Decoding the Vedanta Demerger

Can the demerger help the company bounce back?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

Vedanta’s great divide

A sovereign loan is never just a loan

Vedanta’s great divide

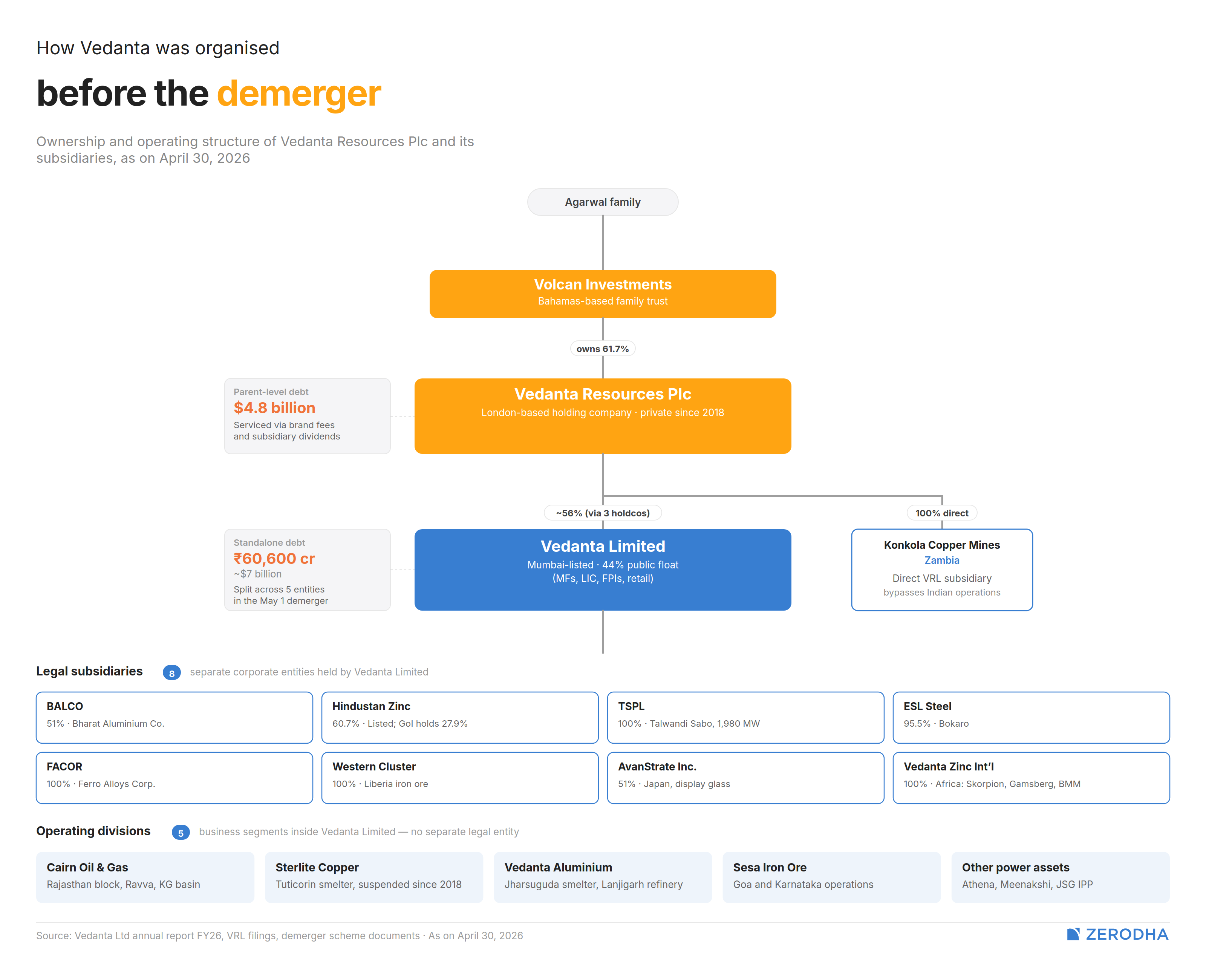

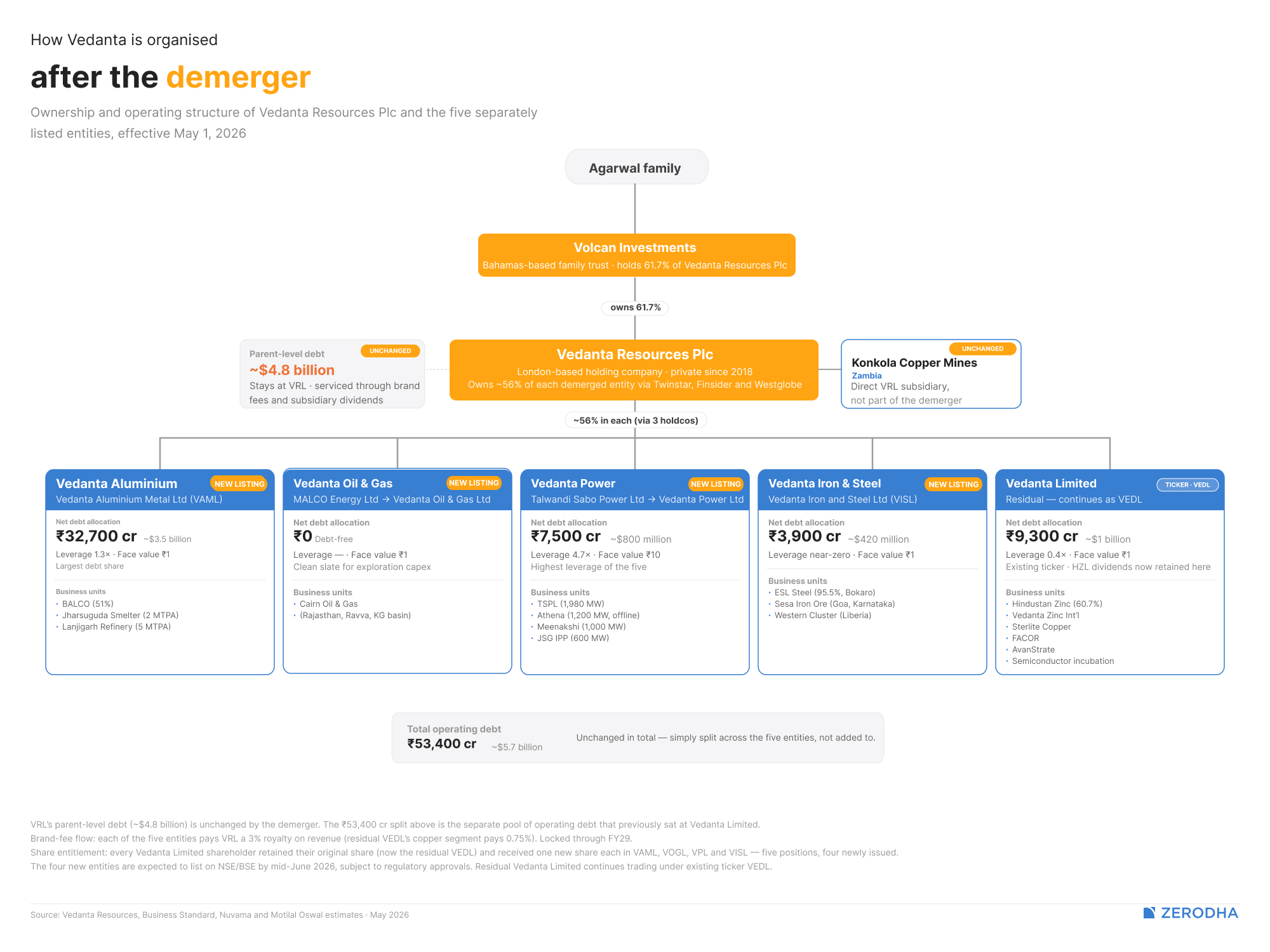

Anil Agarwal spent two decades assembling Vedanta into one of India’s most diversified resources groups. He has spent the last two and a half years taking apart the group’s crown jewel, Vedanta Limited. On May 1, the process completed. Vedanta Limited was broken into five separate listed companies — Vedanta Aluminium, Vedanta Oil & Gas, Vedanta Power, Vedanta Iron & Steel, and a residual Vedanta Limited that keeps the group’s stake in Hindustan Zinc and a few smaller businesses. By the end of June, all four new entities will start trading on Indian exchanges.

This marks one of the largest corporate restructurings in Indian history. The group’s sheer scale beggars belief. It’s one of India’s largest commodity producers. It controls roughly half of India’s primary aluminium market, runs India’s largest integrated zinc and silver business through its majority stake in Hindustan Zinc, and is one of the country’s largest private upstream oil and gas player through Cairn India. It also has substantial copper, iron ore, and steel exposure rounding out its portfolio. All of this is controlled through a holding company in London.

