Brexit and the price of friction

Plus: What does Bank of Baroda’s expensive ₹5,700 crore affair in Abu Dhabi say about Indian banks?

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened; we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

The Brexit story

Bank of Baroda has an expensive affair in Abu Dhabi

You may have noticed that lately, we’ve been doing podcasts with a variety of guests. All of them share one feature: they’re incredibly knowledgeable about a specific niche of how markets work. And we realized that more people should know who they are and what they do, no matter how popular.

Now, those episodes have found a new home: a separate YouTube channel for Subtext. We will be launching at least one episode each week, even two when we can. We’re also on Spotify, Apple Podcasts and we also have a newsletter if you like to read the transcripts instead.

We hope you give our newest baby some love, and we’re also open to guest recommendations from you!

Introducing: Subtext by Zerodha

Hi folks, I’m Bhuvan, and I’m here to tell you that our newest baby, Subtext, has arrived.

The Brexit story

It was an early summer day, ten years ago, when Britain voted to leave the European Union.

Half the country celebrated their freedom from the yoke of Europe. The other half despaired. What would this do to the kingdom’s relationship with the continent? What would it do to the millions of trade relations that connected the two? Europe, surely, would not make this departure easy, or all its other members would clamour for an exit. What if the “single market” was violently torn into two, with British businesses suddenly finding a steep tariff wall to climb? What if Welsh lamb farmers and Scottish distilleries suddenly found hefty tax bills waiting at the French border? It would be economic armageddon.

There were fears, then, of “no deal”: that Europe, Britain’s largest market, would only trade with it on the barest of terms, as if it were any other country. A panic set in.

Experts were pessimistic. The UK Treasury and many independent forecasters claimed that leaving Europe would drag Britain’s economy down substantially in the long run. Most converged on a ~4% drop, with things getting worse if the conditions of Britain’s exit hardened. In fact, the UK Treasury even warned of an immediate recession.

Then, briefly, nothing happened. There was no recession. By late 2020, a deal was on hand — the Trade and Cooperation Agreement (TCA). It gave the country everything it wanted: zero tariffs, zero quotas. There was no cliff after all. Britain had escaped the worst, and all that pessimism now felt like empty scare-mongering. Those that raised concerns were tainted with a nickname: Project Fear.

Now, all these years on, they no longer seem so far off the mark. In the years since, the country’s GDP turned sluggish, its exports dropped, and its productivity stalled. Brexit clearly broke something, even if it wasn’t clear what.

How Brexit bit

Before Britain broke out of Europe, few people actually saw the value of what it had.

Britain had been woven into Europe for nearly fifty years, with millions of delicate inter-connections, many of which were barely visible. A lobster caught off the Scottish coast on Monday could be on a plate in Paris on Tuesday. A restaurant in Manchester could order a German dish-washer, and have it delivered the same week. A car plant in the English Midlands could run with almost no spare inventory, because they could trust parts to ship in from Europe exactly when needed. It was seamless — a single market, with the English Channel just a geographical feature.

And then, there was passporting: which made London Europe’s financial hub. A bank licensed in London could sell its services across the whole continent — without reaching out to regulators in Paris or Frankfurt for separate approval. This made the country a financial gateway to Europe. An American bank could set up a regional headquarters in London, and serve 27 countries across the continent.

This wasn’t simply because Britain had tariff-free access to Europe, though that helped. It was because when it came to business, there was no barrier between the two. Britain was bound to Europe through the invisible plumbing of a shared rulebook and an open borders. Exporters didn’t have to fill forms, prove the origin of their goods, or wait for border inspections.

This was what Britain had put at stake in that fateful vote.

The pinch of uncertainty

In the first few years, though, none of this was touched. One could barely see the economic cost of Brexit.

There was only uncertainty. Even as late as 2019, it wasn’t clear what fate Britain was headed for. The ground was still moving under its feet. For all one knew, there would be no arrangement to fall back on.

