The world’s investment outlook gets bigger and gloomier

When informal businesses become legible

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The world’s investment outlook gets bigger and gloomier

When informal businesses become legible

The world’s investment outlook gets bigger and gloomier

Every year, the UN puts out a report that tries to answer one simple question: where is the world’s money going? Here, we aren’t talking about stock market flows but companies building factories in other countries, buying up businesses across borders, funding roads and power plants that they’ll be tied to for decades.

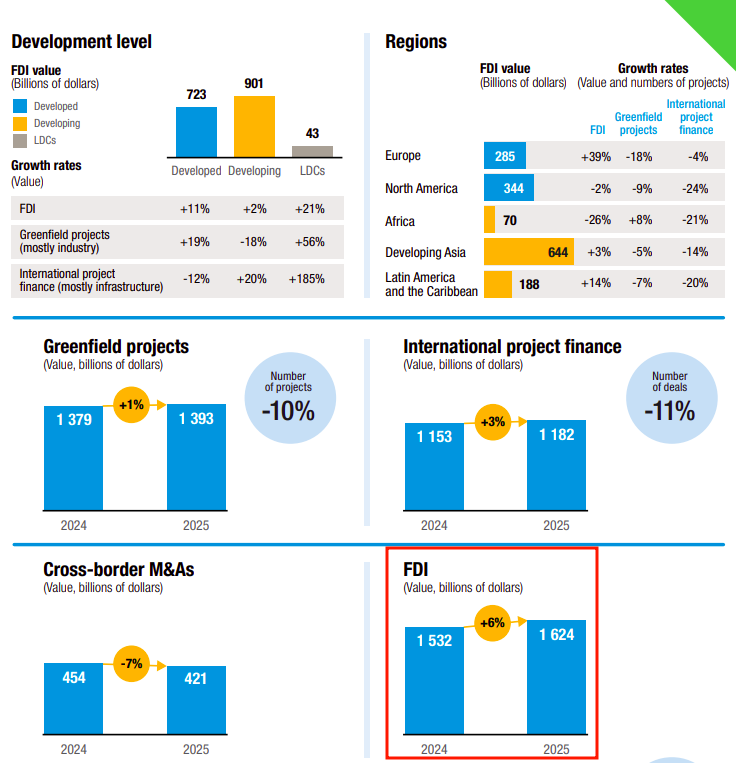

This year’s report just came out, and the top line looks great. FDI investment went up 6% in 2025, to $1.6 trillion.

After a few brutal years, money seems to be flowing again. Except that number is lying to you a little. Or rather, it’s hiding a lot.

One example of what’s being hidden is that a big company will route billions through a financial hub like Switzerland for tax reasons, or to shift cash between its own subsidiaries in different countries. Technically, that money crossed a border, so it counts as “investment“.

But it built no factory and didn’t hire anybody. It’s just money passing through on its way somewhere else. Economists call these conduit flows, and they’re such a big distortion that when the UN strips them out of the global total, that headline 6% growth shrinks to 4%. The report singles out Switzerland and Ireland — some of the world’s biggest tax hubs — as the two centres that drove most of the difference this year.

There are some big impressive numbers on top, and a lot of important nuance buried underneath this 200+ page report. We will look at the most important things that stand out to us.

Where the money actually went

Let’s start with the money itself.

