Full charge, no power: the software behind EVs

Plus: Where are the priorities in India’s priority sector lending norms?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Full Charge, No Power

Where are the priorities in India’s priority sector lending norms?

Full Charge, No Power

Recently, a weird series of videos had surfaced from across India.

E-rickshaws, weaving through traffic, were coming to an abrupt halt. The driver would have no idea why. Nothing would appear broken. As it would turn out, a few people on a nearby footpath had choked the ride from their phones.

This became enough of a menace that India’s IT ministry had to act. Officials initially said two applications had been removed. Shortly thereafter, the ministry directed Google and Apple to remove seven battery-management apps, including BAT-BMS. These apps linked, through bluetooth, to the vehicle’s Battery Management System — the onboard software that watches over a battery pack. They were originally meant for maintenance, but they became a portal for wider misuse.

To us, though, this triggered a more interesting question: why did this vulnerability even exist? Why could these vehicles be stopped so easily? Turns out, while modern petrol cars use software, to the incoming era of electric vehicles, software is everything. It is the lifeblood these cars need to run. It could also become a liability. This is the shift we wanted to explore.

The moment of acceleration

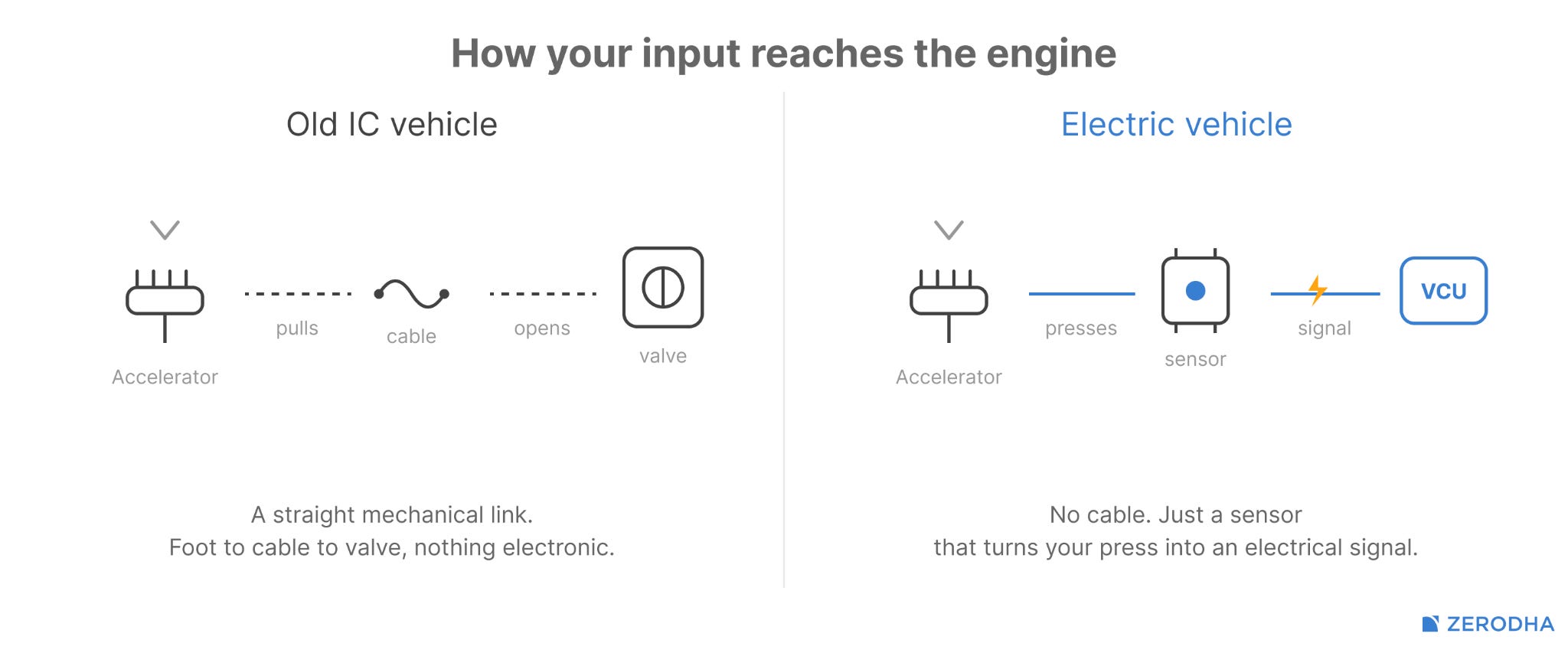

Think of an old petrol car.

