolt — its 10-minute food delivery option that everyone thought was a gimmick — now makes for more than 12% of its food delivery orders. As per its management:

“Currently, over 12% of FD platform orders are through Bolt. New users acquired through Bolt have shown 4-6% higher monthly retention than the platform average.”

What we’re increasingly learning about the delivery business, it seems, is that speed works. People have repeatedly written off quicker deliveries as a stupid metric that VC-backed businesses are needlessly obsessed with. But there seems to be a strong business case for it. Quicker deliveries bring in more orders, and lock customers in.

We could debate about whether you can have fresh food in 10 minutes, but that’s besides the point. One-tenth of those ordering on Swiggy clearly think it’s fresh enough to order.

At the same time, this model hasn’t worked across the board either. Eternal, in contrast to Swiggy, has shut down both Zomato Quick and Everyday. CEO Deepinder Goyal was blunt about this:

“We are not seeing the path to profitability in these without compromising on customer experience.”

So here’s how the chessboard looks. One company is fully bullish on 10-minute food delivery. The other one says it can’t make money with it. But there’s some nuance here: while Eternal may be pulling out of this business, from what we can tell, its subsidiary Blinkit is doubling down on Bistro, a 10 minute fresh food delivery business.

Eternal’s food business is still chugging along. Its GOV grew 16% year-on-year, to ₹9,778 crore. Its adjusted food revenue was up 17% to ₹2,409 crore, while its EBITDA from food hit ₹428 crore, up 153% YoY.

But behind these big numbers, there’s an uncomfortable truth that Goyal admits to. The business has stopped growing as it once did. Why? He offers three main reasons:

People are spending less on eating out or ordering in — especially for non-essential items.

The company has seen a temporary shortage of delivery workers — who have all been lapped up by quick commerce businesses, who are hiring aggressively.

Quick commerce brings more alternatives. Some customers are choosing to order packaged food instead of ordering from restaurants.

Oh, and there’s one more thing. Eternal is cleaning out its platform. It kicked out ~19,000 restaurants due to hygiene or trust issues.

Zooming out, the food delivery business is steady, and it can make money. But the game has shifted. Quick commerce is where the future, and all the current cash burn, lives.

Quick commerce is a money-hungry business

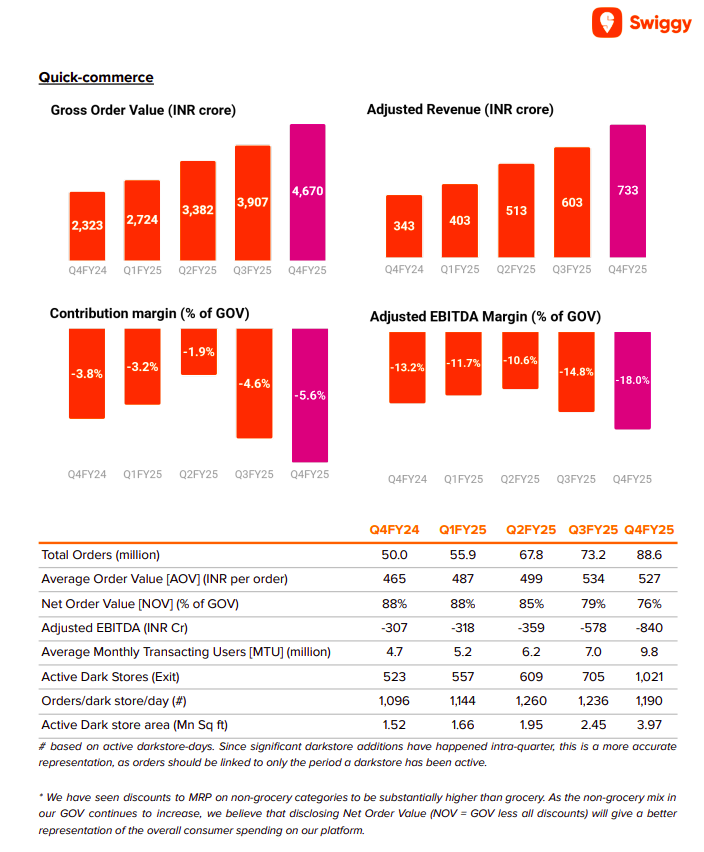

Swiggy’s Instamart added 316 dark stores in one quarter alone. For context, that’s more than the previous eight quarters combined. Within a single quarter, it pushed its store count up to 1,021. And with that, its GOV roughly doubled year-on-year to ₹4,670 crore.

