Beneath the Bagmane REIT IPO

A REIT with equity characteristics

Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

India’s biggest office REIT is also its narrowest bet

India’s bittersweet conundrum

India’s biggest office REIT is also its narrowest bet

The Indian markets are about to see another major REIT IPO. Bagmane Prime Office REIT opens for subscription today, the 5th of May, and closes on the 7th. The entity plans to raise ₹3,405 crore at a price band of ₹95-100 per unit, sitting on a portfolio worth roughly ₹40,000 crore. By size, that makes it the largest pure-play office REIT to ever list in India.

If you’re new to REITs, or want a refresher on what they actually are and why they’re different from buying a real estate stock, we covered all of that when Knowledge Realty Trust went public last August.

The two issues are very different in substance, though. Knowledge Realty was a diversified bet, with 29 assets across 7 cities, deliberately spreading risk. Bagmane is the opposite. On paper, “India’s biggest pure-play office REIT” sounds institutional and broad but in reality, it’s an exceptionally narrow bet: all of its revenue comes from just two corridors of a single city. Most of it comes from just three buildings. And nearly all of the rent is paid by foreign multinationals running their offshore operations out of India.

Is that narrowness a moat? Or is it a single point of failure? If you’re looking to invest in this IPO, that’s the question you must answer. And that answer turns out to be more complicated than either side of that question suggests.

What’s actually good about it

‘Concentration’ is usually a dirty word in investing. One of the first bits of advice any investor gets is “spread your bets, don’t put all your eggs in one basket”. But is there a reason Bagmane’s extreme narrowness could be a feature rather than a bug?