You press the accelerator. A physical process follows. A cable pulls open a valve inside the engine, injecting fuel where it can be burnt. There’s a mechanical link between you and the engine.

Things are different in an electric vehicle. Here, the accelerator sits atop a sensor. When you press the accelerator, it measures exactly how far you’ve pushed it, and turns that measurement into an electrical signal. It is that electrical signal, and not mechanical ones, that the battery and the motor respond to. There’s nothing inside that your hand or foot physically moves.

Not every request gets approved

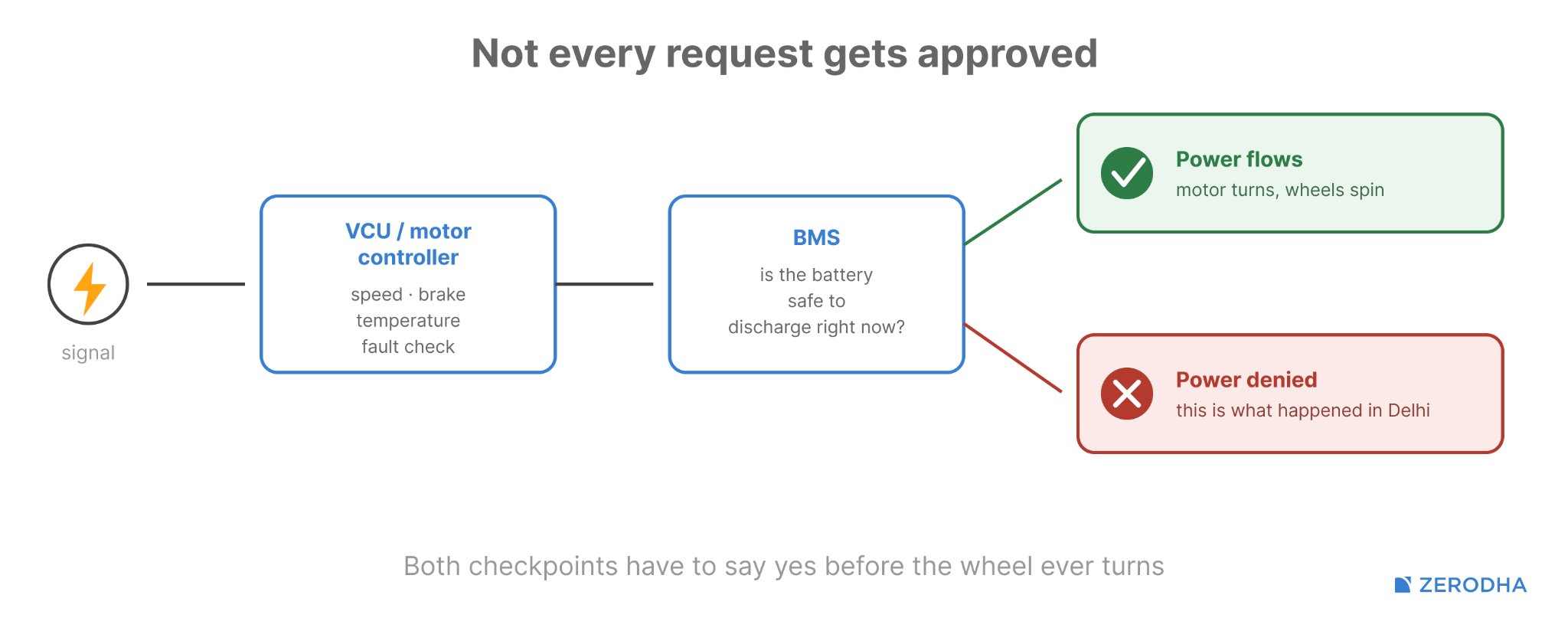

In many modern EVs, the signal from your accelerator goes to something called the vehicle control unit, or VCU, a component that decides what a vehicle should do next. In simpler two- and three-wheelers — like the e-rickshaw in this story — that job often falls to the motor controller instead, which directly controls how much power reaches the motor.