But this rapid expansion took its toll on the company this quarter. Its quick commerce EBITDA loss hit ₹840 crore.

Swiggy’s management, though, insists that the last quarter marked the peak of its losses. As CEO Sriharsha Majety wrote to shareholders:

“We believe that Instamart reached the peak of adjusted EBITDA losses in late Q4. From here on, we expect it to progressively unwind losses... Our corporate adjusted EBITDA break-even timeline continues to remain in sync with the contribution break-even for quick commerce [Instamart].” Because of these costs, the break-even timeline for Instamart has been pushed by two quarters. Back in the December quarter, they said Instamart — and the company overall — would break even by the third quarter (October–December 2025) this year. Now, they’ve pushed that timeline to June 2026.

Instamart’s average order value (AOV) was ₹527, up roughly 13% YoY. AOV is a big deal in quick commerce, because while Swiggy’s cost of fulfilling a delivery — including picking, packing, and last-mile transport — stays more or less the same per order, the larger the basket size, the more revenue they earn per rupee spent on delivery. In other words, higher AOV directly improves unit economics, which is why AOV is one of the most important metrics to track in this space.

Blinkit, meanwhile, added 294 stores this quarter, bringing its total to 1,301. 40% of this network is made up of stores it has opened in just the last two quarters. Most of these new stores, according to the company, are yet to kick into full gear.

So, at the moment, here’s how things look: with its new stores, the company’s GOV rose to 134% year-on-year, last quarter. But on the other hand, its AOV came in at ₹665 — lower than its previous quarter. Now, those are still industry-leading figures. Its AOV was still higher than Instamart’s numbers, or the ₹550 per order that Zepto earned in last year’s December quarter.

At the moment though, the company’s earnings have lagged what it spent on its expansion. As a result, its adjusted EBITDA loss increased to ₹178 crore.

Quick commerce is red hot

There’s one big reason that both companies are having to funnel so much money into their quick commerce business, without the returns showing up: quick commerce is red hot right now. This competition isn’t quite showing up in a discount war, as it did before. But as Blinkit CEO Albinder Dhindsa put it, you can see a clear footprint of this competitive intensity in the fact that margins aren’t improving.

“That is both because there are now more players in the market, and there is obviously more competition across categories to market to the same set of customers which is leading to some margin pressure, both in terms of being able to charge higher delivery fees in some geographies and also in being able to sell more of the higher-margin categories on the platform”

Swiggy’s CFO, meanwhile, said this:

“We have seen competitive pressure continuing to increase not only from the existing players but also there are a set of new players who are entering the market.”

Even as Swiggy and Eternal pump money into the business, Zepto is aiming for 1,200 dark stores. Amazon and Flipkart, meanwhile, are making their own early moves. This isn’t just a space with three players anymore. Everyone wants a piece of your kitchen.

And then there’s Reliance. Reliance’s strategy is different. It doesn’t need to build new stores or warehouses. It already has a huge brick-and-mortar presence, and it plans to use that to jump in. Here’s what they said in their earnings call:

"The big advantage that we have in this segment is compared to other people who have to set up dedicated store infrastructure. For us, we are only leveraging the infrastructure that we already have. My fixed cost is already being taken care of by my store sales. This is all incremental sales and it is only incremental cost that I have to incur to deliver these orders. So we are doing this model in a profitable manner with a very strong unit economics."

In a game where everyone else is burning cash to add capacity, Reliance is cashing in on its surplus capacity. That’s a different way to play this game altogether.

Eternal has pivoted to becoming an Indian Owned and Controlled Company (IOCC). With majority Indian ownership, Blinkit can now get around India’s FDI laws, and that gives it a superpower: it can own its own inventory. This could be big. They claim the working capital need for owning all Blinkit inventory would be under ₹1,000 crore — just 5% of ₹22,000 crore which is Blinkit’s total Net order value or NOV in FY25. From what they say, this pivot wouldn’t hurt their balance sheet too much — even as it improves margins by cutting out middlemen.

On similar lines, Zepto’s latest fundraising round saw an investment from Motilal Oswal. It, too, has actively been working to become Indian Owned and Controlled, although hasn’t formally announced IOCC status.

