BPSL Ruling: Banks, Whistleblowers, and Big Questions

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

🧑🏻💻Have you checked out The Chatter?

Every week, we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Today’s edition goes out this evening. Subscribe to The Chatter to get it in your inbox.

In today’s edition of The Daily Brief:

A pyrrhic win for the rule of law

RBI is getting serious about Co-Lending

A pyrrhic win for the rule of law

The revival of the Odisha plant of Bhushan Power and Steel Limited (BPSL), after it had collapsed under the weight of its own debt, should have been one of the IBC’s biggest success stories.

This was a massive industrial asset that had once failed — due to mismanagement, overleverage, and a stalled economy. But it had found new life under new ownership. The company had started generating profits again. Thousands of crores had been recovered. Tens of thousands of crores in value had been created. A dead asset had been brought back to life. This was one of the largest insolvency cases India has ever seen — and it was messy, dirty and improvised. But ultimately, it seemed to work.

But last week, the Supreme Court ordered that it all be undone.

This is the story of how that happened — and what it means for India’s fragile insolvency ecosystem.

The criticality of debt resolution

The 2000s were a strange time in our economic history. We had stuck the path on our economic liberalisation for a decade, and the example of China showed us what was possible if we carried on. Our own economy seemed like it would soon see double-digit growth. This was a period of profound optimism, of a kind we perhaps haven’t seen since.

This optimism drew people to invest at a scale independent India had never seen before. If this was India’s turn to become Asia’s next tiger, as it seemed at the time, it made sense to build out the backbone of this newly emerging economy. People borrowed heavily, and invested that money into industries like mining, steel, infrastructure and power. Between the financial years 2003 and 2008, total investment shot up from 27% to an all-time peak of 39% of our GDP.

There was, however, a severe risk building up in the background. At the time, there was a lot of easy money available to anyone that wanted to invest: from both Indian and foreign lenders. Many businesses expanded almost entirely on the back of leverage.

But then, our momentum broke. Once the global financial crisis hit, funding dried up. Many companies, now burdened by huge debts and no room to raise more capital, struggled to keep the lights on. Meanwhile, a wave of anti-corruption protests in the early 2010s pushed the government into a period of paralysis, and many infrastructure projects stalled.

Businesses began defaulting on their loans, leaving mountains of ‘Non-Performing Assets’. Many valuable assets — power plants, steel mills and the like — were left to rot, as their debt-laden owners could no longer afford to run them. It took a decade of cleaning up to pull our economy out of this jam.

One of our most important tasks, during this time, was to ensure that we didn’t let the assets of those struggling companies go to waste, or all our growth over the 2000s would be for nothing. To this end, we introduced the Insolvency and Bankruptcy Code (or ‘IBC’), in 2016. The code, among other things, would rescue the idle, rotting assets of an insolvent company, transferring them to someone who could put them to good use. This would ensure that even as businesses and lenders fought endlessly, our economy didn’t lose all that productive potential. The proceeds from this sale, meanwhile, would go into paying off the defunct company’s loans, bringing some relief to its lenders. The law was profoundly important for the health of our economy.

And one of the most important cases under the IBC was that of BPSL.

Bhushan’s bad loans and JSW’s takeover

In its heyday, BPSL was a steelmaking giant, but one that ran almost entirely on debt. It borrowed heavily to set up a massive, state-of-the-art steel plant in Odisha — a big bet on an infrastructure boom that was to hit India. Only, that boom didn’t come quickly enough. The company fell apart during a downturn in the steel industry between 2014 and 2016. By 2017, it owed more than ₹47,000 crore to a variety of banks, and was in no position to pay them back.

This was a monumental sum. The company had become one of India’s largest loan defaulters, in fact. Something had to be done. The RBI labelled BPSL as one of India’s “dirty dozen” — 12 massive bad loans that, taken together, made for ~25% of India’s total NPAs. Their debts had to be resolved urgently for the health of our financial sector.

