Can India’s small businesses be paid on time?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

India’s cash-starved MSMEs get a breather — or do they?

India’s tyre makers just had their best quarter in years

India’s cash-starved MSMEs get a breather — or do they?

In last year’s Budget speech, MSMEs were categorized as the second of 4 key engines of India’s economic development. While MSMEs have always been important to the Indian economy, last year placed them at an even higher pedestal.

On those lines, this year’s Budget made some substantial allocations towards MSMEs. There was a shiny new ₹10,000 crore SME Growth Fund for equity support, as well as a ₹2,000 crore top-up to the Self-Reliant India Fund. One term, however, was mentioned 5 times: TReDS, or the Trade Receivables Discounting System.

Why did it receive so much attention? Well, TReDS gets at a problem that has quietly strangled Indian small businesses for decades: they can’t get paid on time. And without ready cash on hand, they can’t invest, they can’t hire, they can’t grow.

In multiple editions of The Daily Brief, we’ve covered various parts of the puzzle of why Indian MSMEs struggle to be globally competitive. TReDS is yet another key piece in that.

The problem that wouldn’t go away

Before we get into how TReDS works, let’s first get down to the nitty-gritties of a small business.

Take, for instance, an MSME that makes electrical control panels. It supplies its goods to a large firm: like a public-sector thermal power company. The MSME delivers, raises an invoice, and then….waits — for as long as 60-90 days, sometimes much longer. Meanwhile, the MSME still has to make salaries, rent, and so on. But its cash is trapped in a credit sale that’s gone long enough to behave like an interest-free loan.

Effectively, MSMEs are lending money to their buyers for free. In the value chain of the power industry, in this instance, liquidity gets locked up with the lead, large company.

By the end of 2021, the total value of delayed payments owed to Indian MSMEs ran to about ₹10.7 lakh crore. Much of it is driven by an unequal power dynamic where the buyer is comparatively larger than the supplier. The MSME can’t exactly call up, say, Tata or ONGC, and demand faster payment without risking the relationship.

One solution to this, globally, is invoice discounting. Here, the MSME takes its unpaid invoice to a bank or financial institution, which pays the MSME most of the invoice value upfront (minus a small discount), and then collects the full amount from the buyer on the due date. The MSME gets cash it needs immediately, the financier earns a spread, and the buyer gets the goods.

But the invoice discounting market hardly existed before 2014. At the time, only ~10% of total trade receivables were being financed through any formal mechanism. And there were several revealing reasons behind them.

First, the documentation was a nightmare. Until then, unlike today, most invoices were only drafted on paper. Verifying them involved checking on-time delivery of goods, a formal acknowledgement of the liability by the buyer, and so on. All of this involved tons of paperwork moving between the MSME supplier, the buyer, and the bank. The transaction costs for everyone involved were too high.

Second, and most importantly, the buyers — which were mostly large corporate houses — had no incentives to accept invoice discounting. And why would they? After all, delaying payments to MSMEs was like having an interest-free loan for them.

At the same time, invoice discounting in India lacked a strongly-enforced legal framework, offering MSMEs limited legal recourse. Large firms could often avoid accepting the terms of MSME invoices without facing any punitive action. An MSME had no choice but to accept lopsided terms, because if they didn’t, a competing MSME would.

Third, banks never took to it strongly. Instead, they preferred collateral-backed loans and cash overdrafts. This meant that MSMEs, which don’t even have enough assets to begin with, were always disadvantaged. In fact, even with invoice discounting, banks would often assess the creditworthiness of the MSME, rather than the large buyer to whom the invoice is made.

To make things worse, if the buyer didn’t pay the bank, the bank would come after the MSME instead for the money. That defeated its whole purpose.

All this meant that India’s invoice discounting was fragmented for a long time. An MSME would go to the one bank with which it had a relationship, take whatever rate the bank offered, and hope for the best. There was no formal market that offered better price discovery.

Behind all of this was a broader truth: India has not historically been kind to small businesses. Large firms and PSUs enjoy far easier access to credit. Intentional or not, our industrial policies — like the PLI subsidies — have consistently been biased towards bigger firms. The Economic Survey of 2018-19 documented this in painful detail, showing how India’s policy framework had created a nation of “dwarfs” — small firms that never grow — rather than “infants” that scale into globally competitive enterprises.

In 2011, to try and repair MSME financing, the government passed the Factoring Regulation Act. It was a step in the right direction, but it didn’t do much beyond creating a legal framework. It couldn’t yet change long-term behavior in banks and large buyers, or create the kind of formal, liquid market that MSMEs needed.