On which note, Swiggy’s CFO said this:

“There are obviously the regulatory framework as well as our own domestic ownership which continues to go up since our listing and at some point in the future when we believe that is the right time we may also want to consider it but there is no plan in the near future.”

Quick commerce has a funny way of turning everyone desi.

Oh, oh, oh… and just by the way — we learnt a lot of what we’re saying here from both companies’ earning calls. Those are fascinating to us. But then again, we’re a bunch of market geeks. But if you think those hour-long business calls might put you to sleep, we have your back. Check out our new newsletter, The Chatter, where we pick out the nuggets we enjoyed the most from all these calls.

The bottom line

So what are we left with?

Food delivery is profitable, but growth is tapering. Quick commerce is growing fast, but profitability is nowhere in sight. Swiggy is betting on Bolt. Eternalis betting on Blinkit’s higher AOV and new inventory model.

Will that be enough? Will any of this ever make money at scale? Or are we just seeing a multi-billion-dollar experiment in delivery logistics, subsidised by venture capital and public markets?

We don’t know. But in the meanwhile, this is a sector that leaves us completely fascinated.

Can India be the world’s next data center hub?

As the old Arthur C. Clark quote goes, any sufficiently advanced technology is indistinguishable from magic. Writing from the eye of the AI storm, we can very much attest to this. It feels like we’re living in a science fiction world — where computers are slowly eating into everything that a human can do.

But it’s easy to overlook one thing: the technology around us exists because of physical, real-world infrastructure — things you can touch and feel. Without it, AI would disappear, and our phones would all become useless. And yet, we don’t seem to have enough of it in India.

We’re talking, of course, about data centers.

Companies across the world are spending billions of dollars to build more data centers. This includes some of the largest investment announcements in existence — including the ludicrous $500 billion Project Stargate announcements. Unless the entire basis of computing shifts, this is a trend that will stay for a while.

But what do these data centres really do? What’s fuelling the mad rush behind their growth? Does India need them too?

Let’s break it down.

What is a data center, and why do we want so many?

Think of a data center as a massive digital warehouse.

It's basically a building filled with thousands of powerful computers, called servers, that store all our digital stuff — from the Netflix shows we stream, to memes posted on Instagram, to confidential business documents. All of this — literally everything you can access on the internet ever — sits specialized machines designed to run 24/7, packed tightly into metal racks stretching from floor to ceiling. Without them, modern life falls apart.

They’re also big money-spinners. When you hear of apps, tools and businesses being “on the cloud”, this is what people are talking about. None of your data actually sits in the sky — the “cloud” runs on data centers. A large portion of what big tech majors like Amazon, Microsoft, and Google, in fact, comes from the massive data centers they own around the world.

Since data centers are so important, it’s worth taking a deeper look at them.

It’s hard to “measure” data centre capacity — but one thing people often do is look at how much power a data centre consumes, as a rough heuristic. Right now, the world’s data center capacity is at around 40+ gigawatts (GW).

How did we get here?

Data centres, when they began, were just large computers that sat in universities and government departments. But as the internet took off in the 1990s and 2000s, followed by the cloud computing revolution of the 2010s, it triggered exponential growth in the world’s data center capacity. In just two decades, we went from small, local facilities to gigantic, “hyperscale” data centers —- which serve the online world we live in today.

We’re now at the precipice of another inflection point — maybe the biggest one yet — with artificial intelligence.

