Big Tariff Shift? India’s Bold Trade Response!

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube.

In today’s edition of The Daily Brief:

The reciprocal tariffs are here (maybe?)

ITC makes a 3,500 crore acquisition

The reciprocal tariffs are here (maybe?)

A few weeks ago, Donald Trump threatened to slap "reciprocal tariffs” on any country that tariffed American goods more than America tariffed theirs. Those are supposed to kick in today, a day that he’s now calling “Liberation Day.”

India, as we explained before, is right in his crosshairs. We have some of the highest tariff rates in the world — a lingering hangover from our protectionist past. At the same time, over one-sixth of all our goods exports currently go to the United States. If the United States decides to go tit-for-tat in retaliation for our tariffs, that could create serious issues for Indian industry.

Those are just threats, though. Is that how things will actually play out?

We had no clue a month-and-a-half ago, when we first covered this story, and to tell you the truth, we still don’t. That’s the core challenge in trying to anticipate Trump’s moves: he’s trying to keep you on your toes. He bluffs and sends mixed signals in the hope that, by sowing enough chaos in people’s minds, he gets the upper hand. We know this is frustrating if you’re hoping for some predictability to size your investments properly. But sadly, it’s something we’ll all just have to live with.

Oh, and that’s not where things end. Make no mistake; this chaos will only compound. Everyone from businesses to investors to policymakers will react, perhaps sharply, to whatever Trump does. When that happens; when decision-makers across the world respond simultaneously to a volatile situation, what are the aggregate, economy-wide effects you might see? We have absolutely no clue.

Anyhow — if India is to be hit with tariffs, they’ll probably come in by tonight. So, what should you know if you’re trying to assess their impact? What context do you need to anticipate what might happen? In our previous piece on the topic, we tried sketching out the broad contours of India-US trade, and what tariffs could do to this relationship.

Today, we’re going to follow that up with the more immediate context for his moves. We’re going to look at what India has done to try and cajole the United States, and how the two countries’ trade negotiations have panned out over the last month. We’ll also throw in a few speculative questions that we have. We don’t know what any of it might actually mean for you. But hopefully, if we ask enough questions, we’ll begin to see what shape the answer could take.

Let’s dive in!

India’s trying hard to work something out

Ever since Trump came into power, India has been trying to placate him. We’ve been on a trade negotiation blitz, aimed at somehow extracting some sort of concession from Trump.

It began with Prime Minister Modi’s visit to Washington, back in February 2025. The threat of tariffs hung heavy over their talks. Prime Minister Modi made big promises to his American counterpart, signalling that India was willing to engage. He promised to buy more U.S. energy and defense gear. The two countries also announced that they were working their way towards a new trade deal.

Since then, the Indian government has been at work trying to woo the United States. Early in March, Commerce Minister Piyush Goyal met his U.S. counterpart, Howard Lutnick. India’s tariffs came up again in their discussions, along with more discussions around a trade deal. Later, the same month, a US trade delegation landed in New Delhi, to hammer out the details of the proposed trade deal sector-by-sector. The two sides claimed that by this autumn, we might have the first tranche of an agreement in place.

What we didn’t get over any of those meetings, however, was any protection from tariffs.

To show goodwill to the United States, we’ve also made a series of gestures:

One of America’s biggest complaints against India has to do with our high rate of taxes on agricultural products — which average at 113%, and go as high as 300%. India has now offered to slash tariffs on many such products, such as almonds or cranberries.

In the lead up to Prime Minister Modi’s visit to the United States, we made a series of tariff cuts. For instance, we brought down tariffs on imports of heavy motorcycles, from 50% to 30%. In this year’s budget presentation, we also cut tariffs on a series of goods — from luxury cars, to yachts, to heavy machinery.

After PM Modi’s US visit, we announced additional tariff cuts on bourbon whiskey imports, from 150% down to 100%.

India has also given concessions outside of goods trade. For instance, we used to place a 6% tax on ads that Indian companies placed with foreign search engines, social media websites etc. We’ve now scrapped that as well.

According to some reports, in fact, we’ve shown a willingness to cut tariffs on 55% of American imports into India.

It looks like Donald Trump sees our willingness to offer concessions. Recently, for instance, he recently noted that “I heard that India is going to be dropping its tariffs substantially.”