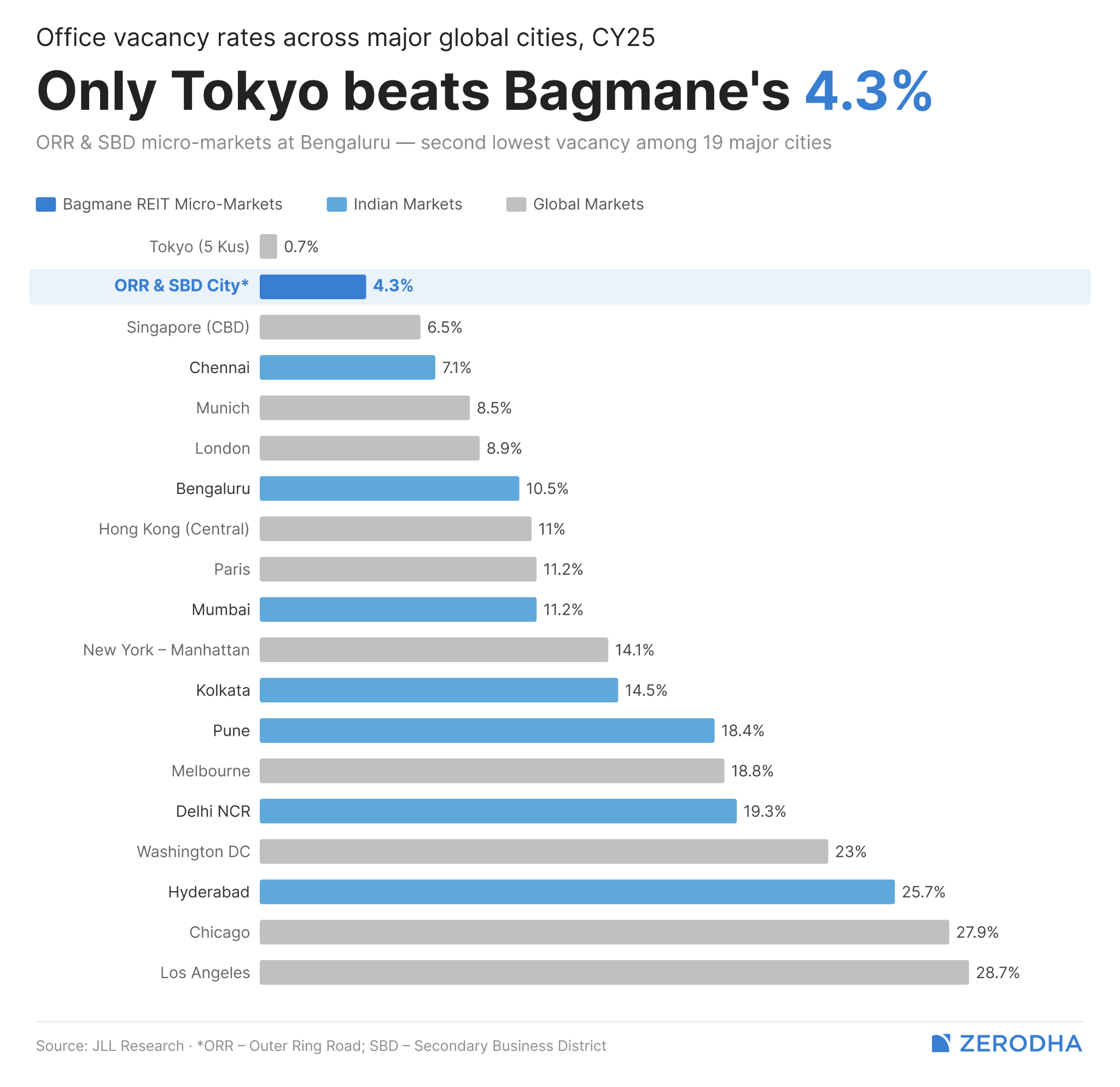

It comes down to the kind of corridors Bagmane has chosen and the kind of tenants those corridors attract. India’s national office vacancy is around 15.2%. Hyderabad’s is 25.7%; more than a quarter of all high quality office space there is sitting empty.

Contrast that to Bagmane’s two corridors: the first is Bengaluru’s Outer Ring Road, which has just 4.1% vacancy. The other is SBD City, with 5.4%. These are hot properties, in other words.

When demand outstrips supply this dramatically, landlords get something rare in Indian commercial real estate: pricing power. JLL forecasts that ORR rents will grow 5.2% annually through CY28, while SBD City rents shall grow at 6.5%. These are micromarkets that far outpace India’s broader real estate.

When it comes to tenants, meanwhile, there’s a little quirk in how Indian office leasing works.

When a company leases an office in India, the landlord hands over a bare shell. The tenant has to build everything inside themselves: cabins, wiring, cabling, cafeterias, server rooms, labs etc. This typically costs them three to five years’ worth of rent. Compare that to the US or Europe, where landlords typically themselves fund roughly a quarter of “fit-out” costs themselves.

This might sound like a small accounting detail, but think of what it means. Indian office tenants are extraordinarily sticky. Imagine a company that has spent five years’ rent equipping a campus the way it wants. Walking away, especially to save a bit on rent, is plain irrational. So most tenants stay and renew. Often, they even expand within the same campus.

Just see Bagmane’s numbers. Between FY23 and the first nine months of FY26, the company leased 7.2 million square feet. 91.7% of that went to existing tenants expanding their footprint. New tenants contributed less than 9%.

Add to this the fact that ~43% of Bagmane’s completed area is “build-to-suit”. That is, the building was custom-designed for a specific tenant’s requirements. There, the stickiness runs even deeper.

The bull case, then, is this: Bagmane runs in office-starved micro-markets where rents have nowhere to go but up. It caters to tenants who can’t easily leave because they’ve sunk too much into their fit-outs. Their average lease runs for 7.4 years, and when those leases come to an end, most renew them for around 15% more rent. That narrowness, in other words, simply ensures reliable cash flows.

The paradox at the centre of the prospectus

But there’s a trickier side to this.