On April 29, two days before the demerger took effect, the combined Vedanta Limited delivered its last ever set of quarterly results: a swan song for the mining giant. Its parting numbers were some of the best it had ever posted — revenues up 29%, net profit up 89%, EBITDA margin coming to a record 44%, and leverage at its lowest level in fourteen quarters.

But that chapter is now closed; a new era lies ahead. Why did Vedanta decide to take this monumental decision? What happens when its five businesses head into their independent lives? Let’s dive in.

How we got here

Anil Agarwal was a 19-year-old in the mid-1970s when he moved from Patna to Mumbai, dropping out of school to trade scrap metal. He started the company that would become Vedanta in 1976, when he bought a small enameled copper manufacturer called Shamsher Sterling Corporation.

A decade later, he founded a new company, Sterlite Industries, to make telephone cables. Sterlite expanded into copper and aluminium through the 1990s, building India’s first private-sector copper smelter at Tuticorin in 1993, then reviving the defunct Madras Aluminium Company in 1995

It was in this established, multi-metal form that Sterlite walked into the Vajpayee government’s privatisation programme in 2001.

The central government was then trying to sell stakes in two of its largest resources companies. Sterlite bought into both. It picked up a 51% controlling stake in Bharat Aluminium Company (BALCO), and a 26% stake in Hindustan Zinc, which it later expanded into a majority. Both deals were controversial, with political critics disputing the valuations for years. In fact, the Hindustan Zinc disinvestment is still being heard in court, more than two decades hence.

Sitting above these was Vedanta Resources Plc: the London-based holding company through which Agarwal controls the group.

Going through London made sense back then. India’s capital markets weren’t deep enough to fund a multi-commodity resources business. The LSE, on the other hand, had an entire framework for a company like Vedanta: specialist resources analysts, the FTSE Mining Index, and an institutional capital base interested in emerging-market commodity bets. And so, Vedanta Resources listed there in December 2003, in the exchange’s second-largest IPO that year.

That money went into major acquisitions, like Zambia’s Konkola Copper Mines, or the iron ore mines at Sesa Goa. But the group’s most transformative deal was its $9 billion acquisition of Cairn India from Cairn Energy. By 2013, the whole portfolio was rolled together as Sesa Sterlite, which was renamed Vedanta Limited in 2015.

But the Cairn deal was also a curse. Roughly half of it was funded by acquisition debt, which was hard to shake off. It was the origin of most of the debt Vedanta still carries, an inheritance that has been rolled over and refinanced through international bond markets ever since.

By 2018, meanwhile, the rationale for the London listing had run out. The stock continuously underperformed peers like BHP and Rio Tinto. The LSE compliance burden, too, was high, and they saw a lot of backlash for the deaths of 13 protesters in Tamil Nadu. Agarwal took the parent private that October, paying roughly $1 billion in buyout costs. But this only added more debt to the company.

The demerger

All this debt was becoming a problem. From October 2022 onwards, Moody’s downgraded Vedanta Resources repeatedly: citing what it called an “unsustainable capital structure”.

Moody’s was pointing to a structural problem. The London parent had no operating cash flows of its own. It had been servicing its debt almost entirely from dividends and brand fees paid up by its subsidiaries. Its conglomerate structure was making refinancing harder. International bond investors looking at a consolidated Vedanta couldn’t see how much of the group’s cash would actually be available for its parent company’s needs.

Hundreds of millions were flowing out of the company to meet its debts. The parent was scrambling to refinance. It sold a 4.3% stake in Vedanta Limited for about $500 million in August 2023, raising Non-Convertible Debentures (NCDs), and spoke to private credit funds about short-term loans. But the pain wouldn’t relent.

By September 2023, Moody’s had downgraded VRL’s bonds to Caa3. They were practically speculative junk.

Vedanta’s structure, it appeared, had ceased to serve its purpose. The parent entity’s valuation had been dragged down by a conglomerate discount. Most of its value was tied to the Hindustan Zinc alone. The rest of its businesses — across aluminium, oil and gas, power, iron and steel, copper — were being valued at very little. They could be worth much more as five separately listed companies, each of which would attract sector-focused investors. If they were separate, each business would have a cleaner balance sheet than the consolidated entity, while distributing the parent’s debt-service burden across multiple cash-flow sources.

And so, on September 29, 2023, Vedanta announced its demerger.

