Delhi shifts gears on its electric gamble

Between carrots, sticks, and good old power grids.

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Delhi shifts gears on its electric gamble

What’s happening in India’s loan bazaar?

Delhi shifts gears on its electric gamble

Delhi has a vehicle problem.

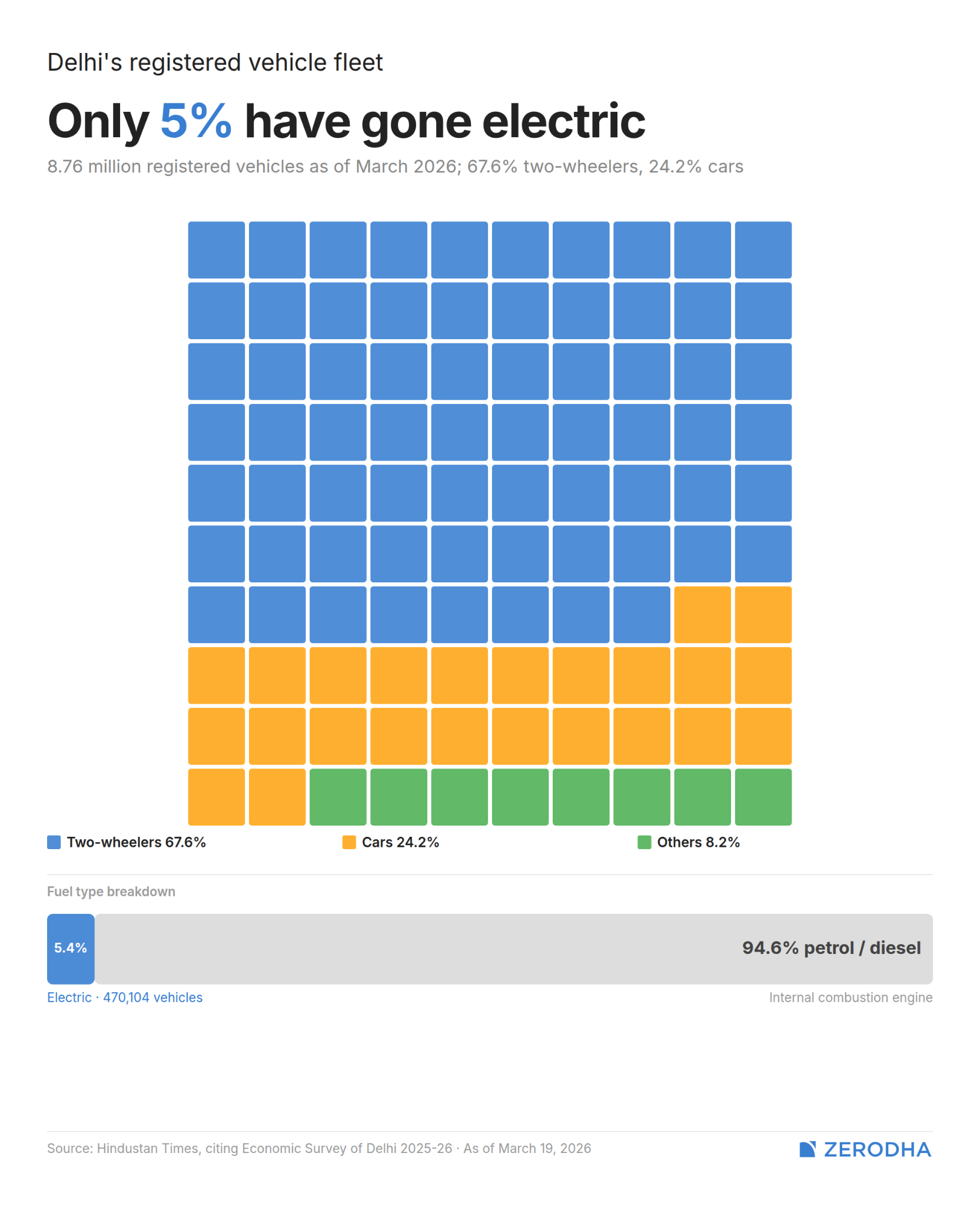

As of March 2026, India’s capital city has 87.6 lakh registered vehicles. As per a report by CSE, of all the pollution Delhi generates locally (as opposed to what blows in from surrounding regions), those vehicles account for over half.

Why that matters is because while Delhi can’t control crop-burning in Punjab or dust storms from Rajasthan, it can control what comes out of tailpipes on its own roads. Arguably, transport is the biggest lever the local government can actually pull to control pollution.

So, partly to respond to this problem, Delhi just announced a new draft EV policy.

If it passes through, it would be one of the most aggressive urban EV transitions attempted anywhere in India. Not because the subsidies are extraordinary, but because the policy is the equivalent of someone putting their foot down. Simply, it sets hard deadlines after which you simply cannot register a new petrol or diesel vehicle in key categories.

To understand how we got here, we need to go back a few years first.

From incentives to mandates

This isn’t Delhi’s first EV policy — that was notified nearly 6 years ago.

Its goal was ambitious: EVs should make up 25% of all new vehicle registrations by 2024, and Delhi would become the EV capital of India. The approach was built on providing sweeteners for adoption, like subsidies to buyers, road tax waivers, scrappage incentives, and so on. It included a State EV Fund, which would be financed through pollution cesses and additional road taxes on petrol and diesel vehicles.