That uncertainty bit. Investments stalled. Businesses put off decisions that were hard to undo. A striking amount of senior management time, in those years, drained into contingency planning. Three-quarters of British CFOs spent at least some time thinking through Brexit — mapping supply chains, war-gaming no-deal scenarios, and restructuring taxes. Almost a tenth of them were spending six hours a week on these problems.

But there was nothing visible. It’s hard to measure the cost of lost time. Perhaps those hours were better spent on new products or business relationships, but that wouldn’t be obvious from the data. If anything, Britain’s trade figures looked surprisingly calm. The Pound had fallen immediately after the vote, making its goods cheaper. That gave British exports a boost, cushioning the hit that Brexit delivered.

This is why, perhaps, it was easy to dismiss the pessimists — especially once the deal came into sight, and it seemed like the country would ease into a zero-tariff relationship with the continent.

Bordering insanity

What wasn’t apparent, though, was that the deal still broke the invisible plumbing that tied Britain to Europe. In its place, there came paperwork.

Even if exporters avoided customs duties, they still had to contend with a border. Consignments now required forms, certificates, and customs brokers. Consider a shellfish exporter that, till now, just sent their catch over to the mainland. Suddenly, they needed an export health certificate, signed by a vet for every consignment — with border checks on the way in. Over those hours spent at the checkpoint, their fresh catch turned stale, and uncompetitive.

In the first few years after the deal, in fact, British food and drink exports to the EU fell 16% below their pre-Brexit level.

Or take British cars. In theory, these could still enter the EU tariff-free. But now, they came with “rules of origin” requirements. Those cars would only see the benefit of zero tariffs if enough of each car had been built in Britain or the EU. Manufacturers now had to track where their thousands of components came from, and arrange for all the necessary documents, or they would end up owing a tariff.

In all, once you added up the forms, the delays, the compliance and the inspections, trading across the Channel became roughly a tenth more expensive — even if the tariffs were still zero. Everything that would happen thereafter could be traced back to this drag.

Meanwhile, British banks no longer had the free hand in Europe they once enjoyed. They were given an inferior “equivalence” standard instead. Their reach in Europe narrowed. European firms can still clear derivative trades through London, but other spheres of work began closing off. Slowly, the business itself began relocating — licences, balance sheets, whole trading desks shifted to other European centres: Paris, Frankfurt, Dublin and Amsterdam.

Counting the damage

There’s a challenge to a story like this, however: how do you estimate the real impact of Brexit? What do you take as your baseline? The years after Brexit were hardly calm: they were marked by a global pandemic, the world entering lockdown, a European war, skyrocketing energy prices, double-digit inflation across advanced economies, and more. Even if the British economy was worse off, with so much tumult, who could say if Brexit was responsible?

Fake Britain

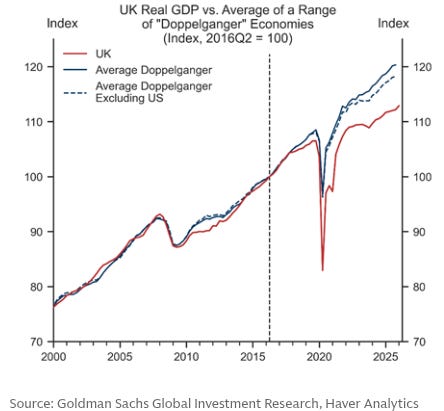

For this, economists came up with a little trick they call the “doppelgänger method”. They took a basket of rich economies — the United States, Germany, and a handful of others. Taken together and weighed appropriately, this basket roughly mimicked the trajectory of pre-2016 Britain. Later on, they ran into the same pandemic and energy shocks as Britain. This basket was a sort of “synthetic Britain”: a picture of what the country would look like if it never voted to leave.

To be clear, this method has holes. The countries in that basket aren’t Britain, however close their trajectories may superficially appear. This is only a proxy. Studies like this, as their own authors will tell you, need a pinch of salt. But they’re informative.