Either way, there’s a component between the accelerator and the engine that checks whether the vehicle should actually do what you’re asking for. It looks at your speed, whether the brake is pressed, whether the battery or motor is too hot or too cold, and whether anything else has gone wrong. Only then does the vehicle decide how much power to deliver.

Then, there’s the ‘BMS’ or Battery Management System. If you don’t know what you’re looking at, this can just seem like a fancy battery percentage detector. But to NXP and Texas Instruments, the two major suppliers of this technology, the BMS is actually a safety system. Even if the rest of the vehicle asks for full power, if the battery itself isn’t in a safe state, the BMS can say no.

This is what, it is believed, were behind the e-rickshaw cases. The apps reportedly connected to the system over Bluetooth, and triggered a command that stopped it from supplying power. When the vehicle asked the battery for power, the tampered BMS refused it.

There are other software systems too that can limit power. The motor, for instance, can cut back if it’s overheating. Traction control can do the same if a wheel starts slipping. And so on.

Keeping everyone in the loop

All of these systems — the VCU, the BMS, and others — carry information. But having information localised to one component isn’t enough; that information must quickly reach the rest of the vehicle. If a vehicle is skidding, for instance, that information can’t remain in the wheel; it must be carried to the VCU so that it can adjust what’s happening.

That’s the job of the ‘CAN bus’, or the ‘Controller Area Network’.

In modern EVs, controllers like the VCU and the BMS pass messages to each other over one or more of these networks. These work a little like a shared line that every part of the vehicle can read from. The battery, for instance, might post that available power is reduced. The brakes might post that they’re not being pressed. Any component that needs that information, then, reads it off the same line, avoiding the need for a private wire running to every other part.

Simpler vehicles work a little differently. Basic e-rickshaws, for instance, may use simple. analogue wiring instead of a CAN network.

From signal to spin

Once the VCU and the BMS agree on how much power to allow, that power has to reach the motor in a form it can actually use. This, again, is the domain of software.

A battery only gives out direct current, or DC. Picture it like water flowing steadily, in one way, down a pipe. Basic electric vehicles, including simple e-rickshaws, use this power directly — with DC motors running on a simple motor controller.

But modern EVs need alternating current or AC. Picture this current like water alternatively being pushed and pulled rapidly in both directions, instead of flowing one way. And so, something has to sit between the battery and the motor, converting the DC power to AC power. That something is the inverter, which Texas Instruments describes as the main power-processing system inside an EV. It adjusts current thousands of times a second.

Only once the inverter has done its job does the motor actually turn, in turn spinping the wheels. Even then, the system keeps watching itself. Sensors report back how fast the motor is spinning, how much current is flowing, and in more advanced vehicles, whether a wheel is slipping — and the car adjusts accordingly. These decisions get revised many times a second.

All of this is orchestrated by software. An EV doesn’t simply receive one instruction and carry it out. It keeps measuring, calculating, and correcting, for as long as the wheels turn.

Slowing down, charging up

The same works in reverse when you slow down.

Lift the accelerator or touch the brake, and the motor now acts as a generator. Electricity goes back into the battery rather than flowing out. This is called regenerative braking — a standard in most modern passenger EVs.

Where it exists, it takes the same kind of coordination as speeding up. The BMS decides how much energy the battery can safely take in. The motor controller decides how much regenerative braking the motor can produce. In more advanced EVs, software decides how much the vehicle slows because of the motor winding down, and how much comes from the actual brake pads. Software also checks when the battery is full or too cold, cutting off the motor and letting regular brakes do more of the work. Slowing an EV down, in other words, is partly a software decision too.

Likewise, charging an EV takes software too.