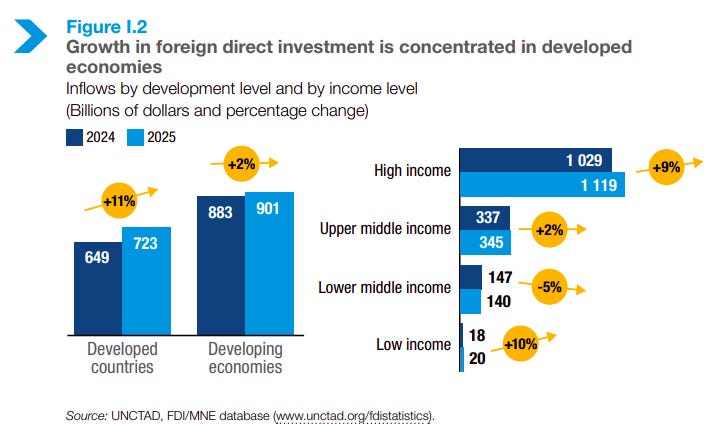

The first thing to understand is that “investment went up 6%“ is an average, and averages hide things. When you split the world into rich countries and poorer ones, the picture splits too. The investment into developed countries like the US and Europe jumped 11%. But on the other hand, investment into developing countries went up 2%.

In a rich country, foreign investment is a bonus. Companies there already have banks, stock markets, and investors lining up to fund them. But in a developing country, foreign investment is often the event. It’s how you build roads, power grids, and factories, because there just isn’t much local capital to do it. Roughly half of all the outside money developing countries get comes from this kind of investment.

And it gets worse at the very bottom. The poorest countries in the world pulled in $43 billion between all of them, which is under 3% of the global total. And almost all of it went into digging things out of the ground — oil, metals, minerals — rather than building anything that could employ people for the long term.

The factories nobody’s building

So where is all the money going, if not into poorer countries?

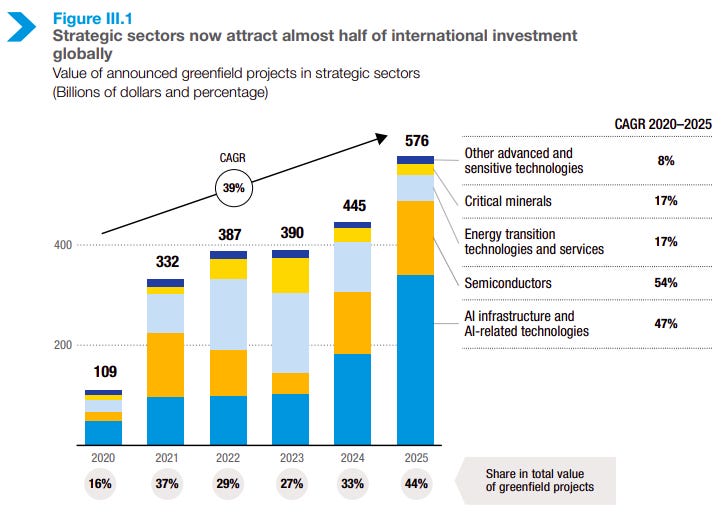

The answer is technology. In essence, that boils down to AI, and, of course, the hardware needed to support it: memory chips, interconnected semiconductors, critical minerals, and to some degree, clean energy. The report groups these as “strategic sectors,” and the shift here is dramatic.

In 2020, these sectors made up 16% of new investment projects. By 2025, they were 44%.

By now all of us know that AI runs on giant data centers, and those data centers need land, a reliable supply of huge amounts of electricity, and water to keep the machines from overheating.

Only a few countries can host all those things: a stable power grid, water, land, and an entire ecosystem of suppliers and engineers. So this money clusters. The top three countries getting strategic-sector money grab 56% of it between them. Poorer countries don’t even have the infrastructure to build a data center in the first place.

Meanwhile, the kind of investment that used to help poorer countries grow is drying up.