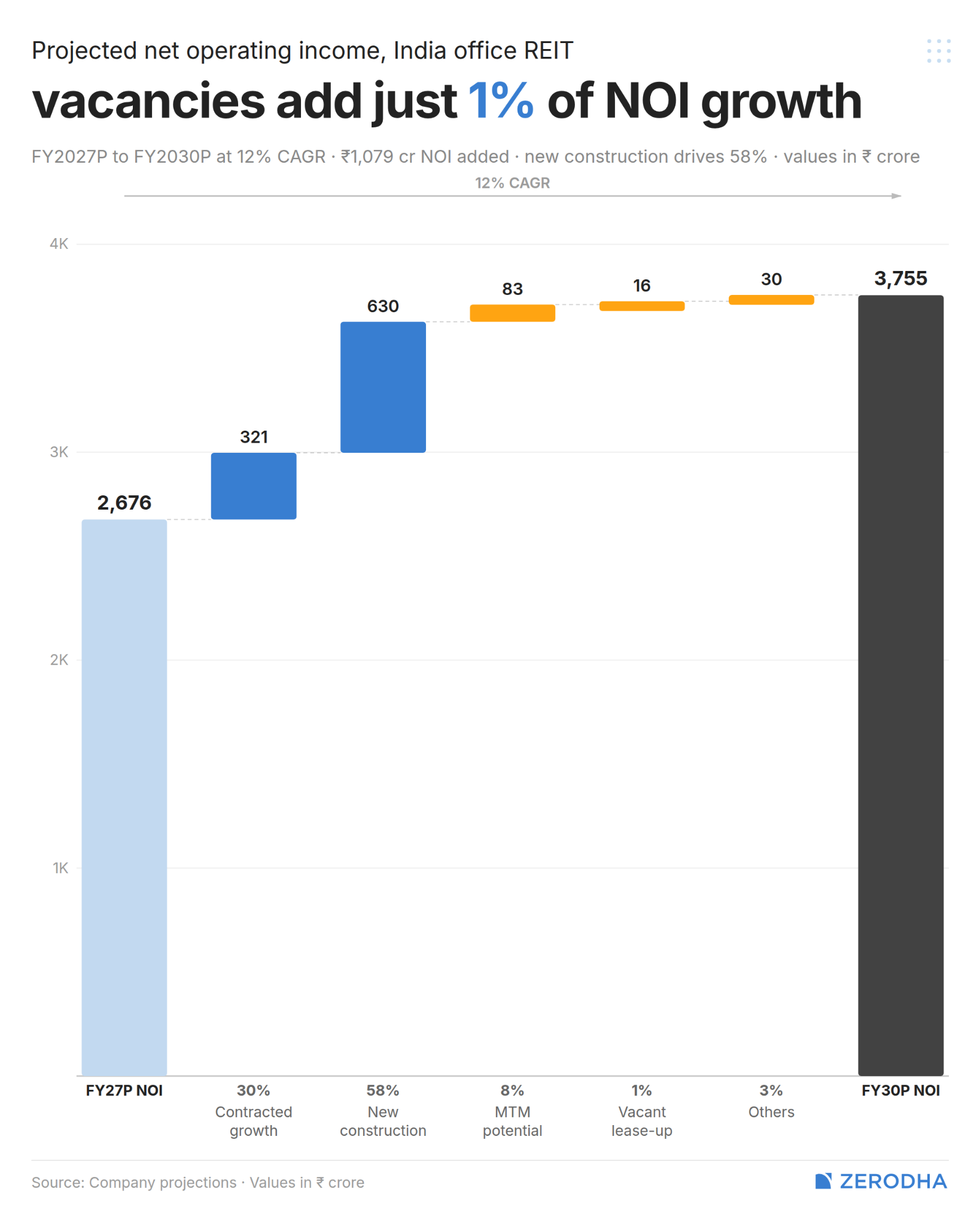

Bagmane’s portfolio is 98.8% full. There’s almost no empty space left. The amount of cash the company is bringing in is about as much as it will ever get. That raises awkward questions for a company about to ask the public for money. In a normal “growing” REIT story, low occupancy is precisely where the headroom for growth comes from. You buy a 70%-full building, for instance, and your revenue growth comes from filling the rest.

Knowledge Realty, for instance, listed at 91% occupancy. It has been steadily filling its remaining space, which fuels a meaningful chunk of its growth.

Bagmane doesn’t have that lever to pull. Its own projections assume that leasing vacant office space will contribute just 1% of growth until FY30. Not 1% per year, by the way. 1% total, over four years.

What, then, are they even promising?

About 30% of their promised growth comes from contractual rent escalations baked into existing leases. Another 8% comes from “mark-to-market”, that is, by re-leasing old, expiring contracts at current market rates. A small 3% comes from “other.” But most of that growth — 58% — comes from buildings that don’t fully exist yet.

If you’re betting on this REIT, then, three-fifths of your bet is plagued by execution risk.

