Connecting rural India to the internet

And can we fix electricity’s demand problem?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how large language model usage changed over the past eighteen months, through the public usage data of one busy AI marketplace.

In today’s edition of The Daily Brief:

The unfinished broadband project

The flip side of India’s power problem

The unfinished broadband project

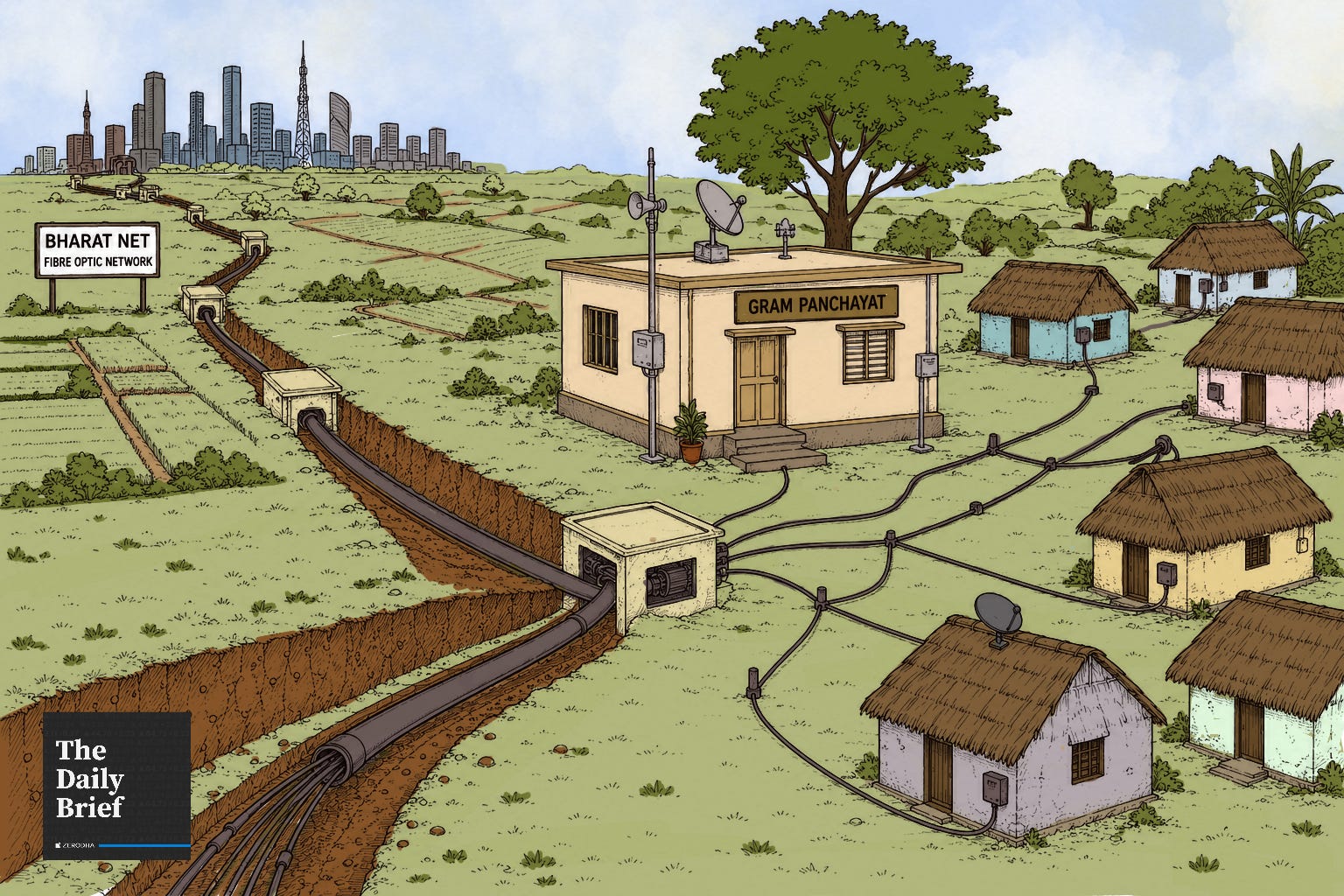

Back in 2011, the government set out on an ambitious project: to give telecom operators and internet providers an open, shared connection point in every part of the country.