Meanwhile, it looked like BSPL’s promoters were trying to salvage whatever they could before abandoning ship. Multiple agencies — including the Enforcement Directorate — started investigating the company for financial fraud. They alleged that once things started getting bad, the company’s promoters pulled out more than ₹4,000 crore from BSPL through shell companies.

But for all of BSPL’s many problems, its massive steel plant in Odisha was still an attractive asset. Selling it would bring back at least some of the money that the banks were owed. When it was auctioned as part of the insolvency proceedings, major steel players — like Tata Steel and JSW — made their bids for it. After a bidding war that lasted over a year, JSW came out ahead. It would pay out ₹19,700 crores to the company’s creditors — around 41% of what they were owed — and would infuse another ₹8,550 crores into the company as equity. Although BSPL’s creditors would lose much of what they had loaned out, they approved this plan through an e-vote.

Only, the process of getting there was deeply messy:

One, it was marked by severe delays at every stage. The initial resolution process ultimately took nearly two years to reach an end — far more than the 270 days the IBC technically allowed. This included all sorts of legal maneuvering, including JSW challenging its own successful proposal before the NCLAT. Nobody took legal permission for these delays, as they had to under the law.

Two, there were procedural issues throughout the bidding process. For one, the bidding process was far from clean: once everyone placed their bids, individual lenders privately negotiated a final deal with JSW, and then declared them the winner — while other bidders were kept in the dark. Moreover, JSW hid important details about its prior ties with BPSL while making its bid — which raised questions on whether it was eligible to bid at all.

Three, ‘operational’ creditors — people who had supplied goods or services to the company — were largely sidelined through this process. The final plan didn’t repay them in full; they were only paid ₹350 crore against claims of ₹733 crore. This isn’t unusual under the IBC, but it did raise questions about how fair this process was, and how it balanced the interests of different creditors.

Four, the ED’s investigation added a lot of confusion to the entire process. Government agencies were probing Bhushan Steel for money laundering and fraud, in parallel to the insolvency proceedings. The ED considered some of the company’s assets as “proceeds of crime” — and tried to freeze them. Crucially, they did so after the resolution had already been approved, so it wasn’t even clear if JSW had a clean right over the plant. Their presence sparked a whole round of legal proceedings.

Five, amidst all the confusion and the many legal proceedings, JSW dragged its feet on actually paying anything out. It only started making its payments in March 2021 — almost four years after insolvency proceedings began. Operational creditors had to wait for even longer.

Six, when it finally took control of the company, it did so through a complex structure. At first, it only took over 49% of BPSL — while the rest was held by a sister company. Moreover, instead of directly infusing capital into the company, it subscribed to “Optionally Convertible Debentures” — which it could turn into shares at its convenience. This allowed it to hold off until it was sure of its investment.

Despite all these pain-points, though, things were slowly turning around. The NCLT and NCLAT ignored these hiccups, and gave things their stamp of approval. The plant changed hands, and came back to life. Its creditors were paid a part of what was due. It seemed like the proceedings were ultimately a success story for the IBC framework. The Supreme Court, however, thought otherwise.

The case before the Supreme Court

Fast forward to 2025. After multiple delays, JSW finally took over BPSL’s Odisha plant in March 2021. It then turned it around over the next four years. In FY 2024, the BPSL unit sold nearly 3 million tonnes of steel — its highest ever. It earned almost ₹22,000 crore in revenue for the year, with a net profit of more than ₹650 crore. In essence, it had successfully breathed life into an asset that was all but dead.

This turnaround required a lot of work. JSW had to restructure its supply chains, weed out bottlenecks, and make major technological investments. Through this, it successfully expanded the plant’s capacity to 3.5 million tonnes a year. And it was now looking to expand even further — with plans in place to increase its capacity to 5 million tonnes a year.

This looked like a success story: the assets had been revived and were being put to use. They hadn’t been lost because of a bankruptcy. This was just as the IBC intended.

