Big trends from this results season

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts or wherever you get your podcasts and video on YouTube.

In today’s newsletter, we look at how the last quarter was for Indian companies and give you a broad overview of everything that happened.

Then, we talk about how India's proposed regulation aims to oversee tech acquisition deals but faces challenges due to limited resources.

Quarterly Review

Let's take a look at how Indian companies performed last quarter, now that the results season is nearly over. With major companies across sectors announcing their results, it’s a good time to reflect on how they fared.

Overall, companies saw their sales grow by 7.7% compared to the same quarter last year. At first glance, 7.7% might seem like a solid number, especially when you consider that last year’s growth was just 2.3%. But there’s more to the story. While sales did improve, profits didn’t keep up. The reason? Companies had to spend more on raw materials and other expenses, which ate into their profits.

But it’s not all bad news. One of the brighter spots was the long-awaited recovery in rural India. Rural regions were hit hardest by COVID and have been struggling ever since, with depressed wages, poor monsoons, and crop failures adding to the woes. However, things seem to be looking up now. People are starting to buy more everyday items like groceries, two-wheelers, and even tractors. The monsoons, which are critical for farming and rural demand, are on track to be normal, helping to fuel this recovery.

On the flip side, the oil industry didn’t fare so well. Elections slowed down government spending, and seasonal factors also played a role in the sluggish performance. Similarly, the cement and steel industries faced their own struggles. Cement sales were low because construction activities slowed during the election season and extreme heatwaves. Steel, too, faced headwinds from lower prices and competition from cheaper imports.

Given the breadth of sectors, it’s tough to cover everything in a short podcast. So, we’ll focus on the consumer companies, financials, and auto companies—sectors that touch our everyday lives and carry significant weight in the Nifty index.

Consumer and Retail Segments:

Rural India’s resilience was one of the biggest positives this quarter. More FMCG companies reported that their growth in rural areas outpaced urban centers compared to previous quarters.

Why?

Companies lowered prices and offered better deals to encourage spending in rural regions. This strategy worked, driving stronger sales. For example, everyday items like toothpaste, soaps, and snacks saw significant boosts in rural markets, thanks to affordable pack sizes and promotions tailored to price-sensitive consumers.

However, heatwaves had a notably negative impact on consumer companies. You might think beverages would do well in rising temperatures, but the heatwaves were so intense that they actually discouraged people from going out, reducing sales in outdoor establishments like restaurants and stores. Consumers, concerned about the economic situation, prioritized essentials like water over discretionary items like soft drinks and alcohol. This trend wasn’t just limited to beverages; other sectors, like home insecticides and paints, also faced challenges. When it’s unbearably hot, home improvement projects like painting are the last thing on people’s minds.

Premiumization, a big trend over the last few years, saw some setbacks this quarter. With high inflation, some consumers opted for value-for-money options, especially in categories like personal care and packaged foods. Companies had to give discounts to push sales of premium products, a shift that was particularly noticeable.

Retail Sector:

The retail sector also had a tough quarter. The extreme summer heat kept shoppers indoors, leading to lower footfalls in malls and retail outlets, especially in categories like apparel and footwear. As a result, companies had to rely more on online sales channels and heavy discounts to maintain their sales. Despite the sluggish overall demand, essential goods and groceries continued to see steady sales, as people prioritized their daily needs.

Financial Services:

Moving on to financial services, banks and NBFCs faced their own set of challenges this quarter. In the banking sector, competition for deposits was fierce, leading to slower deposit growth and rising funding costs. Despite these hurdles, banks managed to maintain steady performance, supported by improving asset quality and strategic moves to sustain profitability.

However, the quarter saw relatively slow growth in both credit and deposits, with many banks reporting lower-than-expected deposit growth, which increased the Credit-to-Deposit ratio. To attract more deposits, banks had to raise their deposit rates, which, in turn, increased their overall cost of funds. This led to a slight moderation in Net Interest Margins (NIMs), the difference between the interest income generated by the bank's loans and the interest paid out to depositors.