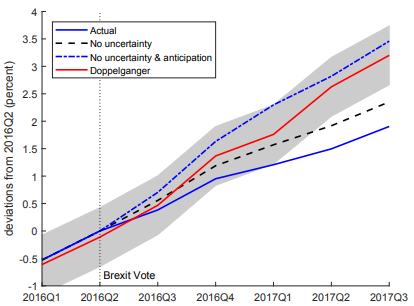

An influential doppelgänger study from 2019, by Benjamin Born and others, showed synthetic Britain diverging from the country’s real trajectory as early as 2016 itself — well before there were actual changes on the border.

In the decade since, however, those divergences have turned into a yawning chasm. The extent of the gap is unclear. Goldman Sachs, for instance, modelled the British economy as being currently 6% smaller than its synthetic counterpart. More conservative estimates put the figure at 4%. Directionally, though, Brexit has clearly hurt the British economy.

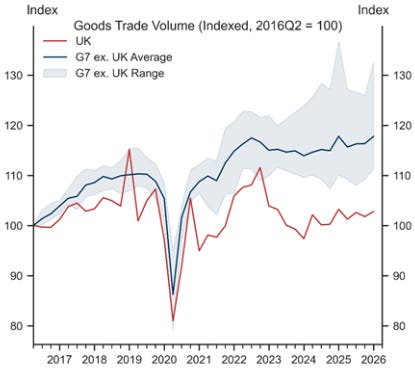

The clearest fingerprint of Brexit comes from Britain’s goods trade data. Where investment and productivity figures were slackening since 2016 itself, Britain’s goods trade was at par with comparable economies all the way until 2021 — when its borders were hit by new restrictions. From that point on, though, there has been a sharp break. By 2024, British goods exports to the EU were around 18% below where they had been in 2019.

Who foots the bill?

Even these sorry numbers obscure something, however: when Brexit came, it didn’t hit everyone equally.

Large British exporters paid for Brexit in inconvenience, but they had the scale to fold these new realities in their operations. With Brexit, they needed to hire legal teams, engage customs brokers, and build software to manage the border — but critically, they had enough shipments to spread the costs.

This is why aggregate trade figures have held up better than feared.

Smaller firms, however, didn’t have this luxury. To them, Brexit added fixed costs that were hard to get around. You couldn’t spread a vet’s certificate or a customs broker’s fee when you were only shipping a few boxes of cheese, or a pallet of craft gin. To do so would swallow your whole margin.

And so, many small businesses simply stopped exporting to the EU. Somewhere between 16,000-20,000 firms stopped selling anything to the bloc. These are numbers that don’t show up in aggregate data, but they changed what a British export business looked like.

Fool Britannia

There were two dreams that Brexit began with.

The first was a vision of “Singapore-on-Thames”: a Britain that, freed from European red-tape, could become a nimble economy with a light rulebook. It didn’t work. To sell in Europe, Britain would still have to comply with European rules. Only, now, they had to track a separate set of rules from within Britain as well.

For instance, Britain attempted to introduce a new British product-safety mark, meant to replace that of the EU. Only, after years of delay and complaints from firms that didn’t wish to certify their products twice, it abandoned the switch and recognised the EU’s mark again.

The other was a dream of “Global Britain”: where the country would replace Europe by signing a web of new trade deals with the rest of the world. It did exactly that — including its deal with India. But none of those new markets came anywhere close to what it lost in Europe.

Ten years on, now, a majority of Britons across party lines express disappointment in Brexit.

It’s easy to laugh at Britain’s pain. But there’s a lesson for us, here.

What Britain lost, in the frenzy of the last decade, was a frictionless trading relationship. Even without tariffs, these tore a hole through its economy. The episode taught us something rare: the cost of trade friction.

We have often argued, on The Daily Brief, that India’s regulatory tedium holds us back. It’s hard to make that argument, however, when nobody can see what the alternative is. In countries where business is easy, that ease is invisible from the outside. But Brexit ran a public experiment: it showed the world what happens when an advanced economy abruptly brings friction back. Even without tariffs, quotas, and other obvious restrictions, they can fundamentally change its shape.