It had approved the National Optical Fibre Network, later renamed BharatNet. This would connect block headquarters to Gram Panchayats through fibre optic cables, enabling connectivity and internet-enabled services in each village.

Fifteen years on, the programme is still unfinished.

The Cabinet has been trying to course correct. In 2022, it approved a merger of BBNL, the company built specifically to run BharatNet, into BSNL, the state-owned telecom operator. The formal amalgamation took years to complete, but came to a close in May-June 2026.

What is the government trying to do, though? Did it work, and if not, why? And what does that mean for the project ahead?

What is BharatNet?

When you use the internet on your laptop, data is reaching you through a chain of cables. At one end is the global internet. At the other end is your device. In between are layers of physical infrastructure: thick cables running between countries, thinner ones between cities, and then those that run to individual homes.

Much of that chain was built by private telecom companies. Naturally, though, they only built these chains where it was commercially profitable — in urban areas with dense populations, decent incomes and short distances between customers. That’s where the economics worked best.

Villages were a different story. With sparse populations spread over large areas, laying cables there came with high costs and low returns. Private operators had little reason to fund such a build-out. BSNL did lay some fibre optic cable in rural areas, but it usually ended at the local telephone exchange. From there, the connection to someone’s actual home ran over the old copper telephone wire used for landline calls, not fibre. A copper wire carries weaker signal than fibre, which gets even weaker the further it travels. A home close to the exchange could perhaps get usable broadband speeds over copper. A few kilometres further, however, the connection would be too slow to use properly.

And so, by 2011, most homes in rural India still lacked a fast, reliable internet connection.

BharatNet was the government’s answer to that gap. It would do what the private sector wouldn’t — run a network of fibre optic cables from towns into rural India, ending at the Gram Panchayat. Some of this fibre would be owned by the government, while some of it would run on existing cables borrowed from other companies.

Why was it built?

The point of this network was to build the most expensive, unprofitable part — running cables to each village. It wouldn’t actually try to sell internet itself. This is why these connections would stop at the Gram Panchayat. To go any further, the government would have to build a retail telecom company that could sell connections to every rural household. That would involve hiring staff, billing customers, and fixing problems door-to-door across hundreds of thousands of villages: a massive capacity sink.

That job was instead left for private telecom operators, internet providers, and cable companies to handle on commercial terms. These companies could offer some services — such as e-governance, e-health, and e-education — directly from these nodes. They could then decide for themselves whether extending the connection to actual homes was worth the cost.

The government approved the project in October 2011. To actually build and manage this network, it set up a company called Bharat Broadband Network Limited (BBNL).

In its first stage, now called Phase I, it connected over a lakh Gram Panchayats by the time it wrapped up in December 2017. Especially back then, it was too expensive to lay entirely new cables across the whole country. So, the project used underground fibre that BSNL, RailTel, and Power Grid Corporation of India had already laid. Each of those cables was a bundle of dozens of individual glass strands inside one protective sheath, and BharatNet was allocated a few dedicated strands within them. The host, meanwhile, continued using the remaining strands for their own services. New fibres were largely laid where existing cables did not reach a Gram Panchayat all the way.

In 2017, it began a second stage, Phase II. The approach, now, was wider. States and private companies were brought in to help build the network. With the internet, these new fibres would mix in radio and satellite links. To deliver that last stretch of connectivity, Wi-Fi hotspots would be added within each Gram Panchayat.

There was a challenge, however. BBNL lacked field staff, customer-facing systems, or day-to-day maintenance machinery. It lacked the ability to keep a live network running. This is why the Cabinet approved merging BBNL into BSNL in 2022.

Who pays for it?

None of this came cheap: not the cable, not the merger, and not the years of delay.