Bagmane has roughly 1 million square feet of office space under construction. It has marked out twice as much as its “future development area.” Its coming up with two on-campus hotels, and a solar plant. The company’s total planned capex over the coming years is ₹31,620 crore. To put that in perspective, it’s roughly twice the company’s FY25 cash from operations, and is well over the net debt currently sitting on the company’s books.

This isn’t a fatal problem. Developing new properties can create enormously amounts of value, especially if those buildings get pre-leased at attractive yields, and the sponsor — Bagmane group — has a long track record of building successfully in Bengaluru. But make no mistake: you’re currently buying promises.

If you’re investing in a REIT, chances are, you want bond-like predictability. Bagmane offers that predictability in its existing 98%-occupied portfolio. But bolted onto that is a development arm, two hotel projects with very different economics from office leasing, and a solar capex story.

Let’s pause on those last two.

The hotels — being built directly on the office campuses — are pitched as a natural amenity for the corporate tenants next door. Their tenant’s hospitality needs, the pitch goes, will be absorbed by the campus itself. Fair. But hotels and offices have very different economics. Office leases are long and rent is paid monthly. Hotels rent rooms by the night, at prices that swings with cycles. Their costs are higher too. Bagmane will need to sign on an experienced hotel operator, ramp up occupancy from zero, and absorb operating losses before they take off.

The solar story has its quirks too. Bagmane operates a solar plant that supplies green power to its tenants, and it’s now doubling down. Instead of buying power from the grid, their tenants could get their electricity from Bagmane itself. Again, it’s an interesting pitch — but one without the long-lease economics that make the office portfolio look so steady. In fact, their solar offerings — which are, to be fair, just ~3% of revenue — are affected by all sorts of things, including BESCOM tariffs revisions.

There’s also a financing wrinkle here. Indian REITs are required by SEBI to distribute at least 90% of their distributable cash to unitholders every year. So they can’t easily retain money to fund all this development themselves. They have to borrow.

That isn’t the worst thing. Bagmane’s existing balance sheet is conservative — with net debt at just 7% of portfolio value, well below most listed REITs. But almost all of its current borrowings are on floating rates. That introduces a whole lot of uncertainty. A 100 basis point move in interest rates shifts its profit before tax by about ₹38 crore. That’s manageable today. But if the development plan needs significant additional debt — and chances are that it will — that risk could multiply.

The cleanest way to think about Bagmane, then, is as a hybrid. It has an existing portfolio: choice properties that bring bond-like stable incomes. But they have a pipeline that is much more equity-like, abd depends entirely on execution. The IPO is asking you to pay a price that values both.

The numbers

Of the ₹3,405 crore Bagmane is raising, ₹2,390 crore is a “fresh issue”. That’s the money that flows into the company to fund the acquisitions of Luxor and Bagmane Rio, two assets being added to their portfolio. The remaining ₹1,015 crore is an “offer for sale” — money that will flow to existing investors, taking some chips off the table. That isn’t abnormal for a REIT.

Its valuation is interesting.

It’s conventional in some ways. At the upper price band of ₹100, Bagmane’s implied market cap is roughly ₹34,000 crore. Its portfolio’s gross asset value is around ₹40,000 crore. That is, the IPO is being priced at about a 15% discount to the value of its assets. That’s broadly how listed Indian office REITs trade in the secondary market.

But the projected distribution yields, though, are higher. That is their estimates of how much cash you’ll get back as an investor if you invest in the IPO. Bagmane is guiding around 6% in FY27, climbing toward the mid-7s by FY30.

Embassy Office Parks REIT — the granddaddy of Indian REITs, with seven years of listed history and 27 quarterly distributions behind it — currently offers a lower trailing yield. So does Knowledge Realty Trust.

That gap creates an obvious question: why are IPO sellers leaving such yield on the table? There’s an optimistic view: REIT IPOs in India are typically priced to attract subscribers because the asset class is still building its retail investor base. These premiums are just a sweetener so that the deal foes through.

The more skeptical view, though, is that those projected yields rely heavily on the development pipeline coming through on schedule and at expected numbers. They project a growth of distributable cash of 20%. Chances are, they’re leaning heavily on a part of the business that hasn’t been built yet. If so, the sellers may have a clearer view of that risk than buyers do, and they’re pricing it in despite higher projected yields.

The truth is probably some mix of both. We, certainly, don’t know the right answer.