But not everyone was happy. The company’s operational creditors were still miffed by how they were sidelined by the process. The government of Odisha had some pending tax dues that it hadn’t brought up earlier, but was seeking now. And the old promoters of BPSL had entered the fray, on the pretext that proper procedure hadn’t been followed. All of them challenged the insolvency proceedings before the Supreme Court.

One week ago, most people would have imagined that the Supreme Court would leave things as is — after all, the resolution was a fait accompli. The plant had already changed hands, and was thriving under its new owners. But instead, the Supreme Court ordered that everything be rolled back.

Why? Well, in short, it saw the whole process as a severe violation of legal procedure. Everyone acted in a compromised fashion in its eyes; nobody stuck to the law:

With the many delays and procedural irregularities, the entire plan was void ab initio — that is, it was never legal to begin with. With all these failures, even the fact that the NCLT and NCLAT approved the plan didn’t rescue it in the court’s eyes.

The committee of creditors, according to the court, failed to exercise their “commercial wisdom” — letting it pass through despite irregularities. This, to the court, hinted at the creditors themselves being compromised. In a sense, the court charged the company’s creditors with failing to protect their own interests — even though none of them complained in the first place.

The NCLAT, in letting the plan pass despite all these irregularities, had abused the process set down by law. It didn’t have the power to condone blatant legal non-compliances.

The court’s harshest words, however, were reserved for JSW. In its eyes, the company was supposed to fulfil its obligations promptly. By dragging its feet, filing unnecessary cases and delaying payments, it had essentially behaved maliciously, and could not be permitted to get away with it.

So what happens in such a situation? Ultimately, this is a little like pushing toothpaste back into a tube. The IBC, frankly, doesn’t even contemplate such a possibility. So, the Supreme Court made a new remedy.

Here’s what it decided: BPSL’s old creditors, the banks, will have to repay JSW the ₹19,700 crore it had paid them within two months. JSW will lose ownership over the plant, and all the revenues besides. The plant will be liquidated. That is, the plant must now be broken up and sold for parts — even though it’s a functioning, profitable business today. The creditors will only be paid from whatever one can earn out of this fire sale.

Given that this is a decision of the Supreme Court, its word is probably final. JSW has limited legal options in the matter — although it can ask for a ‘review’, in practice, that works very rarely.

Where does this leave us?

We’re deeply split about how to think about this decision.

Of course, the Supreme Court is technically correct: from what we can see, the parties didn’t follow the full letter of the law. There were procedural violations every step of the way. And if you constantly turn a blind eye to such irregularities, you eventually compromise the very heart of the law.

But it’s worth thinking about how messy the circumstances were. This was all a test case for a new law, and we were still in the process of figuring out how to implement it. At stake was a massive industrial unit that had failed, and people were risking tens of thousands of crores to bring it to life. There was no universe where the creditors would earn everything back; ultimately, everyone was trying to make the best of a bad situation. Meanwhile, all sorts of criminal investigations — by everyone from the CBI to the ED — threatened to derail everything.

Somehow, through all the confusion and uncertainty, we had reached somewhere. The promise of the IBC — of rescuing assets from those who couldn’t run them — had been fulfilled. Or so it seemed.

There’s something profoundly tragic about how everything finally played out. A thriving steel plant, one with tens of thousands of crores in revenue, will now be torn apart. All the progress made in turning it around will be lost. Its employees will suddenly be forced to fend for themselves. Its creditors will be slapped with an unexpected liability that will be due in two months. They’ll have to pay out whatever little they could salvage from a bad loans, and then wait through lengthy liquidation proceedings. And at the end of it all, they will probably recover less money. And just like that, a pocket of economic productivity, in a country already starved of wealth, will forcibly be shuttered.

And every time someone plans a bid under the IBC in the future, this case will haunt them.

Maybe the Supreme Court had to be harsh, to make sure everyone respected the law. Maybe this was necessary to preserve the rule of law. But if this was a victory for the rule of law, it was a pyrrhic one.