What the demerger actually did

The demerger has turned every Vedanta Limited share into five. In addition to their original Vedanta Limited share, investors will get one share each of Vedanta Aluminium, Vedanta Oil and Gas, Vedanta Power, and Vedanta Iron and Steel. The four new scrips will start trading on Indian exchanges by the end of June.

Underneath this, though, are a variety of decisions on how the group’s existing policies and obligations will flow into the newer structure.

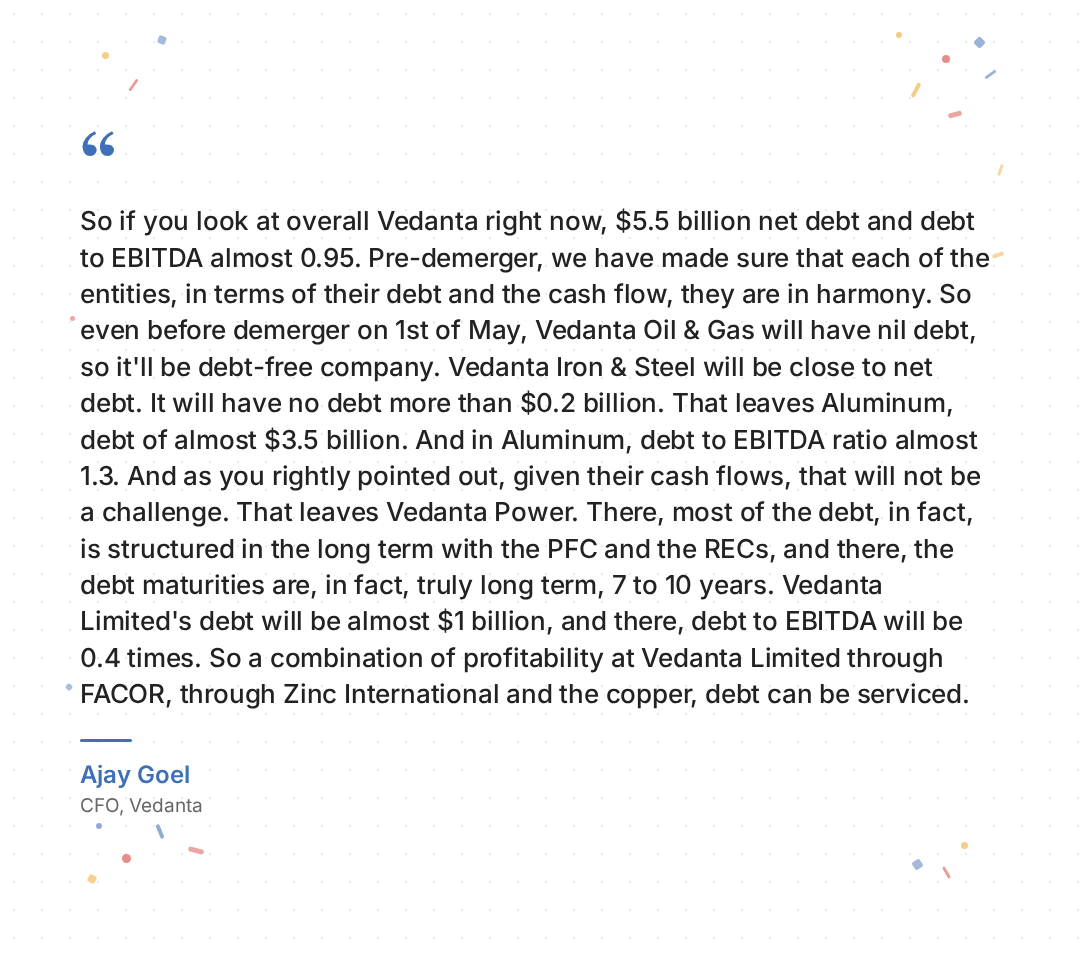

For one, the London-based parent’s debt was pushed down to its subsidiaries.

Net of cash, Vedanta Resources owed about $5.5 billion before the merger. Each of the new entities shall now inherit a portion. Vedanta Aluminium took the largest piece, of around $3.5 billion. Vedanta Power took over a chunk borrowed from Power Finance Corporation and REC, secured against its long-term power purchase contracts. The residual business of Vedanta Limited took about $1 billion. Another $200 million was parked at Vedanta Iron and Steel.

This structure was meant to match each piece of debt to the cash-generating ability of the inheriting entity. Its cash cow aluminium business, with incredible operating margins of ~40%, took on the most — especially since it has a clear growth runway, with planned increases in smelter capacity. Its power entity has long-dated power purchase contracts with durations of 15–25 years, and was therefore given long-tenor debt. And so on.