The bottom line

Bagmane’s assets are genuinely good. The campuses are scarce, and sought after. Their tenants are blue-chip. The cash conversion is clean. The balance sheet is conservative. None of that is in dispute.

But are you being asked to pay for those quality assets? Or are you paying for new assets — which could be just as good, but come without a guarantee? REITs, much like most investments, are only as good as the price you’re paying. Even excellent assets can produce mediocre returns if the entry price already assumes a best case scenario.

India’s bittersweet conundrum

For most of the last thirty years, the number that Indian agriculture ministers dreaded was sugarcane arrears: the accumulated unpaid dues that sugar mills owed to the farmers who grew their raw material.

In bad seasons, this number would swell into the tens of thousands of crores. Farmers would protest, politicians would scramble, state governments would announce emergency packages, and then it would happen again the next bad year. The arrears cycle was so persistent and so politically explosive that it stopped being treated as a solvable problem and became, instead, a permanent feature of Indian agricultural life.

Then, somehow, it was solved.

In the 2023-24 sugar season, Maharashtra, which produces a third of India’s sugar, recorded cane payment arrears of just ₹54 crore at season close, across more than 200 mills, in a state where total dues to farmers that season ran to ₹36,699 crore. Every farmer who grew sugarcane in Maharashtra in 2023-24 got paid on time. The problem had ceased to exist.

But then, by early 2026, the arrears ballooned up to ₹4,252 crore, with 168 of 206 mills yet to clear their dues to farmers. By March the number had climbed to nearly ₹5,000 crore. The problem that had been solved came back roaring, larger than ever.

Then, in April 2026, the Indian government published a draft law that would replace the rules governing the sugar industry that hadn’t been substantially rewritten since 1966. On the surface, it reads like routine regulatory housekeeping. But look more carefully, and what you find is the government encoding a specific economic thesis into statute.

The new law validates the thesis that a sugar mill is not a food company, but an energy company. And this reclassification is also a hopeful attempt at solving the arrears problem of Maharashtra, and other states.

So how did we get here, and is the new law a step in the right direction? That’s the story we’ll be diving into today.

The trap built in 1966

Sugarcane is one of the most politically sensitive crops in India, with around 5 crore farmers and their families depending on it. Sugar mills, which are the only buyers of cane within the farmer’s assigned territory, hold enormous structural power over the farmers who supply them. A mill that delays payment, or simply refuses to pay the full amount, leaves the farmer with little recourse.