The decline in the Current Account Savings Account (CASA) ratio, which indicates low-cost deposits, meant higher funding costs for banks as they had to rely more on term deposits.

NBFCs had a quarter to forget. The mortgage segment, a key driver for NBFCs, faced significant challenges due to a new RBI circular called the Fair Practices Code. This circular introduced stricter rules and added more scrutiny to the loan disbursement process, slowing down the pace at which loans were approved and given out. Asset quality also deteriorated slightly in most product segments, with factors like elections, heatwaves, seasonality, and higher employee attrition rates contributing to operational hiccups. The Microfinance Institutions (MFI) segment, which provides small loans to low-income groups, had a particularly tough time, with lower-than-expected collections and an increase in risky loans adding to the pressure.

On a slightly positive note, borrowing costs for NBFCs largely peaked during this quarter, with some hope that these costs might ease if the RBI decides to cut repo rates in the future. In the gold loan segment, competition has cooled down a bit, which might increase demand for gold loans as unsecured credit becomes harder to obtain.

Automobile Sector:

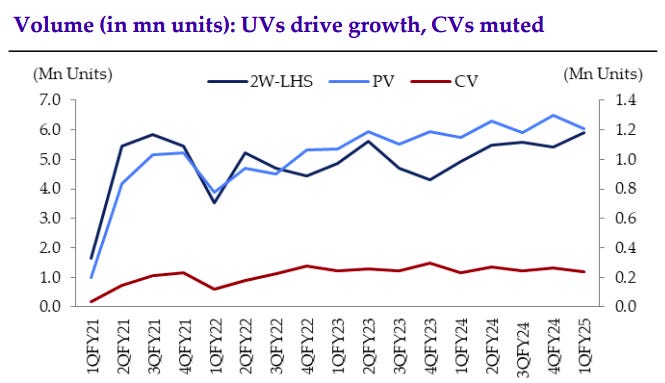

The automobile sector had a mixed performance this quarter, with some segments doing well and others struggling. Overall growth was driven by rising demand in certain segments, stable raw material costs, and ongoing trends like premiumization. The passenger vehicle segment saw moderate growth, with a continued shift towards utility vehicles like SUVs, supported by new model launches and the increasing popularity of hybrid and electric vehicles (EVs).

Premiumization was also a key driver, as consumers opted for higher-end models with advanced features, boosting average selling prices (ASPs) and improving margins for manufacturers

The commercial vehicle (CV) segment had a tougher time, with subdued growth mainly due to the high base effect from the previous year and seasonal factors like elections and extreme weather. However, within the CV space, the bus segment outperformed the truck segment, driven by increased urbanization and the growing need for better public transportation.

The two-wheeler segment had a strong showing, particularly in rural areas where demand for entry-level and mid-segment motorcycles picked up. A better-than-expected monsoon boosted rural incomes and spending, contributing to this growth. Urban consumers also drove demand for premium scooters and bikes, looking for stylish and feature-rich options.

The electric vehicle (EV) segment continued its gradual growth, with more consumers considering electric options, especially in the two-wheeler and passenger vehicle categories. Automakers are increasingly focusing on EVs, investing in new technologies and product development to drive growth in this segment, even though the overall market share for EVs remains relatively small.

On the downside, the export market faced challenges, particularly in regions like Europe and Africa, where economic conditions remained weak. This led to lower export volumes for many automakers, impacting their overall performance. Currency devaluation in key export markets added to the challenges, making it harder for automakers to maintain profitability on exported vehicles.