Enter TReDS

But in 2014, that began to change.

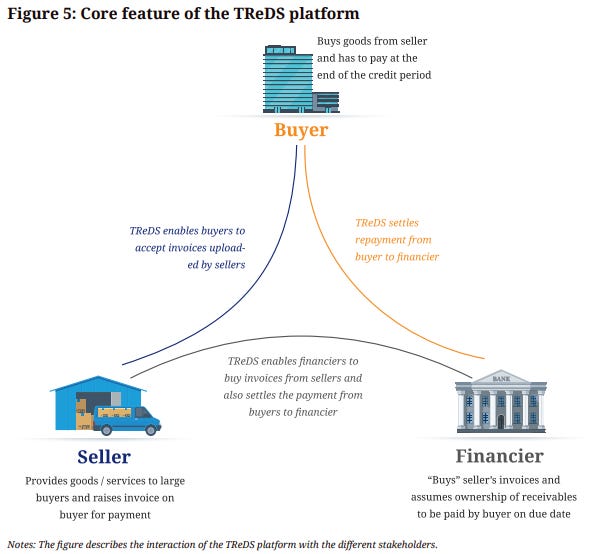

That year, the RBI published a concept paper for what would become TReDS, which went live in January 2017. At its heart, TReDS hoped to create a regulated, electronic marketplace that would solve the problems with older forms of invoice discounting.

Here’s how it works. An MSME delivers goods to a large corporate buyer and uploads the invoice onto the TReDS platform. The buyer logs in and accepts the invoice. Once this is done, the platform creates a “Factoring Unit“, a tradeable financial instrument based on the invoice. Multiple banks and NBFCs can see the invoice and bid on it to finance the unit. The MSME picks the best bid (lowest interest rate), gets paid within a day or two, and the transaction is done for them. On the actual due date, the buyer repays the financier.

Two features made TReDS genuinely different from what came before. First, it introduced competitive price discovery. Instead of being stuck with whatever rate your one bank offered, an MSME could now have multiple financiers bidding for the same invoice.

Secondly, TReDS operates on a “without recourse“ basis, where the risk of a TReDS deal sits squarely with the buyer. Simply, if the buyer defaults, the financier cannot come after the MSME.

This has another important implication: financiers now bid based on the creditworthiness of the large corporate buyer, not the small MSME supplier. An MSME supplying to, say, a AAA-rated PSU can suddenly access capital at 8–10% interest instead of the 12%+ it would pay on a traditional bank loan.

How has TReDS performed?

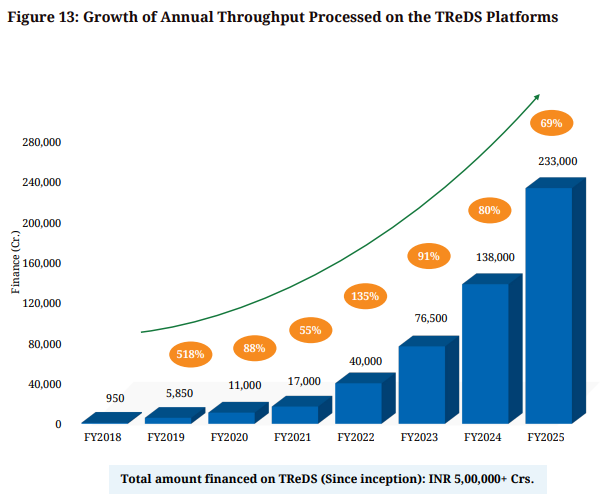

TReDS has grown enormously since its tentative early days.

In FY18, the first year, the total financing throughput on the platform was just ₹950 crore. But by FY22, it hit ₹40,000 crore, and in FY2025, it reached ₹2,33,000 crore.

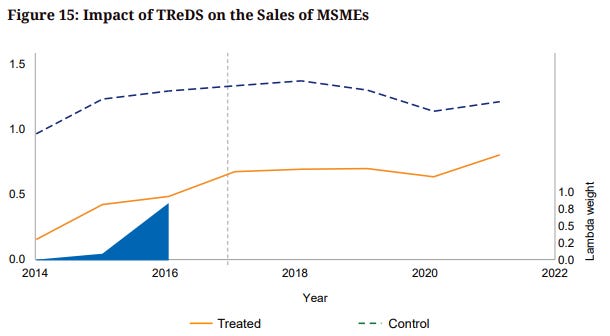

For the MSMEs that actually use it, the system works. Participating firms show an average 8% increase in sales and 4% growth in fixed assets. Each additional financier on the platform reduces the interest rate by 5 basis points. That may sound small, but every fraction of a percent matters to a cash-strapped MSME.