The second decision was a change in dividend policy.

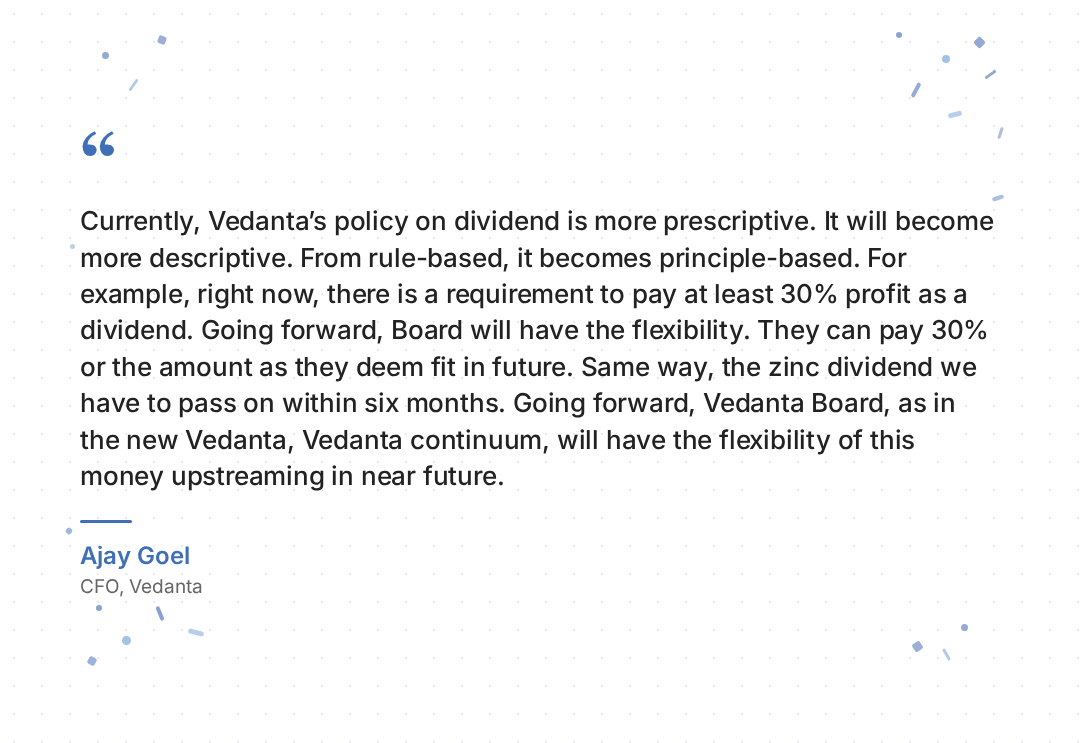

Consider this: Hindustan Zinc is by far the single largest cash generator in Vedanta, and it has long paid generous dividends to its shareholders. Vedanta Limited owns ~61% of HZL, the Indian government another ~28%, while the rest is public. When HZL paid a dividend, Vedanta Limited would get three-fifths of it.

What did Vedanta Limited do with that cash? Until now, it was heavily constrained. Under its current dividend policy, it had to pay out at least 30% of its attributable profits as dividends, while sending all HZL’s dividends to its own shareholders within six months. A lion’s share of that would go to the London-based parent.

Under the new policy, Vedanta Limited’s board will decide what to pay and when. It can hold its cash and deploy it more flexibly.

The third decision regards the brand fee.

Vedanta Resources’ biggest asset, perhaps, is the “Vedanta” trademark. Every Vedanta entity pays a percentage of its revenue for the right to use that name, and the rate has crept up every time the London-based parent has faced debt pressure: from 0.75% in 2017 to 2% in 2021. Under the new arrangement, it will increase further to roughly 3% for most entities, except for the copper business, which shall pays 0.75% because of its thin margins.

That’s an astounding amount of money. The group’s revenue in FY26 was about ₹1.74 lakh crore. A 3% brand fee on that base produces roughly ₹5,200 crore. That covers Vedanta Resources’ annual interest bill, with room to spare.

The new architecture effectively solves Vedanta Resources’ problem from two directions. The parent’s $4.8 billion debt has been broken into five pieces, sitting on five different balance sheets. The cash flowing to the parent now arrives at a higher rate, cleaning up its remaining obligations. Hindustan Zinc’s substantial dividend cash, which used to be upstreamed to all Vedanta Limited shareholders within six months, now stays at the residual entity, where the parent can draw on it through fees and management charges without pushing it to other shareholders.