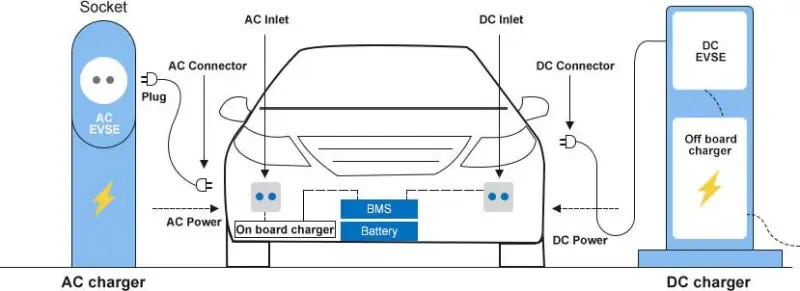

You can’t plug in an EV the way you fill a tank. The vehicle and the charger first exchange safety and power information, working out whether the connection is safe and what the battery’s temperature and charge level allow.

A battery, for instance, can only take in DC, but the power from a wall socket is A. Something has to convert it. During ordinary home charging, the vehicle does this conversion itself. During DC fast charging at a public station, the station does that conversion itself before the power reaches the car. But because these chargers push much more power, the car and charger keep exchanging information throughout the session, checking things like current and temperature again and again as the car charges. Meanwhile, the BMS keeps monitoring the pack throughout, looking for any issues that might need charging to stop midway.

Why EVs go online

All of this takes connectivity.

There is, of course, connectivity inside the vehicle, as its components talk to each other. But the vehicle also communicates with the outside. EVs plug into nearby wireless, Bluetooth or Wi-Fi — matching with things like a diagnostic tool, phones, keys, or a battery app. This is the kind of link the BAT-BMS app used.

Many are also connected to the internet or the cloud, usually over a mobile network. This supports things like navigation, remote monitoring, fleet tracking, and software updates sent from much further away.

This connectivity isn’t inherently a flaw. In fact, it’s usually a feature. It’s what lets an owner check charge remotely, or have a fleet operator track dozens of vehicles at once. This is what makes over-the-air updates possible, letting a manufacturer push new code to a vehicle already on the road, much like a phone receiving an update. India’s Ather has built much of its scooter business around this idea, publishing a running history of updates to its vehicles’ software.

But if there’s one thing the e-rickshaw episode has taught us, it’s that there’s a flip side to this connectivity. If it lets someone outside tap into the system without checking who they are, the level of control they get can be powerful. Since so much of the vehicle runs on software, a malicious party can meddle with anything — from what its screens and dashboards show, to how it charges, to its different ride modes, and more. The e-rickshaw’s discharge control, for instance, likely existed for a legitimate reason, such as maintenance or battery protection. But once an unauthorised phone connected with it, it became a killswitch.

Who owns the code EVs run on

Who, then, is responsible for making sure nothing goes wrong?

Like so much of the auto industry, every car bears the fingerprints of many vendors. The code rarely comes from one place. A battery-pack company or specialised electronics supplier, for instance, might provide the BMS hardware and firmware. A different company might build the app that talks to it. A third company might supply the vehicle’s central computer. Firms such as Bosch, KPIT, Tata Elxsi, and Vector all work as engineering partners across this stack. This spread makes responsibility harder to pin down.

Say, a battery from one company carries Bluetooth hardware. It is controlled by an app from a second company, and talks to the rest of the vehicle through a third company’s software. If someone interferes with the car, who is responsible?

In fact, software can become a persisting problem. When mechanical parts break down, they can usually be inspected and fixed by any independent workshop. Software is different — most workshops are unlikely to have the tools needed to even diagnose software issues. If the company behind some software shuts down, or a manufacturer switches off its servers, some features can simply stop working.

The answer lies in standards. India, for instance, has developed AIS-189 and AIS-190, modelled on UN regulations called R155 and R156. These make sure vehicle software is built and updated securely, avoiding the kind of problem the e-rickshaw incident revealed. But these rules are built mainly around cars, trucks, and buses.

Small two- and three-wheelers like e-rickshaws are exempt. Unfortunately, these are the very vehicles improvised together with batteries, BMS hardware, mobile apps, and vehicle components all coming from different suppliers. They’re also more likely to be serviced by independent workshops that may lack diagnostic tools.

Back to the stalled rickshaw

We began this story looking into a prank carried out with a Bluetooth app. That revealed something much larger, however: a modern EV isn’t simply a battery replacing a fuel tank in a regular car. It’s an electronically controlled system, with software orchestrating the battery, motor controller, and other components repeatedly.