Since then, Delhi has 4.7 lakh registered EVs — about 5.4% of its total vehicle stock. EVs accounted for about 12.7% of new vehicle registrations in FY 2025–26. That’s a 29% jump in absolute numbers from the previous year, and well above the national average of around 8%. The city also consumes more electricity at public charging stations than any other state, and roughly a quarter of national public charging consumption.

Clearly, the policy was not a complete failure. But progress was much slower than envisioned.

After all, petrol and petrol-ethanol vehicles still held ~73% of new registrations in FY26. In the overall stock, ~95% of Delhi’s vehicles are non-EV.

The ticking clock

Where does the 2026 policy differ from the original? Well, mainly, the policy doesn’t just involve handing out carrots — it also involves sticks. In other words, it’s making a switch to EVs more mandatory.

The policy rolls out deadlines segment by segment, starting with the groups that put the most kilometres on the road every day.

The first wall comes for delivery and aggregator fleets. Delivery and ride-hailing vehicles (like Zomato scooters or Uber cabs) clock far more kilometres per day than a personal car or scooter. A delivery rider might do 80–100 km a day, while a personal commuter might do 15. Even a small fleet, in emissions terms, punches above its weight.

So, the policy basically bars any standard petrol or diesel vehicles to be inducted into existing fleets — be it two-wheelers, light commercial vehicles, or N1 goods carriers. A small exception was made for the BS-VI category of two-wheelers.

Then, the policy moves to three-wheelers. Starting 2027, three-wheeler registration in Delhi becomes effectively EV-only. This deadline directly impacts Delhi’s auto-rickshaw drivers. The CNG auto, which itself was once the clean alternative to the diesel three-wheeler, will have to begin its exit from new registrations. Existing CNG autos, though, don’t have to come off the road overnight.

And then, the policy targets everyday commute.

Starting April 2028, only electric two-wheelers can be newly registered in Delhi. Two-wheelers form the largest chunk of Delhi’s total vehicle stock at 67%. They are the default mode of transport for millions of middle-class commuters, students, and small business owners. Banning new petrol two-wheeler registrations is, in scale terms, the boldest bet the policy makes.

To be clear, none of these deadlines force people to scrap their existing vehicles. If, for instance, you already own a petrol scooty, you keep it. But if you’re buying new after these dates, electric is your only option.

Money on the table

The draft doesn’t just set deadlines, though. It tries to shape how and when people switch, who switches first, and what they switch out of.