As Brexit closes ten years, it’s worth asking how much friction we’re willing to live with.

Bank of Baroda has an expensive affair in Abu Dhabi

On July 2, Bank of Baroda told the stock exchanges that its Abu Dhabi branch had paid $600 million — about ₹5,700 crore — to settle a case on a collapsed hospital chain in the Middle East. In the same breath, it said it had admitted no liability and done nothing wrong.

To put that in context, this is one of India’s largest public-sector banks which handed over more than a quarter of its entire annual profit to settle a case with the verdict only weeks away. Immediately, Baroda’s shares fell over 4% the day the news broke and another 3% the day after.

There is no SEBI order here, no RBI enforcement action, no Indian regulatory finding to point to. Almost everything solid that we know comes from two places: the judgments and filings of an Abu Dhabi Court and Baroda’s own thin disclosures.

A collapse that began with a short-seller

The story begins with the hospital chain.

NMC Health was founded in 1975 by B.R. Shetty, an Indian pharmacist who had built a business empire in the Gulf. It grew into the UAE’s largest private healthcare provider, sprawling hospitals, clinics and pharmacies. In 2012 it became the first Abu Dhabi company to list on the London Stock Exchange, and by 2018 it had climbed into the FTSE 100.

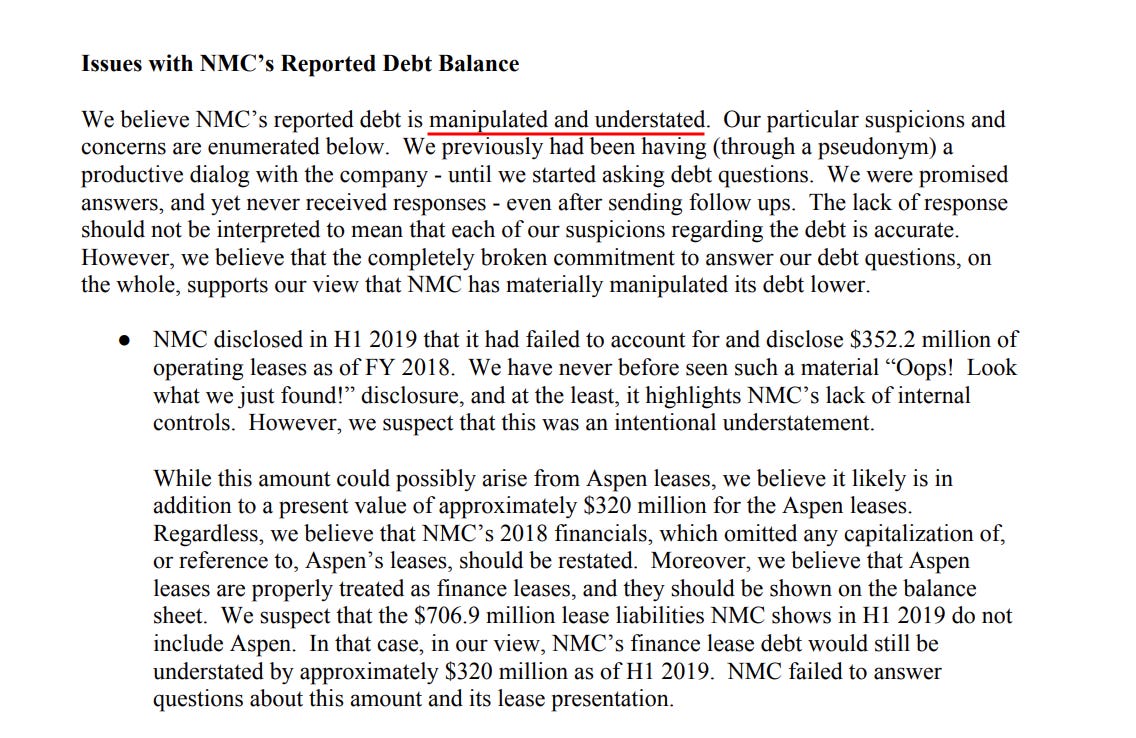

Then, in December 2019, the American short-seller Muddy Waters published a report questioning NMC’s debt accounts. What it exposed was that not only had they over-borrowed, but they had also been lying about how much it owed.