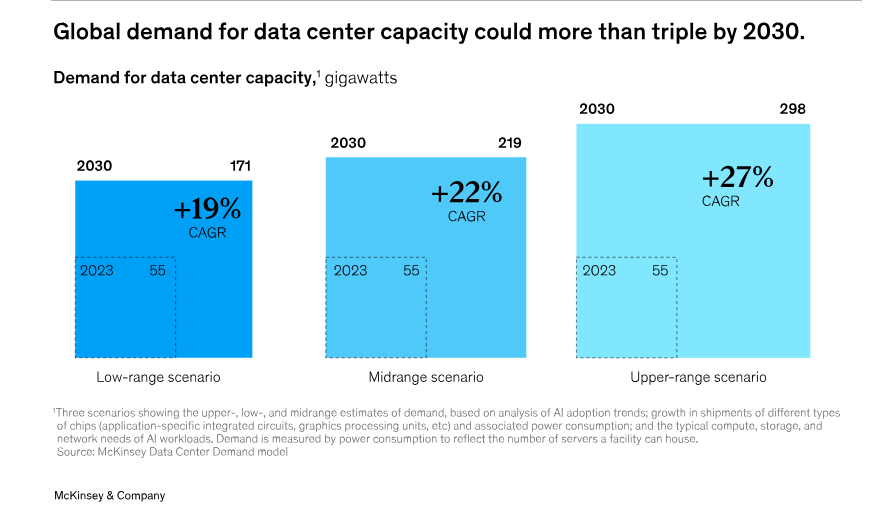

Already, about one-fifth of the world’s data center capacity is being used specifically for AI and AI-run applications. This is just the beginning. Companies are racing to build larger, more specialized data centers to power the AI revolution. The data center market is expected to grow by 17% annually — to reach 100 GW in 2030, according to Citi Research.

That’s how much supply is being added. If anything, demand is growing even faster — to a point where all this extra supply might fail to keep up. McKinsey says the demand for data center capacity could rise by roughly 22% annually until 2030 — to reach an annual demand of anything between 171 and 298 GW.

Around 70% of that demand will be for data centers that can handle advanced AI workloads. And just one type of AI — generative AI — will drive 40% of the total demand.

Should India jump into the fray?

Data centres, from what we can see, are a new gold rush in the making. But is India anywhere in the picture?

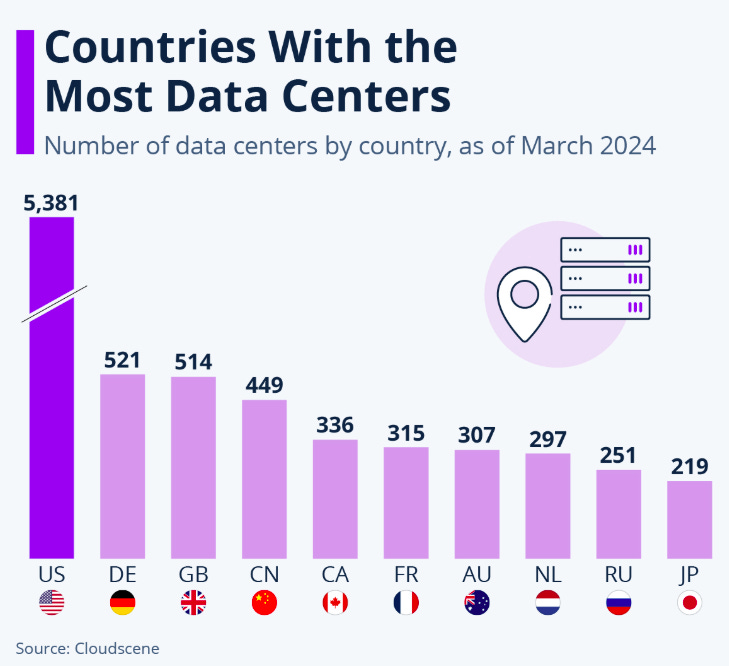

We’re slowly making its way up the data centre ladder. We recently crossed the mega-watts territory and entered the big leagues, giga-watt capacity, with a total capacity of 1.2 GW. We currently have around 150 data centers spread across the country, clustered in key cities — like Mumbai, Chennai, Delhi and Bengaluru. Some of these are run by domestic firms, like Reliance, Adani, or Tata Communications, while others are under the custody of international giants like AWS, Google, Microsoft.

But we’re still a very small player in a large game. India currently hosts only 3% of global data center capacity — despite generating approximately 20% of the world's data. For context, per person, the United States has around 51x the data centre capacity that we do.

There’s a strong case for us to grow our capacity, for two main reasons.

Better connectivity

See, while it might not always feel this way, for you to use the internet, packets of data have to travel physically between your device and a data centre. If a data centre is located far away, that data has to literally move across countries and oceans — and that creates latency. The closer a data centre is, the faster the internet feels for Indian users. Websites load quicker, video calls have less lag, and online games run smoother.

Meanwhile, localised data centres also cut the costs that businesses face in transferring data across borders. AWS, for instance, charges a small fee for every GB it transfers for you between geographies.