But, on the opposite end of the story lie numbers that make this growth look less impressive.

As of March 2025, around 1,35,000 MSMEs were registered on TReDS, while India has over 1.75 crore MSMEs. That’s less than 1% penetration, barely scratching the surface. In 2018, the government mandated that companies with turnover above ₹500 crore must compulsorily register on TReDS. By 2025, about 8,000 corporates had been onboarded, but only around 2,500 were actually active. The rest were dormant.

While TReDS has made invoice discounting smoother, bottlenecks still remain.

The biggest of them all is on the buyer’s side. See, TReDS forces buyers to pay on time. Once a buyer digitally accepts an invoice on the platform, it’s a binding obligation that cannot be disputed. However, the creation of the factoring unit depends entirely on the buyer accepting the invoice, which is optional. So, large firms simply avoid doing that, and instead file invoices outside TReDS.

Also, large corporate firms tend to have their own NBFCs which also handle invoice discounting. Take, for instance, Tata Capital, Bajaj Finance, Reliance Capital, and so on. They have little incentive to use TReDS for the business of their group entities — especially since they earn spreads on doing invoice discounting themselves.

This snag gets worse when the corporate buyer has a weak credit rating. Remember, TReDS bids are based on the buyer’s creditworthiness. If the buyer is a blue-chip business house, banks are happy to line up. But if it’s a mid-sized company without an external credit rating, financiers simply won’t bid. This leaves a huge swathe of MSMEs, which supply to the vast middle of corporate India, locked out of the platform entirely.

Beyond buyer adoption, TReDS also suffered from an implementation gap. For instance, last week in Maharashtra, the state cabinet approved the use of TReDS to clear dues worth ₹70,000 crore that they owed to contractors. But the actual rollout has stalled. Contractors have warned they may have to halt infrastructure projects because they’re servicing interest on loans while the government sits on their bills.

What the Budget changes

This is the context in which this year’s Budget announcements for TReDS become significant.

The Budget has made multiple tweaks to TReDS, the most important of which is making TReDS less optional. In that vein, the government has made TReDS use mandatory for all purchases by PSUs from MSMEs, whether discounted or not. In the state’s view, PSUs should act as pioneers, so that private firms also follow.

To make adoption of this rule easier, the Budget also directly linked the Government e-Marketplace (or GeM) with TReDS. When an MSME sells to the government through GeM, the transaction data flows to financiers on TReDS, making it easier and cheaper for them to assess and finance the invoice.

Second, the Budget extends a credit guarantee for invoices through a Credit Guarantee Fund. This is targeted directly at the “unrated buyer“ problem. If a financier worries about the buyer defaulting, the guarantee fund steps in to cover the loss. It hopes to incentivize banks to bid on invoices from a wider range of buyers, not just the AAA-rated giants. The Credit Guarantee Fund has existed since 2000, but it was never linked to TReDS formally until now.

These are plumbing fixes that aren’t as flashy as monetary commitments. But they matter because they attack the structural reasons why TReDS hasn’t scaled.

Conclusion

These changes are also part of a broader — if belated — recognition that India needs its small businesses to function as reliable suppliers if its larger industrial ambitions are to succeed. You can’t build competitive supply chains in, say, electronics or defence, if the Tier-1 and Tier-2 suppliers at the bottom of those chains are perpetually cash-starved. The changes to TReDS and the new SME Growth Fund hope to give new life to MSMEs.

The early signs of TReDS have indeed been promising, but a cultural shift in how Indian business treats its smallest suppliers is still far away. On that front, TReDS alone won’t be enough to move the needle, but that doesn’t negate its current importance.

India’s tyre makers just had their best quarter in years

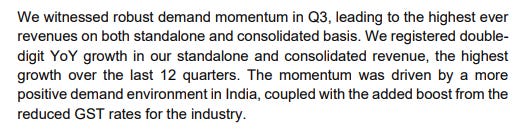

India’s tyre sector just posted its strongest quarter in over a year.

Apollo Tyres, for instance, crossed ₹5,000 crore in quarterly India revenue for the first time. CEAT breached ₹4,000 crore, while JK Tyre’s profit this quarter jumped nearly four times. The volumes of tyres sold increased accordingly — CEAT was up 21%, while JK Tyre was up 16%. Factories are operating at over 85% capacity.

While some tyre companies were riding genuine tailwinds in the past year, this quarter was particularly special due to the GST tax cut in September last year. It reduced the tax rate on tyres from 28% to 18%, changing tyre affordability overnight.