According to the Abu Dhabi Court’s own record of the case, the fraud ran from 2012 to 2020, involving very large sums being funnelled from the company to Shetty and others. This money was allegedly financed by some $4 billion of extra borrowing that was never disclosed in the company’s accounts nor authorised by its board. To hide it, the allegation goes, the group ran its money through a web of “sham supply contracts“ with connected companies and published false year-end accounts to the banks that lent to it.

The forensic work presented at trial suggested that NMC had technically been insolvent since 2013, and that, between 2012-2018, the group paid more into Shetty’s personal accounts than what the listed company earned in profit. Apparently, the money went on things like a private jet and a villa in Dubai Hills.

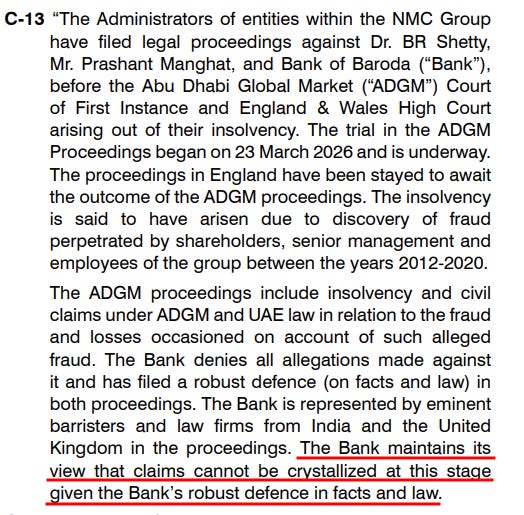

By mid-2020, the parent company had been placed under the control of joint administrators from the restructuring firm Alvarez & Marsal. They took over the duties and responsibilities previously held by the insolvent company’s directors, and their job is to claw back whatever they can for the people a collapsed company owes.

This is where the story of Bank of Baroda starts.

Why an Indian bank ended up in the dock

You see, plenty of banks lent to NMC. Lending to a company that later turns out to be a fraud doesn’t make you complicit. But BoB was more than just a lender; it was also a transaction bank that processed the payments, handled the trade finance and ran the account flows. The money at the centre of the fraud moved through Baroda accounts.

And that, the administrators argued, gave the bank a front seat view of the whole scheme.

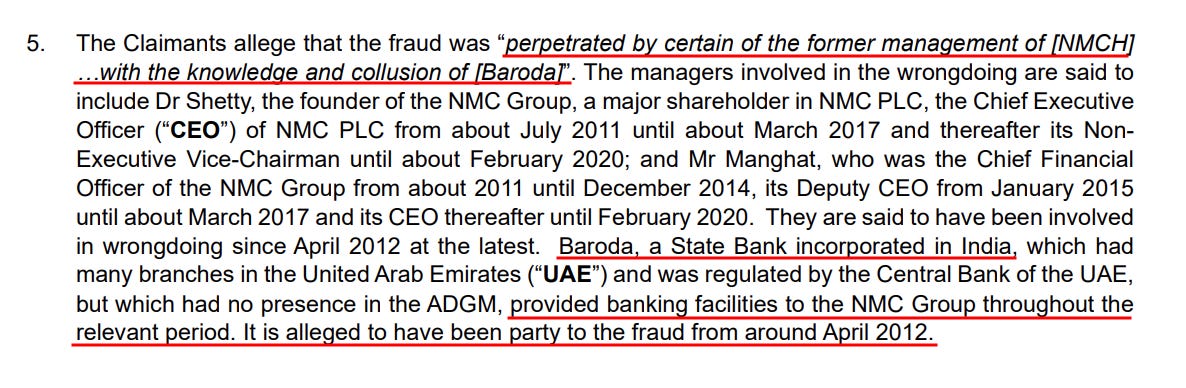

The allegation is as blunt as it gets: the fraud was carried out by NMC’s former management “with the knowledge and collusion of” Bank of Baroda. Specifically, the administrators allege the bank knew that the payments being made to Shetty and his companies had no genuine commercial purpose, and it structured deposits and overdrafts in a way that helped conceal NMC’s true debt.