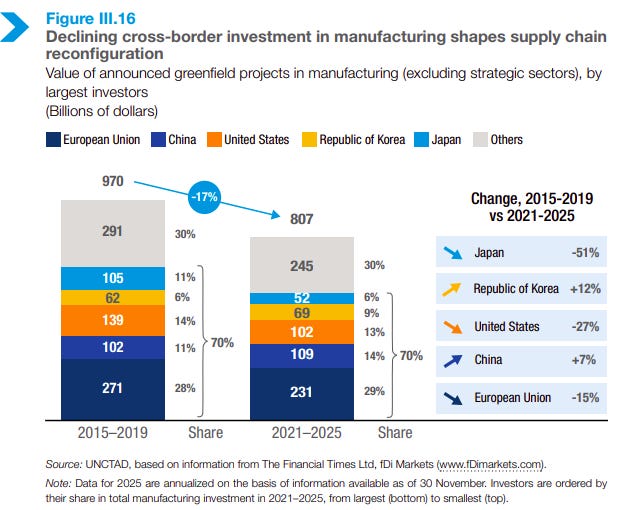

Once you strip out the strategic sectors, the value of new manufacturing projects — textiles, clothes, basic electronics, the ordinary stuff — has fallen about 17% over the past several years. For decades, this was the escalator: a poor country offers cheap labor, foreign companies build factories, millions of people get jobs, and slowly the country moves up. That escalator is slowing down. The companies that used to chase cheap labor are now chasing chips and data centers, and those don’t go to the places that need the jobs.

Who’s doing the investing is changing, too. It’s not just Western private firms anymore. State-owned companies from China and sovereign wealth funds from the Gulf states are using their national wealth to snap up assets abroad. More than a quarter of the companies on the UN’s list of the world’s 100 biggest multinationals are now at least partly state-owned.

What governments are doing about it

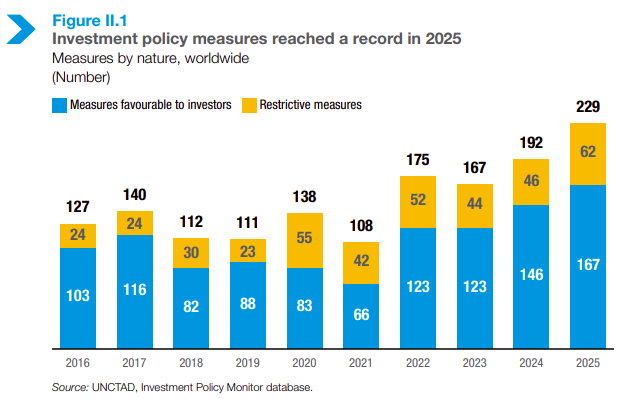

That brings us to the second big theme: governments have stopped sitting back and letting the market decide. In 2025, governments around the world passed 229 new rules affecting foreign investment. That’s the most ever recorded.

For years, the standard playbook was to cut taxes, get out of the way, and let money flow to wherever it made the most sense. That era is over. Governments are now actively steering where money goes, and they’re doing it in two opposite directions at once — pulling some money in, and keeping other money out.

Pulling in

The “pulling in” part has changed shape. It used to be broad tax cuts for everyone, but now it’s targeted cash. Rich countries are handing out massive subsidies — billions of dollars in grants and tax credits — but only to companies that build the things they want, like chip plants and battery factories, and only if they build them at home.

The US and the EU are essentially in a bidding war, throwing money at the same handful of tech companies to get them to build locally. But developing countries find it harder to win a bidding war with such an approach.

So they’re trying something different: instead of a blank tax holiday that costs them money for a decade, they’re tying incentives to results. You get the tax break only if you actually hire local people, or transfer some technology, or use local suppliers. It’s less them begging for investment, and more attaching some strings to it.

Keeping out

Meanwhile, the “keeping out“ part is growing fast. More and more countries are setting up systems to screen foreign investment for national security reasons. They’ve increased their power to review and block a foreign company from buying something sensitive. In 2016, 21 countries had this. By 2025, it more than doubled to 52.

What’s more, the definition of “sensitive“ has ballooned. It used to mean weapons factories and power plants, but now, it can even include data centers, AI startups, telecom networks, and lithium mines. That being said, few deals actually get blocked, but that’s almost beside the point. The mere existence of these reviews can make foreign buyers nervous, slows deals down, and racks up legal costs. And the mere existence of these reviews may be a sign of a bigger expansion on what the term “sensitive” means.

There’s one more thing worth mentioning here, because it lands hard on poorer countries.