But when demand came back, it showed how little room the industry had left to grow. Tyre growth has been fairly muted in the past year, and the GST cut was a gift for many. At the same time, the industry is facing other bottlenecks that threaten its growth.

Let’s dive into how the industry is managing the situation.

Can demand sustain?

With the GST cut, a truck tyre costing ₹35,000 was now effectively reduced to ~₹32,200. A two-wheeler tyre dropped from ₹2,500 to ₹2,300.

When news of the tax cut circulated in August and September, purchasing basically froze. Why buy now when prices drop in two weeks? As a result, tyre companies lowered their inventories significantly. CEAT’s management confirmed that dealer stock, which is normally 15-20 days of sales, collapsed to 2-3 days by September as dealers waited. By October, however, inventories normalised, right after the GST cut became applicable.

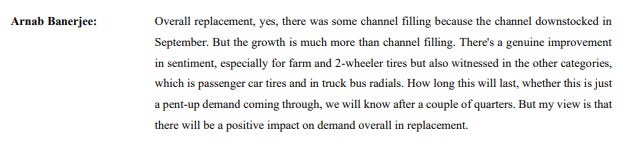

Two-wheeler tyres grew double digits through the quarter. Replacement tyres for commercial vehicles, which had been flat or declining in the first half, showed high single-digit growth. Passenger car tyres that were growing slowly earlier reached mid-to-high single-digit growth. MRF explicitly linked robust sales to the GST reduction.

Meanwhile, Apollo said the GST cut drove their highest quarterly growth in 12 quarters.

But beyond the tax cut, growth in rural markets also drove a bounce back in demand.

MRF credited the monsoon rains for reviving the rural economy. After all, monsoons drive farm income, and farm income drives purchases of two-wheelers and tractors which need tyres. When farmers earn more, they buy vehicles. Moreover, two-wheeler sales are often used to measure rural economic growth.

CEAT reported an increase in replacement demand for their tyres, particularly for farm and 2-wheeler tyres. Even besides replacement demand, they sold far more tyres to tractor OEMs.

Apollo saw huge levels of rural demand across not just two-wheelers and farm tyres, but also passenger cars. Interestingly, they credited their jersey sponsorship of the Indian cricket team with creating a strong brand recall in rural areas. This visibility has translated to sales.

Now, urban replacement demand driven by the GST cut might be temporary catch-up buying. We aren’t sure how long it’ll last. After all, how much of this demand is just catch-up from delayed purchases?

Additionally, before the GST cut, demand was already weak in certain spots, but not entirely because buyers were waiting. Importantly, truckers were earning less per trip due to the decline in freight rates. As a result, many trucks sat idle, and when trucks run less, tyres wear out slowly, delaying the need for replacements.

CEAT’s CEO was candid about the uncertainty. He doesn’t know if this surge is just delayed purchases finally happening, or if it’s a sustained shift in buying behaviour.

That matters because pent-up demand runs out. Once everyone’s caught up on delayed purchases, volumes drop back. But if the lower price actually changed behaviour, demand stays higher. That could mean truck operators replacing tyres sooner, or more buyers choosing branded tyres over cheap alternatives.

For this to be real growth, something about buying behaviour needs to change. Maybe truck operators start replacing tyres earlier instead of waiting until they’re fully worn out. Maybe more buyers will shift from the informal tyre market to official dealers — when GST was 28%, buyers had a stronger incentive to find ways around it. At 18%, though, branded tyres become more attractive. Maybe more buyers choose premium tyres. Without shifts like these, the GST cut would just be a one-off boost.

Meanwhile, the recovery in rural markets is cyclical. It is dependent on a healthy monsoon and growing farm incomes. If the next monsoon is normal, rural buying could continue to be strong even if urban replacement volumes normalize.

The capex race

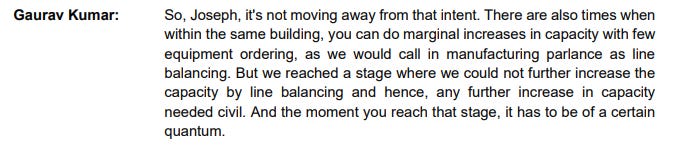

India’s tyre companies are pulling no punches when it comes to investing in new capacity.

Apollo’s board just approved ₹5,800 crore to build new factories over the next three years. CEAT approved ₹1,314 crore for a new Chennai plant. JK Tyre committed over ₹1,130 crore.

Why now? Well, the existing factories are full. Apollo’s truck tyre lines, for instance, are running at nearly full capacity. There’s simply no room to make more tyres without building new space. And when you need to build new space, you’ll need to invest a lot of time and money.