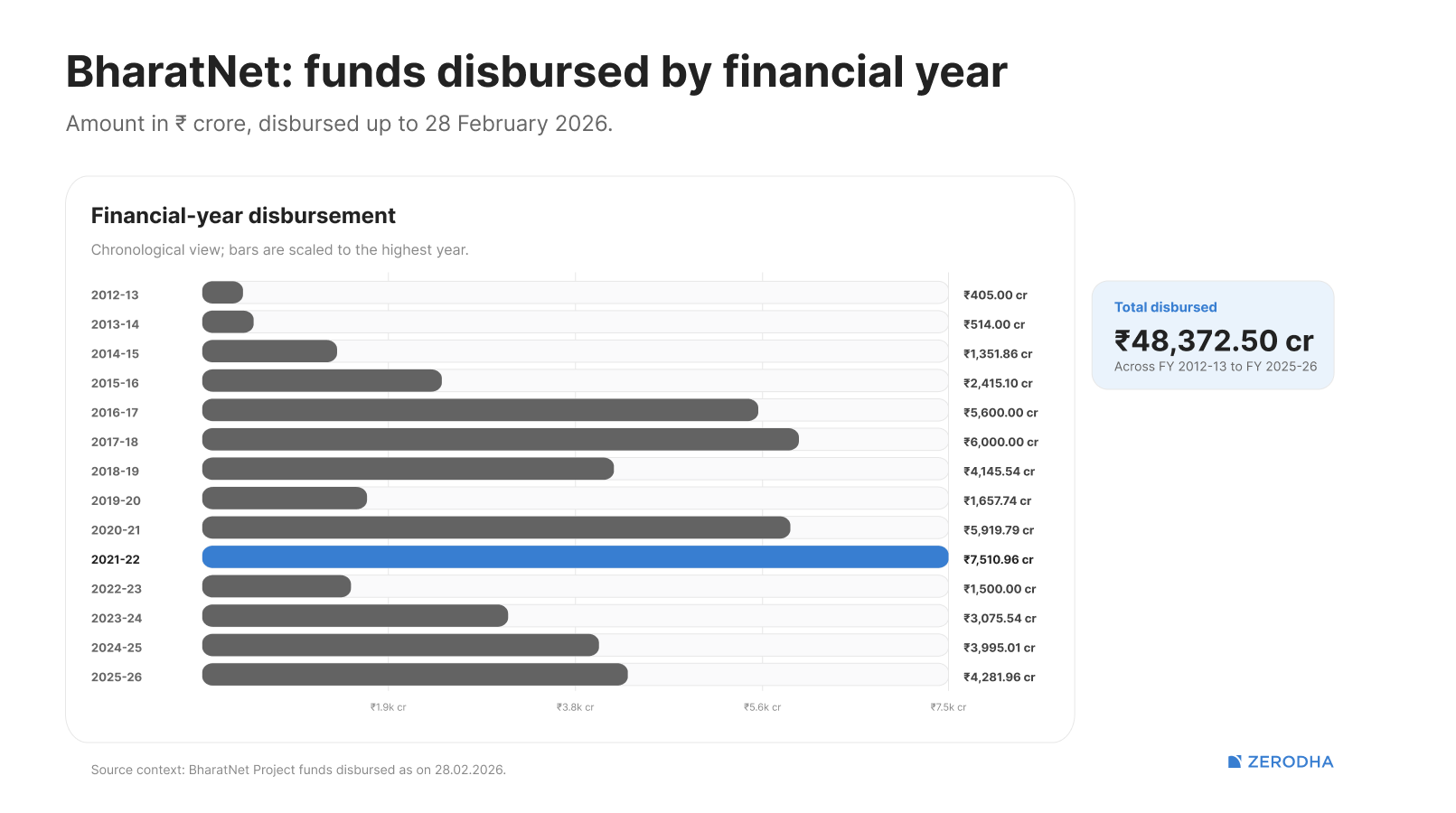

The money came from a government pool called the Digital Bharat Nidhi, earlier known as the Universal Service Obligation Fund. The money for this fund comes from the telecom industry. Service providers contribute a Universal Access Levy equal to 5% of their Adjusted Gross Revenue into this fund. In a way, this is money made from profitable urban markets, redistributed to rural networks that would otherwise never get built.

As of March 31, 2026, the fund had collected over ₹2 lakh crore, of which over ₹48,000 crore had been disbursed under the BharatNet program.