That software can make vehicles safer and more efficient. It can allow faults to be diagnosed or corrected through remote updates. But it can also produce failures. Everything mechanical in the vehicle can work just fine, and it can still sit still, because somewhere inside, a computer has said no.

Where are the priorities in India’s priority sector lending norms?

Recently, SBI Research published a report in support of an interesting request on behalf of the country’s largest commercial bank. It wants roads, highways, airports, ports, and energy corridors to qualify as priority sector lending (PSL).

If adopted, SBI could count the massive infrastructure loans already sitting on its books towards the 40% of lending that the RBI mandates must flow to underserved sectors of the economy.

But wait. Does that mean infrastructure is being considered an underserved sector? After all, infrastructure is a hot sector where loans tend to be highly-rated and often backed by the government. If the numbers are to be believed, it’s not starving of credit currently.

What does it even mean to be underserved, then?

You see, the PSL framework was first formalised in the early 1970s with a simple ethos: left to themselves, commercial banks would lend to the safest, most profitable borrowers, ignoring everyone else. Sections of society like small farmers, tiny businesses, and artisans, who were most in need of credit, were precisely the ones the banking system left behind. PSL was the government’s attempt to force banks to fill that gap by demanding they lend 40% of their credit to designated sectors, or face penalties for falling short.

But what counts as a “priority sector“ has never stayed still.

Over the past five decades, the PSL basket has expanded, contracted, been fought over by regulators, bankers, and politicians, and expanded again. It has changed significantly from what PSL set out to be. The story of PSL is really the story of a perpetual negotiation between the government’s social objectives and the banking system’s commercial instincts.

And, as we shall see, the compromises that emerge are rarely clean.

The purpose of PSL

To understand why PSL generates so much friction, you need to understand that the framework deals with three separate questions whose answers often clash with each other.

Social safety or industrial policy?

The first question: is PSL a social safety net, or is it industrial policy?

What do we mean by this? Like we said earlier, when PSL was instituted after the large-scale nationalization of Indian banks in the 1970s, the intent was overwhelmingly social. Banks were directed to lend to agriculture, MSMEs, or even social infrastructure like schools and healthcare facilities that the formal financial system neglected.

But PSL also serves a second function: steering credit toward sectors the government considers strategically important. In fact, this is the story of many of the East Asian economic successes, like Japan, South Korea, and China. They forced cheap bank loans to be channelled into heavy industry and manufacturing sectors like cars, toys, clothes, and so on.

These two functions can complement each other, of course. However, they can also contradict each other at times. With industrial policy, you may often end up directing loans primarily to large enterprises in important markets because that’s the easiest way to bolster economic output. But those businesses need credit far less than small, struggling firms.

India has often tried to do both social equity and national development under a single 40% target. Export credit was once added in the PSL norms. Meanwhile, renewable energy got its own category in 2015. Other social infrastructure sectors have always been folded in. But the tension between those two goals has never been truly resolved.

Priority status

The second question: when does a sector actually deserve priority status?

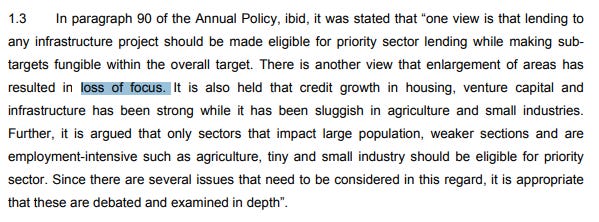

By the early 2000s, the PSL basket had ballooned with additions across successive decades, and the RBI knew this had become a problem. After all, if so many industries get priority status, you dilute credit away from the places that truly need it.

In 2005, the RBI constituted an internal working group chaired by C.S. Murthy to figure out what should stay and what should go. They noted that the PSL norms suffered from a “loss of focus” by granting PSL status to so many sectors.

The panel defined 5 conditions for inclusion into PSL. A sector deserved priority status only if it:

affected large sections of society,

was important to the national economy,

primarily benefited small borrowers,

faced difficulty in accessing bank credit,

generated substantial employment.

The committee recommended narrowing PSL down to just four core segments: agriculture, small-scale industries, small business, and education loans.

Incentives of banks

The third question: what do commercial banks actually want?