So the whole sector is building all at once, for the same reason — everyone ran out of room at the same time.

Now, companies don’t usually just invest because they ran out of room at one given point of time. Heavy capex is undertaken with the expectation that, over the next few years, the market will grow by leaps and bounds. And tyre-manufacturers do expect a huge growth cycle to play out in the long-term.

But, as we mentioned before, tyre-makers currently have a hazy picture of demand in the near future. Moreover, none of this new capacity they’ve commissioned arrives soon. Apollo’s factories won’t be fully ready until late FY29. CEAT’s Chennai plant finishes in mid-FY28. By Apollo’s own estimate, the full payoff from this spending lands only four years from now.

There is a possibility that, by the time this capacity is built, some of the demand vanishes. If that happens, they’ll be left bearing massive fixed costs in the form of excess factory capacity.

Burning rubber

Lastly, while tyre margins expanded on volume, the cost of the primary raw material used to make tyres, rubber, was also rising.

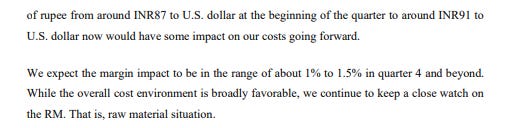

Tyre companies import a lot of rubber. So, some of their margins depend on global prices of rubber, which can be quite volatile. In the quarter, the rupee depreciated from ₹87 to ₹91 against the dollar. As a result, natural rubber moved from $1,700 to $1,800-1,810 per tonne by quarter-end.

Hence, raw material costs rose slightly from the previous quarter, driven primarily by currency depreciation. CEAT guided for 1-1.5% margin impact in Q4 and beyond. JK Tyre, meanwhile, expected an increase of 1-2% in raw material prices.

For now, margins have fared better because the volume effects dominated the impact of currency depreciation. But how long this will last with uncertain demand is a different question.

Interestingly, across the industry, almost no one committed to price hikes to offset input cost inflation, either. As such, they just passed the GST benefit through to customers. Taking that back through price hikes while demand is uncertain will be a hard sell.

But all of this suggests that they’re counting on volume growth to carry the margin story in the near future.

Another hit to profits this quarter involved the new labor laws that kicked in during November, which forced companies to set aside more money for higher gratuity obligations. MRF provisioned ₹77 crore, CEAT ₹58 crore, JK Tyre ₹56.75 crore. These are one-time accounting entries, but they reflect permanently higher costs going forward.

What this means

Nobody really knows how much of this quarter’s demand is real. CEAT’s CEO, Arnab Banerjee, said so himself. He doesn’t know if this is genuine growth or just delayed purchases finally clearing through. They will only find out in the next few quarters.

If demand fades, costs are rising and prices can’t go up easily after a tax cut. New factories arrive in 2027-28, potentially just as demand might normalize.

Rural incomes are rising and more vehicles are on the road. The companies aren’t wrong to expand. But the size of the bets they’ve made, and the speed at which they’ve made them, was driven by one exceptional quarter. Whether that quarter was the start or peak of something is the question nobody can answer yet.

Tidbits

Venezuelan oil discount for India hits record low

Discounts on Venezuelan crude sold to Indian refiners have fallen below $10 per barrel, touching record lows. Higher freight costs and tighter supply have reduced the price advantage. Refiners say deals need deeper discounts to remain attractive, especially with long shipping times adding costs.

Source: Business StandardRBI proposes easier foreign exchange trading rules

India’s central bank has proposed new forex rules giving banks more flexibility to trade on overseas electronic platforms. Banks may also invest surplus foreign currency deposits in long-term foreign government debt. The move aims to modernise trading while keeping risk controls in place.

Source: ET BFSIIndia’s first private helicopter assembly line opens

India has inaugurated its first private-sector helicopter final assembly line in Karnataka, led by Tata Advanced Systems and Airbus. The facility will assemble the H125 helicopter for civil and possibly military use. The first “Made in India” delivery is expected in early 2027, with export plans in sight.

Source: The Hindu BusinessLine

- This edition of the newsletter was written by Manie and Vignesh

We’re now on WhatsApp!

We’ve started a WhatsApp channel for The Daily Brief where we’ll share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops, so you can read or watch it right away. Here’s the link.

See you there!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Thanks for this post.

The MSME TReDS problem is something I have from up close in the past, both as to how it has helped firms and how it has been abused.

What I came here to say is about we could enhance its utility. Why not consider linking it to the GST network whereby the buyer gets opted in by default the moment they take the GST credit into their kitty? You cant have it both ways, can you? What do you think we can do to pass on this to the right ears?