See, old investment treaties often let a foreign company sue a government directly — not in that country’s courts, but in an international tribunal — if a new law hurts the company’s profits. In 2025, companies filed 56 of these lawsuits, and 80% of them were against developing countries. Many involved mining. So when a poor country tries to tighten environmental rules or demand a bigger cut from a mining project, a foreign company can drag it into arbitration and sue for billions in lost future profit.

Supply chains reorganize

For four decades, companies built their supply chains on one rule: find the cheapest place to make something, and ship it wherever it needs to go. It worked as long as nothing broke.

Perhaps, that should be changed to “if nothing broke”. The last five years saw the pandemic, the Suez Canal getting blocked, war in Ukraine, the US and China going after each other with tariffs and, of course, the Strait of Hormuz being choked. It didn’t matter anymore how cheap a supply chain was if it was highly fragile.

So, companies are rebuilding, and they’re willing to pay a bit more to feel safe. They’re moving factories out of countries they see as risky and into friendlier ones, or closer to their customers.

India is gaining, and so are places like Malaysia and Thailand, because of the so-called “China+1“ strategy. But that doesn’t mean companies aren’t leaving China — why would you let go of the country where you continue to have the most advantages? Instead, they’re building backup factories elsewhere so that, in case trade with China gets blocked, they’re not stuck. In all this, the consideration of cheap has gone out the window in place of geopolitical uncertainty.

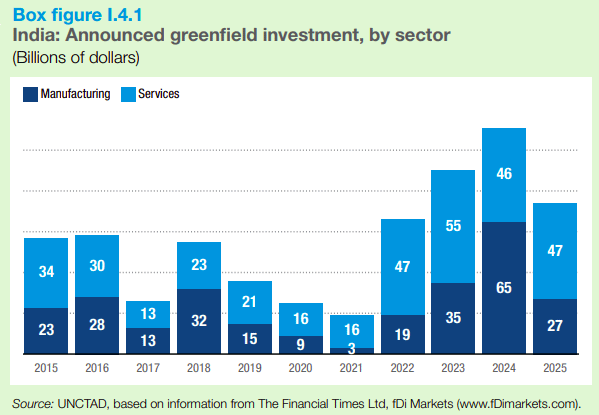

India is a good example of how the headline figure of investments attracted can deceive someone.

The money coming into the country jumped 44% last year to $39 billion. That was one of the biggest jumps anywhere, and it was enough to make us the 11th-biggest destination in the world. On its own, that sounds like nothing but good news.

But there’s a catch. The money going into brand-new projects actually fell, dropping from ~$111 billion the year before to $74 billion. So the money is still coming in, but it’s just going into what already exists rather than greenfield projects.

Conclusion

In summary, the world’s investment story is one of developed nations attracting new funds for emerging technologies. However, the appetite for old ones is dying, and there is a dearth of greenfield investment in developing and poor nations.

A few are pulling it off. Kenya, for instance, generates almost 90% of its electricity from clean sources, and it’s using that to attract data centers because companies under pressure to go green will pay to build where the power is clean. Indonesia, meanwhile, banned exporting raw nickel ore, forcing battery companies to build processing plants inside the country if they wanted the metal. It turned itself into a hub instead of just a mine. But these are pockets of leverage that they have.

At the same time, investment flows are becoming increasingly siloed with increasing de-globalization. Countries are putting stricter marks on what kinds of foreign investment (or, for that matter, imports) they can allow. We’ve known all of this for a while, but the massive numbers put it in a scarier context.

While the $1.6 trillion headline is eye-popping, the outlook is pretty glum for most countries trying to play catch-up. The world is just investing in fewer places, in fewer things, for reasons that have less to do with growth and more to do with fear.

Seen, but not formal

Picture a small cottage tailor; the sorts with two sewing machines in a rented room, stitching blouses and school uniforms for the neighbourhood. It’s the kind of business you see in every corner of India. It takes small pieces of work, for small sums of money, creating a job or two in the process.