RBI is getting serious about Co-Lending

The Reserve Bank of India (RBI) recently published draft regulations on Co-Lending Arrangements early last month. This marked the latest evolution in India’s co-lending journey.

This was a concept that began in 2018 with a simple “co-origination” model: a bank would team up with an NBFC for its priority sector lending (an idea we’ve covered before), and both would share the risks and rewards. It was then revamped in 2020 into the so-called co-lending model (CLM) — where the scope of these arrangements was widened considerably. The draft regulations now bring the latest formulation of this concept.

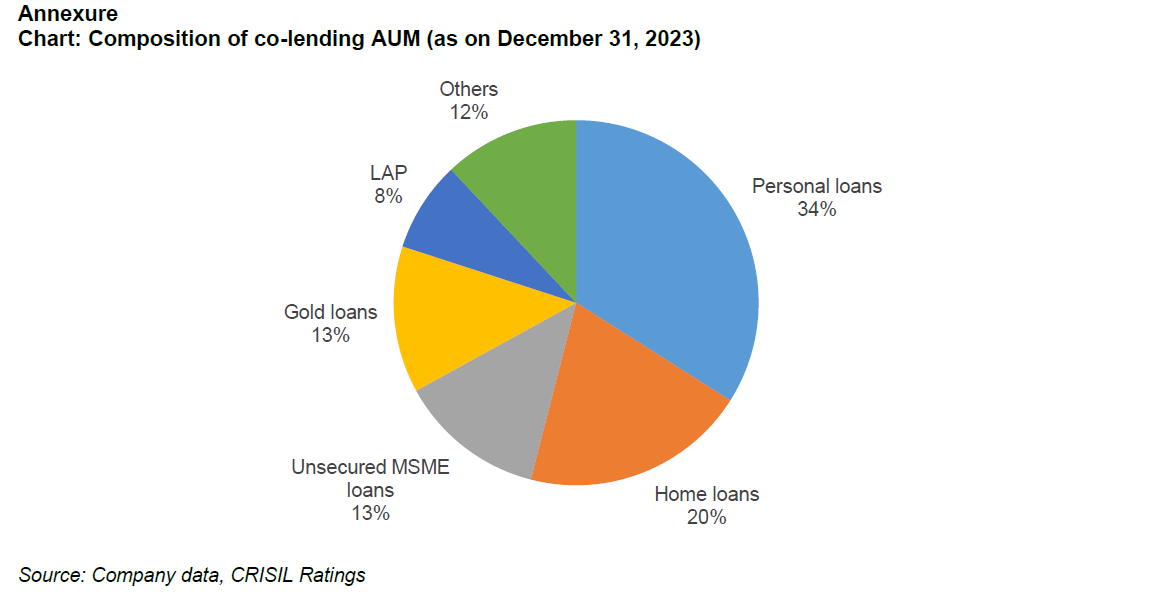

And it’s growing big: within a few years, the total co-lending book of non-bank lenders (NBFCs) is now nearing ₹1 lakh crore in assets, as of April 2024. From just priority sector loans, like those for agriculture and small businesses, co-lending has expanded to many retail loan types — personal loans (34%), home loans (20%), MSME loans (13%), gold loans (13%), and more.

The core idea is straightforward: combine the strengths of two lenders — combining one’s customer reach with the other’s deep pockets — so that more people get loans at lower cost. It’s a “win-win” for both sides – NBFCs get easier access to bank funding and can grow without needing tons of capital, while banks get to reach new customers (and fulfill targets like priority sector lending) by piggybacking on NBFCs’ niche presence.

Now, in value terms, co-lending might look miniscule compared to the total banking credit of ₹181 lakh crores. What this number doesn’t capture, though, is that loans under co-lending arrangements often find themselves going directly in the hands of the bottom decile of the strata of the society. It is those credit starved individuals, who need credit to set up their small business or buy a home for themselves, that may find no bank willing to lend to them, while NBFC loans are simply too expensive. Co-lending gives them a chance at a cheaper source of loans.