But as it enters this new era, what are the shape its operating businesses are taking? For that, let’s look at its most recent results.

What the quarter actually showed

This quarter, most of Vedanta’s record cash flow came from two businesses: its aluminium arm, and Hindustan Zinc, the zinc and silver business in Rajasthan. These are the two big pillars that hold up the Vedanta tent.

The operating profit from its Aluminium business grew 43% for the year, crossing ₹25,500 crore, with margins of 38%. This was the pay-off from investments that had crushed the company’s costs. There are two things you need to make aluminium in industrial quantities: electricity, which is generated from coal, and bauxite, the ore that is refined into the metal. Vedanta’s aluminium business has spent years acquiring its own coal and bauxite mines, so it doesn’t have to buy these raw materials at open-market prices. That pushed its cost of producing a tonne of aluminium down to $1,752, the lowest in five years.

Meanwhile, Hindustan Zinc’s annual operating profit came in at over ₹22,000 crore, up 27% year-on-year, with margins of 56%. This was possible because the cost of producing zinc fell to $959 per tonne, the lowest in five years. These are remarkable numbers; few large industrial businesses anywhere have operating profits at more than half their revenue. This business will remain with Vedanta Limited after the demerger — and with the new dividend policy, the entity will get a lot more discretion over it.

There’s more of a shadow over the remaining entities. Their challenges are significant, and they’re heading into independent life with the conglomerate’s implicit cushion gone.

Vedanta Power, for instance, was reeling from a fatal accident at one of its plants, which killed at least thirteen, and injured more than twenty. The plant — one of the two main ones it operates — has been shuttered. There’s no clarity if it’ll be open any time soon.

Vedanta Oil and Gas has declining reserves. Vedanta Iron and Steel, meanwhile, has a smaller asset base that the market has yet to test.

Next quarter will see the first earnings calls of these five separate entities. It will be the first time each management faces a sector-specific analyst community, without the conglomerate’s averaging effect. We’ll keenly watch how they survive the test.

A sovereign loan is never just a loan

In 2007, Sri Lanka wanted to build a port in the city of Hambantota.

It asked India to help finance it, but we realized that the project was commercially unviable and said no. Then, Sri Lanka asked the US, and they also said no.

After that, Colombo turned to China, which agreed to lend it $307 million at 6.3% fixed interest. This is a normal commercial rate at a time when Sri Lanka’s own treasury bills were paying 12–14%.

A decade later, the Hambantota port would become the most famous case of what commentators called “debt-trap diplomacy“ — it’s the idea that China deliberately lends money to poorer countries knowing they cannot repay, then seizes their assets when they default

When one country sends money to another, the money is usually the smallest part of the deal. A sovereign loan is almost never just commerce, but it’s almost never just a trap as the Sri Lankan example might appear. It’s a bundle of development objectives, export contracts, foreign-policy positioning, and sometimes monetary strategy, all of which move inside a single agreement. And that’s what we’ll be dissecting in this bundle.

Advantage and goodwill

All of this hinges on a fundamental question: why do states lend at all? There are many, but we’ll only tackle four of the most important ones.

The oldest motive is soft power. After World War II, for instance, the US ran the Marshall Plan partly to rebuild Europe and partly to keep it out of the Soviet sphere.

A second motive is export promotion. Every economy that builds infrastructure needs buyers for what it builds. Cheap finance to a foreign government, conditional on procurement from your own engineering and construction firms, is one of the most effective ways to keep your exporters busy.

Then there is resource and logistics security. Take Angola, for example. After emerging from a deadly civil war in the 2000s, Angola financed much of its reconstruction through Chinese loans collateralised against future oil exports. The repayment for the loan wasn’t fixed. It was a percentage of oil revenue that Angola would make from reconstructed assets. That oil revenue would be routed through a Chinese-controlled bank account before the money ever reached Angola and China would take its cut. By one estimate, Angola alone accounted for roughly 70% of China’s resource-secured lending in Africa.

Finally, there’s macro-financial recycling — the boring but largest motive of all. When an economy runs huge structural trade surpluses, what it accumulates has to be deployed somewhere. Ben Bernanke, former Chair of the Federal Reserve, described this in 2005 as the global savings glut. China runs persistent trade surpluses through its exports, and the dollars it saves can’t all sit in US Treasuries forever. So, lending to developing countries is one way to recycle them productively.