In return, BharatNet earns some money. It leases out spare capacity to telecom companies. A company might, for instance, use BharatNet’s rural fibre to connect its mobile towers in remote areas, instead of building its own cables. But those lease revenues amount to about ₹20 crore a year, a fraction of what was spent on the network. It is, in fact, deliberately cheap.

So, BharatNet is publicly funded, and is designed not to recover its costs. Unfortunately, this means it lacks the direct customer feedback loop that forces a private broadband company to fix service quality. A private company losing customers has to respond by cutting prices or improving service. BharatNet has no equivalent pressure.

The only thing moving it forward, then, is policy. There’s no market pressure bringing automatic improvements.

That lack of pressure is visible in how its last-mile problem played out.

Where it stalled

The BharatNet plan rested on a fatal flaw. It assumed that once it would get fibres to Gram Panchayat, private operators and local entrepreneurs would race to extend it further into homes.

Very few did.

Connecting individual homes to Gram Panchayats is commercially unattractive for the same reasons the private sector avoided rural areas in the first place. Their populations are sparse, incomes are low, and the cost of laying the final stretch of cable to each household is too high for households to pay for. Private operators were uninterested. Often, once the fibre arrived at the panchayat, it effectively stopped there.

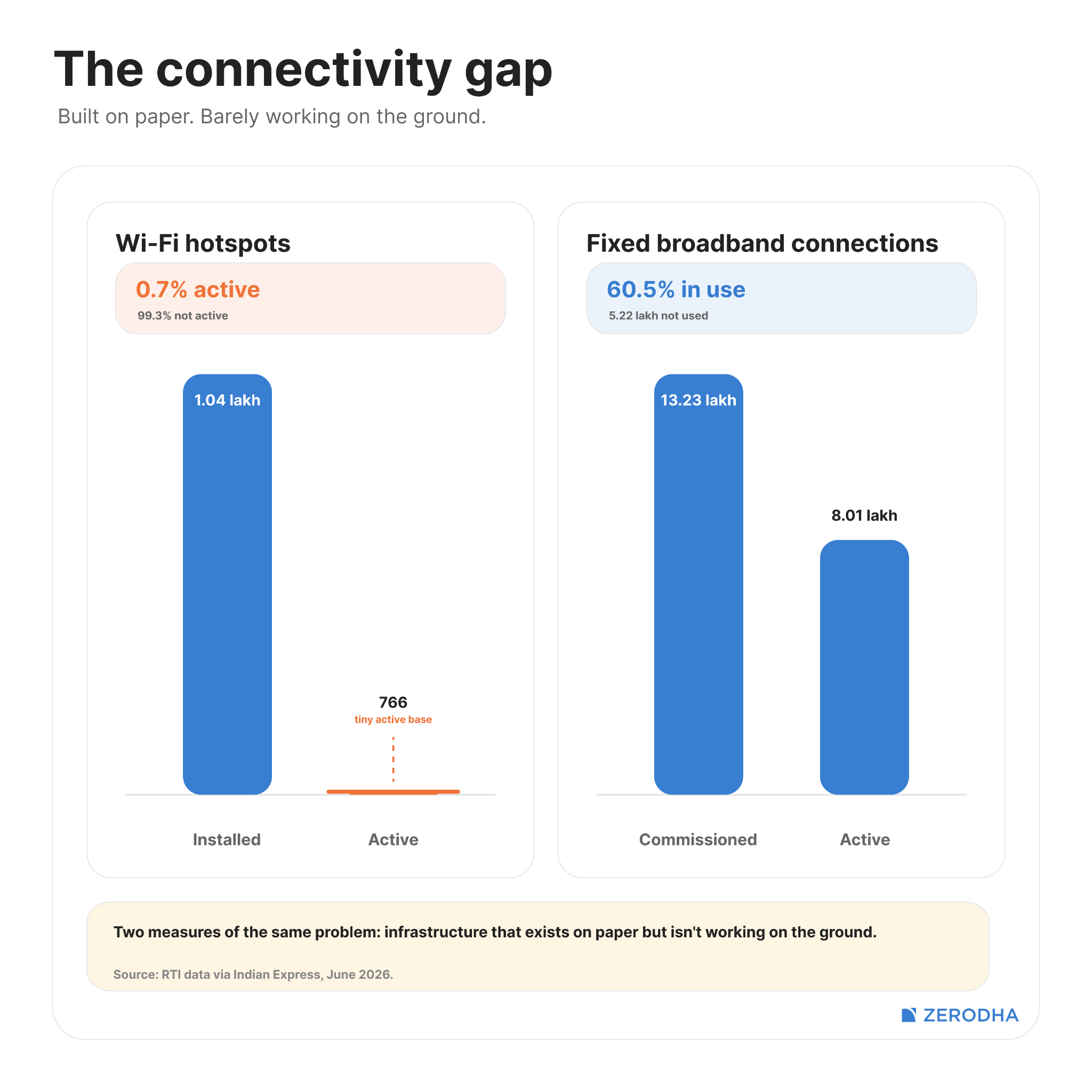

This is why Wi-Fi hotspots were brought into Phase II. If private operators wouldn’t run cables into homes, at least a public hotspot somewhere in the village would give people a way to access the internet. The government installed 1.04 lakh of these across rural India.

But this was easier said than done. Running a Wi-Fi hotspot takes more than just installing a router. It needs a stable power supply, someone available to fix it when it breaks, and a login system simple enough for first-time internet users to manage. Of more than a lakh installed hotspots, by September 2025, less than 800 were working.

That said, there were some places where BharatNet’s fibre actually reached homes and offices. There, telecom operators and local entrepreneurs actually extended wires to homes, signing customers up. Not as many as one would have hoped — by March 2026, against a target of 18 lakh, just over 13 lakh of these connections were built.

That wasn’t the worst of it. Unfortunately, connections alone weren’t enough. Only 8 lakh were actually being used. In fact, the trend is getting worse. New active users actually fell, from 4.5 lakh in 2023, to under 3 lakh in 2024, to barely over 2 lakh in 2025, even as the government kept spending capital.