What is Co-Lending, in Simple Terms?

At its heart, co-lending means two lenders teaming up to give a joint loan to a borrower.

For example, a bank and a non-bank (NBFC) might form a partnership: the NBFC sources a customer and processes the paperwork, and the bank provides a large chunk of the funds. The loan itself is shared between them – each lender keeps a percentage of the loan on their books (say 20% with the NBFC and 80% with the bank). Both lenders thus earn interest on their portion and share the risk in that ratio.

To the borrower, this typically feels like a single loan (often serviced by the NBFC), but behind the scenes two institutions are involved in the funding.

Under the earlier framework, RBI had defined two modes of co-lending:

[1] CLM-1 (Co-Lending Model 1), where both lenders put in their share from day one, from the very first disbursement.

[2] CLM-2 allowed a sort of “originate-and-transfer” model – where one lender (usually the NBFC) could initially disburse the entire loan and later periodically sell a portion (e.g. 80%) to the partner bank. In practice, CLM-2 was a way for banks to cherry-pick loans after origination.

The new 2025 draft does away with the CLM-2 concept in co-lending. Loans must now be co-funded from the start. If a partner only buys into a loan after it’s already made, that’s basically treated as a normal transferring a pool of loans from one entity to another, and not “co-lending”

It’s also helpful to clarify what co-lending is not.

This is not about co-branded credit cards or other products, where two financial companies team up for marketing but don’t share the risk of each loan.

And it’s not the same as a large syndicated loan to a single business. In fact, the draft guidelines explicitly exclude large loans (over ₹100 crore) made via consortium or syndication.

Very specifically, co-lending is typically about relatively smaller loans to many borrowers — not one huge project finance loan shared by a bunch of banks — where both parties take some of the reward, in exchange for putting up with some of the risk.

What’s Changing in the New Draft Rules?

The RBI’s April 2025 draft guidelines propose several significant changes to the co-lending framework. In a nutshell, the rules are being expanded and tightened to encourage more partnerships while protecting customers and managing risks better. Here are the four big changes that we think are the most relevant:

Much Wider Scope: Previously, co-lending was mainly restricted to arrangements between banks and NBFCs for priority sector loans, unless they took special permissions from the RBI. Now, the draft says any two regulated lenders can co-lend, and it’s no longer limited to just priority sectors.

This means a bank could even partner with another bank, or an NBFC with another NBFC, if they find some synergy. It also means co-lending could target any type of loan – housing, consumer, MSME, you name it – not just agriculture or small business loans. As per some studies, about 75% of the co-lending volumes handled by banks are already in non-PSL loans. However, these were based on approvals granted by the RBI on a case by case basis to specific banks that had sought permission. That will no longer be the case.

Moreover, co-lending earlier came with a rigid 80:20 split between the bank and the NBFC. That’s now gone. While earlier guidelines required the NBFC to retain at least 20% of each loan, the new framework does not mandate a fixed ratio. Lenders have flexibility to decide how to share the loan — anything works as long as both have skin in the game. This wider scope could open the door to many new combinations of partners and loan products under co-lending.

Greater transparency and customer protection: Co-lenders shouldn’t confuse the borrower about who their lender is or what the loan terms are. The new rules mandate clear disclosures and agreements. The borrower should know that the loan is being made jointly, and who is responsible for what. The loan agreement must clearly spell out the roles of each partner – for instance, which lender sourced the customer, who is funding how much, who will handle servicing, how to complain if issues arise, etc.

Importantly, the borrower will be told a single blended interest rate, which is essentially the weighted average of the two lenders’ rates for their respective portions. Behind the scenes, each lender charges their own rate on their part, but the customer will only deal with one combined rate. If there are any additional fees – say the bank pays the NBFC a sourcing or servicing fee – that must be kept separate from the interest rate and transparently disclosed.