Unlike many other countries, who have answered Trump’s threats with even more aggression, we’ve been open and cooperative.

But here’s the problem: we still haven’t been able to secure any sort of commitment on tariffs. In fact, the US Trade Representative just released a new report that criticises many of India’s trade barriers once again. The White House Press Secretary, too, has just pointed to India’s “unfair trade practices” on agricultural trade. So there’s no real signal, here, that India will be spared from America’s reciprocal tariffs.

At the same time, the Indian government, too, has indicated that even though we’re open to negotiate, we’re not considering any sweeping tariff cuts. We’re specifically drawing a line when it comes to agricultural products that we do grow at home: like rice, wheat, or dairy products.

So here’s the bottom line: the United States, despite its many mixed signals, has held its line on reciprocal tariffs. And India, while willing to go a long way to accommodate American demands, isn’t willing to give way completely.

What should you expect

While there’s nothing certain about Donald Trump’s trade policies, it looks like the clock has run out. Indian exports to the United States will be subject to tariffs. The only question, then, is how these will play out. We see three possibilities:

The base case: This… isn’t nice. There will be tariffs on India, which directly hit our exports to the United States. The tariffs will hit ~$78.5 billion worth of our exports in some fashion, although we aren’t sure of which industries these tariffs might hit. What makes things worse is that other countries across the world will also face tariffs, sowing chaos through all sorts of supply chains. If countries retaliate against American tariffs, the ensuing disruption could scale up even further.

The optimistic case: We could be hit with tariffs for the better part of this year, only for them to be lowered later. Many recent India-US negotiations have pointed to a trade deal being in the works. The new tariffs may add some urgency to the negotiations. If any of this comes to fruition — which the financial services firm MUFG considers possible, for instance — we might see things ease up after a few months of pain.

The optimistic-to-the-point-of-naivety case: There’s a possibility that some of this is bluster. Trump has previously walked back on some of his tariffs. There are some reports that he’s considering reducing the number of countries that are hit with tariffs (though contrary reports suggest that no exemptions will be given). There’s a small chance that we might escape unscathed, or with tariffs that sound scary, but do little in practice. We wouldn’t hold our breath on this one, however.

Unresolved questions

This is all we know so far. Things are up in the air — at least till now. Upto this point, we’ve just talked about the immediate context of these tariffs. But things certainly won’t stop there. When something this big rocks the global economy, the repercussions are enormous.

We can’t tell you what those will be. All we can do is ask questions. So here are some things on our mind:

What do these tariffs even look like? There’s little from the American government that tells us what these tariffs might actually look like. There are many proposals in play — from specific tariffs on 10-15 countries, to a universal tariff of 20% against all countries. The White House hasn’’t indicated if its tariffs will be placed industry-wise, or if there will be a single rate for each country. Without a sense of what tariffs will be put in place, it’s impossible to predict any outcomes.

How do other countries respond? It’s unlikely that the entire world sits idly by while America dictates global trade policy. Trump’s previous tariffs on China and Canada drew backlash from the two countries. There’s every chance the next tranche of tariffs will invite similar retaliation from across the world — creating even more global uncertainty. There are other uncertainties at play too. For instance, countries might also find more ways of coping with these tariffs, like letting their currencies depreciate — as China did in Trump’s last term. Meanwhile, they’ll also be hard at work finding alternatives for the United States as a trade destination, which could open up opportunities as well.

What does this do to the US economy? The long term sustainability of these tariffs will depend, ultimately, on how much pain they cause for ordinary Americans. And it seems like there’ll be a lot of pain. American businesses, for one, will certainly be constrained by these tariffs. If they pass those costs onwards, you could see considerable inflation as well. If America’s resources go into setting up basic domestic manufacturing, do its cutting edge industries find it harder to access the same resources? What does this mean for its economy? Goldman Sachs, for instance, thinks there’s a 35% chance that America sees a recession this year.

Forgive us for not knowing any more than this. To be honest with you, though, nobody does. If you want to see just how crazy the escalation so far has been, look at this chart:

This is without the reciprocal tariffs. When those kick in, that line should climb much higher. In a worst case scenario, America’s effective tariff rate might climb to ten times what it was in December 2024:

We’re basically staring at an unprecedented situation — at least for the modern era. Which is why we have no point of reference, right now. Everyone’s just guessing, at the moment. Trade policy uncertainty, in fact, is at an all time high:

There’s only one thing we know for sure: we’re at the precipice of a foundational global shift. We’ll probably talk about this many times again, as things become clearer.