Banks love lending to large, well-rated corporates, as well as individuals with high credit scores. The risk of these loans going bad is very low, and the return is assured.

PSL loans have historically been the opposite: small-ticket, high-transaction-cost, and at high risk of turning into non-performing assets (NPAs). The Narasimham Committee, which was formed in the wake of the 1991 liberalization, pointed out that 47% of all bank NPAs at the time came from priority sectors, and recommended slashing the target from 40% to 10%. But the government rejected the proposal outright, fearing political backlash and credit disruptions in rural constituencies.

The disagreements

These three questions have caused multiple historic disagreements in Indian banking. We’ll cover three of those disagreements.

Sector creep

The first was sector creep.

In the 2000s, you had new industries emerge: like software, venture capital, and so on. Their lack of maturity implied that they might have needed credit support. In fact, venture capital was once included in the PSL norms!

Which is where you probably asked the question the RBI eventually asked itself — why does venture capital need credit support? Raising loans for an industry like that should be very easy, and it was. That’s why eventually, VC’s PSL status was revoked.

Such problems even occurred within sectors that were non-emerging.

Take housing, which is a PSL category. The initial logic of making housing a priority sector was that shelter was a universal human need. If the only housing loans doled out were high-ticket, urban ones, rather than small and rural, that would violate the spirit of PSL.

Except, it is that inclusion of high-ticket loans that made it a favorite of bank managers. In 2015, a primary survey of 60 bank branch managers conducted by economists from SBI found that all of them considered housing as the easiest PSL category to underwrite. By contrast, almost none of them found renewable energy or social infrastructure easy categories to lend to, and hence had very limited exposure there.

The result was predictable. The share of PSL directed to agriculture fell from 43% in 1980-81 to 35% by 2014-15. Small-scale industries saw an even sharper decline, from 38% to just 17% over the same period. The basket was growing, but the grassroots sectors that PSL was designed to serve were getting a shrinking share of the pie.

David and Goliath

The PSL norms have not just swung back and forth between sectors, but also between sizes of the businesses they should lend to.

Take, for instance, agriculture. Banks were constantly routing huge loans to agribusinesses and wealthy farmers while claiming to meet their agricultural PSL obligations. That’s why, in 2005, the Murthy committee said that loans above ₹1 crore to corporates would only get one-third weightage when counting toward direct agriculture targets. You could still lend to big agri-businesses, but it wouldn’t count for much in the final PSL ratio calculation.

Another similar example was that of export credit. Export credit typically involves large-ticket loans to big corporates, since those are often the most powerful Indian exporters. But the RBI has typically restricted its inclusion in the PSL norms because such exporters often have access to other forms of capital, like bonds and external commercial borrowings. They don’t need PSL, and their inclusion would crowd out grassroots sectors.

The denominator problem

A third disagreement in PSL norms stems from how it’s calculated.

Before 2007, a bank’s PSL loans were calculated as a percentage of a metric called Net Bank Credit (NBC) — if it met 40%, the bank met its PSL obligations. But the calculation of the NBC required deduction of deposits from non-residents, and off-balance sheet instruments like trade finance. Now, foreign banks with Indian presence had portfolios loaded with exactly those, while having far fewer domestic deposits. That would lower their NBC denominator considerably, inflating their PSL ratio unfairly compared to domestic banks.

Another issue with the NBC was that it was calculated based on a bank’s outstanding advances at the end of a single, specific day. But PSL is a long-term mandate of how many loans were disbursed in a whole year.

So, if a bank recovered some bad debts better, it would reduce both numerator and denominator by the same amount. When that happens, the PSL ratio actually falls, and the bank is penalized for doing its job better. Conversely, unrecovered bad debts counted as outstanding credit, meaning that, In turn, they would be included as PSL loans, inflating the ratio artificially.

So, in 2007, the RBI came up with another metric called Adjusted NBC (ANBC), which improved over NBC’s issues.

But the ANBC had new problems of its own. For one, the ANBC allows banks to deduct the outstanding amounts they raise through bonds for long-term projects like infrastructure and housing. This lowers the denominator, seemingly making it easier for banks to get closer to their PSL requirement. However, the loans that banks dole out for those projects are not counted as PSL, offsetting the earlier deduction in the denominator. This is also directly relevant to SBI’s request to include infrastructure in PSL.