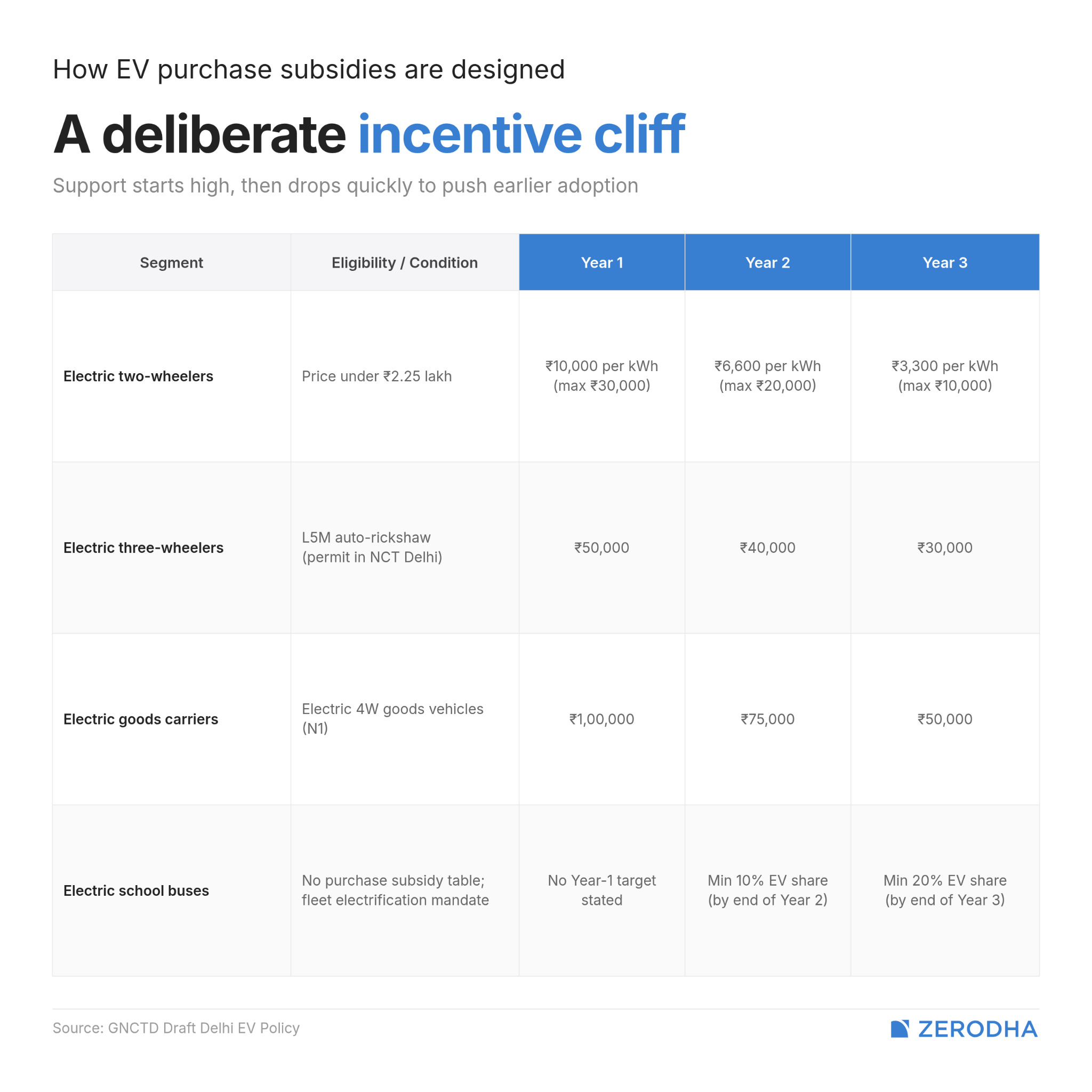

For instance, take how the purchase subsidies are designed. For electric two-wheelers priced under ₹2.25 lakh, the incentive falls sharply over three years — ₹10,000 per kWh (capped at ₹30,000) in Year 1, dropping to ₹6,600 in Year 2 and ₹3,300 in Year 3. The path is deliberately structured in a way to not be gradual, but more sudden. The message to consumers is to switch early, or pay a dearer price later.

A similar logic repeats across segments. Electric three-wheelers, for instance, get ₹50,000 in Year 1, tapering to ₹30,000 by Year 3. Goods carriers see the highest support, up to ₹1 lakh in the first year. The draft even targets school buses. Vehicles that run the most kilometres clearly get steeper slopes.

Then comes the second layer: scrappage, which also provides a sweetener, but with some tight strings attached.

If you scrap a BS-IV or older vehicle at an authorized facility, you get an additional incentive — ₹10,000 for two-wheelers, ₹25,000 for three-wheelers, ₹50,000 for goods vehicles, and so on. But the benefit is heavily conditioned with three criteria:

You will compulsorily need a Certificate of Deposit from the scrapper, without which you won’t receive any incentive.

You must buy the new EV within six months of that

The payment only goes to the registered owner via direct benefit transfer.

Put together, the financial design does three things at once: it pulls demand forward through tapering subsidies, targets high-impact segments where emissions reductions are largest, and uses scrappage to make holding on to older vehicles economically irrational.

Beyond subsidies, the draft proposes a 100% exemption on road tax and registration fees for all electric vehicles registered during the policy period — but with an important limit for cars. Electric cars priced up to ₹30 lakh (ex-showroom) get the full waiver until March 31, 2030. Above that, you pay full tax. In effect, this ensures that the subsidy primarily goes to middle-class buyers, and not the luxury segment.

There’s also a notable addition for strong hybrids — vehicles that combine a petrol engine with an electric motor and can run short distances on battery alone. The draft proposes a 50% reduction in road tax and registration fees for strong hybrid cars priced under ₹30 lakh.

Plugging into the grid

Now, this elaborate carrot-and-stick approach will only work if people can actually charge their EVs. The fear that you’ll run out of battery with no charger in sight is still a major barrier to EV adoption in India. The draft is cognizant of this and does try to tackle it.

One of the most notable requirements in the policy is that every OEM operating in Delhi must ensure at least one public EV charging station per dealer. There’s a minimum of three charging points for two and three-wheelers and two charging points for four-wheelers. Dealerships are already spread across the city and are natural places for people to stop and charge. This puts the onus on OEMs and dealers to be part of the solution, not just sellers of vehicles.

Beyond dealerships, the draft requires that all new civil infrastructure projects under the Delhi-NCR government must be EV-charging-ready, with adequate electrical capacity to enable charger installation. Land-owning agencies must periodically identify land parcels for charging and swapping deployment. The 2020 policy had already required that 20% of parking capacity in new buildings be EV-ready; the 2026 draft expands this to government infrastructure across the board.

On the coordination side, the draft assigns Delhi Transco Limited (DTL) as the nodal agency for the entire public charging and swapping network. It is tasked with assessing current and future EV charging load and coordinating power procurement with the power discoms.

But hardware and coordination are only part of the puzzle. The grid itself needs to be ready. If hundreds of thousands of EVs plug in every evening after work, that’s a spike in demand right when the grid is already under pressure.

To address that, the Ministry of Power’s 2024 EV charging guidelines encourage charging during solar hours. After all, charging at 2 PM, when solar generation is flooding the grid, should cost less than charging at 8 PM when everyone’s running their ACs. The Centre’s amendments to the Electricity (Rights of Consumers) Rules introduced Time-of-Day tariffs: electricity during solar hours should be 10–20% cheaper, while peak-hour rates should be 10–20% higher. Delhi’s regulator, DERC, has already engaged with ToD structures.

For apartment dwellers, though, the picture is more complicated. Delhi’s 2020 policy pushed for DISCOM-facilitated installation of private charging points, and the Switch Delhi portal runs a single-window process for charger installation. But installing a home charger can mean upgrading your household’s sanctioned electrical load, coordinating with a DISCOM-approved vendor, and maybe even setting up a separate meter. Each step adds time, cost, and uncertainty.