In short, the borrower should get full clarity on the cost of the loan and the arrangement, rather than being caught by surprise by hidden charges or unclear lender roles.

Default loss guarantee (first-loss support) allowed: The RBI will now allow a modest Default Loss Guarantee (DLG) in co-lending partnerships. Essentially, one partner (often the NBFC) can assure the other that it will cover a small portion of losses if some loans go bad – up to 5% of the total loan pool under the arrangement.

In co-lending so far, NBFCs sometimes gave informal first-loss guarantees to banks to sweeten the deal. But the law itself was silent on this. Now it’s explicitly permitted, but capped at 5% of the outstanding loan. This means an NBFC could say to a bank, “I’ll take the first 5% of any loss hit, beyond my 20% share, so you’re extra protected.” Such a guarantee can make banks more comfortable partnering (since they have a safety buffer for defaults), and it pushes the NBFC to keep loan quality high.

However, by capping it, RBI also ensures the NBFC isn’t overextending itself with too big a guarantee, and putting itself under risk. It’s a balanced way to encourage risk-sharing innovations while preventing excessive risk transfer.

Unified NPA classification: A perennial issue in joint lending is how to classify a loan as a NPA (Non-Performing Asset) when things go south. The draft guidelines make it clear that if a co-lended loan turns bad for one partner, it must be marked as bad for both. In other words, asset classification has to be consistent across both lenders.

This ensures there’s no regulatory arbitrage or delay in recognizing stress. Both partners will be on the same page regarding the loan’s status. It essentially forces timely recognition of trouble and hopefully more coordinated recovery efforts, since neither can pretend the loan is fine if the other knows it’s not.

What Do These Changes Mean: The Good & Bad?

If we are to look at these changes objectively, here’s how the regulation could play out, if and when it becomes a reality:

Encouraging More Credit Flow via Co-Lending vs. Direct NBFC Funding:

In recent years, bank lending to NBFCs (indirect lending) was robust, but regulators were growing cautious about banks taking large exposures to NBFCs after episodes like IL&FS (2018) and DHFL (2019) crises. These could suddenly create system-wide financial instability.

Co-lending offers an alternative: instead of lending to an NBFC (which concentrates risk on that NBFC’s solvency), a bank can lend with an NBFC directly to borrowers. This moves the risk to individual borrowers, while the bank has direct recourse to their assets. Thus, RBI by expanding co-lending could be steering banks and NBFCs toward a model that spreads risk more granularly.

Unlocking More Funding for MSMEs and Underserved Segments:

A major effect of this move would be to boost credit flow to MSMEs and borrowers who were outside PSL definition. Under the old rules, if an MSME wasn’t part of a priority sector (say, it was a slightly larger enterprise or in a service sector that was not covered), it couldn’t directly benefit from bank-NBFC co-lending. The draft guidelines explicitly mention that broadening co-lending to all loans will provide credit access to MSMEs that earlier could not qualify for such loans.

But this doesn’t automatically mean that money would start pouring in for MSMEs now under co-lending arrangements. It’s now possible, but ultimately, it will only attract capital based on its merit, compared against other places where they can lend profitably.

Operational Complexity & Delays:

The need for coordination between two (or more) lenders at every stage is a big hurdle for co-lending to really take off. Lenders must synchronize their underwriting processes, IT systems, loan documentation, accounting, and customer service. Many banks and NBFCs have found it challenging to integrate technologically – “India does not have too many tech players who can integrate with banks and NBFCs,” as one industry CFO noted. This can lead to delays and teething troubles.

Moral Hazard and Skin-in-the-Game Issues:

A classic concern in risk-sharing models is ‘moral hazard’ – the idea that because the originator (NBFC) doesn’t bear the full risk of a loan, it might not be as careful in underwriting. The 20% minimum retention was meant to mitigate this. And indeed, when NBFCs have skin in the game, it does align their incentives. However, 20% is no longer mandatory. An NBFC might be tempted to originate volumes a bit more aggressively, knowing that a bulk of the risk is with the bank. If not closely monitored, this could lead to deterioration in asset quality of co-lent loans.