ITC makes a 3,500 crore acquisition

Here’s a bit of news from an industry we haven’t talked about before.

ITC is making a massive acquisition. It recently announced that it would acquire Century Pulp and Paper or (CPP) from Aditya Birla Real Estate Limited for ₹3,498 crore. The deal includes a fully integrated paper mill in Lalkuan, Uttarakhand, with an annual capacity of 4.8 lakh tonnes. But the scale is just part of it — for ITC, this is also a strategic play. It helps ITC broaden its horizons, picking up attractive businesses during a dark time for the industry.

While this isn’t something you hear about often, paper actually makes for a decent chunk of ITC’s business. Although it often gets overshadowed by the company’s dominant cigarettes or FMCG portfolio, the paper business is a quiet, cash-generating arm for the company. In fact, its Paperboards and Specialty Papers Division (PSPD) brought in around Rs. 8000 crore in revenue in FY23 — nearly 10% of the company’s top line.

And if you had any doubts about its importance, this acquisition makes it clear — ITC sees even more potential in this space.

A new foothold in the North

So, why is CPP a good acquisition for ITC?

Here’s one answer: it lets ITC sell paper across a wider market. See, paper is a dense, heavy and bulky product. Because of its relatively low value, it doesn’t make sense to carry paper across long distances. To ITC, that created a natural limit for how far its markets extended. Until now, ITC’s paper production was concentrated entirely in South and East India — in places like Telangana, Tamil Nadu, and West Bengal.

CPP’s massive integrated mill in Uttarakhand, now, gives ITC a presence in North India for the first time.

It also de-risks ITC’s operations. It creates a multi-location setup for the company, with more factories to spread its paper business across — something the company specifically called out as a key goal.

But this story isn’t just about geography. Behind the scenes, there’s a lot happening in the paper space in general. And that sets the wider context for what has happened.

Why Now? Understanding the Industry’s Downturn

The Indian paper industry is highly fragmented. Most firms in the industry are small, regional players. CPP, in contrast, is a well-established, large-capacity unit, and when companies realised that it was up for sale, it sparked an intense contest between interested parties. This acquisition reflects a larger trend, in fact.

See, here’s the thing: the paper industry has been going through a bit of a downturn over the last few years. Smaller paper mills are struggling. At the same time, though, bigger players are using this as an opportunity to consolidate the industry to gain scale, efficiency, and pricing power. But why this divergence? If the paper sector is facing a crisis, why would ITC invest thousands of crores into it right now?

To understand that, we need to look at what happened to the industry over the last few years. The Indian paper sector was hit by a double whammy — collapsing margins and rising imports. And much of that can be traced back to how things unfolded during and after Covid.

1. Demand Dropped, Then Imports Surged

During the pandemic, demand for printing and writing paper crashed.

The whole world had suddenly moved online overnight, and for the paper industry, it was an unmitigated catastrophe. The industry’s biggest customers had suddenly lost interest. Offices shut, schools moved online, and paper usage fell across the board. That gap was temporarily filled by pent-up demand in FY23 when things reopened — but it didn’t last long.

What followed was worse.

When consumption picked up as the pandemic subsided, Indian firms found it hard to capture the resurgence of their business. Instead, all that business went abroad. Imports from China and ASEAN countries like Indonesia, Singapore — already competitive due to cheaper production and trade agreements — flooded into the Indian market. Between FY22 and FY24, total paper and paperboard imports jumped 68%, from 1.1 million tonnes to 1.9 million tonnes.

Thanks to trade pacts like the India-ASEAN FTA and the Asia-Pacific Trade Agreement, firms in these countries paid either zero or very low duty when exporting paper to India. That made domestic paper more expensive in comparison — despite often being higher in quality. Indian producers saw their market shares fall, as a result.