On top of that, in apartment complexes, parking and wiring are usually shared, and decisions on shared infrastructure are often controlled by RWAs. Who pays for the wiring upgrade? Where does the charger go? Can others use it, and what happens if the RWA refuses permission? These are conflicts that the policy is yet to address.

What it all comes down to

As of March 2026, Delhi has over 3,100 charging stations and 893 battery swapping stations. A 2022 charging action plan had targeted 18,000 charging points by 2024 — by their own admission, they’re quite far behind.

Delhi’s draft EV Policy 2.0 is, at its core, a bet that a mixture of reward and punishment can do what incentives alone couldn’t. That could be a highly welcome approach. But its success will depend on a lot more than just a shift in framework. What also matters is whether chargers show up where people actually park, whether the grid can handle the load, and whether supply keeps pace with the demand the mandates will create.

If Delhi pulls it off, it could become the template for other Indian cities — and it is already one of the leading adopters of EVs in India. If it doesn’t, the lesson is just as clear: mandates without matching infrastructure are just deadlines that get pushed.

What’s happening in India’s loan bazaar?

Two rating agencies — CRISIL and CareEdge — released reports this week about India’s “securitisation market“. Those reports are filled with terms that, if you saw them in a headline, would probably make you scroll right past. Pass-Through Certificates. Direct Assignments. Asset-backed securitisation. Mortgage-backed securitisation. Priority Sector Lending Certificates.

We came across a similarly cryptic CRISIL headline last year at the same time — about ARCs and Security Receipts — and spent a whole piece decoding it. This time, we want to do the same thing. We’ll start from the very basics of what securitisation actually is, what all these acronyms mean, why they exist, and then get into what these reports are actually telling us about the health of Indian lending.

What does it mean to “securitise” a loan?

Here’s a simple way to think about what it means to securitize a loan.

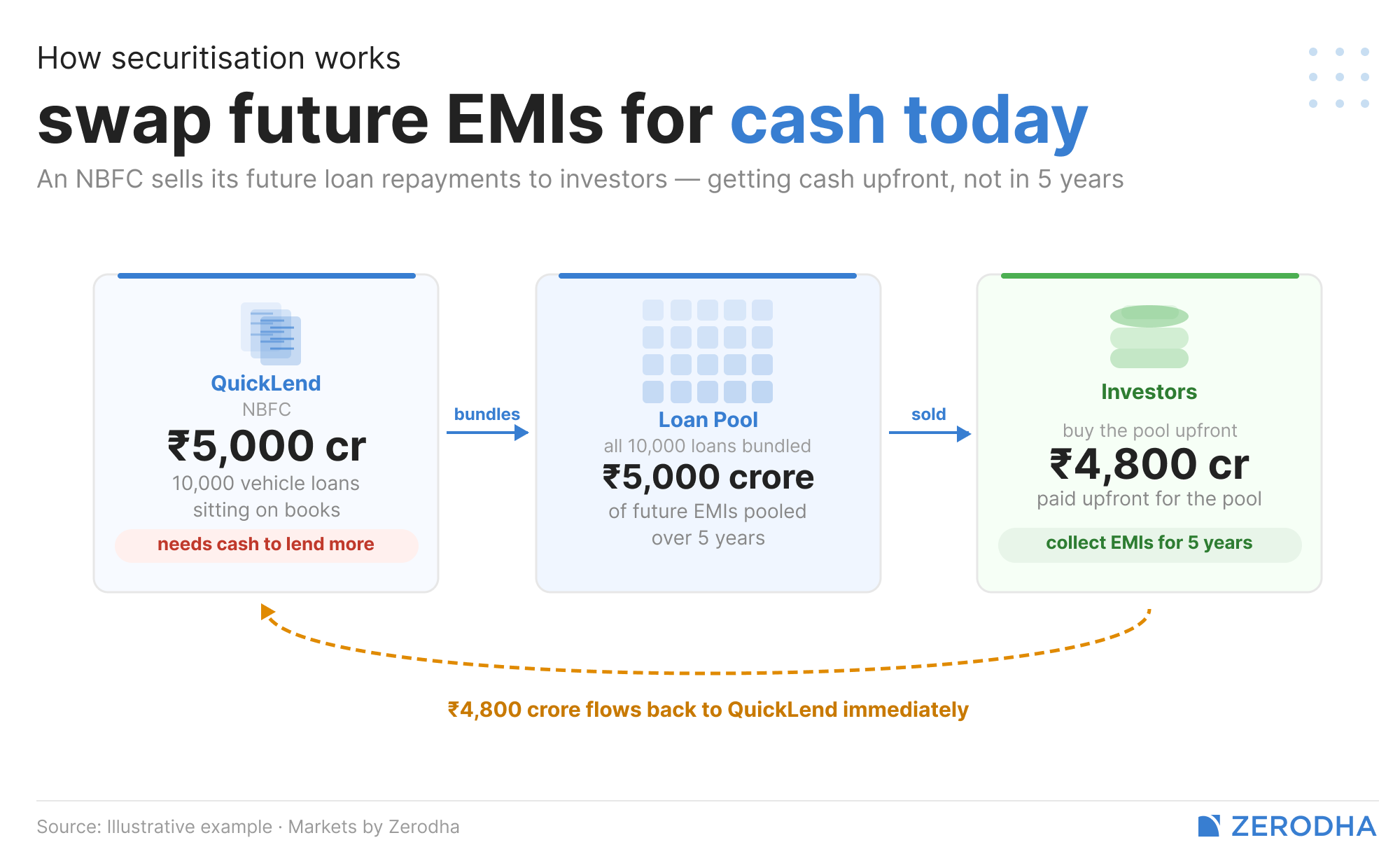

Say an NBFC — let’s call it QuickLend — has given out 10,000 vehicle loans, each worth about ₹5 lakh. That’s ₹500 crore of loans sitting on its books, each of which will be repaid through monthly EMIs over the next five years. QuickLend has an asset — the right to receive those future EMIs — but it doesn’t have cash today. And it needs cash today, because it wants to lend more.