Ownership over data

When Indians’ data sits in another country, we lose “sovereignty” over that data. The way that data is treated depends on those countries' laws and regulations. Now, this might be fine if we’re just talking about videos of cute animals. But for sensitive information like government records, banking details, or healthcare data, this can become a problem.

Having data centers within India means Indian data stays under Indian control. In recent years, this has become a key focus of the Indian government. Under the Digital Personal Data Protection Act, 2023, for instance, the government can require certain types of data to be stored within the country.

It’s not just us:

China’s Cybersecurity Law and Data Security Law require that "important data" and "personal information" collected in China must be stored within Chinese borders, forcing companies like Apple and Microsoft to build data centers within China's borders.

The EU has implemented the General Data Protection Regulation (GDPR) — the world’s most comprehensive data protection framework — which places strict conditions on data transfers outside Europe. In fact, in 2023, Meta was fined €1.2 billion by the EU for transferring EU citizens' data to the United States without adequate protection.

South Korea’s Personal Information Protection Act strictly regulates cross-border data transfers.

And then, there’s a long laundry list of other, smaller benefits: more jobs, more support for our tech ecosystem, and so on.

For all these benefits, though, we are nowhere near having the data centre capacity we need.

What others do well, and what we can do better

If you want to build a data centre, you basically need to line up a few things: you need a tract of land that you can develop. You need cheap power supply, and the ability to cool down the data centre. And you want to be in some place that already has dense network connections, and a steady source of demand.

Countries that have been able to provide some of this have become data center hotspots.

United States: The U.S. benefited from being the early home of the internet. Northern Virginia — just outside Washington DC — becoming a global interconnection hub thanks to historical routing infrastructure and dense fiber networks. Cheap, stable power and large tracts of affordable suburban land enabled massive hyperscaler campuses to flourish. Today, this region alone has about 300 data centers with around 4 GW of capacity – more than all of India's data centers combined.

Europe: The so-called “FLAP” markets — Frankfurt, London, Amsterdam, and Paris — combined strong demand with reliable power, dense fiber connections, and supportive local governance. Even though land was relatively expensive in these regions, these advantages helped it build out considerable infrastructure.

Asia-Pacific: Early on, Singapore became a data centre hub by offering political stability, high-speed international cable landing points, and a pro-business environment. This made it a low-risk entry point for global firms. But recently, land and power constraints have pushed investment to Malaysia and Indonesia, which offered cheaper land, looser regulations, and growing demand.

China: China went on a state-driven digital infrastructure push, prioritising cheap land and power in its western provinces. Meanwhile, strict data localisation laws created guaranteed demand. However, their build-out wasn’t perfect. There was poor alignment between supply and real demand, and reports suggest that up to 80% of China's newly built computing resources are now sitting unused.

These are regions that we should take lessons from.

Now, we do have some inherent advantages. Building and operating data centers in India is already 10-25% cheaper than in competing locations like China or Singapore. But we also face serious hurdles in materially building up our data center infrastructure. According to PwC, India needs to fix a series of issues. Here are just a few:

Complex Approval Processes: Data center projects require permissions from multiple authorities. While some states, like Maharashtra, have implemented a single-window clearance system, many are still burdened by red tape.

Power Reliability Concerns: Power, specifically, is a fundamental obstacle to our data centre build-out. Most Indian data centers are inefficient — operating with a much higher Power Usage Effectiveness (PUE) than the global best practices — which drives up costs. Our grids are also unreliable — with frequent power cuts. For data centers that require 99.99% uptime, this creates significant operational risks.

Environmental Sustainability Challenges: Data centers use enormous amounts of electricity and water, especially for cooling. A high-scale facility can use up to 7 million gallons of water daily. In a country where many states already face water shortages, this adds a lot of strain.

But there are reasons to be hopeful.

Silver linings

A recent FT article paints an encouraging picture around India’s data centre capacity.

India’s data centre market is expanding rapidly. It is already churning out $1.2 billion in revenues, and is growing at more than 20% annually. This is driven by a wild surge in demand — with our average data usage having doubled in just the last five years.

This has been paired with major announcements for new investment. Between 2019 and 2024 alone, we attracted nearly $60 billion in data center investments. By some estimates, we should expect an additional $100 billion in investment by 2027.

Many of these are finding ways around India’s energy problems. For instance, Reliance Industries is planning a gigawatt-scale AI data center in Gujarat, while Adani has announced a decade long ₹50,000 crore plan (about $6.2 billion) for 1 GW of data centers in Mumbai. Both are relying on their captive power generation facilities nearby — by-passing India’s overloaded power ecosystem.