All in all, co-lending space has sprung into action since 2018, when it was formalized. This draft is a big milestone towards taking it more mainstream. We will have to wait and watch how does this translate into real life impact, as intended by the RBI.

Tidbits

Mahindra & Mahindra Q4 Profit Rises 22% but Misses Analyst Estimates

Source: Reuters

Mahindra & Mahindra reported a 22% year-on-year rise in fourth-quarter profit to ₹2.4 thousand crore ($290 million), missing analyst expectations of ₹2.5 thousand crore. Total revenue increased 25% to ₹31.35 thousand crore, exceeding forecasts of ₹30.13 thousand crore. The company’s automotive business, which contributes nearly three-fourths of overall revenue, grew 25% to ₹2.4 thousand crore, driven by an 18% rise in SUV sales, including strong demand for models like the XUV 3X0 and the five-door Thar. The farm equipment segment saw a 23% revenue increase, supported by a 23% rise in tractor sales and a 51% jump in pre-tax profit. However, results were weighed down by a one-time charge of ₹645 crore related to international tractor operations. Despite the profit miss, the company’s top-line performance remained solid across both automotive and farm segments.

SBI Targets 12–13% Loan Growth for FY26 Despite Margin Pressures

Source: Reuters

State Bank of India reported a nearly 10% year-on-year drop in net profit for the January–March quarter, posting ₹18.64 thousand crore compared to ₹20.69 thousand crore a year earlier, though it exceeded analyst estimates of ₹17.73 thousand crore. The bank’s net interest income rose 2.7% to ₹42.77 thousand crore, but its domestic net interest margin fell to 3.15% from 3.47% a year ago. SBI’s loan growth reached 12.03% in FY2024-25, and it now aims for 12–13% growth in FY2025-26, keeping projections nearly flat. Deposits grew by 9.48% last year, with a 9–10% rise expected this year. The bank’s corporate loan book pipeline stood at ₹3.4 lakh crore as of March-end. Meanwhile, the board approved a ₹25 thousand crore equity capital raise to strengthen capital ratios, with timing dependent on market conditions. Chairman C.S. Setty noted that further pressure on margins is expected, assuming another 50-basis-point rate cut by the Reserve Bank of India this year.

Saudi-India Refinery Talks Stall Over Crude Supply Terms

Source: Business Standard

Saudi Arabia’s plans to invest in two Indian oil refineries — BPCL’s east coast complex and ONGC’s west coast Gujarat project — have hit a roadblock over crude supply negotiations. Saudi Aramco is pushing to supply 50% of the crude at official selling prices, while India wants the share aligned with Aramco’s expected 20% stake and at a discount. According to Aramco’s 2024 annual report, its average overseas stake is 35%, but it supplies 53% of the crude to those ventures. Saudi Arabia, once India’s largest oil supplier, has lost market share due to India’s rising imports of discounted Russian crude. The Crown Prince’s 2019 pledge of $100 billion in Indian investments has seen only about 10% realized so far. Previous mega-projects like the $60 billion Aramco–ADNOC refinery and the 20% Reliance stake fell through, increasing pressure to finalize these current deals. Indian refiners, however, believe they can raise local debt without needing Saudi equity if supply terms remain unfavorable. Saudi Aramco is also eyeing up to a 15% stake in IOC’s Panipat refinery, with the Indian government reviewing the proposal.

- This edition of the newsletter was written by Pranav and Kashish.

🌱Have you checked out One Thing We Learned?

It's a new side-project by our writing team, and even if we say so ourselves, it's fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That's all. It's chaotic, it's unpolished - but it's honest.

So far, we've written about everything from India's state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you're looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

I have one question it might be silly but I couldn't understand who gives analyst estimation for financial performance. I know that it is a collection of different analyst expectations but who collect this data and say this is the analyst expectations