Killer acquisitions and competition

Let’s talk about India’s proposed regulation to oversee tech acquisitions. Picture this: You’re the CEO of a tech giant like Amazon or Google. Your company is a powerhouse, an integral part of the global economy. You’re on top of the world, and nobody even dares to step into your domain. But then, someone comes along with a fresh, innovative way of doing business. They start chipping away at your dominance. Suddenly, your massive, well-established company feels like a burden because it’s built for an era that’s starting to fade. This is exactly how the digital camera knocked out Kodak, how Microsoft outpaced IBM, and how Netflix put Blockbuster out of business. The old guard simply couldn’t keep up with the new wave.

As a smart tech CEO, you’re aware that this kind of creative destruction could happen to you too. So, what do you do when a promising new company starts making waves? One option is to swoop in, offer the founder more money than they ever dreamed of, and buy their company. If you can integrate it into your business, great. If not, no worries—a company you own can’t threaten your empire. This is what’s known as a “killer acquisition.”

Now, let’s flip the scenario. Imagine you’re the ambitious CEO of a new startup. Your best-case scenario might be to raise a lot of money, grow the business, go public, and become a multi-billionaire. But let’s be real—few companies make it that far. Aiming for an IPO is like a batsman aiming for a triple century; it’s fantastic if it happens, but the odds are low. So, you need a Plan B: an exit strategy for when massive success seems out of reach. For many founders, that exit is being acquired.

In this sense, both tech giants and startups want acquisitions to be straightforward. If both parties are willing, what’s the problem? Well, there’s a larger issue at play. A 2022 paper by Raghuram Rajan, the former RBI governor, and his co-authors found that big tech companies often create a “kill zone” around themselves. They buy up startups that could potentially challenge them, but that’s not the worst part. The paper suggests that when a big tech company makes an acquisition, it depresses the entire sector. New companies become less likely to enter the space, and venture capitalists are half as likely to invest in it over the next three years.

This seems counterintuitive, right? If tech giants are throwing money at new entrants, shouldn’t that encourage more people to start businesses in that space? Here’s the catch: tech companies thrive on ‘network effects.’ The more users a product has, the better it becomes for everyone. You use Amazon because most sellers are there, and sellers use Amazon because you’re there. The same goes for platforms like WhatsApp. This network effect is a huge advantage for the tech giants but a massive hurdle for their competitors.

Whenever a big tech company makes an acquisition, it gives users another reason to stick with their platform, making it even harder for anyone else to compete. As a result, acquisitions can make a sector less attractive to new businesses.

Now, let’s look at this from a regulator’s perspective. Here’s the dilemma:

- Generally, acquisitions are good because they create efficiencies. The new owner can often do more with the acquired company, which is why they’re willing to pay so much for it.

- Acquisitions also make startups more attractive by providing a way to cash out other than an IPO.

- But sometimes, big companies acquire smaller ones just to prevent a more efficient way of doing business from emerging.

- These “killer acquisitions” can stifle innovation in the sector, reducing its “dynamic efficiency.”

So, what do you do? If you want to regulate this, you need a way to determine whether a particular acquisition is good or bad for the economy. The challenge is, we don’t really have a reliable method for that. The best solution anyone has come up with is this: Make all the big companies report when they plan to acquire someone, and then have some really smart people take a hard look at the proposal. Hopefully, they can figure out if it’s a good idea or not.

India is moving in this direction with its proposed Digital Competition Bill. Under this bill, any acquisition worth more than Rs. 2000 crore (about $240 million) would have to be reported to the Competition Commission of India (CCI). The CCI would then examine the proposal and decide whether the acquisition should proceed. The bill essentially aims to turn the CCI into a super-regulator for India’s tech industry.

Is this a good idea? There’s reason to be cautious. The basic model for this kind of regulation relies on very smart people predicting the future impact of tech acquisitions. The problem is, that the CCI currently doesn’t seem equipped to handle this. It has just three whole-time members carrying the entire workload. The CCI is under-resourced, understaffed, and overworked. At least in its current state, taking on the additional responsibility of policing India’s tech ecosystem might be too much to ask.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

If you have any feedback do let us know in the comments.