Phase III, and a new problem

In August 2023, the government launched Phase III of BharatNet, or officially the Amended BharatNet Program, in the largest redesign of the project since its launch. This time, it set aside almost ₹1.4 lakh crore in new spending.

Two things changed this time.

First, the physical network was redesigned. The original BharatNet ran fibre in a simple straight line from towns to Gram Panchayats. If that line was cut anywhere, by road construction, a water pipeline project, or just physical damage, the village lost connectivity entirely. Infrastructure projects kept endangering these connections. With Phase III’s new design, the fibre is run in a loop instead. If one part of the loop is cut, the signal simply goes the other way.

Second, the programme now pays directly for the last mile, rather than hoping private operators will build it. Under the BharatNet Udyami scheme, local entrepreneurs provide and maintain last-mile connectivity from the village to households, institutions, and enterprises. They receive a one-time incentive for activating new connections, and are given a share of monthly revenue to keep services running.

This phase aimed at a massive ramp up. From only 15 lakh rural households, it targets a tenfold jump, to 1.5 crore connections over five years.

Contracts were soon awarded to build this upgraded network. For instance, Pratap Technocrats signed a contract for over ₹8,000 crore with BSNL for Rajasthan, Haryana, and Assam. Similarly, Tejas Networks won equipment contracts for 7 of the 12 Phase III packages, supplying over 50,000 routers across 57,000 Gram Panchayats.

But there was a problem.

Many Phase III contracts were signed at fixed prices between late 2024 and mid-2025, when commodity prices were lower. Soon, however, the artificial intelligence boom triggered a wave of data centre construction worldwide — which required the very equipment BharatNet did. The flagship cable grade used for BharatNet used to cost ₹300-325 per km. It is now quoted at ₹700-800, roughly doubling in under two years.

Only, the fixed-price contracts left vendors with little room to pass that cost on. Some are now seeking force majeure relief, arguing the cost increase was outside their control. Analysts, however, aren’t sure if this would work for simple commodity repricing.

The road ahead

There’s real progress on the program. By January 2026, close to 7 lakh km of optical fibre cable had been laid. Over 2.18 lakh Gram Panchayats and traditional local bodies were service-ready, against a target of 2.69 lakh. None of this existed fifteen years ago.