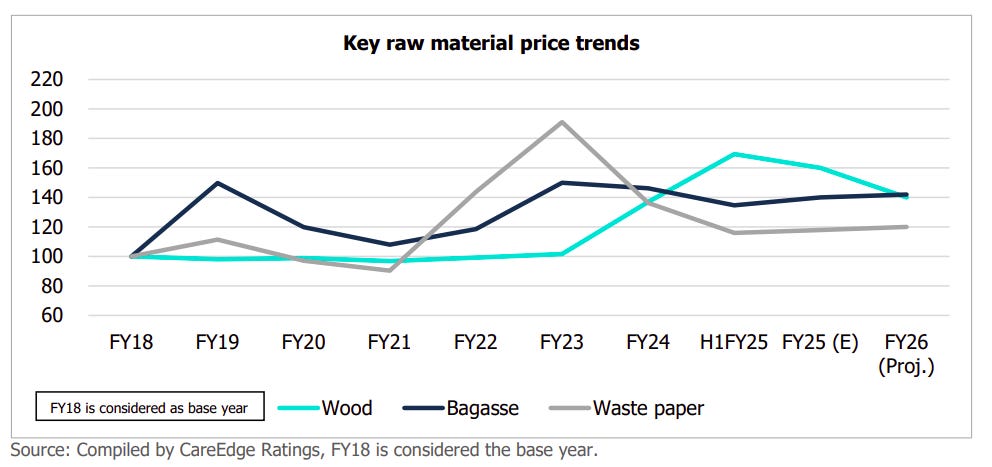

2. Input Costs Exploded

At the same time, the cost of making paper rose sharply. The key input — wood — became harder and more expensive to source.

See, during COVID, tree plantations were paused for a few years. Now, these trees — mostly eucalyptus and subabul — take 3 to 5 years to mature. So, when the country reopened, it suddenly found that it didn’t have new, mature wood to buy. That would take another few years.

Meanwhile, paper wasn’t the only product that required wood. As COVID subsided and Indians returned to the market, there was a sudden surge in the demand for wood from all sorts of industries — like furniture, plywood, and biomass power.

Suddenly, demand went up, even as supply shrank. As a result, domestic wood prices surged. In some cases, margins for paper companies went into the negative after accounting for raw material costs.

Meanwhile, companies couldn’t raise their prices much, because of all the pressure from cheap imports. So, despite steady or even rising sales volumes, profits collapsed.

The combined impact of cheap imports and high input costs has been brutal for the industry. A report by Bobcaps says that the industry’s EBITDA margin fell to just 6.9% in FY25 — the lowest in 20 years. For comparison, the average margin over the past two decades has been around 16-20%.

Because of all the stress the industry was under, domestic production fell — down 5.1% in FY24 If anything, it is expected to slip further this year. Revenues for Indian paper companies are projected to decline by 3–4% in FY25, even as imports continue to rise

So why is ITC still buying?

We can’t tell you for certain, but here’s what we think ITC is really betting on: long-term demand.

The paper industry saw a terrible shock, which threw it off its game for a few years. But that slump won’t last forever. ITC is betting on long-term trends that still favour paper:

India’s per capita paper consumption is only 15–16 kg — compared to 29 kg in China and 57 kg globally. That leaves massive room for future growth, even in an era where everything is going digital.

Paper isn’t just used for books or printing — it’s used for all sorts of things. Some of those segments look especially promising right now. Tissue paper is growing even faster — 13.3% annually — due to greater awareness around hygiene. Cupstock, used in disposable food containers, is growing at 10.5%.

Government bans on single-use plastic are pushing companies to shift to paper-based alternatives. This could open up even more business opportunities.

To ITC, this is a golden buying opportunity — other players are in distress, and valuations are lower. It gets to buy a functioning, strategically located operation at a discount, before things look up once again. This is a steal for the company.

ITC also thinks it can make the CPP unit more efficient. It’s aiming for a 30–40% increase in EBITDA per tonne and targeting high-teens return on capital once operations are fully integrated and optimized.

What the acquisition does for ITC

The CPP deal raises ITC’s total paper capacity from 8 lakh tonnes to 12.8 lakh tonnes — a jump of 60%. This helps solve one of ITC's long-standing constraints: capacity bottlenecks. The company’s existing mills were already running close to full. This new unit gives it breathing room to scale further — and serve the market better as demand picks up.

The deal makes ITC arguably the largest paper producer in the country by capacity. It also brings in new product categories like tissue paper and rayon-grade pulp, which ITC can now plug into its own distribution system.