So, QuickLend does something clever. It takes those 10,000 loans, bundles them into a pool, and sells that pool to investors. Now, the total EMIs that will flow in over five years add up to more than ₹500 crore, because borrowers are paying interest on top of principal.

But investors aren’t going to pay the full future value upfront. They’re taking on the risk of some borrowers potentially defaulting, plus the money comes in over years rather than immediately. So they pay QuickLend a discounted upfront amount — say ₹480 crore — and in return, they get the right to collect those EMIs over the next five years.

The gap between what they pay now and what they collect over time is their return. QuickLend gets its cash, the investors get a stream of repayments that should earn them a decent yield, and everybody’s happy.

That’s securitisation. You’re taking a pool of loans and turning it into something that can be bought and sold. You’re making it into a security, hence the name.

In India, there are two ways securitization works.

The PTC route

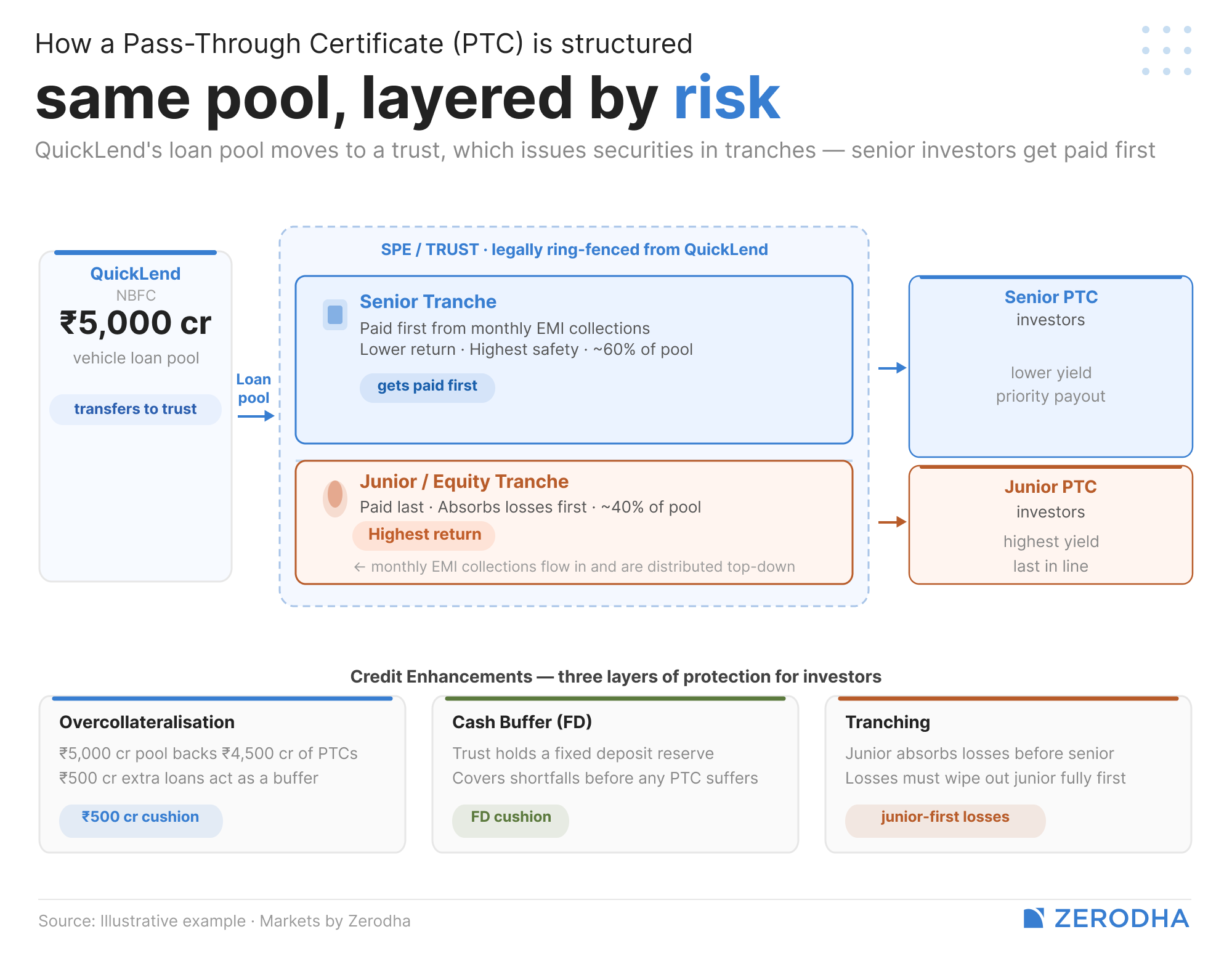

The first route is a Pass-Through Certificate (PTC). Here, QuickLend transfers its ₹5,000 crore vehicle loan pool to a separate trust called a Special Purpose Entity (SPE). This SPE is legally ring-fenced from QuickLend’s business, and it issues securities in the form of PTCs to investors.