How does that work? Well, when you hold a company’s deposits and its overdrafts at the same bank, you can net one against the other, so a heavily borrowed group looks almost debt-free on paper. Time a facility so that it is drawn during the year but cleared just before the reporting date, and the year-end snapshot, which is the number auditors and rival lenders see, comes out clean, before the borrowing is quietly drawn again afterwards.

The sharpest alleged example is when Shetty repaid a $100 million Baroda loan early so that the company could tell its auditors the debt simply did not exist so the creditors would stop asking questions. That is why the administrators say Baroda’s role went past just lending. All of this was happening in the bank accounts of BoB. Whoever at the bank runs the deposits, the overdrafts and the payment flows can see exactly what was happening.

Further, the administrators claim that the bank had a complete overview of virtually every transaction now under scrutiny, and that it failed to run proper anti-money-laundering checks. That could be because its staff knew what was going on, or they were recklessly blind to it. But either way, BoB was to be held responsible.

By the bank’s own account to the court, the stakes were enormous. BoB’s lawyers told the court that it faced claims in excess of $6 billion. It had never seen litigation on this scale, with the disclosure spanning over eight years, more than 500 accounts and some 24 million documents. Much of the relevant data sat on decommissioned servers and with staff working from India who had long since retired or gone home. So, this was a bank staring down a bottomless, years-long fight with its reputation and balance sheet both exposed.

What the courtroom heard

Nearly six years separated NMC’s collapse from its day in court. The administrators spent them tracing where the money had gone and building a case. The Abu Dhabi Global Market (ADGM) Court trial opened on March 23, 2026. Over the following months, Baroda’s own executives were put on the stand to explain how those compliance checks worked in practice.

The picture that came out was of a system running on autopilot.

On a single day in June 2014, the court heard, one bank official cleared 907 money-laundering alerts in 75 minutes; on a day in 2017, another 583 alerts were closed in about two hours. When the administrators’ lawyer suggested this looked less like scrutiny than just rubber-stamping, the bank’s executives pushed back. They said that the alerts may have been examined over several days before being formally closed, so the raw timings misled. One executive said that the bank had to believe what the customer was telling it unless something obviously looked wrong.

Baroda’s formal position was that the whole theory was far-fetched. It argued that the idea of its staff knowingly colluding in a years-long fraud was inherently improbable and that it was a large state-owned bank with no dependence on Shetty’s patronage or motive to help him.

The defendants besides BoB weren’t faring much better, though. Prasanth Manghat, NMC’s former chief executive, told the court he hadn’t had a firm grasp of the international accounting standards that the company was meant to follow when it listed in London. Shetty himself insisted he was himself a victim of a fraud run by his subordinates. Everybody was pleading innocent, and the judgement was due this month.

The cost of walking away

Before the judgement could be passed, on July 2, BoB’s Abu Dhabi branch paid the $600 million settlement fee, getting the case against them dropped. Resultantly, the court proceedings were discontinued and all claims between the bank and administrators were closed.

Baroda’s stated reason was that settling was cheaper and more certain than years of cross-border litigation. Which sounds fair, since a bad judgment could have cost multiples of that while dragging the bank’s name through the mud.

But the timing and the silence are what have people talking. As recently as May, in its own annual report, Baroda was still telling shareholders the claims “cannot be crystallised“ and that it had a robust defence. Weeks later, it wrote one of the largest cheques in its history. Shareholders might not have seen this coming.

Principal and agent

Now, there is a larger question here.