But the programme has missed four successive deadlines. And now, it’s running into a cost shock, fuelled by the AI boom. The government now has to decide how to handle contractors caught between the prices they promised and the prices they are actually paying. If the government tries holding contractors to the original contract terms, companies could slow work down or simply walk away. Offering cost relief keeps construction moving, but sets a bad precedent: that fixed-price government contracts can be renegotiated as soon as prices move.

There are real innovations there. The Udyami model ties local people’s income directly to the success of the program — a real stab at solving the last-mile problem. But is that enough for 1.5 crore new connections? That’s still an open question.

The flip side of India’s power problem

Every evening, when the sun goes down, discoms slam into the hardest part of the day.

The solar panels generating cheap electricity all afternoon disappear. At that very time, demand for electricity spikes. The discom has to buy power on the short-term market at the very moment every other discom is short. Prices become brutal. Roughly 70% of the moments when exchange prices for power hit their ceiling, last year, fell in this 6-to-11 pm window, just a few hours after it was practically free.

We usually treat this as a problem of supply. The grid is short in the evening, so we build things that can fill the gap, like big batteries that store the afternoon’s surplus solar for the night, or more transmission lines to move it around.

All of that is necessary. But there’s a second way to look at the problem: instead of bending supply to match demand, could we nudge demand to move away from the stressed, expensive evening, toward the cheap, sunny afternoon? Could demand actually be flexible, rather than set in stone?

A recent report from the Council on Energy, Environment and Water argues that, for the first time, India is actually in a position to do this.

What if we treat “demand” as a resource?

For as long as power grids have existed, they’ve run on a basic heuristic: demand does whatever it wants, while supply scrambles to keep up. The consumer is treated as passive. Their meter generates a monthly bill, but beyond that, they do whatever they want.

Demand flexibility flips that. The question stops being “how do we match the incoming demand?” and becomes “can we change when demand comes up?” For instance, if you charge an electric car at noon instead of eight at night, you use the exact same electricity — but it costs the system far less.

To be clear, this isn’t about reducing demand during peak hours. It’s about rearranging it. There are times when the grid is drowning in cheap midday solar and would love consumers to use more, lest it be wasted or curtailed. In fact, between May and December last year, India let 2.3 terawatt-hours of solar electricity waste away. This is why we need the flexibility to push demand down, up, or sideways through the day, depending on what the grid needs.

The piece of the puzzle that gets us there is DER, or ‘distributed energy resources’.

A DER is anything sitting on the consumer’s side of the meter that can change its behaviour for the grid. It could be anything: from an AC, to an EV charger, to a factory line, as long as it can shift when it draws power.