But, not all investors want the same deal. Some want safety above all else, and are okay with lower returns as long as they get paid. Others are willing to take more risk if the reward is higher.

So the trust doesn’t issue one single security, but does so in tranches. Think of a tranche like a building with floors. The top floor — the senior tranche — gets paid first from the EMI collections that flow in every month. As long as the pool performs even moderately well, these investors get their money. The ground floor — the junior or equity tranche — gets paid last after everyone above has been taken care of. But it also earns the highest return. If defaults arise, the losses eat into the ground floor first.

On top of this, the trust holds a cash buffer — a fixed deposit that acts as a cushion. And the loan pool is deliberately made larger than the securities issued against it. Remember QuickLend’s ₹500 crore vehicle loan pool? The trust might issue only ₹450 crore worth of PTCs against it. That extra ₹50 crore of loans is called overcollateralisation — it means that even if a bunch of borrowers stop paying, the remaining pool is still large enough to cover what investors are owed.

All of these protections together — the tranching, the cash buffer, the overcollateralisation — are collectively called “credit enhancements.”

The DA route

The second, simpler route is a Direct Assignment (DA).

QuickLend sells the loan pool directly to a buyer — almost always a bank — with no credit enhancements. The bank takes the loans onto its own books and bears the full credit risk. The RBI actually prohibits credit enhancements in DAs. They’re cheaper and faster to execute, which is why they’ve historically been popular. But because there’s no structural protection, only RBI-regulated entities (like banks) can be buyers.

In both cases, the original lender keeps collecting the EMIs and earns a “servicing fee”, while the borrower usually doesn’t even know the loan has changed hands.

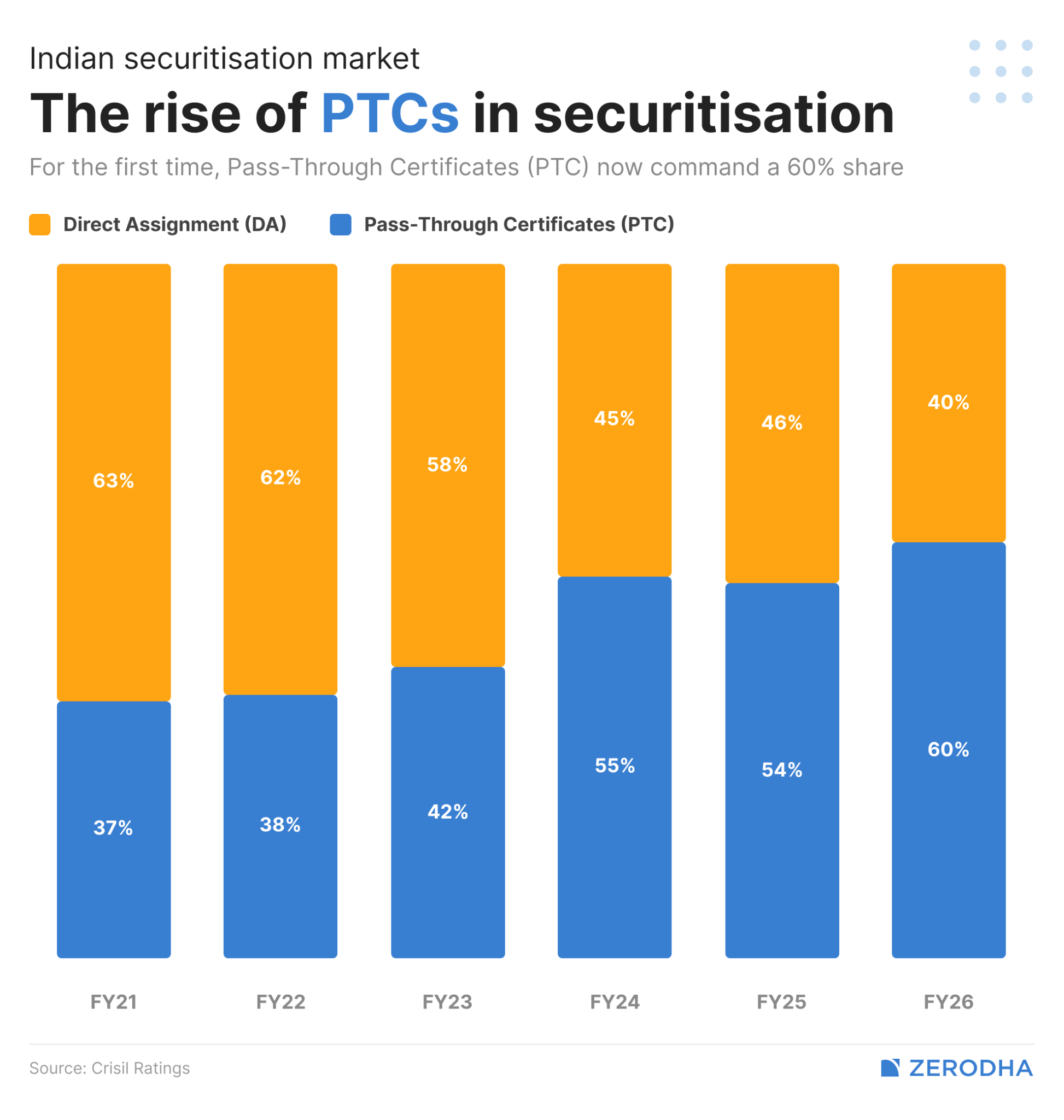

In FY26, PTCs accounted for roughly 60% of all securitisation transactions — an all-time high — and DAs made up the remaining 40%. We’ll come back to why PTCs are gaining ground.