Most of India’s business activity looks somewhat like this. Nine in every ten Indian workers work in conditions like this. Only, these don’t exist in documents, databases or really, in any formal context. To a bank, a tax database, or a labour inspector, they might as well be invisible. This is one of the perennial problems of India’s economy. If you can’t see who your economy comprises, you’re hamstrung in everything else you might want to do.

This June, Soumya Kanti Ghosh and others at the Prime Minister’s Economic Advisory Council came out with an interesting working paper. It has ideas that, while perhaps a tad optimistic, is worth engaging with: they argue that businesses like this are slowly being drawn towards formalisation. Not completely, and not equally in all dimensions. But they’re becoming easier to identify, count and lend to. They’re becoming legible.

What can this legibility do for our economy? Where does it still fall short? For that, let’s dive in.

The seen and the unseen

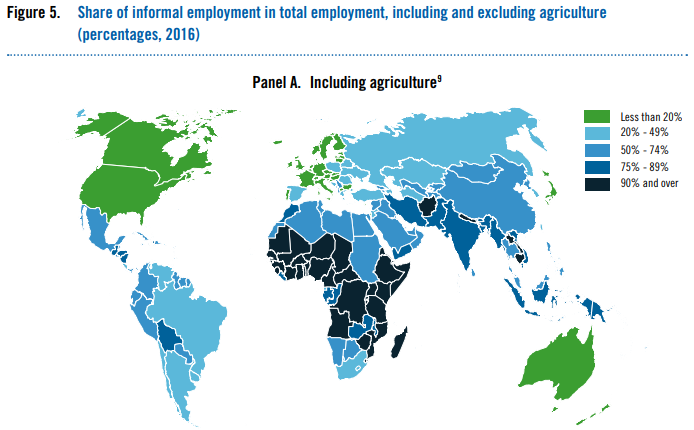

The “informal economy”, if you don’t know better, sounds shady — like businesses deliberately kept off books to dodge taxes or do something illicit. The truth is more banal. This is the part of the business-world that isn’t yet visible to the rubric of formal systems. These are ordinary, legal businesses, carrying out routine transactions. They simply haven’t entered the world of registers and record-keeping. Our cottage tailor might stitch beautiful blouses, and might still lack tax filings, payslips, or a recorded financial history.

This is surprisingly common, all across the world. According to the ILO, two hundred crore people — three in every five of the world’s workers — earn their living informally. The picture is even more skewed for India. Most Indian farming, of course, is entirely informal. But even leaving those aside, India’s roughly 8 crore informal businesses employ close to 13 crore people.

There are serious downsides to the invisibility of this dark economy, both for the businesses themselves and those they employ.

To a business, the formal economy, above all, opens into the financial system. Banks usually only lend to businesses they can see. You need audited books and earnings records to prove that you’re a good borrower. Without that, capital — the lifeblood of any business — becomes inaccessible.

But the bigger downside, arguably, is for the worker. The basic protections a job comes with — a written contract, paid leave, social security — are all creatures of the formal economy. The informal economy, in contrast, only comes with gigs, which can disappear without notice.

It isn’t easy for a business to cross the barrier and become visible, however, because visibility brings friction and scrutiny. Formality brings paperwork, and in India, a lot of it. You need to register yourself repeatedly — with corporate registrars, tax departments, labour departments, and more. You need to handle questions and subject yourself to investigation by everyone from the municipality to licensing authorities. There are benefits to crossing this hump, of course. But as the economists Rafael La Porta and Andrei Shleifer have argued, not everyone can actually avail them.

Our cottage tailor shop, for instance, might just be too small for formality to actually pay for itself. Why make the shift?