Both NBC and ANBC suffer from a structural issue: it is a credit-based metric that ignores statutory reserve locks. When banks collect deposits, they must immediately lock away a sizable portion of those funds to meet the state-mandated Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR). No deduction is made in the ANBC for these ratios even though this money cannot be used for loans. This is why banks have been advocating moving away from ANBC towards a metric that represents their lendable resources.

Why infrastructure, and why now?

This is the context in which SBI’s demand lands.

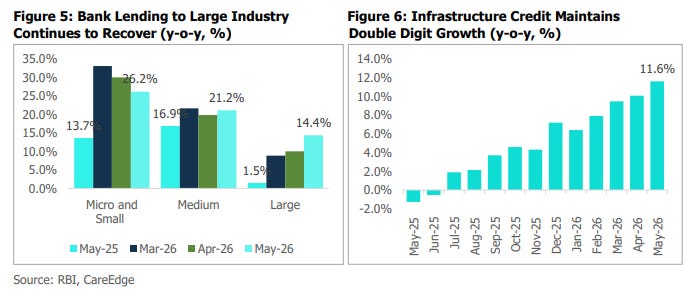

India is in the middle of a historic infrastructure push that includes national highways, dedicated freight corridors, high-speed rail and metro, port modernisation, etc. The capital being deployed is enormous, and banks like SBI are natural financiers for these projects. If infrastructure qualified as priority lending, SBI could instantly reclassify a significant chunk of its existing corporate loan book as PSL-compliant.

And SBI has plenty of incentives to push this.

As per the EAC-PM, SBI’s direct priority sector lending averages just 26.5% of its ANBC, well below the 40% mandate. SBI pays the penalty for this, which is parking 8% of its ANBC in low-yield RIDF deposits. Over the last few years, SBI has also been the biggest net buyer of PSL certificates among public-sector banks, which are issued by banks who have excess PSL loans and want to monetize it. Including infrastructure in PSL would significantly trim these costs.

SBI isn’t wrong that infrastructure matters for national development. But the same argument was made for venture capital and software in the early 2000s. Credit growth in infrastructure has been quite robust through normal commercial channels.