Suppose this had been a private bank. We have a ₹5,700-crore hit with an overseas branch accused of processing fraudulent flows and executives testifying to clearing hundreds of AML alerts an hour. It isn’t hard to imagine what would have happened after that.

Maybe a sharp regulatory response, hard questions for the board and maybe restrictions on the business. We’ve watched that playbook run when Kotak Mahindra Bank, Paytm Payments Bank or HDFC Bank fell short on technology and compliance. The RBI moved fast and hard with direct penalties.

State-owned banks, however, may tend to get a gentler ride. A relevant comparison is UCO Bank’s 2022 mess, when a glitch pushed out hundreds of crores in erroneous transactions and staff reportedly ignored weekend warnings. The bank recovered most of the money, the regulator quietly told lenders to keep IT staff on duty, and life went on. No penalty, no public reckoning.

That asymmetry may not be an accident. Nearly a decade ago, then-RBI Governor Urjit Patel gave a speech with a title that has aged well: banking regulation in India, he argued, is not “ownership neutral”. Unlike for private banks, the RBI cannot remove the directors or management of a state-owned bank, cannot supersede its board, cannot force it to merge, cannot revoke its licence, and cannot trigger its liquidation. Those people are appointed by the government, the bank’s actual owner.

The result, Patel warned, is a system of “dual regulation“ in which the one agency that can move quickly against a bank’s failings — the RBI — has had its teeth pulled when the state is in charge. That’s the frame critics are using now. The finance ministry and the RBI would both have had to intervene for a settlement this size. Yet there’s little visible sign of anyone inside the bank answering for the loss.

It isn’t the first time Baroda’s overseas conduct has raised these questions. The bank was caught up in South Africa’s “state capture” scandal, having kept serving companies tied to the Gupta family after other lenders had backed away. It exited the country in 2017.

That said, the settlement buys the bank closure of a sort. Its biggest overseas legal cloud is gone, and investors at least know the number now. But the NMC saga isn’t finished: the administrators are still pursuing Shetty and Manghat for creditor losses that run past $5 billion.

But the price of the settlement also includes the dilemma Patel raised in 2018: when a state-owned bank loses ₹5,700 crore, who is meant to answer for it? On the evidence so far, it isn’t anyone who ran it.

- This edition of the newsletter was written by Pranav & Kashish.

Tidbits

[1] AAI plans to enter the pilot training business

The Airports Authority of India (AAI) plans to set up flight simulator and pilot type-rating training facilities across its airport network. The move comes as India is expected to require around 30,000 pilots over the next 15–20 years and marks AAI’s expansion beyond airport operations.

Source: The Hindu BusinessLine

[2] Auto companies may soon trade BEE credits to meet fuel-efficiency norms

The government has proposed a credit trading system under CAFE norms, allowing automakers that exceed fuel-efficiency targets to earn and trade compliance credits. Companies that fall short can buy credits from the Bureau of Energy Efficiency, creating a more flexible way to meet emission standards.

Source: The Economic Times

[3] Government’s collateral-free export credit scheme sees limited uptake

Only 140 exporters have signed up for the government’s collateral-free export credit scheme since its launch in January, despite loans of up to ₹10 crore being backed by government guarantees. Experts attribute the weak response to low awareness and cumbersome paperwork, even as the scheme offering interest subsidies has seen much stronger participation.

Source: Business Standard

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Points & Figures by Zerodha

We’re always chasing the day’s biggest stories. But every now and then, we come across a dataset that deserves a closer look than a Daily Brief allows.

That’s what Points & Figures is for.

It’s where we step back from the news cycle and use data visualisations to tell stories about the Indian economy, financial markets, and investing. Stories that are difficult to tell in a ten-minute podcast or a daily newsletter.

Our latest edition traces how India’s digital economy got here, through the data buried in Jio’s IPO filings.

Join us on WhatsApp, where we share interesting soundbites from concalls, articles, and everything else we come across throughout the day. You’ll also get notified the moment a new video or article drops so that you can read or watch it right away.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Remarkable story on brexit, 🙏🏼🙏🏼