Modes of power

Accordingly, the financial instruments used for state-to-state lending also reflect the motives needed to be achieved.

The simplest is a grant. It’s no-strings-attached free money with no repayment terms, and it’s usually given for humanitarian relief, public health, or governance. Most of India’s bilateral assistance to Bhutan, for instance, is grant-based, as is much of what passes for “foreign aid“.

Then, there’s the concessional loan, or the Official Development Assistance (ODA) loan. It is simply a loan that’s almost generous enough to count as aid under international rules. The OECD’s Development Assistance Committee defines ODA as government lending where at least 25% of the value is effectively a gift, usually delivered through below-market interest rates and very long tenures. It’s these kinds of loans will primarily be focusing on in this story.

For instance, the loans given by the Japan International Cooperation Agency (JICA) to the Mumbai-Ahmedabad bullet train project, at 0.1% interest over 50 years with a 15-year grace period, are textbook ODA. It’s partly a developmental gesture, and partly a reminder of who India’s most reliable infrastructure partner has been for forty years.

Then, there are policy-bank loans. State-owned institutions like China Development Bank, China Exim Bank, Japan’s JBIC, Germany’s KfW, and India’s Exim Bank lend at rates close to commercial benchmarks, and take strategic direction from their governments rather than chasing profit. Their signature product is the tied export credit — it’s a loan to a foreign government on the condition that the borrower uses the money to buy goods and services from the lender’s own firms.

For instance, Japan’s tied yen loans typically require around 30% of contracts to go to Japanese suppliers. India’s Lines of Credit through Exim Bank are more aggressive, requiring 75% of procurement to come from Indian firms. In many ways, it’s just industrial policy with an aid label attached. Most Chinese lending to Africa works the same way.

Lastly, you have the central bank swap line, which is emergency liquidity from one central bank to another — a bailout dressed up as monetary cooperation. Of course, there are also sovereign wealth funds, but their primary instrument of influence is equity rather than debt.

The bigness of China

The world uses China’s example, but almost nothing they are doing today is conceptually new. Japan ran the same ODA model for thirty years.

From the 1970s through the early 1990s, Japan built a sovereign-finance machine combining ODA loans, policy-bank lending, and tied the procurement that funnelled the work back to Japanese engineering firms. By 1989, Japan was the world’s largest aid donor. Indonesia, the Philippines, and Vietnam absorbed enormous quantities of Japanese capital, and Japanese firms built much of the region’s modern infrastructure on the back of it.

China arrived with the same model in the 2000s, but with three things it had way more of than Japan did.

First, capital. China’s savings rate hovered near 45% of GDP for two decades — nearly double the rich-world average — generating massive surpluses with nowhere to go at home. Second, idle factories. In the wake of the 2008 crisis, China had issued a massive stimulus, which contributed to building far more steel, cement, and construction capacity than the country itself could absorb. Third is its unique political system that could move policy banks, state firms, and sovereign capital in a coordinated push.

Chinese overseas lending peaked in 2016 at roughly $136 billion in commitments. It has been falling ever since. Many of the early signature projects turned out to be commercially weak: the Hambantota didn’t generate enough traffic, Kenya’s railway project lost money, and Zambia defaulted on its sovereign debt in 2020. As the projects struggled, Chinese state lenders increasingly found themselves refinancing old loans rather than writing new ones.

The composition of Chinese lending has flipped as a result. AidData describes Beijing as “the world’s largest official debt collector,” with rescue lending to distressed sovereign borrowers now outpacing new infrastructure project lending. By the end of 2021, China had run 128 rescue operations across 22 distressed borrowers worth roughly $240 billion. Average penalty interest rates on overdue Chinese loans roughly doubled between the 2014-17 period and 2018-21.

However, beyond the scale, there is one feature that genuinely distinguishes China from the Japanese playbook: the contract design. A 2021 study examined 100 actual Chinese loan contracts across 24 countries, and found three features that aren’t standard in Japanese, World Bank, or any other sovereign lending arrangement.

One, Chinese contracts contain confidentiality clauses that prevent the borrower from disclosing the loan’s terms, or in some cases, its mere existence. Secondly, the contracts also use escrow accounts controlled by the Chinese. The borrower’s commodity export revenues get routed through a Chinese bank account before reaching the borrower’s treasury. Lastly, they include clauses that try to keep Chinese debt out of any collective restructuring with other creditors.

None of this decisively proves the debt-trap thesis. But the contract architecture does mean Chinese lenders tend to build a system optimised for seniority — which is getting paid first when borrowers run into trouble. That matters a lot when things do go wrong.