Almost formal

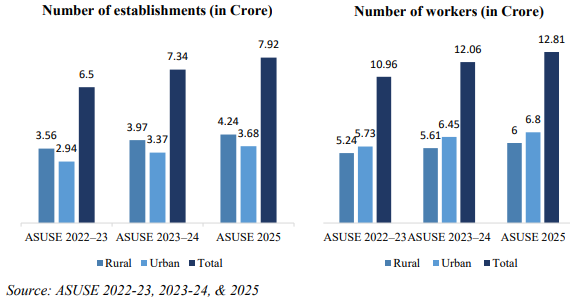

This is the world the paper tries to make sense of, using two surveys from 2025 — the Periodic Labour Force Survey (or PLFS), which looks at workers, and the Annual Survey of Unincorporated Sector Enterprises (or ASUSE) tracks unincorporated businesses.

At first glance, the paper seems to suggest that India’s informality problem is only growing. Across three recent rounds of these surveys, the number of unincorporated firms (other than farms) rose from about 6.5 crore to 7.9 crore. The number of workers they employ grew as well, from roughly 11 crore to 12.8 crore. As the number of such businesses has grown, so has their role in the economy, from marginally below a tenth of our economic output, to marginally above a tenth.

From those numbers alone, India’s informality seems more severe.

It points to something curious, though. Somewhere, buried in its methodology, the paper introduces the idea that formality isn’t a yes-or-no question. A business doesn’t need a full package of legal registrations to become visible. It can register for some things, and have a set of records for some purposes, without being entirely formal.

The paper studies unincorporated businesses — that is, businesses that don’t run as companies. These could be partnerships, family businesses, shops run by sole proprietors, or follow other configurations. They could still have some registrations, though: they could have GST numbers, for instance, or carry a trade license from their local governments. Over the period the paper looks at, the share of such businesses that have some registration have barely grown. Two years ago, they were barely under 37%; now, they’re closer to 37.5%.

But those registered firms aren’t all equal. In fact, the paper creates a 0-100 scale based on how formal they are. Some registrations seem to be overwhelmingly more useful than others. A firm that has an Udyam or Udyam Assist registration, for instance, gets almost twice as much financing as those with any other registration. We’ll come to this shortly.

More interestingly, there are other ways in which these firms are becoming visible, which have nothing to do with the government. Consider internet use: what has become, in our times, one of the first traces businesses are leaving behind — through QR codes, WhatsApp orders, online payments, and the like. Just two years ago, one-fifth of these unincorporated businesses were online. Now, that number has nearly doubled, to two-fifth.

Beyond this, in our humble view, some of the paper’s conclusions are a bit of a reach. But it got us thinking: if there are different levels of formality, what does that tell us? If the government can’t push businesses through the full set of compliances, are there side-doors that can help them get some benefits?

The side door

The government, it turns out, has been thinking on these lines as well.

In January 2023, for instance, the Ministry of MSMEs launched the ‘Udyam Assist Platform’, which runs through the Small Industries Development Bank of India, or SIDBI. This was meant, specifically, for a class of firms that didn’t fit the normal registration route. These firms are too small to cross the regular GST threshold, and file no GST returns at all. Ordinarily, most registrations require their own paper trail, but such businesses would usually have none.

To get around this barrier, the government allowed approved middlemen — like banks, NBFCs, microfinance lenders, and even government departments — sign such businesses up and issue a certificate on their behalf.

Take our cottage tailor once again. If she needed a loan to renovate her shop, before this, she would have to scramble for proof to carry to the bank counter — rent receipts, a passbook, or whatever — and it might or might not suffice. Udyam Assist replaces that with a single document that the bank must recognise.

This doesn’t make the establishment formal. But it gives it a narrow slice of legibility, which the financial system can act on. This comes without the costs of formality — registrations, filings, records — making it easier for a small business to take to. It makes it visible to a credit institution, specifically, without demanding that the business transform itself completely.

There’s more — banks are incentivised, structurally, to give loans to these entities. Under ‘priority sector lending’ rules, banks have to reserve a share of its loans to certain specific groups of borrowers — like small businesses or farmers. These targets have to be hit. Most such borrowers are informal. But now, by government notification, and in the Reserve Bank’s own rulebook, a Udyam Assist certificate is treated exactly like full Udyam registration. This legibility, in other words, helps banks as well.