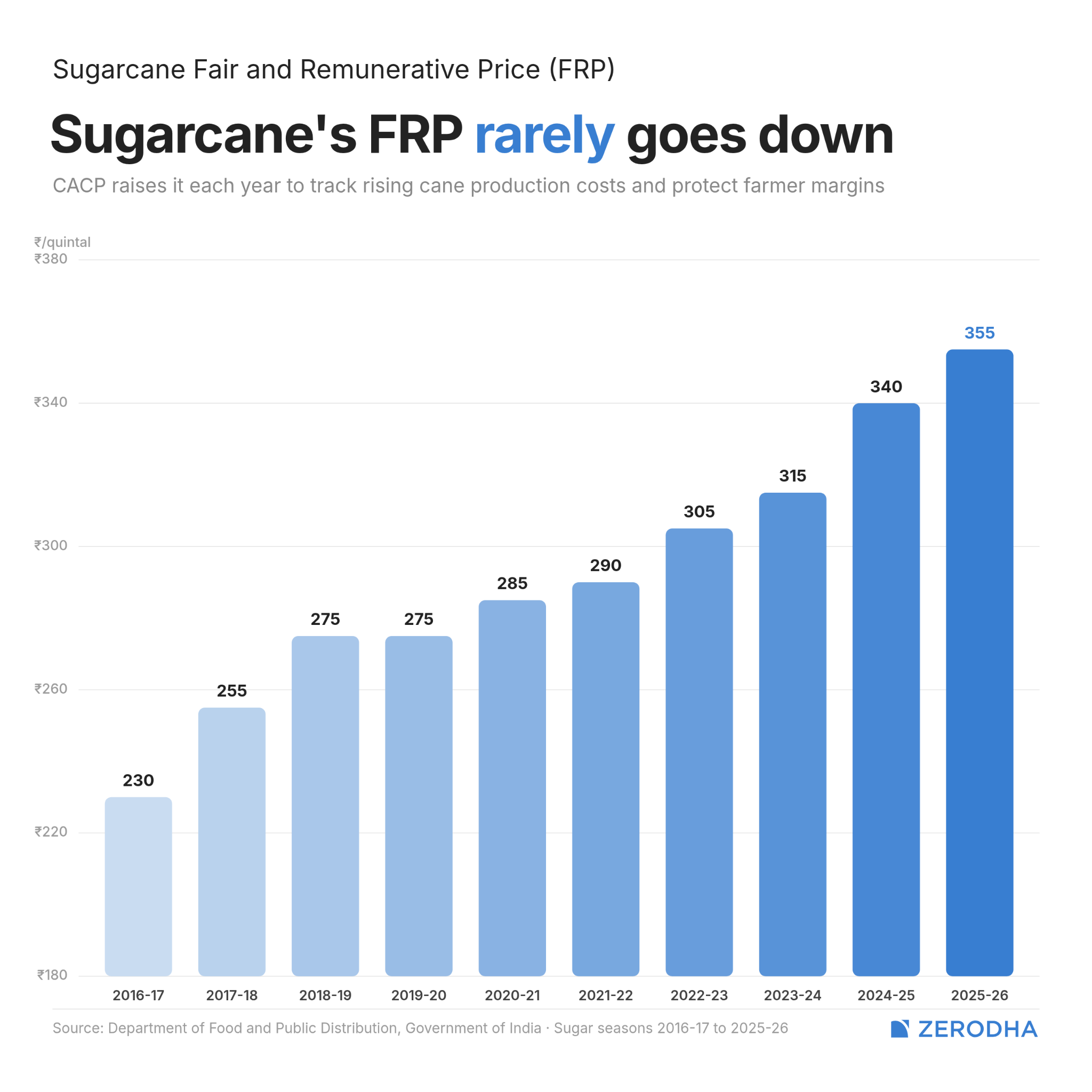

The 1966 Sugarcane (Control) Order was designed to sit between both parties. It required every sugar mill to pay farmers a minimum price — or Statutory Minimum Price — within fourteen days of receiving the cane, with interest penalties for delays. In 2009, it was renamed the Fair and Remunerative Price (FRP), and its calculation was tightened to account for farmer input costs, returns from alternative crops, and a guaranteed profit margin.

In 2013-14, the FRP was ₹210 per quintal. For 2025-26, it stands at ₹355. It has rarely gone down.

And this is where the trap lives.

See, the FRP is a fixed cost that mills must pay regardless of what sugar actually sells for. And because the price is guaranteed, farmers have little reason to reduce cane acreage when the market turns. They grow it anyway, mills crush it anyway, and sugar piles up faster than the country can consume it. India has long been a structural sugar surplus economy precisely because the price guarantee insulates farmers from the consequences of oversupply.

But those consequences don’t just disappear — mills bear them. In a bumper year, production surges, sugar prices fall, and mills find themselves legally required to pay a price that the market will not let them recover. The FRP is not too high in the abstract. It becomes too high the moment sugar prices drop, which in a chronic surplus economy is often. The cash runs short, and the dues for mills pile up.

This was the rhythm of Indian sugarcane for most of the post-liberalisation era, and by 2017-18 it had produced ₹22,000 crore in national arrears. Prior to 2018, the government had pumped nearly ₹12,000 crore in direct subsidies over eight years just to help mills clear their dues.