What if the loan is bad?

Everything we just described applies to borrowers who are paying their EMIs on time. Securitisation is a funding tool for good loans. But what happens when loans go bad and the loan becomes a non-performing asset (NPA)?

That’s a different market entirely — and one we covered in detail last year. When loans go bad, banks sell them to Asset Reconstruction Companies (ARCs), which issue Security Receipts (SRs). They represent the bank’s ongoing stake in whatever the ARC manages to recover. Unlike securitisation, where investors are buying a stream of healthy EMIs, SRs are a bet on whether a troubled borrower’s assets can be liquidated for anything at all.

So think of it this way: securitisation (PTCs and DAs) is for good loans being sold for funding. Security Receipts are for bad loans being sold for recovery. Same principle — loans being transferred from one entity to another — but entirely different risk profiles and buyers.

What India deliberately banned — and why

If some of this sounded familiar, it’s probably because you saw a movie called The Big Short.

The movie was about one of the causes of the 2008 global financial crisis. American banks made terrible mortgage loans to people who couldn’t afford them, packaged those loans into securities, and then did something truly reckless: they re-securitised those securities. They took pools of mortgage-backed securities, which were already a pool of loans, and bundled those into new instruments called Collateralised Debt Obligations (CDOs).

That’s not all. They created CDOs of CDOs, and then added more layers of securitization that we won’t go into the details of here.

Now, the RBI looked at that catastrophe and drew a hard line, banning re-securitisation as well as synthetic securitisation. Only simple, pass-through securitisation of actual performing loans is allowed. The originator must hold the loans for a minimum period before selling them (3-6 months depending on tenure), and must retain at least 5-10% of the pool, ensuring they have skin in the game.

The result is a market that deals in straightforward, granular retail loans — vehicle EMIs, gold loan repayments, microfinance instalments — rather than the multi-layered, opaque structures that added fuel to the fire that was the global financial system.

What the FY26 data tells us

Now that we have the vocabulary, let’s get into what CRISIL and CareEdge are saying.

India’s securitisation market hit an all-time high of approximately ₹2.55 lakh crore in FY26. For context, this market was ₹1.13 lakh crore just four years ago in FY22 — it’s more than doubled.

But the headline number matters less than what’s underneath it. Three shifts stand out.

First, NBFCs have taken over the market. NBFC-originated deals accounted for 97% of all securitisation in FY26, up from 74% the year before. Bank originations collapsed from 26% to just 3%. This was overwhelmingly driven by one institution — HDFC Bank — which had aggressively securitised loans in FY25 to manage its post-merger balance sheet. That’s when it had absorbed huge amounts of advances, but little to no deposits from HDFC, causing the credit-deposit ratio to spike. So HDFC started to securitize its book, to release some funds, and once its credit-deposit ratio normalised, it pulled back almost entirely, and no other bank filled the gap.

For NBFCs, securitisation is how they fund themselves. Unlike banks, they can’t (mostly) take cheap deposits. They borrow from banks and capital markets at 1-3 year tenures, but lend at 5-7 years (or longer for housing). Securitisation solves this mismatch by converting future loan repayments into upfront cash. When the RBI raised risk weights on bank lending to NBFCs in November 2023, making bank credit more expensive, securitisation became even more critical.

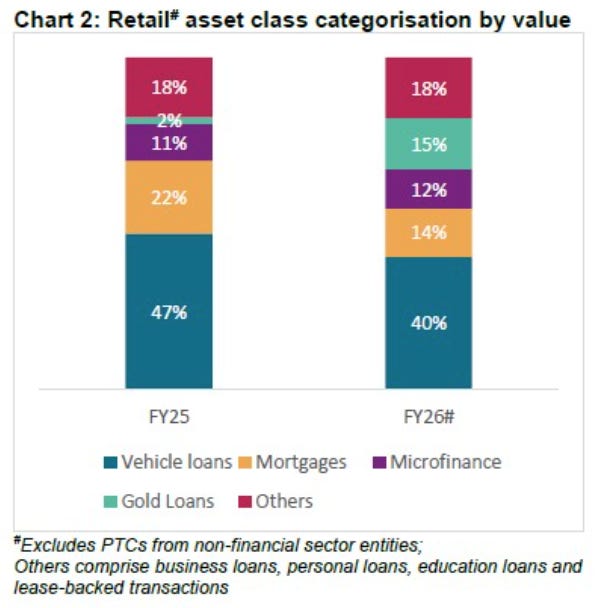

Second, gold loan securitisation came out of nowhere. In FY25, gold-loan-backed deals were barely a blip. But in FY26, they surged to 15% of the market, becoming the second-largest asset class behind vehicle loans. Gold loan disbursements had been rising sharply, up 94% year-on-year in Q3 FY26 alone, driven by rising gold prices and tighter unsecured lending norms.