Meanwhile, the government has stepped in as a backstop, de-risking the decision to lend to such a firm. Through its credit guarantee fund, it covers 85% of loans of up to ₹20 lakh, with no collateral asked of the borrower. If things go wrong, this caps what a lender could lose.

To scale this, interestingly, the government is leaning on another lever of visibility — the internet. Many small businesses were already networked into online platforms. The government turned these into a distribution channel. In September 2025, for instance, the payments app PhonePe began letting merchants generate a Udyam Assist certificate inside the app itself. This was then tied into a credit arrangement with SIDBI.

See this from the eyes of our tailor. A UPI app they once signed on to now gives them a slice of visibility, which makes them eligible for loans — all without having turned “formal”.

Side-stepping formality

Udyam Assist, in just a few short years, has managed outsized success. By July 2026, nearly 3.85 crore firms had signed up through Udyam Assist, alongside almost 9 crore across the full Udyam system. Many of these firms technically lie on the wrong side of the formal-informal divide. But even limited visibility goes a long way in opening doors for them.

But as the economists La Porta and Shleifer have noted, being seen helps at the margin, but it doesn’t turn a subsistence workshop into a thriving business. Businesses are often informal for a range of reasons, and a single intervention may not help them cross the line. This is visible in the Udyam experiment as well. While SIDBI had registered nearly 9 crore enterprises by the end of 2025, a much smaller number — just 3.6 crore — had actually taken a loan.

Meanwhile, for informal workers — the intervention has done very little. In fact, even among India’s regular, salaried workers, more than half have no written contract, and no social security. Selective visibility hasn’t changed their lives.

For all this, however, this experiment points to something interesting. The stubborn informality of India’s economy can sometimes make it feel like an impossible dead-end — a problem so large that nothing can fix it. As it turns out, that is far from the truth. Visibility isn’t an all-or-nothing game, and informal businesses are not static businesses.

Making just a single document easy to attain, in itself, can change the fate of a firm.

- This edition of the newsletter was written by Krishna & Pranav

Tidbits

NPCI is developing a Unified Agent Protocol (UAP) to register, verify, and authorise AI agents to make UPI payments autonomously — pending RBI approval — as UPI hit 22.71 billion monthly transactions worth ₹28.92 trillion in June 2026.

Source: BSThe India-UK FTA takes effect July 15, offering zero duty on 99% of Indian exports. GJEPC projects gem and jewellery exports to rise from $754 million to $2.5 billion, with overall bilateral sector trade reaching $7 billion.

Source: ETDr. Reddy’s has delayed commercial supplies of its semaglutide generics — sold as Obeda, Mashlo, and Olymviq — after finding out-of-specification API batches; the stock fell 5.9%, its steepest drop in four months.

Source: Bloomberg

Tamal Bandyopadhyay on the microfinance industry cycle

After going through 144 concalls across 18 microfinance companies just to watch a single credit cycle play out in slow motion, we were left with a bigger question: why do these crises keep happening, over and over, roughly every few years like clockwork? To make sense of all this, we spoke to Tamal Bandyopadhyay, who has covered Indian banking for nearly three decades, is a senior advisor at Jana Small Finance Bank, and authored the book Pandemonium. Our conversation dives deep into what caused the latest microfinance cycle, how this time is different, and what the industry can do to avoid repeating the same mistakes. Listen to the full conversation on Spotify and Apple Podcasts. Read the key takeaways on Subtext.

Watch the full podcast episode below, where Tamal breaks down the recurring cycles of the microfinance industry.

What We’re Reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Points & Figures by Zerodha

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how India’s digital economy got here, through the data buried in Jio’s IPO filings.

Join us on WhatsApp, where we share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops so that you can read or watch it right away.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

The UN report's analysis is a great read, 🙏🏼