The potential solution

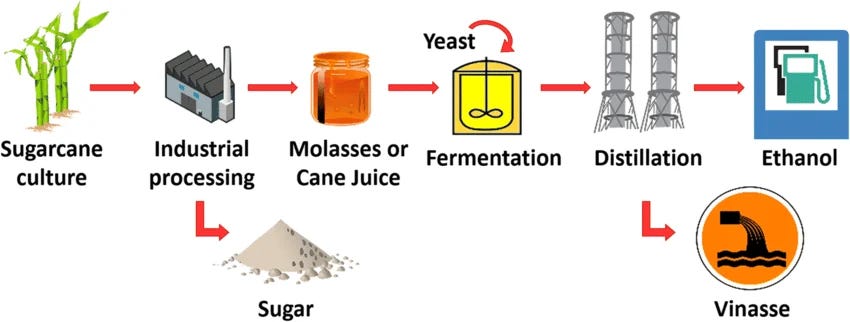

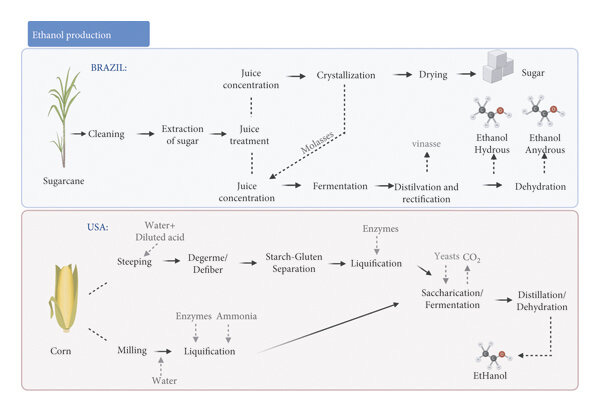

The government’s answer was to give mills a second buyer for the sucrose in their cane. So, in 2018, the National Policy on Biofuels was introduced. It pushed mills to convert excess cane into ethanol and sell it to oil marketing companies at a government-fixed price. Then, as we covered before, this ethanol would be blended into petrol in cars.

This seemed like a reasonable fix for the arrears problem. Ethanol fixes it by giving the same sucrose a guaranteed buyer, oil companies paying a fixed government rate on a fixed schedule, instead of a sugar market that might not cover what the farmer was owed.

Ethanol fixes it not by adding new income but by giving the same sucrose a different, more profitable destination. When a mill converts cane juice into ethanol rather than sugar, it sells the identical molecule to oil companies at a guaranteed price, on a fixed payment schedule. The farmer still gets paid their FRP by a buyer who cannot walk away. Ideally, everyone wins.

Between 2018 and 2023, blending rose from under 2% to over 14%. Oil companies were paying mills ~₹42,000 crore annually for ethanol. This flowed directly toward farmer payments, as evidenced by Maharashtra’s dues falling to ₹2 crore.

How the government broke its own solution

But this fix was short-lived. Between 2023 and 2026, the combined impact of two decisions had dismantled the mechanism that had fixed the problem.

The first decision was to keep raising the FRP. From 2022-23 to 2025-26, it rose from ₹305 to ₹355 per quintal, a 16.5% increase. This is what the FRP is designed to do, and it was a genuine win for farmers.

But while raw material for the mills got more expensive, the procurement price for the ethanol that the mills produce remained unchanged. Their ethanol revenue didn’t grow hand-in-hand with rising raw material costs. B-heavy molasses ethanol, the feedstock most directly tied to cane economics, has sat at ₹60.73 per litre. Sugarcane juice ethanol at ₹65.61.

Undoubtedly, this led to some margin compression for the mills. The cost of producing ethanol from B-heavy molasses is estimated to be ₹66 per litre, while the government pays ₹60.73. Every litre of B-heavy molasses ethanol a sugar mill produces generates a cash loss of roughly ₹5, causing a drain of resources from mills.

The second decision was to bring grain into the ethanol programme.

Now, ethanol isn’t just made from sugarcane, but also grains like maize and rice. To reduce the blending programme’s dependence on just cane, the government brought maize and surplus rice into the programme. The advantage of grain is that it can be processed year-round, unlike sugarcane which is seasonal. The government priced grain-based ethanol aggressively to incentivise this capacity.

And because of this, a new player had entered the picture alongside sugar mills: grain distilleries. This would prove fatal for sugar mills, and hence sugar farmers.

In the first procurement cycle of the 2025-26 ethanol supply year, maize alone took 45.68% of all ethanol ordered by oil companies. In contrast, sugarcane-linked feedstocks combined took 27.5% — that share was over 90% when the programme began. The ethanol programme was thriving, but the sugar mills (and farmers) were being priced out of it, while the grain distilleries were enjoying bumper profits.

Maharashtra’s arrears tell the story directly, ₹54 crore at the close of 2023-24 and ₹2,130 crore at the close of 2025-26, per the Maharashtra Sugar Commissionerate’s fortnightly reports — a 39x jump in two seasons.