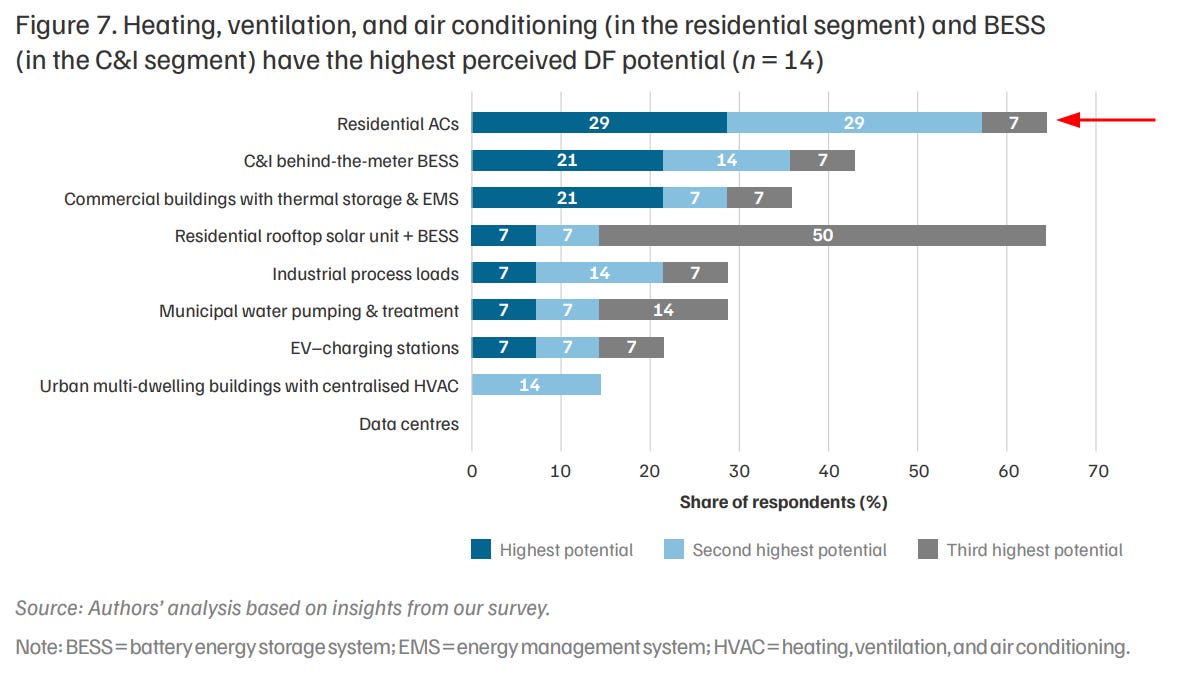

One of the biggest levers, for India, is the air conditioner. In Delhi, for instance, nearly 40% of the evening peak comes from residential ACs alone. It doesn’t make sense to switch a city’s ACs off. But you could nudge a compressor to ease off for fifteen minutes, or let the temperature drift from 24 to 26 degrees. Do that across a few hundred thousand homes at once, and you’ve shaved hundreds of megawatts off the peak, without any new infrastructure. In fact, when the report’s authors surveyed Indian discoms, residential ACs came out as the single most promising flexible load in the country.

How can you do this? You could try market solutions.

Picture a discom that knows tomorrow evening is going to be tight. Instead of bracing to buy expensive power, it can put out a call: I need 100 megawatts less demand between six and nine, and I’ll pay for it. An EV-charging company could offer to push back the charging of a few thousand cars. Or a cold store could offer to delay its compressors. They get paid for this, while the discom skips the painful peak purchase. Nobody is forced to do anything; people are simply selling their flexibility.

Of course, a discom can’t phone a million households individually to put such calls out. But a new kind of middleman can step in — the aggregator. They can bundle thousands of small, scattered loads and offer them to the grid as one dependable block. If one home cuts AC usage, that’s noise. But a few lakh of them, coordinated through software, rival the output of a power station. It’s the same trick as an app pooling thousands of taxi drivers into a reliable city-wide mobility service. The aggregator is, in effect, a new financial intermediary — except the thing it’s pooling and selling is the ability to not use power at the right moment.

The obstacles

If we’re able to make such a shift, the savings could be enormous.

Consider a single overloaded neighbourhood. A discom watching demand climb has two options. It can spend a great deal of money on a new transformer or substation, to handle the few evenings a year when load exceeds its capacity. Alternatively, it can pay local consumers to shave that peak on those handful of evenings.

The better answer is obvious. The cheapest transformer is the one you never have to build. In fact, discoms in Delhi and Mumbai, where land for new equipment simply doesn’t exist, found this particularly attractive.

So why doesn’t this happen already?

Regulatory incentives

Part of the answer lies in how discoms are paid.

India runs under a ‘cost-plus’ model. A utility earns a regulated return on the capital it invests. This creates a perverse incentive — more spending brings more returns. A new substation is a new asset, which brings earnings. Meanwhile, paying consumers for flexibility is an operating cost with no comparable return. This weakens a discom’s incentive to treat demand-side measures as a genuine alternative to network expansion.

There are genuine benefits if we can crack it, however. The report notes that India’s need for grid flexibility could grow five or six times over by 2030. CEEW’s own companion modelling estimates that shifting demand into the sunny hours could avoid something like ₹14,000 crore in battery and transmission spending. As a society, that’s enormously beneficial.

Investing in visibility

For flexibility to be possible, the grid needs to actually see what’s happening at the level of the consumer. It needs data. You cannot pay someone for reducing their demand unless you can verify that they reduced it, by how much, and when.

In other words, we need smart meters.

India has made a genuine start, here. More than ~5 crore smart meters have been installed across the country. So far, unfortunately, we’re mostly using these meters like the dumb ones they replaced — to generate a monthly bill. According to the report, the vast majority of discoms still track demand only at the broad state or utility level. There’s barely any analysis at the level of the individual transformer or neighbourhood. If the grid doesn’t track your behaviour, it can’t reward you for changing it.