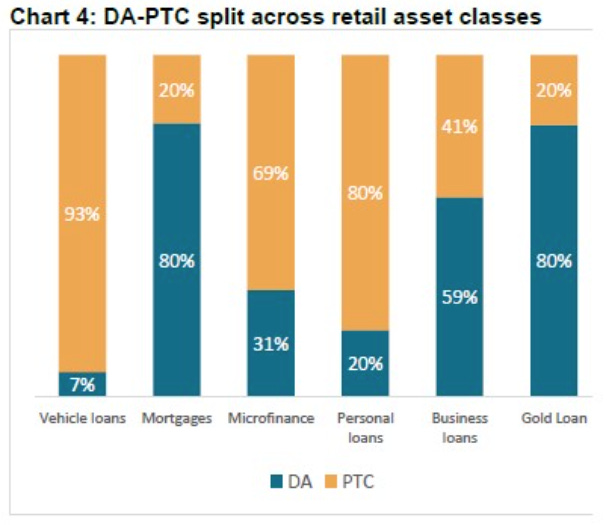

For investors, gold loan pools are close to ideal. The collateral is liquid, easily valued, and physically held by the lender. Loan tenures are typically under 12 months. If a borrower defaults, the lender auctions the gold — recovery is near-certain. These pools don’t even need PTCs; most gold loan securitisation happens through the simpler DA route, because the collateral itself is protection enough.

Third, microfinance (MFI) investors demanded structural armour. MFI loans held steady at ~12% of the market. But how they were securitised changed dramatically. The share of MFI deals going through the PTC route jumped from 30% to 69% in a single year.

That’s because the sector had just come off its worst asset quality cycle in years. Gross NPAs roughly doubled across the industry in FY25. Investors who’d been comfortable buying MFI pools through simple DAs got burned. They didn’t ever stop buying either, but they now demand the credit enhancements that PTCs provide. Investors want to stay, but on different terms.

Why banks are buying all of this

If NBFCs are selling these loan pools, who’s buying them? Well, that’s mostly banks, and not entirely voluntarily.

See, the RBI requires all commercial banks to lend 40% of their credit to “priority sectors“, like agriculture, MSMEs, housing etc.. Miss the target, and you must park the shortfall in a fund at NABARD earning returns that are below market lending rates. The problem is that priority sector borrowers are exactly the customers NBFCs reach well and banks don’t. So banks buy securitised pools of these loans from NBFCs, getting both a performing asset and meeting the priority sector criteria.

But there’s another way to do that: Priority Sector Lending Certificates (PSLCs). If Bank A has excess agricultural lending and Bank B is short, Bank B buys a PSLC from Bank A. There is no transfer of assets or loans. Bank B just gets the PSL “tag” for that year.

But, you might ask, why would a bank buy a securitised pool when it could just buy a PSLC? Well, a PSLC is a pure expense — you pay a fee and get nothing but compliance. A securitised pool, meanwhile, also gives you a decent yield along with compliance. For a bank with surplus liquidity, it’s an obviously better deal.

What does this market tell us about Indian lending?

Securitisation data is, in a sense, a health monitor for India’s credit plumbing. When volumes rise sharply, it can mean NBFCs are being squeezed on other funding channels. When investors shift from DAs to PTCs, it means they’re nervous about asset quality. When gold loan pools surge, it tells you something about how households are borrowing. When bank originations collapse because one institution pulls back, it tells you the market is still dangerously concentrated.

The FY26 numbers tell us that India’s securitisation market is maturing. The originator base broadened from 175 to over 190 entities, with the top 20’s share falling from 71% to 65%. The market is learning to price risk more intelligently, demanding structural protection where asset quality is uncertain and staying simpler where collateral is strong. NBFCs have permanently absorbed securitisation into their business-as-usual operations.

India has built a ₹2.55 lakh crore loan bazaar with strong guardrails and few glaring systemic risks. The question now is whether it can build the depth and liquidity to match the ambition.

Tidbits

India’s unemployment hit a five-month high of 5.1% in March as per PLFS. Urban areas experienced a notable increase in joblessness, contributing to the rise in the overall unemployment figure. Women continue to face greater unemployment challenges than men, while the youth demographic also showed a troubling uptick in joblessness.

Source: Economic TimesThe 2026 summers are set to beat the heat record of 2024. The India Meteorological Department (IMD) has issued official heatwave warnings for isolated pockets in central and eastern India starting mid-April 2026.

Source: Business TodayOhio-based defense manufacturer GE Aerospace and India’s state-owned Hindustan Aeronautics Limited have reached an agreement on technical matters for co-production of F414 engines, the two companies said in a joint statement issued earlier this week. The deal has been in the works for about three years and brings the partners closer to production.

Source: Business Standard

- This edition of the newsletter was written by Vignesh and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Deepak Shenoy on what’s happening with the rupee

Over the past few weeks, the rupee has been moving in ways that aren’t easy to explain. While higher oil prices and rising dollar demand tell part of the story, there’s a more technical layer beneath it. We spoke to Deepak Shenoy to break it down—especially the role of the offshore NDF market. It’s a conversation about arbitrage, RBI intervention, and why the rupee has been so erratic lately. More importantly, it raises a bigger question: are these fixes solving anything at all?

Thank you for reading. Do share this with your friends and make them as smart as you are 😉