There are many other investments in the pipeline. For instance:

Airtel’s Nxtra is investing $600 million to double its data center capacity to nearly 400MW by 2027.

STT GDC is constructing multiple facilities in Navi Mumbai with a combined 40MW capacity each — spending $3.2 billion to nearly triple its capacity.

RMZ Infrastructure has partnered with Colt DCS on a $1.7 billion investment to develop 250MW of data center capacity across multiple Indian cities.

Microsoft, plans to invest $3 billion over the next two years to expand infrastructure in India.

Conclusion

India’s nowhere near the big leagues, when it comes to data centre capacity. But we’re making ambitious strides. Despite India’s many problems, we’re cautiously optimistic about the future.

In recent years, India has made many regulatory and policy changes to support data center growth. The government granted "infrastructure status" to data centers in October 2022 – which makes financing easier and less expensive. The central government is also developing a national data center policy that proposes creating Data Centre Economic Zones and considering data centers under the Essential Services Maintenance Act, which would ensure prioritized resource allocation during shortages.

The private sector, from the looks of it, is responding well.

We still have a long way to go. But if we play our cards right — by fixing power reliability, streamlining approvals, and leveraging its cost advantage — we could emerge as the natural choice for the next phase of the global data infrastructure build-out.

Tidbits

LTIMindtree Secures Record $450 Million Deal

Source: Business Standard

LTIMindtree on Monday announced its largest-ever deal worth $450 million with an undisclosed agribusiness client. The seven-year agreement involves deploying an AI-powered operating model to deliver application management, infrastructure support, and cybersecurity services. This milestone deal marks the biggest since the merger of LTI and Mindtree. The win is a boost to LTIMindtree’s order book, which stood at $6 billion at the end of March 2025, including $3 billion in vendor consolidation opportunities. CEO-designate Venu Lambu described the deal as pivotal in the company’s AI-driven transformation. The company is focusing on large cost-takeout and efficiency-led contracts amid a cautious client spending environment.

Ather Energy Reports 29% Revenue Growth in Q4, Narrows Losses

Source: Business Line

Electric scooter maker Ather Energy reported a 29% year-on-year increase in revenue for Q4 FY25, reaching ₹676 crore compared to ₹523 crore in the same period last year. The company narrowed its net loss to ₹234 crore from ₹283 crore. For the full year ended March 2025, Ather’s revenue rose 28.5% to ₹2,255 crore, while annual net loss reduced to ₹812.3 crore from ₹1,059.7 crore in FY24. Sales volumes for FY25 stood at 1,55,394 units, up 42% from the previous year. The Rizta model, launched in Q2 FY25, contributed 57% of total volumes. Adjusted gross margins surged 2.7 times to ₹428 crore for the full year, supported by improved uptake of the company’s paid software Pro Pack, which was chosen by 88% of customers. Ather also expanded its retail footprint by 32% in Q4, with continued strength in southern markets and growing share in northern states.

Iron Ore Retreats to $99 as China Demand Concerns Resurface

Source: Business Line

Iron ore futures in Singapore slid back toward $99 per ton, erasing gains from earlier this week when prices had risen over 3% to reach their highest close in nearly three weeks. The initial rally was triggered by a US-China trade truce that briefly lifted risk sentiment across global markets. However, prices lost momentum as attention shifted to weak demand fundamentals in China. With the onset of the seasonal off-peak period in construction and manufacturing, steel demand typically declines in May. Additionally, the China Iron and Steel Association reaffirmed the government’s push to curb steel output, further dampening expectations for raw material demand. Steel inventory build-ups have added pressure on mills, prompting cautious raw material purchases. Other industrial metals such as copper and nickel also remained under pressure, reflecting broader market hesitance despite the geopolitical reprieve.

- This edition of the newsletter was written by Krishna and Prerana.

🧑🏻💻Have you checked out The Chatter?

Every week, we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

🌱Have you checked out One Thing We Learned?

It's a new side-project by our writing team, and even if we say so ourselves, it's fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That's all. It's chaotic, it's unpolished - but it's honest.

So far, we've written about everything from India's state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you're looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Great insights!

Is no one proof reading before pressing send?