For this to really work, you also need trust. Smart-meter data is intimate. It reveals when you’re home, when a shop opens, or how a factory runs its shifts. If all parties don’t trust the data sharing system, it will fail.

Right now, there’s no standard way for you to grant permission for a third party to use your meter data. But the India Energy Stack, introduced last year, is trying to fix this. It is an attempt to build common digital plumbing for the power sector, with shared identities for meters and assets and open interfaces so they can all talk to each other. If UPI made payments interoperable, the Energy Stack wants to do the same for electricity data.

Are price signals enough?

Even when all that plumbing is in place, you still have to give people a reason to move their usage.

The obvious lever is price: make power cheaper when demand is low, and behaviour should follow. This is the idea behind time-of-day tariffs. India has been rolling these out, with around 30 states and union territories having some version of these. Eight of them extend them to households, although the rest keep it exclusively for commercial and industrial clients. Seven even offer a genuine discount during solar hours.

But two things complicate the picture.

The first is that there’s really no single “Indian ToD” to point to. Each state’s regulator sets its own version, with different time windows, different price gaps, and different sets of consumers it applies to. For a regular consumers, there’s too much conflicting information to keep track of.

More worryingly, there’s still limited evidence these tariffs are actually shifting much load in India. A price signal alone is a weak lever. People forget, or find it inconvenient, or simply don’t watch prices that closely.

There are three ways to manage this issue. The first is behavioural: you get a message asking you to cut back on power usage, and decide whether to bother. This, it appears, can’t be relied on. But there are ways that don’t rely on your proactiveness. For one, you can make automated adjustments — for instance, you can set your AC to hold between 23 and 25 degrees once, and the device thereafter responds to the grid on its own. This is more dependable. You can also simply let an aggregator adjust your devices within limits you’ve agreed to, with your consent. This can make demand the most flexiblr, but also requires the most trust.

The more automated the flexibility, the more useful it is to the grid, but the more faith it asks of the consumer.

From pilots to programmes

India has run at least eleven documented flexibility pilots since 2012 — Tata Power in Mumbai, automated demand response in Delhi, others. They usually tend to stay exactly that: small, isolated experiments that never grow up. The lessons rarely add up into something a regulator can build on.

But lately, there is some serious momentum. Consider Maharashtra. Its regulator made flexibility a core obligation for discoms rather than an optional side-project. They have to source 1.5% of their peak demand from flexibility this year, rising to 3.5% by 2030. If this is not achieved, then there will be real penalties and equivalent rewards for meeting it. Incentives like this could finally force a utility to go figure out the technology and the procurement.

Today, markets pay for exactly one thing: producing power. The report argues that they should also pay for not consuming it when the grid is stretched, and consuming more when clean power is going spare — essentially, rewarding people for shifting the timing of demand. This is, fundamentally, a new economic model for electricity.

Tidbits

[1] Adani Ports sells 49% stake in Vizhinjam port to MSC unit for $1.4 billion

Adani Ports has agreed to sell a 49% stake in Vizhinjam Port to Terminal Investment Ltd. (TiL), the port arm of MSC Group, for $1.4 billion. The partnership is expected to boost cargo volumes, accelerate the port’s expansion, and strengthen Vizhinjam’s position as a major transhipment hub.

Source: The Economic Times

[2] Cabinet approves ₹30,000 crore infusion into NIIF

The Union Cabinet has approved a fresh ₹30,000 crore capital infusion into the National Investment and Infrastructure Fund (NIIF), doubling the government’s total commitment to ₹60,000 crore. The additional capital will support infrastructure, climate, private markets and growth equity investments.

Source: ET Now

[3] India’s industrial production grows 5.1% in May

India’s industrial output rose 5.1% year-on-year in May, up from 4.9% in April, driven by stronger manufacturing and electricity generation. Manufacturing grew 5.5%, while electricity and gas supply surged 9.9%, offsetting a decline in mining output.

Source: The Hindu BusinessLine

- This edition of the newsletter was written by Vignesh & Kashish.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