This positions the company to take advantage of the industry’s return to form. Despite all its current problems, the Indian paper industry is still one of the fastest-growing in the world. It's a ₹80,000 crore industry, producing over 25 million tonnes annually. And ITC has just positioned itself at the forefront.

It will be interesting to see how this acquisition pans out.

Tidbits

BSNL has begun testing 5G services in major Indian cities including Jaipur, Lucknow, Chandigarh, Bhopal, Kolkata, Patna, Hyderabad, and Chennai. The tests are being conducted on its existing 4G infrastructure, part of a 100,000-site deployment plan. As of March 2025, over 83,000 sites have been installed and 75,000 are operational. The rollout follows delays from the TCS-led consortium, which was awarded a ₹24,500 crore contract to enable the network expansion. BSNL is also preparing for a commercial 5G launch in Delhi within three months through a Network-as-a-Service model. To ease SIM upgrades, BSNL has partnered with Pyro Holdings to offer USIM and over-the-air platforms. The telco’s mobile market share currently stands at 7.99% as of December 2024, reflecting its late entry into 4G and 5G services.

India’s external debt rose 10.7% year-on-year to $717.9 billion at the end of December 2024, up from $648.7 billion in December 2023, according to the finance ministry’s latest Quarterly External Debt Report. On a quarter-on-quarter basis, the debt increased by 0.7% from $712.7 billion recorded in September 2024. The external debt-to-GDP ratio stood at 19.1% in December 2024, marginally higher than 19% in the previous quarter. A valuation effect of $12.7 billion due to the appreciation of the US dollar against the rupee and other major currencies influenced the increase. Excluding this, the rise in debt would have been $17.9 billion quarter-on-quarter. US dollar-denominated debt accounted for the largest share at 54.8%, followed by the Indian rupee at 30.6%, Japanese yen at 6.1%, SDR at 4.7%, and euro at 3%. While the central government's external debt declined, the non-government sector's debt rose during this period.

Vodafone Idea shares surged 10% on Tuesday to ₹7.48 after the Indian government announced it would convert ₹36,950 crore worth of outstanding spectrum auction dues into equity. This move will increase the government’s stake in the telecom company from 22.6% to 48.99%, significantly reducing the company’s debt burden. As of September 2024, Vodafone Idea had a total debt of ₹2.16 lakh cr. This marks the company's best stock performance in more than four months, reflecting positive investor sentiment following the government’s intervention. The conversion specifically targets deferred spectrum payments and forms part of a broader strategy to stabilise Vodafone Idea’s financial position.

Gold prices surged past $3,100 per ounce on Monday, with spot gold touching a record high of $3,128.06 before settling at $3,103.99. US gold futures also climbed to $3,136.10, marking a 0.7% rise in early trade. The precious metal has gained approximately 18% so far in 2025, building on a 27% increase in 2024. This rally places gold on track for its strongest quarterly performance since 1986. Analysts attribute the spike to ongoing uncertainty around tariffs, which has pushed investors toward safe-haven assets. Central bank purchases and demand from exchange-traded funds have further supported prices. Market watchers note some technical resistance that could trigger profit-taking, but the broader bullish momentum remains intact.

- This edition of the newsletter was written by Pranav and Krishna

📚Join our book club

We've recently started a book club where we meet each week in Bangalore to read and talk about books we find fascinating.

If you'd like to join us, we'd love to have you along! Join in here.

🌱Have you checked out One Thing We Learned?

It's a new side-project by our writing team, and even if we say so ourselves, it's fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That's all. It's chaotic, it's unpolished - but it's honest.

So far, we've written about everything from India's state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you're looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are 😉

Hi team,

This was really knowledgeable and I, as a CA student learnt a lot!

Regarding the podcasts for the Daily Brief, please ensure that the speaker doesn't read the text quickly but speak as if people are listening to it while travelling, etc. So, it becomes a easy for us to grasp.

I read the daily brief and aftermath report daily. I can't listen them as a podcast due to this issue that the speaker speaks too fast.

Thank you for the value addition!

Hi team

Could you maybe shed some light on Internationalisation of Indian Ruppee as it is becoming more and more relevant. Mabe sth on where INR stands rn, countries' sentiments, past/upcoming transactions