The Sugarcane (Control) Order 2026

The 1966 order was written in an era when the word ethanol did not appear in the vocabulary of sugar regulation. It governed one output, sugar. The industry had spent eight years building a completely different kind of operation inside a legal container that had no idea it existed.

That’s what the draft Sugarcane (Control) Order 2026 tries to fix.

Its most significant provision is a new conversion formula for FRP calculations: 600 litres of ethanol from sugarcane juice, syrup, or B-heavy molasses will be treated as equivalent to one metric tonne of sugar. Moreover, it allows district collectors to recover unpaid dues by attaching mill assets as land revenue arrears. That’s a considerably sharper instrument than the interest penalty that existed on paper in 1966 and was almost never applied. The law also raises the minimum distance between mills from 15 to 25 km.

The 600-litre equivalence will make a big difference to cane farmers. Under the old framework, a mill that diverted cane juice to a distillery would report a lower sugar recovery rate, reducing its FRP liability. Farmers would be penalised for the mill’s production choice. The new clause imputes the diverted juice back into the recovery calculation, so the farmer is paid as if the sugar had been made regardless of what form the sucrose took. It closes an accounting loophole that did not exist in 1966, since back then, there was no ethanol to divert juice toward.

Now, even if the 2026 order can declare that mills are energy companies, it cannot make them profitable.

That requires a CCEA notification revising ethanol procurement prices upward for B-heavy molasses and sugarcane juice. That notification has not come despite two years of requests from the Indian Sugar and BioEnergy Manufacturing Association (ISMA) for a 50% procurement floor reserved just for sugarcane feedstocks. This would prevent grain distilleries from crowding mills out of a programme that was designed to save them.

Sixty years after India built a legal framework to protect farmers from mills, and watched mills fail to pay anyway because the economics never lined up with the legal requirement, the country is attempting the same move with ethanol.

The FRP will keep rising, the procurement price for sugarcane ethanol needs to rise with it. Until things change, the 2026 law is a piece of regulatory architecture built around a financial proposition that loses money on every transaction it hopes to encourage.

Tidbits

1. India, Canada begin second round of CEPA trade talks to boost ties

The second round of negotiations for a free trade agreement between Canada and India aimed at boosting two-way commerce and investments started on Monday. The pact is officially known as the Comprehensive Economic Partnership Agreement (CEPA) and negotiations will cover trade in goods, services, and other mutually agreed policy areas.

Source: Business Standard

2. Gold futures slide to Rs 1.50 lakh/10g as oil surge, dollar weigh on bullion

Gold prices fell by nearly 1 per cent to Rs 1.50 lakh per 10 grams in futures trade on Monday, tracking weak global trends amid a firm US dollar and elevated crude oil rates. On the Multi Commodity Exchange (MCX), the yellow metal for June delivery declined Rs 1,149, or 0.76 per cent, to Rs 1,50,203 per 10 grams in a business turnover of 9,510 lots.

Source: Moneycontrol

3. Rupee falls 39 paise to close at all-time low of 95.23 against US dollar

Rupee fell 39 paise to close at an all-time low of 95.23 (provisional) against the US dollar on Monday, as the ongoing West Asia tensions cause volatility in global markets, keeping oil prices high and raising fears of inflation and economic slowdown.

Source: Hindu BusinessLine

- This edition of the newsletter was written by Kashish and Aakanksha.

What we’re reading

Our team at Markets is always reading, often much more than what might be considered healthy. So, we thought it would be nice to have an outlet to put out what we’re reading that isn’t part of our normal cycle of content.

So we’re kickstarting “What We’re Reading”, where every weekend, our team outlines the interesting things we’ve read in the past week. This will include articles and even books that really gave us food for thought.

Pranay Kotasthane on Navigating the New Uncertain World

If you enjoy The Daily Brief, here's something we bet you'll like. We recently spoke to Pranay Kotasthane, one of the sharpest minds we read to understand India and its place in the world. We've often featured his insights on this newsletter. This time around, we got him on for a long conversation — one that spans a wide breadth of topics: the world India now has to play in, why the panic around critical minerals is overdone, what's actually holding back manufacturing, what an India-shaped opening in AI might look like, why Bengaluru feels as stuck as it does, and more. Do give it a listen!

Thank you for reading. Do share this with your friends and make them as smart as you are 😉