When things go wrong

Now, Sri Lanka did go wrong, but not in the way the general consensus suggests. The 2022 sovereign default was not caused primarily by Chinese debt. At the time of default, Sri Lanka owed about $37 billion externally. Roughly 36–40% was held by Western bondholders through International Sovereign Bonds carrying coupons of 5–8%, about 19–20% by Chinese creditors, and the rest was a mix of Japan, India, multilaterals, and other bilateral lenders.

The trigger for the default was the international bond maturities, not the Chinese loans. Sri Lanka had issued $12.5 billion of bonds through the 2010s, when credit looked cheap and ratings agencies were tolerant. But when CoVID collapsed tourism in 2020-21, the country couldn’t generate the dollar inflows to roll them over.

Yet, the Chinese contracts did complicate the eventual debt restructuring that Sri Lanka needed to pursue to pay the bonds off. Sri Lanka signed restructuring deals with Western bondholders in December 2024 and with Japan in March 2025, but talks with China over its remaining $4.75 billion in debt are still unresolved. The contracts didn’t cause the default, but they made fixing it harder, and slower, and more expensive.

The cleanest illustration of this is the Hambantota port itself.

The port couldn’t generate enough revenue to service the Chinese loans that built it. So in 2017, Sri Lanka leased it for 99 years to a Chinese state shipping operator, which took a 70% stake in the operating company in exchange for $1.12 billion in cash. The port wasn’t seized as collateral or as a debt-for-equity swap, though — the original Chinese loans for the port are still on Sri Lanka’s books today. What changed hands was operational control of a failing asset, sold to raise dollars for Sri Lanka’s other foreign debt.

Where India fits

What matters now is what happens as these loans mature. China has roughly $1.5 trillion in outstanding sovereign lending across the developing world, and a growing share of it is distressed. The shift from infrastructure lender to debt collector isn’t a choice Beijing made — it’s a consequence of the lending binge of the 2010s catching up.

But even as the old loans sour, they’ve already done something more durable. The tied procurement clauses embedded Chinese firms deep into the supply chains of borrowing countries. Those contracts created relationships, dependencies, and maintenance cycles that outlast the original loan.

Meanwhile, swap lines with over 40 central banks, loan repayments denominated in renminbi, and escrow accounts routed through Chinese banks have wired the yuan into the financial plumbing of dozens of countries. The yuan still accounts for a small share of global reserves, but in the countries that owe China the most, it’s already embedded in the everyday machinery of government finance.

The loans may not have all worked as investments. But as instruments of influence in a world that’s already being forced to decide between the great powers, they may have already paid off.

Tidbits

[1] FMCG firms expect rural demand boost from new jobs scheme

FMCG companies expect the new VB-G RAM G Act replacing MGNREGA to support stronger and more stable rural consumption. The scheme guarantees 125 days of work versus 100 earlier and focuses more on rural infrastructure, which companies say could improve incomes and boost spending on daily-use products.

Source: Business Standard

[2] Eli Lilly pauses obesity campaign in India after regulator warning

Eli Lilly has halted its obesity awareness campaign in India after regulators warned it could indirectly promote prescription drugs like Mounjaro. The company said the campaign was meant to educate people about obesity, but the episode highlights growing scrutiny around marketing of weight-loss medicines in India.

Source: Business Standard

[3] IBA seeks mandatory manure blending to cut fertiliser imports

The Indian Biogas Association has proposed 10% blending of organic manure with fertilisers by 2030, saying it could save India $2 billion in imports annually. The plan aims to improve soil health, reduce dependence on chemical fertilisers, and create a stronger market for biogas-linked organic inputs.

Source: Business Standard

- This edition of the newsletter was written by Aakanksha and Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Kyle Chan on China’s industrial power and entrepreneurship

If you enjoy The Daily Brief, here’s something we bet you’ll like. We recently spoke to Kyle Chan, one of the sharpest minds we read to understand China - we’ve often featured his insights on The Daily Brief. Our conversation dives deep into the dynamics that shape China’s manufacturing landscape. It goes into the nature of Chinese entrepreneurship, how China’s price wars affect innovation (and vice versa), why China’s policies are far less all-knowing than people assume, and how China wields its manufacturing prowess as a geopolitical power. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Love the buildup and the history around the genesis of Vedanta. Very well explained. Would be closely tracking how these companies evolve.

Vedanta is a good example of poor corporate governance. Better trade commodities directly than these de-merged entities.