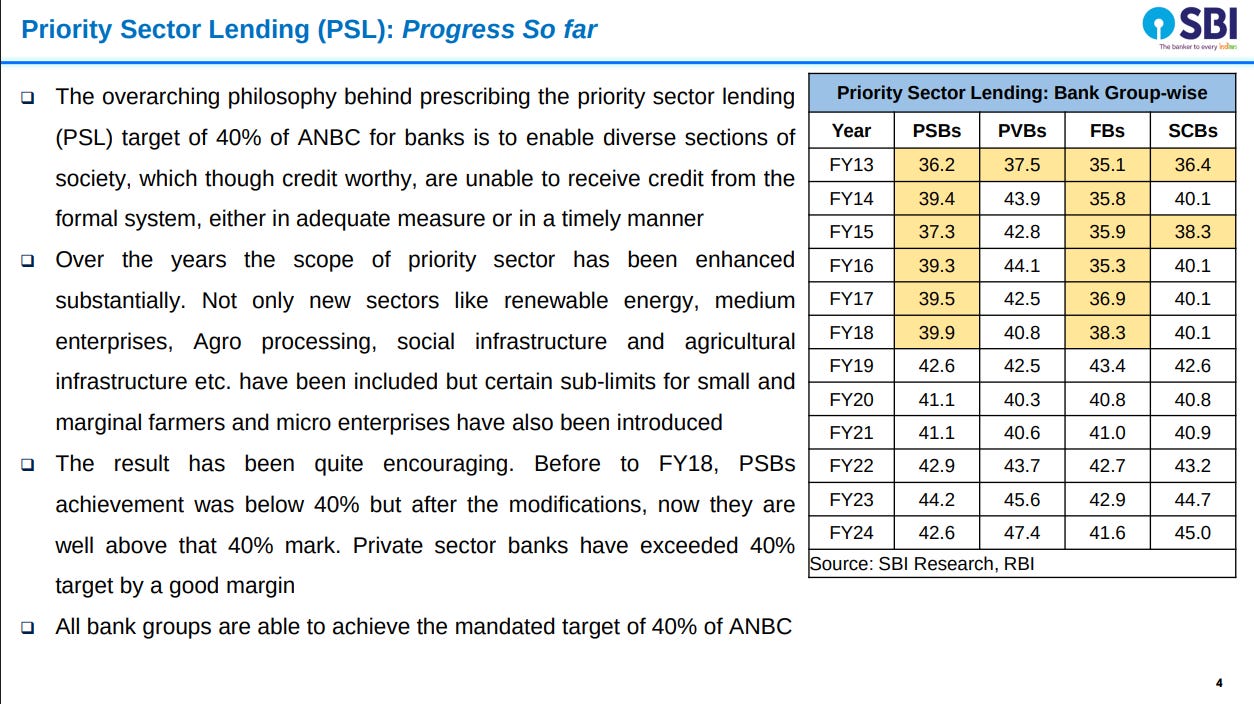

But at the same time, the frictions in today’s PSL norms can’t be ignored. SBI’s document specifically highlights the mismatch between making exemptions for long-term bonds and not exempting loans to those projects. There are many valid concerns raised by banks about the calculation of the ANBC. In fact, it wasn’t until 2019 when each type of bank crossed the 40% PSL threshold.

This is only emblematic of the long-standing, unsettled fight over PSL’s identity. Every expansion of the PSL basket makes it easier for banks to meet their targets but harder for the framework to serve its original purpose. Every contraction protects grassroots credit but intensifies the burden of risk and compliance on banks. As India’s economy sees new sectors demanding capital, the pressure to redefine “priority“ will only intensify.

But if every sector gets priority, no sector really has it.

These are the costs of having a single regulatory mandate simultaneously serve as a social safety net, an industrial policy tool, and a commercially-viable lending framework.

Tidbits

1. Two Irish aircraft lessors have applied to deregister four Boeing 737 Max planes leased to SpiceJet, citing mounting unpaid lease rentals. The airline, which currently operates around 60 daily flights on just about a dozen aircraft, says the targeted planes have been out of service for over a year, and their removal won’t affect active operations.

Source: Economic Times

2. HCLTech’s board has approved a strategic investment of up to ₹3,500 crore to build AI-dedicated data centres in India. The company wants to offer full-stack services — power, storage, compute, GPUs, and models — under one roof for enterprise and government clients. The move comes right after HCLTech’s recent $150 million investment in AI lab Sarvam.

Source: The Hindu BusinessLine

3. Scientists have identified erythrulose, a four-carbon sugar, swirling in a molecular cloud near the centre of the Milky Way, making it the most complex sugar ever found beyond our Solar System. The discovery strengthens the hypothesis that sugars essential to life may have originated in space and arrived on Earth via meteorites.

Source: Nature

4. A coalition of 12 Attorney-Generals has filed an antitrust lawsuit seeking to block Paramount Skydance’s ~$111 billion acquisition of Warner Bros. Discovery, arguing it would reduce competition in theatrical distribution, blockbuster releases, and basic cable licensing. We covered how Paramount battled Netflix to land this deal earlier.

Source: Livemint

5. Record-breaking heatwaves in Europe are squeezing the centuries-old Parmesan cheese business in Italy, causing cows to eat less and produce up to 10% less milk. Energy costs at the climate-controlled warehouses that store cheese wheels have spiked 30% during peak heatwaves. With production restricted to just five provinces and cows required to eat only locally grown hay and grass, the industry has little room to adapt geographically.

Source: Reuters

- This edition of the newsletter was written by Vignesh and Manie

Points & Figures by Zerodha

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how India’s retail lending landscape has transformed, using credit bureau data to reveal why lenders are moving away from unsecured loans and betting increasingly on collateral-backed credit.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

The Chatter by Zerodha

Our team at Markets spends a lot of time reading earnings call transcripts and listening to management interviews. Along the way, we come across plenty of interesting insights that are worth sharing.

That’s what The Chatter is for.

It’s a weekly newsletter where we dig through what India’s biggest companies are saying and bring you the most interesting insights into businesses, industries, and the wider economy.

Join us on WhatsApp, where we share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops so that you can read or watch it right away.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